EPS Mostly Good As GDP and Claims Next

Markets started the day relatively flat on Wednesday. The QQQ rallied into the late afternoon before selling off hard the last hour of the day. However, the large-caps started their selloff early, but again gained steam the last hour of the day. This all left a big ugly black candles in the large-cap indices, which if you squint might be called Evening Star type. Meanwhile, the QQQ printed a white-body Northern Star type candle (just a gap-up short of a Shooting Star). This left the DIA and QQQ failing at all-time high level resistance and SPY pulling back to test that level as support. On the day, SPY lost 0.44%, DIA lost 0.69%, and QQQ gained 0.23%. The VXX gained 2.2% to 21.95 and T2122 fell to the low-end of the mid-range to 27.86. 10-year bond yields fell strongly to 1.545% and Oil (WTI) fell 3% to $82.11/barrel.

After the close, KLAC, EBAY, ALGN, ORLY, XLNX, EXR, MAA, RJF, DRE, and CINF all reported beats on both lines. Meanwhile, EW, F, and AFL beat on earnings but missed on revenue. CTSH, URI, and RE beat on revenue but missed on earnings. And AVB and FLS both missed on both lines. It should be noted that F crushed earnings by almost doubling the street estimate ($0.51 vs. $0.26 estimate).

In earnings so far this morning, MRK, LIN, AMT, MCO, HSY, LH, SIRI, CMCSA, YUM, BAX, TFX, LKQ, ABMD, NLSN, and ADS have all reported beats on both lines. CAT, NOC, WTLW, SWK, TAP, and TXT all beat on earnings but came up short of estimates on the revenue line. At the same time, AEP and XEL beat on revenue but missed on earnings. Finally, TROW, NEM, and MO missed on both revenue and earnings.

In miscellaneous news out of Washington, leaks are reporting that the Budget Bill that is being negotiated between Democrats has been whittled down again. From an original $3.5 trillion, the current size seems to be $2 trillion, but continues to move lower as more of the progressive agenda is abandoned to secure the vote of WV Senator Manchin and to a lesser degree AZ Senator Sinema. With that said, it appears a deal is very near as President Biden is expected to attend the Democratic meeting this morning, which most believe is a signal a deal will be done by then. Simultaneous to the negotiations of the taxes and spending in the bill, CNBC reports that major business groups are already organizing to fight any new business taxes through lobbying and media spending in the states of key Democratic votes. In particular, they want to fight the “Corporate 15% Minimum Tax” that was agreed globally.

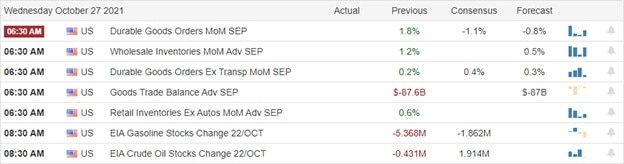

Overnight, Asian markets red across the board. India (-1.94%), Shanghai (-1.23%), and Indonesia (-1.18%) led the losses, but the damage was universal in the region. This came as a higher producer price index and continued electricity crunch are raising the possibility of stagflation down the road a couple of quarters. In Europe, the picture is more mixed at mid-day. The FTSE (-0.28%) and DAX (-0.10%) are slightly lower, but the CAC (+0.60%) is among the half of the continent that is in the green in early afternoon trading. As of 7:30 am, US Futures are pointing toward a green opening as earnings continue to come in strong. The DIA is implying a +0.25% open, the SPY implies a +0.33% open, and the QQQ is implying a +0.58% open at this hour (and ahead of major economic news). 10-year bond yields are up just slightly and Oil (WTI) is off 1.5% in early trading.

The major economic news scheduled for release on Thursday is limited to Q3 GDP and Weekly Initial Jobless Claims (both at 8:30 am) and Sept. Pending Home Sales (10 am). Major earnings reports scheduled for the day include AOS, AGCO, ATI, ADS, AB, MO, AEP, AMT, BUD, AMBP, AVNT, BAX, BC, CARR, CAT, CBRE, CHKP, CMS, CMCSA, DQ, DBD, EXP, EME, FCN, GVA, GPI, HSY, HTZZ, HBAN, ITW, ICE, JHG, KBR, KEX, LH, LECO, LKQ, MDC, MA, MD, MDP, TAP, MCO, COOP, NEM, NLSN, NOK, NOC, NVT, ORI, OSK, OSTK, PATK, PBF, BTU, RLGY, RS, RDS.A, SAIA, SNY, SNDR, SHOP, SIRI, SAH, SWK, STM, TROW, TFX, TPX, TXT, VC, WST, WEX, WLTW, XEL and YUM before the open. Then after the close, ACHC, AMZN, AAPL, ATR, AJG, TEAM, AVTR, AVT, CHE, COLM, DVA, DECK, DXCM, EMN, ERIE, FE, FMX, FTV, GILD, HIG, HUBG, LPLA, MHK, RSG, RMD, SKX, SKYW, SSNC, SBUX, SYK, TEX, TXRH, TFII, X, VALE, WERN, WDC, INT, and AUY report.

Again, the flood of earnings is going to be a main driver. However, don’t overlook the Q3 GDP number possibly changing the mood among traders. Again, I would characterize the reports last night and so far this morning as largely positive. However, there were a handful of high visibility misses, such as TROW and MO as well as CAT missing on revenue. So, be prepared, stay nimble and remember that it is the actual market reaction to the news…not the news itself…that is really important to traders.

The trend remains bullish despite yesterday’s candles and all 3 major indices are still sitting very near all-time highs. Remember, the trend is our friend, but also keep in mind that big dogs AAPL and AMZN report tonight. So, focus on your trading process and on managing the things you can control. Remember that it’s discipline and good trading rules that will win in the long run. And that includes consistently taking profits when you have them and moving your stops. Watch your current positions before looking to add new trades. Trade carefully and think twice about holding through earnings.

Ed

Swing Trade Ideas for your consideration and watchlist: LC, PLBY, LCID, MRVL, F, MCD, OPEN, LVS. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service