Stimulus hopes created a big short squeeze rally, but the uncertainty yesterday afternoon made tremendous price volatility as market sentiment swung violently. Renewed hopes once again have US Futures pointing to a big emotional morning gap, but traders will have to be on guard for more wild price swings driven by political news sensitivity. Adding to the potential volatility is a big day of economic reports that can potentially move the market substantially.

Asian markets had a rough overnight session with the NIKKEI closed due to an electronic system failure. European markets are cautiously bullish this morning as they track developments on the US stimulus package. Ahead of a busy economic calendar, US Futures point to Dow gap up as traders speculate on a stimulus agreement. It could be a wild ride today so stay focused and flexible.

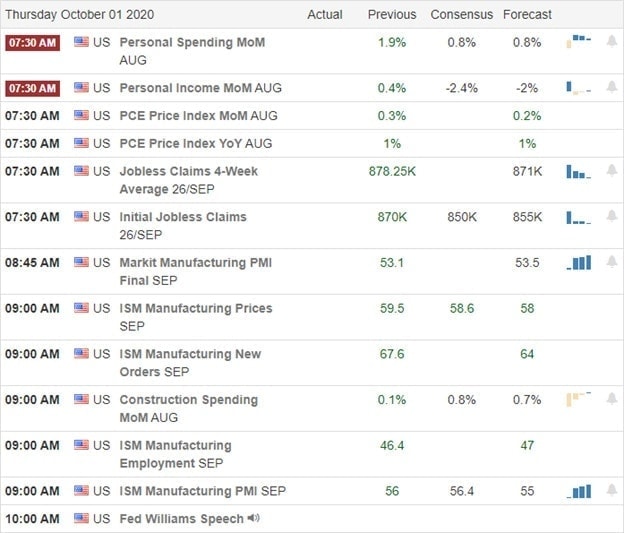

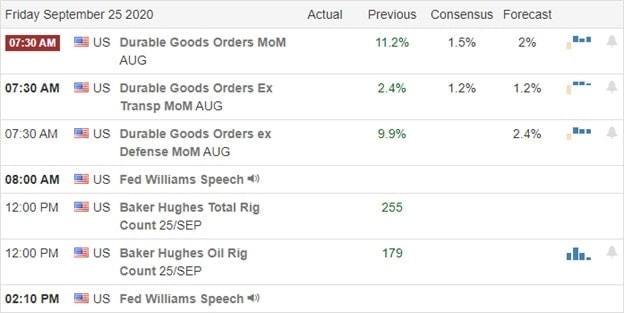

Economic Calendar

Earnings Calendar

On the Thursday earnings calendar, we have another light day with just 9-confirmed reports. Notable reports include CAG, PEP, STZ & BBBY.

News and Technicals’

Hopes of a new stimulus bill and some end of quarter window dressing fueled a substantial short squeeze yesterday. Unfortunately, the day ended with tremendous price volatility when the House delayed the vote on the 2.4 trillion dollar plan. The President has extended an offer for 1.2 trillion, so the standoff continues today. Airlines are moving forward to Furlow around 38,000 employees today, saying they will reverse the decision if another 20 billion in bailout funds, that’s part of the stimulus plan, is approved. The Senate passed, and the President signed a spending bill after funding briefly lapsed, avoiding a government shutdown. Asian markets had a tough night with trading suspended for a full session due to a failure in the Tokyo fully electronic system. Apparently, the backup system all failed as well.

With some hope renewed on a stimulus bill, US Futures point to another big gap-up open this morning. Traders will have to stay on their toes as any news coming out the Washington spin cycle could crate quick price reversals should congress fail. The big move yesterday improved the technicals of the index charts pushing the DIA and SPY above their 50-day averages and increased the risk due to the substantial political uncertainty. Facing another big day of economic reports, prepare for anything as this wild rollercoaster ride continues.

Heading into a big data deluge for the next 3-days the last thing we need was to hear was 28,000 job losses at Disney, 9000 from Shell that will add to the 10’s of thousands of airline workers that could lose their jobs tomorrow if billions in bail money is not approved in the next 24 hours. Expect the considerable price volatility and investor uncertainty to remain with us for the rest of the week if not through the election. As far as the debate goes, all we confirmed is the embarrassing behavior of our leaders.

Asian markets closed mixed but mostly lower overnight, and European markets trade cautiously bearish this morning with modest losses across the board. US Futures have bounced off overnight lows ahead of economic data and a very light day of earnings reports. Stay focused as we test resistance in the indexes as downtrends remain intact.

Economic Calendar

Earnings Calendar

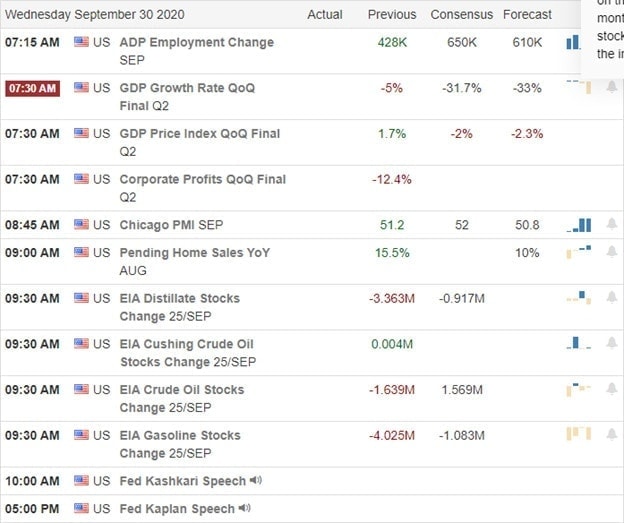

On the hump day earnings calendar, we have a light day with just six companies expected to report. The only notable report is the gold miner NG.

News & Technicals’

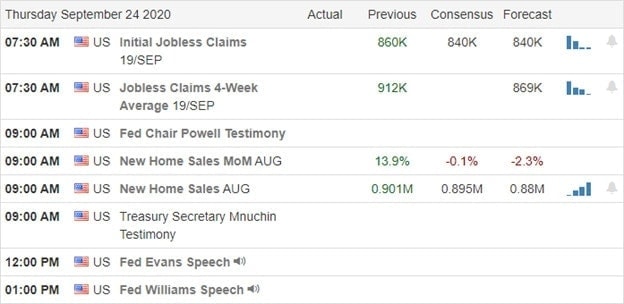

As we head into October, the market focus will turn toward job numbers over the next 3-days. After the bell yesterday, Disney announced a layoff of 28,000 employees. Unless airlines receive billions in bailout money in the next 24 hours, 10’s of thousands of airline employees join the unemployment line. Adding insult to injury, Shell also announced 9000 job cuts as the oil sector continues to suffer impacts from coronavirus. US Futures remained bullish during most fo the Presidential debate, but after it ended, they began to sell-off. I’m not sure we learned anything in the argument that the market didn’t already know but rather sold off merely from the embarrassment of it all. Today before the bell, we will get a jobs reading from the ADP, a GDP report that’s likely to remain to be quite ugly, PMI, Pending Home Sales, and the Petroleum Status numbers. That said, expect more volatility and uncertainty heading into the close with another busy economic calander of market-moving reports on Thursday.

Yesterday’s price action seemed to reflect the uncertainty of the debate and the data deluge ahead, chopping in a rage with equally matched bulls and bears. The DIA, SPY, and IWM remain in downtrends while the QQQ tries to lead the market higher, holding on to its 50-day average by the close. However, with so much data coming our way, anything is possible, so stay focused and flexible.

Yesterday’s rally was a tremendous relief from the selling pressure, but with the indexes thrusting up into price resistance levels all in one move, it also creates a tough decision for traders. Do you buy with the fear fo missing out at the price resistance where a reversal back down could occur, or do you wait for a lower risk entry? Tough decisions with a big week of economic data, coronavirus concerns, and massive political dramas on several fronts adding a hefty dose of uncertainty to the mix. Choose carefully because the next big swing could occur at any time.

Asian markets closed the day mixed but modestly higher in a choppy session, reflecting the uncertainty ahead. European markets after a big relief rally yesterday are in pulling back with Brexit issues and US politics, creating a bit of caution. US futures pulled back from evening highs, shifting slightly negative, but as we approach the open, they have become quite choppy ahead a light day of earnings reports and economic data.

Economic Calendar

Earnings Calendar

On the Tuesday earnings calendar, we have a light day with just 11 companies reporting quarterly reports. Notable reports include INFO, MKC & MU.

News and Technicals’

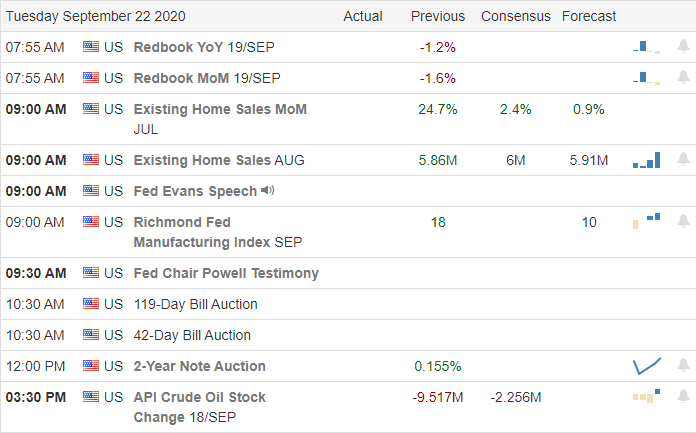

I’m running behind this morning, so this will be a short and sweet report. Yesterday was a nice rally, but unfortunitually, it didn’t change the technicals of the index charts. Pushing back into downtrends and price resistance can easily make us feel as if we’re missing out, and we make the mistake of buying at price resistance and breaking our trading plan rules. Though this could be the beginning of a rally that will extend higher, it could also be nearing the high point or failure point to continue the existing downtrend. Big tech seems to have the best chance of leading us higher, but the high price volatility, morning gaps, and overnight reversals require us to have a higher tolerance for risk.

The T2122 indicator went from oversold to nearly overbought in one fell swoop, and one has to consider the possibility that a similar reversal back down is equally possible. That creates a significant conflict in a trader between the fear of missing out and large potential losses that can quickly occur with such high volatility. The only way I know to resolve that conflict is to stick to your plan and follow your rules. Remember, your plan helps you make money; your plan helps you protect your capital. We have a lot of data coming our way in the next few trading days, so plan your risk carefully and expect the wild price volatility to continue for the foreseeable future.

Last Monday, a punishing gap down for those holding long positions, so I guess its only fair to punish those who held short positions over the weekend with a massive gap up this morning. Anyone else tired of this all or nothing, whipsaw morning gap market? Sadly I suspect there is more to come this week as we face an economic calendar chalked full of market-moving events and enough political drama churning in the news to all investors on edge. If that’s not enough, let’s toss in rising pandemic numbers for an additional dose of uncertainty.

Asian markets closed mixed but mostly higher overnight following reports of US sanctions as tech tensions continue to rise between the US and China. European markets are decidedly bullish this morning, with HSBC bouncing more than 8% on the day. US Futures are wildly bullish this morning, suggesting a Dow gap of more than 300 points to test its 50-average as resistance. With so much data coming our way, expect another week of wild price volatility to challenge traders!

Economic Calendar

Earnings Calendar

On the Monday earnings calendar, we have 19 companies reporting quarterly results. Notable reports include CALM, SINA, THO, UNFI, & WB.

News and Technicals’

Last Monday, the market gapped down huge, so I guess it only makes sense that the futures are pointing to a considerable gap up this morning. The President’s taxes dominate the news cycle this morning with the NYT reporting that he paid no taxes for several years due to business losses. Is should make for some great political drama in the Presidential debate scheduled for tomorrow. A federal judge has temporarily blocked the administration’s ban on new TikTok downloads form US app stores. However, the much broader ban is set to come into effect on Nov.12th was not part of the judge’s order, so expect this more turbulence with the tech tensions between the US and China. Speaker Pelosi still believes there is a chance to pass a stimulus deal, but the other side of the aisle appears much less optimistic that a compromise can be struck. Treasury yields are on the rise as signs of a worsening pandemic worldwide and hear in the US keep investors on edge as to what comes next.

Looking that futures this morning, one would guess there must have been some big news to drive such a surge upward this morning. If there is, it has escaped me! In fact, we face a very uncertain week ahead with a full economic calendar, a GDP number expected to come in pretty ugly on Wednesday, and the Employment Situation on Friday, not mention all the political drama churning up emotion as the election approaches. The bullishness this morning is nice to see but keep in mind the significant price resistance above that includes 50-day moving averages. Traders will have to stay on their toes for a possible short squeeze triggered by the morning gap or the equally likely pop and drop that could occur at resistance. Please fasten your seat belt tightly; it could be a bumpy ride ahead.

As the US House makes another attempt to pass a $2.4 Trillion stimulus package, Goldman Sacks cuts their 4th quarter GDP estimate in half, citing gridlock and fading hopes of additional stimulus. The early evening futures rally faded during the night, suggesting a substantial gap down at the open. With the DIA 200-day just over 1.85% lower, a test of that level is certainly within the realm of possibilities as we slide into a politically charged weekend.

Asian markets closed mixed overnight in a volatile session. European markets, unfortunately, decidedly bearish this morning as travel and tech stocks suffer more bearish pressure. US futures point to a substantial gap down at the open with a Durable Good report pending, rising virus concerns, and a pending Supreme Court appointment adding uncertainty to the weekend.

Economic Calendar

Earnings Calendar

We have a very light Friday earnings calendar with only three confirmed quarterly reports, with none of them rising to notability status.

News & Technicals’

The overnight futures session turned out to be a volatile and challenging as Thursday’s market price action. News that the US House is preparing a new 2.4 trillion stimulus package, including more direct payments, perked up futures during the early evening. However, this morning the bears appear to remain tenacious, reversing the overnight bullishness, now pointing to a lower open on Friday. I suspect as the pressure of reelection continues to grow, there will be a stimulus deal struck this time around. Apple will be back in court soon with the EU appealing there 15 billion tax battle to their highest court, attempting to reverse the lower court decision that favored the company. Goldman Sachs cut fourth-quarter GDP forecast in half, citing the stalemate in Congress that has delayed further government stimulus. Amazon announced a slew of new tech devices to boost the holiday shopping seasion, including a self-flying drone home security device.

Yesterday volatile session added more questions than answers for traders and did nothing to improve the technicals of the index charts. With the lackluster performance of the bulls yesterday and the bears proving much more tenacious than earlier this year, the confidence of a substantial bounce-back rally seems to have faded. With the DIA only 1.85% from testing its 200-day average and the political fireworks expected this weekend, we should not rule out the possibility of a test. On the other hand, the hopefulness of another massive government stimulus package could easily inspire the bulls triggering a short-covering rally. In other words, anything is possible, and traders will need to remain focused and flexible as we slide toward the uncertainty of the weekend.

It’s now clear that the bears were ready to defend price resistance levels in index charts leaving behind disturbing bearish engulfing candles as they overwhelmed the bulls. The T2122 Indicator suggests a very oversold short-term condition exists but with the DIA now less than 2% from its 200-day average, we can’t rule out a possible test. With COVID numbers rising in the US and Europe facing the possibility of a double-dip recession, the path forward is certainly uncertain. I expect price volatility will remain very challenging in the days ahead.

Overnight, in a volatile session, Asian markets closed in the red. European markets facing a resurgence of the virus trade mixed but mostly lower this morning concerned about the global economy. Ahead of earnings, Jobless Claims, and a lot more Fed speak US Futures point to muted and mixed open. Buckle up for another challenging day.

Economic Calendar

Earnings Calendar

We have our busiest earnings calendar this week, with 26 companies stepping up to report. Notable reports include DRI, COST, CAN, BB, KMX, FDX, JBL, RAD, TCOM, & MTN.

News & Technicals’

The early gap up gains quickly faded with the Dow giving up a 176 gain to finish the day down 525 points. With the DIA now less than 2% from its 200-day average, it now seems a likely target. After a Kentucky Court decision, protesters took to the streets that sadly resulted in 2 police officers shot as the protest turned violent. Thankfully both officers are expected to recover from there injuries. According to reports, Europe could be facing a double-dip recession with the pandemic spreading, creating new restrictions and obvious economic impacts. New cases are also rising again here in the US, putting a gloomy uncertainty over the market and path ahead for the US economy.

After a somewhat volatile overnight futures session, they currently point to a muted and mixed open ahead of earings, Jobless Claims, and a considerable amount of Fed speak. The technicals of the index charts are pretty ugly, but there is some hope with the T2122 Indicator suggesting a very oversold short-term condition. The significant bearish engulfing patterns left behind on the index charts are certainly dishearting, and we can’t rule out the possibility that the indexes might eventually test their 200-averages in the near future. However, if the news cycle gives us a little break, a modest relief rally could be in order. Traders will have to stay at the top of their game because wild price volatility is likely to remain quite challenging.

Although this earnings season has produced new record highs and much better than expected company profits, Jerome Powell suggested in his testimony yesterday that more government economic intervention may be necessary. With COIVD-19 cases once again on the rise and the national death toll in the US setting a world record of more than 200,000, the path ahead is definitely uncertain. The US House yesterday passed a spending bill that will prevent a government shutdown if approved by the Senate and signed by the President. Still, as the election looms, political tensions hit a fevered pitch, and the market is understandably concerned about what lies ahead.

Asian markets closed the day mostly higher with Australia leading the gains up more than 2%. European markets are seeing substantial gains this morning ahead of important euro-zone data. US Futures also point to significant gains at the open but be careful chasing the moring pop as we approach the downtrend and the price resistance above.

Economic Calendar

Earnings Calendar

On the hump day Earnings Calendar, we have just 12 companies reporting quarterly results. Notable reports include CTAS, GIS, JKS, & WOR.

News & Technicals’

Breaking a 4-day selling streak, big tech lead a modest relief rally in an otherwise choppy price action day as the indexes grind toward the resistance. After the bell, NKE reported blowout earnings substantially beating expectations and indicating about 12% this morning. The US House passed a spending bill sending it to the Senate for approval to avoid a government shutdown if approved and signed by the President. Sadly, the US has set another grim record in its battle with COVID-19 with a world record death toll that now tops 200,000. Parts of Europe are back under lockdown restrictions, and infection numbers here in the US are once again on the rise, with several states reporting their highest number of infections to date. Without a doubt, the pandemic continues to upend American life, and unfortunately, if numbers continue to rise, the damage to the economy is likely to much worse. With an average daily death toll around 800, it seems we have a long way to go if we are to defeat this microscopic enemy.

On the technical front, all four indexes remain in downtrends and below price resistance levels. Jerome Powell, in his testimony, suggested more government stimulus may be necessary to curb the economic damage of unemployment. However, Larry Kudlow, US Economic Council, later in the day, indicated that additional incentives are not required. No matter what you believe, there remains a tremendous uncertainty for the market to digest in the week and months ahead. This morning futures point to a bullish open but be careful rushing in with a fear of missing out as the indexes approach resistance.

The bears overwhelmed the market worried about political infighting over a high court appointment, a possible government shutdown, a delayed or no 2nd stimulus package, an upcoming election, and rising coronavirus concerns. Even though the bulls fought back, leaving behind some hopeful candle patterns that a relief rally may soon begin, the market downtrend and substantial resistance levels above provide concern that the overall downtrend may not be over just yet.

Asian markets chopped in an uncertain session with rising pandemic concerns. European markets have found a bit more bullishness this morning, getting a modest relief rally after yesterday’s rout. US Futures at the time of writing this report suggest a mixed but relatively flat open with tech doing its best to lead a relief. Expect price volatility to remain high with the market sensitive to the news cycle.

Economic Calendar

Earnings Calendar

On the Tuesday earnings calendar, we have 12 companies reporting quarterly results. Notable reports include NKE, AZO, KBH, SCS, & SFIX.

News and Technicals’

Worries about political infighting over a high court appointment, a possible government shutdown, a delayed or no 2nd stimulus package, an upcoming election, and rising coronavirus concerns had the bears working hard yesterday. The first 4-day string of selling since February has created technical damage and damaged to trader confidence in the path ahead. According to the T2122 indicator, the indexes are in a short-term oversold condition suggesting a relief rally may begin soon but having broken down below the 50-day averages and price support, the resistance above could stop any bullish attempt. Should we see a failure at or near the 5-day average, we can’t rule out the possibility of a 200-day average test in the weeks ahead. We should also consider the chance that we have seen the highs for the year, and the market could settle into a volatile sideways consolidation.

Technically speaking, the rally off of yesterday lows left behind hopeful candle patterns that a relief rally could soon begin. However, with the DIA, SPY, QQQ all below substantial resistance levels, a one day bounce while in a downtrend is nowhere near an all-clear signal to buy the dip. With so much uncertainty ahead, expect extreme sensitivity to the news cycle, overnight reversals, intraday head-fakes, and whipsaws, making price action very challenging to navigate. The silver lining in all of this is that stocks are on sale, and eventually, there will be some bargains when this is over.

A political battle royal has begun for the appointment of a Supreme Court Justice, and the aftershocks are creating market havoc this morning with the US Futures pointing to an ugly gap down open. The morning selling will make the lower low to confirm the downtrend in the DIA, SPY & QQQ. There is also significant pressure in the financial sector after leaked documents that show red-flagged transactions that amount to more than $2 trillion. Today could be a very painful day for the buy the dip buyers that loaded up on trades last week. Be careful as fear and possible margin calls could accelerate the selloff.

Asian markets closed mixed but mostly lower after the report that HSBC moved most of the suspicious money flagged in the leaked report. European markets are decidedly bearish this morning, with indexes trading more than 3% lower this morning. US Futures also point to a painful open that will create substantial damage to trader confidence and technical damage in the index charts. Prepare for a wild ride!

Economic Calendar

Earnings Calendar

On the Monday earnings calendar, we have 18 companies stepping up to report quarterly results, but there are not any particularly notable.

News & Technicals’

It seems the appointment of a new Supreme court justice will become a distraction political battle royal and possibly pulling attention away from completing an additional stimulus package. It’s such a hot topic that candidates received a record 90 million in campaign contributions as it fired up both political bases. Nancy Pelosi has gone as far as to threaten impeachment proceedings in an attempt to block a Trump appointment. This morning’s futures market sums up the intensity of the distraction, with Dow currently expecting a gap down of more than 500 points. According to reports, the President approved the Tiktok deal, and China has responded, saying they will blacklist some US tech firms raising uncertainty for foreign tech business. Leaked US government documents show that several big banks may have moved elicit funds. Germany’s largest bank, Deutsche Bank, tops the list and appears to have facilitated the more of the $2 trillion in suspicious transactions flagged by the US Government. JP Morgan is second on the list. Both banks indicate lower this morning, putting additional pressure on the markets.

The question of whether the 50-day morning average of the Dow holding as price support has been answered this morning with a punishing gap down at the open. The lower low not confirms the downtrend of the DIA, SPY, and QQQ and creates substantial technical damage in the charts. I would not be at all surprised to hear about margin calls that have the potential to accelerate the selling. Today may prove to be one of those awful market days that test a trader’s tolerance to risk. Buckle up for a wild ride.

There was considerable price movement yesterday as the bulls and bears battled for control with MSFT and AAPL leading the QQQ its first close below its 50-day average since April. With the weekend approaching, a light day of earnings and economic news, as well as September options expiration, expect price volatility to continue. Plan your risk carefully as you consider the uncertainty of the weekend ahead.

Asian markets seesawed overnight but ultimately find the inspiration to rally, closing green across the board. With a significant spike in coronavirus and new shutdown measures taking place, European markets trade cautiously mixed but mostly lower this morning. US Futures traders flat to mostly lower overnight, but as the morning pump begins, they have rallied off overnight lows with the tech sector leading the way.

Economic Calendar

Earnings Calendar

On the Friday earnings calendar, we have a very light day with just one company expected to report today. That stock is TC and not at all notable unless you happen to one the sub-$1.00 equity.

News & Technicals’

With MSFT and AAPL under selling pressure, the indexes struggled yesterday with punishing intra-day whipsaws that kept traders on edge. The QQQ attempted to recover its 50-day moving average but ended the day closing below this psychological support. With US Futures mixed this morning, it’s understandable that there may be a little apprehension as we slide into the uncertainty of the weekend. Today is the last day trading for September options, so as traders unwind positions would may see and an extra dose of price volatility. Should the bears find the inspiration to rally, keep the resistance above with the downtrend created by this week’s lower high. Head fakes and intra-day are pretty common on options expiration day, and with the VIX still hovering above a 26 handle, traders must prepare for anything.

With just one small-cap stock reporting and a light day on the economic calendar, there won’t be much to react to except election news and political spin. I would not be at all surprised to see a choppy consolidation day. I wish you all a profitable Friday and a Fantastic Weekend!