Bank Earnings, TWTR Drama, and Ukraine

Markets opened basically flat on Thursday and then sold off the rest of the day. This resulted in black, Bearish Engulfing candles and Oreo Cookie patterns in the SPY and QQQ, with DIA putting in a black candle with all 3 closing on the lows of the day. On the day, SPY lost 1.25%, DIA lost 0.43%, and QQQ lost 2.29%. The VXX rose to 24.99 and T2122 dropped to right in the middle at 50.67. The 10-year bond yields spiked again to 2.827% and Oil (WTI) rose more than 2% to $106.44/barrel.

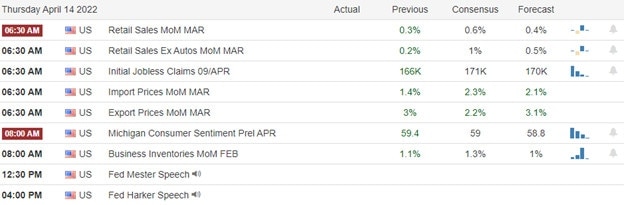

On Friday, we got some positive economic news. The NY Empire State Mfg. Index came in above expectations. The same was true of March Industrial Production, which came in almost double the forecast value (+0.9% vs 0.4% forecast).

SNAP Case Study | Actual Trade

Related to Elon Musk’s hostile TWTR takeover bid, the stock traded in a volatile way Thursday, but never got even close to the offered $54.20/share. It actually closed down 1.68% to $45.08. This seems to imply that the market does not believe the deal will ever happen. Friday, a couple of analysts downgraded the stock as now “being in the middle in an Elon circus.” Also on Friday, a Saudi Prince offered to match Musk’s deal and buy the company at the same price (perhaps offering a more palatable buyer). However, late in the day TWTR board unanimously passed a “poison pill” policy. This means if anybody acquires 15% of company stock without board approval, then other TWTR holders will be allowed to buy additional shares at a deep discount. This would flood the market with shares of TWTR, driving down the price and making a takeover much harder, slower, and more expensive.

So far this morning, BAC and SYF have both reported beating on both lines. At the same time, BK printed a beat on revenue while reporting in-line earnings. However, we should note that BK’s in-line report was still down 11.3% from the prior quarter.

On the Russian invasion story, Russia is continuing to fire missiles at major Ukrainian cities like Karkhiv, Kiyv, and Lviv. Meanwhile, Ukrainian resistance continues to hold out in the last stronghold of the destroyed city of Mariupol. The Russian Donbas offensive is underway with heavy fighting in the town of Kreminna, which is located Southeast of Karkhiv in the Luhansk region. On the economic side, Ukraine has submitted its application questionnaire to join the EU. More importantly, many analysts are now saying that renewed aid is desperately needed as Ukraine is in need of more heavy weapons and, in particular, more ammunition to maintain its fight in the face of the massive Russian assault. So, look for more aid to be coming from NATO countries and new orders to be placed in turn with companies like GD, WCHS, NOC, and RTX.

Overnight, the Asian markets were mixed but leaned to the red side. India (-1.73%), Japan (-1.08%), and Singapore (-0.98%) paced the losses. Meanwhile, Hong Kong (+0.67%), Australia (+0.59%), and Shenzhen (+0.37%) led the gainers. In Europe, stocks are also mixed, but in this case, lean to the upside at mid-day. The FTSE (+0.47%), DAX (+0.62%), and CAC (+0.72%) lead as usual while Russia (-1.76%) is an outlier to the downside in early afternoon trading. As of 7:30 am, US Futures are pointing toward a modestly lower start to the day. The DIA implies a -0.12% open, the SPY is implying a -0.26% open, and the QQQ implies a -0.33% open at this hour. 10-year bond yields are up again to 2.837% and Oil (WTI) is down fractionally in early trading.

The major economic news scheduled for release on Monday is limited to a Fed speaker (Bullard at 4 pm). Major earnings reports scheduled for the day include BAC, BK, SCHW, and SYF before the open. Then after the close, JBHT reports.

In economic news later this week, on Tuesday we get March Building Permits and March Housing Starts. Then Wednesday, we see March Existing Home Sales, Crude Oil Inventories, and Fed Beige Book will be released. On Thursday, we get Initial Weekly Jobless Claims, Philly Fed Mfg. Index and Fed Chair Powell speaks. Finally, on Friday we get Mfg. PMI and Services PMI.

Coming off the 3-day break, it was Elon Musk’s TWTR drama that maintained the spotlight all weekend. Yet, we also find ourselves at the start of another earnings season. And this quarter’s earnings may be more important than many recent quarters’ numbers (and especially guidance) as traders try to read through how well firms will be able to cope with the rising rates and fear of a hard landing. Recently, both major intraday and day-to-day reversals have been the rule. So, continue to be either being very nimble/quick, hedged, or have stops that are loose enough to ride out the whipsaw (and be ready to withstand that short-term pain). Trade carefully and position yourself for the long weekend news cycle.

Stick with those trading rules and manage the things that you can control while trying not to worry about the things you have no control over at all. Trade with the trend, don’t chase, keep consistently taking profits when you have them, and move your stops in your favor. Remember that the first rule of making big money in the market is to not lose big money in the market. Don’t be stubborn, and protect yourself from yourself. If you are wrong, just admit it and take your loss. Trading is a marathon, not a sprint. So, focus on the process and enjoy yourself.

Ed

Swing Trade Ideas for your consideration and watchlist: GPN, TWTR, VLO, IP, OXY, GPS, BP, HON, MMM, TGT, ZTS, EBAY, OTIS, AME, MAS, SHW, SLB. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service