The celebration of the FOMC’s commitment to hold rates at historic lows for years lasted about an hour before the bears reemerged, seemly gaining the upper hand by the close. The price action left behind some troubling candle patterns and set the stage for possible index lower highs at price resistance. With futures pointing to a nasty gap down open, the question now is, will recent lows and the 50-day moving averages hold as support?

Asian markets closed in the red across the board overnight. European markets are also decidedly bearish this morning despite the Bank of England’s’ decision to keep rates low. Ahead of potentially market-moving economic reports, US Futures point to a substantial gap down at the open. Expect another wildly volatile day.

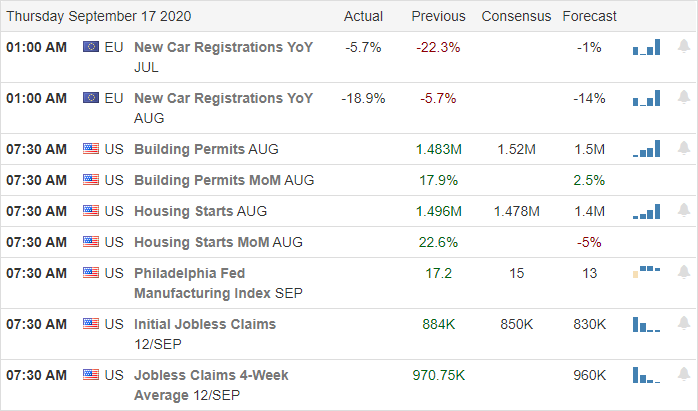

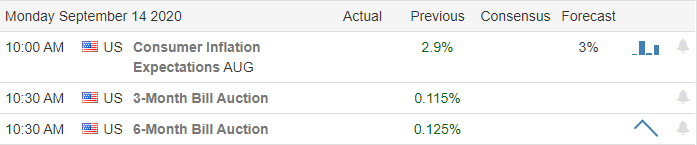

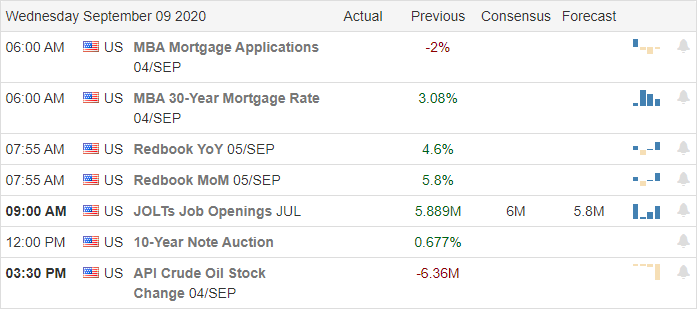

Economic Calendar

Earnings Calendar

On the Thursday earnings calendar, we have a light day with less than 10 confirmed reports. Notable reports include APOG & CMD.

News & Technicals’

After the FOMC committed to keeping interest rates at historic lows, we experienced a nasty intraday reversal with the bears surging into the close. During the Jerome Powells press conference, he noted that the economy looking forward remains uncertain and may take an extended time for employment to recover. Snowflake, ticker (SNOW) doubled yesterday to become the most significant software IPO in market history. The shares priced at $120 per share for the initial offering soared to over $253 in yesterday’s trading. OPEC and its allies are meeting today to discuss production limits. Analysts at this time don’t believe there will further production cuts but do expect the then to renew their commitment to the deep cuts they’ve already made.

The last hour selloff in the indexes left behind some worrisome candle patterns at or very near price resistance levels, possibly setting the stage for lower high price patterns. Early rallies in the financial and oil sectors struggled to hold onto gains as the bears once again seem to gain the upper hand. Unfortunately, the US Futures currently point to a substantial gap down this morning. A painful reminder that buying stocks near price resistance levels is a practice that retail traders should avoid. The question to be answered now is whether the recent lows at or near the 50-day moving averages will hold as price support or will an official downtrend be established? Today we have a light day on the earnings calendar, but before the bell, we will get the latest reading on Housing Starts, Jobless Claims, and the Philly Fed MFG Index. Prepare for another volatile day.

Yesterday ended with a mixed bag on index results heading into a big day of economic data that includes an FOMC statement and the chairman’s press conference. With the indexes closing at or very near price resistance levels, today’s data may well inspire the bulls higher or bring bears out of hiding depending on how investors digest the results. With an elevated VIX and futures pointing to gap up open, it seems an understatement to say anything is possible. Stay focused, and flexible.

Asian markets closed mixed in a rather falt session after Japan reported a disappointing plunge in exports. European markets trade mixed, cautiously awaiting the central bank decision. Overnight futures struggled to gain ground, but as the open near the pre-market pump up has begun suggesting another bullish morning gap. Buckle up.

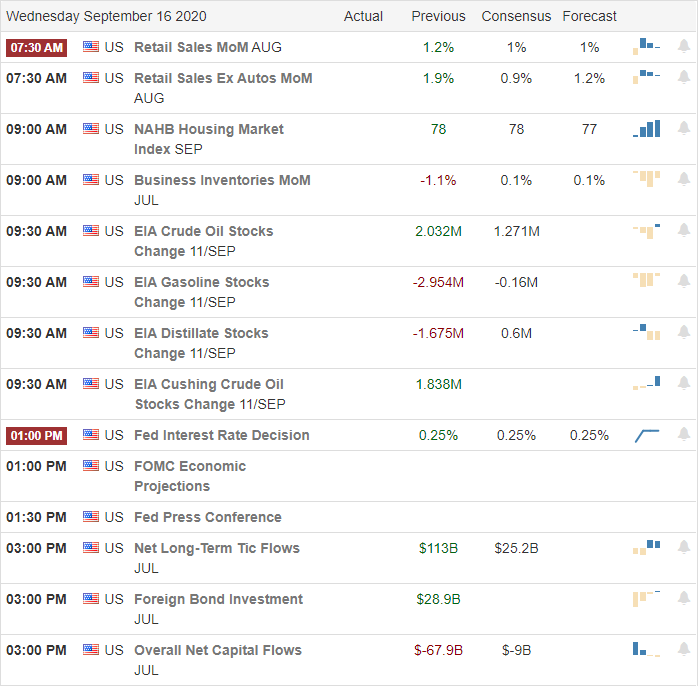

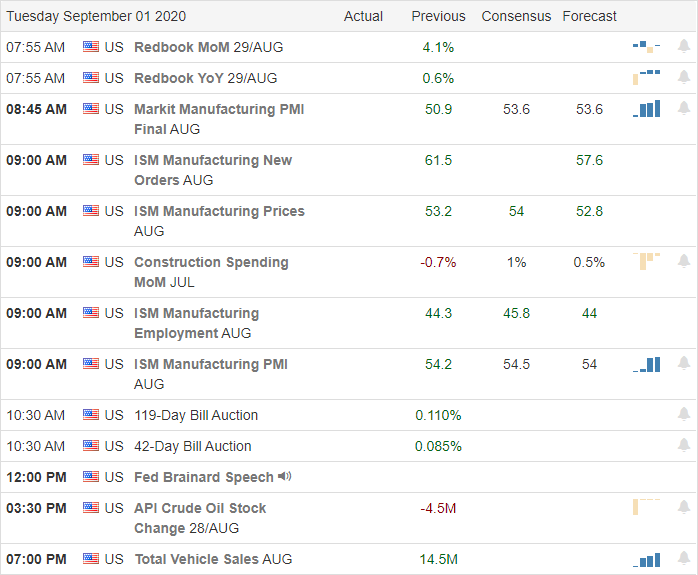

Economic Calendar

Earnings Calendar

On the Hump Day earnings calendar, we have just 16 companies reporting quarterly results. Notable reports include BRC & MlHR.

News & Technicals’

Though there was a lot fo bullish energy at the open yesterday, we ended with a mixed bag of results. The SPY and IWM mostly chopped in a narrow range, with the DIA giving up early gains to close essentially flat. The QQQ and big tech struggled to hold the morning gap in the morning session, but the bulls fought back, closing the index with solid gains near price resistance levels. After the bell, FEX and ADBE produced strong earnings, with both stocks indicating substantial gains at the open today. However, during the night, US Futures seemed to struggle, often dipping into negative territory until early morning pump up began, which seems to have become the standard operating procedure for this year. Blackstone’s Tony James is warning this morning of a possible lost decade where market returns become anemic in a low-interest-rate environment but facing significant headwinds moving forward. During the night, Hurricane Sally strengthened to a Category 2 storm that made landfall at high tide, shutting down power and threatening widespread flooding. What a year! To much water in the south while the Pacific coast burns, suffering from drought.

The FOMC will be in focus today as we wait for there interest rate decision, and of course, all eyes will be on the Jerome Powell at the press conference that follows. If that’s not enough, we keep investors guessing we also have Retail Sales, Business Inventories, Housing Market Index, and a Petroleum Statis report to digest before the 2 PM eastern statement release. Add to that index charts testing price resistance levels and an elevated VIX, and I think it’s safe to say anything is possible. As I write this report, futures point to a gap up open; however, I would not be at all surprised to see very anemic and choppy price action ahead of the FOMC decision. Becare not to chase with a fear of missing out if the morning gap does unfold.

It looks as if yesterday’s nice relief rally will enjoy a flow-through gap up this morning. The question is, will the bears be lying in wait to attack as we approach resistance in the index charts? The lackluster performance of big tech and the new daily record of COVID-19 cases reported by the WHO adds some uncertainty. Remember, the FOMC meeting begins today, and the market will often become choppy as it waits for there direction.

Asian markets closed mostly up overnight as China reported its first positive retail sales report since the beginning of the pandemic. European markets are cautiously bullish this morning as they await the central bank decision. Us Futures point to another substantial gap up open ahead of economic and earnings news and kick off the of the 2-day FOMC meeting.

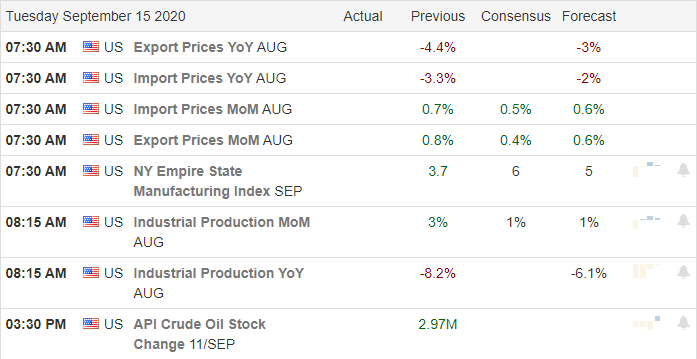

Economic Calendar

Earnings Calendar

On the Tuesday earnings calendar, we have 17 companies reporting quarterly results. Notable reports include ADBE, FDX, and CBRL.

News & Technical

The nice relief rally fell short of breaking price resistance in the index charts as big tech produced a lackluster performance. The VIX pulled back but remained relatively elevated, closing well above 25 handles. The WHO reported a record one-day spike in coronavirus cases and warned that the pandemic shows few signs of slowing. In a somewhat confirming story of the epidemic, the IEA cut 2020 oil demand seeing a ‘treacherous’ path ahead due to the rising cases heading into the fall. The President seems to have walk back his requirement of a TicTok sale approving of the deal with Oracle. Apparently, in the partnership of the social media app, Oracle will be responsible for the privacy concerns that caused potential banning. However, make no mistake the apps fundamental purpose to data-mine users as all social media will continue.

Technically speaking, yesterday’s bounce quickly moved the T2122 indicator from short-term oversold but may near a short-term overbought condition as soon as the open today as the all or nothing knee-jerk reaction volatility continues. The FOMC meeting begins today, and traders should keep in mind that it’s pretty standard for the market to become quite and the price action choppy as we wait for the statement and Powell’s presser. As we approach resistance in the index charts, observe to see if the bears will line up in defense. Yesterday week performance in the big techs is a bit concerning should those bears decide to attack. With the election on the horizon and coronavirus cases rising, the uncertainty of the path ahead is likely to keep traders on edge and volatility high. Plan your risk accordingly.

A big weekend of buyout news combined Friday afternoon bounce that left the DIA and SPY hovering above there 50-day averages has the overnight futures pointing toward a substantial gap up this morning. However, keep a close on the overhead resistance above as new cases of COVID-19 begin to rise, and the presidential election that adds significant uncertainty to the path forward.

Asian markets rallied overnight as Japan’s Softbank lept by 9% after the announcement that Nvidia will buy Arm Holdings from them in a 40 Billion dollar deal. However, European indexes are flat and mostly lower this morning, giving up early gains as Brexit challenges persist. US Futures suggest a gap up of 250 points in the DOW ahead of a light day of earnings and economic reports. Traders should expect challenging price volatility to continue.

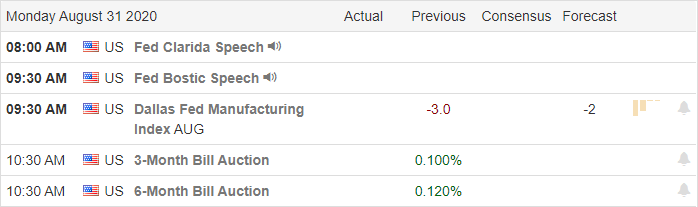

Economic Calendar

Earnings Calendar

On the Monday earnings calendar, we have a light day with just 14 companies stepping up to report. Looking through the list, there is only one, LEN, that stands out as a notable report.

News & Technical’s

As more than 100 wildfires continue to burn, across California, Oregon, and Washington, the search for missing people has begun. Millions of acres have burned with some entire communities decimated as high winds continue to challenge firefighter efforts. With college in full swing around the country, cases of COVID-19 are starting to tick higher once again. The Whitehouse medical advisor warned this weekend to brace for a problematic fall with the likely spread of the virus picking up pace. As of now, nearly 200,000 Americans have fallen victim to the pandemic. Nvidia is spending 40 billion to buy Arm Holdings from SoftBank in a busy weekend news cycle of buyouts. Innunmedics shares doubled after news that Gilead agreed to by the cancer drug maker in a 21 million dollar deal. In the battle for TikTok, it looks like Oracle may have emerged the winner to partner with the popular social media app only days before the ban deadline. According to reports, Chinese owners reject Microsoft’s offer in favor of Oracle this weekend.

The DIA & SPY continue to hover above their 50-day moving averages bouncing Friday afternoon. The QQQ also bounced but lacked the energy to recover its 50-day average by the close. All the buyout news seems to have inspired the bulls this morning, with Futures pointing to a gap up open in the DOW of nearly 250 points. The bullish price action could trigger a bit of a short squeeze this morning but let’s not forget the resistance above the selloff as created. The historically low rates favor the bulls, but the uncertainty of rising COVID-19 cases and the upcoming presidential election could also inspire considerable price volatility.

Another day of wild price action as the market whipsawed early gains into substantial afternoon declines that left behind a bearish candle pattern and likely damage some investor confidence. Adding to the selling pressure was the failed attempt of the Senate to gain the votes needed to advance another COVID stimulus package. Although US Futures point to a bullish open today, keep in mind a test of the 50-day average in the Dow and SP-500 is not out of the question in the days ahead.

Asian markets finished the week on a high note bouncing to close green across the board. However, European markets trade mixed and mostly flat with Brexit issues in focus. US Futures point to a bullish overnight reversal, a welcome relief from the selling ahead of the latest reading on the CPI. Expect price volatility to continue as we slide into the weekend.

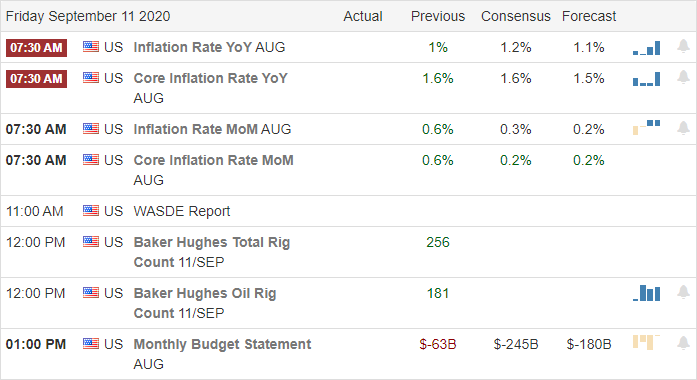

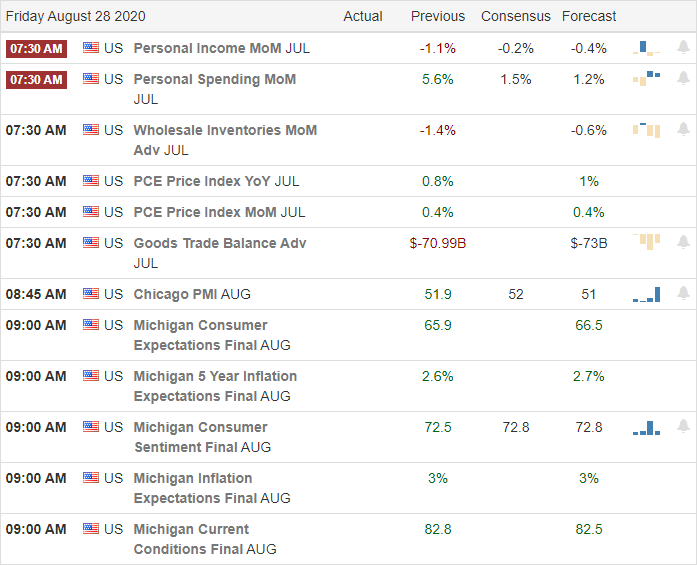

Economic Calendar

Earnings Calendar

On the Friday earnings calendar, we have just 14 companies reporting quarterly results. About the only notable report I can come up with today is the report from KR.

News & Technical’s

Yesterday was another wild ride with the Dow rallying more than 200 points at the open with an intra-day reversal that sent the index plunging more than 500 points, leaving behind an ugly bearish engulfing candle. The SP-500 closed the day less than 25 points above its 50-day average with the Dow just 230 points away. Testing this key technical average seems quite likely in the days ahead even though the Friday morning futures point to an overnight bounce. The Senate tried but failed to move forward another federal stimulus package disappointing a market that had become absolutely addicted to the massive deficit spending. According to reports hacking attacks attempting to influence the outcome of the Presidental election are coming from all over the place. Both campaigns have suffered attacks.

Although there is no technical damage to the index moving averages yesterday, create some price action damage making lower highs and falling below some price support levels. Yesterday’s price action also left behind bearish candlestick patterns and likely damaged the overall investor confidence. The VIX closed above a 29 handle, but it’s interesting to note it didn’t register a sharp increase in fear as the selling accelerated in the afternoon session. I suspect we are at or very near a short-term oversold condition that warrants a bit of a relief rally; however, I would be very wary of the idea that the full market pullback is over.

Traders should fasten their seat-belts tightly because it looks as if the road ahead may continue to be challenging to navigate. With the radical price swings, trading risks are extraordinarily high so consider your decision carefully should you choose to risk your hard-earned money in a market where it is near to impossible to maintain an edge. Very experienced day-traders have the upper hand, while swing and position traders have a substantial risk of intra-day whipsaws and complete overnight rehearsals.

Asian markets closed the day mixed but mostly lower overnight. European markets are modestly bearish this morning ahead of an ECB meeting, and the US futures currently point to a bearish open ahead of earnings and economic reports.

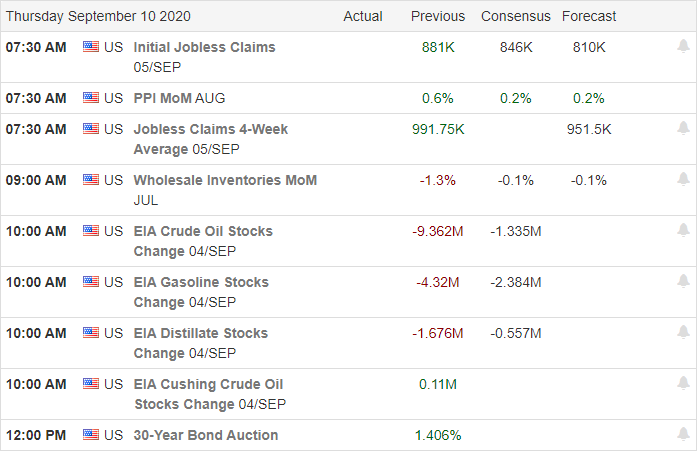

Economic Calendar

Earnings Calendar

On the Thursday earnings calendar, we have 22 companies reporting quarterly results. Notable reports include CHWY, PTON, PLAY, ORCL, & ZUMZ.

News & Technical’s

The wild price action volitility continued yesterday will a big relief rally, but the big question is can it hold. After rising more than 680 points, the Dow dropped more than 200 points in just 30 minutes, heading into the close. The VIX pulled back nicely but ended the day holding at its 200-day average and remaining elevated at the finish, pointing to the significant danger these big price swings create. What comes next is anyone’s guess, so use caution avoiding overtrading because retail traders have little to no edge with such an uncertain condition.

In the index charts, there continues to be no significant technical damage; however, the threat that DIA and SPY may yet test their 50-day moving averages does still exist. Although a light day on the earnings calendar, we do have several notable reports as well as an economic calendar that includes Jobless Claims, PPI before the bell for the market to digest before the open. Currently, futures point to a bearish open, but a lot could change over the next 2 hours with volatility so high. Buckle up the road ahead is likely to remain bumpy and very challenging to navigate.

In the last 3-trading days, we’ve received a reminder that bears still exist despite a very favorable Fed and massive governmental intervention. Although the futures point to a nice relief bounce at the open, let’s not forget that the 50-day average may still get tested in the days ahead. Be careful rushing back into highly volatile price action with the buy the dip mantra ringing in your ears. Stay focused and consider carefully how this wild price action takes away a trader’s edge.

Asian markets closed in the red across the board overnight as tensions with the US continues to grow. European market point to a modest bounce at the open, and the US futures point to a little relief rally ahead of earnings and the JOLTS number at 10:00 AM Eastern. Expect the wild price volatility to continue.

Economic Calendar

Earnings Calendar

On the Hump day earnings calendar, we have 20 companies stepping up to report quarterly results. Notable reports AVAV, ABO, GIII, GME, NAV, RH, VRNT, & ZS.

News and Technical’s

After a 3-day nasty selloff, futures point to a modest bounce this morning. With the Dow closing just 1.2% above its 50-day average and SP-500 hovering less than 1% above this critical technical indicator, traders should be cautious with the buy the dip mantra and rushing into positions. Although there has been nothing typical about this year’s market, we must consider the possibility that 50-day averages may still experience a test of support. Market pullbacks most certainly provide buying opportunities; however, the violence of this selloff adds the tremendous risk head fakes and fast intraday reversals with the VIX so elevated. A bounce may, in fact, provide an opportunity to take some risk off the table rather than add—something to consider as you plan your day forward.

Technically speaking, the indexes were so overextended they have yet to experience any significant technical damage even though the psychological damage has been rather extreme. Fast moves like this make traders very jittery so prepare for considerable price volatility in the days ahead. If this pullback has hurt, you guard yourself against revenge trading. Stay focused on your plan and your rules. The market is a high-risk proposition at the moment, so carefully consider this question. Are you gaining or losing your edge when trying to trade an extremely volatile market. Plan carefully!

Due to a computer snafu, the usual blog is unavailable. Sorry for the inconvenience.

Economic Calendar

Earnings Calendar

On the Tuesday Earnings Calendar, we have just 14 companies stepping up to report quarterly results. Notable reports include BBW, CAL, HRB, JAMF, & SCVL.

The tremendous August market performance looks to finish strong this morning with 3-new companies trading on the Dow as well as new shares from the stock split in AAPL and TSLA. Coming as the biggest August rally since 1986, the question is, can the bullishness continue with a 3-day weekend on the horizon. Stay focused, be careful not to over-trade and extended market and remember bears still exist even though we’ve not seen them for quite a long time.

Asian markets closed mixed but mostly lower overnight, but European markets trade higher this morning inspired by the very dovish Fed. US Futures point to modest gains at the open but could easily add fresh new records as the bulls continue to ride the wave of governmental stimulus.

Economic Calendar

Earnings Calendar

On the last day of August 2020, we have 12 companies repoing quarterly results. Notable reports include SCSC, BAM & ZM.

News & Technical’s

On our last day of August, we have three new companies trading on Dow with APPL and TSLA trading with new shares after splitting their stocks. Historically August is not a great month for the markets, but this year August will end with its most robust performance since 1986 amid unprecedented governmental intervention. The magnitude of the market recovery is nothing short of remarkable considering the national GDP is a negative 31 with 1 in 3 Americans unemployed. According to reports, the FDA is ready to fast track coronavirus vaccine ahead of phase three trials breaking with its typical protocols. Yesterday, India set a new world record, reporting more than 73,000 new infections in a single day. The violent protests in Portland, Oregon, that have gone on for 3-months turned deadly this weekend with a shooting. Killing each other over political ideology is nothing new, but it’s a shame how divided and weaker we are as a nation as a result.

With bullish and fresh new records on Friday, the Futures point to bullish open. Although the index appears stretched, there is at this time no price action clues of bearishness beginning. However, with a 3-day weekend on the horizon, a declining Absolute Breadth Index, as well as a stubbornly elevated VIX, traders should not become complacent. Bears still exist and could attack at any time, so stay focused and flexible.

A new record high in the SP-500 but an intra-day whipsaw and a rising VIX could suggest a little turmoil is brewing under the surface. As we head into a big day of data, the market is hoping to get more clarity and forward guidance on continued aggressive asset purchases from the Jackson Hole symposium. The bulls have enjoyed an incredible run producing the best August for the SP-500 since 1986. Heading into the weekend stay focused and plan your risk carefully yesterday’s turbulence may signal profit-taking could begin at any time.

Asian markets closed mixed but mostly higher overnight after hearing there longer serving Prime Minister will step down citing health concerns. European markets are also mixed but mostly lower this morning as US Futures continue to drive higher with the Dow pointing to a gap up of 100 points but a relatively flat NASDAQ.

Economic Calendar

Earnings Calendar

The Friday earnings calendar is a relatively light day with just 12 companies reporting. Notable reports include BIG & HIBB.

News & Technical s

The new Fed policy that will allow inflation to rise above 2% by keeping interest rates very low for an extended time was approved by the market with a new record high in the SP-500. However, there was some volatility during the day with an intra-day whipsaw that the bulls managed to defend by the close of the day. With the Jackson Hole symposium continuing today the markets are hoping to hear more forward guidance from the Fed and a commitment to continue aggressive asset purchases. With all the warm a fuzzy talk and massive amounts of newly printed money, the SP-500 is headed for it best August since 1986 despite 1 in 3 unemployed Americans. Interestingly the VIX rallied briefly above 26 handles settling at the close in the mid 24’s, indicating investors remain nervous that another market dip is possible.

The technicals of the daily index charts remain very bullish; however, the intra-day whipsaw, a falling absolute market breadth index, and rising VIX may suggest a little trouble under the surface of this historic recovery rally. With a big day of possible news-driven price action and the weekend just around the corner, plan your risk carefully and don’t be surprised if profit-taking picks up to capture the gains of this very bullish week. Have a wonderful weekend, everyone.