The U.K. reported a new, more contagious strain of the virus on Sunday, overshadowing the 900 billion stimulus bill agreement sending the futures sharply lower. If this morning’s gap-down reversal gains momentum, it could be a painful day with price and technical supports substantially lower. Though cooler heads may prevail, make sure you have a plan to protect your capital. Expect extreme sensitivity to the news as countries extend and strengthen restrictions in reaction to the new strain.

Asian markets closed mixed but mostly lower overnight. European markets trade decidedly bearish this morning as new travel restrictions go into place. U.S. futures have bounced off overnight lows but still point to a substantial gap down ahead of a light earnings and economic calendar day. Buckle up volatility and with an extreme sensitivity to news surrounding the new strain.

Economic Calendar

Earnings Calendar

As we kick off the Holiday week, we have a light earnings calendar. Notable reports include FDS & HEI.

News and Technicals’

The second vaccine from Moderna reaches hospitals today after emergency approval last week, with infection and death rates remaining very elevated. Late Sunday afternoon, Congress agreed on a 900 billion dollar stimulus bill, the 2nd largest in history. The House will vote on the bill later today, sending to on to the Senate for approval. Airlines are on track to receive another 15 billion in government support but must call back furloughed workers to receive the payments. Yesterday the U.K. scientists identified a new, more aggressively infectious strain of COVID. In reaction, several countries have already banned travel, and instead of the planned easing of restrictions ahead of Christmas, Parlement may add to lockdown restrictions in an emergency Parliament meeting. After hearing about the stimulus agreement, U.S. futures surged 200 points but have turned sharply bearish as new restrictions in reaction to the new strain worry investors.

After a very volatile overnight futures market fueled on the mixed emotions of stimulus and a more infectious strain of the virus, the market points a substantial gap down at the open. Dow futures more than 600 points but has thus far rallied off the overnight lows. That said, those that were buying up positions before the weekend will likely experience a painful reversal this morning. Perhaps cooler heads will prevail, but this is the kind of event that could easily trigger a swift and significant selloff. Try not to panic and stay focused on the price action but plan to protect your capital if the run for the door gains momentum.

On Friday, the large-caps made a small gap down while the QQQ made a small gap up at the open. However, all 3 major indices then immediately sold off for most of the day. A strong rally the last 20 minutes (perhaps on S&P 500 rebalancing or on Quadruple-witching preparation) still left all 3 with ugly black candles, but at least well up off the lows. (In other words, all 3 indices were black Hammer-type candles with longer lower wicks.) On the day, the SPY lost 0.82%, the DIA lost 0.52%, and QQQ lost 0.30%. The VXX rose almost 2% to 17.08 and T2122 fell just out of the overbought territory to 76.74. 10-year bond yields rose to 0.945% and Oil (WTI) rose to $49.10/barrel.

The weekend drama was about a stimulus and government spending deal as Friday ended with a government shutdown expected and no stimulus deal yet done. Late Friday night Congress kicked the can down the road by passing a 2-day stop-gap spending bill that ended at Midnight on Sunday night. The hold-up on the stimulus deal was down to a few GOP Senators who want to end the Fed’s Lending Authority (kill the programs where the FOMC has been lending to businesses and banks as well as buying bonds after emergency previous Congressional authorization). Late Sunday the two sides finally reached a deal, but Congress didn’t have time to type up and pass that agreement before the shutdown deadline. So, they passed an additional one-day stop-gap spending bill last night that the President signed to keep the doors open.

The other major news from the weekend was that Friday evening the FDA approval of the MRNA vaccine. This announcement was made at the same press conference where the White House Vaccine Chief admitted communications problems had caused 14 states to believe they were getting up to 40% more of the PFE vaccine doses than they had actually been allocated. So, the MRNA vaccine shipping may help fill some holes. The MRNA vaccine began shipping on Sunday and the first vaccinations with this drug should happen Monday. The main advantage of the MRNA vaccine is that it requires slightly less stringent (still -50 degrees) temperatures to store and ship, making its distribution easier. The CDC followed the FDA lead Sunday by authorizing hospitals to administer the new vaccine.

Related to the virus itself, US infections continue to rage across the US, but came down just a bit. The totals have risen to 18,267,579 confirmed cases and 324,869 deaths. As mentioned, the weekend saw a small reduction in new cases, but the 7-day daily average remains 217,630 (over one-third of the world’s cases) and the average number of deaths rose to 2,628 deaths per day. The apparent new threat (new strain) out of UK caused the US Surgeon General to a statement Sunday. He said it is too early to tell if the new strain of the virus would be prevented by the two current vaccines, but other vaccine candidates are on the way in the months to come…so we should trust the scientists.

Globally, the numbers rose to 77,264,853 confirmed cases and the confirmed deaths are now at 1,701,599 deaths. As a reference, the world is averaging about 640,000 new cases and almost 11,000 new deaths per day. In the UK, London was placed under emergency lockdown and PM Johnson says that the Christmas pause in restrictions will be modified as the Health Minister explained that the new virus strain (mutation) is out of control and spreading far worse than the original strain. This news caused the reimposition of restrictions on travelers from the UK in many countries as the US, Denmark, the Netherlands, and even Australia have now detected cases of this new variant. This includes a full stop of travel from the UK to France. In more positive news for Europe, the EU Drug Regulator is expected to authorize the PFE/BNTX vaccine today.

Overnight, Asian markets were very mixed. China was green as Shenzhen (+1.87%), Taiwan (+0.95%), and Shanghai (+0.76%) led the gainers. However, most Asian exchanges were red with Thailand (-5.44%) and India (-3.14%) far outpacing the pack. In Europe, markets are red across the board on massive fear stoked by the new virus strain in the UK. Losses have been in the 2%-3% range as of mid-day. Among the big 3 bourses, FTSE is at -2.03%, DAX at -2.84%, and CAC at -2.63%. As of 7:30 am, US futures are pointing to a significant gap lower. Right now the DIA is implying a -1.38% open, the SPY implying a -1.55% open, and the QQQ implying a -0.99% open.

There is no major economic news or major earnings reports for Monday.

With no economic data or earnings to change the storyline, markets are being dragged South by the new strain of virus in the UK. Expect the details of the stimulus agreement to also get some traction, but its a question of whether Mr. Market focuses on what didn’t make the deal or what did. At least at the start, the Bears have the upper hand. The new MRNA vaccine is the wildcard, but remember PFE sold off in the days after the approval and release of their vaccine. So, be careful and remember this is a holiday-shortened week with light volume expected. It remains very possible that all the big money has already left town for Christmas vacation.

Focus on maintaining discipline. Respect the trend, support and resistance, and price action. Keep working the process and booking those base hits. Don’t let greed get in the way of you achieving goals. Success is built one trade at a time, not by trying to hit the lottery. In short, get rich slowly…one trade at a time, just consistently achieving goals.

Ed

Swing Trade Ideas for your consideration and watchlist: No Trade Ideas for Monday. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The bulls and bears stood toe to toe yesterday, duking it out with either side unable to gain any momentum as we wait on Congress. Evidence continues to show that pandemic restrictions are slowing the economy, and with infection rates exploding to about 1 million every 4-days, I suspect that will only get worse. Has this rally already priced in the stimulus bill? Maybe, so be careful overtrading and consider your risk carefully heading into the weekend and the holiday week ahead.

Asian markets closed the week red across the board in reaction to the Bank of Japan rate decision. European markets this morning show modest gains even as a no-deal Brexit weighs on investor minds. U.S. Futures are trying to shake off overnight lows during the morning pump up that has become all too familiar of late. With a light earnings and economic calendar day, expect an extra dose of news sensitivity as we head into the weekend.

Economic Calendar

Earnings Calendar

We have a light day on the Friday earnings calendar, but we still have a few meaningful reports. Notable reports include APOG, DRI, NKE, & WGO.

News & Technicals’

With an afternoon vote, the FDA endorses the second vaccine choice, with Moderna gains approval for emergency use. A good thing as the infection rate explodes around the country, adding about 1 Million new positive tets in just 4-days. According to reports, the widespread hack included a breach at Microsoft. They are not suggesting millions of Americans may have been affected by the attack. The deadline for a Brexit trade deal is drawing near with several key disputes yet to resolve. A no-deal Brexit could create some stock market and currency market fluctuations. Keep an eye on this developing story.

After gapping higher on high hopes of a stimulus bill, the market seemed to lose momentum quickly and chopped in a narrow range the rest of the day. The Absolute Market Breadth Indicator continues to decline, and the T2122 indicator suggests a very extended condition in the indexes. That said, the bears don’t appear to have any teeth, and the trends remain bullish as we wait for a congressional decision. The indexes appear pensive and wound pretty tight, waiting on a news event that can create an explosive move in either direction. As you plan your risk into this weekend, keep in mind volume tends to decline quite sharply, heading into the Christmas holiday shutdown.

On Thursday, markets gapped about half a percent higher after unexpectedly high Initial Jobless Claims offset optimism stemming from stimulus deal and a second vaccine approval. After the open, prices ground sideways the rest of the day. This left us with all three major indices printing indecisive Dojis at new all-time high closes. On the day, SPY gained 0.56%, DIA gained 0.44%, and QQQ gained 0.65%. The VXX fell almost 1.5% to 16.75 and T2122 rose deeper into the overbought territory at 94.21. 10-year bond yields rose to 0.935% and Oil (WTI) rose over a percent to $48.33/barrel.

In late afternoon Bloomberg reported that the stimulus deal is being hindered by GOP efforts to end virus lending programs. However, at the other end of the spectrum, 2 Senators (one from each party) are continuing to fight for a $1,200 direct payment to Americans instead of the $600 agreed by the 4 Leaders on Tuesday night. So, it seems while the Leaders came to an agreement, the rank and file still have other ideas. As of early Friday morning, House and Senate leaders said they expect a short government shutdown (funding runs out at midnight Friday), followed by a weekend approval vote on a deal covering both government funding and stimulus.

For the second time in two days (and third time in two months), GOOG was sued for antitrust activities on Thursday. This time by a bipartisan group of Attorneys General from 38 states. This suit focuses on allegations GOOG has maintained a monopoly in general search and search advertising. While all these suits will take years to wind through the courts, the repeated announcements don’t help the stock one bit.

Related to the virus itself, US infections continue to rage as the US. The totals have risen to 17,627,070 confirmed cases and 317,929 deaths. Thursday did not see any more bad records but was still a bad day with almost 232,000 new cases and nearly 3,300 deaths. This brings the 7-day averages to 220,690 new cases and 2,599 deaths per day. Of course, the FDA Advisory Panel did recommend the MRNA vaccine for emergency use and FDA and FDA Head Dr. Hahn promised swift action (it will be approved today). If all goes as planned, shipments of MRNA vaccine is expected to start Monday. This comes not a moment too soon as arguments between states, the federal government and PFE surfaced last night over how much vaccine was promised this week and whether shipment allotments have been reduced for the next couple weeks.

Globally, the numbers rose to 75,407,507 confirmed cases and the confirmed deaths are now at 1,671,135 deaths. As a reference, the world is averaging about 642,000 new cases and almost 11,000 new deaths per day. In Asia, Australia is beginning new travel bans between some of its states after a new cluster of cases was found around Sydney (at beaches). In South Korea, 500 Covid-19 patients are waiting on a hospital bed to open up and have waited more than a day at this point.

Overnight, Asian markets leaned heavily to the down side. Only a flat South Korea and India avoided red ink. New Zealand (-1.60%), Malaysia (-1.31%), and Australia (-1.20%) led the losses. In Europe, markets are mostly green so far today. Only Belgium (-0.12%), Portugal (-0.63%), and Russia (-0.53%) buck the trend. However, the big 3 bourses are typical of the modestly green overall picture. Among those, the FTSE (+0.20%), DAX (+0.37%), and CAC (+0.01%) are all up slightly. As of 7:30 am, US futures are pointing to a flat open. Right now the DIA is implying a +0.03% open, the SPY implying a +0.12% open, and the QQQ implying a +0.08% open.

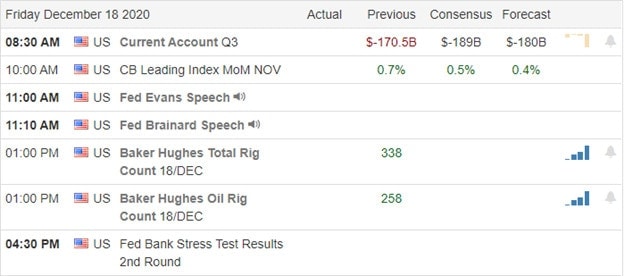

The major economic news for Friday is limited to Q3 Current Account (8:30 am), Fed Bank Stress Test Results (4:30 pm) and a Fed Speaker (Brainard at 11:10 am). Major earnings releases include DRI and WGO before the open. Then NKE reports after the close.

Without a ton of economic data, a government stalemate, and sitting on Option Expiration Friday, the market may wait for more news before making its next move. However, we do sit at all-time highs, and a stimulus deal and new vaccine approval are expected very soon. So, the bulls do have the upper hand. Either way, be careful heading into the weekend in front of a holiday-shortened week. It is very possible all the big money has left town already.

Keep working the process and booking those base hits. Money in the bank trumps a “possible lottery ticket” every time. Keep your discipline and respect the trend, support and resistance, and price action. In short, get rich slowly…one trade at a time, just consistently achieving goals.

Ed

Swing Trade Ideas for your consideration and watchlist: PLAN, PAYC, AUY, JNJ, SHAK, KSU, ALEC, TSLA. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The market seems solely focused on stimulus, rallying the NASDAQ to new record highs. Little details such as declining retail sales, new record hospitalizations, and the highest daily death toll over 3600 Americans won’t stand in its way. Sorry for the sarcasm, but ignoring the economy’s actual state can make for a hazardous situation if the market sentiment suddenly decides to shift. Stay with the bullish trend but stay focused and have a plan to capture gains and protect your capital because a shift south could be swift and punishing.

Overnight Asian markets recovered from early losses to close with modest gains across the board. Across the pond, European markets advance with stimulus talks in focus. Ahead of Housing Starts, Jobless Claims, and the Philly Fed MFG Index, futures currently point to a bullish open fueled up on hopes of more federal deficit stimulus spending. Stay focused as we continue to extend.

Economic Calendar

Earnings Calendar

As usual, the Thursday earnings calendar is one of your busiest days of reports. Notable reports include CAN, BB, FDX, GIS, JBL, NAV, RAD, & WOR.

News & Technicals’

Focused only on stimulus hopes and seemingly ignoring any other economic details, the futures are rising this morning. A miss on Retails Sales, a decline in PMI, with new records of more than 3600 deaths and hospitalizations while on the same day printing new a record on the NASDAQ. Jerome Powell left rates near zero and reintegrated the FOMC commitment to keep them low as long as necessary for the economy to recover. The FDA expects to vote on Moderna’s Covid vaccine later today, and Congress is making progress on the stimulus bill. Several states joined Texas in an antitrust lawsuit against Google, claiming collusion with Facebook fixing advertising prices. Antitrust against the tech giants seem to be shaping up as a theme for 2021.

At the risk of sounding like a broken record, stay with the bullish trend but have a plan to capture gains and protect capital if the market suddenly decides to care about the actual economy’s condition. Before the open, today will get readings on Housing Starts, Jobless Claims, and the Philly Fed MFG Index. The most likely to move the market would typically be the Jobless Claims, but with high hopes of newly printed stimulus debit, even a negative number could inspire new record index highs. I will reiterate that both T2122 and T2101 are both flashing clues to be cautious, so be careful not to overtrade or chase already extended stocks.

The market opened flat after hope for stimulus was offset by a big November Retail Sales miss in the premarket. After that markets ground sideways the rest of the day. All 3 major indices printed indecisive candles (more wick than body), but QQQ also closed at another all-time high close. On the day, SPY was up 0.13%, DIA down 0.16%, and QQQ gained 0.55%. The VXX lost 3% on the day to 16.98 and T2122 fell a bit to 89.27 (still well into the overbought territory). 10-year bond yields were up to at 0.921% and Oil gained slightly to $47.83.

During the day, it was leaked that Congressional Leaders had more or less finalized negotiations on a $900 billion stimulus bill Tuesday night. The deal reportedly will not include either business liability waivers or aid to state/local governments. However, it will include another $600 direct payment to Americans. The hope was to introduce the bill Wednesday after having it written up. However, that did not get done. So, Senate Majority Leader McConnell told Senators to be ready for a weekend vote on the bill. This would mean the government would shut down just after midnight Friday night as the Stimulus bill will be attached to a government funding extension. Also, during the day, the Fed raised its economic forecast to 4.2% GDP growth and unemployment back down to 5% in 2021. Beyond that, Fed Chair Powell said they are holding rates the same and will continue with current policies (near-zero rates, bond buying, etc.) until we reach full employment.

GOOG was also sued Wednesday for antitrust activities by 10 states Attorneys General, led by Texas. This suit also names FB as a co-conspirator and focuses on the alleged monopoly of advertising technologies and services (data tracking, which enables ad targeting). This comes just a day after the new European law was proposed which will regulate and fine the same technologies as too invasive to personal privacy.

Related to the virus itself, US infections continue to rage as the US. The totals have risen to 17,394,314 confirmed cases and 314,629 deaths. Wednesday saw another record number of new cases (248,646) and deaths (3,538). This brings the 7-day averages of 220,217 new cases and 2,570 deaths per day. Meanwhile, the FDA approved a second over-the-counter rapid home covid-19 test (from ABT) on Wednesday. On Thursday the FDA Vaccine Advisory Panel will debate and then vote on whether to recommend the MRNA vaccine for emergency use. (Spoiler alert: they’ll recommend it.) Following a recommendation, it will take hours to a day for the FDA to approve emergency use and shipping of the vaccine will begin about a day after that approval (which will give the CDC time to approve the administration of the MRNA vaccine).

Globally, the numbers rose to 74,662,200 confirmed cases and the confirmed deaths are now at 1,658,062 deaths. As a reference, the world is averaging about 637,000 new cases and almost 11,000 new deaths per day. French President Macron has tested positive shortly after a meeting with other EU leaders. So, many other EU leaders are also now in isolation. In Seoul South Korea, they have experienced the first case of a Covid-19 patient dying while waiting on a hospital bed to open up. This comes as Japan also reported another increase in ICU patients. Interestingly, in Russia, President Putin told his media that mass vaccinations using the Russian “Sputnik” vaccine were necessary for the country. However, he said he would not personally be getting vaccinated because he was “too old.” (This from a man who constantly promotes the idea of his strength, vigor, and fitness.)

Overnight, Asian markets were mixed, but leaned to the green side. Australia (+1.16%), Shanghai (+1.13%), and Shenzhen (+0.93%) led the gainers. Singapore (-0.51%) and Malaysia (-0.42%) led the modest losses. In Europe we see a similar picture so far today. Russia (+1.07%) is an outlier, but the FTSE (+0.01%), DAX (+0.80%), and CAC (+0.40%) are typical. The only losses are very modest and seen among the smaller exchanges in Europe. As of 7:30 am, US futures are pointing to another modestly bullish open. The SPY is implying a +0.52% open, the DIA implying a +0.42% open, and the QQQ implying a +0.48% open at this point in the premarket.

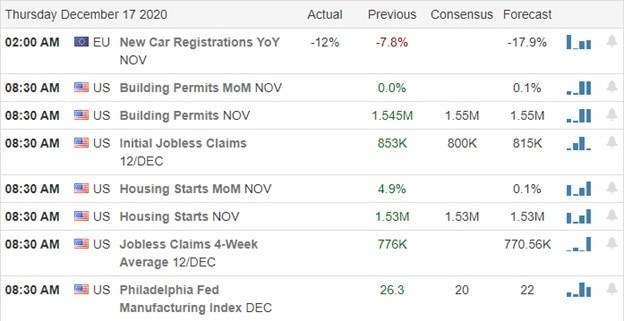

The major economic news for Thursday includes Nov. Building Permits, Nov. Housing Starts, Weekly Initial Jobless Claims, and the Philly Fed Mfg. Index (all at 8:30 am). The major earnings reports include CAN, GIS, JBL, NAV, RAD, SAFM, and WOR all before the open. Then after the close BB and FDX report.

With a considerable amount of economic data at 8:30 am, it is hard to gauge the open just yet. However, the bulls have the upper hand at the moment. With the announcement of a stimulus deal ready for voting and the approval of another vaccine expected, they should have the edge later in the day as well. However, we are counting on politicians and bureaucrats to deliver as expected. So, continue to be careful not to bank too much on the news. Remember a lot of potentially bad news from the virus itself is still possible.

Keep working the process and booking those base hits. Money in the bank trumps a “possible lottery ticket” every time. Keep your discipline and respect the trend, support and resistance, and price action. In short, get rich slowly…one trade at a time, just consistently achieving goals.

Ed

Swing Trade Ideas for your consideration and watchlist: WYNN, CHFS, SONO, VALE, AMD, CLF, X, BLNK, DKNG, CELH, FTCH. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Just 2-weeks before Christmas, Senate leader McConnell congratulates Biden as the president-elect, and he and Schumer say a stimulus funding deal is on the way. That has the futures pointing to new record highs at the open, assuming the data deluge on the economic calendar doesn’t trip up the bulls. Keep in mind that shortly after the open price, action could become light and choppy as we wait for the FOMC decision and press conference beginning a 2 PM Eastern time. Stay on your toes and prepare for the possibility of some price volatility.

During the night, Asian markets closed the day mixed but mostly higher following the U.S. rebound on Tuesday. European indexes are advancing across the board following a positive global growth trend. Here in the U.S., the bulls are fueled up on stimulus hopes ahead of a big day of economic reports. Buckle up it could prove to be a wild ride.

Economic Calendar

Earnings Calendar

The hump day earnings calendar is a light one, but we have a couple of reports worth a look. Notable reports include LEN & TTC.

News & Technicals’

After meeting yesterday on the stimulus bill, Senators McConnell and Schumer hope to soon progress on the funding deal. Hopefulness that the spending bill will soon be on the way is inspiring the bulls once again this morning, likely setting new record highs at the open today. However, attention will quickly turn to the busy economic calendar with Retail Sales, PMI Composite, Business Inventories, Housing Market Index, and EIA Petroleum Status. If that’s not enough to keep traders guessing, we have the FOMC Announcement and the Chairman’s press conference to keep the price volatility alive. In a move that seems to put the presidential election to rest, Senate Leader McConnell congratulates Biden on his win and urges Republicans not to reject the president-elect’s victory.

The bullish trends remain, and with hopes of more stimulus futures point to more record highs this morning. That said, clues are warning that a little caution is warranted. The Absolute Market Breadth indicator continues to downtrend even as the market rallies, suggesting fewer and fewer stocks keep the rally alive. Also, the T2122 indicator is once again suggesting a short-term over-extension. Stay with the trend but have a plan to protect your profits and capital if sentiment begins to shift quickly. Monday’s big rehearsal should serve as a reminder that bears still exist and how quickly the bullish tide can recede from this elevation.

Markets gapped up eight-tenths of a percent before grinding sideways for a few hours. After a small mid-day rally, the ground sideways again the rest of the day, closing near the highs. On the day, SPY closed up 1.34%, DIA up 1.18%, and the QQQ up 1.07%. The VXX fell over 4.5% to 17.56 and T2122 spiked back up deep into the overbought territory at 95.41. 10-year bond yield rose again to 0.908% and Oil (WTI) rose over a percent to $47.54 (the highest since late February).

During the day, House Speaker Pelosi invited her 3 counterpart leaders (House Minority Leader McCarthy, Senate Majority Leader McConnell and Senate Minority Leader Schumer) to a meeting to discuss stimulus and a government funding extension. The four met just after the close, adjourned and then reconvened at 7:30pm. This meeting came after she completed a hour-long negotiation call with Treasury Sec. Mnuchin. McConnell also told reporters Congress would not leave town until a Covid package was complete. There was no report after the evening session, but the developments have raised hope for a deal.

In a follow-up to a previous story about a new EU Law which can fine tech companies up to 10% of their global revenue if they don’t act as good gatekeeper, FB attacked AAPL overnight in praising the new law. A FB spokesman went on to say they hoped the new law will keep AAPL in check from harming consumers and developers. This came after AAPL had previously said it was enabling a privacy feature to allow users to block apps from tracking them across different platforms. (Of course, AAPL will still track users over those platforms.) AAPL responded that FB’s real problem was that its business model is about invasive tracking of consumers. So, this spat is not as much related to the law as it is over AAPL trying to assert dominance over which tech company controls all the data about user’s lives, habits, and preferences to enable it to sell better marketing to advertisers. This will eventually become a hot topic in the US as well.

Related to the virus itself, US infections continue to rage as the US. The totals have risen to 17,143,942 confirmed cases and 311,073 deaths. We are now seeing 7-day averages of 216,733 new cases and 2,528 deaths per day. MRNA submitted the paperwork for approval of their vaccine Tuesday. Also during the day, the FDA approved the first over-the-counter rapid home covid-19 test (from an Australian company). FL reported that a PFE production problem has caused the next two weeks of vaccine shipments to that state to be placed on hold. NYC Mayor DeBlasio says he expects another city-wide lockdown right after Christmas based on the current trends.

Globally, the numbers rose to 73,938,418 confirmed cases and the confirmed deaths are now at 1,644,775 deaths. As a reference, the world is averaging about 628,000 new cases and almost 11,000 new deaths per day. In the UK, Health Minister Hancock announced a new mutation of the virus has been found, which is spreading faster than the original variants, especially in specific places like London. In related news, London was placed under the country’s toughest tier of restrictions as cases spike in the city. In addition, two of the largest British Medical Journals have posted editorials pleading with PM Johnson to not relax restrictions over Christmas as he has promised he will. At the same time, in Northern Ireland, hospitals are beyond full capacity with at least one hospital using parked ambulances to hold dozens of over-flow patients.

Overnight, Asian markets were mostly in the green. Taiwan (+1.68%) was by far the leader among gainers with Hong Kong (+0.97%) and Australia (+0.72%) being more typical. The only red seen was modest losses in Chinese exchanges. In Europe, we see a similar picture so far today. Only Belgium and Finland show any red (modest) as most exchanges are solidly bullish mid-day. The FTSE (+0.98%) is u, as is the DAX (+1.54%), and the CAC (+0.61%). As of 7:30 am, US futures are pointing to a modestly bullish open. The SPY is implying a +0.26% open, the DIA implying a +0.23% open, and the QQQ implying a +0.17% open at this point in the premarket.

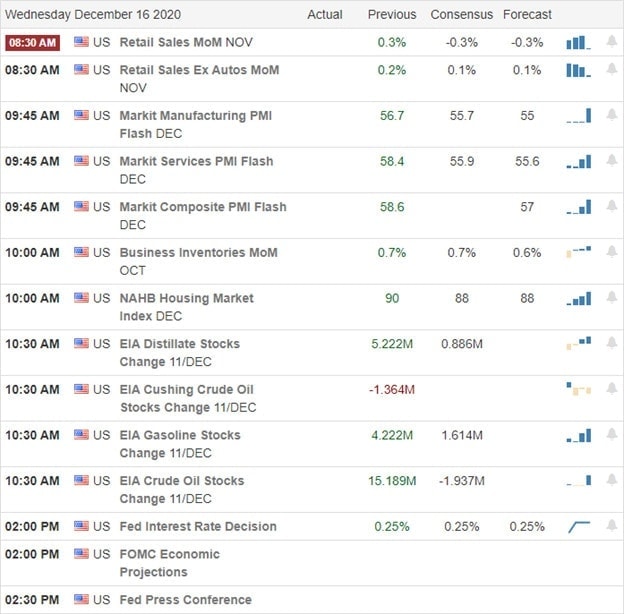

The major economic news for Wednesday includes Nov. Retail Sales (8:30 am), Dec. Mfg. PMI and Dec. Services PMI (9:45 am), Oct. Business Inventories (10 am), Crude Oil Inventories (10:30 am), FOMC Interest Rate Decision, Fed Interest Rate Projections, and FOMC Statement (all at 2 pm), Fed Chair Press Conf. (2:30 pm). Some financial news outlets are worrying over a possible disappointment by the Fed, saying we may see a lessening of the Doveish tone, which may spook markets. The major earnings reports on the day are limited to TTC before the open and both ABM and LEN after the close.

With a considerable amount of economic data today and hope for more progress on a stimulus deal, the bulls may have the edge, but markets may wait to see what the Fed tone is this afternoon before making any big moves. Just remember that it’s politicians that are behind stimulus news. So, anything that comes out are just as likely to be positioning as they are to be a deal announcement. The only edge a deal has remains time pressure as the lawmakers want to leave town as soon as possible. So, just be careful to not get carried away on market news.

Maintain discipline to your trading rules and focus on your process. As always, respect the trend, support and resistance, and price action. Put those singles and doubles in the bank when the market gives them to you. Don’t swing for the fences on every trade. As they say, Bulls make money and Bears make money, but pigs get slaughtered. So, leave the top and bottom picking to the traders who need their ego stroked more than they need to make money.

Ed

Swing Trade Ideas for your consideration and watchlist: PLUG, WFC, NIO, BLNK, CPRI, EYE, CLF, SPWR. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Yesterday was a mixed bag of results in the indexes as vaccine news seems to have lost some of its power to inspire the bulls facing a long winter with more lockdown restrictions likely. However, with the healthcare system bursting at the seams with pandemic patients, Congress feels the pressure to pass a stimulus bill by the end of the week. Could this perhaps inspire a Santa Claus rally, or has is it already baked into the current index prices. Something ponders as you plan your risk facing a hectic week of economic data ahead.

Overnight Asian markets closed in the red across the board, responding to a resurgence of virus concerns. European markets trade cautiously mixed this morning with Brexit talks in focus. Here in the U.S., futures point to an overnight reversal as the bulls gain new energy with high hopes of stimulus money soon on the way.

Economic Calendar

Earnings Calendar

On the Tuesday earnings calendar, we have a light day. Notable reports include AOUT and NDSN.

News & Technicals’

Yesterday the vaccine news that pushed the markets higher at the open ran out of energy, creating a mixed bag of results in the indexes. The QQQ and IWM managed to rally while the DIA and SPY sold-off as the VIX rallied, showing a little fear. It would seem the vaccine news has now baked in, and the market is beginning to focus on the genuine possibility of more restrictions and lockdowns impacting business. The Electoral College has confirmed Joe Biden as the next President of the United States and ended the Trump administration’s long legal battle. Futures are once again rising with Congress working to pass a stimulus bill by the end of the week. With the U.S. death toll topping 300K and the health care system strained nearing capacity in many parts of the country, Congress feels the growing pressure to respond. The big tech social media giants face hefty fines under new UK rules as the U.S. steps up with substantial antitrust pressure of their own.

Although the DIA and SPY selling was significant, the daily charts remain in bullish trends but signal a bit more caution is warranted. It is still possible that the indexes experience a Santa Claus rally is a stimulus bill does get passed. Still, we should also consider the possibility that stimulus hopes have already been priced into the market. With pandemic lockdown restrictions on the rise and a long winter ahead, the stimulus bill’s passage may well become a sell the news event. Yesterday’s price action points to growing volatility and points to the danger of chasing stocks that are already quite extended. We have a lot of data coming our way in the next few days, so plan your risk carefully and remember to take some profits along the way.

Markets gapped up about 0.65% Monday and after a grind sideways for about an hour the large-caps sold off. However, the QQQ maintained their sideways grind all day long. At the close, the SPY and DIA printed ugly black candles while the QQQ left a high wick. On the day the SPY was down 0.47%, the DIA was down 0.63%, and the QQQ gained 0.73%. The VXX gained 2.3% to 18.42 and T2122 fell sharply back into the mid-range at 51.75. 10-year bond yields rose slightly to 0.895% and Oil (WTI) gained three-quarters of a percent to $46.94 (the highest close since March).

During the day, a bipartisan group from the Representatives proposed a $908 billion stimulus compromise bill in the House. Interestingly, this bill essentially mirrors the bipartisan proposal made in the Senate a few weeks ago, but which Senate Majority Leader McConnell would not endorse and has said should be replaced by the White House’s late proposal. The Senate bipartisan group plans to introduce their proposal as 2 bills later Monday. One includes both the business immunity and $160 billion in aid for state and local governments. The other includes all other provisions that have been essentially agreed in negotiations.

In Brexit news, there remains no deal with both sides saying they are far apart. All the deadlines for reaching a deal that can be debated in the respective Parliaments and implemented in time have now passed. Still, the two leaders claim there is still hope with two weeks left until a crash-out of the UK-Europe trade deal. Related to this, the UK has taken action similar to what President Trump wants in the US. The British bill will hold websites (specifically social media) liable for what is posted by any of their users. Fines range up to 10% of global revenue per incident of what the government then says is harmful content.

Related to the virus itself, US infections continue to rage as the US. The totals have risen to 16,942,980 confirmed cases and 308,091 deaths. We are now seeing 7-day averages of 218,226 new cases and 2,527 deaths per day. However, vaccinations did begin Monday in a relative handful of hospitals across the country. The majority of states have received at least some doses of vaccine in a herculean logistics effort. Sec. Azar (HHS) said that if vaccines from MRNA, AZN, and JNJ are all approved quickly, it may be possible for each American who actually wants one to get their first dose by the end of March. This comes as GOOG pushed back the company’s return to offices until at least September.

Globally, the numbers rose to 73,292,455 confirmed cases and the confirmed deaths are now at 1,630,581 deaths. As a reference, the world is averaging about 627,000 new cases and almost 11,000 new deaths per day. In the UK, Health Minister Hancock announced a new mutation of the virus has been found, which is spreading faster than the original variants, especially in specific places like London. In related news, London was placed under the country’s toughest tier of restrictions as cases spike in the city. In addition, two of the largest British Medical Journals have posted editorials pleading with PM Johnson to not relax restrictions over Christmas as he has promised he will. In Germany, the Health Minister urges the EU to follow the UK and US leads and approve a vaccine before Christmas.

Overnight, Asian markets were mixed and flatish, but leaned to the modestly red side. Hong Kong (-0.69%) and Australia (-0.43%) paced the losing exchanges. On the other side, Malaysia (+0.68%) and Shenzhen (+0.39%) led the gainers. However, most Asian exchanges were moderately down on the day. Meanwhile, in Europe, we are seeing a mixed but more active market. The FTSE (-0.35%) is down with the CAC (+0.28%) modestly higher and the DAX (+0.71) bullish so far. However, the biggest moves are seen to the downside by smaller exchanges (Portugal -0.95% and Denmark -0.93%) so far today. As of 7:30 am, US futures are pointing to a bullish open. The SPY is implying a +0.71% open, the DIA implying a +0.63% open, and the QQQ implying a +0.60% open at this point in the premarket.

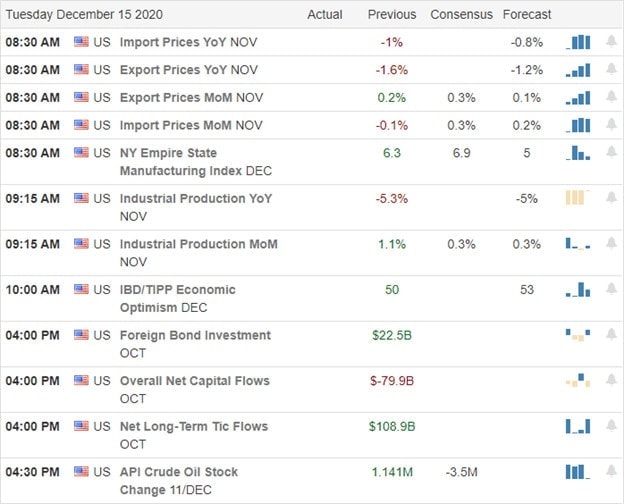

The major economic news for Tuesday is limited to Import/Export Price Indices and NY Empire State Mfg. Index (both at 8:30 am) and Nov. Industrial Production (9:15 am). There are no major earnings reports on the day.

With little economic and no major earnings data, the hope surrounding the beginning of vaccinations and hope for stimulus are likely to give the bulls an edge at the open. However, remember Monday, when a gap higher was met with a selloff by the end of the day. Also, keep in mind that politicians are involved in the stimulus and government funding extension negotiations. This just means that posturing and who knows what kind of news could pop-up at any time until the bills are signed. Also, remember we remain near all-time highs. So, just be careful to not get carried away on either side of the market.

As always, respect the trend, support and resistance, and price action. Stay disciplined to your trading rules and trust your process. Keep taking those singles and doubles that the market offers you. Don’t try to wring every penny out of every last share. It’s better to sell into strength and book the sure profit. Leave “top picking” to the traders who need their ego stroked more than they need to make money.

Ed

Swing Trade Ideas for your consideration and watchlist: EYE, PZZA, DKNG, AMBA, KO, FLEX, PENN, PTON. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service