Fed chairman Jerome Powell will be front and center as he makes

his rounds testifying on Capitol Hill.

Most expect him to defend the Fed’s independence from the administration

and of course many are hoping he will clarify the possibility of a rate cut. With such a strong Job number last week

expectation of a 50 basis point cut has dropped significantly. Also, remember we could learn a bit more about

the Fed’s thinking Wednesday afternoon with the release of last meetings

minutes.

Asian markets closed mixed, but mostly lower overnight and

European markets are currently seeing red across the board this morning. US futures are under some pressure this morning

suggesting a lower open though recovering slightly from overnight lows. Of course, anything that might clarify a rate

decision could move the market short of that I expect choppy price action to

continue as we wait for the kickoff of 3rd quarter earnings season.

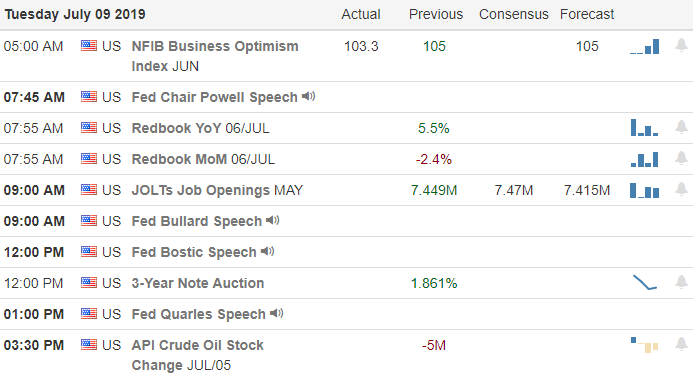

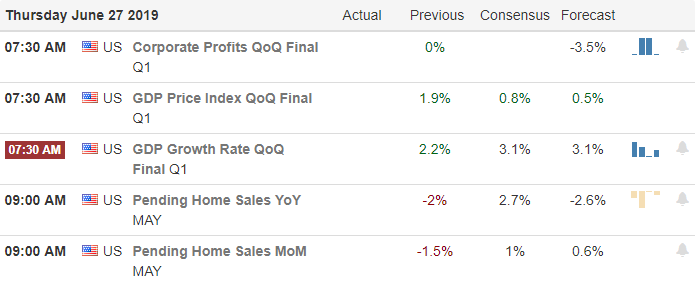

On the Calendar

We have just over 20 companies reporting on Tuesday’s Economic

Calendar. Among the notable reports are

AYI, JEF & SMPL.

Action Plan

Yesterday proved to be about as expected with the market

taking a little break with choppy consolidation price action. Today Powell will begin a 3-day round of testimony

in Congress where he is likely to defend the Fed’s independence from

administrative meddling. All eye are on

the Fed these days with the hope of a pending rate cut. There seems to be a revolving door on the

news agencies with talking heads both for and against a cut. Even Cramer chimed in on the subject to say he

is not sure there will be a cut. Perhaps

we will learn more from the testimony and the release of the FOMC minutes Wednesday

afternoon.

Futures are slightly under pressure this morning as tech’s

slide south amid some downgrades. However,

current trends remain bullish even though there are reasons to have a little

concern with price patterns in the QQQ and IWM.

I continue to expect mostly choppy price action that holds support

levels as we wait for clarification on rate cuts and the kick off to earnings

season.

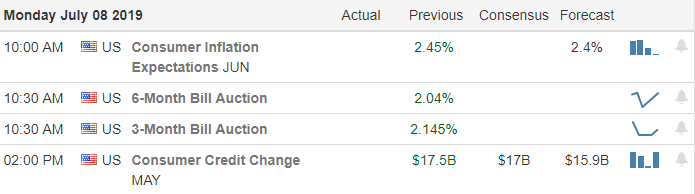

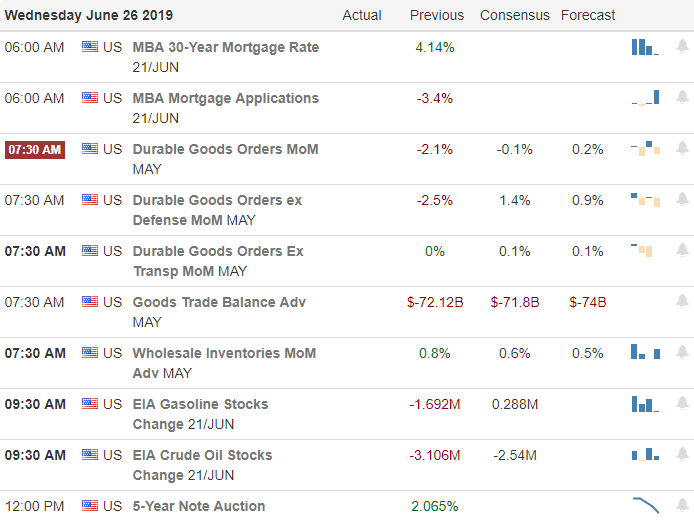

The market is showing a face of disappointment this morning as it would appear to favor an accommodating FOMC rather than strong jobs growth. Asian markets closed lower across the board overnight in reaction the better than expected US Jobs growth. European markets are currently mixed but mostly lower as Deutsche Bank announces huge job losses as it restructures the business.

US futures point to a modestly lower open this morning recovering

significantly from overnight lows as we approach the days open. Light economic and earnings calendars will

provide very little for the market to react to this morning. Considering the kick off the earnings season

is just one week away, and the current rally appears a bit stretched, a little

consolidating price action might be in order.

I would also not rule out a test of the overnight futures low.

On the Calendar

We begin the new trading week with a light day on the Earnings

Calendar that includes only six reports. Of those reporting, none are notable and likely

to move the market.

Action Plan

Markets appear a little disappointed this morning that the

US economy is strong, jobs growth is better than expected and the chance that an

FOMC rate cut has diminished. Although the

strong jobs number initially triggered some selling on Friday, the Bulls still

found the energy to fight back closing just below record highs. The question is, can the Bulls do it again today

or will the Bears show some teeth?

With earnings season set to begin in next week, it could be rather

quiet and choppy, consolidating the rally as we wait for the big banks to start

the festivities. Speaking of big banks,

Deutsche Bank (DB) announced a major restructuring Sunday that will cut between

18 to 20 thousand jobs in an effort to return to profitability. Shares are looking only slightly lower this

morning. Strong trends remain in place

for the DIA, SPY, and QQQ and though the rally may be a bit extended don’t

expect the Bulls to give up easily.

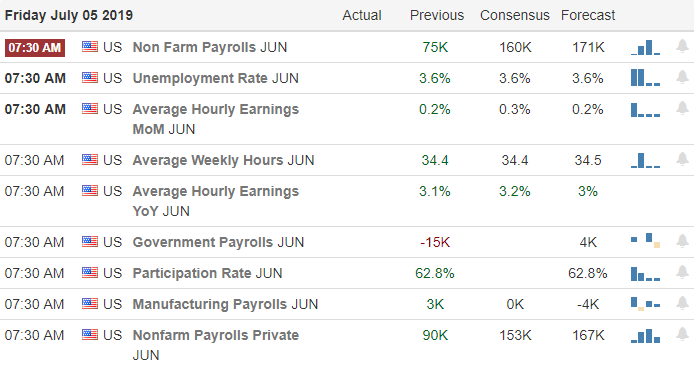

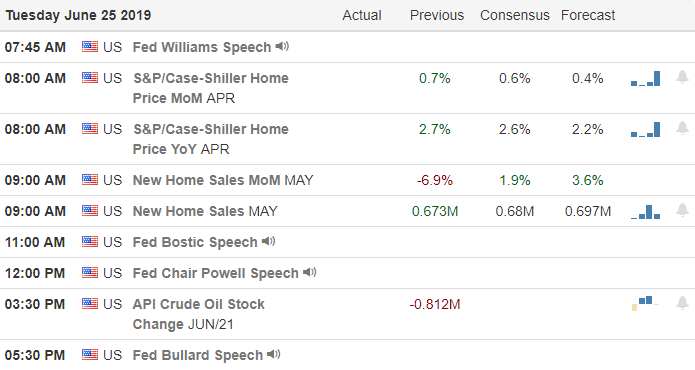

At 8:30 AM Eastern we will get a very importing reading of

the condition on the strength of our economy and the number of jobs it did or

didn’t create. If the Employment Situation

number comes in weak it could provide the FOMC hammer to drive down interest

rates in July. A strong number could

make an interest rate cut difficult if the US Economy continues to show

resiliency in the face of a slowing global economy. One thing for sure is that the number is likely

to receive a significant price action response upon its release and may well

set the direction to today’s market.

Asian markets were a bit subdued last night closing mixed up

mostly higher. European markets are currently lower across the

board and US Futures point to a modestly lower open ahead of the jobs number. The trends are bullish with DIA, SPY and QQQ

breaking out to new all-time highs on Wednesday. The task ahead for the bulls is now to prove

they defend this new price level with a worrisome earnings season beginning in 10-days.

On the Calendar

On the Friday Earnings Calendar we have 16 companies

stepping up to report quarterly results.

None of the reports today are particularly notable unless you happen to

own them.

Limited Seats Available

Action Plan

The key focus this morning will be the Employment Situation number

at 8:30 AM Eastern. If the number comes

in weak it would seemingly provide the FOMC with the cover needed to lower the interest

rate next month. However, the consensus

estimate is suggesting that the number could come in strong with nearly double

the jobs creation from last month. No

matter how the number comes in it’s how the market reacts to the data that important.

At the close on Wednesday the bulls were in full control setting

new all-time high records in the DIA, SPY and QQQ in a show of force rather

remarkable considering the holiday-shortened trading day. Now that we have the breakout it will be

important for the bulls to hold these new levels as price support. That may be a difficult task with so many companies

warning they will miss analysts estimates when earnings season kicks off in

about 10-days.

After some light jousting with bears during yesterdays

morning session the bulls reasserted themselves once again closing the SP-500

at new record highs. With the US/China

trade uncertainty, rising tensions with Iran and a slew of company warnings

about a difficult earnings season ahead the bulls continue to find the energy to

push higher. The current trends are

bullish and as of now the bears appear to have no teeth.

Asian markets closed lower across the board as trade worries

continue to weigh heavily. European markets

are higher the board with the nomination of Christine Lagard as the new head of

the European Central Bank. US Futures

are currently pointing to a modest gap up open ahead of busy Economic Calendar

and an early market close at 1:00 PM Eastern.

After the morning rush volume could drop significantly as trader’s head out

early to celebrate the holiday.

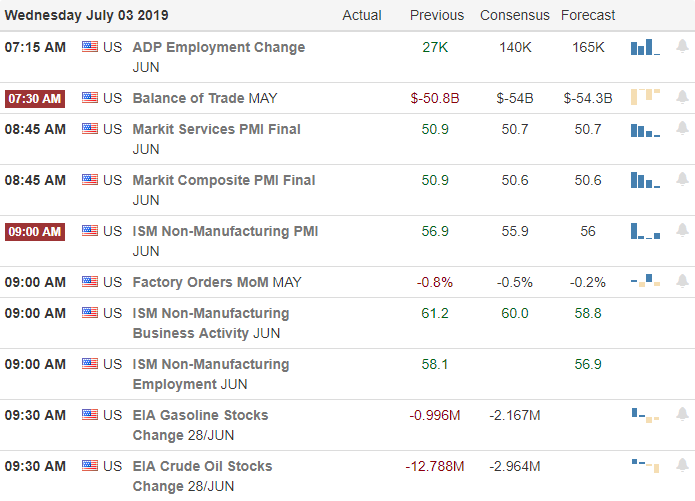

On the Calendar

On the Wednesday Earnings Calendar we have just two

companies ISCA & OMN reporting today.

They are not notable reports and unlikely to move the market.

Action Plan

We have a busy Economic Calendar this morning with ADP,

International Trade, Jobless Claims, Factory Orders, ISM Non-Mfg & the EIA

Petroleum Status. Although we could experience

a morning flurry of activity with the markets closing at 1:00 PM Eastern, the volume

could decline quickly creating anemic price action.

Yesterday’s price action saw choppy slightly bearish price action

during the morning session but the Bulls refused to let that stand to stage an

impressive comeback particularly in SP-500 that closed at another record

high. Trends are still bullish although they

appear to be a bit stretched however that is not stopping the bulls relentless

push higher as the futures point to yet another gap up open this morning. I wish you all a safe and Happy 4th

of July!

The concern I expressed regarding yesterday huge gap seemed

to be shared by the majority of the market producing a pop and drop pattern on

the day. Although the SP-500 inked a new

record high the price action left behind more question than answers about the

path ahead. Asian markets closed mixed

overnight as Australia’s Central Bank cuts interest rates. European markets are flat to ever so slightly

bullish this morning as the world looks for more details and clarity on

US/China negotiations.

US Futures are currently flat to slightly lower this morning

with very little to react to on both the Earnings and Economic calendars. Baring a market-moving news report don’t be

surprised to light and choppy price action today with rapidly declining volume

as traders head out to celebrate the 4th of July. There is a chance that condition lasts for

the rest of the week. Keep in mind the

market closes at 1:00 PM Eastern on Wednesday.

On the Calendar

On the Tuesday Earnings Calendar we have 14 companies

reporting quarterly results. Among the

notable reports AYI, JEF & SMPL.

Action Plan

It would seem my question about what had changed to create yesterdays

huge gap up was shared by most of the market after printing pop and drop

patterns on all major indexes. Although

were was a late day rally to lift the indexes off the day’s lows yesterdays price

action leaves more questions than answers to the path ahead. Further complicating the issue is the growing

Iranian tensions, and the will they or won’t they question regarding interest

rate cuts.

With little for the market to respond to today on the Economic

Calendar and Earnings Calendar as well as the coming holiday futures are suggesting

a flat to modestly lower open this morning.

As I suspect many traders have already headed out to take advantage of some

holiday vacation time don’t be surprised to see some very light choppy price

action today will low volume. It will

not be a surprise if this problem persists the rest of the trading week.

The bulls are in beast mode this morning after the US and

China agreed to a cease-fire and agreed to resume negotiations. Looking at the futures this morning one might

assume the tariff war is over but as of now there is still no clear path to a

deal and current tariffs will remain in place.

The good news is there was no escalation in the rift between the countries.

Asian markets closed mixed but mostly higher on the G20 developments and European markets are currently sharply higher this morning. US Futures currently indicate a soaring gap up that will likely set new record highs and punish any traders caught short. Keep in mind with the market closing early Wednesday for the holiday volume will likely begin to decline sharply over the next 2-days as traders head out to celebrate. It is entirely possible the biggest price move of the day will be the gap so be careful not to chase.

On the Calendar

On Monday’s Earnings Calendar we have 14 companies reporting

results but none are particularly notable.

Action Plan

Tariffs remain in place but the US and China have agreed to

come back to the negotiations table. The

President also agreed to ease restrictions American companies from selling products

to Huawei. Chetan Ahya, global head of

economics describes the meeting results as “an uncertain pause”, with no clear

path to a deal. However, the bulls are

celebrating the meeting results of the meeting this morning and the futures are

flying high.

I would expect new record highs this morning and anyone

caught short will likely be squeezed out this morning. Unfortunately the biggest price move of the day

may be the gap so be very careful not to get caught up in the excitement and

chase into the open. Let’s keep in mind

that the market will close early on Wednesday in observation of the 4th

of July holiday. That means volume is likely

to begin dropping as traders head out early to celebrate.

With the big meeting between the US and China presidents on Saturday

it would seem that anything is possible by Monday morning. Will they or won’t they? The hope of a deal seems to remain remarkable

high as the bulls once again show strength in the morning futures. Asian markets closed lower across the board

overnight but European markets are all cautiously higher ahead of the G20.

Even the beleaguered IWM managed to join the DIA, SPY and

QQQ yesterday by closing just above its 50-day average. Although the futures suggest a modest gap up

this morning we must be very careful and thoughtful of the potential risk of

this weekend. I don’t know about anyone

else but I will avoid adding additional risk ahead of this weekend and will likely

reduce my current holdings to protect my capital from the unknown.

On the Calendar

On the Friday Earnings calendar we only have 13 companies

reporting their results. Among the notable

are STZ & KHC.

Action Plan

The bulls remain very tenacious this morning even after

learning that next quarter earnings are expected to flat. One must wonder how we can remain near

all-time highs without earnings growth. Possible

rate cuts will certainly help and of course a trade deal with China would be a

game changer but those are still some big unknowns. It seems a lot would have to go exactly right

which makes me wonder if we’re coming close to pricing the market to

perfection. Only time will tell.

Technically speaking the current trend is up and the bulls are

in control with the Futures pointing to a bullish open. Remember the potential market volatility in

reaction to the G20 meeting results after the president meets to discuss trade

relations with China. Plan your risk carefully

heading into the weekend keeping in mind the holiday week that follows. Have a wonderful weekend everyone!

Let’s all hope cooler heads prevail or the 4th of

July shortened trading week could create some wild fireworks in price action volatility. Futures markets have currently recovered since

the report and now suggest a relatively flat open. However, it would be wise to consider the

risk of this coming weekend and carefully plan how you can protect your capital

given the price volatility that may result.

Early this morning the Wall Street Journal report seems to

have upset the apple cart quickly reversing futures markets that had held

positive all night. If the report is

correct the list of demands that Chinese President XI Jinping will present to

President Trump at the G20 seems only to inflame trade war tensions and diminish

the odds of a deal.

On the Calendar

On the Earnings Calendar we have nearly 40 companies reporting

results today. Notable earnings include CAN,

CAG, JEF, MKC, NKE & WBA.

Action Plan

US Futures held positive most the night until but quickly

reversed negative after the Wall Street Journal reported that Chinese President

Xi Jinping will present a list of demands to resolve the trade war to President

Trump at the G20 meeting. If the report

is correct it would seem the odds of a deal at the G20 decline to zero. Let’s us all hope it’s not true or we are likely

to face another round of tariff increases.

Other troubling news for the Dow Futures is the BA has

reported it found another software problem in their grounded aircraft. BA is indicated to gap more than 4% lower at the

open today. As you plan your risk for

the weekend ahead consider the volatility that could result from the G20 developments

and the 4th of July holiday the following week. It would seem to be a near impossibility to hold

on to a trading edge heading into this weekend.

The tenacious bulls pushed the market to new record highs with

a glass half full attitude that the FOMC would give them a bigger rate cut than

it now seems the Fed is not quite ready to give. Then they grabbed on to a late night headline

from Secretary Munchin that the US/China trade deal is 90% complete reversing afternoons

yesterday bearishness. Finish reading

the story and what Munchin said he hoped for a completed deal by years

end.

If he’s right could mean another six months of negotiations and

market uncertainty. It would seem the

bulls once again see the glass half full.

A trade deal with China would be a game changer but six more months of

news cycle spin and possible tweet storms means the road ahead could be full of

potholes and very challenging to navigate.

The news-driven gap this morning could create a short squeeze but it also

has the potential of a pop and drop pattern.

Stay focused and disciplined to your rules.

On the Calendar

On the hump day Earnings Calendar we have 18 companies

reporting quarterly results today.

Notable reports today include KBH, BB, GIS & PAYX.

Action Plan

After learning that the FOMC plan to move much more

cautiously than the somewhat exuberant market has expected the short-term price

action turned decidedly bearish yesterday afternoon. No doubt many likely entered short positions yesterday

expecting at a modest pullback at a minimum.

However, during the night we get a statement from Treasury Secretary

Mnuchin that the trade deal is 90% complete and markets around the world reacted

bullishly.

Had they gone beyond the headline they would have also seen

the statement that he hoped a completed deal by the end of the year. If it’s going to take another 6-months to work

out the final 10%, I think it’s safe to say the devil is in the details and we may

still have a long bumpy road ahead. US

Futures are pointing to a gap up of around 100 Dow points. Truly a

glass half full kind of market. Those

caught short will be squeezed hard this morning and could propel the indexes

higher. On the other hand the morning

pop could set up a pop and drop pattern so be patient to see if buyers will

support the gap.

Taking a break ahead of more Fed speak as Jerome Powell speaks with the New York Times at 1:00 PM Eastern today. Some are speculating that he may try to reduce the current market exuberance of expected rate cuts. Certainly this adds some uncertainty to the day as if we didn’t already have enough of that with growing Iranian tensions and a pending G20 with US/China trade hanging in the balance.

Asian markets closed lower across the board during the night

and European markets are modestly lower in reaction to the new US sanctions on

Iran. US Futures are also modestly lower

ahead of a busy economic calendar day and a few noteworthy earnings reports. There is a lot to consider as we plan today amid

the uncertainties but as for now the bulls are firmly in control and I would

not expect them to give up easily.

On the Calendar

On the Tuesday Earnings Calendar we have 21 companies

stepping up to report. Among the notable

reports are MU, FDX, FDS & LEN.

Action Plan

With more Fed speak today and the pending G20 meeting it

would seem the market is taking a wait and see approach. Some are concerned that Jerome Powell may

temper the market’s exuberance over possible rate reductions in his interview

with the New York Times at 1:00 PM Eastern today. Of course what he will say and how the market

will react only time will tell but should be a consideration as trader plan how

to approach the market today.

Technically speaking a little resting consolidation after

such a big move this month seems logical even without pending uncertainty. The bulls are in control and unless the Fed

changes the market’s perception I don’t see that changing. While a pullback may be in the card for the

near future, a hold above the 50-day averages builds a bullish case.