Trading was subdued as we wrapped up May with only the QQQ producing a monthly gain with just a handful of tech giants doing the work. The bears showed a little more effort early in the day but the bulls once again staged a late-day rally while waiting for a debt ceiling vote. Now that the bill has passed the House it is on to Senate for more wrangling and deal-making that could last through the weekend. Combine that with a busy morning of economic data and some notable earnings reports traders should prepare for just about anything as June trading begins.

While we slept Asian markets traded mixed but mostly higher responding bullishly to the debt ceiling vote in the House. European markets are also seeing a relief rally after hitting 2-month lows yesterday on an inflationary decline to 6.1% which was better than expected. U.S. futures recovered from modest overnight lows suggesting a bullish open ahead of a busy economic calendar and a smattering of earnings reports.

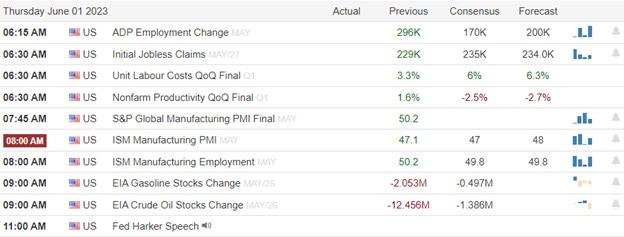

Economic Calendar

Earnings Calendar

Notable reports for Thursday include AVGO, CAL, CVGW, CHPT, COO, DELL, DBI, DG, FIVE, HRL, LULU, M, MDB, S, VMW, ZS, & ZUMZ.

News & Technicals’

The U.S. Congress has taken a major step to avoid a default on its debt obligations. On Wednesday night, the House of Representatives passed the Fiscal Responsibility Act, which would raise the debt ceiling until December 2022. The bill was the result of a bipartisan agreement between House Speaker Kevin McCarthy and President Joe Biden, who praised the lawmakers for their “courage and compromise”. The bill now heads to the Senate, where Majority Leader Chuck Schumer vowed to “do everything we can to move the bill quickly” and prevent a catastrophic economic crisis.

The inflation pressure in the eurozone eased slightly in May but remained well above the European Central Bank’s target. According to official data released on Thursday, the annual headline inflation rate in the 19-country bloc dropped to 6.1% from 7% in April, defying analysts’ expectations of 6.3%. The core inflation rate, which excludes volatile food and energy prices, also fell to 5.3% from 5.6%. Despite the moderation, investors still anticipate the ECB to tighten its monetary policy further in the coming months, as it has already raised its key interest rate twice this year to curb inflation to its 2% goal.

The global market mood was subdued on Thursday as investors weighed a mixed bag of economic data and corporate earnings. U.S. stocks fell for a second day, with the Nasdaq being the only major index to post a monthly gain in May, thanks to a handful of tech giants that led the rally. Commodities also retreated, as China’s manufacturing sector showed signs of weakness despite easing pandemic restrictions, dampening the demand for oil and metals. Meanwhile, U.S. Treasury yields declined, with the 10-year yield hovering around 3.6%, but the yield curve remained inverted, signaling a pessimistic outlook for growth. Today along with some notable earnings reports we face a big morning of possible market-moving economic data so prepare for some volatility on our first trading day in June.

Trade Wisely,

Doug

Comments are closed.