First Q3 Earnings Reports Are Strong

Markets gapped up a bit at the open on Tuesday, but it was another bull trap. Stocks immediately sold off before doing an all-day roller-coaster that ended just up off the lows. So, all 3 major indices have now taken out their 8ema, but are sitting at a recent potential support. On the day, SPY lost 0.24%, DIA lost 0.35%, and QQQ lost 0.35%. The VXX fell almost 2% to 24.63 and T2122 remains in the mid-range at 58.25. 10-year bond yields fell to 1.572% and Oil (WTI) was unchanged at $80.52.

The JOLTs report on Tuesday showed what appears to be serious wage pressure. 4.3 million workers quit their job in August, the highest amount since December 2000. A number of analysts say this is a clear indication that workers were unhappy with their current wages (and past raises) and see the huge number of job openings as a rare opportunity to improve their situations. The only way to address this would be for employers to significantly raise wages to retain as well as draw in new employees. In addition, this first month of data seems to point to “extended unemployment benefits” not being a primary driver for the problem of finding workers. Together, these will mean real earnings pressure for companies without pricing power.

At the close on Tuesday, Bloomberg reported that AAPL is likely to slash iPhone 13 production orders by as many as 10 million units. The company was expected to make 90 million iPhone 13s during Q4, but is now telling partners the number could be as much as 10 million units less. The cited reason is the TXN and AVGO are not able to meet chip demand. For its part, AVGO does not produce the chips they sell, they purchase production capacity from TSM, which may be a read-through to TSM and by extension TSM’s other major customers (AMD, NVDA, QCOM, and INTL).

In market news this morning, JPM posted a significant beat on earnings ($3.74 vs $3.00 per share estimated) but missed on revenue. BLK reported significant beats on both lines while FRC posted more modest beats on both lines. DAL also reported significant beats on both lines on growing travel demand. Weekly mortgage demand continued to stall last week as rates rose. 30-year fixed-rate conforming loan rats rose from 3.14% to 3.18% on average. As a result, refinance loan applications fell 1% while new home purchase loan applications rose 2% versus the week prior.

Overnight, Asian markets were mostly in the green. Taiwan (-0.70%) and Japan (-0.32%) showed the only real red in the region. Meanwhile, Shenzhen (+1.54%), Singapore (+1.43%), and South Korea (+0.96%) led the region higher. In Europe, a similar story is taking shape. Russia (-1.05%) is the only significant red. Meanwhile, the FTSE (-0.09%), DAX (+0.74%), and CAC (+0.24%) are typical of the spread we see across the continent at mid-day. As of 7:30 am, US Futures are pointing toward a mildly positive open. The DIA is implying a +0.11% open, the SPY implying a +0.15% open, and the QQQ implying a +0.34% open at this hour. The Dollar is trading lower, while 10-year bond yields and Oils are both slightly lower in early trading today.

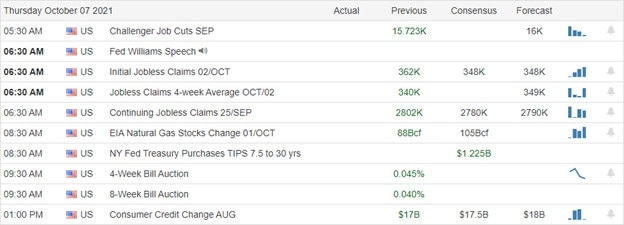

The major economic news scheduled for release on Wednesday includes Sept. CPI (8:30 am), Fed. Budget Balance and Sept. FOMC Minutes (both at 2 pm), and a couple of more Fed speakers (Brainard at 4:30 pm and Bowman at 8 pm). Earnings season kicks off again today with reports scheduled from BLK, SDAL, FRC, INFY, JPM, and WIT before the open. There are no major reports scheduled for after the close.

Premarket prices seem to be modestly bullish this morning as the first indications from earnings are that corporations are doing just fine, despite the fear over inflation, chip shortages, supply chain woes, and Covid. However, remember that the downtrend remains intact and the 8ema seems to be acting as resistance in early action. Trade carefully, today is only the first salvo of earnings data. Don’t jump to conclusions or get caught up in the need for action or FOMO.

Focus on your trading process and on managing those things you can control (while not worrying about things you can’t influence). Watch your current positions before looking to add new trades. Remember, it’s discipline and good trading rules that protect us from ourselves. Consistently take profits when you have them. Don’t let greed get the better of you. Finally, remember that we have monthly options expiring at the end of the week. So, it’s time to think about closing, rolling, or riding into expiration with very little time value left.

Ed

Swing Trade Ideas for your consideration and watchlist: RLX, ANY, GOTU, AG, FSM, NKLA, COST, MO, AOS. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service