While index trends remain very bullish, uncertainty continues to swirl, making it very challenging for the market to see the light at the end of the tunnel. A delayed stimulus deal, mounting pandemic impacts, rising China tensions, and a very contentious election on the horizon is likely to keep volatility high and price action challenging in the months ahead. Though the bulls are clearly in control, don’t forget the bears still exist, so stay focused because this very news-driven market can quickly shift.

Asian markets closed mixed but mostly higher overnight, even as Japan’s economy shrank in the 2nd quarter. European markets trade in the green but have fluctuated as they cautiously monitor geopolitical tensions. US Futures point to a bullish open as the SP-500 continues to challenge overhead price resistance attempting to set a new record high.

Economic Calendar

Earnings Calendar

With the majority of 3rd quarter earnings in the rearview, we have a much lighter week of reports with just 22 companies reporting this Monday. Notable reports include CRMT, FN, JD, & NAT.

News & Technical’s

After another low volume light choppy price action Friday, the SP-500 continues to struggle with overhead resistance and an elusive new record high. However, being this close, the last several days of consolidation builds upon the bullish trend, and I suspect institutions will likely push it though before that is a chance of any meaningful pullback. As the 2020 election nears, the Democrats call for the Postal chief to testify at an urgent hearing to discuss concerns over ballot handling after recent operations changes. Speaker Pelosi is planning to call the House back into session to vote on a Postal Service bill that’s likely to trigger a political firestorm. Just one more thing to deal with as this very divisive election season heats up. Federal bailout numbers of the airline industry swelled to more than $25 billion this year, but that may not be enough to prevent a massive wave of industry layoffs. As many as 75,000 could soon lose their jobs as the pandemic continues to impact airline operations. Boeing reported its second straight month of negative sales growth with far more order cancelations than new sales.

Although the technicals of the index charts remain quite bullish delays of the next stimulus bill, pandemic, tensions with China, and the ramp-up into the election silly season present considerable uncertainty for the overall market. I do suspect the SP-500 will soon make a new record high, but traders will have to stay on their toes as the market digests a likely very news-driven month ahead. Make no mistake; the bulls remain in control; however, this historic rally back to pre-pandemic highs remains quite volatile, and we should expect that turbulence to continue for the foreseeable future.

Friday was another indecisive day, with the bulls unable to push the SPY up through the all-time highs and the bears unable to get any traction either. This all came after July Retail Sales which at the same time was improved and much lower than expected. The SPY closed dead-flat, the DIA up 0.14%, and the QQQ down 0.12%. The VXX remained flat at 25.44 and the T2122 (4-week New High/Low Ratio) rose slightly back up into the overbought territory at 85.06. 10-year bond yields were also flat at 0.709% and Oil (WTI) was also flat, closing at $2.23/barrel.

After the close, the US-China Trade Deal Phase 1 review (scheduled for video conference Saturday) was canceled. This may or may not have had something to do with the President’s renewed threats/pressure on Byte Dance (TikTok) to divest US operations. However, it does give extra time for potential cooling off and, if planned, for China to buy additional goods prior to the review.

Over the weekend, large parts of CA have gone back into rolling power blackouts as their electric grid is unable to keep up with demand. The proximate cause of the grid trouble was a combination of region-wide wildfires and a major heatwave. Places like Sacramento are forecast to hit well in excess of 100 degrees early this week and the “heat dome” that is preventing rain and causing high temperatures is projected to last for 2 weeks. While the main news from the story is residential, a large number of businesses will also be impacted. Not least among them will be the state’s largest electrical utilities, PCG and EIX.

On the virus front, in the US, the numbers show we now have 5,567,765 confirmed cases and 173,139 deaths. While the new cases are falling, the 7-day averages remain stubbornly just under 53,000 new cases and 1,065 deaths per day. The good news includes 20 states with falling rates, 17 holding roughly stable, and only 13 states with rising infection rates. In a testing-related story. Saturday, CNBC reported their survey of 9,400 Americans, which found that 40% of virus test results are coming too late to be useful for either clinical or tracing purposes. In an unrelated story, the number of tests being done remains 10% below where it was a few weeks ago with no reason given for the reduction.

Globally, the number of cases rose to 21,852,024 confirmed cases and 773,586 deaths. In Europe, the recent uptick in cases continues. Over the weekend France saw a post-lockdown record high of new cases on both Saturday and Sunday. The UK has had 6 straight days over 1,000 new cases. Italy has also reinstituted a nation-wide mandatory mask mandate while also closing all bars and nightclubs. However, in Spain, hundreds of people protested in Madrid against mask requirements. In Asia, the outbreak in India continues to grow. Current 7-day averages are now at 62,500 new cases and 950 virus deaths in that country. (Keep in mind that Indian numbers are suspected to be under-reported and must be weighed against a population of 1.4 billion.)

Overnight, Asian markets continue to stay mixed. China and New Zealand led to the upside. Meanwhile, South Korea and Japan led to the downside. Europe is also mixed at this point, but leans more to the green side with modest moves. The FTSE leads the gainers at +0.61% so far today. In the US, as of 7:30 am futures are on the green side of flat. Nasdaq is the leader with its futures pointing to a gap up of 0.68%. The large-caps are positive, but much closer to flat.

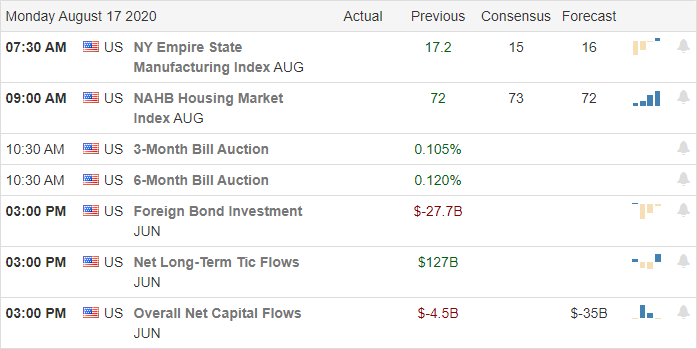

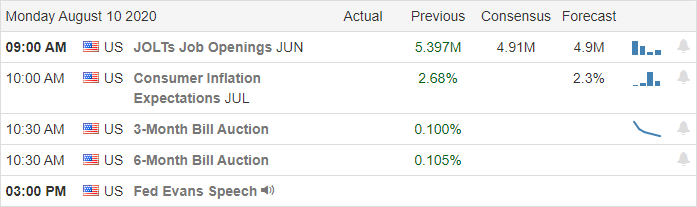

The only major economic news for Monday is the NY Fed Empire State Mfg. Index (8:30 am). Major earnings reports are also very limited with JD reporting before the open and BEST reporting after the close.

The SPY still sits just below its all-time high after 4 straight days of testing resistance at that level. The longer SPY sits there without failure, the more likely this bull run is to continue. It just seems like the bulls won’t give an inch and the bears have no traction at all. However, markets do seem hesitant as politicians have given up on a stimulus deal for now.

Follow the trend and stick to your trading rules. Don’t try to predict reversals or chase moves you have missed. Above all, take profits as you go. Remember, our job is to be consistently profitable, not get rich in a few months. And welcome back to a new week. Happy Monday all.

Ed

The Daily Swing Trade Ideas for today: RIOT, DXC, Z, VIAC, NBL, RCL, AMAT, DG, XOP. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Thursday was an indecisive, up-and-down day that started with a tiny gap down in the large-caps and tiny gap up in the QQQ. This came after a better than expected Initial Jobless Claims report that came in just under 1 million new claims. However, after the roller coaster ride, markets closed very near where they opened, putting in a Doji candle in all 3 major indices. On the day, QQQ closed up 0.23%, SPY down 0.19%, and DIA down 0.22%. VXX was also flat at 25.51 and T2122 fell just outside the overbought territory at 78.57. 10-year bond yields were up strongly to 0.717% after the big afternoon bond sale and Oil (WTI) closed down a touch to $42.36/barrel.

As has been the case, there was no progress between Democrats and the White House on a stimulus bill. Senate Majority Leader McConnell adjourned the Senate for the “August Recess.” This followed the House having already adjourned, but the Senate did not even give the caveat House Speaker Pelosi had given of “Adjourned Pending a deal on a Stimulus Bill.” This means a deal is very unlikely for weeks to come as both sides (Congressional and Administration) will be much more focused on conventions and politicking than governing for at least the next few weeks.

In an interesting after-hours story, Fed Governor Brainard said the Boston Fed has been experimenting with a cryptocurrency in collaboration with MIT. The multi-year project will focus on digital currency. This seems a direct reaction to FB proposing (and then abandoning) its own alternative to Bitcoin in 2019. Brainard said that no decision has been made yet on whether to create the new cryptocurrency. However, programmers working for the Cleveland, Dallas, and New York Federal Reserve banks are collaborating on a study of implementations and implications of this technology. So, it certainly appears to be headed that way.

On the virus front, in the US, the numbers show we now have 5,416,014 confirmed cases and 170,422 deaths. The news cases Thursday were 54,364, which is just under the 7-day average. The daily deaths fell a bit to 1,284, but still well above the 7-day average. In the afternoon, Dr. Fauci said that he was not pleased with how things are going. (Specifically, he said he was disturbed by the increase in positive test rates in states like OH, KY, IN, and TN.) However, he also said we need to think about returning to a sense of normalcy, but do so while social distancing and wearing masks. On that topic, GA Governor Kemp dropped his non-starter lawsuit against Atlanta Mayor Bottoms mask mandate.

Globally, the number of cases rose to 21,100,844 confirmed cases and 758,012 deaths. In Europe, the EU closed a deal with AstaZeneca to buy 300 million doses of vaccine at an undisclosed price. In the UK, they reinstituted travel restrictions (quarantine for incoming passengers from France, Malta, or the Netherlands). This comes as France declared the cities of Paris and Marseilles as “areas of active virus circulation.” In Asia Hong Kong reported a 9% contraction of their economy for Q2 and said they expect the overall year to see a 6%-8% contraction versus 2019. (Given riots and a pandemic, that isn’t exactly shabby…if valid numbers).

Overnight, Asian markets were again mixed, but also more volatile. China led the 1% gainers, while South Korea India, and Thailand led those losing over 1%. However, in Europe we see red across the board so far today on the UK travel restrictions. The FTSE and CAC are down 1.755% apiece, the DAX down 1.04% and the rest of Europe down between 0.75% and 1.50% so far Friday. In the US, as of 7:30 am futures are mixed, but leaning red. The QQQ is pointing to a 0.13% gain at the open while both large cap indices are pointing to about a 0.32% fall at the open.

The major economic news for Friday includes July Retail Sales and Q2 Nonfarm Productivity (both at 8:30 am), July Industrial Production (9:15 am), and July Business Inventories, Mich. Consumer Expectations and June Retail Inventories (all 3 at 10 am). There are no major earnings reports on the day.

The SPY still sits just below its all-time high. It still seems likely the bulls won’t give in to the bears before they reach that goal of new highs. However, markets do seem hesitant as politicians of all stripes have given up on a stimulus deal for now and more economists are predicting slower recovery in Q3 and Q4 than seen in Q2. So, be a bit careful betting either direction in the short run here.

All we can do is either lighten up positions, tighten up stops or pay extra attention to any trend reversal. Follow the trend, don’t over-extend and stick to your trading rules. Don’t try to predict reversals or chase moves you have missed, and take those profits as you go. Remember, our job is to be consistently profitable, not get rich in a few months. Also, bear in mind its Friday…of the political silly season. I might be wise to lighten up on your risk before the weekend news cycles.

Ed

The Daily Swing Trade Ideas for today: PAGS, XLU, RIOT, SLV, ENPH, WU, CL, CDE, HL, NLOK. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

A rebound in the tech sector bounced the QQQ off of trend and price support helped to push the SP-500 within 6 points of a new record high. It seems unlikely to me that we get that close to a big market headline, and the institutions fail to push it through. However, we still have to deal with Jobless Claim data and a big day of bond auctions with rate and currency pricing implications digest today that could create some price volatility. Tuesday afternoon reminded us that the bears are still out there and their restless, hungry, so stay focused and flexible should they happen to find some inspiration in the news.

Asian markets closed mostly bullish overnight even as Australia’s jobless rate hit a 22-year high. European markets appear to be on the cautious side this morning, trading slightly lower as they monitor jobless numbers. US futures are choppy and flat this morning while poised to set a new SP-500 record as we wait on earnings, jobless claims, and significant day of bond auction data.

Economic Calendar

Earnings Calendar

The Thursday earnings calendar is the busiest day of the week, with 124 companies reporting quarterly results. Notable reports include AQN, AMAT, BIDU, BAM, FTCH, GLOB, IQ, NTES, TPR, & TK.

News & Technical’s

Ahead of Jobless Claims and a big day of bond auctions US government debit prices are rising this morning. Today the US Treasury will auction $35 Billion in 8-week bills, $30 billion in 4-week bills, and $26 billion in 30-year bonds. Interestingly gold futures are trading lower this morning while silver futures trade slightly higher. Negotiations on the next stimulus bill seem to have ground to a halt and descended into rhetoric driven finger-pointing match of whos to blame. Which side blinks first is anyone’s guess, but they do both seem to agree on the $1200 taxpayer payments. There are new concerns about the accuracy of COVID test data. According to reports reported new infections have declined 19% over the last 7-days, but testing has fallen by as much as 12% over the same period. Texas cases have dropped off by 10%; however, the number of tests fell 53% over the last two weeks. The big question, are the numbers artificially skewed, or are we gaining ground in the pandemic battle? Only time will tell as the nation prepares to reopen schools and colleges.

Yesterday’s rally closed the SP-500 just 6 points below new record highs with a rebound in the tech sector leading the charge higher. The pullback in the QQQ tested support and trend with buyers surging back into the big-5 tech stocks. The bearish price action on Tuesday afternoon was unable to follow-though as we expected. All eyes are on the weekly jobless claims coming out at 8:30 AM eastern. Stay focused and flexible with a new record close at hand and the T2122 indicator suggesting an overextended market we should prepare for just about anything to occur.

The bulls refused to give back any more ground as they can smell those all-time highs just a quarter percent above in the SPY. So, stocks gapped up 0.80% and rallied in a volatile way all day long, closing in the top 20% of their range. On the day, SPY closed up 1.36%, DIA up 1.00%, and QQQ up a hefty 2.52%. As those numbers show, money flooded back into those high-tech, mega-cap FAANG stocks, especially TSLA on the follow-through to its stock split. VXX was down sharply to 25.50 and T2122 also dropped a touch to 91.94 (still well into the overbought territory). 10-year bond yields rose again to 0.67% as money chased risk and Oil (WTI) rose $42.59/barrel.

On the virus front, in the US, the numbers show we now have 5,360,488 confirmed cases and 169,135 deaths. The news cases Tuesday were 54,345, which is just under the 7-day average. However, again the 1,386 deaths were well above the average. The only real news on this front is concern over the data quality. The number of tests done in the most infected states (FL, TX, CA) have fallen in the last two weeks, as the national average number of daily tests has fallen 19% in that time. This reduction takes place even while the percent positive results has increased over that time. In addition, another group of three dozen public health advisors sent a letter to HHS extremely concerned about the Federally mandated change in data collection procedures and mechanisms causing inaccuracies.

Globally, the number of cases rose to 20,836,339 confirmed cases and 747,865 deaths. In Asia, China announced today that chicken (or perhaps its packaging) imported from Brazil tested positive for the virus. India reported 67,000 new cases, which was a record high for that country. Meanwhile, in Europe, France saw its largest increase in daily cases since May 6.

Overnight, Asian markets were mixed again, but this time lean to the green side of flat. The winners were led by Japan (+1.78%) and Singapore (+1.28%). The only loser of note was Australia (-0.67%). Elsewhere the Asian market could best be described as just on the green side of flat. In Europe, markets are broadly in the red so far today. The FTSE leads the losses (-1.14%), but everywhere except Russia (+0.46%) sees some red at this point in the day. In the US, as of 7:30 am futures are pointing to a flat open. The Nasdaq futures are just on the green side, while the SPY and DIA futures are just on the red side of break-even.

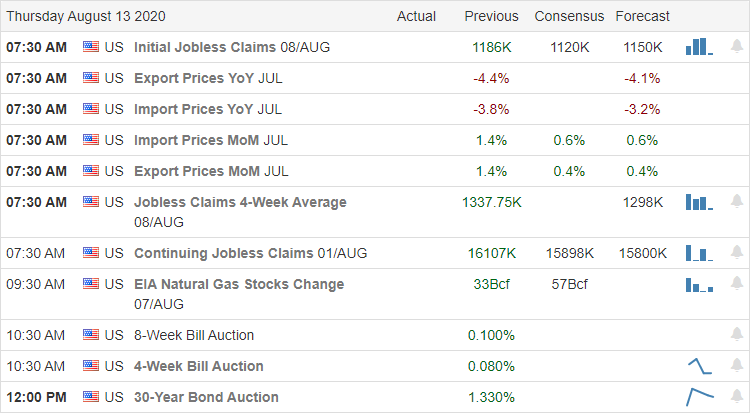

The major economic news for Thursday is limited to July Import / Exports and Weekly Initial Jobless Claims (both at 8:30 am). Major earnings are limited to ENS, NTES, and WCC before the open. Then after the close AMAT, BIDU, and IQ report.

The SPY sits just below its all-time high. It seems likely the bulls won’t give into a pullback before it tastes those sweet new highs. So, be careful betting on shorts until that has been accomplished. However, despite Tuesday’s black candle, markets remain quite extended. So, longs carry a fair bit of risk here too.

All we can do is either lighten up positions, tighten up stops or pay extra attention to any trend reversal. Stick with your trading rules and execute them with discipline. Don’t predict reversals or chase missed-moves, and don’t be greedy. Take your profits along the way. Remember, our job is to achieve trade goals consistently, not to hit the lottery.

Ed

The Daily Swing Trade Ideas for today: PHM, KHC, MAS, CL, FAST, DHI, EBAY, FTV, SWKS, KLAC. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The bears make a rare appearance leaving behind some concerning candle patterns, but I suspect they will find it very difficult to gain much momentum with a possible record high in the SP-500 so close at hand. Remember bearish candle pattern requires follow-through to be valid, and this morning the bulls are pushing hard in the futures to punish traders that took early short positions. Institutions want that new record headline, and it seems unlikely they will give up this close to making it happen.

Asian markets had mixed but mostly bullish results during the night, and European markets whip around mixed this morning over the possible return of the virus. US point to a substantial overnight reversal of yesterday’s bearish close with the Dow expected to gap up more than 225 points.

Economic Calendar

Earnings Calendar

On the Hump Day earnings calendar, we have 87 companies stepping up to reports quarterly results. Notable reports include LMND, CSCO, EAT, CHU, ENS, FOSL, GMAB, YY, JMIA, LYFT, PING, SDC, SPTN, TCEHY, VFF, WPM, & ZTO.

News & Technical’s

Presidential candidate Joe Biden has chosen California Senator Kamala Harris for his running mate this fall. If Biden wins in the fall, he will be the oldest elected president at 78 possible, putting Harris teed-up for a run for the top job after one term. President Trump announced a deal Moderna of 100 for 100 million doses of coronavirus vaccine as Russia comes under considerable criticism for rushing the widespread use of a vaccine after test just 100 individuals. As a result of COVID economic impacts, the UK is now in recession with a record economic plunge over 20%. Yesterday Florida reported a record 276 death caused by the virus on Tuesday. A grim reminder we have a long way to go in our battle with the disease. Congress remains deadlocked on the next stimulus bill continuing to point fingers at one another to pass the blame for the delay.

Yesterday’s price action left a few questions for the traders to ponder as the bears made a rare appearance in the afternoon session to snap 8-straight days of a market rally. They left behind concerning candlestick pattern, but this morning the bulls are fired up again, pointing to a substantial gap up. I think it’s improbable the bears will have a chance to gain much momentum with the SPY so close to setting a new record high. In-fact the selling yesterday may have picked up just enough short interest to pull off a quick short squeeze to help secure that new record high headline. That said, once the new record is achieved, a rest or pullback in the market is not out of the question. Stay focused, and flexible.

Markets gapped up four-tenths of a percent on hopes from Russia’s approval and claim it has a safe and effective vaccine. Stocks then rode the roller-coaster until mid-afternoon. However, at 2 pm a steep selloff started and ran all the way into the close. It is possible a story that no stimulus package was imminent or perhaps an early leak prior to the announcement that Former-VP Biden selected Senator Kamal Harris as his running mate was the cause. (Personally, I think it was the Big-10 canceling fall football that sank spirits.)

Regardless of the cause of the late selloff, of the 3 major indices, only the QQQ broke its uptrend. However, SPY closed down 0.83%, DIA down 0.34%, and QQQ down 1.89% as a rotation from the tech high-fliers into recovery economy tickers continued even during the selloff. VXX was up to 36.95 and T2122 fell a touch to 93.19 (still deep in the overbought territory). Oil (WTI) was down slightly to $41.68/barrel and 10-year bond yields rose strongly to 0.64%.

After the close, TSLA announced a 5-for-1 stock split for stockholders as of August 21. During the day BA reported 43 more plane orders were cancelled in July (bringing the total to 836 cancelled so far this year). However, that significant decrease needs to be weighed against the fact the company still has almost a 4,500-plane production backlog to work through.

On the virus front, in the US, the numbers show we now have 5,306,851 confirmed cases and 167,761 deaths. New cases for Tuesday were at 54,519, which is slightly under the 7-day average. However, the 1,504 deaths for the day were well above the average. After the close, the President announced the US had reached a deal with MRNA to buy 100 million doses of their experimental vaccine for $1.53 billion. The state of FL reported a record jump in virus deaths on the day (increasing almost 3x from Monday). Interestingly, that state’s average daily new cases were down 38%, but tests done per day dropped an even larger 46% in the last two weeks (likely partially due to hurricane Isaias).

Globally, the number of cases rose above 20 million as it reached 20,553,328 confirmed cases and 746,652 deaths. The UK reported that its economy contracted 20.4% in Q2. This is right in line with analyst expectations following a small contraction in Q1. However, it does put them technically into a recession. Germany saw a new spike as they reported over 1,000 new cases Tuesday. While that is less than 2% of the US cases, bear in mind that they also only have 25% of the US population.

Overnight, once again Asian markets were mixed. Hong Kong and Thailand were the only decent size gainers. Meanwhile, China and New Zealand led the losers. The rest of the countries delivered smaller moves spread around break-even. In Europe, bourses are technically mixed but lean heavily toward the green. The DAX is just on the red side of flat while Sweden and Denmark are showing half-percent loses. Elsewhere we see a healthy green numbers, led by the FTSE being up 1.1%. In the US, as of 7:30 am futures are pointing to a gap higher. Today the gaps will be less varied with the SPY looking at +0.74%, the QQQ at +0.89%, and the DIA at +0.93%.

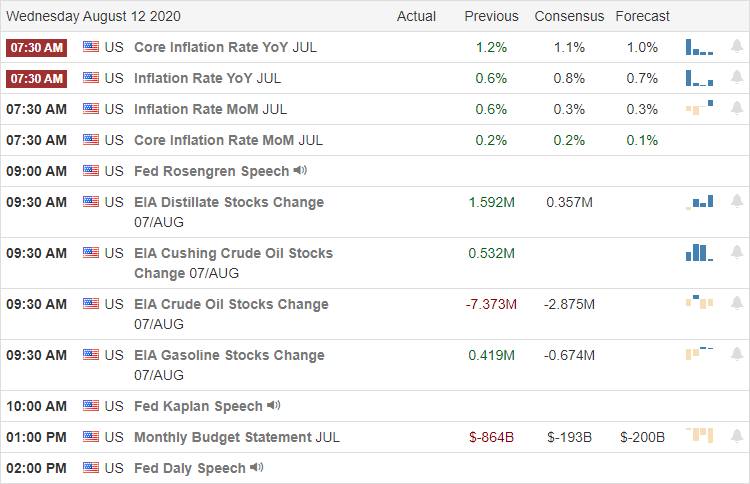

The major economic news for Wednesday includes July CPI (8:30 am), Crude Oil Inventories (10:30 am), July Federal Budget Balance (2 pm), and 3 Fed speakers (Rosengren at 10 am, Kaplan at 11 am, and Daly at 3 pm). Major earnings are limited to AIT, APG, and PFGC before the open. Then after the close CACI, CSCO, and SPTN report.

The large-caps put in their first black candle since July 28 yesterday, following the QQQ which put in its 3rd in a row. Still, as mentioned above, the trend remains bullish in the large-caps and the QQQ barely broke its own. The point is that it is hard to call Tuesday’s late selloff a trend break. So, all we can do is keep an eye on it and not go too long or short until we get more information. Stick to those trading rules and execute with discipline. Don’t predict reversals or chase missed-moves, and don’t be greedy. Take your profits along the way. Remember, our job is to achieve trade goals consistently, not to hit the lottery.

Ed

The Daily Swing Trade Ideas for today: CME, QCOM, SQ, SCHW, MA, STNE, PLNT, V, FTV, W. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Hopeful vaccine news out of Russia is inspiring the bulls for a gap up open this morning that may well set a new record high in the SP-500. Although Congress continues the battle of soundbites and rhetoric, there is still significant hope they will soon come to an agreement on more stimulus. How this might affect the Presidential executive orders is unclear but slowing the debit spending no longer the issue. It’s the battle of who’s willing to spend the most.

Asian markets closed missed but mostly higher overnight with Hong Kong leading the way up 2.11%. European markets are sharply higher across the board up to more than 2.5% on recovery hopes. US Futures indicate a very bullish gap up open with the SP-500 nearing a new record high ahead of earnings and PPI data.

Economic Calendar

Earnings Calendar

On the Tuesday Earnings Calendar, we have a decline, with 88 companies stepping up to report. Notable reports include NIO, GOOS, CSPR, HUYA, IHG, LITE, MAC, MLCO, RRGB, SFTBY, SYY, & VIAV.

News & Technical’s

Yesterday’s bullish move left the SP-500 less than 1% from new record highs. Airlines reported that travel is increasing, providing a big lift to the sector, including a BA which rallied more than 5.5%. Heavy equipment manufacturers DE, CAT, and CMI buying surged yesterday with energy and financial sectors also gaining ground. During the night, Russia claims the development of the world’s first coronavirus vaccine lifting the futures markets sharply higher this morning. Of course, a lot of testing will have to is required before the acceptance of a new vaccine here in the US, but with global cases topping, 20 million hope is high. New US sanctions against Chinese government officials yesterday once again ratchet up tensions between the countries, adding uncertainty to global banks. As MSFT works to buy TikTok, the French government opens an investigation into privacy concerns of the popular social media App.

With the bulls solidly in control and the futures pointing to a bullish gap open, the SP-500 is likely to reach a new record high. Traders should be careful not to chase stocks already well within a bullish run with the fear of missing out. Remember, this will be the 8th straight day of gains, increasing the odds of a market rest or pullback at any time. The T2122 indicator this buying wave is very stretched, and a new record high could be the catalyst that brings out some profit-takers. Having said that, we should rule out the possibility that Congressional Stimulus news could provide another shot of energy for the bulls. Stay focused, flexible, and plan your trading carefully.

Markets opened flat, rode the roller-coaster all morning, and then were calm all afternoon. There was what appears to be a rotation underway, out of the mega-cap FAANG stocks that have led the rally since March and into the “big recovered economy” stocks such as Industrials and Energy. On the day SPY was up 0.30%, QQQ was down 0.43%, and DIA was up 1.28% (on that rotation). VXX fell once again to 25.75 and T2122 rose slightly to 97.34, deeper into the overbought territory. 10-year Bond yields rose to 0.58% and Oil (WTI) rose to $41.99/barrel.

The President’s executive orders from Saturday seemed to be a non-story on Monday. Uncertainty, likely legal challenges, and the limited nature of the orders made the focus stay on a bi-partisan deal. Treasury Sec. Mnuchin said the White House was willing to put more money on the table, but reportedly made no new offers. Democrats have not made another offer either after their “meet in the middle” $2 trillion deal rejected Friday. Both sides said over the weekend (and again Monday) that they are ready to negotiate, but the sides have also not talked since Friday according to Mnuchin.

In related news, President Trump floated that he is again seriously considering doing a Capital Gains tax cut. As with the Payroll Tax and to be charitable, it is unclear if he has the legal authority to cut taxes by himself. While he claimed this move would create a lot of jobs via reinvestment, he reportedly also decided against the action a year ago because it would not help the working class enough. (For example, the top 1% of taxpayers had over 75% of the long-term capital gains last year per the IRS report.) However, it is another stimulus idea under consideration.

On the virus front, in the US, the numbers show we now have 5,251,997 confirmed cases and 166,201 deaths. In good news, for the first time in well over a month, there are less than 50,000 virus hospitalizations in the country. This comes as the 7-day average of both new confirmed cases and deaths have leveled off after the very recent pullback. So, the front line of the fight is getting at least a little respite.

Globally, the number of cases rose above 20 million as it reached 20,281,373 confirmed cases and 739,770 deaths. In the early hours today, President Putin claimed their country had given regulatory approval for a Russian vaccine that had proven safe and effective. In a jab at the west, they named this vaccine “Sputnik V” and Putin said they had ordered a billion doses for global distribution. Markets popped on the news, despite widespread skepticism about the truth and science behind the claim. Whether true or not, the news did give hope for the vaccine development underway in the UK and US.

Overnight, Asian markets were mixed again. China and Taiwan led the losers this time, while Japan, Hong Kong, and South Korea led gainers. However, in Europe markets are strongly green across the board on Russia-prompted vaccine hopes. The FTSE is up 2.5%, the DAX up 2.6%, and the CAC up 2.7% so far today. In the US, as of 7:30 am futures are pointing to a varying gap higher. The DIA implied open is up 1%, the SPY up 0.62%, and the QQQ up 0.39% seemingly reinforcing the rotation from high-flying tech into mainstream recovery economy names.

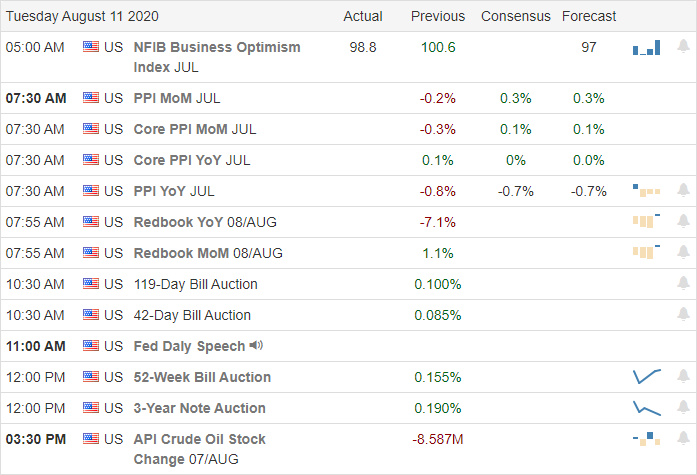

The only major economic news for Tuesday is July PPI (8:30 am) and a Fed speaker (Daly at noon). Major earnings are also very limited to BR, SYY, and YPF before the open. There are no major earnings reports after the close.

Markets continue their bullish march. With no major economic news and high spirits from the Russian vaccine approval, we may well see more upside run. However, beware that we are over-extended and that it appears a controlled (not desperate selling or buying, just methodical movement from one group to another) rotation is ongoing. So, don’t fight the trend, but remain aware that another pause or swing to the downside may come soon. Keep your discipline and mind those trading rules. You put them in place for a reason (to help control emotion and avoid mistakes). As always, follow the trend, don’t predict reversals or chase missed-moves, and take your profits along the way. Remember, we just need to make our goals consistently. We don’t have to swing for massive gains on any one trade.

Ed

The Daily Swing Trade Ideas for today: PLAY, HWM, DFS, NBL, FTI, F, XLE, TSN, WMT. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

With stimulus money once again flowing with the stroke of the Presidential pen, the path to record highs in the SP-500 is clear for the bulls for an easy headline. Although we have several significant reports on the economic calendar this week, today is light, allowing earnings news and politics to drive the day. While a new record in the SP-500 seems likely soon, traders should watch for possible profit-taking that could begin at any time having moved up 7-days in a row.

Asian markets closed Monday mixed but mostly lower remaining cautious with the rising tensions between the US and China. However, European indexes are green across the board this morning, and US futures have recovered from overnight lows suggesting a modestly bullish open to begin the week.

Economic Calendar

Earnings Calendar

Although the 3rd quarter earnings season starts slowing this week, Monday’s calendar remains quite busy with more than 200 companies reporting. Notable reports include ANGI, GOLD, CGC, CDR, SCOR, CEIX, DUK, AGM, GOGO, HVT, IAC, INO, IPAR, JCOM, MAR, MELI, OXY, ON, PPL, APTS, RCL, SEAS, SPG, TME, TLRY, & WKHS.

New & Technical’s

With the stroke of a pen, the President signs a series of executive orders extending coronavirus relief through the end of the year after Congress failed to reach an agreement on the stimulus bill. Those unemployed will receive $400 in additional financial support down from the $600 that lapsed over a week ago. However, it requires the State to come up with $100 of the $400 benefit, and it’s unclear if they can do so. The initial market reaction to this action showed mixed results, but the additional deficit spending has gold and silver futures flying high this morning. Some analysts say gold could ready $4000 an ounce! With the election less than 100 days away, the President also raised tariffs on aluminum reigniting the trade war with Canada, and of course, Canada retaliated in kind. This weekend the US reached another grim milestone, topping 5 million coronavirus cases. Daily infection rates have begun to level off in Florida, Texas, and California, with some mid-west, states becoming a concern as their numbers surge.

With the SP-500 just over 1% from new record highs and the stimulus money flowing again, I suspect the path is clear for the bulls to push forward. Although the index has moved higher seven sessions in a row, I can’t imagine institutions failing to reach that out for that record-high headline. However, traders will also have to stay focused on the possible profit-taking that could begin at any time. With a light day on the economic calendar, earnings results and political spin cycle are the likely drivers for today.