Last week’s financial failures quickly highlighted how fragile our banking system has become with a slowing economy and a quantitative tightening cycle to battle inflation. However, as federal regulators work to backstop the SVB failure, worries grow about just how far the contagion has already spread. Add in a massive week of market-moving economic data and the stage for another week of wild price volatility as investors face a very uncertain path forward. Expect face-ripping whipsaws of significant overnight reversals as the market comes to grips with inflation, a possible recession, and a slowing economy.

Asian markets trade mixed as Hong Kong surges 1.95% and Japan falls 1.11% as uncertainty grips the financial system. On the other hand, European markets trade decidedly bearish this morning as banks sell off 5.7% as the bank failures ripple through the monetary system. U.S. futures went on a rollercoaster ride at night after regulators announced a backstop plan for SVB as investors worry about the potential contagion spreading to other banks. Prepare for another wild day of price action.

Economic Calendar

Earnings Calendar

With first-quarter earnings winding down and the stock buyback blackout period about to begin, so will all the hyper-earnings emotion until we begin the 2nd quarter silly season. Notable reports for Monday include GTLB & KOD.

News & Technicals’

Regulators approved plans Sunday to backstop depositors and financial institutions associated with Silicon Valley Bank. Officials will unwind both SVB and Signature Bank, ensuring that depositors can access their funds on Monday. The Federal Reserve stepped in with a separate facility that will provide loans for up to one year for institutions affected by bank failures. “Today, we are taking decisive actions to protect the U.S. economy by strengthening public confidence in our banking system,” leading regulators said in a joint statement.

Billionaire investor Bill Ackman said the U.S. government’s intervention to protect depositors after the implosion of Silicon Valley Bank is “not a bailout” and helps restore confidence in the banking system. In a tweet, Pershing Square CEO said SVB’s fallout on Monday noted the government did the “right thing.” But not all Wall Street analysts are convinced the regulator’s action will shore up confidence in the U.S. banking system and limit the fallout. “I don’t think that you can understate the danger that the American banking system is in,” veteran bank analyst Dick Bove told CNBC’s “Squawk Box Asia” on Monday.

“In light of the stress in the banking system, we no longer expect the FOMC to deliver a rate hike at its next meeting on March 22,” Goldman economist Jan Hatzius said in a Sunday note. The firm expects the latest measures to “provide substantial liquidity to banks facing deposit outflows” and boost confidence among depositors.

The failures of Silvergate and SVB banks brought out the bears in a big way last week, bringing to light just how fragile our banking system has become in the slowing economy. Suddenly the Fed is back into bailout mode as the market worries just how far the banking contagion might spread. Nevertheless, the futures market rallied sharply during evening trading after the decision to announce the SVC backstop plans to regulators. However, the bailout enthusiasm seems to have faded substantially this morning, and traders should plan for considerable price volatility as the market comes to grips with the uncertainty of what comes next. With a massive week of market-moving economic data, prepare for just about anything in the week ahead.

Markets started out basically flat on Friday (down 0.15% on the SPY, down 0.18% in the DIA, and up 0.11% in the QQQ). All three major indices then meandered sideways in the morning, with an up wave reaching the highs of the day at about 11:30 am. At that point, the SPY, DIA, and QQQ all sold off strongly until 2 pm. The rest of the day was spent in a relief bounce and then heading back down to the lows of the day at 3:50 pm before ending on a modest 10-minute bounce. This action gave us larger-bodied, black candles with wicks on both ends. The QQQ (which has been the leader for some time) took out its most recent swing-low (completing a Dreaded-h pattern) as well as breaking down through and closing just below both its converging 50sma (rising) and 200sma (falling). At the same time, the SPY closed at a potential support level.

On the day, all 10 sectors were in the red with Financial Services (-2.75%) once again leading the way lower while Communications Services (-0.32%) held up best. At the same time, the SPY lost 1.44%, the DIA lost 1.04%, and QQQ lost 1.40%. The VXX spiked more than 11.4% to 52.93 and T2122 dropped even more deeply into the oversold territory at 2.08. 10-year bond yields plummeted to 3.704% (a massive 0.219% move for bond yields) and Oil (WTI) climbed 1.27% to $76.68 per barrel. So, Friday saw the bears react to February Payrolls by anticipating that the Fed will not like stronger-than-expected jobs growth and will hike rates more than traders had already baked in. This all happened on huge volume (at least in terms of recent months), the highest in the last four months…which begs the question as to whether this was capitulation?

In economic news, February Nonfarm Payrolls came in above expectation at +311k (compared to a forecast of +205k but well below the blowout January reading of +504k). At the same time, Feb. Private Nonfarm Payrolls also beat expectations at +265k (versus the forecast of +210k and again, below the blowout January number of +386k). Meanwhile, the February Participation Rate crept up to 62.5% (up from 62.4% in January). However, the February Unemployment Rate unexpectedly rose to 3.6% (above the forecasted 3.4% and the January value of 3.4%). On top of all this, the February Average Hourly Earnings (year-on-year) increased less than expected at +4.6% (as compared to the forecast of +4.7% but still well above the January reading of +4.4%). So, overall, the bulls could hang their hat on the increase in payrolls showing good growth while also decreasing in pace as the Fed wants at the same time the wage growth is easing slightly. However, the bears could see still much stronger job growth than anticipated and wage growth still far above the Fed’s target rate. Finally, at 2 pm, the February Federal Budget Balance showed a larger deficit than was expected at -$262.0 billion (versus a forecast of -$256.0 billion).

In stock news, after widespread rumors, FRC and WAL both calmed markets Friday saying their liquidity and deposits remain strong and neither expects spill-over effects from the SIVB implosion. Elsewhere, MRNA said Friday that it is planning to hire 2,000 employees by the end of 2023 as well as setting up new West Coast offices as it plans to scale up RNA vaccine research. (For comparison, MRNA had 3,900 employees at the end of 2022.) Meanwhile, Reuters reported that GM is exploring the use of ChatGPT in a collaboration with MSFT. In M&A news, a majority of RBA shareholders have voted in favor of the company buying IAA for about $7 billion (cash and stock). At the same time, AAPL shareholders rejected two proposals from politically conservative groups related to diversity and business done with China. In other news, seeking some good press (and/or avoiding negative) NSF agreed to give members of two unions up to seven paid sick days per year. In addition, F announced they will resume the production of F-150 Lightning trucks today after solving battery cell manufacturing defects. Finally, a rash of companies (especially silicon valley startups) are being forced to address how much of their assets are now tied up (and potentially lost) due to the failure of SIVB. Among these are RBLX (who said 5% of its cash is tied up at SIVB) and ROKU (who said 26% of its cash is tied up at that bank). It is worth noting that the FDIC only insures $250k in deposits. However, capitalism never misses an opportunity as, on Saturday, several hedge funds began offering to buy the deposits of companies with stranded capital at a price of 60 cents on the dollar or less.

In stock legal and regulatory news, on Friday, SIVB was halted before the opening bell by the SEC and the bank itself was shut down by State of CA regulators who turned it over to the FDIC after the company failed to raise enough capital in its last-ditch stock offering Thursday. Elsewhere, Reuters reported an exclusive on Friday saying that the OCC (Options Clearing Corporation, the largest options clearing house) and the FIA (Futures Industry Assn.) have begun investigating the risk of 0DTE (Zero Days to Expiration) options contracts in a project that began on March 1. This comes after analysts at JPM publicly said they fear 0DTE options could supercharge volatility, turning a 5% intraday loss into a 25% or greater rout. (0DTE volume on the S&P500 have tripled since January.) The leaning seems to be toward continuing to allow 0DTE options, but industry members are nervous (or perhaps are not making as much or in as much control of that new market yet). Meanwhile, after the close Friday, the FAA approved BA restarting the deliveries of 787 Dreamliners following the company resubmitting previous erroneous data analysis.

In bank fear news, the shocking speed behind the collapse of SIVB (the 16th largest US bank) has made many think back on how quickly Lehman Brothers and Bear Sterns went under. Speaking of speed, on Sunday, the FDIC completed the auction for buyers of SIVB assets after being unable to find a bank to acquire the entirety of SIVB. Sunday morning, Treas. Sec. Yellen told CBS reporters that the government will not bail out SIVB, but is already working with its depositors on ways to secure their uninsured funds beyond what the FDIC insures. Later that same day, Sec. Yellen ordered the FDIC to allow SIVB depositors to have access to all their money Monday. (So, the FDIC has been ordered to bail out the depositors, if not the bank, by increasing the amount of deposits covered.) Meanwhile, CNN reports that other US banks are now sitting on more than $620 billion in unrealized losses. Since the banking system is all built on confidence, any fear of bank runs could cause a vicious cycle of fear causing runs and runs causing more fear. By Sunday night, the Treasury Dept., Fed, and FDIC made a joint decision to close SBNY due to this systemic risk. However, Reuters reported that several sources told them there will be some major government action (involving the Fed, Treasury Dept., and FDIC) to shore up the system. Most likely, this will be announced before the open today.

Overnight, Asian markets were mixed. Hong Kong (+1.95%), Shanghai (+1.20%), and South Korea (+0.67%) led the gainers. Meanwhile, Thailand (-1.66%), India (-1.49%), and Singapore (-1.42%) paced the losers. In Europe, with the lone exception of Russia (+0.26%), the regions are in the red across the board at midday. The FTSE (-1.69%), DAX (-2.10%), and CAC (-1.92%) are leading the region lower in early afternoon trade. As of 7:30 am, US Futures are pointing to a mixed but green open. The DIA implies a flat +0.05% open, the SPY is implying a +0.36% open, and the QQQ implies a +0.89% open at this hour. At the same time, 10-year bond yields are plummeting again (as traders seek safe havens) to 3.549% and Oil (WTI) is down 1.54% to $75.50/barrel in early trading.

There are no major economic news events scheduled for Monday. The major earnings reports scheduled for the day are limited to LU and ZIM before the opening bell. There are no reports scheduled for after the close.

In economic news later this week, on Tuesday, we get February CPI, API Weekly Crude Oil Stocks, and hear from Fed member Bowman. Then Wednesday, February PPI. Feb. Retail Sales, NY Empire State Mfg. Index, Jan. Business Inventories, Jan. Retail Inventories, and EIA Weekly Crude Oil Inventories are reported. On Thursday, we get Feb. Building Permits, Feb. Housing Starts, Feb. Export Price Index, Feb. Import Price Index, Weekly Initial Jobless Claims, and Philly Fed Mfg. Index. Finally, on Friday, Feb. Industrial Production, and Michigan Consumer Sentiment are reported.

In earnings later this week, on Tuesday, we hear from CAL, IHS, GES, LEN, and STNE. Then Wednesday, ARCO, CLMT, ADBE, FIVE, HSAI, YY, TPC, and ZTO report. On Thursday, we hear from ASO, DG, GIII, MOMO, JBL, BEKE, LE, SIG, TITN, WSM, and FDX. Finally, Friday, AQN and XPEV report.

So far this morning, ZIM reported beats on both the revenue and earnings lines. At the same time, LU missed on revenue and reported in-line with analyst expectations on the earnings line. Neither company has changed guidance as of this point.

In late-breaking news, HSBC bought the entirety of SIVB’s UK operations for the princely sum of $1.21 (1 pound sterling). So, UK customers of SIVB will continue life as normal while HSBC absorbs SIVB in that country. Elsewhere, GS has changed its call for the Fed next week. GS now expects no rate hike (pause), down from its earlier call of a quarter-percent hike this time around. Obviously, the reason for the change is an expectation the Fed will not want to change liquidity or make any more changes until the SIVB shock works its way out of the financial system. Traders have also shifted their bets with Fed Fund futures now showing a 66% probability of a quarter percent hike and a 34% of no hike at all.

With that background, it looks like futures are pulling back in the last 15-20 minutes. We are now looking at more of a flat (large-cap indices) to modestly up (QQQ) open to the day. Extention is not a problem in terms of the T-line (8ema). However, the T2122 indicator is very stretched. As I see it, SPY has no real support below til it reaches the 378-379 area. Meanwhile, the DIA has very, very modest support right here and then none until it reaches the 311 area. As for QQQ, I see no support until it reaches the 284 area. Expect volatility today. There will likely be unscheduled news and soothing words from the FDIC, Fed, Treasury Sec. Yellen, and maybe the President. However, it is hard to say whether the market will take those as a good thing or a reason to panic.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Well, that was a day. On Thursday stocks gapped modestly higher at the open (up 0.19% in the SPY, up 0.36% in the DIA, and up 0.14% in the QQQ). We even saw a little positive follow-through in all three major indices for the first half hour of the day. However, then the bears stepped in taking the whole market on a steady selloff that lasted until 3:25 pm. Only a very modest bounce in the last half hour kept all three indices from closing on their lows. This action gave us large, black-bodied, Bearish Engulfing candles in the SPY, DIA, and QQQ. All three also formed Doji Continuation (Doji Sandwich) patterns, suggesting more downside to come. The QQQ crossed back below its T-line (8ema) and the two large-cap indices both gave up the support level of the most recent swing low. SPY and DIA also crossed back below their 200sma.

On the day, all 10 sectors were in the red with Financial Services (-3.48%) leading the way lower (read “getting crushed”) and Consumer Defensive (-1.03%) and Utilities (-1.05%) holding up best. At the same time, the SPY lost 1.83%, the DIA lost 1.65%, and QQQ lost 1.76%. The VXX spiked more than 10% to 47.51 and T2122 dropped back deep into the oversold territory at 4.61. 10-year bond yields dropped to 3.905% and Oil (WTI) dropped 1.50% to $75.51 per barrel. So, Thursday was a very decisively bearish day with the market not seeming to wait on Friday’s February Payrolls data. This all happened on greater than average volume (the most volume we’ve seen in two weeks).

In economic news, the Weekly Initial Jobless Claims came in higher than expected at 211k (compared to a forecast of 195k and the prior week’s reading of 190k). However, the main economic news on the day was President Biden’s budget proposal. This was highlighted by a $3 trillion reduction in the federal deficit over 10 years. The President proposes paying for this reduction by quadrupling the tax on company stock buybacks (but this only raises it from 1% to 4%). He also proposed a “Billionaire Tax” on all households worth more than $100 million, which prohibits them from paying less than a minimum rate of 25%. In addition, he proposed raising the corporate tax rate to 28% (from the current 21%, but still well below the 35% rate in place before the 2017 corporate tax cuts). The other major plank of the proposal was the shoring up of Medicare by increasing the Medicare Tax on individuals making more than $400k/year from 3.8% to 5%. The White House claims this would ensure Medicare solvency through 2050. While there were many other provisions, the most notable was a 3.2% increase in Defense spending and an $800 million increase in border security funding (both Republican favorites). This budget proposal was simply a political move, pushing the things Biden ran on (and will likely run on again in 2024) while daring the GOP to put forth their own actual counter-proposal. However, the GOP is restricted by Senate Majority Leader McConnel’s stated desire to increase defense spending, the GOP having jeered the idea of cutting Social Security or Medicare at the State of the Union speech, and there not being nearly enough other spending to cut in order to actually achieve the GOP’s claim that it will pass a balanced budget and reduce the deficit without raising taxes. However, despite challenges on the GOP side, in truth, President Biden’s proposal was dead on arrival in the GOP-led House as proposed. So, the actual budget is very unlikely to look like what either side wants, particularly if the deficit is going to be addressed.

In stock news, Reuters reported mid-day that CHRW is in “advanced talks” to name former UPS COO Barber as its new CEO. Elsewhere, bank stocks were crushed on Thursday after the Wednesday night decision by SIVB to do a multi-billion-dollar equity offering and also to sell tens of billions of dollars worth of securities at a loss in order to shore up its balance sheet. (SIVB lost over 60% on the day while, in sympathy, USB lost 7.01%, BAC lost 6.2% WFC lost 6.18%, JPM lost 5.41%, and C lost 4.1%.) In other news, under pressure from GOP Attorneys General, MA, V, and AXP announced a decision to “pause” a plan to implement unique transaction codes for guns and ammunition in the way that other product category sales are differentiated. Meanwhile, BYDDY followed in the footsteps of TSLA by offering new discounts on certain models purchased by the end of March. At the same time, GM announced Thursday that it has offered buyouts to most salaried employees and expects to take a pre-tax charge of up to $1.5 billion to cover the costs. In better news, CAT announced that it is seeing strong construction equipment demand in North America. As a result, CAT CFO Bonfield said Thursday that he believes the US will avoid a recession. After the close, the AAL pilot’s union said it has set a strike authorization vote for April. Also after the close, Reuters reported that DIS CEO Iger said the mouse house will consider making content for other companies (platforms), similar to the HBO model.

In stock legal and regulatory news, the FTC announced it is exploring a probe of META and GOOGL (among a total of 8 social media firms) for deceptive advertising on their platforms. (The final vote on whether to go ahead with the investigation will happen next week.) As reported yesterday, CS has delayed the release of its annual report. We now know the late-night call from the SEC was about previous “revisions” CS had made to its consolidated cashflow reports for 2019 and 2020. Elsewhere, FINRA has fined broker Webull $3 million for failing to exercise due diligence before approving its customers to trade options as well as poor response to customer complaints. After hours, the FTC announced it had unanimously voted to take action to block ICE from acquiring mortgage data vendor BKI (in a deal for $13.1 billion). Meanwhile, US Senator Rubio has introduced legislation aimed at blocking the F deal with Chinese battery company CATL. (The bill would void tax credits for EVs using batteries from that plant. This bill is a layup for Rubio because the plant is not in his state, it targets a Chinese firm, and “green projects” are not something his party’s base supports.) Finally, the SEC is set to vote on March 15 on 3 new rules that will dictate how brokers, clearing houses, and other financial companies handle the risk of hacking, respond to customer data theft, and disclose cybersecurity events to them and the public. In a perhaps-related story, BLKB was fined $3 million by the SEC Thursday after the close for misleading disclosures related to a 2020 ransomware attack the company suffered.

After the close, ULTA and DOCU reported beats on both the revenue and earnings lines. Meanwhile, TKC and ORCL both missed on revenue while beating on earnings. On the other side, MTN beat on revenue while missing on earnings. Unfortunately, HVRRY, GPS, and QFIN missed on both the top and bottom lines. It is worth noting that ORCL, ULTA, and DOCU all raised their forward guidance. However, GPS and MTN both lowered forward guidance.

Overnight, Asian markets were deeply red across the board. Hong Kong (-3.04%), Australia (-2.28%), and Japan (-1.67%) led the way, but the “best” showing in the region was New Zealand (-0.84%). Meanwhile, at midday, Europe is following Asia lower with red across all exchanges. The FTSE (-1.68%), DAX (-1.20%), and CAC (-1.10%) lead the way on volume as usual but the entire region is well into red territory with the best early afternoon performance coming from Norway (-0.40%). As of 7:30 am, US Futures are pointing toward a mixed start to the day not far on either side of the flat line. The DIA implies a -0.22% open, the SPY is implying a -0.10% open, and the QQQ implies a +0.08% open at this hour. At the same time, 10-year bond yields plummeted to 3.825% and Oil (WTI) is down more than a percent to $74.95/barrel in early trading.

The major economic news events scheduled for Friday include February Avg. Hourly Earnings, Feb. Nonfarm Payrolls, Feb. Participation Rate, and Feb. Unemployment Rate (all at 8:30 am), and Feb. Federal Budget Balance (2 pm). The major earnings reports scheduled for the day include ERJ before the opening bell. There are no reports scheduled for after the close.

So far this morning, JKS and BKE have reported beats on both the revenue and earnings lines. Meanwhile, KT missed on both the top and bottom lines. (ERJ has not reported yet.)

In late-breaking news, SIVB is scrambling to avoid a “run on the bank” after many funds advised clients to pull their cash out of that bank. It looks like, after yesterday’s 60% drop, SIVB is poised to gap down another 45% this morning. Meanwhile, crypto got crushed Thursday following the collapse of SI. It looks like there is more follow-through on that move again this morning. Elsewhere, US-China economic tensions continue to increase as more countries got on board with President Biden’s export-to-China restrictions Thursday. For their side, all week Chinese officials have called out US policies as showing the US is nakedly trying to “hem in” China rather than compete economically. However, regardless of all other news, the US market tune is going to be called by February Payrolls data at 8:30 am. After last month’s massive and unexpected jobs creation and historic drop in unemployment, the market greatly fears another strong number will push the Fed into an unexpectedly large rate increase the week after next.

With that background, it looks like the market is recovering from a push lower overnight. As of this moment, all three major indices seem to be roughly flat and waiting for the Payroll data. The short-term trend remains bearish as the DIA and SPY will try to climb back above the 200sma that was given up yesterday and the QQQ retested the convergence of 50sma and 200sma overnight (which happens to coincide with the most recent QQQ swing low). Extention is starting to get a little large in terms of the T-line (8ema). However, the T2122 indicator shows the market deep into the oversold (reversal) territory. As I see it, SPY has some support right where it closed Thursday, but DIA still has a good way to fall before it finds a support level as of now. The QQQ has potential support at the most recent swing-low of 288.50-ish. Expect volatility today, particularly after 8:30 and then shortly after the open.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Disappointing economic data and continued hawkish comments from Powell kept the bears engaged Wednesday. Still, the bulls defended vital price support levels at the close, raising hope of a near-term relief rally while evidence of a pending recession grows. Today investors will deal with Jobless Claims and more Fed comments as we wait for the potentially market-moving Employment Situation report Friday before the bell. Big point moves and substantial intraday whipsaws remain likely, so plan your risk carefully.

While we slept, Asian markets traded mixed as China reported inflation growth of 1%, the slowest pace so far this year. This morning, European markets trade with modest declines across the board as investors grapple with higher interest rates and growing recession concerns. However, U.S. futures trade near the flat line this morning as we wait on Jobless claims while hoping for a relief rally inspired by the buying into the Wednesday close. Expect the challenging price action to continue as we wait for the Friday Employment Situation report.

The Netherlands has become embroiled in political tensions between the United States and China, with the former looking to ensure that Beijing does not use the most advanced chip technology. As a result, Dutch Foreign Trade Minister Liesje Schreinemacher said, “the existing export control framework for specific equipment used for the manufacture of semiconductors needs to be expanded in the interests of national and international security.” China has been working to bolster its domestic semiconductor industry, but it remains far behind the likes of Taiwan, South Korea, and the U.S. New semiconductor export controls have been imposed by the U.S. on China, and the eurozone nations will soon follow suit.

President Joe Biden this week called for higher taxes on wealthy Americans to extend Medicare funding as part of his 2024 budget. The plan would increase the net investment income tax to 5%, from 3.8%, for earnings of more than $400,000, including regular income, capital gains, and so-called pass-through business income. However, the plan is unlikely to pass in the Republican-controlled House of Representatives.

Solanezumab’s failure is a blow to efforts to treat Alzheimer’s in people in the very early stage of the disease and has not yet shown clinical symptoms. In addition, Solanezumab did not clear or halt the accumulation of brain plaque and did not slow cognitive decline in the treatment participants. Lilly is developing two other Alzheimer’s treatments in late-stage clinical trials.

Inflationary economic data and the continued hawkish comments from the Fed kept the bears engaged on Wednesday though the VIX showed little fear and key price supports held in the major indexes. However, the U.S. dollar remained strong, and the bond inversion worsened during the day, suggesting a recession that will likely be made worse by the Fed having to raise rates to combat inflation. Evidence is mounting that it’s much less a question of whether the market will decline but more of when the decline gains strength. That said, the current short-term oversold condition may trigger a little relief rally but don’t ignore the overhead resistance as the likely area where the bear could gather for the next attack.

Markets opened flat on Wednesday and then proceeded to undulate sideways the rest of the day. This left the large-cap indices just on either side of where they closed on Tuesday and the QQQ managed a small gain by rallying the last 30 minutes of the day. This action gave us indecisive, Spinning Top candles in all three major indices. The QQQ managed to cross back above its T-line (8ema). Meanwhile, the SPY is retesting its 50sma. All of this happened on just below-average volume.

On the day, six of the 10 sectors were in the green as Utilities (+0.80%) led the way higher and Energy (-0.58%) lagged behind the other sectors. At the same time, the SPY was up 0.16%, the DIA was down 0.12%, and QQQ was up 0.50%. The VXX fell 1.64% to 43.05 and T2122 rose but remains in the oversold territory at 14.29. 10-year bond yields climbed to 3.989% and Oil (WTI) dropped 1.38% to $76.51 per barrel. So, Wednesday was an indecisive or “wait and see” day where the market might be waiting on the February Payrolls data.

In economic news, the February ADP Nonfarm Employment Change saw a greater than expected increase at +242k jobs (compared to a forecast of +200k and the Jan. reading of +119k). Later the January Exports came in up to $257.50 billion (up from $249.00 billion) while the January Imports were also up at $325.80 billion (up from $316.20 billion). As a result, the January Trade Balance came in very slightly better than expected at a deficit of $68.30 billion (versus a forecast of a $68.90 billion deficit but also worse than the December reading of $67.20 billion deficit). A little later in the morning, the January JOLTS (Job Openings) came in higher than expected at 10.824 million (compared to the forecast of 10.500 million but down from the December value of 11.234 million openings). Then the EIA Weekly Crude Oil Inventories showed a drawdown of 1.694 million barrels (versus a forecast inventory build of 0.395 million barrels and much lower than the prior week’s 1.165-million-barrel build). On the Fed front, Chairman Powell testified again and was questioned (mostly political theatre for many Congressmen) for hours. Basically, he said nothing new. He reiterated if (and emphasized only if the totality of) data warrants it, the Fed might increase the pace of rate hikes. Again, the basic idea is that inflation is not falling as fast as the Fed would like. So, the terminal rate likely will be higher than the old 5.1% estimate, but he did not say how much higher. He also said many times that no decision has even been made even on the size of the rate hike to be announced on March 22.

In stock news, on Wednesday, PYPL instructed its real estate agents to sell its main office (headquarters) in Ireland according to the Irish Times. The company responded saying the move is a result of the remote work nature of the last three years. However, PYPL did lay off 2,000 Irish employees at the end of January. Later, Reuters reported that JPM is cutting ties with the Gemini cryptocurrency exchange. In other news, Reuters also reported that Japan Airlines has decided (but has not announced yet) that it will buy 20 of the 737 Max jets from BA. Elsewhere, CSX was the latest railroad to suffer an accident as one of their trains derailed in West Virginia, spilling diesel fuel into the New River. After the close, Reuters reported that UBER is exploring whether to sell its logistics unit (Uber Freight) or spin off and IPO the unit. (The unit was started when UBER acquired logistics firm Transplace in 2017.) In other news, Bloomberg reports that AAPL has reshuffled the management of its international businesses in order to put a bigger focus on India. Also after hours, SI announced it is winding down operations and will voluntarily liquidate. The stock plummeted in post-market trading.

In stock legal and regulatory news, the NHTSA opened a “special investigation” into a February fatal crash in CA involving a TSLA Model S where the so-called auto-pilot feature was suspected of being used. Meanwhile, the CEO of LUV told reporters that the airline is not counting on being able to deploy BA MAX 7 planes in 2023 as the plane still has not completed the FAA certification process. He went on to say LUV expects some of the BA-promised plane deliveries for 2023 will now slip into 2024 and regardless of the delivery date, it then takes six months from delivery until the plane is in use. Across the pond, MSFT told the UK it will license the “Call of Duty” video game franchise to SONY for 10 years as part of the company’s efforts to get UK approval for the purchase of ATVI. (The UK ruling is due in April.) After hours, the US International Trade Commission banned the import of video-streaming fitness devices made by PTON after a judge found those devices infringed on patents held by DISH. The Administration has 60 days to review the decision before it takes effect. However, Presidents rarely reverse such rulings.

In energy news, the Wall Street Journal reported that new intelligence suggests that the Nord Stream gas pipelines were attacked by a pro-Ukrainian group made up of Ukrainian and Russian individuals. As mentioned above, the EIA reported Wednesday that US oil inventories fell for the first time since December last week (10 straight weeks of build broken last week). The report also said refineries operated at 86% of capacity (about 4% below the long-term average for this time of year). Gasoline inventories fell by 1.134 million barrels after refineries cut gasoline production. However, distillate (diesel and heating oil) inventories rose 0.138 million barrels compared to an expected drawdown of 1.038 million barrels.

Overnight, Asian markets were mostly in the red. Japan (+0.63%) was the lone appreciable gainer in the region. However, India (-0.93%), Hong Kong (-0.63%), and South Korea (-0.53%) led the vast majority of the region lower. Meanwhile, in Europe, with the exceptions of Greece (+1.10%) and Denmark (+0.37%) the entire region is in the red. The FTSE (-0.55%), DAX (-0.37%), and CAC (-0.31%) are leading the region lower in early afternoon trade. As of 7:30 am, US Futures are pointing toward a down start to the day. The DIA implies a -0.08% open, the SPY is implying a -0.28% open, and the QQQ implies a -0.55% open at this hour. At the same time, 10-year bond yields are rising again to 3.997%, and Oil (WTI) is up fractionally to $76.75/barrel in early trading.

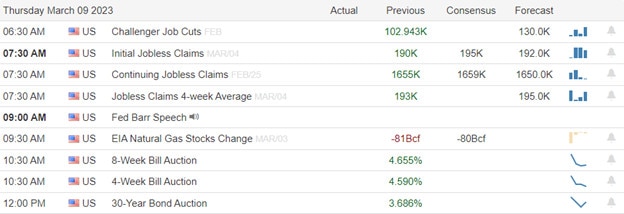

The major economic news events scheduled for Thursday are limited to Weekly Initial Jobless Claims (8:30 am). Major earnings reports scheduled for the day include BJ, GCO, GBTG, JD, WLY, and TTC before the opening bell. Then after the close, QFIN, DOCU, GPS, ORCL, ULTA, and MTN report.

In economic news later this week, on Friday, we get Feb. Avg. Hourly Earnings, Feb. Nonfarm Payrolls, Feb. Participation Rate, Feb. Unemployment Rate, and Feb. Federal Budget Balance. In earnings Friday, we hear from, ERJ.

So far this morning, BJ and SKHSY reported beats on both the revenue and earnings lines. Meanwhile, JD and GCO missed on revenue while beating on the earnings line. Unfortunately, HVRRY missed on both the top and bottom lines. It is worth noting that BJ raised its forward guidance while GCO lowered its forward guidance.

In late-breaking news, other than SI deciding to liquidate, the big news of the day will be the release of President Biden’s budget proposal. It is expected to contain a 25% minimum billionaire tax and a major increase in capital gains tax in order to achieve $3 trillion in deficit reduction over 10 years as well as bolstering Medicare and Medicaid to keep those programs solvent through 2050. Elsewhere, CS is delaying the release of its annual report “after receiving a call from the SEC late Wednesday night.” Details of the call were not released other than CS saying its management will need time to understand the SEC comments. Meanwhile, executives from NSF will face a grilling from the Senate this morning (10 am) over the railroad’s safety problems that led to a spate of recent derailings and specifically the East Palestine OH crash that caused a major chemical spill.

With that background, it looks like the market is just on the bearish side of undecided at least until the Weekly Jobless Claims are released. Meanwhile, the downtrend remains in place as well as all three major indices being below their T-line (8ema). SPY also continues its test of its 50sma. Extention is not a problem from the T-line, but the T2122 indicator remains in the oversold territory. As I see it, both SPY and DIA are still in a potential support area. QQQ may have marginal support here, but it is far less obvious than in the large-cap indices. All three have potentially stronger support levels a little ways below. Of course, all three also have resistance to work through overhead if the bulls plan to make a run.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

On Tuesday, all three major indices opened flat. Markets then treaded water until 10 am, when the bears sold us off very hard for 15 minutes as Fed Chair Powell’s remarks were absorbed. From that point (10:15 am), we saw a slow, meandering selloff the rest of the day, closing near the lows. This action gave us large, black-bodied candles which completed Evening Star-type signals in the SPY, DIA, and QQQ. The SPY and DIA both crossed back below their T-lines (8ema), while the QQQ is still right at that retest. SPY is also back down to retest its 50sma.

On the day, all 10 sectors were in the red with Basic Materials (-2.36%) led the way lower, while Industrials (-0.99%) and Technology (-1.03%) held up better than the other sectors. At the same time, the SPY was down 1.52%, the DIA was down 1.70%, and QQQ was down 1.23%. The VXX rose 2.40% to 43.87 (after a 1-for-4 split) and T2122 dropped back deep into the oversold territory at 9.59. 10-year bond yields climbed to 3.968% and Oil (WTI) plummeted 3.82% to $77.39 per barrel. So, Tuesday was a “wait and see” day that was then owned by the bears once Fed Chair Powell delivered his remarks and answered questions.

In economic news, Fed Chair Powell’s testimony before the Senate stole the show. In his remarks, Powell said US interest rates will probably have to rise further than the Fed previously thought in order to tame inflation. He also said that (if the totality of the data were to indicate faster tightening was warranted) “we would be prepared to increase the pace of rate hikes.” Further, he said that FOMC policy will need to stay restrictive “for some time” and ”the historical record cautions strongly against prematurely loosening policy.” This testimony flipped market bets, which had been strongly predicting a 25-basis-point hike in March but which now show 29.5% of bets are on a quarter-point hike and 70.5% are betting on a half-percent increase. Later, during questioning, Powell said a US debt default would have dire consequences for the economy and would likely cause long-lasting harm. Specifically, he said “Congress really needs to raise the debt ceiling. If we fail to do so, I think the consequences could be…extraordinarily adverse and could do long-lasting harm.” Other questions focused on each political party’s pet agenda items, but most were not noteworthy. Then, after the close, the API Weekly Crude Oil Stocks Report came in with a larger drawdown than expected. API reported the draw was 3.835 million barrels (compared to an expected drawdown of 0.308 million barrels and the prior week’s inventor build of 6.203 million barrels).

In stock news, MULN announced it will be unveiling both an electric cargo van and a class 3 low-cab truck this week at an Indianapolis truck show. Elsewhere, ON shares gained Tuesday after announcing a long-term deal to supply technology to BMW for the carmaker’s electric vehicles. Meanwhile, Reuters reported that BA is facing delivery problems for both 767 freighters and KC-46 tanker planes. The issue centers around center fuel tanks made by TGI, which had not completed cleaning and paint adhesion processes prior to delivering the components. The problem will significantly impact deliveries of 30-40 aircraft. At the same time, BX and TRI are selling $2 billion worth of their holdings in the London Stock Exchange to raise cash for other projects. In the Auto industry, TSLA CEO Musk announced Tuesday the company’s next-generation small car “would operate mostly autonomously.” (However, this is the same claim he has made for many years.) After hours, Reuters reported that WE is in talks with investors to restructure more than $3 billion in existing debt as well as looking to raise more cash from those investors. Finally, FDIC officials spent Tuesday at SI, looking for ways to save at least part of the bank.

In stock legal and regulatory news, META failed to get a lawsuit thrown out Tuesday and will need to proceed to trial. The suit alleges META stole confidential information from AI startup Neural Magic. As of last year’s filing, Neural Magic was seeking $766 million, but that number has likely skyrocketed as META recently rolled our new AI features. In possibly related news, the META AI model (LLaMa) leaked online Tuesday and was available for anyone to download the code. Elsewhere, a panel of US federal appellate judges questioned whether the SEC should have rejected the application by Grayscale to convert its GBTC into a Bitcoin spot-price ETF. (A ruling is not expected until the fall.) Meanwhile, as expected, the Dept. of Justice filed suit to stop the JBLU acquisition of SAVE on grounds it violates antitrust interests. At the same time, Reuters reports that AMD and NVDA are scrambling to determine whether they need to halt product sales to Chinese-listed Inspur Group after that company was added to the US export blacklist. (Inspur is the third-largest supplier of servers in the world as of Q3 and, therefore, would be a major customer for both NVDA and AMD.) It is unclear if INTC also supplies Inspur. Finally, Bloomberg reported that AMZN has defeated an attempt by employees to sue as a group as they try to recoup internet expenses they incurred while working from home during the pandemic.

After the close, CRWD, CRGY, and MBC all reported beats on both the revenue and earnings lines. Meanwhile, CASY missed on revenue while beating (significantly) on the earnings line. It is worth noting that CRWD raised its forward guidance.

Overnight, Asian markets leaned heavily to the downside. Hong Kong (-2.35%) and South Korea (-1.28%) were by far the largest losers and led the region south. Still, Japan (+0.48%) and India (+0.24%) managed to eke our gains. Meanwhile, in Europe, the bourses are mixed but the red outnumbers the green on the board at midday. The FTSE (-0.07%), DAX (+0.30%), and CAC (-0.08%) are typical of the region in early afternoon trade. As of 7:30 am, US Futures are pointing toward a start just on the green side of flat. The DIA implies a +0.08% open, the SPY is implying a +0.09% open, and the QQQ implies a +0.15% open at this hour. At the same time, 10-year bond yields are up to 3.972% and Oil (WTI) is off fractionally to $77.42/barrel in early trading.

The major economic news events scheduled for Wednesday include ADP February Nonfarm Employment Change (8:15 am), January Imports/Exports and January Trade Balance (both at 8:30 am), Fed Chair Powell testifies before Congress again and Jan. JOLTs Job Openings are reported (both at 10 am), EIA Crude Oil Inventories (10:30 am), WASDE Ag Report (noon), and Fed Beige Book (2pm). Major earnings reports scheduled for the day include ABM, BF.A, CPB, GOL, KFY, LTH, REVG, and UNFI before the opening bell. There are no major reports scheduled for after the close.

In economic news later this week, on Thursday, Weekly Initial Jobless Claims are reported. Finally, on Friday, we get Feb. Avg. Hourly Earnings, Feb. Nonfarm Payrolls, Feb. Participation Rate, Feb. Unemployment Rate, and Feb. Federal Budget Balance.

In earnings news later this week, on Thursday, BJ, GBTG, JD, WLY, TTC, QFIN, DOCU, GPS, ORCL, ULTA, and MTN report. Finally, on Friday, we hear from, ERJ.

So far this morning, CPB, KFY, and REVG have reported beats to both the revenue and earnings lines. Meanwhile, ADDYY, ABM, and LTH all missed on the revenue line while beating on earnings. On the other side, UNFI beat on revenue while missing on the earnings line. (BF.A and BF.B report at 8 am.) It is worth noting that UNFI has lowered its forward guidance while KFY raised its forward guidance.

In late-breaking news, after Powell’s remarks Tuesday, the bond market inversion has grown to the largest in more than four decades. Talking heads are telling traders to brace for a full percent hike later this month, but the Fed Fund futures still don’t show that possibility as getting any betting. (The Fedwatch tool shows a 26.5% probability of a quarter-point hike and a 73.5% probability of a half-percent hike. So, no money even worth mentioning has been bet on three-quarters of a percent, let alone a full percent, hike on March 22. Elsewhere, mortgage application volume increased 7.4% for the week with applications to refinance up 9% and new how purchase applications up 7%. This came despite mortgage rates increasing to 6.79% (up from 6.71%) and points rising to 0.80 from 0.77 during the week (for a 30-year, fixed-rate, 20% down loan). Finally, for the first time since 2016, a new nuclear reactor has come partially online (splitting atoms) in the US (GA). The reactor is scheduled to be fully operational this summer.

With that background, it looks like the market is at least waiting on the morning data before showing any cards. Later, Fed Chair begins testifying (to the House this time) at 10 am. Do not expect him to say anything different from yesterday, but we may get a bit more political point-making from the House. Meanwhile, the downtrend is back in control after yesterday’s bearish signal, and the lower high (although it had broken the short-term downtrend line) in all three major indices. The T-line is still being tested in the QQQ, with the other indices being close enough they could be retested from below today. So, extension is no problem from the T-line standpoint. However, we are in the oversold area of T2122. As I see it, both SPY and DIA are at/in a potential support level. QQQ may have marginal support here, but it is far less obvious than in the large-cap indices.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Although the bulls pushed to test overhead index resistance and downtrend levels, the bullish energy faded into the close as we hurry up and wait for Powell’s Senate testimony this morning. Recent inflationary economic data will likely inspire some tough questioning from the committee. Will we see a tough-talking hawkish Chairman or the gentle dovish version still touting a soft landing that supports the current rally? Expect considerable price volatility as traders and investors hang on every word looking for the path forward. Anything is possible, so plan carefully.

Asian markets traded mixed with modest gains and losses, awaiting the chairman’s congressional testimony. However, European bulls work to add to recent gains, apparently expecting dovish Fed comments. U.S. futures also try to put on a brave face suggesting a modestly bullish open, hoping Powell’s comments will support the recent index surge upward with Fed pivot ringing in its ears.

Economic Calendar

Earnings Calendar

Notable reports for Tuesday include CASY, CRWD, DKS, DOLE, JKS, SWIM, MANU, SE, SQSP, SFIX, SUMO, THO, & WTI.

News & Technicals’

Best Buy has struck a deal to sell devices and handle the installation of a program that allows patients to get hospital care at home. The consumer electronics retailer is expanding its healthcare business as sales of other consumer electronics slow. CEO Corie Barry said on an earnings call that Best Buy expects sales in its health division will grow faster than the rest of the business this fiscal year.

Return-to-office plans fall short leaving commercial real estate empty and at risk of default. CEO Corie Barry said on an earnings call that Best Buy expects sales in its health division will grow faster than the rest of the business this fiscal year. He added that the Covid-19 pandemic forced millions of people to work from home for the first time, and they don’t necessarily want to go back.

Meta is planning more cuts after its first round of layoffs, possibly affecting thousands of jobs. The layoffs could begin this week and affect thousands of employees. The cost-cutting comes in addition to previously announced plans to lay off 13% of Meta workers. Meta CEO Mark Zuckerberg is pitching 2023 as the “Year of Efficiency.”

Monday’s market was essentially a hurry-up-and-wait event as bulls attempted to crack resistance and downtrend levels early in the session. However, uncertainty about the pending Powell testimony faded enthusiasm, leaving shooting star patterns across the indexes. As the Senate committee grills the Fed chairman, what he says will be far less important than how the market interprets his answers. Recent economic reports could spark a bit more hawkish-sounding Powell, disappointing a market that wants to hear dovish statements to support the current rally. The charts suggest big price swings are possible, so expect considerable volatility, whipsaws, and reversals as investors try to guess what comes next as Powell speaks.

Markets made a modest gap higher at the open (up 0.24% in the SPY, up 0.12% in the DIA, and up 0.44% in the QQQ). At that point, we had a small divergence as the bulls stepped in to lead a slow steady rally in the SPY and QQQ until 12:20 pm. Meanwhile, the DIA bobbed sideways over that same time. However, the bears got all three in sync when they stepped in at about 12:25 pm to take us on a slow decline that bottomed out at 3:30 pm with price right back at Friday’s closing level. The last 30 minutes saw a minor rally up off the lows across the SPY, DIA, and QQQ. This action gave us Shooting Star-type candles in all three major indices. It happened on less-than-average volume in the SPY and DIA and slightly greater-than-average volume in the QQQ.

On the day, eight of the 10 sectors were in the red as Basic Materials (-1.98%) led the way lower, while Utilities (+0.43%) held up better than the other sectors. At the same time, the SPY was up 0.07%, the DIA was up 0.14%, and QQQ was up 0.11%. The VXX fell 1.74% to 10.71 and T2122 dropped back into the lower half of the midrange at 37.50. 10-year bond yields climbed all day after started down significantly to close at 3.964% and Oil (WTI) was up 1.02% to $80.49 per barrel. So, overall, Monday was a bullish day all morning and a bearish day all afternoon, which ended up little changed. Still, the omens were not good for the bulls, leaving that gap-up high wick in all three of the major indices.

In economic news, January Factory Orders came in down, but better than expected at -1.6% (compared to a forecast of -1.8% and the December reading of -1.7%). At the same time, the NY Fed released a report saying that after three years of turmoil, global supply chains are back to normal with pressures on supply chains falling into better reading (fewer problems) than at any time since August 2019. Elsewhere, Natural Gas prices crashed Monday with the April front-month natural gas contract falling 14.5% after revised weather forecasts indicated mild temperatures ahead for the Spring in both the US and Europe.

In stock news, the Wall Street Journal reported that PARA is considering the sale of its majority ownership of the BET and VH1 cable networks. Elsewhere, DXCM shares fell hard Monday after rival ABT received FDA approval for two glucose monitoring and insulin delivery systems. ABT said it is partnering with PODD, TNDM, and YPSN for launches in multiple countries. Meanwhile, UIS and BBBY fell sharply after both were removed from the S&P 600 Small-Cap Index. However, FICO was down slightly after being added to the S&P 500 (to replace LUMN which was moved to the Small-Cap 600 index and gained 4.1% on that move). In other news, LMT said it has resumed testing on its “advanced” F-35 jets (after a stoppage due to a government delivery halt over an engine safety concern). Separately, RTX was awarded a $5.2 billion contract to produce 278 engines for the F-35 (with a government option for up to buy up to 518 more engines). After the close, Bloomberg reported the TSLA has lowered the price of the “Plaid” versions of its Model S and Model X cars by another 4.3% and 8.3% respectively. At the same time, SCHW petitioned the SEC to withdraw its two recently proposed rules that would force all orders to be sent to auction and give customers the best possible execution of orders (essentially banning payment for order flow). Finally, TEAM announced after hours that it will lay off 500 employees (5% of its workforce).

In stock legal and regulatory news, Bloomberg reported Monday that the US Dept. of Justice will file suit to prevent JBLU from acquiring SAVE on antitrust grounds. (The $3.8 billion deal has been under fire related to ticket pricing and flight availability in the Northeast corridor.) Bloomberg added that the US Dept. of Transportation is expected to launch parallel proceedings also intended to block the deal. Elsewhere, the NHTSA has opened an investigation into AMZN’s self-certification of its Zoox robotaxi in 2022. Meanwhile, the US Supreme Court again declined to settle a split among Appeals Courts over whether federal wage laws allow workers to bring nationwide class-action type lawsuits when it refused to hear a case from an FDX employee. (Several companies had been pushing courts to limit lawsuits over wage issues, such as unpaid overtime, to cover only those employees in the single state where the suit was filed. So, the court’s refusal to hear the case is a de facto ruling in favor of the position of companies…FDX in this case. Meaning, if a company does wrong, it must be sued in every state in order for the employees of all states to be made whole.) After the close, FERC (Federal Energy Regulatory Commission) requested answers to another set of questions from the Freeport LNG export facility in Texas, before it will be allowed to restart full commercial operations. (The plant had already begun a partial restart after eight months of outage following a fire and explosion.) Finally, after hours, RIO agreed to pay the SEC a $15 million civil penalty for bribing officials in Guinea in order to retain mining rights.

In miscellaneous news, on Saturday San Francisco Fed President Daly said the Jan. inflation data “suggests the disinflation momentum we need is far from certain.” She went on to suggest that “tighter (Fed) policy, for a longer time, is likely needed,” but she did not speak to specific policy moves other than to suggest she thinks the 5.1% terminal projection made in December will be revised upward. Elsewhere, on Sunday, the Chinese government set a slightly lower annual growth target compared to 2022. China is looking for GDP growth of 5% according to a report released at the opening of the country’s annual parliament meeting. This compares to the 2022 target of 5.5%. Meanwhile, also Saturday, it was reported that F had filed a patent application for technology that remotely disables heating/air conditioning, radio, and ultimately the car itself if the customer fails to make lease payments on time. The patent also includes a feature for self-driving cars to return themselves to F impound lots. However, F says it has no (current?) plans to deploy these technologies itself. (Still, I be there are a lot of banks that would like to have those features installed.) Finally, the FDA rejected an application from Elon Musk’s Neuralink, which had wanted to start testing its brain implants in humans.

Overnight, Asian markets were mostly in the green on modest moves, with the exception of China. Shenzhen (-1.98%), Shanghai (-1.11%), and Hong Kong (-0.33%) were the only red in the region. Meanwhile, Thailand (+0.72%), India (+0.67%), and Australian (+0.49%) led the rest of the region higher. Over in Europe, the bourses are evenly split between red and green bourses at midday. The FTSE (+0.24%), DAX (+0.11%), and CAC (+0.12%) lead the region on volume (as always). However, it looks like Europe is just as eager for another clue from Fed Chair Powell as the US markets. As of 7:30 am, US Futures are pointing toward a start to the day just on the green side of flat. The DIA implies a +0.02% open, the SPY is implying a +0.12% open, and the QQQ implies a +0.22% open at this hour. At the same time, 10-year bond yields are down to 3.94% and Oil (WTI) is off six-tenths of a percent to $79.96/barrel in early trading.

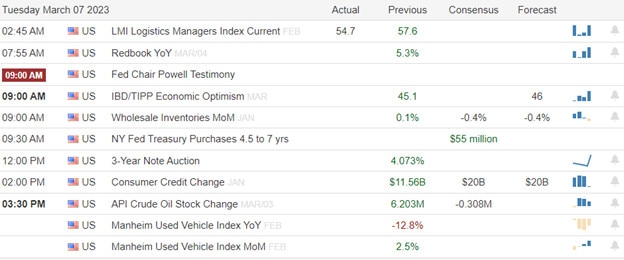

The major economic news events scheduled for Tuesday are limited to Fed Chair Powell testifying before Congress (10 am) and then the API Weekly Crude Oil Stocks Report is released at 4:30 pm. Major earnings reports scheduled for the day are limited to DKS, DOLE, ESAB, FERG, SE, and THO before the opening bell. Then, after the close, CASY, CRGY, and CRWD report.

In economic news later this week, on Wednesday, we get ADP February Nonfarm Employment Change, Jan. Imports and Exports, Jan. Trade Balance, Fed Chair Powell testifies before Congress again, Jan. JOLTs Job Openings, EIA Crude Oil Inventories, WASDE Ag Report, and Fed Beige Book. On Thursday, Weekly Initial Jobless Claims are reported. Finally, on Friday, we get Feb. Avg. Hourly Earnings, Feb. Nonfarm Payrolls, Feb. Participation Rate, Feb. Unemployment Rate, and Feb. Federal Budget Balance.

In earnings news later this week, on Wednesday, we hear from, ABM, BF.A, CPB, GOL, KFY, LTH, and REVG. On Thursday, BJ, GBTG, JD, WLY, TTC, QFIN, DOCU, GPS, ORCL, ULTA, and MTN report. Finally, on Friday, we hear from, ERJ.

So far this morning, DKS, DOLE, SE, and ESAB have all reported beats to the revenue and earnings lines. Meanwhile, THO missed on both the top and bottom lines. It is worth noting that THO lowered its forward guidance while DKS raised its guidance. It is also worth noting that DKS crushed expectations with more than double the same-store sales growth in Q4 than analysts had expected.

In late-breaking news, Bloomberg reports META will lay off thousands more employees as soon as later this week. Elsewhere, BBY has entered a new market, by striking a deal with Atrium Health. This will expand the BBY “Geek Squad” offering to include the delivery and setup of durable medical equipment (DME) such as heart monitors, vitals, oxygen delivery, etc.

With that background, it looks like the market remains undecided and is waiting on guidance from Fed Chair Powell. So, beware volatility as his opening statement is released and then he begins his testimony at 10 am. Meanwhile, the recent downtrend line remains broken in all three major indicies. However, their 3-day upward move is not very secure either. We definitely have not put in a new higher-low to signal a bullish trend yet. We have no problem with extension (either according to T2122, or the T-line). As I see it, we remain basically at the same place we were in premarket Monday. The DIA is testing a potential resistance level, SPY has a little room to run before hitting its next resistance level, and QQQ has the most headroom above before hitting its next potential resistance level. DIA also has its 50sma just overhead and you could draw a longer-term downtrend just above in the QQQ. Continue to be careful in an unsettled market (especially where the Fed wants to raise expectations for their terminal rate and tamp down any hope for a rate cut this year). (With that said, current Fed Fund Futures say there is a 70.8% probability of a quarter-point hike in two weeks while 29.2% are betting on a half-point hike. Not a single sole has bought futures to indicate they are betting on either no hike or a larger than half-percent hike.)

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Markets gapped modestly higher at the open Friday. The SPY gapped up 0.45%, the DIA gapped up 0.32%, and the QQQ gapped up 0.59%. After that, with the exception of some volatility the first 40 minutes, the bulls were in control in all three major indices. We saw a slow, steady rally the rest of the day, which closed near very the high. This action gave us gap-up, large, white-bodied candles with small lower wicks and almost no upper wick. All three of the major indices crossed back above their T-line (8ema) and the DIA is back up very near a retest of its 50sma.

On the day, all 10 sectors were in the green with Technology (+2.09%) leading the way higher and Consumer Defensive (+0.39%) lagging behind the other sectors. At the same time, the SPY was up 1.60%, the DIA was up 1.14%, and QQQ was up 2.07%. The VXX fell almost 3% to 10.90 and T2122 spiked higher into the edge of overbought territory at 83.16. 10-year bond yields dropped back below the key 4% level to 3.958% and Oil (WTI) jumped up 2.16% to $79.85 per barrel. So, overall, Friday was a risk-on, bullish day with a slow, steady gain all across the market and all day long. This all happened on greater-than-average volume in both the SPY and QQQ but a little less-than-average volume in the DIA.

In economic news, the February S&P Global Composite PMI came in slightly below the expectation at 50.1 (compared to a forecast of 50.2 but above the January reading of 46.8). At the same time, the February US Services PMI came in slightly above the anticipated level at 50.6 (versus the forecast of 50.5 and well above the January value of 46.8). Moments later, the ISM February non-Mfg. PMI also came in above forecast at 55.1 (compared to an expected value of 54.5 but still slightly below the January reading of 55.2). So, overall, the data suggest the global economy is just slightly less strong than anticipated (but still expanding), but the US economy was a bit stronger than expected last month. Finally, on the Fed front, Richmond Fed President Barkin said Friday that he doesn’t see a case for a rate pause yet. He also said he could see the terminal Fed Funds rate reaching 5.5%-5.75%. However, Barkin also called for the Fed to “move more deliberately (smaller hikes) than we did last year.”

In stock news, on Friday, AMZN announced it will push back the start of construction of its new Virginia second headquarters. No timetable was given for the resumption of the project that was expected to create 25,000 jobs. Elsewhere, META announced price cuts on its VR Headsets ($1499 to $999 and $499 to $429) in an effort to stimulate demand. At nearly the same time, Bloomberg reported that RIVN executives have been telling employees the company could produce 62,000 electric vehicles in 2023. However, the company denied the report and said its forecast of 50,000 vehicles for the year still stands. Later, TSM told Reuters they will be hiring more than 6,000 new engineers in 2023. However, those new jobs are mainly for their Taiwanese facilities. Meanwhile, NVDA said the Biden Administration limiting items it authorizes to sell to Huawei is likely to have a “high economic impact” on NVDA. Reuters reported that QCOM will also suffer moderate economic impact from the decision. After hours, SI announced they are discontinuing its crypto payment exchange network effective immediately. The company said it was a “risk-based decision” after serious doubts had been raised earlier in the week as to whether SI could remain afloat. On Saturday, Sky News (UK) reported that GS is among the suitors interested in acquiring the Subway sandwich chain. Subway was put up for sale at a $10 billion price tag last week.

In stock legal and regulatory news, on Saturday, the HHTSA announced that TSLA has recalled about 3.500 Model Y cars over loose bolts securing second-row seat frames. On Sunday, Investing.com reported on how the EU is expected to rule on two deals. It reports that sources tell them the EU will approve the MSFT $69 billion acquisition of ATVI. However, AVGO is expected to receive an antitrust warning over the impact of its $61 billion acquisition of VMW. This likely means AVGO will need to propose remedies to the EU concerns in order to move forward. Ohio reported Saturday that another NSF train derailed in the state, this time in the Western half of the state. NSF reports that there were no hazardous materials on the train, although authorities had residents shelter in place as a precaution and the accident caused power outages in the area after taking out power lines.

In miscellaneous news, on Saturday San Francisco Fed President Daly said the Jan. inflation data “suggests the disinflation momentum we need is far from certain.” She went on to suggest that “tighter (Fed) policy, for a longer time, is likely needed,” but she did not speak to specific policy moves other than to suggest she thinks the 5.1% terminal projection made in December will be revised upward. Elsewhere, on Sunday, the Chinese government set a slightly lower annual growth target compared to 2022. China is looking for GDP growth of 5% according to a report released at the opening of the country’s annual parliament meeting. This compares to the 2022 target of 5.5%. Meanwhile, also Saturday, it was reported that F had filed a patent application for technology that remotely disables heating/air conditioning, radio, and ultimately the car itself if the customer fails to make lease payments on time. The patent also includes a feature for self-driving cars to return themselves to F impound lots. However, F says it has no (current?) plans to deploy these technologies itself. (Still, I be there are a lot of banks that would like to have those features installed.) Finally, the FDA rejected an application from Elon Musk’s Neuralink, which had wanted to start testing its brain implants in humans.

Overnight, Asian markets were mixed but leaned to the green side. South Korea (+1.20%), Japan (+1.11%), and Taiwan (+0.99%) led the region higher. Meanwhile, in Europe, markets are even more mixed and lean to the red side at midday. The FTSE (-0.60%), DAX (+0.19%), and CAC (+0.17%) lead the region on volume. However, Russia (+0.88%), and outlier Greece (-3.26%) are the biggest movers in early afternoon trade. As of 7:30 am, US Futures are pointing toward a mixed and flat start to the day. The DIA implies a -0.10% open, the SPY is implying a -0.07% open, and the QQQ implies a +0.01% open at this hour. At the same time, 10-year bond yields are down briskly to 3.921% and Oil (WTI) is off 1.44% to $78.53/barrel in early trading.

The major economic news events scheduled for Monday is limited to January Factory Orders (10 am). Major earnings reports scheduled for the day are limited to CIEN and AZUL before the opening bell. Then, after the close, TCOM, NTNX, BBAR, and PTVE report.

In economic news later this week, on Tuesday, Fed Chair Powell testifies before Congress and then we get API Weekly Crude Oil Stocks Report is released. On Wednesday, we get ADP February Nonfarm Employment Change, Jan. Imports and Exports, Jan. Trade Balance, Fed Chair Powell testifies before Congress again, Jan. JOLTs Job Openings, EIA Crude Oil Inventories, WASDE Ag Report, and Fed Beige Book. On Thursday, Weekly Initial Jobless Claims are reported. Finally, on Friday, we get Feb. Avg. Hourly Earnings, Feb. Nonfarm Payrolls, Feb. Participation Rate, Feb. Unemployment Rate, and Feb. Federal Budget Balance.

In earnings news later this week, on Tuesday, DKS, DOLE, ESAB, FERG, SE, THO, CASY, CRGY, and CRWD report. The Wednesday, we hear from, ABM, BF.A, CPB, GOL, KFY, LTH, and REVG. On Thursday, BJ, GBTG, JD, WLY, TTC, QFIN, DOCU, GPS, ORCL, ULTA, and MTN report. Finally, on Friday, we hear from, ERJ.