Very volatile price action at yesterday’s close and on overnight whipsaw that’s once again challenging price resistance levels is likely has traders scratching their heads wondering what comes next? I suspect there were many traders stopped out by the selloff at the end of the day, and there will short traders also seeing losses this morning with the overnight reversal. Could we see a short squeeze this morning big enough to break through resistance, or will the bears continue to hold the line? Your guess is as good as mine.

Asian markets closed mixed but mostly flat on the day. European markets are dancing around the flat-line this morning cautiously, monitoring economic recovery efforts. US Futures are boldly gaping up once again ahead of earnings and economic reports that include the FOMC minutes at 2 PM eastern today. Buckle up for another bull/bear battle at price resistance and plan for price volatility to remain challenging.

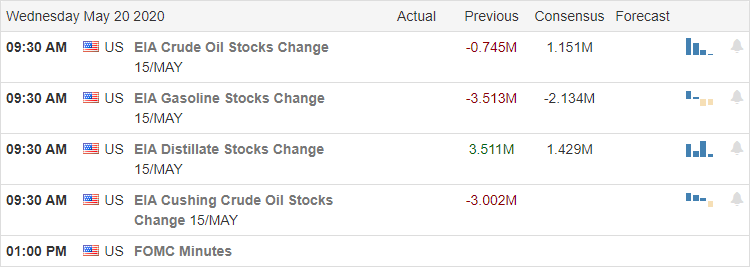

Economic Calendar

Earnings Calendar

On the Wednesday earnings calendar, we have 65 companies stepping up to report. Notable reports include ADI, RDY, EXPE, HUYA, LB, LOW, MCK, SCVL, TTWO, TGT, VER & ZTO.

Technically Speaking

After yet another overnight gap, the market spent the rest of the day chopping sideways struggling to find the energy to break through resistance. Then at the end of the day, a report suggesting the release of a virus treatment way too soon as critical testing metrics were still missing created a sharp market selloff. The volatile price action continued through the evening as overnight futures rebounded, adding insult to injury for those stopped out in yesterday’s whipsaw. Those putting on short positions will also fell the pain this morning as futures push for another gap up opening that may create a bit of short squeeze this morning.

The DIA, SPY, and IWM left behind bearish engulfing patterns at price resistance levels yesterday with the SPY showing the 3rd failure at price resistance. However, the overnight whipsaw is once again challenging price resistance, and the possibility of a short morning squeeze may be just enough to push prices through this level. Of course, a lot will depend on today’s earnings and economic reports that include the FOMC minutes. Even with the late day selling, T2122 suggests a short-term extended condition, and the Absolute Breadth Indicator continues to downtrend, making for a very confusing market condition. Coupled with chart resistance and wild price volatility, what comes next is anyone’s guess! Be careful not to chase the morning gap, getting caught up in fear of missing out. Stay focused on price waiting for proof that gap up can find buyers this morning.

On Tuesday, the bulls couldn’t find the energy to get past the bad news that the MRNA coronavirus vaccine trial did not actually produce the data required to be pass a Phase 1 trial. So, the Monday enthusiasm seems to have been very premature based on just company good feelings. As a result, all 3 major indices failed their breakout levels and printed bearish candles closing at the lows. The SPY was down 1.03%, the DIA down 1.51%, and the QQQ down just 0.25%. The VXX gained to 36.03 and T2122 fell a bit down to 82.05. 10-year bond yields fell to 0.688% as money bid up bonds. However, Oil (WTI) managed to gain to $32.36/barrel.

The Congressional Budget Office announced that it projects GDP to drop 38% in Q2, which is inline with Wall Street estimates. Fed Chair Powell also testified before Congress, essentially saying they will spend whatever it takes to put the economy right. Treasury Sec. Mnuchin testified as well, saying the Administration is fully prepared to provide more money and take more risks (including losses) on business bailouts.

$97 for the next 100 subscribers, then $147

On the Virus front itself, the global headline numbers are 5,006,675 confirmed cases and 325,322 deaths. The UK said it will need massive participation from Brits in order to get their summer harvest done as they expect only about a third of the foreign workers who normally perform the harvest. In Europe, Germany has agreed with neighboring countries to being slowly easing border restrictions.

In the US, we have 1,571,131 confirmed cases and 93,558 deaths. Johns Hopkins University reported that 17 states have seen at least a 10% increase in new case rates in the last week. However, 16 states have also seen a drop of at least 10% over the period. This comes as every state will be at least partially open as of today.

Overnight, Asian markets were mixed with China down while Japan and South Korea were up. In Europe, we also see a mixed story at this point. France and Belgium are down, but the UK and Germany are just on the green side of flat now. As of 7:30 am, US futures are pointing to more than a 1% gap higher as Lowes reported same-store sales grew over 11% and it beat on both the top and bottom lines.

The major economic news on Wednesday is limited to Oil Inventories (10:30 am) and FOMC Minutes (2 pm). Earnings are limited to ADI, EV, FRO, LOW, MCK, RCL, and TGT before the open. Then CPRT, EXPE, LB, SNPS, and TTWO report after the close.

Based on Tuesday’s candle, we might expect a lower-low today and all 3 major indices do remain near a resistance/breakout point. However, the bulls have a strong tendency to run hard in spite of any bad news and the bears haven’t been able to string together a sustained pullback for two months. As said above, markets are looking to gap higher again. So, all we can do is watch the short-term chart and then trade the chart in front of you. Don’t chase or predict, and remain cautious about longer-term swing trades.

Ed

No Trade ideas for today. Trade smart, take profits along the way and trade your plan. Also, don’t forget to check for upcoming earnings. Finally, remember that the stocks/etfs we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

After learning of a small but hopeful clinical trial of a Covid-19 treatment, the market lept higher yesterday to challenge the upper range of resistance of the DIA, SPY, and IWM. The big move left a big gap below, and unfortunately, the Absolute Breadth Index declined as the big-4, AAPL, AMZN, MSFT, and GOOG continue to dominate the indexes. Perhaps today the bulls will find the energy to push through the resistance, but it would not be out of the question to see some profit-takers come in after a one day move of more than 900 Dow points.

Asian markets rallied overnight on hopes of a virus treatment. European markets are trading cautiously flat this morning, and the US futures have recovered early losses to indicate a flat open ahead of earnings and the congressional testimony of Jerome Powell.

Economic Calendar

Earnings Calendar

Retail in focusing the Tuesday earnings calendar with less than 50 companies reporting results today. Notable reports include HD, WMT, AAP, NTES, SINA, URNB & WB.

Technically Speaking

The day after a massive surge in the indexes on the back of warm and fuzzy Powell comments as well hopeful virus treatment news. President Trump reviled yesterday that he has been taking hydroxychloroquine as a preventative virus treatment for the last couple of weeks. Health officials quickly discouraged that course of action, suggesting possible harmful side effects. After an investigation of the WHO, the President is threatening to cut off funding the organization permanently. He has given the WHO 30 days to make substantive improvements accusing them of being China-centric. Home Depot, HD reported sales jumped 7% last quarter, but costs associated with the coronavirus weighed down profits for the quarter, sending the stock down by 3% early this morning. WMT will also report before the bell this morning, shedding light on pandemic impacts on retail.

The DIA, SPY, and IWM tested the upper range of the consolidation yesterday as the bulls raced in reacting to hopeful news. The SPY briefly popped above recent resistance but by the close slid back just enough to leave questions in trader’s minds. Early this morning, futures were pointing to a pullback of more than 100 points, but as the morning progresses, the tenacious bulls have clawed back the decline. The T2122 indicator jumped into the bearish reversal zone on the big rally; sadly, the Absolute Breadth Index declined to suggest fewer and fewer stocks are responsible for lifting the indexes. Will the bulls find the inspiration to break the current resistance, or will the bears find the energy to continue their defense? Perhaps, we will find out today. Plan your risk carefully, staying focused on price action as the battle begins.

Bulls were large and in-charge Monday as futures came into the morning confident on Fed Chair Powell’s Sunday interview remarks. Then, during pre-market, MRNA announced it had positive results in an early-stage human test of a vaccine. That was all the bulls needed to hear to run full-speed ahead. A 2.5% gap up was followed-up by a morning rally. From about 11:30 am, prices drifted very slightly bullish right up to the last minutes. However, in those last moments of the day profit-takers jumped in to pull price back down to the morning highs. On the day, the SPY closed up 3.05%, DIA up 3.81%, and QQQ up 1.86%. The VXX was down sharply to 34.24 while T2122 closed well into the overbought territory at 93.40. The 10-year bond yield was up strongly to 0.726 as money flowed out of bonds and Oil (WTI) had another sharply higher day closing above $30 for the first time since mid-March at $32.74/barrel.

On the Virus front itself, the global headline numbers are 4,911,720 confirmed cases and 320,454 deaths. In Europe, France and Germany jointly proposed a $550 billion fund, set up on loans secured by all 27 EU-member countries, to pay for grants to sectors and regions most economically impacted by the pandemic. Belgium, France, Poland, and Denmark also introduced legislation to prevent any company with a presence in a “tax haven” from receiving any state aid. Separately, France reiterated that it will proceed with its “3% digital tax” regardless of what the rest of the world does (no delay from virus impacts).

$97 for the next 100 subscribers, then $147

In the US, we have 1,550,539 confirmed cases and 91,985 deaths. WMT earnings were way up on a massive e-commerce increase. MRNA decided to capitalize on the good news cycle from announcing a “positive” vaccine trial by offering $1.34 billion in new stock (at $76/share).

Overnight, Asian markets were strongly green, as they followed the US on MRNA and Powell news from Monday. In Europe, we see a different story, where markets are mixed, but leaning much more heavily to the red side (especially the 3 big indices). As of 7:30 am, US futures are flat, sitting just on either side of break-even for the open.

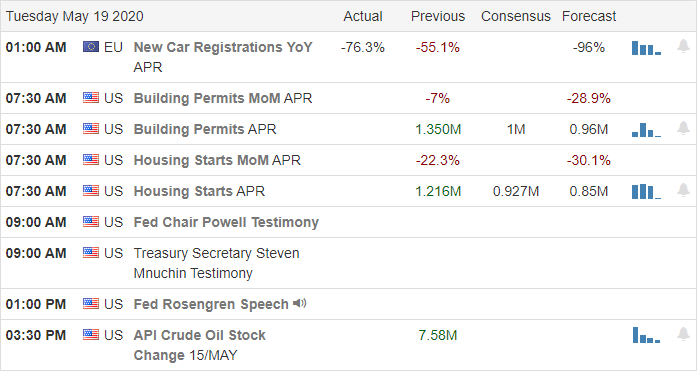

The major economic news on Tuesday is limited to Apr. Building Permits and Apr. Housing Starts (bot hat 8:30 am), and Fed Chair Powell testifies and Fed Voter Kashkari speaks (both at 10 am). Earnings are also very light with only AAP, HD, KSS, and WMT reporting before the open. Only NTES reports after the close among majors.

Fed Chair Powell will likely call the tune again today. His testimony before Congress is expected to confirm that the Fed has the bulls back. He is also likely to reiterate that he feels Congress and the White House need to provide more stimulus on the fiscal side. However, keep in mind that despite Monday’s strong day, the 3 major indices all sit right at a resistance/breakout point. So, we are not quite free of the sideways range that has controlled markets the last few weeks. Still, the bulls have the momentum now. Watch the short-term chart in front of you. Don’t chase or predict, and remain cautious about longer-term swing trades.

Ed

Trade ideas for your consideration and watchlist: SGRY, CREE, WW, CCXI, ST, XPER, EVOP, IMGN, JNUG, GLUU, IMMU, NFLX, TPTX, CHWY. Trade smart, take profits along the way and trade your plan. Also, don’t forget to check for upcoming earnings. Finally, remember that the stocks/etfs we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Friday evening, the House passed a 3-trillion dollar stimulus bill, but it’s unlikely to pass the Senate and if it should the President has vowed to veto. Jerome Powell sees the possibility that the US GDP could shrink by as much as 30% in comments made this weekend. However, as states begin to reopen the US Futures only see bullishness this morning even as the Covid-19 death toll tops 90,000 with more than 1000 American dying almost every day of the last 2-weeks.

Asian markets closed in the green overnight even as Japan slips into recession. European markets are bullish this morning as Euro-zone continues to lift lock-down restrictions. US Futures point to a gap up of nearly 400-points ahead of earnings and a light day of economic news. Let’s party with the bulls but keep a close eye on the overhead resistance of this wide-range consolidation on the DIA, SPY, and IWM.

Economic Calendar

Economic Calendar

On the Monday earnings calendar, we have 120 companies reporting their quarterly results. Notable reports include BIDU, APLE, BILI, IQ, SFTBY, TRVG.

Technically Speaking

US Futures are surging this morning as investors weighed comment by Chairman Jerome Powell suggesting the GDP could shrink more than 30%. He said, struggling retail will continue to struggle even as the country reopens, suggesting that businesses will have to deal with sales volumes 25 to 50 percent of normal. Rather grim statements, but the bulls don’t seem to care, choosing instead to rally hard in the pre-market action. Apple has plans on reopening 25 stores this week, requiring mandatory masks and temperature checks. Several states are opening health clubs and restaurants with new social distancing requirements. New US rules requiring special licensing to sell chips to Huawei will be a big blow to the Chinese 5G tech giant and may also stir trade tensions between the US and China. Friday evening, the US House passed a 3 Trillion dollar stimulus package that would send another $1200 to American taxpayers. However, the package has little chance of passage I the Senate, and the President has vowed to veto the bill should it reach his desk.

As the county reopens, only 3% of the population has been tested, with 1.4 million cases recorded thus far. More than 1000 Americans have died from Covid-19 almost every day this past week, as the death toll tops 90,000. To say the reopening will be challenging my be the understatement of the year. Last week’s hold of the 50-day moving averages is a technically positive signal. However, traders should also note that we remain in a large consolidation range in the DIA, SPY, and IWM. At the end of the last week, the absolute breadth of the overall market continues in a downtrend as the big-4 does most of the heavy lifting. With the futures pointing to a considerable gap up open this morning, keep an eye on overhead resistance levels as the T2122 indicator is likely to reach an overextended condition.

Prices gapped 1% lower at the open again Friday, this time on horrible April Retail Sales. However, the bulls stepped in again and led a day-long rally that closed near the highs. The result was a minimal day with the SPY up 0.46%, the DIA up 0.07%, and QQQ up 0.65%. VXX fell slightly to 36.60 and the T2122 (4-week High =-Low Ratio) rose back to 68.25, still in the mid-range. 10-year bond yields climbed to 0.644% as money sought bond shelter a bit. Oil (WTI) continued its strong rally, up over 7.5% again to $29.65/barrel. For the week all 3 major indices were down.

After the close Friday it was announced that BRKB (Warren Buffett) had reduced its holdings of GS by 84%and JPM (down only 3%), while boosting holdings of PNC. They also exited positions in TRV and PSX. In other business news after the bell, JCP filed for bankruptcy protection as expected and now has 2 months to reorganize.

The House passed the Democrats $3 Trillion Relief/Stimulus bill Friday evening. The White House and Senate Republicans declared it DOA, but the White House also said it would support some new stimulus bill. So, politics as usual. Then on Sunday Fed Chair Powell told CBS that jobless rate could top 30%. However, and assuming there is no second wave of virus, he foresees a steady economic recovery in the second half of 2020, but full recovery won’t happen until there is a vaccine. He also mentioned a need for more fiscal relief/stimulus, that the Fed will not consider negative rates, and that the full-recovery timeline is likely 2021. Treasury yields overnight suggest the market liked what Powell told 60 Minutes and may rally.

$50.00 discount with code: Privilege

Going into the Week, market sentiment is confused at the moment (unless Powell’s words tipped the scale). The AAII reported over 50% of individual investors who respond to their weekly survey are bearish (their market outlook over the next 6 months) for the third time in fourth weeks. Fund Tracker also reports money flowed out of equity funds last week. However, the Put/Call ratio shows a decline in defensiveness and the survey of Active Investment Money Managers shows a neutral to slightly bullish stance.

On the Virus front itself, the global headline numbers are 4,820,347 confirmed cases and 316,967 deaths. In an interesting move, India has prohibited bankruptcy filings for a year in addition to raising the insolvency threshold 100-fold. Japan reported that it had slipped into a recession, even before COVID-19, posting a 7.3% GDP decline in Q4 of 19 and a 3.4% contraction in Q1 of 20. Finally, later this morning France and Germany will announce a joint initiative covering a wide range of topics, including economic recovery.

In the US, we have 1,527,951 confirmed cases and 90,980 deaths. Texas’ daily new case numbers has started trending higher again as it opens. However, some of the other “early opener” states like Georgia are not reporting a change in trend. AAPL is opening many of its retail stores this week, with visitors required to wear masks and have their temperature checked prior to entry. On the government front, the US is considering changing the PPP loan rules to allow small businesses to use more (all?) of the money for things other than payroll, while still being forgiven and also giving them longer to obtain the money.

Overnight, Asian markets were mixed but leaned toward the green. In Europe, we see green across the board so far today. As of 7:30 am, US futures are following Europe with markets pointing toward a 1%-1.5% gap higher at the open.

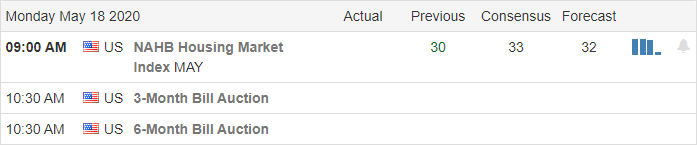

There is no major economic news on Monday. Earnings are also very light with only IGT, SE, and SOHU among large premarket reports. After the close only BIDU, FTK, and IQ report among large companies.

Jerome Powell may have come to the Bulls rescue again with his Sunday interview. Futures turned decisively at that point. However, for the last few weeks markets have been chopping sideways and we are still well within that range. So, there is no overall trend, but very short-term the bulls seem to have the ball. High volatility remains in place. Keep watching the short-term chart in front of you. Don’t chase or predict, and remain cautious about longer-term swing trades.

Ed

Trade ideas for your consideration and watchlist: CGC, MJ, PINS, OKE, NVAX, CVET, CIEN, TSCO, ILMN, ORLY, LOPE. Trade smart, take profits along the way and trade your plan. Also, don’t forget to check for upcoming earnings. Finally, remember that the stocks/etfs we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Yesterday the bulls pulled off an impressive hold of price support and the 50-day averages of the DIA, SPY, and IWM with the oil and financial sectors leading the way. The question today is will that rally continue heading into the weekend after a big morning of economic reports that set shockingly bad market records. This morning futures are quite volatile as they wait for the big data drop. Buckle up for the possibility of a wild ride.

Asian markets close overnight little changed even after reporting there industrial output number came in better than expected. European markets trade mixed its eye on economic reports and uncertain economic reopening. US futures indicate anything is possible by the time the market opens as they grapple with a substantial economic data drop.

Economic Calendar

Earnings Calendar

On the Friday earnings calendar, we have more than 170 companies reporting quarterly results. Notable reports include DKNG, JD, MFG, PBF, & VFC.

Technically Speaking

After a very rocky start on Thursday morning, the bulls stepped up, putting in a solid defense of critical price support levels. Oil and financial stocks led the rally with JPM recovering 4% and AXP lifting more than 7%. Follow the Jerome Powells call for additional Congressional stimulus the President appears likely to support another round of direct payments to citizens. The House plans to vote on a 3 trillion dollar plan as early as today, but Senate leadership continues to say it will not support the current bill. What comes next is unclear, but it seems the pressure for policymakers to continue to rack more up historic deficit spending measures soon.

Yesterday’s rally created an impressive hold of the 50-day average on the DOW, SPY, and IWM indexes. The market-leading QQQ maintained a comfortable cushion between its price and critical averages. Futures this morning are showing a considerable amount of volatility ahead of a big day of economic data. Topping that list is Retail Sales with estimates suggesting a historic decline in consumer spending is likely. In just the last hour, futures have gone from pointing to a bullish open to now suggesting a substantial gap down. Plan for considerable volatility as we head into a weekend of uncertainty as more and more states try to reopen their economy.

Prices gapped 1% lower at the open on the back of a worse-than-expected initial jobless claims number (3mil vs 2.5mil expected). However, after the dust settled for 30 minutes the rest of the data was a strong, steady climb with prices closing near the high. Technically, the SPY and especially DIA seemed to find support off the 50sma and bounced. However, it is hard to say any of the 3 major indices broke their now 3-day downtrend. For the day, SPY gained 1.22%, DIA gained 1.69%, and QQQ gained 1.14%. The VXX was down a bit to 37.67 and 10-year bond yields fell to 0.62%. Oil (WTI) rallied nearly 10% again to close at $27.73/barrel.

The cause of the day-long rally seems to be two-fold. First, even though new initial jobless claims were worse than expected, the continuing jobless claims only rose by less than half a million. This means that although almost 3 million people filed for unemployment this week, over 2.5 million also went back to work. Secondly, in the inverse logic of markets, bad numbers mean it is more likely we will see more stimulus from both the Fed and fiscal sides of government. This was reinforced when Fed voter Kashkari told CBS that Congress will have to send Americans more money as he sees the recovery taking 12-18 months.

On the Virus front itself, the global headline numbers are 4,546,070 confirmed cases and 303,863 deaths. In Germany, the government reported the worst Q1 contraction since the 2008 Financial Crisis and projected a 10% decline in GDP for Q2. The Russian outbreak continues to run wild as they reported another 11,000 cases again. In Asia, the virus worry is limited to a few hotspots. However, India reported another 4,000 new cases and China very recently locked down several cities/provinces again.

$50.00 discount with code: Privilege

In the US, we have 1,457,649 confirmed cases and 86,912 deaths. Among the fallout, JCP is expected to file for bankruptcy today. CNBC reports that the White House would now likely support a new round of stimulus checks as proposed by Democrats, but this is not an official announcement and only based on sources. The House is set to vote on the Democrat’s $3 Trillion bill, but both the Republicans in the Senate and the White House had called it “DOA.” So, again, this all seems to be negotiating tactics in the political theatre.

Overnight, Asian markets were mixed, but the red boards were not that far below break-even. In Europe, the same is true, but leaning even more to the green side as France and Finland are the only red at this point in the day. However, as of 7:30 am, US futures are in the red, now pointing to a 0.70% gap lower at the open.

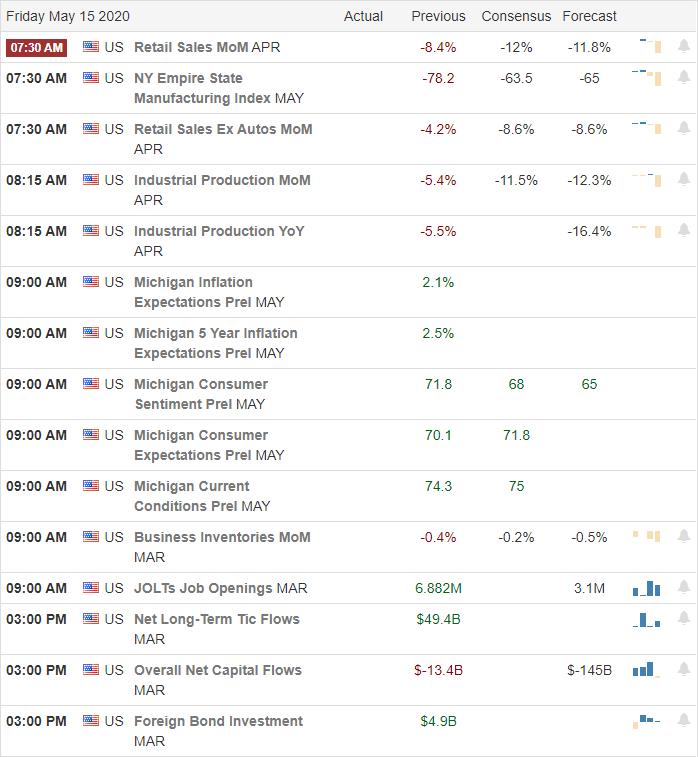

The major economic news for Friday includes Apr. Retail Sales and NY Fed Mfg. Index (both at 8:30 am), Apr. Industrial Production (9:15 am), Mar. Business Inventories, Mar. JOLTS, Michigan Consumer Sentiment and Mar. Retail Inventories (all at 10 am). The only major earnings on tap for Friday are JD, PBF, and VFC all before the open.

A bounce off of support helped the bulls Thursday. However, they were unable to break the 3-day downtrend that has formed this week. While the bulls are not likely to accept the setback for long, it is Friday and a pause to absorb weekend reopening news might not be a bad thing. Weekend news on the next round of stimulus and some feedback on new cases during reopening may be something traders want in their pocket before making more big bets. So, the short-term pullback continues and high volatility remains in place. Keep watching the short-term chart in front of you. Don’t chase or predict, and remain cautious about longer-term swing trades.

Ed

No trade ideas for Friday. Trade smart, take profits along the way and trade your plan. Also, don’t forget to check for upcoming earnings. Finally, remember that the stocks/etfs we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The FOMC Chairman Jerome Powell said they stand ready to do whatever is necessary to support the economy but also warned that the recovery is likely long-lasting impacts for business and employment. He also called on Congress and the Whitehouse, suggesting more will be required to stimulate the economy. According to reports, China has launched cyberattacks against virus research firms attempting to steal possible treatment options. With friends like this who needs enemies!

Asian markets closed the day lower across the board, with Japan falling nearly 2%. European markets are trading lower this morning with the FTSE down more than 2% this morning. US Futures have flirted with a flat to slightly bearish open as we wait on earnings and, of course, another jobless report that may add 2.5 million to the 33 million already unemployed. Expect higher price volatility as we head toward the weekend.

Economic Calendar

Earnings Calendar

On the Thursday earnings calendar, we have our biggest day this week, with 300 companies reporting. Notable reports include AMAT, ACB, BAM, DENN, NOLK, PBR, SSYS, & WIX.

Technically Speaking

The futures tried to get a rally going in yesterday’s pre-market but was unable to hold onto gains gaping lower after a disappointing PPI number. Jerome Powell delivered a word of warning that the recovery is likely to be difficult and may have lingering impacts for several years. He reassured that the FOMC would continue aggressive operations as long as necessary and but said they would need more help from Congress to stimulate the economy. Long story short, this will be a costly, challenging, and likely very volatile economic recovery. In other news, the US is reporting that the Chinese government has launched cyber-attacks against virus research facilities attempting to steal research on treatments and possible vaccines. Companies are encouraged to strengthen their security and report any attacks or breaches to the FBI.

At the close yesterday, the DIA was less than 3 points away from it’s 50-day moving average and near a critical level of price support. The IWM missed testing it’s 50-day by only a few ticks before bouncing in the last few minutes of the day. The SPY held at the price support to 5/4/20 clinging to the 34 EMA, but looking at the QQQ, the selloff of the last couple days is nothing more than an overextended pullback. We have a somewhat volatile overnight future session that currently suggests a flat to moderately bearish open. However, with 300 earnings reports and another jobless number where another 2.5 million people will be added, the 33 million already unemployed, anything is possible by the open. With a big day of economic data on Friday, we should expect an extra dose of price volatility as we slide into the weekend.