Consolidate Word Combining Companies Consolidation Organization

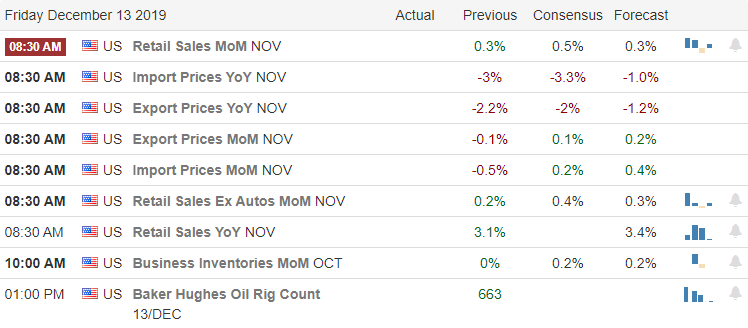

The trends remain bullish but since Monday afternoon, the market

seems very comfortable with the price level has slipped into a choppy

consolidation. With the VIX registering

little to no fear and light earnings and economic calendars, we may see much of

the same today. News on Brexit could

create some volatility. Although the market has largely ignored the impeachment

drama, there is the outside possibility of a market reaction once the official

vote occurs later today.

An RWO Membership is a Great Gift idea!

Asian markets closed mixed overnight as the monitored Brexit developments. European indexes are trading mixed and cautious on the revived fears of a no Brexit deal. US Futures this morning hover around the flat-line, looking for some inspiration that may not occur until the bigger economic reports scheduled on Thursday and Friday.

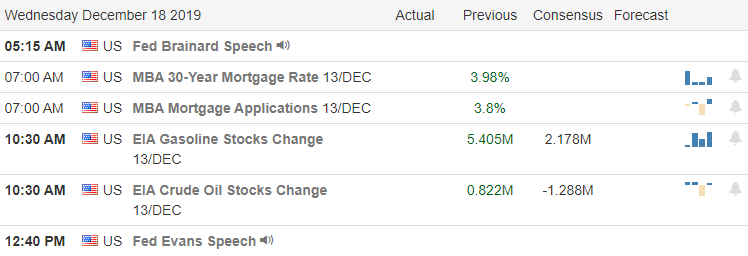

On the Calendar

On the Hump Day Earnings Calendar, we have 15 companies stepping

up to quarterly results. Notable reports

today include MU, PAYX & GIS.

Action Plan

Today the House is likely to vote to impeach the president with

votes falling across party lines. Thus

far, the political has been little more than a distraction but we should not

rule out the possibility of price reaction after the vote. It may or may not occur but it’s better to prepare

than being caught flat-footed in the heat of the moment. Brexit is now back in the news as the Prime

Minister risks a No Deal exit from the Euro block by the end of the year. After the bell yesterday, FDX missed on

earnings and guided lower as the bad blood with AMZN continues to grow.

With a light day of earnings reports and only the Petroleum

Status number to react to on the Economic Calendar bulls and bears my find it

difficult to find inspiration. I would

not be surprised to see light choppy price action continuing the consolidation

that began Monday afternoon. That said,

the trends remain bullish, and with the VIX showing little to no fear the bears

seem unable to mount much of an attack. In

this environment, stocks with momentum can continue to higher or lower but as always

keep an eye on support and resistance levels for profit opportunities.

In a display of force, the bulls rushed into the morning

session seeming buying with both hands quickly pushing the Dow up 200

points. However, about an hour into the

day, a switch flipped and, buying fatigue seemed to settle over the market giving

back half of the Dow gains by the close.

Overall breadth was strong as stock all over the market reached out to

new 52 week highs and inking new record index highs. With a light day on the earnings calendar this

morning, perhaps the Housing numbers can provide some inspiration.

The Gift of Membership!

Asian markets closed green across the board last night but

European markets are trading modestly in the red this morning after their

record-breaking rally yesterday. US Futures traded in the red most of the night,

and this morning continues to suggest a modestly bearish open ahead of earnings

and economic reports.

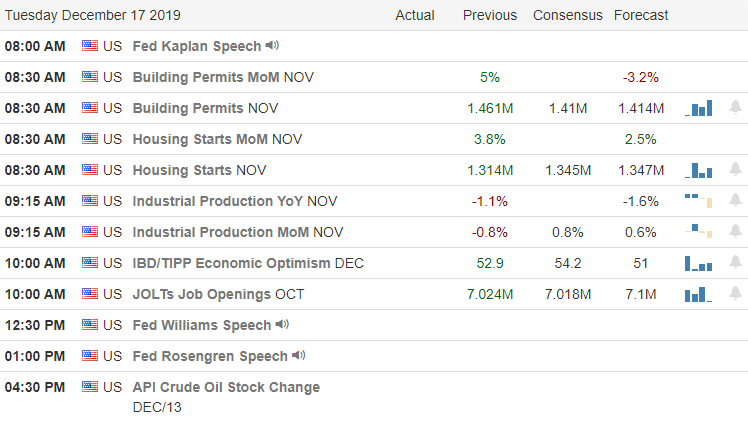

On the Calendar

On the Tuesday Earnings Calendar, we have 17 companies

fessing up to quarterly results. Notable

reports include CTAS, FDX, JBl & NAV.

Action Plan

11 Pipers Piping

In the morning session yesterday it seemed traders could not

buy stocks fast enough as the Dow surged more than 200 with good overall breadth. Then suddenly it seemed we hit a point of

buyer exhaustion and the rest of the day the market drifted sideways and south giving

up 100 of the Dow points previously gained.

The strong breadth would suggest there is more bullishness to come but

price action itself suggests a little caution with the Dow having left behind a

shooting star pattern while the IWM appears stalled at price resistance. The QQQ remained strong through the close,

but the SPY printed a hanging man suggesting a little caution is warranted.

Perhaps we can find some inspiration in the Housing Starts

number at 8:30 AM which according to consensus estimates, should remain strong. Also, keep an eye on the Industrial Production

and JOLTS reports. Futures trading in

the red most of the night and at the time of writing this report still suggest

a modestly lower open, but that could easily change based on earnings and

economic reports. Although the price

action is giving us contradictory signals, the overall index trend remains bullish,

and thus far, the bears don’t seem to have sharp teeth.

With a partial trade deal, no new tariffs, and the FOMC

behind us, the market breathed a sigh of relief, setting new records in the DIA,

SPY and QQQ. Now the question is, has

the market already priced in this good news, or will the bulls continue to find

inspiration allow for a Santa Clause rally into the New Year? Although the full House is preparing to vote

on the presidential impeachment, it has thus far only served as a distraction

rather than impacting this tenaciously bullish run. As of now, the bulls remain in control, and the

index trends continue to point higher. As

always, stay focus on price action watching for clues of change.

Give the Gift of Membership!

Overnight Asian markets closed mixed but mostly lower even

amid better-than-expected industrial output.

Across the pond, the Stoxx 600 hits new record highs in response to the US/China

deal as European indexes see only green this morning. Not to be outdone, the US Futures point to modest

gains at the open ahead of several economic reports with PMI numbers the most potentially

market-moving.

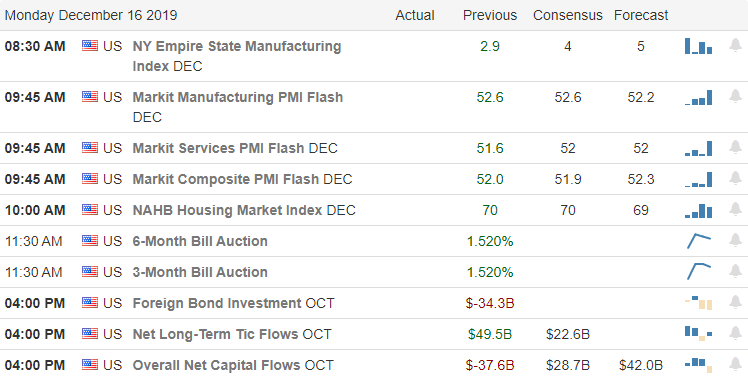

On the Calendar

On today’s Earnings Calendar, we have 22 companies reporting

quarterly results, but there are no particularly notable reports.

Action Plan

The nine ladies are dancing!

Friday was a day of wild volatility as the market reacted to

the US/China trade news. Removing the

December tariffs proved to be a big relief to the market but as we learn about

what’s in the trade deal, it will be interesting to see how the market responds. Has the deal already ben priced in, or will it

continue to inspire the bulls? One thing

for certain with new record highs printed in the DIA, SPY and QQQ on Friday the

trend is up and the bulls at this point remain in control.

With just nine days until Christmas, trade deal, tariffs

& FOMC behind us, the stage may be set for a Santa rally taking us right

into the New Year. One possible stumbling

block is the impeachment process that may serve as a distraction but, the market to this point has had little concern

as the political drama heads to the full House for a vote. As I write this note, the Futures point to bullish

open ahead of manufacturing, PMI, & housing numbers. Be careful chasing the morning gap by waiting

to see if buyers follow-through to avoid the possibility of a pop and drop bull

trap.

What a difference a day makes! After learning the US and China have reached a tentative that removes the looming tariff overhang, the bulls easily pushed the DIA, SPY, and QQQ to new record highs. Futures this morning seem quite confident that the President will accept the Phase 1 agreement removing the weekend stumbling block and clearing a path for a possible Santa Clause into the new year. The huge victory for Boris Johnson in the UK sets the stage for Brexit to occur, and the Sterling is soaring as a result. After a long day debate, the House committee is likely to vote on impeachment today but with the trade news it will likely be a non-event for the market.

Give the Gift of Membership!

Overnight, Asian markets rallied as much as 2%, with the

pending weight of new tariffs now lifted.

European markets are also in rally mode this morning in reaction to the

trade deal and the history-making UK election results. US Futures point to a substantial gap up open

that well set new records for the second time this week. Remember, gaps are gifts so consider taking

some profits as we head into the weekend.

On the Calendar

On the Friday Earnings Calendar, we have only 11 companies

reporting results and there are no particularly notable events today.

Action Plan

Sing the 12 Days of Christmas

What a difference a day makes. Yesterday we learned the US and China reached

a tentative agreement. We are still waiting

on the President to accept the deal but the market seems quite positive he will

do just that. Although there are very

few details about what’s in this Phase 1 agreement, the bulls confidently set

new record highs in the DIA, SPY, and QQQ after hearing the news. The UK Prime Minister Boris Johnson accomplished

a remarkable win that will secure Britain’s exit from the Euro block. After 14 hours of debate, the impeachment

committee postponed their vote until sometime today to send the articles of

impeachment to the full house for their decision.

The market’s around the world are responding positively to the

trade news helping the US Futures point to yet another record-making day at the

open. Assuming the President will accept

the deal sometime today, we have the makings for a very bullish day to close

the week. Removing the massive tariff

overhang from the weekend will make it much easier for the bulls to remain in

control of this trend. It may also open the door for a nice Santa

Clause rally as we head into the New Year.

Impeachment, Tariffs, and Brexit, Oh My! While the House impeachment committee prepares

a Thursday vote charging the president with high crimes and misdemeanors,

citizens of Britain go to the polls as the Prime Minister fights for a majority. What a tangled web of uncertainty the market

faces as we wait. After learning that

the FOMC will hold the line on interest rates and the positive economic comments

by the Chairman, the DIA, SPY and QQQ closed with modest gains. One wonders if they can continue to remain so

brave if we head into the weekend still waiting on a presidential tariff

decision.

Overnight Asian markets closed mixed but mostly higher as they closely monitor trade and tariff developments. European markets are moderately green across the board as the watch developments in the UK election and wait on an ECB rate decision with Christine Lagarde at the helm. With an impeachment vote pending, US Futures are pointing to modest gains at the open as the President prepares to meet with trade advisers. Keep a close eye on price action for clues as we wait for possible market-moving news.

On the Calendar

On the Thursday Earnings Calendar, we have 22 companies

reporting quarterly results. Notable

reports include COST, ADBE, AVGO, CIEN, ORCL.

Action Plan

13 day to Christmas!

After cutting the interest rates three times in 2019, the

FOMC decided to stand pat and have encouraging words about the overall

economy. As expected, there was very little

price movement after the release, but the bulls finally manged a positive Dow

close by the bell. The house impeachment

committee debated late into the evening with a vote likely to occur sometime

today, sending the articles to the full house vote. Across the pond, British citizens are voting today

in an attempt by the Prime Minister to win a party majority that will pass his

Brexit deal. Should his party win gain,

the majority needed the Brexit deal could occur rather quickly and may affect

the overall market. Should they lose,

the opposing party promises a new vote to determine if the country wants to

proceed with Brexit at all.

As we wait for the decision on the Dec 15th

tariffs, the bulls have done a very good job of defending the overall index

trends. However, as the weekend approaches,

one wonders how long they will remain this brave in the face of so much uncertainty. Futures are modestly bullish this morning ahead

of the Jobless Claims, and PPI reports. After

the bell, we will hear from ADBE, AVGO, COST, & ORCL earnings that could prove

to be market-moving. A confusing and

worrisome market to be sure so plan your risk carefully.

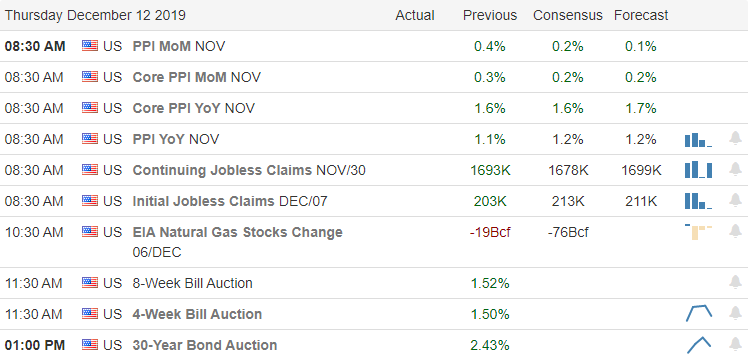

Do you have an Edge? That is the question I continue to ask myself as we wait on trade talks and a tariff decision. We know the market continues to be very sensitive on this subject, and we experienced yesterday the market could move substantially on any news report or rumor on the subject. Every trader should consider carefully consider their risk as this market-moving decision approaches. If that would not enough, we also have an FOMC rate decision at 2:00 PM Eastern to consider today. Although the expectation is the committee will hold rates steady, a change in the statement or the Chairman’s press conference can create some price volatility.

Overnight Asian markets closed mixed but mostly higher as they

closely monitor tariff news and the possibility of a Phase 1 trade deal. European indexes trade mixed but mostly lower

this morning ahead of the FOMC rate decision.

US Futures ahead of the CPI report indicate a relatively flat and mixed

open with the QQQ looking the most bullish, but that could change significantly

by the open. Don’t be surprised if

indexes become light and choppy as we wait on the FOMC decision that may well

prove an overall non-event.

On the Calendar

On the hump day Earnings Calendar, we have 37 companies fessing

up their quarterly results. Notable

earnings include AEO, LULU, TLRD, PLCE, UNFI, & VRA.

Action Plan

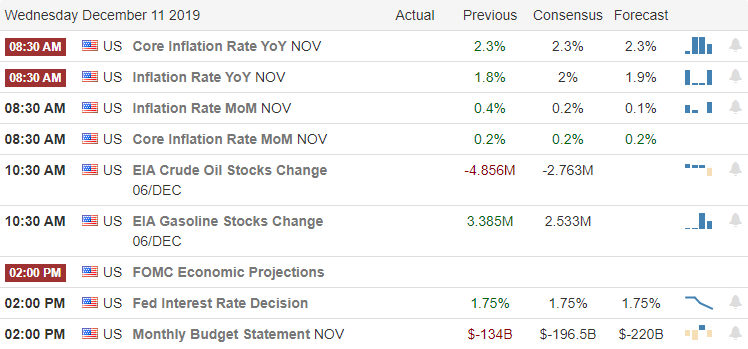

Only 14 days to Christmas!

Before the market opens today, we will get the latest

reading on the CPI number. Consensus estimates

expect a slight decline but could move the market and affect the open if the

reading happens to surprise. At 2:00 PM,

FOMC will release the results of the 2-day interest rate meeting. Their decision is likely to be a non-event

because the expectation is they will hold rates steady and unlikely to change forward

projections. Of course, if during the

Chairman’s press conference, if we learn something more about their forward-thinking,

we could experience some price volatility.

As the House prepares to impeach the President, the main

market focus at the moment is the US/China trade deal and, more importantly,

what it may mean for the Sunday scheduled tariff increase. We saw the market sensitivity

to this yesterday as the pre-market futures quickly recovered due to a Journal

report. Then, when the government couldn’t

confirm the tariff delay as reported, the market quickly reversed to the negative

whipsawing prices. With that in mind,

carefully consider your risk as we wait for the Presidents decision.

Articles of impeachment, pending tariffs, or phase one deal,

and a pending FOMC decision is a trifecta of uncertainty and possibly the

perfect storm for price volatility. This

morning the bears are reacting to the uncertainty but we could be just one news

report or tweet away that from triggering major sentiment shift. What comes next is anyone’s guess and the

question we much answer is how much risk are we willing to take while we wait

for the next shoe to drop. If it happens

during the day, traders can react, but if it occurs overnight, traders will

have have to deal with the aftermath. Consider

your risk very carefully!

Asian markets closed mixed but mostly negative as China

consumer inflation jumps in November and pork price surge 110 percent. Across the pond, Eurozone indexes are red

across the board as they closely monitor the approaching tariff deadline. US Futures indicate the bears are once again

making a push lower this morning with the Dow pointing to 100 point gap down ahead

of earnings and economic reports.

On the Calendar

On the Earnings Calendar, we have 26 companies stepping up

to report quarterly results. Among the

notable reports today are GME, AZO, PLAY, & OLLI.

Action Plan

Santa will be here in 15 day!

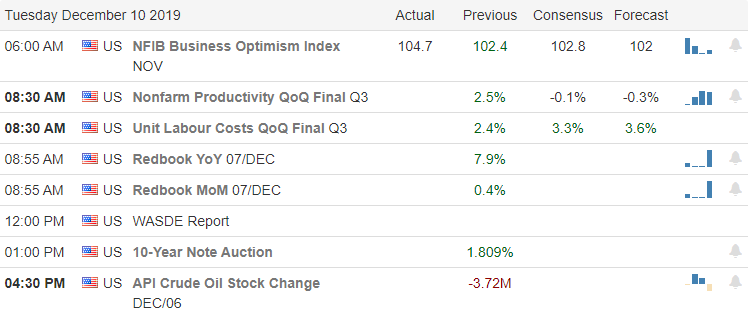

It would appear that Congress has made some progress may finally complete the North American trade deal that has been languishing for many months. At the same time, the House has prepared articles impeachment that may be released as early as today and voted on by the end of the week. While all this political drama has been unfolding, the market has been holding its breath, waiting for clarification of the Phase 1 trade deal with China or if there will be a new tariff increase this Sunday. Monday’s sideways chop displayed the uncertainty of the market. According to the reports, China has agreed increase its soybean purchases and reported pork price spiked 110% in November.

As we wait for some clarification, the bears have come out to

play with futures markets pointing to lower open this morning. A little fear seemed to creep into the

thinking of the market yesterday with the rising 16% as the indexes price

chopped sideways. Today begins the 2-day

FOMC meeting with an announcement scheduled for 2:00 PM Eastern Wednesday. Although they have projected a wait a see approach

on further rate cuts, waiting for their actual decision always adds a twinge of

uncertainty for the market to work through.

After a big Friday rally and at the cusp of new record highs,

the market this morning is tiptoeing on a bed of pin and needles. Will there or won’t there be a Phase 1 trade

deal? What will the President decide about

the Dec. 15th tariff increase? The market is waiting for answers to these questions

and the decision is likely to have substantial impacts on overall market sentiment. Tensions

between the countries flared once again with China accusing the US of violations

of international law after the House passed a bill citing human rights violations

for their use of detention camps.

Overnight, Asian markets closed mixed but mostly higher even after reporting declines in exports for November. European markets are modestly lower across the board this morning and US Futures chop around the flat-line with a slightly bearish lean. With such a big decision pending, plan your risk carefully, and plan for the possibility of substantial moves depending on the answer we receive!

On the Calendar

On the Earnings Calendar, we have 27 companies fessing up to

their quarterly results. Among the notable

earnings are CASY, CHWY, SFIX, TOL, & MTN.

Action Plan

What, no premarket pump, no 5 AM news citing unnamed sources

to start the day? Well, that’s a change

that we will have to keep a close eye on as we move toward the December 15th

tariff deadline. Though the Director of

the National Economic Council Larry Kudlow said on Friday that the Phase 1

trade deal was getting closer to completion, China appears to be very unhappy this

morning. Last week the House passed a

bill chastising China for its use of detention camps. During the night, China claims the bill

violates international law flaring tensions between the two countries once

again. The President’s decision could be

critical for the market direction this week.

Until then, we wait on pins and needles!

Santa is coming!

Technically speaking, the bullish trend is still in tack, but

after a 4-day recovery rally of more than 675 Dow points, perhaps a little rest

is just what the doctor ordered. The SPY

came very close to breaking to new record highs on Friday’s strong rally. However, close also means that the price

resistance above did its job of holding the line as we wait on an important

tariff decision. What happens next could

be some big moves either up or down, depending on the decision. Remain flexible and plan your risk

accordingly.

The two days of light choppy price action is likely to get a

shot of volatility this morning with the release of the Employment Situation

number at 8:30 AM. Although the ADP

number showed a sharp decline, it will be interesting to see if that will

manifest in the government number. The

bulls seem to suggest the number will be positive as the once again pump up the

early morning futures. As we head into

the weekend facing a tariff increase on the 15th, I would not be too

surprised to see some profit-taking.

Asian markets closed the week on a bullish tone with modest

gains across the board. European markets

are moving higher this morning green across the board. US Futures also point to bullish gains at the

open that could easily expand the gap if the Employment number is positive or diminish

if the number happens to be disappointing.

Plan you risk into the weekend carefully as the political football of

US/China trade continues to be kicked around in the news.

On the Calendar

On the Friday Earnings Calendar, we

have a relatively quiet day with only 15 companies reporting. Notable earnings include BIG and GCO.

Action Plan

Another day of chop after attempting a pre-market pump,

traders took a wait and see approach.

This morning the focus will turn toward the Employment Situation number,

and once again the futures are tiring to lift the market ahead of the number. The good news is we will likely get some

price action today, but the question remains will retail traders get much of a

chance, or will it most of the price action occur in the gap. One thing for sure is that the bulls are still

in control with a relentless optimism amidst the political uncertainty.

After the morning rush, the market could once again turn its

attention to the pending tariff increase scheduled on the 15th. It the bulls continue to ignore the potential

risks pushing toward new record highs, or will there be some profit-taking into

the weekend to avoid the risk? Only time

will tell, but I, for one, will want to be more of a profit-taker rather than

adding risk into the weekend.

The big morning gap yesterday seemed to be met with a lot of

uncertainty as to what happens next with the Phase 1 trade agreement. The bulls find very few buyers after the gap,

and the bears could not inspire any sellers, so we lingered the rest of the day

in a choppy sideways consolidation waiting for news to break the deadlock. Although the uncertainty remains, the futures

market that had been flat most of the night found some inspiration somewhere to

once again point to a bullish gap up open.

Asian markets closed positive across the board overnight as confusion over the trade continues. European markets are trading mixed but mostly higher this morning ahead of German economic data. US Futures point to a 100 point Dow gap ahead of the biggest day of earnings this week and some potential market-moving economic reports. The market is very news sensitive regarding trade, so remain flexible as sentiment could quickly shift as this political drama continues.

On the Calendar

On the Thursday Earnings Calendar, we have our biggest day

of the week, with 51 companies reporting. Notable reports include ULTA, AOBC, CM, CLDR,

DOCU, DG, DLTH, EXPR, GWRE, JILL, KR, MIK, SIG, PLCE, TIF, & ZM.

Action Plan

After the morning pop yesterday, the price action in the

indexes stagnated in a sideways chop seemly uncertain as to what comes next. However, this morning, futures have found

some inspiration even though the future of the Phase 1 trade deal remains uncertain. With the decline in petroleum reserves and

the expectation that OPEC may make deeper cuts in oil production, there was

some nice movement in the sector yesterday, helping to the overall market.

Today is the biggest day of earnings this week and could provide

the source of inspiration for the bulls or the bears. However, in light of yesterday’s sharp decline

in ADP numbers, the Friday Employment Situation report may create more

consolidation after the morning rush while we wait. With the market sensitivity to any news on

the trade deal and what that might mean for tariffs, traders will have to

remain very flexible and prepared for quick price action surges or reversals. As the indexes move back up toward price

resistance levels, remember to take some profits.