Though traders hoped for another day of bullish relief on Friday, the bears roared into action, defending price resistance levels and reversing indexes to 2022 lows. As we begin a new trading week chalked full of earnings data, we also have to deal with an FOMC rate decision Wednesday afternoon. Though the market is overdue for a relief rally, the bulls will have their work cut out, so much overhead resistance and technical damage to repair in the index charts. Prepare for another week of challenging price action that could easily include wild intraday whipsaws and overnight reversals.

Asian markets traded mixed overnight as Chinese factory activity contracted in April. European markets trade mixed to mostly lower this morning after the weak China data with the U.K. market closed. With a big day of data and an FOMC decision Wednesday, the U.S. futures market point to a bullish open, hoping to spur a slight recovery after the punishing Friday selloff.

Economic Calendar

Earnings Calendar

We have a hectic week of earnings reports to keep traders guessing and high price volatility. Notable reports include AKR, AGNC, AMKR, AIRC, ANET, CAR, EXP, CBT, CHGG, CC, CLX, CVI, DVN, FANG, FN, GPN, GPRE, GPP, IPI, LEG, MGM, MCO, MOS, NE, NTR, NXPI, OHI, ON, OTTR, PK, SAIA, SIX, SEDG, TTI, RIG, & WMB.

News & Technicals’

Apple CFO Luca Maestri said supply constraints related to Covid-19 could hurt sales by between $4 billion and $8 billion. Nokia CEO Pekka Lundmark said that the Finnish telco would have grown faster in the last quarter had it not been for supply chain issues. The lockdowns in China add to short-term uncertainty, Lundmark said, about Nokia’s chip supply chain. During the Berkshire Hathaway shareholder event, Watten Buffett said inflation swindles almost everybody as he and Charlie Munger railed against bitcoin, a market mania that has turned it into a gambling parlor. Berkshire’s operating earnings were flat year over year at $7.04 billion. This comes amid a sharp drop in the company’s insurance underwriting business. The company’s net earnings came in at $5.46 billion, down more than 53% from $11.71 billion in the year-earlier period. The slowing U.S. economy impacted the flat operating results, which contracted in the first quarter for the first time since the onset of the Covid-19 pandemic. For many decades, the Nordic nation has shared an 808-mile land border with Russia and has carefully walked a foreign policy tightrope between Moscow and the West. During the Cold War, Finland adopted a neutrality policy, meaning it would avoid confrontation with Russia. But its long-standing neutrality, cherished by many Finns, could end due to Russia’s unprovoked invasion of Ukraine. Treasury yields start the week higher, with the 5-year rising to 2.95%, which remains slightly inverted over the 10-year pricing a 2.92%, and the 30-year rose to 2.99% in early trading.

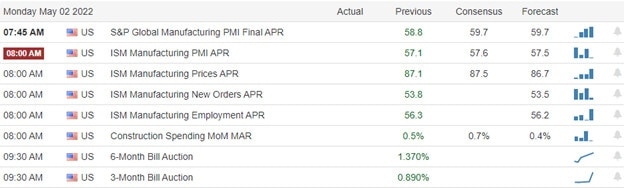

The bears roared into action on Friday, triggering a brutal day of selling and quickly dashing hopes that the relief rally that began on Thursday could follow through a second day. Futures markets are trying to rebound slightly this morning, but the bulls will have their work cut out with so much technical damage to repair. Moreover, with a massive week of earnings and an economic calendar with an FOMC rate decision on Wednesday, traders should plan for another hectic week of challenging price action. To kick things off, we have PMI and ISM Mfg. reports along with Construction spending and three and six-month bond auctions. The T2122 indicator is back in an extreme short-term oversold condition. Still, with an aggressive Fed decision just around the corner, the bulls may find it challenging to overcome the bears, especially near resistance levels on the index charts. Watch for intraday whipsaws and overnight reversals this week with all uncertainty ahead.

On Friday, stocks gapped down after disappointing earnings from AMZN and even more scary guidance from INTC, AMZN, and others. After 30 minutes of finding their footing, the bears took firm control and drove markets on an all-day selloff that closed very near the lows in all 3 major indices. This left us with big, ugly, black candles in all 3 and took the QQQ to its low of the year with SPY only 0.30% above the February 24 low. On the day, SPY lost 3.58%, DIS lost 2.73%, and QQQ lost 4.38%. The VXX gained 6.4% to 27.71 and T2122 dropped deep into the oversold territory at 3.27. 10-year bond yields spiked to 2.926% and Oil (WTI) fell almost 0.9% to $104.45/barrel.

On Saturday, BRKB (Berkshire Hathaway) held its annual meeting. Among the topics discussed was the fact that BRKB bought back $51 billion worth of stock during Q1. The company also purchased 14% of OXY ($7 billion) over a 2-week period in March and significantly added to its CVX position during Q1. They also have bought 9.5% of ATVI (in a simple arbitrage bet for when the MSFT acquisition closes). Charlie Munger blasted BRKB investor CalPERS for having called for organizational changes including the replacement of Warren Buffett as Chairman. On other topics, Munger said the stock market is a “mania of speculation” and said that HOOD was “justly unraveling” for disgusting practices. He also warned people to avoid cryptocurrencies. For his part, Buffett as usual said he is having a lot of trouble finding anything worth buying and that he’s in a mode of “preparing BRKB for an economic stall” (hence the buying a big stake in non-cyclical oil companies).

Over the weekend, Bloomberg reported that China’s economy has slowed rapidly as its “Covid Zero” lockdowns are hurting deeply. The lockdowns have closed factories and other businesses, kept consumers from spending, and closed transportation systems like trucking and ports. Factory activity fell to the lowest level in 2 years with Mfg. PMI falling to 47.4 for the month. Meanwhile, Services PMI fell to 41.9 in April (the lowest level since Feb. 2020). China’s National Bureau of Statistics said that 19 of 21 sectors had seen a contraction over the month. This in itself tells you how bad it is since China is notorious for painting a rosy picture in official reports.

On the Russian invasion story, US House Speaker Pelosi led a small delegation of US lawmakers to Kyiv on Sunday for talks that included Ukrainian weapons needs. This comes in front of Congressional wrangling over President Biden’s new $33 billion aid request for Ukraine that was sent to Congress last week. In Russia, Sunday it was disclosed that $5 million worth of farm equipment (which Russians stole from a Ukrainian DE dealership since the invasion) has been remotely disabled. Dutch Dock Workers also refused to unload a tanker of Russian oil. More importantly, the German Econ. Minister Baerbock also announced that Germany would be free of dependence on Russian oil by this summer. That pulls forward the timeline for that independence by at least 3-6 months from previous estimates. This comes as the Financial Times reports Germany has now called for the EU to add a phased-in ban of Russian oil as part of a new round of sanctions on Moscow. Bloomberg also reports that Russian state-owned Gazprom reported that its gas exports fell 22% month-on-month in April. Despite this drop in supply, LNG prices have not spiked due to mild weather and increased supply from other sources, such as the LNG, SHEL, and TOT. Finally, as of Monday, Swedish Foreign Minister Linde said it is now all but certain that Sweden and Finland will both apply for NATO membership after weekend talks.

Bloomberg reported early this morning that Elon Musk sold another $4 Billion of TSLA stock in order to diversify and raise cash for his TWTR bid. Most of that selling was done on Tuesday, the day TSLA stock fell 12%. Bloomberg also says his pitch to bankers for funding for the TWTR takeover included job cuts, other cost-cutting, as well as the implementation of new ways to monetize the platform (recoup investment). However, in a bid to prevent TSLA from sliding further, Musk also added a comment to the SEC filing, saying that he has no more plans to sell TSLA stock.

Overnight, the Asian markets were lower on mostly modest moves as all the Chinese exchanges closed for a Labor Day holiday. Australia (-1.18%), New Zealand (-0.84%), and South Korea (-0.28%) paced the region Monday. In Europe, stocks are nearly red across the board at mid-day, with the sole exception of London. The FTSE (+0.47%), DAX (-0.60%), and CAC (-1.43%) are typical and lead the region as Europe digests bad Chinese data and the proposition of Energy sector sanctions on Russia. As of 7:30 am, US Futures are pointing toward a modestly green start to the day. The DIA implies a +0.40% open, the SPY is implying a +0.36% open, and the QQQ implies a +0.49% open at this hour. 10-year bond yields are down slightly from Friday to 2.912% and Oil (WTI) is off almost 3% to $101.64/barrel in early trading.

The major economic news scheduled for release on Monday is limited to Apr. Mfg. PMI (9:45 am), Apr. ISM Mfg. PMI (10 am). Major earnings reports scheduled for the day include AMG, ARLP, BRKB, CAN, EDP, FMX, GPN, GPRE, ITRI, JELD, MCO, ON, SAIA, TKR, and WEC before the open. Then after the close, ARGO, ANET, CAR, BGCP, BXP, CBT, CC, CLX, CNO, CTRA, CVI, DVN, FANG, EXPE, FN, FLS, FMC, KMPR, KMT, LEG, LOGI, MGM, MOS, NTR, NXPI, OGS, SANM, SEDG, RIG, TA, WMB, and WWD report.

So far this morning, BRKB (Saturday), EPD, WEC, GPN, TKR, SXC, and PK have all reported beats on both revenue and earnings. Meanwhile, AMG missed on revenue while beating on earnings. On the other side, CAN, and MCO have reported beating the estimates on revenue but missed on the bottom line. Finally, JELD and ARLP reported misses on both lines.

Economics news coming later this week includes Mar. Factory Orders and Mar. JOLTs Job Openings on Tuesday. Then on Wednesday, we see ADP Apr. Nonfarm Payrolls, Imports/Exports, Mar. Trade Balance, Apr. Service PMI, Apr. ISM Non-Mfg. PMI, Crude Oil Inventories, FOMC Statement, FOMC Rate Decision, FOMC Press Conference. On Thursday, we get Weekly Initial Jobless Claims, Q1 Nonfarm Productivity, and Q1 Labor Costs. Finally, on Friday we see Apr. Avg. Hourly Earnings, Apr. Nonfarm Payrolls, Apr. Participation Rate, and Apr. Unemployment Rate.

This week we will see almost 1,500 earnings reports. The major reports coming later in the week include AMD, AIG, DD, EL, FIS, HLT, ITW, KKR, MPC, PFE, PRU, PSA, SPGI, SBUX, and TRI on Tuesday. Then Wednesday we get BKNG, CTSH, CTVA, CVS, EMR, FTNT, IDXX, JCI, MAR, MET, MRNA, PXD, O, REGN, and UBER. On Thursday, we see APD, APO, BDX, COP, D, EOG, ILMN, ICE, MCK, MNST, MSI, PH, RSG, SRE, SQ, VRTX, WELL, and ZTS. Finally, on Friday we get CI.

So, another heavy week of earnings has kicked off. This morning those earnings are leaning green but are more mixed than earlier reports this quarter. As has been the case recently, it is the forward guidance that most traders are waiting to hear since the bad Q1 GDP Print last week has everyone fearing recession. With that said, remember that the trend is still very clearly bearish, but that we have seen choppy moves (white candles, intraday reversals, and plenty of wicks in the bearish trend). Caution is still the smart play. Don’t get caught chasing a gap only to be caught in a whipsaw you are not prepared to weather.

Remember that the first rule of making big money in the market is to not lose big money in the market. Staying hedged, nimble, and measured are good things…not bad. So, don’t be stubborn, and protect yourself from yourself. Nobody is right all the time. If you’re wrong, just admit it and take your loss. Just focus on your process and enjoy yourself. Stick with your trading rules and manage the things that you can control while trying not to worry about the things you have no control over at all. Trade with the trend, don’t chase, keep consistently taking profits when you have them, and move your stops in your favor.

Ed

Swing Trade Ideas for your consideration and watchlist: HSY, UNG, MO, SQQQ, MMM, BAC, KO, LLY, KBH, GM, MSFT, AAPL, HD, BTU, SLB, HAL, AA, TSLA. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Although the bulls had a slow start, they finally overwhelmed the bears triggering a short squeeze relief rally. However, with a round of tech giant earnings after the bell that discontinued investors, the bulls will have their work cut out for them if they intend to follow through to the upside on Friday. As we slide into May with rate increases on the horizon, expect price action to remain challenging and an active group of bears heading into the summer.

Asian markets close green across the board overnight with the hope of more policy support from China as their economy continues to contract. European markets are green across the board this morning, boosted by earnings even as their inflation hits their 6th straight record inflation reading. Facing another round of earnings and economic data, U.S. futures point to a bearish open, with the Nasdaq leading the way.

Economic Calendar

Earnings Calendar

We have less drama on the Friday earnings calendar, with about 100 companies fessing up to results. Notable reports include ABBV, AON, AZN, B, BLMN, BMY, CBOE, CHTR, CVX, CL, COWN, XOM, HON, IMO, LHX, LYB, NWL, NMRK, PSX, SLCA, WPC, WY & WETF.

News & Technicals’

According to filings with the Securities and Exchange Commission, Elon Musk sold roughly $4 billion worth of Tesla shares in the days following his bid to take Twitter private. The bulk of the CEO’s sales were made on Tuesday, the filings showed. As a result, Tesla shares fell 12% that day but edged higher on Wednesday by less than one percentage point. As the filings became public Thursday evening, Musk wrote on Twitter, “No further TSLA sales planned after today.” Apple’s revenue grew nearly 9% year over year during the quarter ended in March. But shares fell nearly 4% in extended trading after Apple CFO Luca Maestri warned of challenges in the current quarter, including supply constraints that could hurt sales by up to $8 billion. In addition, the tech giant authorized $90 billion in share buybacks. Amazon on Thursday gave a revenue forecast that trailed analysts’ estimates. Growth rates are at their slowest since the dot-com bust in 2001. In addition, the company recorded a $7.6 billion loss on its investment in electric vehicle maker Rivian. Tensions between Russia and the West appear to have risen dramatically over the last week. In the last few days alone, Russia stopped gas supplies to two European countries and has warned the West several times that the risk of a nuclear war is very “real.” Russian President Vladimir Putin said that any foreign intervention in Ukraine would provoke what he called a “lightning-fast” response from Moscow. Treasury yields fell slightly in early Friday trading, with the 10-year dipping to 2.8386% and the 30-year slipping to 2.9145%.

The bulls had a slow start yesterday, but they ultimately overcame those feisty bears to trigger a short-covering relief rally. At the end of the day, the question on everyone’s mind is, can we get at least one more day of follow-through to the upside? Sadly after a round of disappointing big tech earnings, the bulls may find that very challenging on the last trading day of April. With the Fed planning rate increases beginning next month and the sharply contracting GDP to a negative 1.4, thoughts of a coming recession could make the bears very active this summer. Expect volatility to remain high in the weeks ahead as investors grapple with all the uncertainty.

On Thursday stocks gapped strongly higher at the open on positive earnings news. However, they immediately faded that gap, retesting the previous close, only to reverse again at 10:30 am to start a strong rally that lasted until 3:30 pm when they sold back off a bit the last 30 minutes. This left us with large white candles with large wicks at the bottom and smaller wicks at the top of the candle across all 3 major indices. (Too much wick to call any of the 3 a Morning Star pattern.) On the day, SPY gained 2.52%, DIA gained 1.88%, and QQQ gained 3.55%. However, that late-day selloff into the close gave back the T-line (8ema) in all three. The VXX lost 4.26% to 26.04 and T2122 climbed back out of the oversold territory to 31.79. 10-year bond yields were off to 2.83% and Oil (WTI) spiked 3.24% to $105.32/barrel.

Prior to the open Thursday, Q1 GDP came in much worse than expected. The number reported annualizes to a -1.4% GDP growth rate. This compares to 2021 final GDP number (+6.9%) and the analysts consensus forecast for Q1 of +1.1% (annualized). Of course, that bad number will be revised in the future. Economists also said that this print was exaggerated by temporary problems such as the Q1 supply chain bottlenecks at West Coast ports. However, despite the “don’t panic” spin, it was clearly a bad print. Nonetheless, markets ignored the bad news and gapped higher. In other economic news, the Weekly Initial Jobless Claims came in just as forecast at 180k for the week.

After the close, AAPL, INTC, GILD, WDC, SYK, MHK, AJG, OLN, KLAC, CE, AVTR, FBHS, COOP, DLR, SWN, CSL, AEM, HUBG, TEX, ATR, BIO, ENSG, TEAM, BZH, SKYW, WIRE, CENX, SM, ACA, MERC, and MATW all reported beating estimates on both revenue and earnings. Meanwhile, HIG, PFG, ATUS, CINF, LPLA, and WU missed on revenue while beating on earnings. On the other side, AMZN, EMN, SSNC, TKC, ROKU, DXCM, and ULCC beat on revenue while missing on earnings. However, RMD, DNZOY, LHX, HOOD, X, and CG missed on both lines.

In other after-hours earnings-related news, AAPL significantly beat on both lines and increased its buyback program to $90 billion for 2022. However, the company also warned of supply chain troubles (China Covid lockdowns) that could hurt Q2 numbers by between $4 billion and $8 billion. Elsewhere, AMZN lowered guidance which raises the fear that consumers are starting to be tapped out by inflated prices. They also took a $7.6 billion loss on their RIVN stake. In addition, INTC offered lower than expected guidance for Q2. Finally, HOOD reported it has fewer active users and shrinking revenue due to smaller order flow that they could sell. This is evidence that the meme stock craze and “day trading while working from home” have both decreased significantly over the last few months.

Bloomberg reported early this morning that Elon Musk sold another $4 Billion of TSLA stock in order to diversify and raise cash for his TWTR bid. Most of that selling was done on Tuesday, the day TSLA stock fell 12%. Bloomberg also say his pitch to bankers for funding for the TWTR takeover included job cuts, other cost-cutting, and implementing new ways to monetize the platform (recoup investment). However, in a bid to prevent TSLA from sliding further, Musk has added a comment to the SEC filing, saying that no more sales of TSLA stock are planned.

Overnight, the Asian markets were mostly very strongly green. Hong Kong (+4.01%), Shenzhen (+3.69%), and Shanghai (+2.41%) led the way higher. However, there were positive moves of over 1% in most exchanges. Only India (-0.83%) showed a significant loss. In Europe, stocks are mostly modestly green at mid-day. The FTSE (+0.07%) and CAC (+0.09%) lag, but the DAX (+0.68%) is typical of the region in early afternoon trading. As of 7:30 am, US Futures are pointing toward a gap down and red start to the day. The DIA implies a -0.44% open, the SPY is implying a -0.89% open, and the QQQ implies a -1.18% open at this hour. 10-year bond yields are trading up at 2.871% and Oil (WTI) is up over 1% to $106.61/barrel in early trading.

The major economic news scheduled for release on Friday includes Mar. PCE Price Index, Q1 Employment Cost, and Mar. Personal Spending (all at 8:30 am), Chicago PMI (9:45 am), and Mich. Consumer Sentiment (10 am). Major earnings reports scheduled for the day include ABBV, AB, AON, ARCB, AZN, BLMN, BMY, CRI, CBOE, CHTR, CVX, CL, XOM, HE, HON, IMO, LHX, LYB, MGA, NWL, NMRK, NVT, PSX, SYNH, TRP, and WY before the open. There are no major earnings reports scheduled for after the close.

So far this morning, AZN, BMY, HON, LYB, PSX, WY, CX, and CRI have all reported beats on both revenue and earnings. Meanwhile, CHTR, AON, SXT, and TAL all missed on revenue while beating on earnings. On the other side, XOM, CVX, CL, and CNX have reported beating the estimates on revenue but missed on the bottom line. Finally, CG, TIGO, and UOVEY reported misses on both lines.

The final flurry of earnings reports (in an earnings blizzard week) came last night and this morning. Again, the numbers were mostly positive, but not all were good and the devil is in the details. Also, the forward guidance (which has struck fear in many traders) has disappointed. With that said, remember that the trend is still very clearly bearish in the mid-term, despite a strong day Thursday. And whipsaw continues to be the norm recently. So, beware of a potential gap-and-reverse move after the open. Caution is still the smart play, especially with the weekend news cycle ahead. Don’t get caught chasing a gap only to be caught in a whipsaw you are not prepared to weather.

Remember that it’s Friday. So pay yourself. Also bear in mind that the first rule of making big money in the market is to not lose big money in the market. Staying hedged, nimble, and measured are good things…not bad. Also, don’t be stubborn, and protect yourself from yourself. Nobody is right all the time. So, if you’re wrong, just admit it and take your loss. Trading is not a sprint, it’s a marathon. Just focus on your process and enjoy yourself. Stick with your trading rules and manage the things that you can control while trying not to worry about the things you have no control over at all. Trade with the trend, don’t chase, keep consistently taking profits when you have them, and move your stops in your favor.

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

On Wednesday markets went on a wild all-day roller-coaster ride, only to end up not far from where it closed Tuesday. This left us with indecisive, long-legged Doji candles in all 3 of the major indices. On the day, SPY gained 0.26% (mostly on the pre-market gap), DIA gained 0.16%, and QQQ lost 0.12%. The VXX rose more than 3% to 27.30 and T2122 rose, but only to 4.15 which is still deep in the oversold territory. 10-year bond yields rose to 2.836% and Oil (WTI) rose fractionally to $102.07/barrel.

After the close, QCOM, MOH, AMGN, AFL, AVT, CHRW, PPC, DFS, URI, HOLX, HTZ, EHC, MTH, MEOH, PLXS, MAT, ICLR, NLY, FIX, MYRG, ALSN, AVB, ESBMRN, PTC, TDOC, WSC, MAA, HP, TYL, and FWRD all reported beating estimates on both revenue and earnings. Meanwhile, FB, CYH, RE, EQIX, AXS, AR, CCS, AWK, AMED, INVH, and AUY missed on revenue while beating on earnings. On the other side, F, PYPL, TROX, SLM, CAKE, CMPR, PINS, and NBR beat on revenue while missing on earnings. However, ORLY, ACGL, FTI, CACI, CP, LVS, EQT, ALGN, GGG, and UCTT all missed on both lines.

In economic read-throughs from earnings news, F saw a quarterly profit only dragged lower by its stake in RIVN. PYPL also lowered its annual guidance, citing a pullback in consumer spending. PPC also said that restaurant demand for chicken has returned to pre-pandemic levels. Chinese shipping giant (container ships) Yang Ming Marine Transport said that supply chain issues may show signs of easing. The company said the Los Angeles and Long Beach port delays have been reduced, with only a 40 ship backlog waiting to unload (10-14 days of wait time compared to weeks a few months ago). The company also commented that new (Biden Administration) port procedures, such as requiring empty containers to be immediately moved and adding off-port storage facilities, should improve the flow even more in the second half of 2022.

FB shares are soaring this morning after missing on revenue and beating on earnings. The proximate cause seems to be that the company reported that they have started growing its number of users again. Among other big pre-market gainers we see CTMX, ENDP, FNGU, LC, MXL, and NOW. Among big pre-market losers we find ALGN, AMGN, BTU, CPZ, FLWS, FNGD, JKS, ORLY, SOXS, SQQQ, SWK, TDOC, TECS, UVXY, and VLON.

Overnight, the Asian markets were nearly green across the board. Only Shenzhen (-0.23%) showed any red while Japan (+1.75%), Hong Kong (+1.65%), and Australia (+1.32%) led the way higher. In Europe we see the same picture taking shape at mid-day. Only Finland (-0.05%) shows any red. Meanwhile, the FTSE (+1.04%), DAD (+1.44%), and CAC (+1.66%) are leading the continent higher in early afternoon trading. AT 7:30 am, US Futures are pointing toward a strong gap higher at the start of the day. The DIA implies a +0.91% open, the SPY is implying a +1.61% open, and QQQ implies a +2.29% open on earnings-fueled strength. 10-year bond yields are back down a tad to 2.819% and Oil (WTI) is off fractionally to $101.55/barrel in early trading.

The major economic news scheduled for release on Thursday is limited to Q1 GDP and Weekly Initial Jobless Claims (both at 8:30 am). Major earnings reports scheduled for the day include FLWS, AOS, AIMC, AEP, AIT, ARES, ABG, BAX, BFH, BC, CARR, CAT, CHD, CNX, CMCSA, DPZ, DTE, LLY, EME, FAF, FCNCA, FCFS, FTV, FCN, GTX, GOL, GFF, HSY, HUN, IP, IPG, IRM, JKS, KBR, KDP, KEX, LH, LAZ, LECO, LIN, LKQ, MDC, HZO, MA, MCD, MD, MRK, NLSN, NOK, ORI, OPCH, OSTK, PATK, PBF, BTU, PCG, PBI, POR, PHM, RLGY, RS, SNY, SNDR, SIRI, SAH, SO, LUV, SWK, SRCL, TROW, TFX, TPX, TXT, TMO, TNL, TWTR, VIRT, VC, GWW, WBS, WST, WEX, WTW, and XEL before the open. Then after the close, AEM, LNT, ATUS, AMZN, AAPL, ATR, ACA, AJG, TEAM, AVTR, BZH, BIO, CSL, CE, CENX, CLW, COLM, DXCM, EMN, WIRE, ENSG, ERIE, FSLR, FBHS, ULCC, GILD, HIG, HUBG, INTC, KLAC, LPLA, MTX, MHK, COOP, NOV, OLN, OMF, PFG, RMD, ROKU, SKYW, SM, SWN, SSNC, SYK, TEX, TFII, X, WFG, WDC, and INT report.

So far this morning, CMCSA, MRK, CAT, SNY, TMO, LIN, LLY, NOK, MO, SO, IP, MCD, PBF, CARR, AEP, CTE, XEL, LKQ, SCMMY, BAX, KDP, RS, PHM, HSY, IPG, SIRI, LUV, FAF, HUN, BC, CHD, MDC, IRM, TPX, VIRT, AIT, AOS, VC, LAZ, TFX, HZO, KEX, FCNCA, AIMC, MD, WEX, and FCFS have all reported beats on both revenue and earnings. Meanwhile, NOC, SWK, LH,, ABG, KBR, NLSN, and WST all missed on revenue while beating on earnings. On the other side, FAF, TROW, JKS, GTX, ERJ, ARES, TNL, POR, CNX, and PTEN have reported beating the estimates on revenue but missed on the bottom line. Finally, SAH, SRCL, OSTK, FLWS, and STRA all reported misses on both lines.

Once again we saw a blizzard of earnings last night and this morning. For the most part, this was a good report card for stocks and markets reflect a renewed optimism before the open today. However, remember that the trend is still very clearly bearish, we were very over-extended to the downside as of yesterday’s close, and a ride on the whipsaw has been normal recently. So, beware of a potential pop-and-drop or at least the possiblity that a bull move could be nothing but a relief rally. Also keep in mind that there are still more earnings to come, including AAPL and AMZN after the close today. My point is that we need to be cautious. Don’t get caught chasing a gap only to be caught in a whipsaw you are not prepared to weather.

Remember that the first rule of making big money in the market is to not lose big money in the market. Staying hedged, nimble, and measured are good things…not bad. Also, don’t be stubborn, and protect yourself from yourself. Nobody is right all the time. So, if you’re wrong, just admit it and take your loss. Trading is not a sprint, it’s a marathon. Just focus on your process and enjoy yourself. Stick with your trading rules and manage the things that you can control while trying not to worry about the things you have no control over at all. Trade with the trend, don’t chase, keep consistently taking profits when you have them, and move your stops in your favor.

Ed

Swing Trade Ideas for your consideration and watchlist: LUV, V, GSK, BTU, MCD, FB, SWK, RHI, IP, DAL, MMM. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

On Tuesday, the bears went to work with the uncertainty of inflation and rate increases, producing an ugly pop and drop that ultimately tested 2022 market lows. However, this morning’s futures suggest an overnight reversal and relief rally ahead of more uncertain earnings and economic data. Traders should keep a close eye on overhead resistance levels as we rally the possibility of entrenched bears willing to hold the downtrend with the FOMC rate decision coming soon. Expect another day of very challenging price action that could include more pops and drops, intraday whipsaws as well as continued overnight reversals.

During the night, Asian markets traded mixed, with Shanghai surging upward while worries of a collapsing Japan sent the Nikkei lower. This morning, European markets are in rally mode despite Russia shutting off gas supplies to Poland and Bulgaria. With a big day of earning and economic data ahead, U.S. futures point to a substantial gap up open. So, buckle up for another wild day of price action!

Alphabet reports a weak earnings quarter and revenue mix due to a sharp decline in YouTube. As a result, GOOGL missed on the top and bottom lines for the first quarter. On the other hand, other Bets, which includes self-driving car unit Waymo, nearly doubled its revenue compared to the year prior. Microsoft beat expectations on the top and bottom lines. In addition, fourth-quarter revenue guidance for each of the company’s three business segments surpassed analysts’ expectations surveyed by StreetAccount. The company announced plans to buy Activision Blizzard for almost $69 billion in the quarter. On Wednesday, Russia’s gas supplies to Eastern Europe are looking highly uncertain after Poland and Bulgaria were told their supplies would stop. The move comes after both countries refused Moscow’s recent demand to pay for gas supplies in rubles. It also coincides with a sharp rise in tensions between Western allies and Russia as the war in Ukraine continues into the third month. Cheaper gas is one of Walmart’s perks to get customers to sign up for Walmart+. The membership program already included a gas discount, but Walmart has doubled the savings per gallon and expanded the number of gas stations to more than 14,000. The big-box retailer is flexing its low prices as a competitive advantage, with inflation driving up the price of food and fuel. Robinhood announced laying off 9% of full-time employees in a blog post made by CEO Vlad Tenev Tuesday afternoon. Robinhood reported 3,800 full-time employees as of Dec. 31. Amid rising costs and supply chain instability, General Motors reaffirmed its earnings expectations for 2022 despite reporting a lower net profit and margin than a year ago. GM reaffirmed its pretax adjusted earnings forecast of between $13 billion and $15 billion for the year while raising its net income expectations to $9.6 billion and $11.2 billion. GM also reaffirmed plans to produce 25% to 30% more vehicles than last year. Treasury yield traded nearly flat early Wednesday morning, with the 5-year at 2.80%, the 10-year trading at 2.77%, and the 30-year ticking higher to 2.86%.

Tuesday produced an ugly pop and drop as worries over rate changes and earnings disappointments inspired the bears. The DIA and SPY held the 2022 market lows, but unfortunately, the QQQ and IWM created new lows for the year. After the bell, mixed results in earnings added to the uncertainty, but this morning futures look ready to begin a relief rally. The T2122 indicator supports a relief rally showing a substantial short-term oversold condition. That said, we have a long way to go before the index charts can develop bullish patterns. Remember, we have significant overhead resistance and downtrends that can harbor entrenched bears ready to attack, so plan your risk carefully. Expect price volatility to remain challenging with another big day of earnings and economic data.

Stocks gapped down about six-tenths of a percent on Tuesday, following Asia and Europe on fears of Covid’s impact through China on the global economy. Markets then proceeded to sell off all day long. With that said, the morning and last hour selloffs were much stronger than the mid-day drift lower. This left us with big, ugly, black candles that were essentially Marubozu (shaved head) candles that closed on the lows. On the day, SPY lost 2.78%, DIA lost 2.35%, and QQQ lost a whopping 3.77%. The VXX gained 6.25% to 26.35 and T2122 dropped deep into the oversold territory at 2.88. 10-year bond yields fell sharply to 2.743% and Oil (WTI) spiked 3.7% to $102.14/barrel.

During the day, the US Senate confirmed Lael Brainard as Vice-Chair of the Fed, making her the country’s top banking regulator as well. This may be of note inasmuch as she has been the lone vote against easing bank regulation on several previous Fed votes. In other economic news during the day, March Durable Goods Orders, Conf. Board Consumer Confidence and March New Home Sales all came in slightly below the expected number.

In a follow-up to the Elon Musk, TWTR, and TSLA story, it appears traders believe that having his attention split again (between TSLA, SpaceX, Boring Company, and now TWTR) will hurt TSLA. TSLA stock fell 12.19% on the day (wiping out $129 billion in market cap in the process). This came on top of the half a percent pullback the stock put in after the announcement on Monday afternoon.

After the close, MSFT, V, TXN, TNET, TER, MDLZ, MTDR, BHE, JBT, EXAS, CB, EW, COF, AGR, CMG, RHI, RUSHA, SKX, HA, BYD, DHX, FFIV, and ENPH all reported beating estimates on both revenue and earnings. Meanwhile, GM, MKSI, and CHE missed on revenue while beating on earnings. On the other side, JNPR and HA beat on revenue while missing on earnings. However, GOOG, GOOGL, FANUY, and EQR missed on both lines. With that said, GOOG/GOOGL also announced a $70 billion share buyback program (up from $50 billion last year). Finally, despite missing on revenue and citing supply chain issues, GM maintained its revenue forecast for the year and raised its earnings outlook.

In non-earnings news after the close, HOOD announced it is laying off 9% of its full-time staff. The company claimed the layoffs were to get rid of redundancy caused when they grew too fast last year. Elsewhere, it was also announced that AMZN will not face any OSHA penalties stemming from the 2021 tornado-related collapse of its Illinois warehouse. In electric car news, LCID announced that they have received an order for 100,000 cards from the Saudi Arabian government. GM also announced that they have now received 140,000 reservations for their Chevrolet Silverado EV. The latter two announcements were clearly responses to F announcing massively increased electric F-150 as well as other EVs (600k by 2023 and 2 million by 2026).

On the Russian invasion story, Russia is ratcheting up tensions with the West in a game of chicken. Russian Foreign Minister Lavrov went so far as to say the threat of nuclear war was “very, very real.” Later in the day, Russia decided to cut its supply of gas going to Poland and Bulgaria. The suspension was ostensibly because the two countries refuse to change their contracts to pay in Rubles instead of the dollars that are specified in the contracts. However, another potential reason is that Poland has recently given heavy weapons (tanks, artillery, and perhaps Mig jets) to Ukraine. For their part, former close Russian ally Bulgaria has led efforts in the EU to sanction Russia and has raised funds to help Ukraine strengthen its defenses. Elsewhere, for the first time, German Economic Minister Habeck said that a full embargo on Russian oil would be manageable. Finally, the Justice Dept. also announced after the close that it will be seeking additional authority from Congress to seize and sell Russian assets. Attorney-General Garland said he hopes for the authority to give the proceeds of those sales directly to Ukraine.

Overnight, the Asian markets were mostly red, with the exception of mainland China. Taiwan (-2.05%), Japan (-1.17%), and South Korea (-1.10%) passed the widespread losses. However, Shenzhen (+4.37%) and Shanghai (+2.49%) were clear outliers and the only appreciable green in the region. (The China rally came as official data showed that Chinese industrial profits rose 8.5% in Q1. This result shocked analysts who were expecting Covid-related slowed profits.) In Europe, stocks are green across the region at mid-day, with the lone exception of Greece. The FTSE (+0.83%), DAX (+0.25%), and CAC (+0.44%) lead the way on market-cap and volume. However, some of the smaller exchanges are moving more (especially Russia at +3.01%) in early afternoon trading. As of 7:30 am, US Futures are pointing toward a gap higher at the start of the day. The DIA implies a +0.90% open, the SPY is implying a +0.67% open, and the QQQ implies a +0.54% open at this hour. 10-year bond yields are up a bit to 2.767% and Oil (WTI) is up fractionally to $101.99/barrel in early trading.

The major economic news scheduled for release on Wednesday includes Mar. Trade Balance and Mar. Retail Inventories (both at 8:30 am), Mar. Pending Home Sales (10 am), and Crude Oil Inventories (10:30 am). However, there is a blizzard of major earnings reports scheduled for the day including AMT, APH, ADP, BA, BSX, BG, CVE, GIB, CHKP, CHEF, CME, CSTM, DAN, ETR, EEFT, EVR, FISV, GRMN, GD, GPI, HOG, HELE, HES, HUM, IQV, KHC, MHO, MKL, MAS, NSC, ODFL, OSK, OC, PAG, PRG, ROL, R, SABR, STX, SLGN, SPOT, SHOO, STM, TMUS, TMHC, TEL, TECK, TDY, TRN, UMC, VRT, WNC, and WAB before the open. Then after the close, AFL, ALGN, ALSN, AMED, AWK, AMGN, AR, ASGN, AVB, AVT, AXS, BMRN, CHRW, CACI, CP, CG, CLS, CCS, CAKE, FIX, CYH, DFS, ESI, EHC, EQT, EQIX, RE, F, GGG, HP, HTZ, HOLX, ICLR, INVH, JBSS, LVS, MAT, MTH, FB, MEOH, MAA, MOH, MYRG, NBR, NEX, ORLY, PYPL, PPC, PINS, PLXS, PTC, QCOM, RJF, RRX, NOW, SAVE, FTI, TDOC, TROX, UCTT, URI, WFRD, WSC, and AUY report.

So far this morning, CNC, UPS, VLO, ADM, GE, PEP, MMM, UBS, DHI, SHW, WM, GLW, ATLKY, AVY, GPK, ROPST, So far this morning, AMT, HUM, BG, GSK, GD, KHC, ADP, TEL, STM, GPI, BSX, ASAZY, SPOT, GIB, DAN, OC, CSTM, TMHC, DASTY, CME, EVR, HELE, WNC, and SHOO have all posted beats on both revenue and earnings. Meanwhile, TMUS, DB, TECK, UMC, and TDY all missed on revenue while beating on earnings. On the other side, VRT, CVE, MKL, ETR, and CHKP have reported beating the estimates on revenue but missed on the bottom line. Finally, BA, CS, EEFT, HOG, LYG, RNECY, TLSNY, TRN, and WAB all reported misses on both lines.

Another huge wave of largely good earnings leads the news today. Elsewhere, Europe is so far shrugging off the risks posed by Russia cutting natural gas supplies to two European nations as well as the Germans saying a Russian oil embargo would be “manageable.” With that said, despite backing off overnight highs, it looks like we are back in the “day-to-day chop” mode…at least at the start of the day. Also remember, that despite yesterday being an exception to the rule, we have been experiencing intraday reversals a lot lately. So, do not get caught in any whipsaw you are not prepared to weather. Respect the market condition and continue to be cautious. Don’t be in a hurry to chase gaps and early moves. It is better to give up a little of the move than to have to suffer through reversal pains after you jump early.

Focus on the process and enjoy yourself. Stick with your trading rules and manage the things that you can control while trying not to worry about the things you have no control over at all. Trade with the trend, don’t chase, keep consistently taking profits when you have them, and move your stops in your favor. Remember that the first rule of making big money in the market is to not lose big money in the market. So, don’t be stubborn, and protect yourself from yourself. If you are wrong, just admit it and take your loss. Trading is a marathon, not a sprint.

Ed

Swing Trade Ideas for your consideration and watchlist: No Trade Ideas today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

After a turbulent morning session dominated by bears, the bull won the day, triggering a relief rally to squeeze out short traders as they took profits. However, anything is possible with a jam-packed day of market-moving earnings and economic reports. So, keep a close eye on overhead resistance and support levels as the market react to all the data and prepare for possible gappy market opens the rest of the week as the tech giants report. Price action will likely be challenging as the drama unfolds with so much at stake. Plan your risk carefully!

Asian markets trading mixed during the night as many of the big banks downgraded the growth potential of China as the lockdown continues. However, European markets see green across the board this morning despite a Russian nuclear threat. U.S. futures point to a bearish open with the uncertainty of earnings and economic data ahead.

Economic Calendar

Earnings Calendar

Big Tech will highlight the earnings reports on Tuesday, with nearly 200 companies listed on the Tuesday calendar. Notable reports include GOOGL, MSFT, MMM, ADM, ARCC, AVY, BYD, CNI, CAI, COF, CNC, CMG, CB, GLW, DHI, ENPH, EQR, EXAS, FFIV, FANUY, GE, GM, HUBB, JBLU, JNPR, MDLZ, MSCI, NAVI, NTRS, NVS, PEP, RRC, RTX, SHW, SSTK, SKX, TER, TXN, TRU, TZOO, UBS, UPS, VLO, V, WM, & WH.

News & Technicals’

According to the top Russian official, “ the threat of nuclear war is real after the U.S. expressed the desire to see Moscow weakened. On Monday, the Twitter board agreed to a $44 billion buyout from Tesla CEO Elon Musk. However, few additional details are known, leaving users and employees uncertain about the future. In addition, the Tesla CEO has shared little about how he plans to improve Twitter, though he’s offered many criticisms. As a result, it’s unclear who will lead the company under Musk’s ownership or what is ahead for the company’s workforce. Twitter Chief Executive Parag Agrawal told employees on Monday that the future of the social media firm is uncertain after the deal to be taken private under billionaire Elon Musk closes. He was speaking at a town hall meeting that Reuters heard. “Once the deal closes, we don’t know which direction the platform will go,” Agrawal said. Donald Trump said he wouldn’t return to Twitter on Monday even if Elon Musk reversed the former president’s ban. “I was disappointed by the way Twitter treated me. I won’t be going back on Twitter,” the former president told CNBC’s, Joe Kernen. Twitter permanently suspended Trump from the platform in January 2021 following the attack by his supporters on the U.S. Capitol. Several economists at major investment banks have cut their China growth expectations in just about a week. The new median forecast among nine financial firms tracked by CNBC expects 4.5% China GDP growth for the full year. Nomura had the lowest forecast, while UBS cut its estimates the most. Treasury yields continued to dip slightly in early Tuesday trading, with the 5-year trading at 2.82%, inverted over the 10-year at 2.78%, and the 30-year pricing at 2.86%.

On Monday, the bears dominated the early trading session to test 2022 lows, but bulls won the day, triggering a nice relief rally as short traders took profits. We have a jam-packed economic calendar today coupled with the massive anticipation of the big tech earnings from MSFT and GOOGL after the bell. The tech giants will continue to report throughout the week, keeping traders guessing and the price action volatile. Significant point gap up or gap down opens could occur as a result, so plan your risk carefully as the drama unfolds. As we rally, respect overhead resistance levels and avoid the fear of missing and the desire to chase stocks that could gap substantially, vastly increasing the risk. Disappointing reports could also create huge point intraday whipsaws, so plan your risk carefully and be careful not to overtrade.

Markets gapped lower at the open Monday and then the bears gave us about half an hour’s worth of follow-through before bobbing along the bottom until noon. However, then the “intraday reversal” norm kicked in as the bulls stepped in and led a rally that lasted the rest of the day. This left us with white, large-bodied hammer-type candles in the SPY and DIA while the QQQ came up just short of printing a Bullish Piercing Candle. With that said, the SPY and QQQ are still a bit extended below their T-line with the DIA closer, but certainly not testing the 8ema yet. On the day, SPY gained 0.58%, DIA gained 0.68%, and QQQ gained 1.29%. The VXX fell more than 5% to 24.80 and T2122 rose but remains inside the oversold territory at 14.29. 10-year bond yields fell sharply to 2.822% and Oil (WTI) fell more than 2.9% to $99.07/barrel (which was well up off the lows of the day).

Following through on Sunday’s news, the board of TWTR reversed course and accepted Elon Musk’s offer of $54.20/share to take the company private. The stock closed up 5.64% to $51.69 after gapping up 4.25% at the open. The deal is still subject to the approval of a shareholder vote. Assuming the deal closes, this puts the TWTR platform in the hands of one of the company’s former most vocal critics (who happens to have used the platform to break the law, for which he was fined tens of millions of dollars by the SEC). While he is mainly just a PR man for all his companies, the key question for longer-term investors is how hands-on he will be and what this might mean for TSLA. Cryptocurrency (and Musk favorite) Dogecoin also jumped 20% on the news, pricing in the hope that he will continue to heavily promote Dogecoin through TWTR.

Also in the afternoon, F announced it expects to increase electric F-150 production by 3.5 times for 2022 over previously announced production numbers (150k units vs. 40k units announced last year). This would dwarf the production plans from RIVN and GM, which are expected to produce in the area of 10k units during the same period. The company said it was confident it would hit this production plan and is aiming to have produced over 2 million electric vehicles by 2026. TSLA, the leader in electric vehicles, has announced, but has not actually shipped any of its own “cyber trucks.”

Today another AMZN facility in NY will be voting on unionizing. Elsewhere, the Shanghai area reported a record After the close, CCK, WRB, PKG, OI, AXTA, CDNS, SBAC, and ARE all posted beats on both the top and bottom lines. Meanwhile, WHR, AMP, and ZION missed on revenues while beating on earnings. On the other side, UHS and CR beat on revenue while missing on the earnings line.

In economic news, after the close, the USDA updated its Food Price Outlook for 2022. The new forecast calls for 5%-6% overall food inflation in the US over the remainder of the year. Included in this number is a forecast 5.5%-6.5% increase in “away from home” food prices. Elsewhere, also after the close, a survey was released that showed 40% of US small businesses plan to raise prices by at least 10%. The survey was conducted by the National Federation of Independent Businesses (NFIB) between April 14 and 17 covering 540 of their small business members. The survey also found that nearly another half of the surveyed companies plan to increase prices between 4% and 9%.

Overnight, the Asian markets were mixed but leaned to the downside as China is again expanding testing and lockdowns for Covid. Australia (-2.08%), Shenzhen (-1.66%), and Shanghai (-1.44%) paced the losses while India (+1.46%) led gainers by more than a percent over South Korea (+0.42%) and Japan (+0.41%). In Europe, stocks are mostly green at mid-day. The FTSE (+0.82%), DAX (+0.89%), and CAC (+1.11%) lead the region higher while only Portugal and Greece show any red in early afternoon trading. As of 7:30 am, US Futures are pointing toward another down start to the day. The DIA implies a -0.44% open, the SPY is implying a -0.43% open, and the QQQ implies a -0.48% open at this hour. 10-year bond yields are dropping again to 2.799% and Oil (WTI) is up fractionally to $98.87/barrel in early trading.

The major economic news scheduled for release on Tuesday includes Mar. Durable Goods Orders (8:30 am), Conf. Board Consumer Confidence and Mar. New Home Sales (both at 10 am). Major earnings reports scheduled for the day include MMM, AAN, ALLE, ARCH, ADM, ARCC, AVY, CNC, GLW, CEQP, DHI, ECL, ENTG, GE, HUBB, NSP, IVZ, JBLU, MSCI, EDU, NTRS, NVS, NVR, PCAR, PEP, PII, BPOP, RTX, ROP, ST, SHW, SCL, TRU, UBS, UPS, VLO, and WM before the open. Then after the close, ACCO, GOOGL, ASH, AGR, BHE, BYD, CNI, COF, CHX, CHE, CMG, CB, CSGP, EW, EQR, EXAS, FFIV, GM, GOOG, HA, IEX, JPNR, MTDR, MSFT, MKSI, MDLZ, NCR, RRC, RHI, RUSHA, SKX, TER, TX, and V report.

So far this morning, CNC, UPS, VLO, ADM, GE, PEP, MMM, UBS, DHI, SHW, WM, GLW, ATLKY, AVY, GPK, ROPST, JBLU, ALLE, SCL, ENTG, and ARCH have all posted beats on both revenue and earnings. Meanwhile, RTX, NVS, CJPRY, and MSCI all missed on revenue while beating on earnings. On the other side, IVZ and ARCC have reported beating the estimates on revenue but missed on the bottom line. Finally, NMR, PII, FANUY, and AWI all reported missed on both lines.

A huge surge of mostly good earnings leads the day’s news. That is saying something, considering that Russian Foreign Sec. Lavrov threatened the West to stop supporting Ukraine by telling an interview that the threat of the war in Ukraine escalating into a nuclear war was “very, very real.” Another wave of those earnings will hit after the close, with MSFT and GOOGL headlining that list. Despite the positive earnings news and even PEP raising its forward guidance, the premarkets look to be taking back much of Monday’s gains. The fear of spreading covid impacts from China (but hitting the global economy) is also weighing on the minds of longer-term investors, which is a headwind for bullish traders. However, remember that both intraday reversals have been the norm for a while now. So, respect that fact and continue to be cautious. Don’t be in a hurry to chase gaps and early moves. It is better to give up a little of the move than to have to suffer through reversal pains after you jump early.

Focus on the process and enjoy yourself. Stick with your trading rules and manage the things that you can control while trying not to worry about the things you have no control over at all. Trade with the trend, don’t chase, keep consistently taking profits when you have them, and move your stops in your favor. Remember that the first rule of making big money in the market is to not lose big money in the market. So, don’t be stubborn, and protect yourself from yourself. If you are wrong, just admit it and take your loss. Trading is a marathon, not a sprint.

Ed

Swing Trade Ideas for your consideration and watchlist: VLO, SYY, TGT, JNJ, IBM, GPRO, PSTG, KSS, PEP. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

On Friday, the bears showed up with lots of reinforcements, and the carnage created significant technical damage to all four index charts. Asia and Europe have joined the selling as economies slow amid the punishing inflation and the soon to be aggressive FOMC rate increases. As the indexes test the low’s 2022, we have a big week of earnings and economic data that could save or sink the market into a complete bear condition. With so much at stake, expect very challenging price action in the days ahead that could easily cause substantial point whipsaws and overnight market reversals.

As we slept, Asian markets suffered significant selling, with Shanghai falling 5.13% as pandemic impacts extended. European markets trade decidedly bearish this morning as global sentiment declines. With U.S. futures suggesting a gap down open to test the market lows of 2022, there is a palpable uncertainty as we face a substantial week of earnings and economic data.

Economic Calendar

Earnings Calendar

We have a hectic week of earnings ahead, with more than 100 companies listed on the Monday calendar. Notable reports include ATVI, ARE, AXTA, BOH, CDNS, KO, CR, LII, OI, OTIS, PKG, PHC, SBAC, WRB, WHR, & ZION.

News & Technicals’

Twitter’s board met Sunday to discuss Elon Musk’s takeover bid after the billionaire disclosed he had secured $46.5 billion in the financing, a source close to the situation told CNBC. The person said the board is looking for other offers, and the company could provide an update by the time it reports its latest financial results Thursday, if not before. Centrist Macron obtained 58.54% of the votes on Sunday, whereas his nationalist and far-right rival Le Pen got 41.46%. Back in 2017, when the two politicians also disputed the second round of the French presidential vote, Macron won with 66.1% of the support, versus Le Pen’s 33.9%. Addressing her supporters in Paris Sunday night, Le Pen conceded defeat but said: “We have nevertheless been victorious.” China’s capital city of Beijing reported a spike in Covid cases over the weekend and warned more would be found since the virus had spread undetected in the city for a week. The city’s business district of Chaoyang began three days of mass testing on Monday for anyone living or working in the region. The increase in cases in Beijing comes as mainland China faces its worst Covid outbreak since early 2020, and most of Shanghai, China’s largest city, remains under prolonged lockdown. European stocks opened sharply lower on Monday as investors digested the projected result of the French presidential election and monitored the latest developments in Ukraine. France’s Emmanuel Macron has comfortably beaten his rival Marine Le Pen in Sunday’s election, securing a second term as president on his pro-business and pro-EU agenda. Treasury yields pulled back in early Monday trading, with the 5-year declining to 2.85%, the 10-year slipping to 2.82%, and the 30-year falling to 2.88%.

Friday’s selling created significant technical damage, with all four indexes closing below their 50-day averages. With the Asian and European markets joining in on the selling, U.S. markets look to open lower to begin a hectic week of earnings. With rising inflation and an aggressive Fed, will earnings be able to hold us at 2022 market lows, or will the results push into a complete bear market condition? On the hopeful side, the T2122 indicator suggests a short-term oversold condition that could bring about a relief rally anytime. However, if this week’s earnings disappoint, the path ahead might be filled with hungry bears. If that’s not enough drama, we have a big week of market-moving economic data to keep us guessing. Expect a challenging week of wild price action that could easily include huge point whipsaws and overnight market reversals as the drama unfolds.