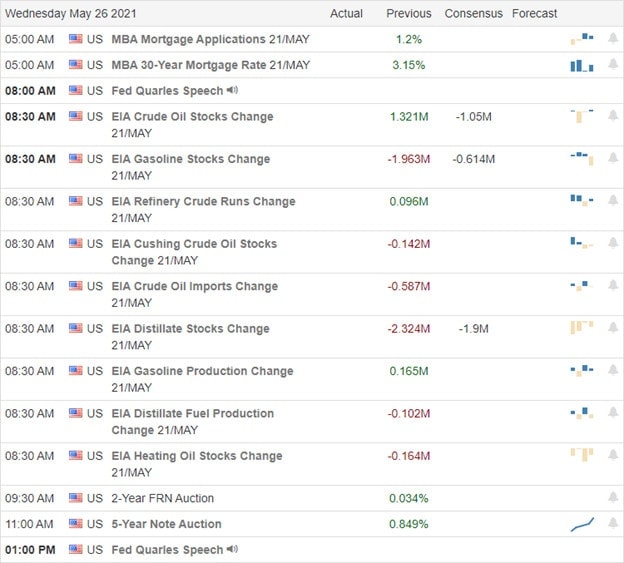

The Amazon antitrust action by the Washington D.C. attorney general quickly dampened the bullish energy yesterday. Indexes took a little break resting at or near price resistance levels in the charts. The IWM is the only index that suffered some technical damage as it once again failed at its 50-day average. Keep in mind after the Thursday morning economic reports, don’t be surprised if volumes begin to decline as traders escape early to extend Memorial day vacations. Plan carefully as we slide into a 3-day weekend and begin summer trading.

During the night, Asian markets closed with modest gains led by the HIS gaining 0.88%. However, European markets are trading very cautiously this morning near the flatline but mostly lower when writing this report. As earnings roll out this morning, the U.S. futures point to a bullish open ahead of the Petroleum numbers as they test overhead resistance levels.

Economic Calendar

Earnings Calendar

We have just over 30 companies listed on the earnings calendar this morning, but several are unconfirmed reports. Notable reports include NVDA, ANF, AEO, BBW, CPRI, DKS, APPS, ELF, NXGN, PDD, PSTG, SNOW, & WDAY.

News & Technicals’

Washington D.C. attorney general Karl Racine began an Amazon antitrust action claiming the company is unfairly raising consumer prices. The lawsuit alleges the company utilizes monopoly pricing power contracts with third-party sellers. An ad was running in the UK stating, “time to buy,” Bitcoin was banned by the Advertising Standards Authority. Treasury yields traded mixed this morning, with the 10-year rising slightly to 1.567% while the 30-year declined slightly to 2.256%. China is once again failing to live up to its trade commitments in the phase one trade deal. Chinese purchase of U.S. goods through April is 73% of what they should be according to the agreement. China is also in the news for cracking down on cryptocurrency mining activities proposing punishments for companies or individuals involved. Being a central hub of crypto mining activity could create more price volatility in the digital currency.

Technically speaking, the DIA and SPY are in pretty good shape though still challenged by overhead resistance. The QQQ and the IWM have the biggest hurdles to overcome with significant price resistance levels above. That said, the bulls are once again pumping the premarket, trying to inspire buyers as the morning earings rollout. Later this morning, we will get a reading on the Petroleum Status that could be very important for the IWM that once again failed at its 50-day average yesterday. Remember, as we slide into a 3-day weekend, the volumes could become light as traders head out early to extend their vacations. Plan your risk accordingly.

Markets gapped up modestly on Tuesday and the immediately began fading the gap. After the first hour, all three major indices were back down to at least flat and then proceeded to grind sideways in a tight range the rest of the day. This left us with something close to a Dark Cloud Cover candle in the SPY and a Bearish Engulfing in the DIA. On the day, SPY lost 0.20%, DIA lost 0.22%, and QQQ gained 0.15%. The VXX was flat at 37.70 and T2122 fell to 65.43. 10-year bond yields fell again to 1.557% and Oil (WTI) was just South of flat at $65.87/barrel.

After the close San Francisco Fed Pres. Daly told CNBC “the economy is strong, but it’s way too early to tighten policy.” She also described her stance on inflation as “firmly in the transitory camp” (referring to her previously stated position that inflation is not snowballing and will subside on its own starting early in 2022). In an unrelated story, Corn futures fell 6% on the day (a massive move in futures) as markets fear of a larger than expected supply hit commodity speculators hard. This move was based more-or-less solely on a USDA report saying that 90% of intended corn acres have been planted as of Sunday. (While ahead of last year at this time, this is just in-line with a normal planting year.)

The Attorney General of the District of Columbia sued AMZN Tuesday on the basis of anti-trust activity. The suit alleges AMZN maintained a monopoly through pricing contracts (a “price parity clause” in their contracts with third-party sellers) that prevent price competition. The cluses prohibit third-party sellers from selling their products cheaper in any other venue than the AMZN Marketplace, and lets the company penalize any vendors that violate that clause. DC claims this amounts to making AMZN Marketplace a virutal monopoly and reduces price competition that hurts consumers. AMZN responded by saying “the DC Atty. Gen. has the situation exactly backwards” sicne their marketplace helps third-party sellers exists and therefore generally guarantees price competition overall.

Related to the virus, new US infections continue to fall. The totals rose to 33,947,189 confirmed cases and deaths are now at 605,208. However, the number of new cases is falling again and are back down to an average of 24,668 new cases per day (the lowest number since June). Deaths are still plateauing or falling more slowly, but are now down to 550 per day (the lowest number since March 2020).

Globally, the numbers rose to 168,572,477 confirmed cases and the confirmed deaths are now at 3,501,270 deaths. The trends are better again as we have seen a slowing in the rate of increase now that India has passed its peaked. The world’s average new cases are falling quickly now, but remain at 569,439 new cases per day. Mortality, which lags, is also falling, but remains at 11,609 new deaths per day. India surpassed 27 million total cases, but the daily new case count was below 200,000 for the first time in over a month. Meanwhile, Malaysia now has more covid cases per million people than India (about 33% more) as of Sunday. While Malaysia is a small country, it borders much larger countries and trade routes.

Overnight, Asian markets were mostly in the green on modest moves. Thailand (+1.08%) and Hong Kong (+0.88%) led the gains while Shenzhen (-0.35%) paced the losses. In Europe, markets are lean to the red side so far today. The FTSE (-0.29%) and DAX (-0.18%) are down modesty while the CAC (+0.03%) is flat. The rest of the continent is split on modest moves. As of 7:30 am, US Futures are pointing to a positive open in the markets. The DIA is implying a +0.27% open, the SPY implying +0.35% open, and the QQQ implying +0.42% open.

The major economic news scheduled for Wednesday is limited to Crude Oil Inventories (10:30 am) and a Fed speaker who presdents at two events (Quarles at 10 am and 3 pm). Other new includes the CEOs of the major banks (JPM, C, MS, BAC, WFC, and GS) begin two days of grilling in front of Congress today. Major earnings reports before the open include ANF, CPRI, DKS, LI, and PDD. Then after the close, UHAL, AEO, CHNG, DBI, DXC, MOD, NVDA, WSM, and WDAY report.

Bitcoin has climbed back above $40,000 this morning, 33% above the lows of last week, but still 38% below the April highs. At the same time, Gold rose overnight to over a 4-month high (back above $1,900/oz.). With limited news planned and bond yields in check, perhaps the Fed statements have alleviated the inflation fears for the moment. Whether that is true or not, it appears the bulls will make the opening push at the bell again this morning. However, remember that we still have resistance overhead and the bulls are showing to be tentative after a few strong days.

Stick with the trend and respect support and resistance levels (but don’t just assume they will hold). As always, keep locking in profits as soon as you achieve your trade goals and maintain discipline by following your trading rules. Consistency is the key to long-term trading success. So, keep hitting singles and doubles rather than swinging for the fence.

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

As inflation fears subsided, the index chart technicals continued to improve yesterday. That said, price action remains challenging, and it’s worth noting that this all-or-nothing market environment has swung up and down nearly 2000 points in the last 7-days. Challenging may be an understatement! We still have overhead resistance levels to overcome, so be careful chasing stocks well above support and near resistance. New records may be just around the corner, but we still can’t rule out bear attacks near resistance highs. Stay focused on price action for clues.

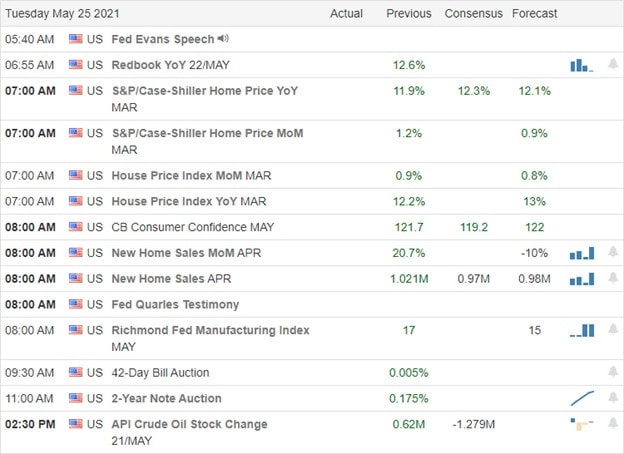

Overnight Asian markets rallied strongly, led by SHANGHAI surging 2.40% by the close of trading. Across the pond, the DAX hits an all-time high while the FTSE and CAC trade oddly near the flatline. Ahead of earnings, Case-Shiller, Housing data, and Consumer Confidence numbers, the U.S futures push for another bullish gap up open.

Economic Calendar

Earnings Calendar

We have under 25 companies reporting today, but we have several potential market movers on the list. Notable reports include A, AZO, CBRL, INTU, NAT, JWN, RRGB, SOL, TOL, URBN, & ZS.

New & Technicals’

Elon Musk said he spoke to bitcoin miners, and after doing so, the price surged to near $40,000. Make you wonder how much longer the SEC will allow him to get away with this manipulation and why would anyone want to own something that one person can move the price so dramatically. What’s the next move, Elon? Amazon could announce a deal as early as today to buy MGM Studios. The $9 billion deal would be AMZN’s biggest acquisition since the Whole Foods purchase in 2017. Ahead of Case-Shiller numbers and the New Home Sale figures, Treasuries are drifting lower this morning. The 10-year fell to 1.591%, and the 30-year dipped to 2.283%. After one denial after another, the evidence begins to mount that Covid-19 came from a Wuhan Lab. The WHO has repeatedly said the virus jumped from bast to humans, but there is no evidence that the virus exists in bat populations after extensive testing.

Chart technicals continued to improve yesterday as inflation fears subsided. The tech giants enjoyed substantial rallies pushing indexes toward resistance levels. In this all-or-nothing market environment, I would not rule out the possibility of new record highs in the DIA or SPY by the end of the week. However, with the recent volatility, we should also not rule out the possibility of another bear attack near market highs. Keep in mind the Dow has covered nearly 2000 points in just the last 7-day of trading.

Interestingly the Absolute Market Breadth indicator continues to decline as we surge higher. It is, however, encouraging that the VIX suggests market fear is subsiding. Stay focused and flexible as volatile price action is likely to remain challenging.

The bulls took charge from the start on Monday as markets gapped higher at the open and followed-through for the first hour. However, that was the end of the movement for the day as stocks ground sideways in a tight range the remainder of the day, but ended on a slight pullback in the range. This left us with gap-up candles in all 3 major indices, with the DIA failing to break out of the highs of the last couple weeks. On the day, SPY gained 1.02%, DIA gained 0.56%, and QQQ gained 1.68%. The VXX fell over 4% to 37.73 and T2122 inched closer to the overbought territory at 76.81. 10-year bond yields fell significantly to 1.603% and Oil (WTI) spiked 3.81% to $66/barrel.

Big tech led the way Monday as AMAT, TSLA, and NVDA each gained over four percent. However, the FATMAG stocks all did well with FB and GOOG both gaining over 2.6%, AMZN and AAPL both gaining over 1.3%, and MSFT gained 2.29% on the day. For its part, Bitcoin had another volatile day after dropping below $32,000 on Sunday night, it rebounded 20% Monday after Elon Must tweeted that he had been talking to Bitcoin miners and that they committed to coming up with planned renewable energy plans which he found potentially promising. Also aiding the surge was a JPM bullish call for the stock of the main crypto exchange COIN.

In business news, CNBC reported late Monday that AMZN is very near a deal to buy MGM for between $8 and $9 billion. The deal would add to the AMZN Video content catalog and increase the company’s ability to compete against NFLX, DIS, and the newly merged WarnerMedia and DISCA. Elsewhere, after hours, Bloomberg reported that SQ will soon offer checking and savings accounts in addition to its current merchant (card processing) services. This will add another competitor to the bank space now dominated by JPM, BAC, WFC, C, and USB.

Related to the virus, new US infections continue to fall. The totals rose to 33,922,937 confirmed cases and deaths are now at 604,416. Still, the number of new cases is falling again and is back down to an average of 25,189 new cases per day (the lowest number since June). Deaths are still falling more slowly, but are now down to 543 per day (the lowest number since July 2020). The TSA reported on Monday that air travel was nearly back to 2019 number last weekend with 1.8 million people flying versus a 2019 number of 2.1 million for the same weekend. PFE announced that the first shots of its proposed booster (which combines the covid vaccine with a streptococcus vaccine) were administered as its trial of 6-month post “full vaccination” has begun.

Globally, the numbers rose to 168,032,095 confirmed cases and the confirmed deaths are now at 3,488,576 deaths. The trends are better again as we have seen a slowing in the rate of increase now that India has passed its peaked. The world’s average new cases are falling quickly, but remain at 581,560 new cases per day. Mortality, which lags, is also falling but remains at 11,864 new deaths per day. The Summer Olympics took another hit on Monday as the US added Japan to its “Do not travel” travel advisory list. Meanwhile, Taiwan (the world’s largest exporter of microchips, including TSM) has extended it’s national lockdown by at least 3 more weeks. Since these measures prohibit any gatherings of more than 5 people and require masking at all times, it is reportedly impacting business operations.

Overnight, Asian markets were almost exclusively in the green. New Zealand (-0.87%) was the lone red, with Shanghai (+2.40%), Shenzhen (+2.34%), Hong Kong (+1.75%), and Taiwan (+1.58%) leading the bullish surge. In Europe, markets are slightly more mixed, but remain mostly in the green so far today. The 3 major exchanges FTSE (-0.08%), DAX (+0.74%), and CAC (+0.09%) set the tone as usual, with smaller exchanges tending to slightly larger moves. As f 7:30 am, US Futures are pointing to another positive open. The DIA is implying a +0.26% open, the SPY implying a +0.30% open, and the QQQ implying a +0.43% open.

The major economic news scheduled for Tuesday is limited to Conf. Board Consumer Confidence, April New Home Sales, and a Fed speaker (Quarles) (all at 10 am). Major earnings reports before the open include AZO, CBRL, DY, ESLT, and VSAT. Then after the close, A, INTU, JWN, TOL, and URBN report.

CNBC reports that part of the cryptocurrency’s extreme volatility of late has been caused by large traders using 100-to-1 leverage. This has caused 20% to 30% swings in a day. However, so far this morning, the price of Bitcoin has stabilized. In stocks, the bulls seem to have the premarket momentum again today. However, with no new revelations driving the move, it remains a case of reopening expansion enthusiasm versus fear that overheating will cause the Fed to pump the breaks. As we approach the all-time highs again, there is still resistance overhead. Still, the short-term and long-term trends remain bullish although we seem to be later in the cycle.

Stick with the trend and respect support and resistance levels (but don’t just assume they will hold). As always, keep locking in profits when you achieve your trade goals and maintain discipline by following your trading rules. Consistency is the key to long-term trading success. So, keep hitting singles and doubles rather than swinging for the fence.

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Last week’s bounce substantially improved the technical picture in the DIA and SPY. However, the bulls still have a lot of work to clear overhead resistance levels in the QQQ and IWM. With a busy week of earnings and economic data, anything is possible, but possible traders will have to stay focused and flexible with big price swings. Buying the dip works only if the market moves higher. Remember, the market will top at some point in time, and buying the dip will prove painful. Plan your risk carefully and keep in mind gap up opens near resistance levels can run into entrenched bears. Be careful not to chase.

Asian markets opened the week mixed with modest gains and losses by the close of the session. European markets trade with modest gains this morning, starting the week with a modicum of caution., The U.S. futures point to bullish open with a light day of earnings and economic data as bulls try to inspire enough buying to break through resistance levels. Volatility is likely to remain high and watch for the possible a pop and drop near resistance.

Economic Calendar

Earnings Calendar

We start the week off with 38 companies listed on the earnings calendar with several unconfirmed. Notable reports include API, CRMT, XOG, & NDSN.

News & Technicals’

We have a pretty busy week on the earnings calendar this week, along with housing numbers, durable goods, GDP, and Personal Income to keep traders busy as we wrap up May. As you plan forward, remember that following Monday, the market is closed for Memorial Day. Bitcoin continues its wild fluctuations dropping to 32,000 but trying to start the week positive this morning. Treasury yields are drifting lower this morning, with the 10-year slipping to 1.617% and the 30-year dipping to 2.315%. The Nobel prize-winning economist Robert Shiller believes there is a bubble forming. He says he’s most worried about housing, crypto’s, and stocks calling it a “wild west” mentality among investors.

Last week’s relief rally substantially improved the indexes’ technical picture, but there are still questions to be answered. Rallying to reclaim support levels and break downtrends is the first step, and now we need some proof the bulls can hold them as support. Substantial overhead resistance still exists in the QQQ and IWM. In last week’s bounce, the T2122 indicator moved near overbought levels, and with the futures pointing to a bullish open, we should watch for the potential of a pop and drop pattern. The VIX closed on Friday just above a 20 handle, holding above its 50-day average and price support. So though the technical picture has improved, there are still questions to be answered. I would not rule out the possibility of a rally to end the week that could even make new record highs. However, we can also not rule out the possibility that the bears could defend resistance highs. Stay focused and avoid chasing with the fear of missing out.

Markets gapped higher at the open on Friday, but then traded slowly lower all day, closing near the lows in the SPY and QQQ. The DIA closed as an indecisive Doji candle. On the day, SPY was flat (-0.08%), DIA was just positive (+0.15%), and QQQ was down 0.55%. The VXX fell to 39.48 and T2122 rose up to just outside the overbought territory at 77.19. 10-year bond yields were down slightly to 1.623% and Oil (WTI) shot up 3.13% to $63.88/barrel. Bitcoin ended a tumultuous week on a major down leg, losing 10.26% on the day as China’s State Council concluded they should crack down on bitcoin mining.

After the close Friday, FOMC voter and San Francisco Fed Pres. Daly told Bloomberg that she expects the temporary factors that are leading to inflation “will persist the rest of this year, but will start to roll off at the beginning of next year.” She went on to say that Fed policy is in a good place right now and that policy makers need to be patient and not start tightening too soon. However, on Sunday Bloomberg also reported that the Chinese government is now decreasing infrastructure spending in a bid to reduce the commodity price bubble caused, in-part, by their massive expansion over the last 6-7 months. The report said this did not spell disaster for commodity bulls, since the US expansion is taking up slack with its larger stimulus plans. However, they did say that industrial metals cycles tend to coincide with China’s credit cycle. Which could mean good news in months to come for business input costs (reduced inflation)..

On Saturday, CNBC reported that for the first time in 25 years the ratio of worker pay to corporate profits has started to budge. In other words, the massive layoffs from the global pandemic have caused a situation where companies need to compete for labor in a way not seen since the 1990s. As a result, worker pay grew 3% in the first quarter. However, according to analytics from MCO, the ratio of compensation to profits still remains at the level of the late 1960s. That said, MCD, UA, BAC, and CMG are among the companies saying they will raise wages on average (sometime over the next several years). MCO says this will not impact corporate profitability in the short-term, but if the trend continues it could have an effect in 2023 or 2024.

Related to the virus, new US infections continue to fall. The totals rose to 33,896,660 confirmed cases and deaths are now at 604,087. However, the number of new cases is falling again and are back down to an average of 25,083 new cases per day (the lowest number since June). Deaths are still plateauing or falling more slowly, but are now down to 553 per day (the lowest number since July 2020). The CDC announced that 25 states have now vaccinated at least half of their adult population. This comes as 61% of the adult population has received at least one shot and almost 50% of adults are fully vaccinated.

Globally, the numbers rose to 167,589,687 confirmed cases and the confirmed deaths are now at 3,479,788 deaths. The trends are better again as we have seen a slowing in the rate of increase now that India has passed its peaked. The world’s average new cases are falling quickly now, but remain at 592,614 new cases per day. Mortality, which lags, is also falling, but remains at 12,088 new deaths per day. The Japanese government is decrying a slow uptake in vaccination, even in the main cities planned to host the summer Olympics. Less than 2% of the population is vaccinated and even Tokyo is seeing less than a third of the number of daily vaccinations the government has deemed necessary.

Asian markets were mixed overnight on modest moves, but leaned slightly to the green side. Shenzhen (+0.62%) led to the upside and South Korea (-0.38%) led to the down side. In Europe we see a similar story taking shape as of mid-day. All 3 of the large exchanges are in the green so far, but most of the smaller exchanges are on the red side. The FTSE (+0.18%), DAX (+0.44%), and CAC (+0.02%) are all slightly green at this point in their day. As of 7:45 am, US Futures are all in the green. The DIA is implying a +0.28% open, the SPY implying a +0.43% open, and the QQQ implying a +0.62% open. Oil is higher in premarket by 1.40%.

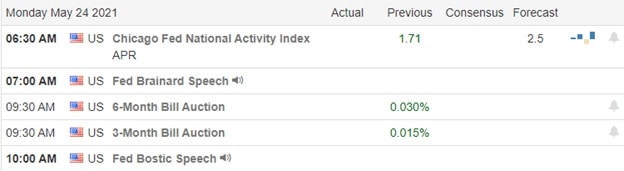

The major economic news scheduled for Monday is limited to two Fed speakers (Brainard at 9 am and Bostic at noon). There are no major earnings reports before the open. However, after the close NDSN reports.

Markets look to be opening inside the range of the last few days. The bulls seem to have the premarket momentum, but there are no new revelations driving the move. It remains a case of reopening expansion enthusiasm versus fear that overheating will cause the Fed to pump the breaks. With a very strong quarter of earnings just behind us and high expectations for strong profits in the current quarter, the bulls have the general momentum. However, there is resistance overhead and we are coming off one hell of a bull run. So, this is a “climbing the wall of worry” situation…meaning we seem to be later in the cycle.

As always, keep locking in your profits when you achieve your trade goals and maintain discipline by following your trading rules. Stick with the trend and respect support and resistance levels (but don’t just assume they will hold). Consistency is the key to long-term trading success. So, keep hitting singles and doubles rather than swinging for the fence.

Ed

Swing Trade Ideas for your consideration and watchlist: KHC, INSG, MARA, INTC, XHB, INO, SPCE, F, SRPT, DDD, RIOT. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

We all enjoy a nice relief rally but keep your eyes focused on the overhead price resistance levels because that will reveal if the bulls have what it takes to plow through bearish defenses. I wouldn’t expect smooth price action with the VIX holding a 20-handle and still above its 50-day average. Though the DIA and SPY hold bullish trends, the QQQ and IWM remain uncomfortably below significant resistance levels. Plan your risk carefully as we slide into the weekend.

Overnight Asian markets ended the week with a mixed and choppy session, with Taiwan surging 1.6%. European markets trade mixed with modest gains or losses as they wait on economic data. Ahead of PMI and Housing data, U.S. futures point to bullish open as bonds pull back slightly.

Economic Calendar

Earnings Calendar

On the Friday earnings calendar, we have a lighter day of reports with just 14 companies listed. Notable reports include BAH, BKE, DE, DSX, FL, & VHC.

News & Technicals’

A nice relief rally began yesterday as the buy the dip traders satisfied their appetite, lifting tech and crypto. The U.S Treasury calls for stricter cryptocurrency compliance with IRS suggesting it poses tax evasion risk. Janet Yellen proposes a global minimum corporate tax rate of 15% and says discussions should continue to be ambitious to push the rate even higher. Israel and Hamas agree to a cease-fire; however, both sides seem very skeptical about it holding as they sling insults back and forth at each other. Treasury yields are drifting slightly lower this morning, with the 10-year dropping to 1.618% and the 30-year coming in at 2.323% ahead of PMI and housing data.

Though we experienced a nice relief rally, the bulls still need to show the willingness to follow through, clearing overhead price resistance levels. The tech giants provided a significant portion of the rally, but a quick look at the charts shows they are still in downtrends. The QQQ was able to get above its 50-day average, so the test now is, can it hold it as support? This morning bond rates are softening slightly, which could be very helpful to the struggling tech sector. The VIX closed the day above its 50-day average and a 20 handle. We should continue to expect significant price volatility and should not rule out the possibility of reversals as we approach price resistance levels. Be careful not to chase as you plan your risk heading into the weekend.

Markets gapped up on better than expected (lower) new Jobless Claims and then the bulls followed-through with the exception of a brief break at noon and another the last half-hour of the day. This left us with a second strong bullish candle in a row and broke the string of losses, but the market is also coming into one of the areas of resistance caused by the action the last two weeks. On the day, SPY gained 1.04%, DIA gained 0.57%, and QQQ gained 1.93%. The VXX lost 5.5% to 40.03 and T2122 rose at bit to 63.56. 10-year bond yields fell to 1.632% and Oil (WTI) fell over 2% to $62.05/barrel.

At the end of the trading day Treas. Sec. Yellen announced that the US has proposed a global minimum corporate tax of 15% to the OECD (Org. for Economic Cooperation and Development). Treasury officials later told the press that the OECD meeting had featured “earnest talks” toward a global minimum tax. The idea is to prevent companies for shifting earnings to hide from taxes as the many major companies do now. Earlier in the day, the Treasury Dept. had announced a stricter crackdown on cryptocurrency usage and said it would require reporting of all transfers worth $10,000 or more. Also separately, the Fed announced it would take the next step in developing its own digital currency this summer (in a move seen as catch-up to the Chinese who have been testing a Chinese Cryptocurrency for over a year).

In the wake of the Colonial Pipeline mess, after the Close Thursday, it was reported that one of the largest insurance companies in the US has paid hackers $40 million in ransom. In a story broke by Bloomberg, it was revealed that CNA paid the massive ransom to regain control of their computer network in late March. Bloomberg said the company would not confirm the ransom paid, but did confirm the hack and said it was a different hacker group (at least in name) than the one that shutdown Colonial. Welcome to the new age.

Related to the virus, new US infections continue to fall. The totals rose to 33,833,181 confirmed cases and deaths are now at 602,616. However, the number of new cases is falling again and are back down to an average of 28,735 new cases per day (the lowest number since June). Deaths are still plateauing or falling more slowly, but are now down to 573 per day (the lowest number since July 2020). The CDC reported that vaccinations rates have fallen over 46% from their peak, but at the same time 38% of American adults are fully vaccinated. However, Dr. Fauci (NIH) reiterated Thursday that we will need booster shots, but that we don’t know yet how soon and suggesting the amount of time between vaccination and booster may actually vary by vaccine.

Globally, the numbers rose to 165,912,336 confirmed cases and the confirmed deaths are now at 3,446,477 deaths. The trends are better again as we have seen a slowing in the rate of increase now that India has passed its peaked. The world’s average new cases are falling quickly now, but remain at 623,846 new cases per day. Mortality, which lags, is also falling, but remains at 12,296 new deaths per day. JNJ announced Thursday that its vaccine has joined PFE, MRNA AZN, and 3 others in a study being conducted by the UK. That study is looking to identify the best seasonal booster shots as follow-on to initial vaccination. The EU also reached a deal on when and how to give Covid-19 Vaccine Passports, which is expected to enable an increase in travel across Europe. While India has now passed 26 million cases, a new focus is on a deadly, post-covid infection called “black fungus” that attacks people with weakened immune systems in that region and that their government is just now starting to track.

Asian markets were mixed overnight, but leaned to the green side. India (+1.81%), Taiwan (+1.62%), and Japan (+0.78%) led the gainers while Malaysia (-0.83%) and Shenzhen (-0.81%) paced the losses. In Europe, markets lean even more heavily to the green side, but on modest moves so far today. The FTSE (-0.06%), DAX (+0.20%), and CAC (+0.50%) are typical with outliers like Greece (-4.03%), Denmark (+1.24%), and Norway (+1.41%). As of 7:30 am, US Futures are pointing to a positive open. The DIA is implying a +0.34% open, the SPY implying a +0.31% open, and the QQQ implying a +0.28% open.

The major economic news scheduled for Friday is limited to Mfg. PMI and Services PMI (both at 9:45 am) and April Existing Housing Sales (10 am). Major earnings reports before the open include BAH, DE, FL, and VFC. Then after the close there are no major reports.

The bulls are looking to follow up on the strong run they have made since the open Wednesday (which to be fair was at a nasty gap-down level). However, we are just now clawing back to the level we were at a week ago and there remains resistance overhead. While yesterday’s news of the Biden administration wanting to clamp down on tax cheats and proposing a global minimum corporate tax don’t seem to be major market threats, the fear of losing an “easy Fed” remains a cloud that is hanging over the bulls head. So, in that sense, our fight back to the all-time highs remains “climbing the wall of worry.”

Don’t forget it’s Friday. So, consider what you need to do to protect against weekend headline risk. You don’t want to get caught like those longs who ran into the Colonial pipeline news 2 weekends ago. As always, keep locking in your profits when you achieve your trade goals and maintain discipline by following your trading rules. Stick with the trend and respect support and resistance levels (but don’t just assume they will hold). Consistency is the key to long-term trading success. So, keep hitting singles and doubles rather than swinging for the fence.

Ed

Swing Trade Ideas for your consideration and watchlist: LAZR, IQ, IRM, XL, NOK, INO, CSCO, INSG. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Though the index charts have taken some technical damage, the DIA and SPY finding the energy to hold at their respective 50-day averages provide hope that a relief rally may soon follow. However, the damage in the QQQ and IWM is much more significant and will require substantial effort by the bulls to reverse the current downtrends and overhead price resistance levels. The elevated VIX suggests we should expect challenging price volatility as the bulls and bears battle for control. Inexperienced traders will likely find this environment very costly due to the speed and range of the point moves, overnight reversals, and whipsaws that are likely to occur.

Asin markets traded mixed but mostly lower overnight though Japan’s exports surged in April. European markets are currently green across the board this morning after the Fed talks of tapering. On the other hand, U.S. futures point to a bearish open though will off the overnight lows ahead of Jobless Claims and the Philly Fed numbers.

Economic Calendar

Earnings Calendar

Today we have just 39 companies listed on the calendar, but several of them have not confirmed their reports. Notable reports include AMAT, BJ, CSIQ, DECK, HRL, KSS, RL, PANW, & ROST.

News & Technicals’

Facebook is facing some court challenges that could lead to a ban on its EU-U.S. data transfers. Blocking their transatlantic data flow will have profound implications for other U.S. tech giants. Bitcoin plunges 30% and at one point touched 30,000 yesterday, which constitutes a 50% haircut from recent highs. Hamas says it sees a cease-fire possible in the coming days, but this fight has gone on for decades and is unlikely to find a resolution anytime soon. The 10-year Treasury yield dipped this morning to 1.663%, and the 30-year fell to 2.371% after investors digested the FOMC minutes, where there were hints that the committee might begin pulling back on debit purchases.

Yesterday’s sell-off created some technical damage in the index charts, but there was also a few rays of hope, with the DIA and SPY finding at least some temporary support at their 50-day moving averages. Unfortunately, the QQQ and IWM are under this critical psychological level but managed to hold the price supports of last week’s selling. Recovery, however, could be challenging with both technical and price action resistance levels overhead blocking the potential relief rallies. The VIX closed well below its high of the day but remained quite elevated above a 22 handle so expect considerable price action volatility to continue. Experienced day-traders will likely have the upper hand in this environment, while swing traders may find the quick whipsaws and complete overnight reversals very challenging.

Markets did a classic gap-and-reverse on Wednesday as the bears gapped all 3 major indices significantly lower and then the bulls slowly rallied all day. All 3 indices printed strong white candles, but only the QQQ managed to completely close the gap. On the day, SPY lost 0.28%, DIA lost 0.52%, and QQQ gained 0.11%. The VXX rose almost 5% to 42.35 and T2122 fell down close to the oversold territory at 26.45. 10-year bond yields rose to 1.674% and Oil (WTI) fell over 3% to $63.40/barrel.

Bitcoin had one hell of a roller-coaster day Wednesday. It suffered more than a 30% drop (from over $43,000 to $30,000) before putting in a 30% rally (from $30,000 back up over $42,000) and then finally settled closer to the top of the range ($38,900). While some analysts called this a capitulation, others explain the fall as a reaction to the recent reversal of acceptance of the cryptocurrency. For example, the IRS and DOJ have recently both launched investigations into the main cryptocurrency exchange, China warned their financial institutions not to provide services related to any cryptocurrency, and TSLA announced no longer accepting the would-be currency in payment for their products.

In the April FOMC Meeting Minutes released Wednesday, the Fed basically said what it has been saying for months. They are unconcerned about that they see as transitory inflationary pressures. Specifically, “there is no need to change policy now, but it might be appropriate to consider tapering at some point” was the consensus view. Markets did not react since this was a known position. However, some analysts say the minutes showed the Fed may reconsider if rapid progress continues. As always, the glass is either half full or half empty depending on your perspective.

Related to the virus, US infections are rising again after plateauing at a level above the fall level. The totals have risen to 33,802,324 confirmed cases and deaths are now at 601,949. The number of new cases is falling again and are back down to an average of 29,975 new cases per day (the lowest number since June). However, deaths are still plateauing at the new lower levels, now at 591 per day (the lowest number since July 2020). Dr, Fauci (NIH) told the press that infection rates are decreasing in all 50 states, down 18% nationally from one week ago. He told Axios that should the trend continue, it will be safe enough to resume indoor activities like dining soon. However, in answer to one question he reiterated that it is likely we will need a booster shot within a year of completing vaccination. JNJ announced Wed. evening that 100 million doses of its vaccine are held up in FDA inspection due to contamination problems at one of JNJ’s contract manufacturers (Emergent). No word on whether this is somehow related to JNJ falling behind promised delivery schedules to the EU.

Globally, the numbers rose to 165,629,929 confirmed cases and the confirmed deaths are now at 3,433,602 deaths. The trends are slightly better again as we have seen a slowing in the rate of increase no that India is believed to have peaked. The world’s average new cases are falling quickly now, but remain at 637,518 new cases per day. Mortality, which lags, is also falling, but remains at 12,360 new deaths per day. The UK is taking heat as it defends continuing to allow direct flights from India amid a 28% surge in cases of the Indian 617 variant. However, the number of cases is still just under 3,000 per day. As if semiconductor shortages were not bad enough already, Taiwan is now battling its worst outbreak (which pales in comparison to neighboring China, let alone the US). So far, businesses have not been ordered shut. However, that country is the world’s largest supplier of silicon semiconductors.

Asian markets were mixed overnight on mostly modest moves. New Zealand (+1.27%) and Australian (also +1.27%) were the largest movers with India (-0.83%) pacing the losses. In Europe, markets are broadly green with only Russia and Norway in the red. The FTSE (+0.21%), DAX (+0.52%), and CAC (+0.58%) are fairly typical of the continent at this point in the day. As of 7:30 am, US Futures are pointing to a mildly down open. The DIA is implying a -0.33% open, the SPY implying a -0.19% open, and the QQQ implying a flat -0.03% open.

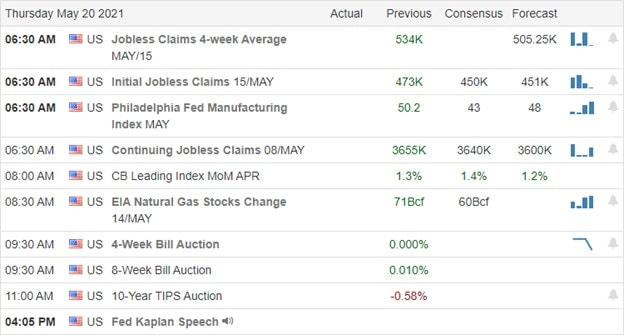

The major economic news scheduled for Thursday is limited to Weekly Initial Jobless Claims and Philly Fed Mfg. Index (both at 8:30 am). Major earnings reports before the open include BJ, CSIQ, HRL, KSS, WOOF, RL, and TCEHY. Then after the close, AMAT, DECK, ENS, FLO, and ROST report.

After the nasty gap-down, the bulls were in charge all day Wednesday. However, they came up just a bit shy of erasing the gap except the QQQ which just barely got the job done. All 3 major indices now sit just above support that may have held yesterday. It is very hard to trade a gap-and-fade market. It’s even harder when markets may be at a short-term swing point. So, be careful. With that said, it is likely to be Jobless Claims that call the tune this morning…or more to the point, how those claims can be inferred to impact inflation. This is because it remains the fear of losing an “easy Fed” that has powered the bears for some time now.

If you’re trading this market, be very nimble, hedged and/or small. As always, keep locking in your profits when you achieve your trade goals and maintain discipline by following your trading rules. Follow the trend and respect support and resistance levels. However, don’t just assume they will hold. Consistency is the key to long-term trading success. So, keep hitting singles and doubles rather than swinging for the fence.

Ed

Swing Trade Ideas for your consideration and watchlist: No Trade Ideas today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service