Bears Shrug Off Strong Earnings

Markets gapped up slightly on Tuesday, but then ground sideways with a slight bearish lean. This action resulted in Dark Cloud Cover candles in the SPY and DIA and a Doji in the QQQ (which also closed at yet another all-time high close). However, overall, it was a flat day in which SPY lost 0.16%, DIA lost 0.08%, and QQQ gained 0.15%. VXX rose less than a percent to 17.20 and T2122 fell back further into the mid-range at 63.01. 10-year bond yields were flat at 1.033% and Oil (WTI) was also flat at $52.75/barrel.

After the close, AMD and MSFT both posted beats on both the top and bottom line. In fact, AMD revenue was up 45% for the year in 2020 and said they expect 37% revenue growth in 2021. For its part, MSFT revenue rose 17% on an annual basis (up from 12% the prior quarter). Meanwhile, SBUX beat earnings estimates despite a 5% drop in same-store sales for the quarter as the company announced its COO is leaving to take a CEO role elsewhere. However, the company missed on the earnings line.

Weekly mortgage demand fell again by 4%, but remain 16% higher than a year ago. This comes as 30-year fixed rates rose from 2.92% last week to 2.95% in the most recent week. However, the housing boom price inflation is being reflected in the size of mortgages. This is reflected in the average new loan amount being at a record $395,200.

Related to the virus itself, US infections continue to rage as the US. The totals have risen to 26,011,222 confirmed cases and 435,452 deaths. The number of new cases fell in 47 states again as the average new cases has fallen to 171,270 new cases, but deaths rose again and remain high at 3,417 per day. In fact, with 5 days left, January is already the deadliest month so far in terms of the virus. President Biden announced the purchase of 200 million more doses of vaccine and set a goal of American life returning to normal by the end of summer. This new purchase includes 100 million doses from each PFE-BTNX and MRNA. In addition, the administration announced that next week the shipments to states will increase from 8.6 million doses/week to 10 million (a 16% increase), to be distributed based on state populations. Finally, JNJ says it is optimistic that Phase 3 trial result data on their own vaccine will be available to be submitted next week.

Globally, the numbers rose to 100,929,027 confirmed cases and the confirmed deaths are now at 2,169,680 deaths. In good news, the world’s average number of new cases is down again to 585,431 per day, but deaths remain high at 14,331 new deaths per day. Ireland extended its national lockdown until March 5. In Germany, the capital city of Berlin will now require two tests instead of one for everyone being tested in an effort to detect new variants earlier and prevent the closure of any more hospitals. In an effort to prevent a situation like the AZN vs EU tension over vaccine delivery, French drugmaker Sanofi has struck a deal to license the PFE-BTNX vaccine and will make 125 million doses of the vaccine exclusively for the EU.

Overnight, Asian markets were mixed on moderate moves. Japan (+0.31%), Shenzhen (+0.28%), and Taiwan (+0.27%) were among the winners. South Korea (-0.57%), Hong Kong (-0.32%), and Australia (-0.65%) were among the losers. India (-1.91%) was a outlier to the downside. In Europe, markets are strongly red across the board. The big 3 bourses show FTSE (-1.00%), DAX (-1.72%), and CAC (-1.27%) as of midday. At 7:45 am, US Futures are also pointing toward a significant gap down. The DIA is implying a -0.88% open, the SPY implying a -1.02% open, and the QQQ implying a -0.66% open.

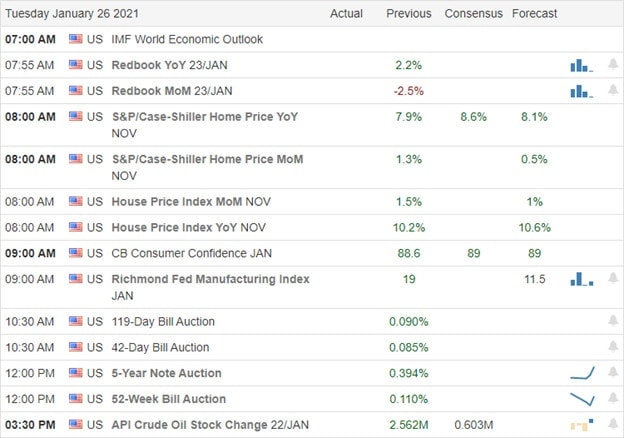

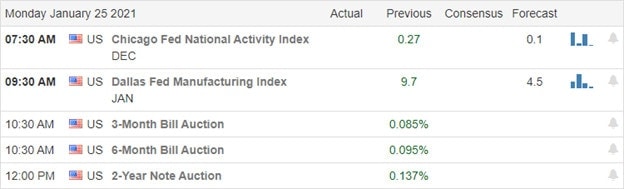

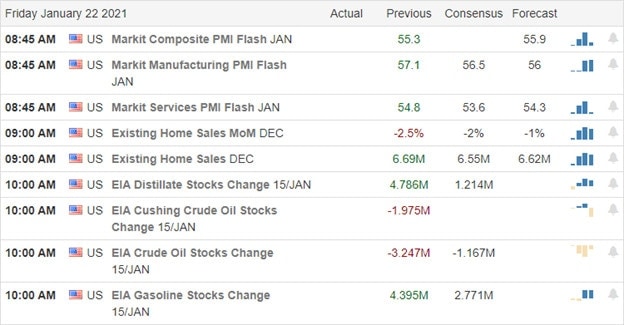

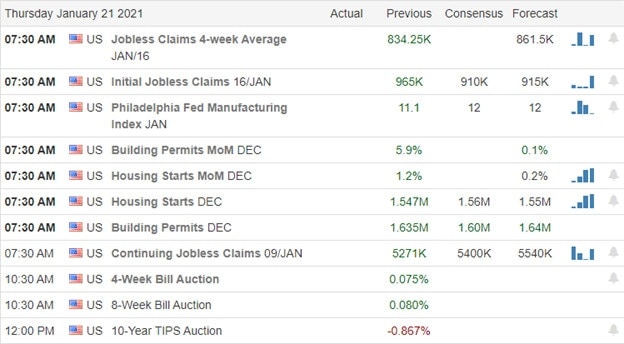

The major economic news for Wednesday includes Dec. Durable Goods Orders (8:30 am), Crude Oil Inventories (10:30 am), FOMC Rate Decision and FOMC Statement (2 pm), and the FOMC Press Conf. (2:30 pm). Major earnings reports on the day include ABT, APH, ANTM, T, ADP, BX, BA, EAT, GLW, GD, HES, KNX, NDAQ, NSC, OSK, PGR, TEL, TDY, TXT, and VFC before the open. Then after the close, AMP, AAPL, AVT, CACI, CP, CCI, EW, FB, HOLX, LRCX, LSTR, LVS, LEVI, and MTH report.

Despite strong earnings from major players, markets seem poised to drop at the open, perhaps on profit-taking new all-time highs or maybe on fear over what the Fed will do. Regardless, watch your longs closely and be cautious chasing any new positions at the moment.

There will be another day and another trade. Don’t feel like you have to trade every day. That’s one of the benefits of trading. We can take a day off when conditions (or our mood) warrants. As always, follow the trend, respect support and resistance, and don’t chase the moves you missed. Lock in your profits when you achieve trade goals and stick to your discipline. Remember, trading is a long-term game. We don’t have to try to get rich every day.

Ed

Swing Trade Ideas for your consideration and watchlist: AAOI, SIG, MJ, AG, FCEL, BLNK, SRNE, PLUG. You can find Rick’s review of those tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service