China Cuts Deposit Rates, Russian Terror

Monday was an interesting day, both dead and volatile at different times driven by the news that the Fed may raise bank capital requirements on one hand and AAPL product announcements on the other. The SPY opened flat (up 0.06%), DIA opened up 0.05%, and QQQ opened down 0.05%. Then, markets diverged as the DIA sold off until 11:30 am before rallying slowly and steadily until 1 pm followed by another selloff that went all the way into the close (on the lows). At the same time, SPY chopped around until 10:30 am before starting a slow, steady rally that reached the highs of the day at about 1:10 pm. From there SPY saw stronger selling to reach the lows of the day at 3:10 pm before grinding slightly bullish into the close. Meanwhile, QQQ rallied all morning (in a more volatile wave) reaching the high of the day at about 1:10 pm. From there it too sold off even more sharply with large black candles at 2:35 pm and 3:05 pm before rallying back up off the lows in the last hour of the day. This action gave us a white-bodied Shooting Star type candle in the QQQ, a black-bodied Spinning Top type candle (with a larger upper wick) in the SPY, and a Bear Harami candle in the upper third of Friday’s candle in the DIA.

All three major indices remain above their T-line (8ema). On the day, seven of the 10 sectors were in the red as Industrials (-0.88%) led the way lower, and Communication Services (+0.44%) held up better than other sectors. At the same time, DIA lost 0.57%, SPY lost 0.19%, and QQQ gained 0.07%. VXX fall 1.83% to end at 30.61 and T2122 fell back just outside the overbought territory at 76.00. 10-year bond yields fell all day (after being up big early) to end at 3.685% while Oil (WTI) also pulled back after very early day gains to end the day flat at $71.86 per barrel. So, again, Monday was a Dr. Jekyll – Mr. Hyde day where there were periods of dead action, periods of slow and steady trend, intraday reversals, and also 5-minute periods of extreme move in the QQQ. However, taken from a higher-level view, it was just an indecisive day. All this took place on just below-average volume in the QQQ, just above-average volume in the DIA, and significantly lower-than-average volume in the SPY.

In major economic news, the May S&P Global Composite PMI came in a bit lower than expected at 54.3 (compared to a forecast of 54.5 but still above the April reading of 53.4). At the same time, the May Services PMI also came in a bit lower than expected at 54.9 (versus a forecast of 55.1 but above the April value of 53.6). A few minutes later, April Factory Orders were reported well below what was anticipated at +0.4% (compared to a forecast of +1.1% and even below the March reading of +0.6%). The May ISM Non-Mfg. Employment was also a bit low at 49.2 (versus the forecast of 51.0 and even below the April value of 50.8). Finally, the May ISM Non-Mfg. PMI was also below expectations at 50.3 (compared to a 51.8 forecast and the April reading of 51.9). So, overall, we saw several moderately worse-than-expected economic data point on the day. However, at the same time, all the PMI readings above 50.0 signal economic expansion. By themselves, they mean little. The question is whether this data shows enough slowing to influence Fed opinions.

SNAP Case Study | Actual Trade

In stock news, on Monday, UNH made an unexpected $3.26 billion all-cash offer to buy AMED. This news saw AMED gap 13% higher and follow-through to close at the highs, up 15.44% ($91.74). At the same time, UBS also announced it expects to close its CS takeover by June 12. Elsewhere in the Finance space, Canadian insurer Fairfax Financial Holdings has agreed to buy 63 real estate construction loans from KW for $2.1 billion. (This is notable because KW acquired those loans plus 11 others from PACW during the regional bank scare. KW had paid $2.4 billion which was a $200 million discount. As part of the deal, Fairfax also gets a $200 million equity position in KW.) In the auto space, GM said Monday that it will invest more than $1 billion to upgrade internal-combustion pickup truck production capacity at two Flint, MI plants. In the tech space, AAPL gapped and ran higher (up 2.2% at a point) to an all-time high ahead of its Developer Conference (product announcements). However, markets then sold the news as AAPL went on a bearish tear in the afternoon to close down 0.76%. Meanwhile, BX announced it has agreed to buy a San Antonio Texas resort from RHP for $800 million.

In stock legal and regulatory news, a US judge has postponed the start of a trial between the city of Stuart FL, and MMM over “forever chemicals” in the city water supply. This was because the parties said they were nearing a settlement. The suit had sought more than $100 million in filtration and remediation damages. Meanwhile, the NHTSA announced that TSLA has agreed to voluntarily recall a small number (a couple hundred) Model Y cars over a safety concern related to a loose fastener on the steering wheel (which could detach completely). While this was a tiny recall, TSLA Model Y vehicles have had reports of detached steering wheels globally dating back to May 2020 and TLSA said only 105 of its Model Ys could be affected. Elsewhere, the state of TX won the latest round of its antitrust lawsuit against GOOGL as the case was ordered returned to a federal court in TX on Monday. (GOOGL had been fighting to have the case moved to NY.) After the close, NSC filed to ask a US judge to throw out a class action lawsuit brought on behalf of the 500,000 area residents impacted by the toxic chemical spill resulting from the train derailment in East Palestine OH.

After the close, JOAN reported misses on both the revenue and earnings lines. The earnings miss was a 59% downside surprise.

Overnight, Asian markets were mixed but leaned to the red side. Shenzhen (-1.58%), Australia (-1.20%), and Shanghai (-1.15%) paced the losses. Meanwhile, Japan (+0.90%), South Korea (+0.54%), and Taiwan (+0.28%) led the gainers. In Europe, we see the same picture taking shape at midday with only four (of 15) bourses in the green. Greece (+1.56%) is by far the biggest gainer while Russia (-1.88%) is by far the biggest loser. However, as always, the CAC (-0.27%), DAX (-0.16%), and FTSE (-0.29%) lead the region (this time lower) in early afternoon trade. In the US, as of 7:30 am, Futures are pointing toward a very modest red start to the day. The DIA implies a -0.08% open, the SPY is implying a -0.06% open, and the QQQ implies a -0.05% open at this hour. At the same time, 10-year bonds are down to 3.674% and Oil (WTI) is down nearly 2.34% to $70.46 per barrel in early trading.

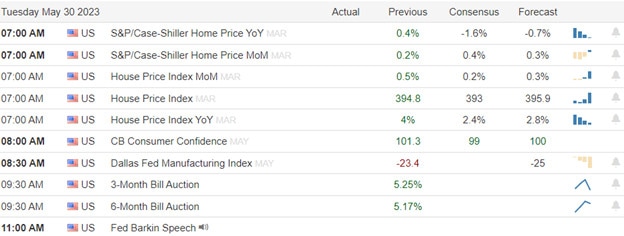

The major economic news events scheduled for Tuesday are limited to EIA Short-term Energy Outlook (noon) and API Weekly Crude Oil Stocks Report (4:30 pm). The major earnings reports scheduled for the day are limited to ABM, ASO, CHS, SIEN, CNM, CBRL, FERG, GIII, SJM, and THO before the open. The after the close, CASY and PLAY report.

In economic news later this week, on Wednesday, April Imports/Exports, April Trade Balance, and EIA Crude Oil Inventories are reported. On Thursday, we get Weekly Initial Jobless Claims, Fed Balance Sheet, and Bank Balances with the Fed. Finally, on Friday, the WASDE Ag Report comes out.

In terms of earnings reports later this week, on Wednesday, BF.A, CPB, OLLI, UNFI, GME, GEF, and TCOM report. On Thursday, we hear from DBI, REVG, SIG, TTC, DOCU, and MTN. Finally, on Friday, NIO reports.

In miscellaneous news, at its Global Developer Conference, as expected, AAPL announced a new “mixed-reality” headset (for a paltry $3,500 which is about three times the price of the current top-end brands) which will not be launched until sometime in 2024. At the same time, AAPL announced that the last of its computers will move away from INTC chips to “its own chips” (produced by TSM using the Arm architecture). In addition, AAPL announced a new iOS 17 for the next generation of iPhones to be announced/offered later this year. Elsewhere, in Ukraine overnight Russia blew up a dam on the massive Dnipro River, unleashing about 5 billion gallons of water toward 80-100 villages. While crop production should not be impacted in a huge way, global Wheat prices jumped 3% on the news. (Obviously, the more important issue for Russia was the terroristic destruction of Ukrainian electric infrastructure (hydro-electric plant), and flooding delaying and encumbering a Ukrainian counter-offensive in the South of the country. Finally, China asked its biggest banks to lower deposit rates again overnight. Theoretically, this would drive more consumer spending and/or possibly support more lending (or at least free up some bank money to cover bad loans). Obviously, the overall goal is to stoke the Chinese economy and help its floundering real estate sector.

So far this morning, FERG, THO, SJM, CIEN, and GIII have all reported beats on both the revenue and earnings lines. Meanwhile, ABM, CNM, and CHS all missed on revenue while beating on earnings. (CBRL and ASO report closer to the open.) There have been no announced guidance changes. It is worth noting that major surprises came from GIII (a 244% upside earnings surprise) and THO (a 98% upside earnings surprise). However, even though both were major upside surprises, both were also down sequentially from the prior quarter’s earnings.

With that background, it looks like markets are looking to consolidate a bit more with small, black-body candles just below the prior close in the premarket. However, none of the three major index ETFs appear to be headed to a retest of their T-line (8ema) today, at least at this point. So, the bullish trend remains intact as of now. In terms of over-extension, only the QQQ is extended from (above) its T-line and the T2122 has also dropped back (just) outside of the overbought territory. So, more consolidation or pullback may be in order, but technically we have a little room left to run before we are truly over-extended. As mentioned above, even on small-body indecisive days like Monday, intraday volatility and chop have been the norm. So, again remain alert.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Saudi Oil, APPL Visors, and Bank Holdings

Friday was the Bulls’ Day. It may have been the Debt Ceiling bill passing, a Bullish take on economic data, or just traders being happy that it was Friday. Whatever the cause, the bulls ruled markets on the day. This started with a gap higher (up 0.63% in the SPY, up 0.65% in the DIA, and up 0.53% in the QQQ). This was followed up by a strong rally in the first minutes of the session and then the only tiny bearish wobble of the whole day. Still, by 10:05 am, the Bulls were running again. For the QQQ, the run ended shortly after 11 am before a sideways grind in a tight range took over for the rest of the session. SPY ran up until 11:30 am before grinding sideways with a slightly bullish trend the rest of the day. DIA led the way for once, continuing its rally until about 2:45 pm before grinding sideways the rest of the way into the close. This action gave up large white candles with tiny wicks in the DIA and SPY while the QQQ printed a gap-up, white-bodied, Spinning Top candle. If you had seen Thursday’s candle as having completed a Morning Star signal, Friday was definitely bullish follow-through.s.

All three major indices are back above their T-line (8ema) and DIA broke strongly up through its 50sma. On the day, nine of the 10 sectors were in the green with Basic Materials (+3.44%), Industrials (+3.15%), and Energy (+3.14%) out in front pulling the rest of the market higher. Meanwhile, Communications Services (-1.16%) was the only sector in the red on a terrible day for TMUS, T, and VZ. At the same time, SPY gained 1.45%, QQQ gained 0.75%, and DIA gained 2.15%. VXX plummeted another 4% to end at 31.18 and T2122 shot up deep into the overbought territory at 96.46. 10-year bond yields rose sharply to 3.698% while Oil (WTI) jumped another 2.52% to end the day at $71.87 per barrel. So, again, Friday was no day to be a short and no fun at all for the bears. This all happened on average volume in the SPY and QQQ while DIA had significantly heavier-than-average volume.

In major economic news, the May Nonfarm Payrolls came in smoking hot at +339k (compared to a forecast of +180k and an April reading of +294k). May Private Nonfarm Payrolls were hot also at +283k (versus +160k forecasted and just a little hotter than April’s +253k value). So, again, our economy continues to produce a lot of jobs…much more than expected. The May Participation Rate remained the same at 62.6% (which is slightly higher that the predicted fall to 62.5%). However, the “odd man out” among this data was the May Unemployment Rate, which jumped up to 3.7% (compared to a forecast of 3.5% and the April reading of 3.4%). That discrepancy given all the newly created jobs leads me to suspect perhaps some seasonal (or other) adjustments are at least partly to blame for the significant rise in unemployment.

SNAP Case Study | Actual Trade

There will be no Fed speak between now and the June 14 announcement. The Fed entered into its pre-meeting “blackout period” on Friday. However, in other economic speak Friday, JPM President Pinto (Jamie Dimon’s #2) told investors loan demand is declining even as regional banks are also tightening credit requirements. He said, “There is no doubt that regional banks and smaller banks … are lending a bit less … I don’t think that the big banks have really changed their lending standards, there is not a huge amount of loan demand in the first place.”

In stock news, early Friday Bloomberg reported that AMZN is in talks to offer its own wireless service for Prime members. This caused dramatic falls in stock prices for T, TMU, and VZ. (The telcos denied that have any talks with AMZN later in the day.) Then, mid-morning, Reuters reported that the Debt Ceiling agreement “stranded” $16 billion in low-priority Defense spending that has usually always been added to “must pass” bills at the last second. (Despite this, Congress still raised the Defense budget $80 billion more than the President requested, a trend that has been the norm each year for several years.) The $16 billion “lost” would have funded tanks from GD, a plane from LMT, and a small ship from HII. Elsewhere, CBOE announced that it is expanding into allowing cross-listing (US and international listings) which will make it a direct competitor of ICE and Nasdaq. At the same time, SU told its employees it plans to cut 1,500 jobs (from a base of 16,550) by the end of the year. In a similar vein, TSN announced its terminating (262 of 500) corporate staff (including key executives) located in South Dakota who chose not to relocate to Arkansas. Later, GM and PKX announced they are expanding their chemical battery partnership adding another $1 billion to expand capacity at their Canadian plant. Meanwhile, in another blow to truth, GOOGL said Friday afternoon that its YouTube unit will stop removing content that spreads falsehoods and lies about past US Presidential elections. For GOOGL, the important aspect is there were rumblings from advertisers over the weekend as a result of the action. The fear for GOOGL is another mass desertion by advertisers, similar to what was experienced by Twitter when Musk decided to go “free for all” on misinformation.

In stock legal and regulatory news, the NHTSA fined STLA and GM a combined 363 million on Friday for average fuel economy violations. Friday morning, CC, DD, and CTVA a $1.185 billion settlement agreement with the water systems that serve the vast majority of US citizens related to “forever chemicals” that got into drinking water. This avoids a federal trial that was set to begin today. Later, Bloomberg reported sources told them that MMM had reached a tentative $10 billion settlement over the same issue with the same entities. (However, the MMM settlement has not been confirmed by the two sides publicly.) Elsewhere, a US District judge in Seattle approved a $415 million settlement of a class action lawsuit involving IGT and an unlisted co-defendant. At the same time, a District of Columbia judge dismissed a 2018 lawsuit brought against META by the Washington DC government (which had claimed the company misled users over the Cambridge Analytica scandal). Later Friday, a judge in MA threw out motions that had been filed by F, GM, TM, etc. in an attempt to prevent a law from taking effect which forces automakers to allow “right to repair” access to all auto data needed to repair vehicles. (In other words, prohibiting automakers from forcing repairs and parts to only come from the automakers.)

Overnight, Asian markets were mostly green. Japan (+2.20%), Australia (+1.00%), and Hong Kong (+0.84%) led the winners. Meanwhile, the only three exchanges in the red were Shenzhen (-0.47%), New Zealand (-0.30%), and Malaysia (-0.13%). In Europe, we see a very similar picture taking shape at midday with only two spots of red on the board. The CAC (-0.07%), DAX (+0.17%), and FTSE (+0.55%) are leading the way in early afternoon trade. In the US, as of 7:30 am, Futures are pointing toward a mixed, flat start to the day. The DIA implies a +0.09% open, the SPY is implying a +0.07% open, and the QQQ implies a -0.10% open at this hour. At the same time, 10-year bonds are spiking higher at 3.751% and Oil (WTI) is up just over 2% to $73.18 per barrel in early trading.

The major economic news events scheduled for Monday include May S&P Global Composite PMI and May Services PMI (both at 9:45 am), April Factory Orders and May ISM PMI (both at 10 am). The major earnings reports scheduled for the day are limited to SAIC before the opening bell and JOAN after the close.

In economic news later this week, on Tuesday we get EIA Short-term Energy Outlook and API Weekly Crude Oil Stocks Report. Then Wednesday, April Imports/Exports, April Trade Balance, and EIA Crude Oil Inventories are reported. On Thursday, we get Weekly Initial Jobless Claims, Fed Balance Sheet, and Bank Balances with the Fed. Finally, on Friday, the WASDE Ag Report comes out.

In terms of earnings reports later this week, on Tuesday we hear from ABM, ASO, CHS, SIEN, CNM, CBRL, FERG, GIII, SJM, THO, CASY, and PLAY. Then Wednesday, BF.A, CPB, OLLI, UNFI, GME, GEF, and TCOM report. On Thursday, we hear from DBI, REVG, SIG, TTC, DOCU, and MTN. Finally, on Friday, NIO reports.

In miscellaneous news, analyst firm Refinitiv said Friday that much stronger than expected recent earnings (covering 494 of the S&P 500) have led it to raise its estimate of Q1 earnings to flat versus the same quarter of 2022. This is after the firm had forecast a 5.1% drop in earnings for the quarter as late as the start of April. On Sunday, OPEC+ decided to stay with their current production levels with the Russian delegate telling the press that the level will be extended through 2024 (they were to expire at the end of 2023). However, Saudi Arabia announced it will implement an additional voluntary, one-month reduction of 1 million barrels per day in July (which it could voluntarily extend for additional months). Finally, the Wall Street Journal reported early today that large banks may face a 20% increase in required capital holdings as early as this month. The report said this would only impact banks with more than $100 billion in assets (lowering that definition threshold from $250 billion in assets). This would cause significant changes to lending standards and investment approaches, which might act as a “rate hike by other means.”

So far this morning, SAIC was the only report and it beat on both the revenue and earnings lines. The company also raised forward guidance.

With that background, it looks like the market is undecided early this Monday morning. All three major index ETFs are above their T-line (8ema) and sitting at Friday’s strong closing level. All three could be seen as sitting not far below, just above, or at a potential resistance level. All three could also be seen as a bit extended above their T-lines, with QQQ (market leader) being the most extended. T2122 also tells us the market is deep in the overbought territory. So, keep your eye open for consolidation or pullback. As usual, intraday volatility and daily-level chop have been the norm…again be aware. Lastly, AAPL is expected to announce new products and product lines mid-day today. Frankly, I don’t think much of the market potential of augmented reality glasses (GOOGL tried and failed and META has been desperately and not very successfully trying to sell the same thing for years). Then again, I never thought AAPL’s phone would take the world by storm either all those years ago. So, just be aware and see if AAPL can fire up the QQQ and SPY.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Default Off Table With May Jobs Up Next

Markets opened just on the green side of flat (up 0.06% in the SPY, down 0.15% in the DIA, and up 0.01% in the QQQ). DIA then sold off for the first 30 minutes while the SPY and QQQ chopped sideways. However, at 10 am, all three major indices started strong rallies that lasted until 12:30 pm before grinding sideways with a much lesser Bullish trend until 2:30 pm. Then we saw another, shorter, strong rally before we saw strong profit taking the last 40 minutes of the day in all three. This action gave us large white candles with wicks on both ends in the SPY and QQQ. The DIA was more of a white-bodied Spinning Top candle that closed right at its T-line. All three major index ETFs could be called Morning Star signals if you squint or are liberal with signal definitions.

On the day, nine of the 10 sectors were in the green with Basic Materials (+2.02%) and Energy (+1.96%) out in front pulling the rest of the market higher while Utilities (-0.36%) was the only sector in the red. At the same time, SPY gained 0.95%, QQQ gained 1.16%, and DIA gained 0.43%. VXX plummeted 5.72% on the day to end at 32.49 and T2122 shot back up into the mid-range at 60.26. 10-year bond yields fell sharply to 3.601% while Oil (WTI) jumped 2.83% to end the day at $70.03 per barrel. So, Thursday was the Bulls’ Day as optimism over the Debt Ceiling bill passage spread and economic data painted a picture that could be spun as bullish. This all happened on average volume in the SPY and DIA while QQQ had less-than-average volume.

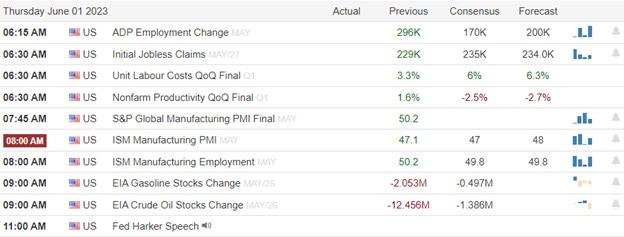

In major economic news, the May ADP Nonfarm Employment Change saw a much higher than expected +278k jobs (compared to a forecast of +170k but still less than April’s +291k). Shortly afterward, the Weekly Initial Jobless Claims came in just below the anticipated level at 232k (versus the forecast of 235k but slightly above the prior week’s 230k). At the same time, Q1 Nonfarm Productivity (quarter-on-quarter) was not nearly as bad as feared at -2.1% (compared to the forecast of -2.7% but still much worse than the Q4 +1.7%). Q1 (quarter-on-quarter) Unit Labor Costs were up but again far better than feared at +4.2% (versus a forecast of +6.3% while still a full percent higher than the Q4 number of +3.2%). All of the above tells us businesses are continuing to hire briskly and layoffs are slightly better than expected. Meanwhile, the “wage inflation pressure” is falling sharply without as much loss in productivity as feared. Later in the morning, May Manufacturing PMI was reported just shy of the anticipated level at 48.4 (compared to the 48.5 forecast but still lower than the April 50.2 reading). Next the ISM May Mfg. PMI also came in just shy of expectations at 46.9 (versus the forecast of 47.0 and not far below the April value of 47.1). At the same time, the May ISM Mfg. Price Index came in well below projections at 44.2 (compared to a forecast of 52.0 and far below the April 53.2 value). Finally, EIA Weekly Crude Oil Inventories showed an unexpected build of 4.488 million barrels (versus a forecasted drawdown of 1.101-million-barrels and drastically different from the prior week’s 12.456-million-barrel drawdown). All-in-all, we saw several pieces of news that can be read as decreasing inflationary pressures, while businesses continue to hire briskly and Manufacturing is not falling off a cliff.

SNAP Case Study | Actual Trade

In Fed talk, Philly Fed President Harker spoke again Thursday. He went even further than he had on Wednesday, telling the National Assn. for Business Economics, “It’s time to at least hit the stop button for one meeting and see how it goes,”. Harker went on to say he sees promising signs that the Fed’s previous hikes are having a cooling effect, particularly on housing prices. At the same time, he said uncertainty over inflation dynamics and the pace of credit tightening make him wary of continuing to raise rates until after the Fed’s prior hikes have been given more time to work. Finally, he said he expects inflation to fall to 3.5% this year, expects GDP to grow about 1%, and sees unemployment growing to 4.4% by year end.

In debt ceiling news, the Penn University Wharton school Budget Model Research Group said Thursday that the Republican claimed $1.3 trillion in spending cuts (over 10 years) may mostly evaporate. Since no deal is binding on a future Congress, the Wharton group expects the same situation that happened after the 2011 debt ceiling deal when Congress simply increased spending again once the next election passed. The study expects $1 trillion of the $1.3 trillion in cuts to simply evaporate after the 2024 election. Elsewhere, Senate Majority Leader Schumer announced the Senate will stay in session this weekend until the debt ceiling increase is passed. Both Schumer and Minority Leader McConnell vowed to do all they could to speed the bill to passage and onto the President’s desk. However, several GOP Senators are pushing to have amendments allowed. For example, the Republican caucus expected to offer several defense-related amendments alone. GOP Senator Graham also threatened to tie up the bill “until Tuesday” (default) if he doesn’t get a guarantee a supplemental Defense Spending bill to follow. At the same time, GOP Senator Paul also threatened to stall the bill into default unless he can add an amendment calling for more spending cuts. Democrats were not immune to the amendment desire either as Senator Kaine introduced one that removes approval for a Nat. Gas Pipeline across his state. The odd Senate rules allow would also be problematic. While it takes 60 votes to pass the bill, amendments can be added with only 50 votes. Of course, any amendment at all would mean a passed bill would need to go back to the House for another vote before it can head to President Biden for signature. At the end of the day, leaders Schumer and McConnell got tough with their caucuses because A) there was no time to screw around and go back to the House, and B) the Senate never works on Fridays or Weekends. So, the bill passed unamended late last night on another bi-partisan vote of 63-36.

In stock news, on Thursday, GS warned that its trading revenue could fall 25% this quarter. This echoes JPM’s May announcement it expects trading revenue to be down 15% for the quarter and the Wednesday MS warning that trading results will be “notably down.” In a related story, the CEO of BAC announced that he expects trading revenue and investment banking fees to be roughly flat in Q2. Elsewhere, META announced a new “mixed reality” headset for $499 ahead of AAPL’s expected unveiling of a headset next week. At the same time, CNBC reported that MSFT has signed a deal to spend billions of dollars over multiple years with startup CoreWeave in order to provide infrastructure for the inclusion of ChatGPT in MSFT products. Meanwhile, the CEO of LUV said late Thursday that he expects the industry-wide pilot shortage to last for three years. (LUV currently has 40 planes sitting idle because of the shortage while AAL has said they have 50 mainline jets and 150 regional planes idled by a lack of pilots.) After the close, BA announced it is “standing down” (canceling) plans for a manned test flight into space of the company’s Starliner rocket. The flight had been scheduled for July. Also after the close, Reuters reported that NKLA is planning a reverse stock split in order to come into compliance with the Nasdaq requirement that shares be valued over $1.

In stock legal and regulatory news, the US Supreme Court ruled 9-0 in favor of WORK (a “direct listing” of CRM) throwing out a lower court decision and ordering the 9th US Circuit Court of Appeals to reconsider the investor class action case over alleged fraudulent prospectus that had been filed against the company. Elsewhere, GPS has settled (under undisclosed terms) a lawsuit filed by Patagonia Inc. claiming GPS had illegally copied a pocket design. At the same time, EU Antitrust regulators announced they will decide by July 6 whether to clear the $1.7 billion AMZN acquisition of IRBT. Back on this side of the pond, the US Medicare health plan announced it will limit reimbursement for Alzheimer’s drugs from ESAIY and BIIB to only cases where it was prescribed by doctors in the agency’s database. (This will hinder drug sales to Medicare users.) Meanwhile, the US Supreme Court dealt a blow to unions when it ruled 8-1 to make it easier for employers to sue over strikes that cause property damage. (A concrete company’s union drivers went on strike while trucks were filled with concrete. The concrete hardened and caused the company major expenses to remove the cement from the trucks and, of course, the loss of the concrete itself.) In other news, F filed suit against Blue Cross Blue Shield, accusing the insurer of a price-fixing conspiracy that artificially inflated the automaker’s health insurance costs to cover its employees.

After the close, DELL, AVGO, LULU, and COO all reported beats on both the revenue and earnings lines. Meanwhile, FIVE missed on revenue while beating on earnings. Unfortunately, VMW missed on both the top and bottom lines. It is worth noting that both AVGO and LULU raised their forward guidance. The only major surprise was a 52% upside earnings shock from DELL (although it was still a 32% earnings decline).

Overnight, Asian markets were mostly (and in some cases strongly) green. Hong Kong (+4.02%) was way out front, but Shenzhen (+1.50%), South Korea (+1.25%), Japan (+1.21%), and Taiwan (+1.18%) also dragged the rest of the region higher. In Europe, we see a similar picture taking shape with only Russia (-0.48%) in the red at midday. The CAC (+1.30%), DAX (+1.20%), and FTSE (+0.91%) lead on volumes as always but some of the smaller bourses have moved even more in early afternoon trade. In the US, as of 7:30 am, Futures are pointing toward a gap higher to start the day. The DIA implies a +0.56% open, the SPY is implying a +0.53% open, and the QQQ implies a +0.53% open on elation that the US will not default (which would have crashed the global economy). At the same time, 10-year bond yields are slightly higher at 3.608% and Oil (WTI) is up 1.70% to $71.27 per barrel in early trading.

The major economic news events scheduled for Friday include May Avg. Hourly Earnings, May Nonfarm Payrolls, May Private Nonfarm Payrolls, May Participation Rate, and May Unemployment Rate (all at 8:30 am). There are no major earnings reports scheduled for the day, either before the open or after the close.

In miscellaneous news, the Fed reported after the close Thursday that Bank borrowing from its emergency lending programs fell again this week to $285.7 billion (from $288.7 billion the week prior. This was also far below the peak of $343.7 billion borrowed the week of the SIVB collapse in March. This decrease also helped the Fed’s Balance Sheet to decline $51 billion to $8.349 trillion last week. Elsewhere, CNBC reports that early this morning WMT announced it is switching its e-commerce and customer pickup packaging to replace plastics with recyclable paper mailers and boxes. At the same time, Bloomberg reports that major financial sector names are in a “talent arms race” where JPM is leading big banks in hiring AI-related talent (but most of the other usual suspects in that group are wearing out horses to catch up) and major hedge funds are spending millions of dollars in signing bonuses and offering larger cuts of trading profits to hire and retain top trading talent.

With that background, it looks like the Bulls are breaking all three major index ETFs up out of their recent trading ranges. The DIA is trading back above its T-line and arguing with a potential resistance level as is the QQQ at this hour, while SPY has a little more room to run before it contends with a potential level at highs not seen since mid-August of last year. However, there is some volatility in premarket action. Remember that traders are thrilled that default is off the table but there is still a lot of data coming at 8:30 am that may change the market outlook. So, traders remain apprehensive. Not that it matters this morning but SPY and DIA have no T-line extension problem as of now while the premarket move has QQQ getting a bit extended again. On the T2122 front, that indicator tells us we are in mid-range and have plenty of room to run (in either direction). Be prepared for volatility and remember that it’s Friday. So, pay yourself (take profits), move stops, and hedge yourself for the weekend. With all that said, the Bulls have the whip hand so far this morning.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Subdued

Trading was subdued as we wrapped up May with only the QQQ producing a monthly gain with just a handful of tech giants doing the work. The bears showed a little more effort early in the day but the bulls once again staged a late-day rally while waiting for a debt ceiling vote. Now that the bill has passed the House it is on to Senate for more wrangling and deal-making that could last through the weekend. Combine that with a busy morning of economic data and some notable earnings reports traders should prepare for just about anything as June trading begins.

While we slept Asian markets traded mixed but mostly higher responding bullishly to the debt ceiling vote in the House. European markets are also seeing a relief rally after hitting 2-month lows yesterday on an inflationary decline to 6.1% which was better than expected. U.S. futures recovered from modest overnight lows suggesting a bullish open ahead of a busy economic calendar and a smattering of earnings reports.

Economic Calendar

Earnings Calendar

Notable reports for Thursday include AVGO, CAL, CVGW, CHPT, COO, DELL, DBI, DG, FIVE, HRL, LULU, M, MDB, S, VMW, ZS, & ZUMZ.

News & Technicals’

The U.S. Congress has taken a major step to avoid a default on its debt obligations. On Wednesday night, the House of Representatives passed the Fiscal Responsibility Act, which would raise the debt ceiling until December 2022. The bill was the result of a bipartisan agreement between House Speaker Kevin McCarthy and President Joe Biden, who praised the lawmakers for their “courage and compromise”. The bill now heads to the Senate, where Majority Leader Chuck Schumer vowed to “do everything we can to move the bill quickly” and prevent a catastrophic economic crisis.

The inflation pressure in the eurozone eased slightly in May but remained well above the European Central Bank’s target. According to official data released on Thursday, the annual headline inflation rate in the 19-country bloc dropped to 6.1% from 7% in April, defying analysts’ expectations of 6.3%. The core inflation rate, which excludes volatile food and energy prices, also fell to 5.3% from 5.6%. Despite the moderation, investors still anticipate the ECB to tighten its monetary policy further in the coming months, as it has already raised its key interest rate twice this year to curb inflation to its 2% goal.

The global market mood was subdued on Thursday as investors weighed a mixed bag of economic data and corporate earnings. U.S. stocks fell for a second day, with the Nasdaq being the only major index to post a monthly gain in May, thanks to a handful of tech giants that led the rally. Commodities also retreated, as China’s manufacturing sector showed signs of weakness despite easing pandemic restrictions, dampening the demand for oil and metals. Meanwhile, U.S. Treasury yields declined, with the 10-year yield hovering around 3.6%, but the yield curve remained inverted, signaling a pessimistic outlook for growth. Today along with some notable earnings reports we face a big morning of possible market-moving economic data so prepare for some volatility on our first trading day in June.

Trade Wisely,

Doug

BYOB Member’s e-Learning 5-30-23

Much Data and Debt Ceiling Bill Moves On

Wednesday started off with a Bearish gap (down 0.45% in the SPY, down 0.30% in the DIA, and down 0.48% in the QQQ). The two large-cap index ETFs continued lower for the first hour, reaching the lows of the day at about 10:30 am before grinding sideways until about 1 pm. At that point, the bulls led a rally back up to the opening level by 2 pm and then another sideways chop into the close. Meanwhile, QQQ rallied the first 30 minutes of the day, fading the opening gap before the Bears stepped back in at 10 am. The tech-heavy NASDAQ reached the lows of the day at about 11:30 am and then also ground sideways until 1 pm before rallying back to the opening level at about 1:35 pm. From there, we saw a much wavier sideways action all the way into the close. This action gave us gap-down Doji candles in all three major indices. The QQQ is still well above its T-line (8ema), while the SPY retested its T-line (from above) and held on the day. The DIA retested its own T-line from below and remained below that level..

On the day, seven of the 10 sectors were in the red with Energy (-1.78%) way out in front pulling the rest of the market lower while Utilities (+0.72%) and Healthcare (+0.67%) held up better than the other sectors. At the same time, SPY lost 0.68%, QQQ lost 0.57%, and DIA lost 0.30%. VXX fell 0.78% on the day to end at 34.46 and T2122 fell just into the oversold territory at 17.77. 10-year bond yields fell again to 3.645% while Oil (WTI) plummeted another 2% to end the day at $68.02 per barrel. So, Wednesday was a bearish day as markets seemed to fear that the House won’t get the Debt Ceiling bill passed and that might give MAGA Senators the ability to stall the deal in the Senate past the deadline causing a debt default. However, as the day progressed, House Democrats helped Speaker McCarthy get the bill to a floor vote last night. So, traders were left unsure and that gave us an indecisive day on the Bearish side of neutral. This all happened on average volume across the three major indices.

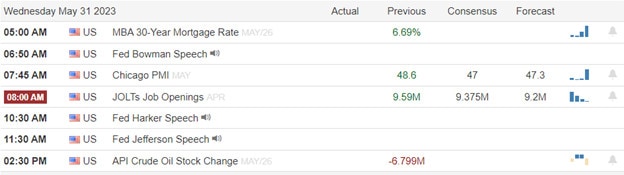

In major economic news Wednesday, the May Chicago PMI came in well below what was expected at 40.4 (compared to a forecast of 47.0 and the April reading of 48.6). This was the worst reading in six months and indicates there is a contraction in the Manufacturing sector in the Chicago region. Later, the April JOLTs Job Openings number was higher than anticipated at 10.103 million (versus a forecast of 9.775 million and a March value of 9.745 million). The new openings came mostly in Retail, Healthcare, Transportation, and Warehousing. After the close, the API Weekly Crude Oil Stock Report showed a significant unexpected inventory build of 5.202-million-barrels (compared to a forecast of a drawdown of 1.220-million-barrels and a vast swing from the previous week’s 6.799-million-barrel drawdown).

SNAP Case Study | Actual Trade

In Fed speak, early Wednesday Cleveland Fed President Mester (hawk, not a voter) told the Financial Times that (in her estimation) the FOMC does not have a “compelling reason” to pause on its interest rate hikes at the upcoming June Meeting. A bit later, Fed Governor Bowman (hawk and voter) told a Boston audience that she thinks the rebounding residential housing market could impact how the Fed acts next in the inflation fight. She said the Fed has been waiting on falling rents to have an impact on headline inflation numbers, but real estate prices have been rising. However, she said that now home prices have been “leveling out recently, which has implications for our fight to lower inflation.” (She did not explain how or when it might impact decisions.) On the other side, Philly Fed President Harker (borderline dove and voter) said he is in the pause camp. He told an event Wednesday afternoon, “I think we can take a bit of a skip for a meeting,” … “I am definitely in the camp of thinking about skipping any increase at this (coming) meeting.” Finally, Fed Governor Jefferson (hawk and voter) said, “A decision to hold our policy rate constant at a coming meeting should not be interpreted to mean that we have reached the peak rate for this cycle,” which has been taken as hawk approval of a pause.

In stock news, INTC’s CFO relieved some market fear over sales as he told an investor conference that he sees Q2 Revenue tracking at the upper end of previous guidance. (The fear came from the fact INTC has no AI products and is not participating in the recent AI-chip craze.) Later, WMT announced shareholders had sided with the CEO and defeated all nine investor-proposed proposals (including revealing China risk exposure, conducting an independent safety review, and disclosing company political contributions). Elsewhere, TSLA has begun shipping its cars to customers with only a 50% charge (and also giving the customer TSLA Supercharging credits) as a safety measure. At the same time, the CEO of F said that his company’s cost to produce electric vehicles may not drop to match its cost to produce gasoline vehicles until 2030. (Analysts had been projecting cost parity by 2025.) At the close, DOW announced it is cutting its Q2 revenue forecast while citing slower macroeconomic growth (specifically noting weaker Chinese demand) and weaker market prices. After the close, Reuters reported more than 100 AMZN corporate employees walked off the job in protest of the company’s “return to office” and climate policy changes on Wednesday afternoon. (This work stoppage only happened in Seattle, but more than 1,900 AMZN employees globally have pledged to protest over those issues.) Also in after-hours news, LCID announced it has raised $3 billion through a new equity offering (the majority bought by the Saudi Sovereign Wealth Fund). Finally, the Biden Administration has agreed to let GE build jet engines for Indian military aircraft. (The agreement will be announced during President Biden’s June 22 visit to India.)

In stock legal and regulatory news, CHWY won a US Appeals Court case, invalidating the company’s 2019 $13,000 fine related to workplace safety after the death of an employee. The ruling said, “The retail industry as a whole lacked notice of the engineering reconfiguration requirements that OSHA now alleges are mandatory”. Later, AMZN agreed to pay the FTC $25 million to settle allegations it has violated children’s privacy rights by having the Alexa voice assistant constantly monitoring conversations. In a separate case, the AMZN agreed to pay the FTC $5.8 million for violating privacy by having its Ring Doorbell system include cameras that were placed in the bedrooms and bathrooms of female customers in 2017 (again, constantly recording and sending data to the company). Meanwhile, META threatened to remove all “news” content from the view of users in the state of CA. This came in reaction to a CA state bill that would require online platforms to pay news publishers a usage fee for republishing their news stories (the same issue that has been faced in Australia, Canada, and Europe). Elsewhere, BA said it is taking a “considerable amount of time” to get FAA approval of the company’s 737 MAX 7 and 10 planes. The company spokesman went on to say they “hope” the 737 MAX 7 will still be certified by the end of this year and 737 MAX 10 certification is projected still to be sometime in 2024. (LUV has already pushed back plans to have the 737 MAX 7 in service into 2024 after initially having it scheduled to be in service this summer.) After the close, the NHTSA announced that F has recalled 142,000 2015-2019 Lincoln SUVs over fire risk. At the same time, a new trial over JNJ talc asbestos claims began in CA. This overrides the company’s attempt to settle claims and avoid liability via the “Texas Two-Step Bankruptcy” of a subsidiary.

In debt ceiling news, the Congressional Budget Office (nonpartisan) announced late Tuesday that the new work requirements the GOP had said would save money, would actually cost money because the agreement exempted veterans and the homeless. This complicated things on the GOP side, reducing what they can claim when talking to their supporters. Later, 52 House Democrats crossed the aisle to vote with the majority of GOP members in a procedural vote which allowed a final floor vote. Then last night, after hours of tedious posturing speeches, the House did pass the bill 314-117 with the support of 165 Democrats and 149 Republicans (bipartisan support). After this vote was finalized, late last night Senate Majority Schumer stood in a virtually empty Senate chamber to place the bill on the calendar for today. Senate leaders of both parties hope to see the bill passed within 48 hours. However, the Senate rules make it easy for a single Senator to grind the process to a halt. And, at least two Senators (Lee and Rand) have publicly said they want to see the bill stopped. So, the solution seems to be progressing. However, it’s not quite a done deal yet.

After the close, CRM, JWN, CHWY, PVH, NTAP, PSTG, VEEV, CRWD, and OKTA all reported beats on both the revenue and earnings lines. Meanwhile, NGL and VSCO both missed on both the top and bottom lines. CRM, VEEV, and OKTA all raised their forward guidance while VSCO lowered its guidance.

Overnight, Asian markets were mixed. New Zealand (+0.87%) and Japan (+0.84%) were by far the largest gainers. Meanwhile, Thailand (-0.79%) was by far the biggest loser on the day. In Europe, the bourses are green across the board at midday. The DAX (+1.11%), CAC (+0.67%), and FTSE (+0.39%) are leading the region higher in early afternoon trade. In the US, as of 7:30 am, Futures are pointing toward a start to the day just on the green side of flat. The DIA implies a +0.03% open, the SPY is implying a +0.24% open, and the QQQ implies a +0.20% open at this hour. At the same time, 10-year bond yields have risen to 3.664% and Oil (WTI) is down another seven-tenths of a percent to $67.63 per barrel in early trading.t.

The major economic news events scheduled for Thursday include ADP May Nonfarm Employment Change (8:15 am), Weekly Initial Jobless Claims, Q1 Nonfarm Productivity, and Q1 Unit Labor Costs (all three at 8:30 am), May Manufacturing PMI (9:45 am), ISM May Mfg. PMI (10 am), EIA Crude Oil Inventories (11 am), Fed Balance Sheet, and Bank Balances with the Fed (both at 4:30 pm). We also get a Fed speaker (Harker at 1 pm). The major earnings reports scheduled for the day are limited to BILI, DOOO, CAL, DG, HRL, M, and SPTN before the open. Then after the close, AVGO, COO, DELL, FIVE, and LULU report.

In economic news later this week, on Friday, we get May Avg. Hourly Earnings, May Nonfarm Payrolls, May Private Nonfarm Payrolls, May Participation Rate, and May Unemployment Rate. In terms of earnings reports later this week, there are no major reports scheduled for Friday.

In miscellaneous news, DB released a study Wednesday saying a wave of bank loan defaults is imminent in the US and Europe. The study expects the peak of defaults to be in Q4 of 2024 and cites the “fastest monetary tightening cycle in 15 years” as the primary cause. With that said, the study said default risks are higher in the US than in Europe and it estimates an 11.3% peak default rate for loans in the US. In a related story, the FDIC said Wednesday that it has added four lenders to its confidential list of “problem banks,” increasing the number on the list to 43. Elsewhere, after all the Fed speak on Wednesday, traders dramatically shifted the probabilities (based on Fed Fund Futures) of a rate hike at the upcoming June 14 Meeting. The Fedwatch Tool tells us this morning 72% of traders expect no rate change with 28% still expecting another quarter-point hike.

So far this morning, M, DOOO, and BILI all reported beats on both the revenue and earnings lines. Meanwhile, HRL, SPTN, and CAL all reported misses on revenue but beat on the earnings lines. Unfortunately, DG missed on both the top and bottom lines. So far, there have been no changes made to guidance. In terms of surprises, M gave us the only significant shock with a 22% upside surprise on earnings (even though that number also represented a 48% earnings decline).

With that background, it looks like the market is still undecided this morning, giving us a premarket candle inside Wednesday’s candle at this point. The DIA seems to want to retest its T-line from below while the QQQ may be thinking about working on a J-hook pattern. For its part, the SPY is just treading water this morning. Perhaps traders are waiting on all the data to come later this morning. The QQQ is a little closer to its T-line than it has been but remains the most extended of the three major index ETFs. Meanwhile, the T2122 indicator is now just inside the oversold territory. Just remember, the economic data is likely to revive talk about whether the Fed will hike rates again in two weeks and news out of the Senate (related to stalling the Debt Ceiling bill) may throw a wet blanket on the Bulls. So, be cautious and ready for volatility.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Enthusiasm Faded

Monday began inspired by a compromise in Congress but the early enthusiasm faded as the path passage looks to have a challenging and uncertain outcome. However, a late-day rally led once again by the very extended tech giants left indexes little changed by the close. Today we have several Fed speakers, Chicago PMI, JOLTS, the Beige Book, and several notable earnings reports to inspire the bulls or bears. Unfortunately, it will be the news about the progress or lack thereof that’s likely to determine the deminer of the market as we wait.

Asian markets traded sharply lower overnight as China’s factory activity numbers disappointed and new signs of real estate defaults reemerge shaking the confidence of recovery. European markets also trade red across the board as they monitor the political wrangling in Congress. U.S. futures though off of their overnight lows continue to point to a bearish open ahead of earnings and economic data with plenty of Fed speak tossed in for good measure.

Economic Calendar

Earnings Calendar

Notable reports for Wednesday include AAP, AI, CPRI, CHWY, CONN, CRWD, CRM, DCI, FRO, GME, NTAP, JWN, OKTA, PSTG, TCOM, and VSCO.

News & Technicals’

The U.S. Congress moved closer to averting a historic default on Monday as a bipartisan bill to raise the debt ceiling cleared a crucial hurdle in the House of Representatives. The bill, which would suspend the debt limit until December 2022, passed the House Rules Committee with the support of Rep. Tom Massie, a key Republican swing vote who had previously opposed raising the debt ceiling. The bill now heads to the full House for a final vote, where it is expected to pass with mostly Democratic votes. The Senate had already approved the bill last week with 50 Democrats and 14 Republicans voting in favor. The compromise bill came after weeks of tense negotiations and brinkmanship between the two parties over how to address the debt ceiling, which is the legal limit on how much the federal government can borrow to pay its bills. If Congress fails to raise or suspend the debt ceiling by Monday, the U.S. Treasury would run out of cash and be unable to pay its obligations, triggering a default that could have catastrophic consequences for the global economy.

The CEO of JPMorgan Chase & Co, Jamie Dimon, urged the leaders of the U.S. and China to talk more and solve their problems on Wednesday. He said this during his first trip to China since he said sorry for making a joke about China’s ruling party in 2021. Dimon said the U.S. and China are the biggest economies in the world and they have some issues about trade and security that can be fixed. He said they should not cut off their ties but try to make them safer. Dimon’s bank wants to grow more in China and it was the first foreign bank to own all of its securities business there. The U.S. and China have not been getting along well for a long time and they have been arguing about many things. Last week, some officials from both sides met and talked about trade. On Tuesday, the U.S. said a Chinese plane was too aggressive when it flew near a U.S. plane over the sea.

After a positive start, enthusiasm faded learning that the debt deal had a difficult road to passage whipsawing prices and keeping uncertainty high. The S&P 500 finished flat on Tuesday following news that a tentative agreement on the debt limit has been reached in Washington. Global equities were generally mixed on the day, as were commodities with gold moving higher and oil lower. Interest rates were down with the 10-year Treasury yield back near 3.7%. The technology sector was once again the decisive leader with a handful of tech giants doing most of the work. Today Fed member talk increases with Chicago PMI, JOLTS figures, and the Beige Book this afternoon. Traders will also have some notable earnings to inspire the bulls and bears as we wait on demagoguery and political gamesmanship driving market emotions to end.

Trade Wisely,

Doug

Tentative Debt Agreement

The President came to a tentative debit agreement over the long weekend providing some bullish premarket inspiration. However, tentative is the keyword here as the R’s and D’s in the congressional bodies try to pass the 2-year deal by Wednesday. I wouldn’t be surprised if we experience some substantial whipsaws as they let the rhetoric fly adding uncertainty to the process. After Friday’s rally on the disappointing Core PCE numbers we face a big week of Jobs data, a declining number of earnings events, and the question of can big tech giants continue to rally on all the AI without a correction.

Asian markets traded mostly higher overnight as they wait on the key U.S. debt vote later this week. European markets appear a bit more tentative as they wait for Congress trading mixed this morning. However, U.S. futures continue to power higher this morning driven mostly by the tech giants continuing to shrug off Friday’s rising inflation data. Watch for possible a whipsaw after the morning gap.

Economic Calendar

Earnings Calendar

Notable reports for Tuesday include AMBA, BOX, CGC, HPE, HPQ, & SPWH.

News & Technicals’

Stocks are set to rise on Tuesday after a deal to raise the debt ceiling for two years was reached by Biden and McCarthy. The deal needs Congress’s approval by Wednesday to avoid a default by June 5. Investors are relieved by the deal amid inflation and banking woes.

North Korea has confirmed its plan to launch a military spy satellite in June, which it claims is needed to monitor the U.S. and its allies’ military activities in the region. The announcement has raised alarm among neighboring countries, especially Japan, which has ordered its forces to shoot down the satellite or any debris if they enter its territory. The launch is seen as a provocation by North Korea, which has been testing missiles and nuclear weapons since 2022 in defiance of U.N. sanctions. The launch also coincides with the 70th anniversary of the U.S.-South Korea alliance, which has been conducting joint military exercises near the border with North Korea. The launch news has boosted the shares of South Korean defense companies, such as Firstec, Victek, and Korea Aerospace Industries, which rose by 3.8%, 3.3%, and 0.6% respectively on.

The war between Russia and Ukraine escalated on Tuesday as Moscow reported a drone attack on its capital that damaged several buildings and injured two people. The Russian Defense Ministry accused Kyiv of being behind the attack, which it said involved eight drones that were all shot down by air defenses. Ukraine has not commented on the allegation. The drone attack came after Kyiv suffered three Russian bombardments in 24 hours, killing one woman and wounding 13 others. The Ukrainian authorities said the attacks were carried out by missiles and drones launched by Russia.

As we begin a holiday-shortened week the bulls are inspired due to the tentative debt agreement between the President and Speaker. Now comes the task of passing the 2-year deal by Wednesday so I would not rule out some substantial whipsaws as the rhetoric flies between the R’s and D’s along the way. With the number of earnings declining markets will have a lot of jobs data to react to this week as traders grapple with the next FOMC rate decision coming up on June 14th after the disappointing Core PCE last Friday. Can giant tech continue to rise on AI hopes without a correction? We will soon find out, so buckle up for another wild week.

Trade Wisely,

Doug

Debt Deal And CB Consumer Sentiment

Markets opened modestly higher on Friday (gapping up 0.17% in the SPY, up 0.30% in the QQQ, and up just 0.12% in the DIA). However, this open just fueled the Bulls to rally strongly until 11 am in all three major indices. At that point, the two large-cap index ETFs ground sideways (with a very slight bullish trend in the SPY and a slight Bearish trend in the DIA) for the rest of the day. At the same time, QQQ trended modestly higher from 11 am to 3:15 pm, before taking profit the last 45 minutes of the day. This action gave us gap-up large white-bodied candles with smaller upper wicks in all three major index ETFs. The DIA also printed a Morning Star signal (while just failing to close above its T-line (8ema) after a retest. SPY did cross back above its T-line and QQQ is now very extended above its T-line.

On the day, all 10 sectors were in the green with Technology (+2.56%) way out front leading the market higher, and Energy (+0.06%) and Healthcare (+0.10%) lagging way behind the other sectors. At the same time, the SPY gained 1.30%, DIA gained 0.94%, and QQQ gained 2.56%. VXX dropped 3.83% on the day to end at 35.65 and T2122 climbed back up into the mid-range at 50.84. 10-year bond yields fell slightly to 3.81% while Oil (WTI) gained 1.32% to end the day at $72.78 per barrel. So, Friday was the Tech Bulls’ Day again, with TSLA (+4.72%), AMD (+5.55%), and AMZN (+4.44%) pulling the rest of the QQQ and SPY upward on the promise of AI-based chip sales after a blowout report from MRVL. Fear of a US Debt Default fell off as all day the reports said a deal was very close. This all happened on greater-than-average volume in the QQQ and DIA and slightly below-average volume in the SPY.

In major economic news Friday, April Durable Goods Orders came in much stronger than expected at +1.1% (compared to a forecast of -1.0% but still much weaker than the March reading of +3.3%). At the same time, the April PCE Price Index also came in stronger than expected on the annual rate at + 4.4% year-on-year (versus a forecast of +3.9% and a March value of +4.2%). On the month-on-month metric, April PCE Price Index came in right on target at +0.4% (against a forecast of +0.4% but still stronger than the March +0.1% reading). Meanwhile, the April Personal Spending month-on-month came in very hot at +0.8% (versus the forecast of +0.4% and much higher than the March reading of +0.1%). On the business side, Preliminary April Retail Inventories showed a decline of 0.1% (compared to the March 0.1% increase). Later in the morning, Michigan Consumer Sentiment came in higher than anticipated at 59.2 (versus a forecast of 57.9 but still less than the April value of 63.5). These measures show a stronger consumer than economists have been expecting with a slightly better outlook for the future.

SNAP Case Study | Actual Trade

In stock news, the IPO of ATMU, Atmus Filtration Technologies (a spinoff of CMI), opened at $21.67 and closed at $22.40 after pricing at $19.50/share on Thursday night. CMI raised $275 million from the IPO and retains 83% control of the company. Meanwhile, Mexican President Lopez Obrador said Friday that his government may buy up 50% of the stock in Banamex (the C Mexican subsidiary, which C announced Wednesday it would spin off via IPO). He told the press Mexico has $3 billion for this purchase and if his stock valuation is anywhere near correct it means C will take a major hit on the unit (which it purchased for $12.5 billion in the early 2000s). On Saturday, MSFT announced it will discontinue some of its hardware products like ergonomic keyboards. Elsewhere, in a potential blow to major importers (AMZN, DOLE, TGT, WMT, FDP, LOW, HD, etc.) the Panama Canal has ordered ships to lighten their loads and also increased transit fees due to a severe drought lowering the level of lakes used to flood docks over the course of the canal.

In stock legal and regulatory news, a US judge approved $50 million settlement of a class-action lawsuit against AAPL over defective MacBook keyboards. Elsewhere, MSFT laid out the grounds of its appeal against the British Competition and Markets Authority’s veto of the company’s acquisition of ATVI. MSFT said its appeal is based on “fundamental errors” in the CMA’s assessment of the company’s cloud gaming services. At the same time, six major European insurers have quit the Net-Zero Insurance Alliance (aimed at forestalling climate change by committing to reduce greenhouse gases) in the 36 hours prior to the Friday close. The insurers all cited US Republican political attacks (on behalf of fossil fuel industries) as the GOP has prioritized the financial health of those industries over climate. Bank of England Governor (and co-chair of the COP26 project) Carney decried the losses and warned the political attacks are now interfering with the Insurance industry’s ability to price climate risk, harming their investors, policyholders, and the local governments that will suffer climate impacts. Meanwhile, ETRN’s long-delayed Mountain Valley natural gas pipeline (in WV and VA) was dealt another legal blow Friday. The US District Court in DC ruled that the US Federal Energy Regulatory Commission had “inadequately explained its decision not to prepare a supplemental environmental impact statement” (that would address the) “unexpectedly severe erosion and sedimentation along the pipeline’s right-of-way.” Later, PFE and MRNA were sued by ALNY over patent infringement related to the two company’s COVID-19 vaccines. The ALNY suit seeks unspecified damages, but PFE made $37.8 billion and MRNA made $18.4 billion from the sale of the vaccines in question. Finally, a San Francisco Federal jury awarded SONO $32.5 million in its suit against GOOGL over patent infringement related to wireless audio devices.

In debt ceiling news, on Friday, Treasury Sec. Yellen announced that numbers were refined and it has now been determined that June 5 would be the actual date of default (as opposed to “as soon as June 1”). However, by Saturday afternoon, the two sides had reached an agreement. The deal increases the debt ceiling enough to avoid a similar situation for two years. It raises defense spending by a whopping 11% over 2023 even kicking in an additional (unexpected) 3% while keeping non-defense spending roughly flat in 2024 (versus ’23 levels) and then increasing it by 1% in 2025. The deal phases in some work requirements for SNAP (food stamps) but then ends those same work requirements in 2030. It also rescinds about $30 billion in unspent COVID-19 aid (not to include veterans’ medical care or $5 billion for creating the next generation of vaccines and treatments). The agreement also calls for a “lead environmental agency” to develop new comprehensive environmental reviews intended to appease the oil and gas industry by theoretically speeding up project approvals.

Nobody wins or loses a negotiation. However, based on reactions, it appears the MAGA faction of Republicans believes they lost. There is enough there for them to claim credit (such as reducing IRS staffing). However, the lack of reality in what they promised “they” would do and the fact that outrage is their political style likely means they were always going to be “the loser” of any deal. On the other side, many of the most Progressive Democrats may well feel similarly (related to work requirements on SNAP and the loss of funding to increase IRS enforcement on the top one percent). However, at least as of now, that group has expressed their concerns in a less bombastic way. For the markets, it is expected that we do see those extremists (maybe both sides, but the GOP side is the one to watch) threaten to kill or at least delay a vote on the deal until there is a default. Concerningly for us traders, I have heard commentators imply that the President and Speaker are counting on market turmoil to apply pressure to the extremists and get the bill turned into law. That may mean the war of words is not over…or may ramp up this week. Votes are scheduled to begin on Wednesday in the House.

Overnight, Asian markets were mixed and split evenly in number. South Korea (+1.04%) was by far the biggest gainer while Malaysia (-0.57%) lost the most. All of the other exchanges fell in the middle on modest moves. Meanwhile, in Europe, we see a similar story taking shape at midday. The DAX (+0.56%), CAC (-0.36%), and FTSE (-0.50%) lead a mixed region with on massive moves underway in early afternoon trade. In the US, as of 7:30 am, Futures are pointing to a green start to the morning. The DIA implies a +0.14% open, the SPY is implying a +0.55% open, and the QQQ implies a +1.13% open at this hour. At the same time, 10-year bond yields are down sharply to 3.719% and Oil (WTI) is off 1.13% to $71.85 per barrel in early trading.

The major economic news events scheduled for Tuesday are limited to Conference Board Consumer Confidence (10 am). The major earnings reports scheduled for the day are limited to ESLT and SKY before the open. Then after the close, HPE, HPQ, YY, AND UHAL report.

In economic news later this week, on Wednesday, we get Chicago PMI, April JOLTs Job Openings, Fed Beige Book, API Weekly Crude Oil Stocks Report and two Fed speakers (Bowman and Harker). Then Thursday, ADP May Nonfarm Employment Change, Weekly Initial Jobless Claims, Q1 Productivity, Q1 Unit Labor Costs, May Manufacturing PMI, ISM May Mfg. PMI, EIA Crude Oil Inventories, Fed Balance Sheet, Bank Balances with the Fed, and a Fed speaker (Harker) are reported. Finally, on Friday, we get May Avg. Hourly Earnings, May Nonfarm Payrolls, May Private Nonfarm Payrolls, May Participation Rate, and May Unemployment Rate.

In terms of earnings reports later this week, on Wednesday, AAP, CAE, CPRI, CD, DCI, HOV, CHWY, CRWD, NTAP, NGL, JWN, OKTA, PSTG, PVH, CRM, and VEEV report. Then Thursday, we hear from BILI, DOOO, CAL, DG, HRL, M, SPTN, AVGO, COO, DELL, FIVE, and LULU. Finally, on Friday, there are no major reports scheduled.

So far this morning, ESLT beat on revenue while missing on earnings. On the other side, SKY missed on revenue while beating on earnings. (TNP reports at 8:20 am.)

With that background, it looks like the Bulls are frisky again this morning in the QQQ and SPY. The tech-heavy NASDAQ will be gapping to levels not seen in 14 months with prices now near the overnight highs similar to how they were in premarket Friday. The SPY is gapping as well but has backed off early highs. Still, an open where it sits now will take the main index ETF back to levels not visited since August of last year. However, the stodgy mega-caps remain just in the red and are at their premarket lows. If we open at this level, DIA will be just under its T-line and not giving the follow-through to the Friday Morning Star that the Bulls would have been hoping to get. QQQ is very extended from its T-line while SPY may also be just a bit stretched (both to the upside). Still, the T2122 indicator sits right in the mid-range, telling us we have some room to run. Just remember, the Debt Ceiling may be agreed upon by leaders but there are plenty of people who may decide it is a better political move to throw a wrench in the works (coincidentally getting a lot of headlines in the process) than it would be to get the bill approved and move on to other business. This is particularly true since the deadline has been shown to not hit until June fifth. So, beware of volatility and news risk.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you