The bulls ran hard Tuesday with the dollar pulling back and the anticipation of strong earnings results from the titans, but unfortunately, big tech disappointed and delivered weak forward guidance. However, the norm of late is for significant pre-market recovery from overnight lows, and today that pattern is repeating. Although the market has primarily ignored bearish economic reports this week, we should still take note of the Mortage Apps, International Trade, Inventories, New Home Sales, and Petroleum numbers out this morning. Though technical conditions have improved, watch overhead resistance levels and plan for the challenging price action to continue.

During the night, Asian markets rallied despite the Australian inflation rate hitting a 32-year high. However, European markets trade flat to slightly lower in a volatile session. With a big day of earnings hope and several potential market-moving economic reports, U.S. futures are well off their overnight lows after the disappointment of big tech results. Watch for the possibility of a pop-and-drop or big-point whipsaw, keeping in mind the Durable Goods, GDP, and Jobless Claims figures before the bell Thursday.

Markets opened with a small divergence as the large caps gapped slightly lower while the QQQ capped about 0.35% higher. However, the 3 major indices got back in lock-step immediately as the bulls led a strong rally for the first 30 minutes. At that point, all 3 went switched to a very slow rally that lasted until 12:20 pm. Then we saw the first real selling of the day as the indices pulled back between 0.5% and 0.75% over the next hour before rebounding the same amount between 1:30 pm and 2:30 pm. From there we made another wave, leaving us very near the highs at the end of the day.

On the day, all 10 sectors are in the green with Energy (+0.40%) by a large margin the most lagging sector while Technology (+2.83%) and Consumer Cyclical (+2.82%) led the way higher. SPY gained 1.60%, DIA gained 1.09%, and QQQ gained 2.07%. The VXX was down 3.86% to 19.17 and T2122 is now at the extreme overbought territory at 97.67. 10-year bond yields plunged to 4.10% and Oil (WTI) was up 0.38% percent to $84.89/barrel. This action left us with large white candles having a small wick at the top. All 3 of the major indices have also clearly broken their longer-term downtrend and have begun a new uptrend. Still, it is worth noting that price is now getting pretty far above the T-line (8ema) on the daily chart and we will need some rest soon. So, all-in-all, it was a third straight bullish day that is getting a little bit extended at this point.

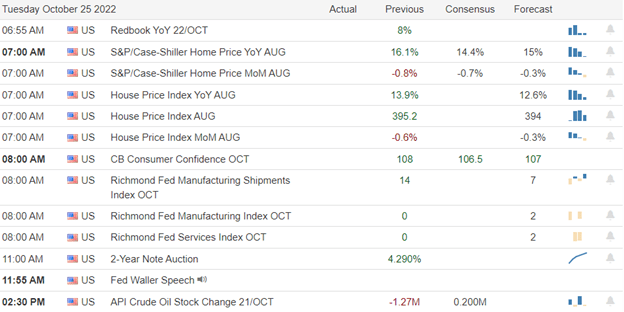

In economic news, Conference Board Consumer Confidence came in below forecast at 102.5 (versus the expected 106.5 and the previous reading of 107.8). Then after the close, the API Weekly Crude Oil Stocks reported a major and unexpected build of 4.520 million barrels (compared to a forecasted build of 0.200 million barrels and last week’s drawdown of 1.270 million barrels).

In stock news, Bloomberg reported that Elon Musk has told bankers that the TWTR deal will close on Friday at $54.20/share (free money since it closed at $52.78 on Tuesday). Meanwhile, TSLA gained EPA approval to begin delivering their Semi trucks. Across the pond, PM gained conditional approval from the EU to buy Swedish Match (the largest cigarette alternative maker in Europe). The conditional part is that PM has pledged to divest Swedish Match’s logistics arm. In Canada, CGC has formed a US holding company to allow it to expand into the US market. CGC stock soared 27% on the news. Finally, AMZN has begun to roll out a new payment method. Some US users can now pay for purchases via a mobile app owned by PYPL. This will be available to all US customers before Thanksgiving.

In miscellaneous news, the Chinese Yuan fell to new lows Tuesday (onshore at its weakest position against the dollar since 2009 and offshore at the lowest since its introduction in 2010). This comes despite the Dollar pulling back significantly Tuesday. The industry group ELFA reported Tuesday that US companies borrowed 11% more to finance equipment leasing in September compared to the same month in 2021. Also of note, in their earnings report, CMG said they have seen only “minimal resistance” to price hikes from their customers. This suggests the consumer is still largely healthy. On the other side, also in their earnings report, V said they are seeing the growth of spending slowing as consumers are struggling with inflation. Elsewhere, mortgage demand fell slightly last week, with new purchase applications down 2% and refinance applications down just 0.1%. However, overall loan demand has fallen to the lowest level since 1997 with the average interest rate up to 7.16% (from 6.94% the prior week) for a 30-year, fixed-rate, conforming loan.

After the close, AMP, AXTA, BYD, CNI, CHX, CB, CSGP, WIRE, ENPH, EQR, FFIV, FE, JNPR, MTDR, MSFT, NBR, RUSHA, TER, TXN, UHS, and V all reported beats on both the opt and bottom lines. Meanwhile, CC, CMG, HA, MAT, NCR, and NEX all missed on revenue while beating on earnings. On the other side, AGR and SKX beat on revenue while missing on earnings. Unfortunately, GOOGL, GOOG, and SPOT missed on both the top and bottom lines. Among all these, TXN, SPOT, MAT, SKX, and FFIV all lowered their forward guidance. However, CNI, CHX, HA, and ENPH all raised their forward guidance.

So far this morning, BG, BMY, GD, TMO, KHC, WM, ADP, GPI, CSTM, SLGN, ROP, HOG, TKR, EVR, CPG, PRG, EXP, CHEF, WNC, DRVN, and EDU all reported beats on the top and bottom lines. Meanwhile, CME, PAG, OC, OTIS, GRMN, UMC, TMHC, KBR, HLT, ODFL, TDY, and VRT all missed on revenue while beating on earnings. On the other side, BSX, AVY, and WFRD beat on revenue while missing on earnings. However, MAS missed on both the top and bottom lines. It is also worth noting that BG, ROP, TDY, TKR, DHEF, WNC, and EDU all raised forward guidance. On the other side, OTIS, MAS, and AVY lowered guidance. (BA, BSBR, IQV, STX, NSC, APH, R, SID, HES, FTV, BCO, MHO, COOP, FSV, GTX, BPOP, and ROL report later this morning.)

Overnight, Asian markets leaned heavily toward the green side. Only India (-0.42%) and Thailand (-0.26%) were in the red. Meanwhile, Shenzhen (+1.68%), New Zealand (+1.32%), and Hong Kong (+1.00%) led the region higher. In Europe, the picture is much more mixed at midday. The FTSE (-0.32%), DAX (+0.56%), and CAC (+0.06%) lead the region in volume as always. However, some of the smaller exchanges show bigger moves in early afternoon trade. As of 7:30 am, US Futures are pointing toward a mixed, red start to the day. The DIA implies a -0.05% open, the SPY is implying a -0.61% open, and the QQQ implies a -1.53% open as the major indices diverge. 10-year bond yields are dropping again at 4.055% and Oil (WTI) is up four-tenths of a percent to $85.66/barrel in early trading.

The major economic news events scheduled for Wednesday include Sept. Goods Trade Balance and Sept. Retail Inventories (both at 8:30 am), Sept. New Home Sales (10 am), and EIA Weekly Crude Oil Inventories (10:30 am). The major earnings reports scheduled for the day include APH, ADP, AVY, BSBR, BA, BSX, BCO, BMY, BG, CHEF, CME, SID, CSTM, CPG, DRVN, EXP, EVR, FSV, FTV, GRMN, GTX, GD, GPI, HOG, HES, HLT, IEX, IQV, KBR, KHC, MHO, MAS, EDU, NSC, OTIS, OC, PAG, BPOP, PRG, ROL, ROP, R, STX, SLGN, TMHC, TDY, TMO, TKR, UMC, VRT, WNC, WM, and WFRD before the open. Then, after the close, AEM, ALGN, ALSN, AMED, NLY, AR, ACGL, ASGN, AVT, AXS, BMRN, CACI, CP, CCS, FIX, CYH, DLR, ESI, EHC, EQT, RE, FLEX, F, FBHS, FWRD, ULCC, GGG, INVH, JBT, KLAC, MTH, META, MEOH, MAA, MOH, MUSA, MYRG, ORLY, OII, OLN, OMF, PTEN, PPC, PLXS, RJF, SEIC, NOW, SNBR, STC, FTI, TDOC, TROX, UCTT, URI, VMI, VFC, and WFG report.

In economic news later this week, on Thursday, we get Sept. Durable Goods Orders, Q3 GDP, and Weekly Initial Jobless Claims. Finally, on Friday, Sept. PCE Price Index, Q3 Employment Cost Index, Sept. Personal Spending, Michigan Consumer Sentiment, and September Pending Home Sales are reported.

Earnings continue to flood in with, frankly, generally good results. However, at the margins, mega-tech names are showing pressure from corporate IT spending and Marketing budgets. This is pointing toward the recession people have been talking about for months, but which has only materialized slowly and in spots. This is just a data point, some will choose to see it as great news, expecting the Fed to start easing soon. Others will see it as a sign of dread. What’s important is not how you, I, or any individual see it. Instead, how does the overall market react to it…what does price do?

All 3 major indices have also broken out of their crooked type (non-flat neckline) “inverted head and shoulders” (bottoming) patterns. The market extension is getting overdone, but is not completely beyond the pale yet. So, we need a rest or pullback, but it does not have to come today. Continue to show caution and be patient (wait for confirmation). With high volatility and less certainty at the moment, you either need to be able to handle the pain of all that volatility or this may be the time to pursue more cautious trading strategies (options spreads for example), including remaining hedged, quick, and/or small.

Don’t be stubborn. If you have a loss, just admit you were wrong and take it before it grows. And when price does move in your direction, always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all OUR MONEY!). Also, keep in mind that trading is not a hobby. It’s a job. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: BITO, NAT, OKTA, MRO, XLE, INTC, XOM, EBAY, VLO, and PFE. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The bulls maintained control on Monday through the huge-point morning whipsaw, highlighting the danger of highly emotionally charged price volatility. The PMI number, though ignored, provided context to the relief rally uncertainty as the U.S. economic growth declined. All eyes will be on the tech giants GOOGL and MSFT earnings results after the bell though we will have to deal with Case-Shiller and Consumer Confidence numbers during the morning session. Expect the wild price gyrations to continue, and plan for substantial morning pops or drops depending on the big tech reports.

While we slept, Asian markets whipsawed in a volatile session to close mixed on the day. With HSBC down 6% this morning, European markets trade mixed with eyes on earnings results. However, U.S. futures point to a modest pullback at the open as they wait in hopeful anticipation of the GOOGL and MSFT reports while dealing with those pesky economic reports that continue to suggest an economic slowing is underway. Anything is possible, so plan carefully in this hyper-emotional market condition.

Economic Calendar

Earnings Calendar

We have nearly 90 companies listed on the Tuesday earnings calendar with the kickoff of big tech reports after the bell today. Notable reports include MMM, AGYS, AMD, AXTA, BYD, BIIB, CLF, CC, CMG, CB, KO, GOOGL, GLW, ENPH, FFIV, GE, GM, HAL, ITW, JBLU, JNPR, KMB, MAT, MSFT, NVR, PHM, RTX, SHW, SKK, SPOT, TXN, UPS, VLO, V, WH, &XRX.

News & Technicals’

UPS reported revenue that fell below analyst expectations and earnings per share that beat them. The United Parcel Service said declines came from its supply chain solutions division, which includes freight forwarding. However, the company reaffirmed its full-year guidance of $102 billion in revenue and adjusted operating margin of 13.7%. Ford Motor is updating its popular Escape as part of a two-pronged sales strategy alongside the newer, more rugged Bronco Sport. The starting price for the 2023 Escape ranges from roughly $29,000 for an entry-level model to $40,000 for a plug-in hybrid electric vehicle. The goal is to differentiate the mainstream Escape from the more rugged Bronco Sport, allowing each vehicle to form a niche in the compact vehicle segment.

Britain’s new Prime Minister Rishi Sunak set to take office Tuesday, assuming with it one of the most daunting political inboxes in modern British history. The former finance minister will be tasked with remedying multiple crises, including soaring inflation, higher energy costs, industrial unrest, and a battered economy. Sunak has warned that the U.K. faces a “profound economic challenge” and pledged to instill “stability and unity.”

UBS aims to improve its Asia-Pacific business, and CEO Hamers said he sees “some opportunities to grow” in China. The investment banking division saw revenues down by 19%, with the lower performance in equity derivatives, cash equities, and financing revenue offset by foreign exchange revenues. The Global Wealth Management division also reported lower revenues, down by 4% year-on-year.

Although we experienced a large morning gap and whipsaw, the bulls maintained control into the close as prices stretched into resistance levels as the Dow surged through its 50-day average. Today we will have to deal with Case-Shiller, Consumer Confidence numbers, and a bevy of earnings results that will include the market-moving reports from MSFT and GOOGL. Perhaps that will fix the imbalance of the indexes, with the SPY and QQQ lagging behind the surging DIA. With the hype and emotion of earnings, the markets can undoubtedly move higher but keep a close eye on the substantial overhead resistance levels for possible entrenched bear attacks. As a result, price volatility will likely remain highly challenging, giving experienced day traders the advantage. With all eyes on the giant tech results, we should also plan for big-point morning pops or drops that could extend the relief rally or quickly reverse the direction. Plan your risk accordingly.

On Monday, the large caps gapped up about one-half of one percent and then the bulls followed through strongly for 30 minutes. Meanwhile, the QQQ opened only a modest 0.15% higher and the bulls moved it only modestly higher until 10 am. However, at that point, the whipsaw kicked in to see a very strong selloff in the next 30 minutes across all 3 of the major indices. At 10:30, markets reversed again as we saw a more modest rally that lasted 2 hours. Then, after 12:30 pm, we saw a sideways rollercoaster ride until all 3 indices broke out of the range to the new highs at 2:45 pm. That afternoon rally continued until 3:30 pm when we saw a modest selloff in the last half-hour of the day. This action is giving us white-bodied candles with wicks at both ends, but a larger lower wick. (The QQQ also bounced up off its T-line or 8ema.)

On the day, seven of the ten sectors are in the green. Basic Materials (-1.01%) was the lagging sector, while the Consumer Defensive (+1.22%) sector lead the market higher. The SPY has gained 1.22%, DIA gained 1.34%, and QQQ gained 1.10%. Meanwhile, the VXX was down 1.53% to 19.94 and T2122 is now in the overbought territory at 84.03. 10-year bond yields have recovered from an early pullback to be at 4.247% and Oil (WTI) is down one-third of a percent to $84.83/barrel. Overall, a bullish day with considerable intraday whipsaw taking out the gap chasers and weak hands. Still, the market did end up higher, if a tad indecisive.

In economic news, Manufacturing PMI came in below expectations at 49.9 (versus 51.0 forecast and 52.0 in September). Services PMI also came in even further below expectations at 46.6 (versus 49.2 forecast and 49.3 in September). These numbers show contractions in US economic activity (for the fourth straight month). Elsewhere, Treasury Sec. Yellen also spoke in the afternoon to a securities industry group. She acknowledged a liquidity problem in the bond markets, which are raising costs (prices) and said her department was looking at ways to enhance stability and increase liquidity. She also declined to comment on Japanese intervention to prop up the Yen. She said she was not aware of any measures Tokyo was taking and had not been recently notified of such steps by them (although they were notified of a previous intervention by the BoJ, which Japan claimed was to offset volatility).

In stock news, TSLA cut the price of its Model 3 and Model Y cars in China by about 5% in an effort to stimulate demand. On the other side of such action, AAPL raised prices on its Apple TV+ and Apple Music subscription services. After the close, the SEC charged CRON and its former Chief Commercial Officer with accounting fraud. The FTC also proposed a settlement with UBER (which acquired the sanctioned company Drizly in 2021) over a lack of security standards which resulted in a data breach that exposed the personal data of 2.5 million consumers in 2020.

In energy news, Natural Gas prices in the Permian Basin (West Texas) plunged on Monday (down to as low as $0.20 / million BTU) as booming production overwhelmed the pipeline networks. (This compares to the US benchmark now trading at about $5.) This stems from KMI pipeline maintenance in its Gulf Coast Express and El Paso pipeline networks.

After the close, CDNS, CLS, SUI, ARE, AAN, SSD, RRC, and CADE all reported beats on both the top and bottom lines. Meanwhile, DFS and ZION both reported a beat on the revenue line while missing on earnings. On the other side, WRB, PKG, and CR all missed on the revenue line while beating on earnings. However, CCK and BRO both reported misses on the revenue and earnings lines.

So far this morning, CNC, GM, ADM, KO, UBS, SHW, SYF, HAL, BIIB, PII, GPK, PNR, POR, and ARCC all reported beats on the revenue and earnings lines. Meanwhile, GE, SAP, JBLU, and IVZ all beat on revenue while missing on earnings. On the other side, VLO, UPS, NVS, MMM, TRU, MSCI, and TRN all missed on revenue while they also beat on earnings. However, HSBC, CLF, PHM, XRX, MCO, and ST all missed on both the top and bottom lines.

Overnight, Asian markets were mixed in much more modest moves than the Chinese plunge on Monday. Taiwan (-1.48%) Shenzhen (-0.51%), and India (-0.42%) paced the losses. Meanwhile, New Zealand (+1.11%), Japan (+1.02%), and Thailand (+0.59%) led the gainers. In Europe, we see a similarly mixed picture at midday. The FTSE (-0.71%), and DAX (-0.84%) are negative while the CAC (+0.33%) is among the green exchanges in early afternoon trade. As of 7:30 am, US Futures are pointing toward a modestly red start to the day. The DIA implies a -0.40% open, the SPY is implying a -0.28% open, and the QQQ implies a -0.03% open at this hour. 10-year bond yields remain volatile as they have plunged back down to 4.177% while Oil (WTI) is off 1.47% to $83.31/barrel in early trading.

The major economic news events scheduled for Tuesday include Conf. Board Consumer Confidence (10 am), API Weekly Crude Oil Stock (4:30 pm), and Fed member Waller speaks (1:55 pm). The major earnings reports scheduled for the day include MMM, ALFVY, ADM, ARCC, BIIB, CNC, CLF, KO, GLW, FELE, GE, GM, GPK, HAL, HSBC, HUBB, ITW, IVZ, JBLU, KMB, MCO, MSCI, NVS, ONB, ORAN, PCAR, PNR, PII, POR, PHM, RTX, SAP, ST, SHW, SYF, TRU, TRN, UBS, UPS, VLO, and XRX before the open. Then, after the close, GOOGL, AMP, AGR, AXTA, BXP, BYD, CNI, CHX, CC, CMG, CB, CSGP, WIRE, ENPH, EQR, FFIV, FE, GOOG, HA, JNPR, MTDR, MAT, MSFT, NBR, NCR, NEX, RUSHA, SKX, SPOT, TER, TXN, UHS, and V report.

In economic news later this week, on Wednesday, Sept. Goods Trade Balance, Sept. Retail Inventories, Sept. New Home Sales, and EIA Weekly Crude Oil Inventories are reported. On Thursday, we get Sept. Durable Goods Orders, Q3 GDP, and Weekly Initial Jobless Claims. Finally, on Friday, Sept. PCE Price Index, Q3 Employment Cost Index, Sept. Personal Spending, Michigan Consumer Sentiment, and September Pending Home Sales are reported.

Earnings continued to grind on with a flood of reports this morning. So far, the premarkets are on pause (just on the red side of flat) as it digests the deluge of news. In late news, Bloomberg is reporting that the Fed is among the group holding huge paper losses from all the bonds they bought up during the pandemic QE phase. With that backdrop, the QQQ and DIA have broken their downtrend lines and SPY is challenging that level now. markets are looking to challenge their bearish trends. All 3 major indices have also broken out of crooked type (non-flat neckline) “inverted head and shoulders” (bottoming) patterns. The market extension is not extreme but is starting to be a minor factor. However, intraday reversals and indecision remain the issues traders need to have a handle on (the biggest threat). So, continue to be cautious and show patience (wait for confirmation). With high volatility and less certainty at the moment, you either need to be able to handle that pain or this may be the time to pursue more cautious trading strategies (options spreads for example), including remaining hedged, quick, and/or small.

Don’t be stubborn. If you have a loss, just admit you were wrong and take it before it grows. And when price does move in your direction, always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all OUR MONEY!). Also, keep in mind that trading is not a hobby. It’s a job. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: UPS, GSK, RBLX, INTC, DVN, FCX. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The bulls and bears are stuck between a rock and a hard place. First, the bulls become energized, rushing in at any hint or rumor that the Fed may back off on rate increases. Then the bears push right back every time we get reminded of the slowing global economy and the possibility of a severe recession. Then, toss in earnings season, inflation, geopolitical issues, and let the price action mayhem begin. The market-moving giant tech reports that begin this week will likely increase the challenges for the retail trader. Expect overnight reversals and big-point intraday whipsaws, so plan your risk carefully!

Asian markets traded mixed, with the tech-heavy Hong Kong exchange dropping 6.36% and the Yen weakening despite intervention. However, European markets trade green across the board after a report showed business activity slowed. Ahead of a big week of earnings and the PMI report, the pre-market pump is underway, pushing for a gap up open. Plan for another challenging week of high-emotion price action.

Economic Calendar

Earnings Calendar

This week we really ramp up the number of earnings and begin hearing the results of the market-moving tech giants. Notable reports for Monday include AGNC, BOH, CDNS, CR, DFS, LOGI, PKG, PCH, RRC, SCHN, & ZION.

News & Technicals’

European business activity slows, impacted by high energy costs and raising concerns about a deepening recession. In addition, firms have been under pressure due to higher inflation, mainly from energy costs and wage pressures. “The situation economically is getting worse quite rapidly,” said Chris Williamson, a chief business economist at S&P Global Market Intelligence. The euro lost ground against the U.S. dollar and the British pound during morning deals in London, trading at $0.982 and £0.868, respectively, following the latest PMI data.

Tesla shares slipped in pre-market trade on Monday after the company cut the price of some of its cars in China. The electric carmaker’s shares were down around 3% before the market opened. The starting price for the Model 3 sedan was cut to 265,900 yuan ($$36,615) from 279,900 yuan. The Model Y sports utility vehicle now costs 288,900 yuan versus the previous price of 316,900 yuan.

Former Finance Minister Rishi Sunak looks set to become the next prime minister of the U.K., with votes to be counted Monday afternoon. Former Defense Minister Penny Mordaunt is his only rival after former Prime Minister Boris Johnson pulled out of the race Sunday. Bond yields held steady in early Monday trading, with the 2-year at 4.47% inverted over the 10-year at 4.14%.

The market seems caught between a rock and a hard place, creating challenging and dangerous price swings for the retail trader. Any hint or rumor that the Fed may slow rate increases or pause brings out the bulls and the social media posts shouting that the bottom is in! Then we get economic reports reminding us of the slowing global economy and the fears of a severe recession energizing the very aggressive bears. Toss in all the earnings season hype, and you have the perfect recipe for volatility, whipsaws, gaps, and overnight reversals. Adding to the price action mayhem is all the emotion associated with the tech giant earnings reports that begin in earnest this week. It may be a good time to remember that cash is a position, but if you plan to trade, plan carefully and be prepared for just about anything this week.

Once again, on Friday, the large cap indices opened flat while the QQQ gapped down about 0.40%. However, again, the bulls stepped in right away to rally all three major indices by close to 2% over the first hour, before the bears stepped in to sell off all 3 almost back to the open level over the course of the second hour. Markets reversed again then at about 11:15 am, starting a long, steady rally that lasted the rest of the day. This action is giving us Bullish Engulfing candles in the DIA, SPY and QQQ that all closed near their highs. All 3 have also crossed back up above the T-line (8ema). However, only the DIA broke through the resistance level from earlier in the week.

On the day, all ten sectors were in the green. Communications (+0.40%) lagged the rest by almost 1.35%, while Basic Materials (+3.76%) was by far (again by 1.32%) the biggest gaining sector. The SPY gained 2.42%, DIA gained 2.50%, and QQQ gained 2.35%. The VXX fell 0.39% to 20.25 and T2122 spiked to just outside the overbought territory at 79.42. 10-year bond yields fell back from early gains to close at 4.221% and Oil (WTI) was up 0.78% to $85.17/barrel. So, all-in-all, it was a strong bullish day to close out a very choppy and volatile week.

In economic news, the September Federal Budget Balance came in massively below the forecast. For the month, the deficit fell 430 billion (which was the biggest drop in history), compared to the forecasted -173.5 billion (and a reduction of $220 billion in August). This reduction cut the current deficit in half from the 2021 number of $2.776 trillion to $1.375 trillion (which is still a significant deficit). Interestingly, the decline came mostly from an $850 billion increase in revenue (compared to about a $550 billion decline in spending).

In Fed speak news, San Francisco Fed President Daly (a Dove) told a UC Berkeley Economic group that the FOMC should avoid putting the economy in an “unforced downturn.” She went on to say that “people should not think it will be a 75-basis-point hike forever” and she thinks the Fed has to “do everything in their power to not overtighten,” concluding that “the time is now to start talking about stepping down (the increases).” Later in the afternoon, Chicago Fed President Evans reiterated his previous statements, indicating the FOMC needs to get rates “a bit above 4.5% and then hold to reassess.” (Rates are currently at 3.00% – 3.25% with two meetings left this year.)

On the regulatory/legal front, after the close Friday, toymaker MAT agreed to pay $3.5 million to settle SEC charges over financial misstatements in Q3 and Q4 of 2017. Elsewhere, a US Judge has ruled that the victims of the BA 737 Max crashes were “crime victims” and rescinded BA’s immunity from criminal prosecution (which was part of the company’s $2.5 billion settlement in January 2021). Nasdaq has prohibited IPOs from Chinese companies (at least 4) for the time being. The cancellations are due to Nasdaq’s concern over trading activity around such IPOs and problems identifying the pre-IPO shareholders as well as the circumstances of their ownership.

In international news, China (Xi Jinping) shuffled its Central Committee (leadership) on Saturday as Xi was elected to his third term as leader. The shakeup threw out many market-oriented former members including the “walking out” of former members (and potential rivals of Xi) such as former President Hu Jintao in a staged event that was a bit reminiscent of Saddam Hussein’s infamous Bath Party Purge meeting. In related news, after his reelection, in his headline speech, Xi seemed to indicate an accelerated timeline for reunification with Taiwan in a somewhat vague manner. This all caused a weakening of the Yuan (to 7.3 per Dollar) and plunging stock markets as traders deal with the idea of Xi’s new government not having the market-oriented supporters it has had up until now. Finally, in the UK, former Finance Minister Rishi Sunak seems to be closing in on being elected the next Prime Minister. (Votes should be counted by the afternoon US time.)

In other stock news, the CEO of VALE said Friday that his company is considering a spinoff its copper and nickel mining unit in the near term. Meanwhile, COST had its contract with the Teamster Union (covering 18,000 employees) ratified.

Overnight, Asian markets mixed with Chinese exchanges plunging (see above). Hong Kong (-6.36%), Shenzhen (-2.06%), and Shanghai (-2.02%) led the region lower. Still, Australia (+1.54%), South Korea (+1.04%), and Japan (+0.31%) as well as a few others managed to print some green candles. Meanwhile, in Europe, exchanges are green across the board at midday. The FTSE (+0.22%) lags as the UK government reshuffle continues. However, the DAX (+1.25%), and CAC (+1.50%) are leading the rest of the region higher in early afternoon trading. As of 7:30 am, US Futures are pointing toward a modestly green start to the day. The DIA implies a +0.35% open, the SPY is implying a +0.29% open, and the QQQ implies a +0.14% open at this hour. 10-year bond yields have plunged back to 4.158% and Oil (WTI) is down 1.2% to $84.05/barrel in early trading.

The major economic news events scheduled for Monday are limited to Mfg. PMI and Services PMI (both at 9:45 am). The major earnings reports scheduled for the day include KEX, PHG, and SCHN before the open. Then, after the close, AAN, ARE, BRO, CADE, CDNS, CLS, KOF, CR, CCK, DFS, LOGI, PKG, RRC, SSD, SUI, VLRS, WRB, and ZION report.

In economic news later this week, on Tuesday we get Conf. Board Consumer Confidence, API Weekly Crude Oil Stock, and Treasury Sec. Yellen Speaks. Then on Wednesday, Sept. Goods Trade Balance, Sept. Retail Inventories, Sept. New Home Sales, and EIA Weekly Crude Oil Inventories are reported. On Thursday, we get Sept. Durable Goods Orders, Q3 GDP, and Weekly Initial Jobless Claims. Finally, on Friday, Sept. PCE Price Index, Q3 Employment Cost Index, Sept. Personal Spending, Michigan Consumer Sentiment, and September Pending Home Sales.

As we start a week of heavy earnings, the bulls seem to be continuing their Friday move. Financial media are now saying they are seeing “some signs of a reversal.” However, the big banks tell us more downside lays ahead as the bad news of the recession is still out in the future. With that backdrop, markets are looking to challenge their bearish trends. As I’ve been saying, all 3 major indices are working on obvious “inverted head and shoulders” (bottoming) patterns. Market extension is not yet a factor. However, we do sit just outside of the overbought territory in terms of the T2122 indicator. However, intraday reversals and indecision remain the norm (and biggest threat). So, continue to be cautious and show patience (wait for confirmation). With high volatility and less certainty at the moment, this may be the time to pursue more cautious trading strategies (options spreads for example), including remaining hedged, quick, and/or small.

Don’t be stubborn. If you have a loss, just admit you were wrong and take it before it grows. And when price does move in your direction, always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all OUR MONEY!). Also, keep in mind that trading is not a hobby. It’s a job. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: BAC, JNJ, WMT, WFC, NFLX, DE, NUE, DVN, FCX. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

As bond yields and the dollar continue to increase, hopes of an earnings-driven rally seem to have quickly faded as the recession worried markets struggle with overhead resistance. At this point, we seem to have a tick-for-tick correlation between the indexes and the price movement of the indexes. So expect the wide-ranging price swings to continue with a light day of earnings and economic data. With so many attempts and failures to break through resistance levels, keep an eye on price supports because it’s not hard to imagine that the bears could resume control.

Asian markets closed mixed but mainly lower as rising rates and recession fears persist. With the U.K. in political turmoil and European markets trading red across the board this morning, monetary pressures grow with the rising dollar. Although U.S. futures try to rally off of overnight lows in the premaket pump, the relentless rise in bond yields continues to steal the wind from the sails of the earnings rally hopes. Plan for the uncertainty to continue as long as the yields and dollar continue to rise.

Economic Calendar

Earnings Calendar

We have a lighter day on the earnings calendar with around 20 confirmed reports. Notable reports include AXP, HCA, HBAN, SLB, SMPL, & V.Z.

News & Technicals’

The race to find Truss’ replacement is already well underway. Candidates vying to succeed Truss as prime minister have until 2 p.m. London time on Monday to gather the support of at least 100 Conservative Members of Parliament to run. It is an exceptionally high bar of nominations for a party composed of 357 MPs and caps the number of candidates able to contest for the leadership to a maximum of three.

Defense analysts say evacuating civilians from the occupied Kherson region in southern Ukraine could set the scene for another Russian withdrawal. Up to 60,000 civilians are expected to be evacuated in the next few days from the part of the Kherson region on the west bank of the Dnipro River. Aluminum is the latest casualty of global economic headwinds as prices sink amid alleged dumping of Russian aluminum, weakening global demand, and soaring operational costs. Earlier this week, aluminum stocks in London Metals Exchange (LME) warehouses leaped, sparking concerns about the potential dumping of Russian-origin aluminum. The White House had already considered a ban on aluminum imports from Russian producer Rusal. Russia is not only a major producer of primary aluminum but also embedded in global supply chains needed to make the metal, bauxite, and alumina.

The yield on the 10-year Treasury hit a fresh 14-year high on Friday, while the 2-year note traded in the territory last seen in 2007, making a 15-year high as signs of a recession worried markets. As a result, the U.S. dollar continues to gain strength and has become almost tick-for-tick correlated with the major indexes. Currency fluctuations and growing concerns of a treasury liquidity crisis are impacting the major banks just days after surging on better-than-expected earnings results. With a light day on the earnings and economic calendars, it may be difficult for the market to find inspiration unless something changes in bond yields. The earnings-driven hope of relief seems to have quickly subsided, so keep a close eye on price supports because it’s not difficult to imagine new market lows.

The large-cap indices opened flat on Thursday while the QQQ gapped down about 0.40%. However, the bulls stepped in right away to rally all three major indices by 1.3% to 2% over the first hour, reaching the highs of the day at about 10:30 am. From there we saw a sideways grind for an hour before the bears stepped in to lead a long, steady selloff, reaching the lows of the day at 2:30 pm. The rest of the day saw a sideways rollercoaster ride not too far from the lows. This action gave us a black-bodied Inverted Hammer-type candle in the SPY and DIA. The QQQ formed a black-bodied Doji with a large upper wick. The SPY and QQQ both retested and slightly broke below their T-line (8ema).

On the day, seven of the ten sectors were in the red. Communications (+0.55%) was by far the biggest gaining sector while Utilities (-2.22%) and Industrials (-1.72%) led the way lower. The SPY lost 0.83%, DIA lost 0.34%, and QQQ lost 0.51%. The VXX fell 1.31% to 20.33 and T2122 fell but remains in the mid-range at 36.73. 10-year bond yields spiked again to 4.241% and Oil (WTI) was flat at $85.71/barrel. So, all-in-all, it was another indecisive day punctuated by intraday reversals.

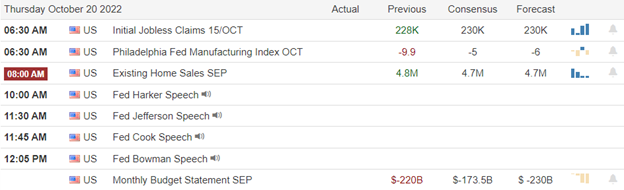

In economic news, Philly Fed Mfg. Index came in as -8.7, which was far worse than the -5.0 forecast, but also better than last month’s -9.9. At the same time, Weekly Initial Jobless Claims came in much better than was expected at 214k (versus the 230k forecast and last week’s 226k). Meanwhile, September Existing Home Sales fell 1.5% to a 10-year low of 4.71 million (which was essentially in line with the forecast of 4.70 million, but worse than the August number of 4.78 million) as mortgage rates continue to climb. In the afternoon, Philly Fed Pres. Harker said Thursday that rate hikes have done little to keep inflation in check. He went on to say “we are going to keep raising rates for a while” and “I expect we will be well above 4% by the end of the year.” This falls in line with the current rate being 3.25% and Fed Fund Futures now pricing in a 0.75% rate hike for November and December.

On the regulatory/legal front, the TX state AG has sued GOOGL for breaking the state’s law which prohibits companies from collecting user biometrics (facial recognition and voice data) without explicit user consent. This is very similar to the state’s lawsuit against META for Facebook doing the same thing. Meanwhile, AMZN is now facing a $1 billion lawsuit in the UK, claiming that the AMZN Marketplace abused its position and information to favor its own products over marketplace vendors. Elsewhere, the US Dept. of Justice has requested more details about the proposed $8 billion deal for CVS to buy SGFY. Finally, after the close, it was announced that WMT has agreed to pay the state of Florida $215 million to resolve claims related to its pharmacy’s part in opioid addiction in the state.

In other stock news, at the close, DB announced it has cut an unspecified number of staff from its investment banking unit as M&A activity (i.e., possible business) has dried up. Elsewhere, the IPO for PRME (Prime Medicine) opened 12% higher than the IPO price of $17 first trading at $18.97. Meanwhile, at the close, XOM announced it has agreed to sell its Montana refinery (which processes 63,000 barrels per day) to PARR for $310 million. Well after the close, PFE said they expect to hike the cost of US covid-19 vaccines by 300% (from $30/dose to $120/dose) in the first quarter of 2023, when the original government purchase contracts expire and the cost is shifted from government to private insurers. In addition, the Washington Post reported that Elon Musk told potential investors in his TWTR buyout that he plans to cut the TWTR staff by 75% (from 7,500 to under 2,000). Finally, Bloomberg reported this morning that the Biden Administration is now discussing whether some of Musk’s ventures should be subjected to national security reviews (TWTR was not mentioned specifically, but the stock is suffering in pre-market on this news).

In international news, UK PM was forced to resign Thursday after only 6 weeks in office. So, the UK is back in search of a leader. However, the Tory party is fast-tracking the system this time and they may have named a new PM by Monday. Whoever is selected will be pressured to renounce unfunded tax cuts (especially at the corporate and top-end brackets) as well as reaffirm the government commitments to cost of living increases in government programs. Meanwhile, the strong dollar continues to hurt most foreign economies as the Yen hit a 32-year low against the dollar (over 150 Yen per Dollar) and the Euro fell further below parity Thursday. Japan is back to saber rattling about intervention to strengthen the Yen, but there is little they can do when the US Fed is aggressively hiking rates and Japan’s economy is fragile enough that the Bank of Japan cannot match pace.

After the close, CSX, UFPI, SIVB, and SAM all reported beats on both revenue and earnings. Meanwhile, SNAP and THC missed on revenue while beating on earnings. On the other side, WAL beat on revenue while missing on earnings. However, both RHI and WHR missed on both the top and bottom lines. It should also be noted that WHR, RHI, and THC all lowered their forward guidance.

Overnight, Asian markets leaned heavily to the red side on mostly modest moves. It was Singapore (-1.75%) that was an outlier while Taiwan (-0.98%), Australia (-0.80%), Hong Kong and Shenzhen (both -0.42%) paced the losses. Malaysia (+0.61%) was by far the largest gainer. Meanwhile, in Europe, exchanges are down across the board at midday Friday. The FTSE (-0.72%), DAX (-1.34%), and CAC (-1.54%) are leading the region lower as markets react to the overnight collapse of the UK government (the 2nd in two months) and a plummeting British Pound. In the US, as of 7:30 am, US Futures are pointing toward a down start to the day. The DIA implies a -0.33% open, the SPY is implying a -0.35% open, and the QQQ implies a -0.67% open at this hour. 10-year bond yields are soaring again to 4.265% and Oil (WTI) is up a half of one percent to $84.92/barrel in early trading.

The major economic news events scheduled for Friday are limited to a Fed speaker (Williams at 9:10 am). The major earnings reports scheduled for the day include AXP, ALV, EEFT, HCA, HBAN, IPG, RF, SLB, and VZ before the open. There are no earnings reports scheduled for after the close.

So far this morning, VZ, AXP, SLB, IPG, HBAN, and EEFT have all reported beats on both the revenue and earnings lines. Meanwhile, HCA missed on revenue while beating on earnings. On the other side, RF beat on revenue while missing on earnings. However, ALV reported a miss on both the top and bottom lines.

With that backdrop, the bearish trend remains in place (both the short-term one from this week and the longer-term one since August). Again, all 3 major indices continue to flirt with printing an inverted head and shoulders (bottoming) pattern. Market extension is not a factor, either in terms of the T-line or T2122. However, intraday reversals and indecision remain the norm as we have seen a lot of gaps and wicks this week. So, continue to be cautious and show patience (wait for confirmation). With high volatility and less certainty at the moment, this may be the time to pursue more cautious trading strategies (options spreads for example), including remaining hedged, quick, and/or small. Beyond this, do not forget that it’s Friday. So, pay yourself and consider taking some money off the table ahead of the weekend’s new cycle.

Don’t be stubborn. If you have a loss, just admit you were wrong and take it before it grows. And when price does move in your direction, always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all OUR MONEY!). Also, keep in mind that trading is not a hobby. It’s a job. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas today (Rick is out). You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Monday speculation delivered a pop-and-go-nowhere, Tuesday and pop-and-drop, Wednesday and gap down and chop with low volume, so what comes next? Uncertainties abound, making it challenging for lowered earnings estimate beats to overcome economic worries. With a big day of earnings and economic reports, bond yields rise, and currencies continue to fluctuate, so plan for more whipsaws, reversals, and wild price volatility as a deepening recession looms.

With the Japanese Yen falling to 150 per dollar, Asian markets closed red across the board overnight. European markets struggle for direction amidst the rising bond yields and the U.K. political turmoil. U.S. futures recover from overnight lows, once again pumping for a gap-up open ahead of earnings and economic figures trying to sustain a relief rally despite the economic uncertainties. Expect more whipsaws, reversals, and challenging price volatility as global recession worries continue to grow.

Economic Calendar

Earnings Calendar

As a general rule, Thursday is the busiest day on the earnings calendar, and that is true for today, with nearly 60 companies listed. Notable reports include ABB, ALK, ALL, T, BX, SAM, DHR, DOW, FITB, FCX, MMC, NOC, NUE, NVR, PM, POOL, SNAP, TSCO, UNP, THC, & WHR.

News & Technicals’

Tesla reported $1.05 in adjusted EPS, ahead of expectations of 99 cents, on revenues of $21.45 billion, lighter than the $21.96 billion expected. Net income (GAAP) reached $3.33 billion, more than double a year ago, while automotive revenue rose 55% from the previous year’s quarter. The company warned about a bottleneck in transportation capacity for delivering new cars in the final weeks of the quarter and said it was “transitioning to a smoother delivery pace.” On Tesla’s third-quarter earnings call, CEO Elon Musk said the company is not cutting production “in any meaningful way, recession or not recession.” “We’re very pedal to the metal come rain or shine,” Musk said. Regarding Musk’s proposed $44 billion acquisition of Twitter, he said that the company “sort of languished for a long time but has incredible potential.”

On a fast-moving day of developments, Wednesday saw a high-profile resignation, reports of parliamentarians being bullied, and further speculation over how long Truss may have left. The culmination of events prompted one member of the Conservative Party to express his anger with the government publicly. “This is an absolute disgrace,” Conservative lawmaker Charles Walker told BBC News on Wednesday evening. “I think it’s a shambles and a disgrace. It’s utterly appalling,” he said.

The Japanese yen weakened past 150 against the U.S. dollar, a key psychological level, reaching levels not seen since August 1990. The Bank of Japan’s two-day meeting is slated for next week. However, policymakers have ruled out a rate hike to defend against further weakening of the currency. On Thursday, Reuters reported Japanese Finance Minister Shunichi Suzuki said the government will take “appropriate steps against excess volatility.”

So far, the wild emotion over earning results has produced a gap and go-nowhere, a pop-and-drop, and drop and chop with low volume, so what comes next? Trouble in Britten, rising bond yields, and currency fluctuations worry markets of a possible liquidity crisis looming. Combine that with inflation, rising interest rates, and the prospect of a deepening recession, and that’s a lot of uncertainty for earnings reports to overcome! In addition, today, we have the potential market-moving economic reports from Jobless Claims, Philly Fed MFG Index, and Existing Home Sales figures to drive additional uncertainty about what comes next. So sinch up your big boy pants and prepare for another day of turbulence, speculation, talking head spin, and drama.

On Wednesday, the major indices gapped down (SPY – 0.50%, DIA – 0.40%, and QQQ – 0.70%) at the open. We then saw a rollercoaster ride that was highlighted by a sharp morning rally (taking us to the highs of the day at 10:30 am), a slow mid-day selloff (taking us to the lows of the day at 1 pm) and a sideways oscillation the rest of the day. This action left us with gap-down, indecisive, Spinning Top candles (perhaps Doji in the QQQ) across the 3 major indices. The SPY and QQQ both retested and held their T-lines (8ema) and all 3 traded lower than average volume.

On the day, nine of the ten sectors were in the red with only Energy (+2.13%) in the green. Meanwhile, Healthcare (-2.23%) and Consumer Cyclicals (-1.98%) led the way lower. SPY lost 0.71%, DIA lost 0.41%, and QQQ lost 0.36%. The VXX rose 0.78% to 20.60 and T2122 fell back to the mid-range at 56.35. 10-year bond yields spiked to 4.131% and Oil (WTI) rose 3.36% to $85.63/barrel. Overall, it felt like an indecisive day where the market is waiting on something and can’t make up its mind.

In economic news, September Building Permits came in a bit above expectation (1.564 million versus 1.530 million forecast and 1.542 million in August). However, Sept. Housing Starts came in below forecast (1.439 million actual versus 1.475 million forecast and 1.566 million in August). The EIA Weekly Crude Oil Inventories came in well below expectations with a drawdown of 1.725 million barrels (compared to a build of 1.380 million barrels forecast and last week’s massive 9.880-million-barrel build). On the Fed front, Minneapolis Fed President Kashkari (strong hawk) told an audience that the US job market remained too strong and inflation probably has not peaked yet. He went on to say that the FOMC may need to raise rates above 4.75% this year to fight inflation, but his best guess is that inflation should start to react sometime next year, allowing the Fed to pause its rate hikes. Then last night, St. Louis Fed President Bullard told an audience that he expects the FOMC to end its “front-loading” of aggressive interest-rate hikes by sometime early next year. He went on to say that beyond that, the central bank could use “small adjustments” to control the situation as inflation cools.

In stock news, Bloomberg reports that T is working with MS to fund a joint venture with some unspecified infrastructure partner with the aim of investing billions of dollars in the US fiber-optic network expansion. Meanwhile, FFIE announced that the company has cut jobs and reduced salaries (in exchange for employees getting equity positions) in order to conserve cash. However, the company is still in talks to raise cash because the conservation will not sustain its burn rate. Meanwhile, GOOGL-owned Waymo announced it will launch its self-driving ride-hailing service into Los Angeles soon, but on an unspecified date. (The service is now available and has operated in Phoenix since 2018.) GTBIF is teaming up with Canadian convenience store chain “Circle K” to sell marijuana at gas stations (with a separate entrance) in 10 Florida locations starting next year.

In energy news, the US Senate quietly advanced the NOPEC bill aimed at punishing OPEC+ countries for their recent production cuts. The bill would remove the sovereign immunity that national oil companies now have, allowing them to be sued for collusion on price-fixing. (It’s unclear how the US could enforce rulings, even if companies like Saudi Aramco were found guilty by a US court.) Earlier, President Biden announced the release of an additional 15 million barrels of oil from the Strategic Petroleum Reserve as well as a plan to begin replenishing the reserve once oil prices hit $70. It is also worth noting that the US Dollar gained again Wednesday against all its peer currencies (in lock-step with the spike in bond rates). This made oil cheaper, yet even so, the fear over supply and reduction in US oil inventories drove oil prices higher.

After the close, IBM, EFX, STLD, KALU, LRCX, LBRT, and CCI reported beats on both the revenue and bottom lines. Meanwhile, TSLA missed on revenue while beating on earnings. On the other side, KMI, UMPQ, and PACW beat on revenue while missing on earnings. At the same time, LSTR beat on revenue and came in inline on earnings. However, PPG, AA, KNX, and LVS all missed on both the top and bottom lines.

So far this morning, T, PM, DOW, AAL, DHR, ERIC, GPC, DGX, ALK, POOL, SNA, MSM, and SNV all reported beats on both the revenue and earnings lines. At the same time, ABB, FITB, KEY, and HRI all beat on revenue while missing on earnings. On the other side, NOK, BX, MMC, TSCO, and DOV all missed on revenue while beating on earnings. At this point, there have been no companies that reported misses on both lines today. (NUE, FCX, UNP, MAN, and WSO report closer to the opening bell.)

Overnight, Asian markets were mixed but leaned heavily to the downside. Hong Kong (-1.40%), Australia (-1.02%), and Japan (-0.92%) led the move lower. Only Malaysia (+1.60%), India (+0.30%), and Thailand (+0.25%) managed to stay green in the region. In Europe, we have a more mixed picture at midday. The FTSE (+0.01%), DAX (-0.37%), and CAC (+0.44%) are typical of the widely split continent in early afternoon trade. As of 7:30 am, US Futures are pointing toward a modest gap higher to start the day (ahead of data). The DIA implies a +0.51% open, the SPY is implying a +0.36% open, and the QQQ implies a +0.15% open at this hour. 10-year bond yields are down slightly to 4.128% and Oil (WTI) is up 1.67% to $86.98/barrel in early trading.

The major economic news events scheduled for Thursday include Weekly Jobless Claims and Philly Fed Mfg. Index (both at 8:30 am), Sept. Existing Home Sales (10 am) and a pair of Fed Speakers (Harker at noon and Bowman at 2:05 pm). The major earnings reports scheduled for the day include ABB, ALK, AAL, T, BX, DHR, DOV, DOW, EWBC, ERIC, FITB, FCX, GPC, HRI, KEY, MAN, MMC, MSM, NOK, NUE, PM, POOL, DGX, SNA, SNV, TSCO, UNP, WSO, and WBS before the open. Then, after the close, SAM, CSX, RHI, SNAP, SIVB, UFPI, WAL, and WHR report.

In economic news later this week, on Friday, Fed member William speaks. In earnings reports later this week, on Friday, we hear from AXP, ALV, EEFT, HCA, HBAN, IPG, RF, SLB, and VZ.

In late-breaking international news, the UK government is in turmoil after PM Truss fired another key cabinet member (and again replaced them with someone who did not support her) and the Tory party whip had to use literal force to make Tory members vote the way the PM wanted them to vote. So, the UK media is now openly handicapping who will replace Truss. Meanwhile, in China, the government is weighing whether or not to cut the quarantine time for foreign visitors. At the same time, the top Chinese technology official has summoned Chinese semiconductor companies to an emergency meeting on how to counter President Biden’s chip sale restrictions. Finally, in Ukraine, the Russian use of Iranian “kamikaze drones” to attack both cities and general and electrical infrastructure, in particular, has caused enough damage that President Zelenzkyy has imposed nationwide electric use restrictions.

With that backdrop, the bearish trend continues while all 3 major indices flirt with printing an inverted head and shoulders (bottoming) pattern. Market extension is not a factor, either in terms of the T-line or T2122. Still, the intraday reversals and daily chop remain serious concerns. So, continue to be cautious and show patience (wait for confirmation). With high volatility and less certainty, this may be the time to pursue more cautious trading strategies, including remaining hedged, quick, and/or small.

Don’t be stubborn. If you have a loss, just admit you were wrong and take it before it grows. And when price does move in your direction, always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all OUR MONEY!). Also, keep in mind that trading is not a hobby. It’s a job. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas today (Rick is out). You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service