The Indexes whipsawed on Friday began with a bit of bullish hope on the better-than-expected Core PCE reading but that hope quickly faded on a failed vote budget vote in the house. However, with 3 hours to spare Congress passed a 45-day extension kicking the problem down the road to provide the market with more uncertainty during the 4th quarter earnings season. Today we have PMI, ISM, and Construction Spending figures to inspire the bulls and bears. Plan for price action to remain challenging with a big week of job numbers while waiting for the big bank reports to kick off 4th quarter earnings silly season.

Asian markets trade mixed after China reported an improvement in factory activity surging Hong Kong higher by 2.51%. However, eurozone manufacturing continued to decline bringing in modest selling across European indexes to begin the week. With U.S. manufacturing numbers pending U.S. futures work to recover some early loss as they chop around the flatline while relieved over no government shutdown, at least for now.

Economic Calendar

Earnings Calendar

There are no notable earnings reports to begin the first trading day of the 4th quarter.

News & Technicals’

Bill Ackman, the billionaire investor and founder of Pershing Square Capital Management, has expressed his interest in doing a deal with X, the social media platform formerly known as Twitter. Ackman’s new investment vehicle called a SPARC, or special purpose acquisition rights company, received approval from the Securities and Exchange Commission (SEC) on Friday. A SPARC is a type of blank-check company that allows investors to buy shares in a future merger or acquisition deal, without knowing the target company in advance. Ackman told The Wall Street Journal that he would “absolutely” do a deal with X if the opportunity arises. Ackman is an active user of X, where he posts about various topics, such as his support for the presidential candidates Vivek Ramaswamy and Robert Francis Kennedy Jr. Ramaswamy is a former biotech executive and author of the book Woke, Inc., while Kennedy is an environmental lawyer and activist. Ackman said he admires both candidates for their courage and integrity.

China, the world’s largest consumer of many commodities, has been showing a strong appetite for various raw materials, despite the slowdown in its overall economic growth. Goldman Sachs, a global investment bank, said in a recent note that China’s demand for commodities such as iron ore, copper, aluminum, oil, and gas has been growing at “robust rates” in the past few months. The bank attributed this to several factors, such as the recovery of industrial activity, the expansion of infrastructure spending, the resilience of the property sector, and the diversification of energy sources. The bank also said that China’s demand for commodities is likely to remain high in the near term, as the country faces supply constraints and environmental challenges. However, the bank also warned that China’s demand for commodities could moderate in the longer term, as the country shifts to a more consumption-driven and low-carbon economy.

The World Bank, an international financial institution that provides loans and grants to developing countries, has lowered its growth forecast for developing East Asia and the Pacific for this year and the next. The region, which includes countries such as China, Indonesia, Thailand, and Vietnam, is expected to grow by 5% in 2023, down from the previous estimate of 5.1%. The growth projection for 2024 has also been revised down from 4.8% to 4.5%. The World Bank said that the region’s growth prospects are facing several risks, such as the uncertainty of the pandemic, the uneven recovery of global trade and investment, and the rising debt levels of governments, corporations, and households. The World Bank urged the countries in the region to adopt prudent fiscal and monetary policies, strengthen their health systems and social protection, and promote green and inclusive growth.

Equity markets began Friday with a nice gap up reacting to the Core PCE numbers but, after a failed vote to prevent a government shutdown indexs whipsawed finishing the day lower with uncertainty. The S&P 500 lost about 4.8% in September and about 6.4% since its peak on July 31. The Nasdaq suffered more losses, falling by 5.5% in September and by 7.5% since July 31. The bond market was stable on Friday, with the 10-year Treasury yield at 4.58%, close to its highest level in the cycle. The bond yields have risen sharply in September, by nearly 0.5% for the 10-year bond, affecting both stock and bond returns. Today traders have PMI, ISM, and Construction Spending along with some short-term bond auctions to deal with as we kick off the first trading day of the 4th quarter. A relief rally is overdue but expect the price action to remain challenging as we wait for the beginning of the earnings session. Though the government avoided a shutting down we will be dealing with this uncertainty again having kicked the can down the road for 45 days. Price action is likely to remain challenging so pan your risk carefully.

On Friday, markets gapped strongly higher as the Fed’s favorite inflation gauge came in better than expected. The SPY gapped up 0.71%, DIA gapped up 0.65%, and QQQ gapped up 0.98%. However, at that point, the DIA immediately began selling while the SPY traded sideways, and the QQQ continued to rally. This lasted until 10 a.m. when the SPY and QQQ followed the DIA selling off. The selling lasted until all three major index ETFs reached the lows of the day at 2:30 p.m. From that point, the rest of the day saw a sideways grind sideways along the lows with a very, very slight bullish trend. This action gave us black-bodied candles that retested (and failed) their respective T-lines (8ema). In addition, DIA printed a Bearish Engulfing candle, SPY came close to printing a Dark Cloud Cover, and QQQ just printed a large-body, black candle with wicks on both ends. This happened on above-average volume in the DIA and SPY, as well as average volume in the QQQ.

On the day, six of the 10 sectors were in the red led by Energy (-1.51%) way out front leading the other sectors lower. Meanwhile, Consumer Cyclical (+0.42%) holding up better than the other sectors. At the same time, the SPY lost 0.24%, DIA lost 0.50%, and the tech-heavy QQQ gained 0.07%. VXX gained almost 2% to close at 23.32 and T2122 fell but remained just outside the oversold territory at 21.90. 10-year bond yields fell slightly to 4.579% while Oil (WTI) lost just over one percent to end the day at $90.77 per barrel. So, Friday was another whipsaw day that gave us a strong gap-up, which was met by a selloff that ripped the face off of gap chasers. This was not helped when the dysfunctional House GOP failed to pass even their extremist version of a set of appropriations bills, leading to what is likely a government shutdown as of Sunday. The Senate plans to pass a bipartisan funding bill Saturday (after their own GOP troublemaker, Sen. Paul forced the long wait instead of a fast-track Thursday vote after the bill passed 77-19).

The major economic news reported Friday included the August PCE Price Index which came in lower than expected at +0.4% month-on-month (compared to a forecast of +0.5% and a July reading of +0.2%). That amounted to an August PCE Price Index year-on-year of +3.5%, which was in line with the forecast and a tick higher than the July value of +3.4%. The “Core” numbers, which strip out food and energy, on a month-on-month basis were +0.1% (lower than the forecasted and July reading of +0.2%). On a year-on-year basis, the Core number was +3.9% (in line with forecast and down significantly from the +4.3% in July). At the same time, August Personal Spending came in just as predicted at +0.4%, which was down very sharply from the July +0.9% value. Meanwhile, the Preliminary August Trade Goods Balance showed a significantly better than anticipated deficit of -$84.27 billion (compared to a forecast of -$91.20 billion and the prior month’s -$90.92 billion). Preliminary August Retail Inventories came in up 0.6% versus the dead-flat +0.0% in July. Later, September Chicago PMI survey results were a bit below predicted at 66.0 (versus a 66.3 forecast but slightly above the August reading of 65.5).

In Autoworker contract talks and strike news, in a hopeful sign, the UAW dropped its unfair labor practices charges against GM and SLTA on Friday. (The union had filed charges with the NLRB on Aug. 31.) Then in late morning, the UAW expanded the strike, this time hitting a GM plant and an F plant. The added facilities bring 6,900 new workers to the strike, which has now increased to cover 17% of the workers whose contracts are under negotiation (18,300 total out of 146,000). Later, the F CEO Farley said the UAW was “holding a deal hostage” over EV battery plants. UAW President Fain fired back that Farley was “lying about the state of the negotiations,” going on to say the CEO “hasn’t been at the bargaining table this week or for most of the last 10 weeks. If he were there, he’d know we gave Ford a new comprehensive proposal Monday and still haven’t heard back.” (For what it is worth, the CEO of F has previously said he expects massive workforce reductions once the transition to EVs is complete. Perhaps as much as 40% workforce reduction.) Following those lines of contention, GM CEO Barra said she felt “It’s clear that there is no real intent to get an agreement (on the union’s part).”

In government shutdown news, having broken their word from June, the House GOP failed to approve even their own extreme government funding bill Friday. (It would have caused 30% budget reductions in most departments of the government.) However, 21 GOP members voted against the bill, either because it was not extreme enough for them or because they were more interested in political theatre than the situation. One of the most extreme right-wing members (Gaetz) even approached Democrats, trying to strike a deal that would allow him to replace the Speaker with a Freedom Caucus member. Then Saturday, with only 9 hours left (and perhaps in response to Gaetz’s move), Speaker McCarthy reversed course by reaching across the aisle to pass a 45-day CR with Democratic help. The bill passed 335-91, with 126 GOP votes (58%) and 209 (all but 1) of the Democratic votes. The CR removed additional support for Ukraine but, oddly, doubled US disaster relief again. (President Biden asked for $4 billion, the Senate made it $8 billion additional, and the House doubled it again to $16 billion.) The removal of Ukraine aid led to the lone Democratic thumbs down in the House and caused Dem. Senator Bennet to hold up a fast-track vote in the Senate. However, with three hours to spare the Senate approved the House CR bill 88-9 as-is (meaning no reconciliation and re-votes in both houses were needed). Then the President signed the bill shortly before the deadline. Dow futures jumped more than 100 points on the news that the shutdown was averted. The bottom line is that a shutdown was avoided by kicking the can 45 days down the road…and we can now look forward to more drama a week or so before Thanksgiving. In the meantime, Gaetz said he will move to remove McCarthy as Speaker this week for the high crime of reaching across the aisle to Democrats to keep the government open.

In stock news, Reuters reported exclusively Friday that CG is in talks to acquire two units from MDT for more than $7 billion. Sources tell them an agreement could be reached within a few weeks. Elsewhere, the Teamsters Union picketed two AMZN distribution facilities in CA on Friday. At the same time, TSLA announced that one of its semi-trucks traveled over 1,000 miles in a single day. (There was no word about any load. So, it must be assumed it was just the truck with no trailer. For reference, a semi with a load will typically travel 650 miles in an 11-hour shift, which would be about 1,300 in a driver-team day.) Later, Reuters reported that APO is among two finalist investors to acquire bankrupt SAS airline. Monday marks the separation of K from its snack business which will trade under KLG. Industry analyst IQV reported that 1.8 million people got COVID-19 vaccine shots last week, with 1 million getting the PFE shot and 800k getting the MRNA vaccine. RYAAY announced it is reducing its Winter flight schedule, citing BA not delivering promised jets on time. (RYAAY said it now expects to get 14 at most of the 27 aircraft scheduled for delivery in Q4 from BA.) After the close, WFC announced it had sold $2 billion of its private equity investments to a group or private equity firms including CG. Then on Saturday, AAPL announced it will be issuing a software update to address a problem on its newly released iPhone 15, which has caused the phones to overheat. AAPL said the phones are “running hot” due to bugs in iOS 17, a temporary set-up period of the phone, and bugs in apps. On Sunday, AMZN took an image hit as many customers reported receiving email confirmations of gift card purchases, that they never bought. This led the customers to fear account hacking or much more ominously that AMZN may have been hacked. As of Sunday evening, AMZN is still investigating.

In stock government, legal, and regulatory news, the SEC announced Friday that eight more broker-dealers have settled over employees discussing business using off-books messaging channels. IBKR, FITB, PWP, and Nuveen paid a total of $91 million combined. IBKR also paid $20 million to the CFTC over similar charges. At the same time, a federal judge in OH declined to block the Biden Administration from negotiating the price of drugs for the Medicare plan. Elsewhere, MS, BCLYF, and DRW Securities won a dismissal of a private suit alleging the institutions manipulated SPX options linked to the VIX in 2018. The SEC fined D.E. Shaw $10 million for violating whistleblower protection rules. Later, the SEC reported that 10 firms were charged a cumulative $79 million for recordkeeping violations. At the same time, NLRB accused AMZN of violating the terms of a 2021 agreement that required the company to allow workers to unionize if they choose. After the close, HOOD said it expects to see charges of $100 million in Q3 related to regulatory and legal issues. Finally, the US Dept. of Energy is in the final stages of talks to lend $1 billion to LAC to allow the company to build out the largest lithium deposit in the US. The loan is said to provide more than half the funding for the operation.

Overnight, Asian markets were evenly split in number but leaned bullish on the strength of the move. Hong Kong (+2.51%) and Taiwan (+1.24%) were by far the biggest movers and led the region higher as New Zealand (-0.47%) was the biggest loser on the day. In Europe, the bourses are leaning to the res side at midday with only four bourses in the green. The CAC (-0.18%), DAX (-02.7%), and FTSE (-0.26%) lead the region lower with Russia (+0.92%) an outlier to the upside in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a mixed, flat start to the day. The DIA implies a -0.02% open, the SPY is implying a +0.02% open, and the QQQ implies a +0.17% open at this hour. At the same time, 10-year bond yields are moving higher again to 4.631% and Oil (WTI) is up just under another percent to $91.66 per barrel in early trading.

The major economic news scheduled for Monday includes September S&P US Mfg. PMI (9:45 a.m.), September ISM Mfg. PMI and September ISM Mfg. Prices (both at 10 a.m.) We also have three Fed speakers (Chair Powell at 11 a.m., Harker at 11 a.m., and Williams at 1:30 p.m.). There are no major earnings reports scheduled for Monday.

In economic news later this week, on Tuesday we get JOLTs Job Openings and API Weekly Crude Oil Stocks. Then Wednesday we get Sept. ADP Nonfarm Employment Change, Sept. S&P Global Services PMI, Sept. S&P Global Composite PMI, Aug. Factory Orders, Sept. ISM Non-Mfg. PMI, Sept. ISM Non-Mfg. Price Index, EIA Crude Oil Inventories, and Fed member Bowman speak. On Thursday, we get August Imports, August Exports, Weekly Initial Jobless Claims, the Fed Balance Sheet, and two Fed Speakers (Mester at 9 a.m. and Daly at noon). Finally, Friday, Sept. Avg. Hourly Earnings, Sept. Nonfarm Payrolls, Sept. Private Nonfarm Payrolls, Sept. Participation Rate, Sept. Unemployment Rate, and a Fed speaker (Waller at noon).

In terms of earnings reports later this week, on Tuesday MKC, CLM, and NG report. Then Wednesday, we hear from AYI, HELE, and RPM. On Thursday, CAG, STZ, LW, and LEVI report. Finally, on Friday, there are no major earnings reports scheduled.

In miscellaneous news, US crop exports are at risk again as water levels in the Mississippi River have fallen below safe barge traffic levels again. Just like the Panama Canal, barge operators are being forced to carry smaller, lighter loads per barge to avoid grounding. In a related story, the low freshwater level of the river has allowed saltwater to creep up the river from the Gulf of Mexico, endangering or ruining drinking water supplies. The US Army Corps of Engineers has been working on an underwater dam to slow the creep since July and will begin barge delivery of 36 million gallons of fresh water per day to the lower Mississippi area starting this month.

In late-breaking news, CA Governor Newsome appointed Laphonsa Butler to the open interim position to replace Senator Feinstein who died last Thursday. Her seat will be up for election again in November 2024. Elsewhere, in good labor news, the UAW and VOLAF (Volvo, Mack trucks) reached a new labor deal just before midnight last night to avoid a strike. The tentative deal must still be ratified by UAW members. In less good labor news, union healthcare workers of Kaiser Permanente (private) told CNBC is it not likely that the 310,000 workers will reach a deal with management of the healthcare giant. This makes a strike, which has already been authorized by the workers, likely across CA, OR, WA, VA, and Washington DC as soon as Wednesday.

With that background, it looks like the pop from Saturday night’s government shutdown avoidance did not last long. All three major index ETFs opened the premarket with a strong gap higher but have sold steadily since, giving us gap-up large black candles in all three so far in the early session. All three remain below their T-line (8ema) and 50sma. (However, QQQ did gap above before selling back below its T-line this morning.) So, for now, the short-term trend clearly remains headed lower. In terms of extension, none of the three major index ETFs are far below their T-line (8ema) and the T2122 indicator is still just outside of its oversold range. This tells us either side has room to run if they can find the momentum to do so.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

After a very volatile day of price action, indexes closed little change after the Senate passed a temporary spending bill to keep the government open but that is likely dead on arrival in the House wanting to curb the deficit spending. With the worries of a shutdown weighing on investors’ minds, they will have to deal with a GDP, Jobless Claims, a flurry of Fed Speakers that include Jerome Powell as well as a handful of notable earnings reports. The focus will then quickly turn to the Friday Core PCE inflation numbers. Though a relief rally could begin at any time it may prove to be anemic in light of the government shutdown worries. Expect the challenging price action to continue.

Overnight Asian markets closed mixed but mostly lower as rising oil and bond yields and more real estate woes plagued China. European markets have recovered slightly from early lows training around the flatline as leisure stocks suffer from consumer weakness. Ahead of market-moving economic reports, U.S. Futures are trying to put on a positive face despite all the uncertainties ahead. Buckle up it is likely to be another volatile day.

Economic Calendar

Earnings Calendar

Notable reports for Thursday include CAN, BB, KMX, JBL, NKE, and MTN.

News & Technicals’

Oil prices reached their highest level in more than a year, as the supply of crude oil in a major storage hub decreased to its lowest level since last summer. The U.S. West Texas Intermediate (WTI) futures, which are the benchmark for U.S. oil prices, rose to $95.03 per barrel during the Asian trading hours, the highest since August 2020. This was driven by the decline in crude oil inventories at Cushing, Oklahoma, which is the delivery point for WTI futures and the largest storage hub in the U.S. According to the latest data from the Energy Information Administration (EIA), the crude oil stocks at Cushing fell by 3.6 million barrels to 34.8 million barrels in the week ending September 17, the lowest since July 2020. The drop in Cushing stocks reflects the strong demand for crude oil in the U.S., as well as the impact of Hurricane Ida, which disrupted the production and transportation of oil in the Gulf of Mexico. The surge in oil prices also reflects the global recovery in oil demand, as well as the ongoing supply constraints from OPEC+ and other producers.

The labor dispute between the United Auto Workers (UAW) union and the three major U.S. automakers, General Motors, Ford Motor, and Stellantis, is escalating as the union threatens to expand its strikes if the negotiations do not make significant progress by Friday morning. The UAW, which represents about 146,000 workers at the three companies, has been on strike since Sept. 15, after the expiration of their labor contracts on Sept. 14. The strikes currently affect about 18,300 workers, or 12.5% of the UAW members, at several plants across the country. The main issues in the negotiations are wages, health care, job security, and electric vehicle production. The UAW announced last week that it would increase its strikes to more plants if the talks did not advance by Sept. 22. However, as of Tuesday, no breakthroughs have been reported, and the union has set a new deadline of 10 a.m. ET on Sept. 24. If the deadline is not met, the UAW said it will announce more strikes at more plants, potentially disrupting the production and sales of the automakers.

Evergrande, the Chinese property giant that is facing a debt crisis, has suspended its shares from trading on the Hong Kong stock exchange since Sept. 16. This is not the first time that the company has halted its shares from trading. In March 2020, Evergrande also suspended its shares, citing a major restructuring plan. The shares did not resume trading until Aug. 28, 2021, after a 17-month hiatus. However, the company’s troubles did not end there. Earlier this month, Evergrande postponed a meeting with its creditors, where it was supposed to discuss a debt restructuring plan. The company has about $300 billion of debt and has been struggling to pay its suppliers, contractors and investors. The situation has sparked fears of a possible default and contagion in the Chinese and global markets.

The stock market ended a very volatile day with little change, waiting on market-moving economic data and the worries of a government shutdown. The Senate approved a temporary funding bill to prevent a government shutdown, but it looks like it will be dead on arrival at the House of Representatives, which is attempting to curtail the massive deficit spending. Yields also rose, with the 2-year Treasury yield reaching over 5.1% and the 10-year yield closing around 4.6% as the dollar continued to surge higher with the oil sector. Today the bulls and bears will look for inspiration in the GDP, Jobless Claims, and a handful of notable consumer-based earnings. We will also have a flurry of Fed members speaking including Jerome Powell as we wait on Friday’s Core PCE inflation figures. We are overdue for a relief rally but keep in mind if it should begin it could be muted by government shutdown worries.

On Wednesday, markets gapped modestly higher at the open (up 0.26% in the SPY, up 0.23% in the DIA, and up 0.33% in the QQQ). However, then the Bears took over and slowly sold off in a wavy move that eventually took us to the lows of the day at 2:15 p.m. Then the Bulls stepped in to drive an hour-long rally that took the SPY and QQQ to the highs of the day (and the DIA back into the morning gap at 3:15 p.m.). At that point, we saw a modest selloff in the last 45 minutes of the day in all three major index ETFs. This action gave indecisive candles in all three. The SPY printed a black body Doji or small-body Spinning Top candle. The QQQ gave us a long-legged, black-bodied Doji. Finally, the DIA printed a black-body Hammer-type candle. This happened on above-average volume in the DIA and SPY, as well as slightly less-than-average volume in the QQQ.

On the day, the market was split with five of the sectors in the green and 5 in the red as Utilities (-1.83%) way out front leading the other sectors lower. Meanwhile, Energy (+2.26%) way, way out in front (by 1.5%) leading the rest higher. At the same time, the SPY gained 0.04%, DIA lost 0.18%, and the tech-heavy QQQ gained 0.23%. VXX fell hard to close at 23.97 and T2122 jumped back up but remained in the oversold territory at 12.24. 10-year bond yields spiked again to 4.607% while Oil (WTI) also spiked up to end the day at $93.68 per barrel. So, Wednesday was another whipsaw day that seems to have been largely influenced by the impending government shutdown (and its effect on markets). We saw a modest gap up, a long and slow selloff, a sharp rebound, and then one last modest leg down. After all of that, markets ended the day not very far from their Tuesday close.

The major economic news reported Wednesday was limited to August Durable Goods Orders which came in better than expected at +0.2% (compared to a forecast of -0.5% and far better than the July reading of -5.6%). At the same time, August Core Durable Goods Orders came in even better at +0.4% (versus a forecast and July reading of +0.1%). Later the EIA Weekly Crude Oil Inventory Report showed a greater-than-expected drawdown of stocks at -2.170-million-barrels (compared to a forecasted -1.320-million-barrels and the prior week’s -2.135-million-barrels).

In Autoworker contract talks and strike news, the UAW threatened to expand its strike against the Big 3 Automakers on Friday, if significant progress is not made in the meantime. The UAW President will announce the next steps in a streamed videocast at 10 a.m. Eastern Friday. (So far, only about 12% of UAW members have gone on strike.) Later, on Wednesday night, the ex-President talked at UAW members (not to them) when he counter-programmed the GOP Presidential debate by speaking at a non-union auto parts supplier in Detroit. The UAW was not involved in his visit and he was not scheduled to speak to UAW leaders.

In stock news, Reuters reported that the META executive leading the company’s AI Chip program is leaving the company at the end of the month. In related news, META unveiled a new AI assistant to help Facebook users create images, etc. At the same time, LCID opened its new plant in Saudi Arabia on Wednesday. (The Saudi government committed to buy 100,000 vehicles from LCID over the next decade.) The facility will serve the whole Middle East producing 155,000 cars per year. Later, in a twist, cryptocurrency exchange Kraken announced it is planning to offer trading of US-listed stocks and ETFs. Kraken has filed for FINRA licensing as a broker-dealer and is now targeting a launch date in 2024. At midday, VLKAF (Volkswagen) took a major hit with an IT outage in Germany that shut down production of cars across the whole group of brands including Porsche and Audi. Elsewhere, in one of the largest real estate deals so far this year, WFC announced it is investing $550 million in retail real estate in New York City’s 20 Hudson Yards building. (Half a billion doesn’t go as far as it used to as the investment only gets WFC the 5th-7th floors of the building.) At the same time, NYC shares surged in volatile trading after a tender offer from Bellevue Capital Partners. (NYC stock closed up 28.62% after trading in a 44% range on the day.) Later, NEE stock took an 8.23% loss on the day (massive for a utility) after the CEO attributed poor recent company performance to higher interest rates. PTON jumped 30% higher in after-hours trading following the company announcement that it had signed a 5-year partnership with LULU. (The companies agreed to become the exclusive partner of the other, with LULU being the exclusive apparel provider to PTON and PTON being the exclusive digital fitness content provider to LULU.)

In stock government, legal, and regulatory news, controversial hedge fund Citadel has decided to fight the SEC, refusing to turn over employee “off books” private messages in apps like WhatsApp and Signal. The fund (known as the biggest buyer of order flow from brokers) is threatening to sue the SEC to avoid disclosing the (probably damning) information. CG, APO, KKR, BX, and others were served notice to turn over employee “off books” communications at the same time. Several large banks paid significant fines for such collusion. Elsewhere, WASH agreed to pay a civil penalty of $9 million to the Dept. of Justice to settle charges of discriminatory lending. At the same time, the Dept. of Justice sued EBAY, claiming the company was violating the Clean Air Act by selling harmful products, including devices to defeat vehicle emissions controls. (The case could theoretically lead to billions in fines with a penalty of nearly $6,000 for each of 343,000 such devices the government claims were sold through EBAY.) Later, the US Senate advanced a bill aimed at allowing banks to finance legal marijuana ventures. The bill now moves to the Senate floor for debate. In auto news, HYMTF (Hyundai) and Kia are recalling 3.37 million vehicles over the risk of engine fires according to the NHTSA. Later, a CA federal court ruled in favor of QCOM dismissing a consumer suit alleging the chipmaker’s exclusive contracts with phone makers artificially inflate phone prices. By midday, Epic Games appealed to the US Supreme Court to review its AAPL antitrust case, in hopes of overturning lower-court rulings. In other AAPL news, after the close, AAPL was ordered to face a private antitrust lawsuit brought by payment card issuers accusing the company of stifling competition for its Apple Pay Mobile Wallet, enforcing a monopoly in the US over the iPad, iPhone, and Apple Watch tap-to-pay market. (The suit alleges that unlike the GOOGL Android platform, which lets users choose between the GOOGL Wallet, Samsung Wallet, and others, AAPL forces its users to use the AAPL wallet.) Also after the close, a CA federal judge refused to overrule the Santa Barbara County Supervisors who had denied XOM the permits needed to replace a pipeline that has been ruptured since 2015 with a fleet of 25,000 tanker trucks (which would have allowed XOM to reopen its closed offshore platform). Finally, the judge randomly assigned to hear the FTC antitrust case against AMZN has recused himself without citing a reason. The case was reassigned, based on rotation, to a judge nominated by President Biden. However, the FTC has asked the case to be assigned to yet another judge who is already hearing smaller private antitrust cases against AMZN.

After the close, MU reported beats on both the revenue and earnings lines. Meanwhile, WOR missed on revenue while beating on earnings. However, CNXC, FUL, and JEF all missed on both the top and bottom lines. It is worth noting that FUL also lowered its forward guidance.

Overnight, Asian markets were mixed but leaned toward the red side. Taiwan (+0.27%) was the biggest mover among the five green exchanges while Japan (-1.54%), Hong Kong (-1.36%), and New Zealand (-1.23%) were by far the biggest losers among the seven exchanges in the red. In Europe, we see a similar story taking shape at midday with just five of 15 bourses in the green (led by Russia +1.16%). The CAC (+0.24%), DAX (+0.01%), and FTSE (-0.39%) lead the region on volume in early afternoon trade. Meanwhile, in the US, Futures are pointing to a mixed and mostly flat start to the day as of 7:30 a.m. The DIA implies a +0.08% open, the SPY is implying a +0.01% open, and the QQQ implies a -0.16% open at this hour. At the same time, 10-year bond yields have spiked again to 4.641% and Oil (WTI) is off a quarter of a percent to $93.45 per barrel in early trading.

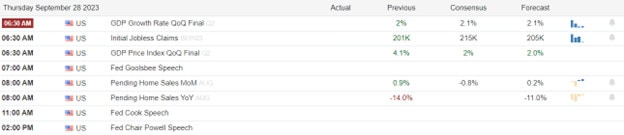

The major economic news scheduled for Thursday includes Q2 GDP, Q2 GDP Price Index, and Weekly Initial Jobless Claims (all at 8:30 a.m.), August Pending Home Sales (10 a.m.), and Fed Balance Sheet (4:30 p.m.). Fed Chair Powell speaks at 4 p.m. The major earnings reports scheduled before the opening bell is limited to ACN, KMX, and JBL. Then after the close, NKE reports.

In economic news later this week, on Friday, August PCE Price Index, August Goods Trade Balance, August Personal Spending, August Retail Inventories, Chicago PMI, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-year Inflations Expectations, Michigan 5-year Inflation Expectations are reported and Fed member Williams speaks.

In terms of earnings reports later this week, on Friday, CCL reports.

In miscellaneous news, an interesting event took place in China on Wednesday. Regional lender Shengjing Bank agreed to sell $24 billion worth of assets (including mostly non-performing loans and corporate bonds) to a government entity. Given the state of China’s real estate market, the move raised eyebrows. Elsewhere, a US Senate staffer leaked to Reuters that the MSFT email server security flaw (made public in July) allowed Chinese hackers to steal 60,000 emails from the State Department. Meanwhile, data shows us that US oil prices continue to rise in large part due to oil producers continuing to ship more oil abroad and draw down US stocks despite lower US demand. (It is more profitable to ship and sell oil abroad than it is to sell in the US.) In spite of that dynamic, US gasoline inventories rose over a million barrels last week, as refineries have plenty of oil supply. This took place in the face of what was expected to be a gasoline drawdown of half a million barrels, based on falling retail sales. So, we have plenty of oil and gasoline. It is just cheaper to ship the oil abroad and the market allows the industry to keep raising fuel prices (consumers reduce the demand but only do so slowly). In other words, prices are stickier than demand. Finally, the House GOP remains at square one, working through 700 proposed amendments and four ridiculous partial funding bills that are dead on arrival anyway. This is due to Speaker McCarthy remaining subservient to a radical minority of his party refusing to do anything bipartisan. McCarthy and his handful of MAGA Congressmen have told sources that they think a shutdown will gain them more concessions. He has even decided to change the subject, talking about non-issues by saying he wants to “sit down with the President to secure the border.” In the meantime, both sides of the aisle acted as grownups in the Senate and have advanced a compromise 45-day CR to fund the government.

With that background, it looks like traders are undecided but leaning bearish in the premarket. All three major index ETFs are printing small, indecisive, but definitely black-bodied candles in the early session. Perhaps we are waiting on the GDP or Jobless Claims for a clue. All three remain well below their T-line (8ema) and 50sma. So, for now, the short-term trend clearly remains headed lower with retests of the August and June lows either accomplished or being the apparent next target for the Bears. In terms of extension, as I said, all three major index ETFs are far below their T-line (8ema), with QQQ obviously stretched furthest, and the T2122 indicator is still in its oversold range. This tells us we are in need of a bounce or at least a pause to relieve the pressure. However, we must remember the market can remain oversold (or overbought) longer than we can stay solvent while betting against it.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Equity markets dropped sharply on Tuesday with investors worried about higher rates with data indicating the consumer is wreaking adding to the bearish sentiment. The Costco report after the bell would seem to support the notion of a struggling consumer despite their top line beat of estimates. Today investors will have to deal Mortgage Apps, Durable Goods, and Petroleum numbers as well as a handful of notable reports to find directional inspiration. We are overdue for a relief rally but keep in mind if it does begin it could rather be muted with a possible government shutdown possible at midnight Friday. Expect the challenging price action to continue if the possibility persists.

Overnight Asian markets reversed early bearishness finding some relief in some industrial data and Australian inflation modest improvement to close mostly higher overnight. However, European markets remain muted and mostly lower this morning as consumer data cause continued sentiment concerns. U.S futures on the other hand are trying to put on a brave face an inspire a bit of a relief rally ahead of potential market-moving earning and economic reports with a looming government shutdown weighing on investor’s minds.

Economic Calendar

Earnings Calendar

Notable reports for Wednesday include CNXC, FUL, JEF, MU, PAYX, & WOR.

News & Technicals’

The U.S. is facing a potential government shutdown if Congress fails to pass a spending bill by Oct. 1, the start of the new fiscal year. This would mean that many federal agencies and programs would have to stop or reduce their operations, affecting millions of Americans and the economy. This is not the first time that the U.S. has faced such a situation, as political disagreements over the budget and the debt ceiling have often led to impasses in the past. In fact, in 2011, after a prolonged standoff over raising the debt limit, S&P downgraded the U.S. long-term credit rating from AAA, the highest possible rating, to AA+, indicating a slightly higher risk of default. The downgrade was a historic and unprecedented move that reflected the growing political polarization in Washington.

Costco, the wholesale retailer, reported its quarterly earnings on Tuesday, beating the analysts’ expectations. The company earned $1.25 per share, higher than the estimated $1.17 per share. The revenue was $44.77 billion, also higher than the expected $43.99 billion. However, the company’s comparable sales, which measure the sales growth at stores open for at least a year, were not very impressive. The comparable sales increased by 1.1% globally, but only by 0.2% in the U.S., which is Costco’s largest market. The company attributed this to the strong performance of its grocery business, which offset the weaker demand for discretionary items, such as clothing, jewelry, and furniture. Costco also faced higher costs due to the pandemic, such as wages, sanitation, and e-commerce investments.

Indonesia, the largest e-commerce market in Southeast Asia, is planning to tighten its regulations on online shopping, especially on social media platforms. The country’s Ministry of Trade said on Tuesday that it is working on a new rule that would ban transactions on social media, such as Facebook, Instagram and TikTok. The ministry said that social media platforms are not registered as e-commerce businesses and do not comply with the existing laws and standards. The move is aimed at protecting local consumers and sellers, especially the micro, small, and medium-scale enterprises (MSMEs), which have been affected by the influx of foreign goods sold through social media. President Joko Widodo said that the MSMEs have seen their sales start to decline due to the unfair competition from foreign products. The new regulation is expected to benefit the traditional e-commerce players in Indonesia, such as Sea Ltd., which operates Shopee, one of the leading online shopping platforms in the region. Citi, a global bank, said that the regulation would reduce the competitive pressure from TikTok, which has been expanding its e-commerce presence in Indonesia.

The stock market dropped sharply on Tuesday, reversing the gains from Monday, as investors were worried about the Fed’s plan to keep interest rates high for a longer period. The Fed’s decision was based on its assessment of the inflation and labor market conditions. The sectors that suffer the most today are the ones that depend on consumer spending and innovation, such as consumer discretionary and technology. The only sectors that performed better were the ones that provided essential goods and services, such as health care and consumer staples. The energy sector also benefited from the rising oil prices. The global markets also followed a downward trend. Today we have a few notable earnings reports as well as Mortgage Apps, Durable Goods, and Petroleum numbers for the bulls or bears to find inspiration. The indexes remain in an extreme short-term oversold condition so be prepared for a relief rally to begin at any time assuming the data does not pile on to the bearishness. Also, keep in mind any relief rally could be muted due to the uncertainty of a possible government shutdown on Oct. 1st.

Markets gapped down on Tuesday (down 0.73% in the SPY, down 0.63% in the DIA, and down 0.73% in the QQQ). All three major index ETFs followed through the first hour before then trading sideways in a tight range until 1:15 p.m. At that point, all three took another leg lower for 30 minutes before trading sideways along the lows for the last 2.25 hours of the day. This action gave us gap-down, black-bodied candles with small wicks on both ends across the SPY, DIA, and QQQ. All three remain stretched below their T-line (8ema) and 50sma, with the DIA falling down through its 200sma on the day. This happened on a bit below-average volume in the QQQ, right at average volume in the SPY, and a bit above-average volume in the DIA.

On the day, all 10 sectors were in the red with Utilities (-2.65%) way out front leading the other sectors lower. Meanwhile, Healthcare (-0.45%) held up much better than the other sectors. At the same time, the SPY lost 1.47%, DIA lost 1.16%, and the tech-heavy QQQ lost 1.50%. VXX spiked to close at 25.04 and T2122 cropped back to the low end of the oversold territory at 3.47. 10-year bond yields spiked above four-and-a-half percent to 4.55% while Oil (WTI) also gained almost one percent to end the day at $90.54 per barrel. So, the day started off bearish and step-by-step continued that way for the rest of the day. This took us back to a state of being over-extended to the downside.

The major economic news reported Tuesday included Building Permits, which were up but still a touch below expectations at 1.541 million (compared to a forecast of 1.543 million and the prior reading of 1.443 million). That amounted to a 6.8% increase while the forecast called for a 6.9% increase. Later, the September Conf. Board Consumer Confidence came in a touch low at 103.0 (versus a forecast of 105.5 and well down from the prior value of 108.7). At the same time, August New Home Sales also came in light at 675k (compared to the forecast of 700k and well down from the July 739k number). That was a decline of 8.7% month-on-month versus the July number which was a 8.0% increase over June. Then, after the close, the API Weekly Crude Oil Stock report showed a 1.586-million-barrel build (compared to a forecasted drawdown of 1.650 million barrels and much increased from the previous week’s 5.250-million-barrel drawdown.

In Autoworker contract talks and strike news, President Biden joined the UAW picket line on Tuesday. During remarks over a bullhorn, he was asked whether autoworkers deserved a 40% raise. He answered “Yes.” On the same trip, Biden met with auto suppliers impacted by the strike where MEMA (auto supplier trade group) asked him to provide federal assistance to ensure the viability of the idled parts suppliers.

In stock news, QCOM announced Tuesday that it has entered into a multi-year partnership with Japanese IT company NTT to develop a 5G ecosystem that promotes the adoption of 5G and “AI over 5G” in Japan. At the same time, the CEO of FWONA (which owns 83% of SIRI) proposed that the radio unit of FWONA be spun off and then merged with SIRI. Later, FSR closed up 9.60% (after trading in a volatile 20% range) after reaffirming its plan to increase vehicle deliveries to 300 per day later this year (and saying it had already produced 5,000 of its SUVs). Elsewhere, LILM announced it has begun assembly of its jet-powered electric VTOL jet. This comes just two months after successful tests of a full-scale prototype in Germany. At the same time, MMM agreed to pay $10 million for violating sanction restrictions on sales to Iran. Later, ICPT received an unsolicited $19/share cash bid from Alfasigma. This was an 82% premium on the price at the time but ICPT closed up more than 79% on the news. At the same time, TGT reported that it would close nine stores across four states on Oct. 21, citing organized retail theft rings that were threatening employees, customers, and inventory shrinkage.

In stock government, legal, and regulatory news, the Financial Times reported that TSLA (along with several European carmakers) is the subject of an EU probe into whether its cars (built in China) are receiving unfair subsidies. Later, JPM paid $75 million to the US Virgin Islands to settle a lawsuit over the bank’s ties to Jeffrey Epstein. Elsewhere, the FTC and 17 states filed suit against AMZN over alleged antitrust violations that allowed the giant to dominate large segments of online retail. The case was assigned to Reagan-appointed judge Coughenour. Later the Canadian government announced it will review the proposed merger between BG and Viterra (a company backed by GLCNF). That merger would create another grain giant, close to the scale of competitors ADM and Cargill. However, it would make a 3-way grain triopoly. After the close, a federal judge in AM has overturned a jury verdict of $176.5 million against LLY in favor of TEVA over infringement on three patents. Meanwhile, a federal district judge in Atlanta ruled in favor of a venture capital fund (backed by JPM, BAC, etc.) and against the conservative anti-diversity plaintiff that had charged the fund was acting illegally because it considered the racial identity of award recipients. (This will be appealed as it was brought by the same group that was behind the anti-affirmative action decision by the Supreme Court earlier this year.) Also after the close, the SEC announced that HYZN has agreed to pay $25 million to settle charges of fraud (without admitting guilt, naturally). Finally, after the close, the FCC announced it would reintroduce “net neutrality” regulations to prohibit T, VZ, CMCSA, and others from blocking websites, slowing internet speeds, or charging higher prices for access to different websites. This is a huge deal and has been fought tooth and nail by the big telecom and cable companies while it will be cheered by AMZN, NFLX, and other major content platforms. The FCC will vote Oct. 19 on whether to solicit public comment (which is when the opponent media blitz will begin).

After the close, AIR, COST, and MLKN all reported beats on both the revenue and earnings lines. The AIR and COST numbers were quarter-on-quarter increases, but despite its own “beats” the MLKN numbers were actually down almost 15% quarter-on-quarter. Nonetheless, MLKN also raised its forward guidance.

Overnight, Asian markets were mixed but leaned toward the green side with only four of 12 exchanges in the red. Hong Kong (+0.83%) was by far the biggest mover as the other moves in either direction were for less than half of a percent. In Europe, we see a similar mixed picture taking shape at midday. Greece (-1.52%) is the largest loser and Russia (+0.66%) is the biggest gainer. However, as usual, the CAC +0.05%), DAX (-0.12%), and FTSE (-0.21%) lead the region on volume in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a green start to the day. The DIA implies a +0.27% open, the SPY is implying a +0.36% open, and the QQQ implies a +0.35% open at this hour. At the same time, 10-year bond yields have backed up a bit again to 4.505% and Oil (WTI) is up another 1.42% to $91.69 per barrel.

The major economic news scheduled for Wednesday is limited to the August Durable Goods Order (8:30 a.m.) and EIA Weekly Crude Oil Inventories (10:30 a.m.). The major earnings reports scheduled before the opening bell are limited to PAYX. Then after the close, CNXC, FUL, JEF, MU, and WOR report.

In economic news later this week, on Thursday, we get Q2 GDP, Q2 GDP Price Index, Weekly Initial Jobless Claims, August Pending Home Sales, Fed Balance Sheet, and Fed Chair Powell speaks. Finally, on Friday, the August PCE Price Index, August Goods Trade Balance, August Personal Spending, August Retail Inventories, Chicago PMI, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-year inflation expectations, Michigan 5-year Inflation Expectations are reported and Fed member Williams speaks.

In terms of earnings reports later this week, on Thursday, CAN, KMX, JBL, and NKE report. Finally, on Friday, CCL reports.

In miscellaneous news, the Wall Street Journal reported that the tentative deal struck between Writers and Hollywood studios will allow the studios to train AI models on the work of the writers, although the writers would be compensated for the work trained upon. (This may well leave writers vulnerable to replacement. Studios have done similar things with actors, recording a day or two of lower-tier actors from many angles at scale rate and then using CGI trained on those recordings to produce realistic “cast of thousands” effects in many future movies.) In related news, the Writers Guild union called for their strike to end today with a member vote on the tentative deal still pending. Elsewhere, Reuters reported that OpenAI is in talks with institutional investors about selling existing shares at a price that values the company between $80 and $90 billion. (For reference, earlier this year, OpenAI got an investment that valued the company at $30 billion.) If completed, this would make OpenAI one of the most valuable private companies. Finally, House Speaker McCarthy and his MAGA-placating approach have continued to make little (no) progress toward avoiding a government shutdown. Luckily, on the other side of the building, the Senate is working in a bipartisan fashion (led by both Majority Leader Schumer and Minority Leader McConnell) to move forward a short-term continuing resolution to fund the government through Nov. 17. A procedural vote on this passed 77-19 and this CR also includes $6 billion for disaster relief and $6 billion in additional support for Ukraine. Late Tuesday, moderate GOP members of the House said they are now willing to invoke a seldom-used “discharge vote” procedure to force a House vote on a CR negotiated between the moderate GOP members and Democrats. Having the GOP Governance Caucus (Anti-burn it all down MAGA group) do the work of governing allows McCarthy to continue kowtowing to 20 extreme-right members while actually keeping the government operating. However, it’s unsure what that discharge vote might mean for McCarthy’s Speakership.

In late-breaking mortgage news, in China, police have placed the founder of the troubled China Evergrande Group in “police control.” This is the latest indicator that a liquidation of the company may be in the cards and comes a day after creditors gave the company until October 30 to submit a debt restructuring deal to avoid their moving for that liquidation. Back in the US, the Mortgage Brokers Assn. reports that the average rate for a conforming, 30-year, fixed-rate loan rose to 7.41% this week (up from 7.31% the week before). As a result, new home loan applications fell 2% week-on-week (and were down 27% versus the same week last year). At the same time, applications for loan refinancing fell 1% week-on-week (down 21% over the same week in 2022).

With that background, it looks like the Bulls are gapped us up in the premarket. However, so far in the early session, we are seeing black-bodied, “inside day” candles in all three major index ETFs. (This means that the premarket open was the early session high so far.) All three remain well below their T-line (8ema) and 50sma. The morning gap also did not give the DIA enough energy to retest its 200sma so far this morning. So, for now, the short-term trend is clearly remains headed lower with retests of the August and June lows as the apparent next target for the Bears (except in the SPY where those two targets have already been achieved). In terms of extension, as I said, all three major index ETFs are far below their T-line (8ema) and the T2122 indicator is also in the low end of its oversold range. This tells us we remain stretched and are in need of a bounce or at least a pause to relieve the pressure. However, we must remember the market can remain oversold (or overbought) longer than we can stay solvent betting against it.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

After a bearish start to the day, the bulls worked to begin a relief rally that lacked momentum as investors moved cautiously in this final trading week of September. The rising bond yields contributed to the uncertainty with the 10-year bonds topping a sixteen-year high. Today we face more possible market-morning economic reports and a few more notable earnings to inspire the bulls or bears. Expect the challenging price action to continue and watch and be prepared for some big point whips or reversals and pent-up waiting for an opportunity.

Asian markets closed their Tuesday session red across the board as real estate woes continue with inflation data on the horizon. European markets also trade cautiously bearish this morning with German manufacturing continuing to decline under the economic pressures. U.S. futures point to a bearish open ahead of earnings and economic data possibly reversing yesterday’s tepid bullishness.

Economic Calendar

Earnings Calendar

Notable reports for Tuesday include AIR, CTAS, COST, FERG, MLKN, SNX, PRGS, & UNFI.

News & Technicals’

The global economy is facing a serious threat from the escalating tensions in Eastern Europe. The war in Ukraine, which started in 2014, has not only caused human suffering and political instability but also strained the relationships between the economic superpowers, such as the US, China, Russia, and the EU. The conflict has also increased the risk of sanctions, trade wars, cyberattacks, and military confrontations. Jamie Dimon, the CEO of JPMorgan Chase, suggested that Eastern Europe was the epicenter of risk, and compared the situation to the aftermath of World War II. He said that the world had not faced such a complex and uncertain scenario before, and warned that it could trigger inflation, deficits, and recessions

Ukraine is facing a challenging situation as it tries to maintain its international support in its conflict with Russia. The war, which has been going on since 2014, has caused thousands of deaths, millions of displacements, and widespread damage. Ukraine relies on its allies, especially the US and the EU, for political, economic, and military assistance. However, some recent diplomatic gaffes, such as the leaked phone call between President Zelensky and President Biden, have raised doubts about the strength of their partnership. Moreover, public opinion in both Europe and the US has shown a decline in support for Ukraine’s cause, especially when it comes to providing more funding and weapons. Some analysts fear that Russia could take advantage of this situation and try to undermine Ukraine’s alliances and increase its aggression.

The artificial intelligence (AI) chip market is heating up as more startups compete with established players like Nvidia and Arm. One of them is Kneron, a U.S.-based semiconductor company that specializes in edge AI solutions. Edge AI refers to the processing of AI tasks on devices such as smartphones, cameras, and robots, rather than on cloud servers. Kneron announced on Tuesday that it raised an additional $49 million in its funding round, bringing its total funding to over $100 million. The round was led by Taiwanese giant Foxconn, the world’s largest electronics contract manufacturer and a key supplier of Apple’s iPhones. Other investors included Alltek, a communications tech company, and several venture capital firms. Kneron said it will use the funds to accelerate the commercialization of its AI chips, which are designed to enable low-power and high-performance edge AI applications across various industries.

After the DIA tested and held its 200-day moving average the bulls worked to provide a little relief rally on Monday but lacked momentum with inflation data looming later this week. The ongoing increase in U.S. Treasury yields, which have reached their highest level for the year, surpassing 4.5% for the 10-year bond added to Monday’s uncertainty. The U.S. dollar, which tends to appreciate when investors seek safety, has also risen sharply. The DXY dollar index is above 105, its highest level for the year, creating some headwinds for global companies and markets. Today we have a few more notable earnings reports that could provide some inspiration for the bulls or bears and may also give us a glimpse into the 4th quarter as well as hints to the strength of the consumer. Investors will have to also deal with Case Shiller, FHFA House Prices, Consumer Confidence, New Home Sales, a 2-year bond auction as well as more Fed member pontifications. Plan carefully as Asian and European bearishness tries to reverse yesterday’s relief all at once at the open.

Monday was another lackluster day in the market. The SPY gapped down 0.24%, the DIA gapped down 0.28%, and the QQQ gapped down 0.23%. The three major index ETFs then vacillated back and forth across their opening gaps until 11:15 a.m., when the Bulls moved the SPY and QQQ back up above the Friday closing level and they traded sideways in a tight range until 3:55 p.m. Meanwhile, the DIA continued its meandering in the morning gap until 3:55 p.m. However, the strongest candle of the day for all three was the last 5-minutes which took all three out on their highs of the day. This action gave us a large, white-body Marubozu (shaved head) in the SPY, a white-bodied Piercing Candle in the QQQ, and what could be seen as a large-body, white Hammer in the DIA. This all happened on less-than-average volume in all three major index ETFs.

On the day, seven of the 10 sectors were in the green with Energy (+1.20%) way out front leading the other sectors higher. Meanwhile, Communications Services (-0.93%) was by far the biggest laggard sector. At the same time, the SPY gained 0.42%, DIA gained 0.12%, and the tech-heavy QQQ gained 0.47%. VXX was just on the green side of flat to close at 22.90 and T2122 climbed but remains in the oversold territory at 14.13. 10-year bond yields spiked above four-and-a-half percent to 4.531% while Oil (WTI) was just on the red side of flat to end the day at $89.88 per barrel. So, in the first 90 minutes of the day markets were undecided. They then made a small move higher only to be undecided again until the last 5 minutes. All-in-all, it was a nothing day that did not change the support or resistance levels and did not show much of a change in sentiment. At best it gave us a little relief from Bearish over-extension.

There was no major economic news reported Monday. However, MCO (Moody’s) warned that a government shutdown would be bad for the US creditworthiness and the US credit rating would come under pressure. In the process, MCO essentially issued a stern warning to Congress (in a way to the House GOP since they have decided to not reach across the aisle in the hope of a much more conservative Budget). MCO is the only rating agency that still gives the US its top credit rating.

In Autoworker contract talks and strike news, less than a day after it ratified its new contract with F (by 54% for versus 46% against), Unifor (Canadian version of UAW) announced that its next negotiation target is GM Canada. (The F contract provides the reinstatement of defined benefit programs, double-digit percentage raises, and a one-time $10,000/employee bonus.) Meanwhile, in the US, after the close, F announced it will stop construction work on its planned $3.5 billion battery plant in MI. The company cited its uncertainty about the ability to remain competitive while locked in contract negotiations. The UAW responded by calling the move a “thinly veiled threat to cut jobs.”

In stock news, OpenAI announced that its ChatGPT engine now has voice and image interaction capabilities similar to AAPL’s Siri and AMZN’s Alexa services. These are likely to be quickly added to the MSFT AI assistants built into Office, Bing, and other MSFT products. SPOT is also using this to translate content into different languages. Later, analysts began reporting inside information indicating that TSLA will be revising its Q3 delivery numbers in the next few days. The analysts expect about a 2.5% cut in the number of vehicles actually delivered in Q3. At the same time, MSTR announced that it has recently purchased another $147.3 million worth of Bitcoin bringing their Bitcoin holdings to $4.68 billion. Elsewhere, PFE announced it has restarted production at its NC plant that was damaged by a tornado on July 19. PFE says it will have all of the plant restarted by year-end but will continue to see lower-than-previous production until mid-2024. At the same time, QCOM denied published reports that it is closing its Shanghai China R&D facility. QCOM admitted it will be reducing headcount but will not close the facility. Over in Europe, NSANY (Nissan) announced that all new vehicles it sells in Europe will be fully electric by 2030. After the close, COST announced it is now offering its members access to a $29/visit online primary-care visit, a $72/visit virtual checkup (including a standard lab panel), and a $79 online therapy session. The service is available in all 50 states. COST won’t accept health insurance since the service is primarily aimed at uninsured Americans.

In stock government, legal, and regulatory news, a German court ruled that NFLX is infringing on an AVGO patent related to high-efficiency video encoding. The court then issued an injunction requiring that NFLX quit using the technology in question. (This could reshape NFLX service performance and/or result in a deal very favorable to AVGO. Elsewhere, MGM has been named in a class-action lawsuit filed Friday. The suit alleges the name, address, email address, date of birth, social security number, driver’s license number, and other personal information of MGM loyalty program members were taken by hackers as a result of lax security (no encryption) during the Sept. 7 cyberattack. At the same time, a subsidiary of DB has been fined $25 million by the SEC for misstating ESG reporting (greenwashing). Later, the NHTSA said that TM recalled nearly 22k Tundra and Tundra hybrid trucks due to wrongly labeled carrying capacities. Meanwhile, YELP has asked a judge to disqualify a law firm from defending GOOGL because the firm previously represented YELP on matters related to the YELP suit against GOOGL. After the close, the NHTSA announced it opened an investigation into a JBLU flight on Monday that experienced severe turbulence, injuring 7 of the passengers and one of the flight crew. Also after the close, AAL filed an appeal of the court ruling requiring it to end its “alliance” with JBLU. (JBLU previously said it would not appeal in order to protect its $3.8 billion acquisition of SAVE.)

After the close, THO reported beats on both the revenue and earnings lines. However, despite being significant sales and earnings beats, the numbers showed a quarter-on-quarter decline of 28%. So far this morning, FERG beat on both the revenue and earnings lines. However, UNFI missed on revenue while beating on earnings. It is worth noting that FERG raised its forward guidance while UNFI lowered guidance. (SNX and CTAS report closer to the opening bell.)

Overnight, Asian markets were nearly red across the board with only Malaysia (+0.15%) hanging onto green territory. Meanwhile, Hong Kong (-1.48%), South Korea (-1.31%), Japan (-1.11%), and Taiwan (-1.07%) led the rest of the region lower. In Europe, we see a similar picture taking shape at midday. Only Greece (+0.40%) and Denmark (+0.26%) are in the green while the CAC (-0.78%), DAX (-0.73%), and FTSE (-0.01%) lead the region lower. In the US, as of 7:30 a.m., Futures are pointing toward a down start to the day. The DIA implies a -0.39% open, the SPY is implying a -0.46% open, and the QQQ implies a -0.54% open at this hour. At the same time, 10-year bond yields are back down to 4.493% and Oil (WTI) is off two-thirds of a percent to $89.08 pre barrel in early trading.

The major economic news scheduled for Tuesday includes Building Permits (8 a.m.), Conference Board Consumer Confidence and August New Home Sales (both at 10 a.m.) and API Weekly Crude Oil Stock report (4:30 p.m.). We also have another Fed speaker (Bowman at 1:30 p.m.). The major earnings reports scheduled before the opening bell are limited to CTAS, FERG, SNX, and UNFI. Then after the close, AIR, COST, and MLKN report.

In economic news later this week, on Wednesday, August Durable Goods, and EIA Weekly Crude Oil Inventories are reported. On Thursday, we get Q2 GDP, Q2 GDP Price Index, Weekly Initial Jobless Claims, August Pending Home Sales, Fed Balance Sheet, and Fed Chair Powell speaks. Finally, on Friday, the August PCE Price Index, August Goods Trade Balance, August Personal Spending, August Retail Inventories, Chicago PMI, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-year Inflations Expectations, Michigan 5-year Inflation Expectations are reported and Fed member Williams speaks.

In terms of earnings reports later this week, on Wednesday, we hear from PAYX, CNXC, FUL, JEF, MU, and WOR. On Thursday, CAN, KMX, JBL, and NKE report. Finally, on Friday, CCL reports.

In miscellaneous news, Bloomberg reported that the major exchanges quietly changed the waiting period between listing and options being allowed to trade. The waiting period was reduced from four to two days after listing to chase the volume. (Options trading volume has more than doubled since 2019.) Elsewhere, Reuters reported Monday that the SEC has collected WhatsApp, Signal, and other messaging service communications for thousands of major investment firm employees. The report said the “illegal off-channel” communication investigation is expanding. CG, APO, KKR, TPG, and BX, are among the listed companies involved in the expansion. Meanwhile, financial services firm AON released a report saying that the pension plans of the largest US companies are the healthiest they have been in 12 years after years of record corporate profits. The report said the average “funded ratio” of S&P 500 companies was 102% as of last Thursday. (This is the highest ratio since prior to 2011.)

In late-breaking mortgage news, industry analyst Insider Intelligence reported this morning that META Threads is struggling to grow. The report said Threads ranks above only Tumblr among the social media platforms in terms of US users. In politics, Congress returns from the 4.5-day weekend they were given when the right-wing part of the GOP caucus killed Speaker McCarthy’s move for a continuing resolution last Thursday. McCarthy said yesterday that the House will vote again on a 45-day CR and budget bills today with a government shutdown looming Saturday. Elsewhere, President Biden will join the UAW on the picket line today (with the former President expected Wednesday so that he can counter-program the next GOP debate instead of participating). Elsewhere, a senior AAPL VP will be testifying today in the GOOGL antitrust trial. Sr. VP Cue will testify about how and why AAPL chose GOOGL as its default search engine for iPhones.

With that background, it looks like the Bears are gapping us down in premarket. So far in the early session, we are seeing small-bodied, white, indecisive, “inside day” candles in all three major index ETFs. All three remain well below their T-line (8ema) and 50sma. So, for now, the short-term trend is clearly headed lower with retests of the August and June lows as the apparent next target for the Bears (except in the SPY where those two targets have already been achieved). In terms of extension, as I said, all three major index ETFs are far below their T-line (8ema) and while the T2122 indicator is also in its oversold range, it has climbed up off the extreme end of that 20-point span. This tells us we remain a bit stretched, but the bounce Monday reduced the pressure at least a little.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Although many were likely hoping to see a bounce on Friday the uncertainty of the hawkish FOMC and the pending inflation data later this week left behind more questions than answers. As the Dow hovers near its 200-day average, we can’t rule out the possibility of more bearish pressure this morning. However, with the short-term oversold condition of the index charts, there is also some hope of a cautious relief rally as we wait on Retail Sales, GDP, and the critical Core PCE numbers. Will it prove bullish or bearish, that is the big question for the week. So plan carefully with the path forward so clouded in uncertainty.