On Friday, markets breathed a sigh of relief, finding some willing bullish buyers encouraging those holding short positions to take some profits heading into the weekend. Sadly the bullish move left more questions than answers, unable to breach overhead price resistance levels. Additionally, with the national average gas prices hitting a new record high, possible recession talk increased over the weekend. We will kick off the week with a reading on Empire State MFG. Data with a retail earnings focus throughout the week. Keep a close eye on overhead resistance levels for entrenched bears and expect price volatility to remain challenging in the week ahead.

Asian markets traded mixed overnight as China’s economic numbers disappointed as lockdowns continue to weigh on the economy. European markets trade with modest declines this morning as inflation impacts weigh on investor confidence. U.S. futures also point to modest declines at the open, struggling to find momentum amidst the uncertainties of the path forward.

Economic Calendar

Earnings Calendar

As we kick off a new trading week, the earnings calendar has a theme of retail reports. Notable reports Monday include ACRX, BZFD, CCSI, DAC, FTK, GAN, IPW, KALA, NU, PASG, PTE, RYAAY, SSYS, TTWO, TME, TSEM, WRBY, WEBR & WIX.

News & Technicals’

Ukraine has been unable to export grains, fertilizers, and vegetable oil, while the conflict also destroys crop fields and prevents a typical planting season. In addition, some nations have imposed restrictions on exports. This is the case in India, for example, which announced Saturday a ban on wheat sales “to manage the country’s overall food security.” On Sunday, Amazon’s Jeff Bezos tweeted that inflation is most hurtful to the least affluent in the United States. The comments from Bezos were in response to a thread in which President Joe Biden claimed the U.S. was on track to see its largest yearly deficit decline. Bezos on Friday called out President Biden over a tweet that said taxing wealthy corporations could help lower inflation. Former Goldman Sachs CEO Lloyd Blankfein said he believes the economy is at risk of recession. Speaking on “Face the Nation” on CBS, Blankfein said a recession is “a very high-risk factor.” There’s a path. It’s a narrow path,” said Blankfein, who retired from Goldman Sachs several years ago and now holds the title of senior chairman. The pandemic exacerbated a pilot shortage by slowing down training, hiring and creating a wave of early retirements. Airlines offered pilots early retirements to cut labor bills during the depths of the pandemic. The process to become airline-qualified in the U.S. is lengthy and expensive, making entry barriers high. After disagreeing on pricing, the Irish low-cost airline terminated talks over a substantial order of Boeing 737 Max 10 jets worth tens of billions of dollars in September 2021. O’Leary told CNBC following Ryanair’s full-year results that the company had been “very disappointed with the performance” of Boeing from a commercial perspective over the last 12 months. Treasury yields eased slightly in early Monday trading, with the 10-year slipping to 2.91% and the 30-year dipping to 3.08%.

We finished the week with a sigh of relief as the market found a few willing buyers giving short some traders a good reason to take profits heading into the weekend. But unfortunately, the technical picture of the index charts remains strongly bearish, with substantial resistance levels blocking the path to recovery. Moreover, during the weekend, the talk of a likely recession increased as the insidious inflation tax continues to impact consumer spending. The national average gas price set another new record this weekend at $4.48 per gallon, with diesel rising to $5.57, adding pressure to everything we buy, sell or do. It will be interesting to see how this might impact the earnings performance of the retailers scheduled to report this week. As for me, I will plan for the wild volatility to continue watching for bear attacks at or near price resistance levels.

On Friday, stocks gapped up 1% – 1.5% in the major indices and then followed through to the highs of the day just after noon. Then the afternoon saw a roller-coaster ride that ended on an upswing, but not at the highs. This left us with gap-up, white candles that failed a test of the down-trending T-line (8ema) in all three major indices and the small-cap IWM. On the day, SPY gained 2.34%, DIA gained 1.45%, and QQQ gained 3.71%. The VXX fell more than 3.5% to 25.97 and T2122 climbed out of the oversold territory to 25.97. 10-year bond yields closed up to 2.937% and Oil jumped 4% to $110.38/barrel. On the week, all the major indices printed gap-down, indecisive, long-legged Spinning Top candles.

Part of the reason for Friday’s rally was the Fed removing some uncertainty from the market. FOMC Chair Powell said on Thursday that larger rate hikes are off the table for now, but the Fed will be hiking rates half of a percent at each of the next two Fed meetings (June 15 and July 27). Elsewhere, it was revealed that top tax officials from the US, UK, Canada, Australia, and the Netherlands met in London Friday to discuss 50 potential crypto-based tax crimes. These crimes include a $1 billion Ponzi scheme carried out cross-border using an unspecified cryptocurrency as well as NFTs.

Meme stock trading came back into vogue last week. Some examples include GMA closing up almost 10% on a 10% gap up Monday and trading in a 12.5% range over the week. AMC closed down 14.17% while trading in a 45% range during the week. BBBY closed down more than 20% and traded in a 35% range during the week. BB closed up about 4% after trading in a 25% range during the week. Finally, HOOD closed up 5.63% after trading in a 41% range over the week.

On the Russian invasion story, Russia took action against Finland, stopping the supply of electricity (20% of the country’s power supply) and also stopping the flow of natural gas (used to generate another 6% of the country’s power) after the Finn government announced it will ask parliament to approve an application for NATO membership. On Sunday, Sweden followed suit, with PM Andersson saying the country will now work toward NATO membership. (This raises the question of how Russia will react. Will they cut off gas flows to Europe as they did to Finland?) Early Monday, MCD said it will sell its closed Russian stores rather than ever try to reopen. From Russia’s standpoint, this raises the specter of whether the 1,000 companies which closed operations in its country will ever reopen. Elsewhere, India has banned wheat exports in anticipation of a global shortage due to Ukraine being unable to ship grain and droughts worldwide. This is not a huge fear for the US (other than price hikes being ensured). However, Asia, Africa, and to a lesser extent parts of Europe need to worry about food shortages coming.

Energy markets and stocks/ETFs may face more turmoil this week. In Europe, nat. gas prices were up 10% last week after the shutdown of one-third of the Russian Natural gas flow. This week the EU is expected to unveil its $195 billion Euro plan to completely stop importing Russian oil and gas by 2027. The plan is expected to include deals with Egypt, Israel, and Nigeria for natural gas to replace the current Russian supply as a stop-gap. Elsewhere this week, many of the major US retailers will be reporting this week. So, there may be guidance or at least a read-through on the outlook for consumers as markets gauge a potential economic slowdown.

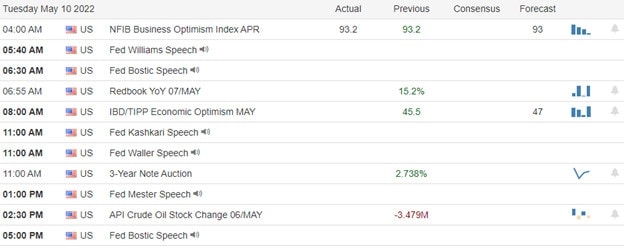

Economic news later this week includes April Retail Sales, April Industrial Production, Mar. Business Inventories, Mar. Retail Inventories, and a couple Fed speakers on Tuesday. On Wednesday we get April Building Permits, April Housing Starts, and Crude Oil Inventories. Then Thursday we see Weekly Jobless Claims, Philly Fed Mfg. Index, and April Existing Home Sales. There is no major news scheduled for Friday.

Overnight, Asian markets were mixed in very modes moves (by recent standards). Singapore (+0.82%), Japan (+0.45%), and Taiwan (+0.43%) led the gains. Meanwhile, Shenzhen (-0.59%), Shanghai (-0.34%), and South Korea (-0.29%) paced the losses. In Europe, we see a similar story taking shape at mid-day. Notable exceptions are Russia (+2.25%) and Denmark (+1.65%). However, the FTSE (+0.05%), DAX (-0.53%), and CAC (-0.29%) lead the way as usual. As of 7:30 am, US Futures are pointing toward a slightly negative start to the day. The DIA implies a -0.14% open, the SPY is implying a -0.34% open, and the QQQ implies a -0.48% open at this hour. 10-year bond yields are down a bit to 2.913% and Oil (WTI) is also down almost 1% to $109.42/barrel.

The major economic news scheduled for release on Monday is limited to NY Empire State Mfg. Index (8:30 am) and a Fed speaker (Williams at 8:55 am). Major earnings reports scheduled for the day are limited to TSEM and WEBR before the open. Then, after the close, TTWO and TME report.

So far this morning TSEM reported beats on both lines. Meanwhile, WIX has reported beating the estimates on revenue but missed on the bottom line. Finally, MARUY has reported misses on both lines.

Notable earnings reports later in the week include WMT, HD, SE, AER, and KEYS on Tuesday. Then on Wednesday, we get reports from LOW, TGT, CL, ADI, ARCO, CSCO, SNPS, CPRT, BBWI, and SQM. On Thursday we hear from VIPS, KSS, BJ, CAE, WMS, AMAT, ROST, VFC, FLO, PANW, and DECK. Finally, on Friday we see numbers from DE, FL, and BAH.

Coming off a very volatile week and working on 7 straight weeks of losses in the DIA (6 straight in both the SPY and QQQ), markets sit at the edge of bear market territory. Premarkets seem to suggest a wait-and-see feeling this morning, perhaps waiting on the retailer reports coming this week to give a read-through to whether the consumer is tapped out or not. Inflation, geopolitical risk, and cryptocurrency meltdowns also weigh on Mr. Market’s mind. So, caution remains the smart play. Remember the trend is still to the downside, despite Friday’s nice candles. Also bear in mind that those bullish candles failed a test of the T-line. This does not mean they will always fail, it just suggests there remains a lot of resistance overhead. Remain nimble and hedged. Above all, don’t give in to FOMO -OR- feel the need to predict a reversal.

Trading is a job, not a lottery ticket. So, work the process. Stick with your trading rules and manage the things that you can control while trying not to worry about the things you have no control over at all. Trade with the trend, don’t chase, keep consistently taking profits when you have them, and move your stops in your favor. Also, remember that the first rule of making big money in the market is to not lose big money in the market. So, don’t be stubborn, and protect yourself from yourself. Keep in mind that nobody is right all the time. When you’re wrong, just admit it and take your loss. As they say, the best time to have taken a $500 loss is when you are now staring at a $1,500 loss.

Ed

Swing Trade Ideas for your consideration and watchlist: EPAM, KO, CVX, GILD, CLX, WDC, OXY, VTRS. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Unfortunately, PPI disappointed investors as the inflation improvements hyped by analysts and the financial media failed to show a meaningful change. However, there was a silver lining in the last thirty minutes of the day as the bulls finally pushed back, giving hope that an overdue relief in the selling might begin. With a light day on the earnings calendar, we still have to deal with the Import/Export and Consumer Sentiment reports to find out if the bulls can stay inspired to rally, so stay focused on potential whipsaws as we move toward the uncertainty of the weekend.

Overnight Asian markets rallied, with Hong Kong and the Nikkei surging upward by more than 2.50%. European markets are also in the spirit of a relief rally, seeing green across the board this morning. With a lighter day of earning and economic data U.S. point to a bullish open after six straight days of selling. Expect price action to remain challenging, watching for large point whipsaws as we slide toward the uncertainty of the weekend amid all the geopolitical tensions.

Economic Calendar

Earnings Calendar

We have a much lighter day on the Friday earnings calendar with about 75 listed but a large number of them unconfirmed. Notable reports include DTEGY, HMC, LFMD, RGF, and SDPI.

News & Technicals’

Bitcoin jumped back above $30,000 on Friday as it rebounded from levels not seen since late 2020. Luna, the cryptocurrency associated with TerraUSD, or UST, is now worth $0 as the stablecoin has dramatically lost its $1 peg. On top of the UST saga, crypto markets have been hit by a number of other headwinds. Elon Musk says the Twitter deal is on hold as he waits to find out the number of fake accounts. Twitter’s stock plummeted 18% following the announcement. Musk announced last month that he intends to buy Twitter for $44 billion. He’s tweeted that one of his main priorities would be to remove “spambots” from the platform. Fed Chairman Jerome Powell cautioned Thursday that getting inflation under control won’t be easy. “Nonetheless, we think there are pathways … for us to get there,” he said in an interview with Marketplace published Thursday. Senior administration officials said that the Food and Drug Administration would announce specific actions to increase baby formula imports in the coming days amid a nationwide shortage. During the first week of May, 43% of baby formula supplies were out of stock at stores across the U.S., according to Datasembly, a company that tracks retail data. The shortage comes after Abbott Nutrition, the nation’s largest baby formula manufacturer, closed its plant in Sturgis, Michigan, amid a recall due to contamination concerns. Four infants who consumed products from the plant were hospitalized with bacterial infections. Two of the infants died.

NATO membership would be a historic decision for Finland, which shares a 1,300-kilometer border with Russia. Atlantic Council’s Northern Europe director Anna Weislander says both Finland and Sweden are well prepared to meet the oft-repeated political and military threats against the move by Russian President Vladimir Putin. The armed forces of both countries enjoy high compatibility with NATO member states, she said. Japanese conglomerate SoftBank Group may, for the first time, spend more on share buybacks than investments through its landmark Vision Fund, according to CLSA’s Oliver Matthew. SoftBank on Thursday posted a record $27 billion loss in its Vision Fund as tech stocks have plummeted in recent months. Shares of SoftBank soared more than 12% on Friday but still finished the week more than 2% lower as investors globally have shunned riskier assets such as tech stocks. Treasury yields surged higher in early Friday trading, with the 5-year up nine basis points to trade at 2.91% as the 30-year also rallied nine basis points to 3.07%.

The bears kept up the selling pressure yesterday after the PPI disappointed investors hoping for more of an improvement. However, in the last 30 minutes, a sharp larry began cutting the day’s losses substantially. Futures suggest a bullish open, hoping that the Import/Export and Consumer Sentiment numbers don’t give more inspiration to the bears. After six straight days of selling, indicators suggest we are overdue for a relief rally. If we do trigger some short covering, remember to respect overhead resistance and downtrend levels for entrenched bears likely willing to defend.

Markets gapped down Thursday as PPI came in as expected, +0.5%, which was way down from last month’s +1.6%. The Core PPI (stripping out volatile food and energy) came in lower than expected (+0.4% vs +0.6% forecast). After the gap down, stocks rallied to the highs of the day at 11am when a reversal and strong, sustained selloff took markets to the lows at 3pm. However, the day ended on strong rally off the lows to end the day basically flat. This left us with indecisive, long-legged Spinning Top candles in all 3 major indices. On the Day, SPY lost 0.09%, DIA lost 0.25%, and QQQ lost 0.21%. The VXX fell to 26.93 and T2122 climbed a bit, but stayed deeply in the oversold territory to 1.60. 10-year bond yields fell to 2.873% and Oil (WTI) rose 1.13% to $106.90/barrel. Consumer Cyclicals (+1.63%) and Healthcare (+1.50%) led on the day with Utilities (-0.79%) and Basic Materials (-0.60%) pacing the losses.

During the day Fed Chair Powell was reconfirmed for a second term. In other market-related news, the cryptocurrency story refused to go away today with the supposedly-stablecoin LUNA losing 97.48% of its value (dropping to $0.03 in value). Ethereum also lost 8.7% and Bitcoin remained relatively stable, down 2%, but hitting $26,000 before closing at $29,400 (down from $41,500 less than a month ago). Treasury Sec. Yellen told reporters the recent volatility and decoupling of so-called pegged stablecoins is a clear example of why the government should be regulating that market.

Meme stock mania made a comeback Thursday with AMC trading in a 29% range to close up 8% on the day. In addition, GME traded in a 30% range, was halted multiple times for excess volatility, and closed up 10.13%. TLRY also 9.36% on a relatively stable 14% range while BBBY traded in a 17% range to close up only 1.95%. HOOD also spiked 5% on the day, but this might also have been on leaks related to the after-hours story that a cryptocurrency exchange CEO is buying a 7.6% stake in HOOD. This caused the stock to spike +41% in after-hours trading.

After the close, MSI, EDR, and PAM all reported beats on both revenue and earnings. Meanwhile, HLI missed on revenue while beating on earnings. On the other side, TOST, COMP, and VZIO beat on revenue while missing on earnings. US Senator Paul has killed the effort to fast-track the aid package to Ukraine. He is demanding a special Inspector General to oversea all spending from the package. He refused to allow it to be voted on as an amendment, instead insisting it must be part of the main bill. This will delay passage by several days despite strong bipartisan support.

This morning, Elon Musk says his purchase of TWTR is “temporarily on hold.” The reason for this pause is an audit to verify that less than 5% of TWTR accounts are not real people but actually fake/bot users. TWTR has also frozen hiring and has rescinded job offers previously made until the deal closes. TWTR stock is plummeting in premarket trading, down 14% at time of this writing. Elsewhere, Bloomberg reports that Fed Chair Powell reiterated that the FOMC will hike rates by half a percent at each of its next two meetings. He also said that whether or not the economy goes into recession is outside of the Fed’s control. Finally, the Terra project has stopped processing block chain transaction for the second time in less than a day. This came as the company scrambled to find a way to reconstitute their network in the face of Luna having dropped to practically zero. Binance has already suspended trading of that crypto.

Overnight, Asian markets leaned heavily to the green side. Japan (+2.64%), Hong Kong (+2.68%), and South Korea (+2.12%) led the gainers with only 3 exchanges just barely in the red. In Europe, stocks are following Asia with all but 2 exchanges well into the green at mid-day. The FTSE (+1.56%), DAX (+1.35%), and CAC (+1.53%) lead the way with only Belgium and Denmark slightly in the red in early afternoon trading. As of 7:30 am, US Futures are pointing toward a strong gap higher to start the day. The DIA implies a +0.75% open, he SPY implies a +1.09% open, and the QQQ implies a +1.66% open at this hour. 10-year bond yields are back up to 2.904% and Oil (WTI) is up 1.7% to $107.96/barrel in early trading.

The major economic news scheduled for release on Friday is limited to Apr. Imports/Exports (8:30 am), Michigan Consumer Sentiment (10 am), and a couple of Fed speakers (Kashkari at 11 am an Mester at noon). Major earnings reports scheduled for the day are limited to HMC before the open. There are no major earnings reports after the close.

So far this morning HMC reported beats on both lines. Meanwhile, DWAHY, ISUZY, and TRYIY missed on revenue while beating on earnings. On the other side, KDDIY, GASNY, OJIPY, BPIRY, and AACAY have reported beating the estimates on revenue but missed on the bottom line. Finally, SMFG, MARUY, RKUNY, ATASY, PBSFY, and AHKSY have reported misses on both lines.

Premarkets seem to be gapping strongly in favor of the bulls this morning as markets try to prevent the SPY from slipping into a bear market (down 20% from its recent high). However, remember that the last two gaps higher were “bull traps” that were met with strong selloffs. So, don’t go chasing gaps, especially gaps against the trend. Regardless of the action today, it seems very unlikely that any of the major indices can avoid yet another down week. Inflation, geopolitical risk, and cryptocurrency meltdowns are also on Mr. Market’s mind. So, caution remains the smart play. Remain nimble, hedged, and small (if not flat) as we head into the weekend. There is certainly no need to panic or experience FOMO. If you want to trade this market, unless you are a daytrader, the smart move is to stick with the downtrend. The bears still have all the momentum.

Stick with your trading rules and manage the things that you can control while trying not to worry about the things you have no control over at all. Trade with the trend, don’t chase, keep consistently taking profits when you have them, and move your stops in your favor. Remember that the first rule of making big money in the market is to not lose big money in the market. So, don’t be stubborn, and protect yourself from yourself. You also don’t need to be in the market all the time. If this isn’t a market condition you thrive in, then get out of the way. It will settle out at some point and it’s far better to wait and have money for the right market condition than to force trades now and be busted when things do turn. Keep in mind that nobody is right all the time. If you’re wrong, just admit it and take your loss. Focus on your process and enjoy yourself.

Ed

Swing Trade Ideas for your consideration and watchlist: No Trade Ideas Today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Despite the analyst’s prognostication that the CPI had peeked, we learned yesterday that inflation keeps chugging along at 40-year highs bringing out the bear to set new 2022 lows by the close. Today we get another look at the impact of inflation on producers with the PPI report. We will also see if jobless claims declined as analysts expect before the bell. Though bond yields are declining this morning, the national average gas price ticked higher to $4.42, increasing the consumer’s pressure which does not bode well for the consumer sentiment report expected Friday morning.

Asian markets saw red across the board, with Hong Kong leading the selloff down another 2.24%. European markets also see nothing but red this morning, with the DAX, FTSE & CAC down more than 2%. With another busy day of earnings and critical economic data pending, U.S. futures point to a bearish open but have recovered substantially from overnight lows. Get ready for another day of wild price swings.

Economic Calendar

Earnings Calendar

We have a busy day on the Thursday earnings calendar, though the number of notable’s continues to decline. Notable reports include AFRM, ACB, TAST, COMP, CEG, CYBR, DUOL, AG, HGBL, HIMX, LSF, LZ, PDFS, PHUN, POSH, RYAN, SIEGY, SIX, DTC, SQSP, TPR, TTM, TOST, UTZ & VZIO.

News & Technicals’

Tether sank to as low as 98 cents Thursday morning, according to data from CoinGecko. It’s meant to be pegged one-to-one to the U.S. dollar. Tether’s decline came after terraUSD, a different stablecoin, plummeted below 30 cents Wednesday. Bitcoin continued to decline losing 2021 gains, falling as low as $26,595.52 Thursday morning, hitting its lowest level in over 16 months. Ether’s second-biggest digital currency tanked as low as $1,789 per coin. A growth slowdown is underway in the U.K. after the economy shrank by 0.1% in March, with economists expecting further contractions this year. The surprise monthly contraction presents a worry for Prime Minister Boris Johnson’s government as the country’s cost-of-living crisis is yet to reach its peak. Sterling hit a two-year low versus the U.S. dollar following the GDP data as traders digested growing uncertainty about the U.K.’s economic outlook. NATO membership would be a historic decision for Finland, which shares a 1,300-kilometer border with Russia. Atlantic Council’s Northern Europe director Anna Weislander says both Finland and Sweden are well prepared to meet the oft-repeated political and military threats against the move by Russian President Vladimir Putin. The armed forces of both countries enjoy high compatibility with NATO member states, she said. A growth slowdown is underway in the U.K. after the economy shrank by 0.1% in March, with economists expecting further contractions this year. The surprise monthly contraction presents a worry for Prime Minister Boris Johnson’s government as the country’s cost-of-living crisis is yet to reach its peak. Sterling hit a two-year low versus the U.S. dollar following the GDP data as traders digested growing uncertainty about the U.K.’s economic outlook. Treasury yields fell in early Thursday trading, with the 10-year dipping to 2.84% and the 30-year declining to 2.99%.

After learning that inflation keeps chugging along at 40-year highs, we experienced another hectic day of whipsaws on Wednesday that set new 2022 lows at the close. Though indicators suggest a substantial short-term oversold condition, the market faces another reading on inflation before today’s open to determine the level of pressure in producer prices. We will also get a reading on the Jobless Claims that analysts project declined last week, and they are also expecting a decline in PPI. However, futures markets don’t seem to share that confidence this morning after yesterday’s disappointment. So, will the data continue to pile on the gloom inspiring the bears, or will it give confidence in the bulls to begin a relief rally? We will soon find out. The news that Findland and Sweden may apply to join NATO is another thing to keep an eye on as Russia warns of a Catastrophic conflict that could be the result. Traders should expect the wild price action to continue with so much uncertainty.

On Wednesday CPI came in hotter than expected (but still better than last month) and as a result premarkets pulled back, giving us a small gap down at the open. From there, the QQQ led the other indices into an all-day selloff that closed near the lows in all 3 major indices. This gave us big, ugly black candles and new 52-week lows in all three. On the day, SPY lost 1.61%, DIA lost 1.02%, and QQQ lost 2.99%. The VXX diverged from expectations by only rising a fraction to 27.28 and T2122 fell even more deeply into the oversold territory at 0.81. 10-year bond yields fell to 2.93% and Oil (WTI) spiked 5.4% to $105.18/barrel after having lost 10% in the prior couple of sessions.

As mentioned, the April Consumer Price Index showed an 8.3% increase (year on year), which was higher than the 8.1% expected, but still less than March’s 8.5%. Analysts say this indicates we are at peak inflation and could see it slacking off later this year. However, the Core CPI number (which strips out volatile food and energy impacts) was up 0.6% in April which was much higher than the 0.4% expected. While markets are still pricing in “just” a half-percent hike in June, the potential for a three-quarter percent hike seems back in the cards as the Fed’s favorite inflation measure (Core CPI) came in well above expectations.

After the close, FUJIY, STE, and DOX reported beats on both revenue and earnings. Meanwhile, CPNG missed on revenue while beating on earnings. Finally, DIS, VIV, and OPHLY reported misses on both lines. With that said, DIS did beat significantly on Disney+ subscription estimates.

Cryptocurrency volatility is off the charts again, even by crypto standards. Bitcoin was down almost 11% this morning before recovering some 8% of that loss. This comes as COIN had to explain the risk of bankruptcy to their users after $200 billion of wealth has been wiped out by selloffs over just the last 24 hours. At the same time Project Terra (Luna and UST stablecoins) continue to decouple from their supposed peg to the US Dollar. At one point Wednesday, UST was trading at less than 30 cents while Luna has lost 97% of its value in the last day.

On the Russian invasion story, the Russian Foreign Ministry told the US Ambassador in Moscow that Russian-controlled portions of Ukraine will be requesting annexation by Russia. Meanwhile, Italian PM Draghi said that Italy European companies can pay for their gas in Rubles without breaching sanctions, in direct conflict with EU guidance on the matter. The other developments were diplomatic, with Russia warning of nuclear war if the West continues to send arms to Ukraine and train their military, Finland moving very close to requesting NATO membership, and the UK signing a security guarantee with/for Sweden.

Overnight, Asian markets were red across the board. Taiwan (-2.43%), Hong Kong (-2.24%), and India (-2.22%) led the way lower. However, the only exchanges to avoid a 1% loss were Shanghai (-0.12%) and Shenzhen (-0.13%). In Europe we see the same picture taking shape at mid-day. The FTSE (-2.04%), DAX (-1.97%), and CAC (-2.13%) are leading the way lower as disruption to natural gas supplies, disagreement over caving to Russian demands for Rubles, and inflation are the main fears of the day. As of 7:30 am, US Futures are pointing toward a down start to the day ahead of the morning data. The DIA implies a -0.36% open, the SPY implies a -0.50% open, and the QQQ implies a -0.95% open at this hour. 10-year bond yields are down again to 2.841% and Oil (WTI) is off 1.3% to $104.35/barrel in early trading.

The major economic news scheduled for release on Thursday include Apr. PPI and Weekly Initial Jobless Claims (both at 8:30 am), the WASDE Report (noon), and a Fed speaker (Daly at 3 pm). Major earnings reports scheduled for the day include BAM, DDS, KELYA, NICE, PRMW, TPR, USFD, and WE before the open. Then after the close, AQN, COMP, EDR, MSI, TOST, and VZIO report.

So far this morning BAM, TOELY, SFTBF, SOMLY, UTZ, TPR, WE, and CIXX have reported beats on both revenue and earnings. Meanwhile, SFTBY, NSANY, CSIOY, YPF, and HIMX all missed on revenue while beating on earnings. On the other side, NTTYY, SSMXY, and ALIZY have reported beating the estimates on revenue but missed on the bottom line. Finally, SIEGY, TEF, KUBTY, SSDOY, KNBWY, BOUYY, FUJHY, STBFY, TAST, TINLY, and GHG have reported misses on both lines.

Premarkets continue to be red this morning with PPI and Jobless Claims coming before the bell. Geopolitical and cryptocurrency risks are also on Mr. Market’s mind. However, we have another few weeks before the next Fed hike and the betting has not changed in the last week. Most futures traders expect a half-point hike. So, we have time to adjust and no major changes are expected. Again, no need to panic or experience FOMO. If you want to trade this market, unless you are a daytrader, the smart move is to stick with the downtrend. The bears still have all the momentum.

Stick with your trading rules and manage the things that you can control while trying not to worry about the things you have no control over at all. Trade with the trend, don’t chase, keep consistently taking profits when you have them, and move your stops in your favor. Remember that the first rule of making big money in the market is to not lose big money in the market. So, don’t be stubborn, and protect yourself from yourself. You also don’t need to be in the market all the time. If this isn’t a market condition you thrive in, then get out of the way. It will settle out at some point and it’s far better to wait and have money the market condition you prefer than to force trades now and be busted when things do turn. Keep in mind that nobody is right all the time. If you’re wrong, just admit it and take your loss. Focus on your process and enjoy yourself.

Ed

Swing Trade Ideas for your consideration and watchlist: BTU, VET, SWN, TECK, TCOM, MOS, ABC, HAL, APA, SLB, KWEB, AIZ, L, ANTM, KR. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

As we waited for the CPI number, Tuesday proved to be a rollercoaster ride of uncertainty, starting with a nasty pop and drop that made new 2022 lows while chopping all afternoon wildly. We will soon know the result, and the question is, will it inspire the bulls or the bears? Get past that, and we still have to deal with a PPI number on Thursday as prices at the pump hit new record highs. So, prepare for just about anything as the drama unfolds amidst another big day of uncertain earnings results.

While we slept, Asian markets caught a modest rally with data showing their inflation heated up in April. Likewise, European markets are in rally mode despite a substantial jump in natural gas prices as the ECB confirms rate hikes ahead. With hopefulness, the CPI will show that inflation has peaked, U.S. futures suggest a gap up open similar to yesterday. Will this one hold, or will we see another disappointing pop and drop?

Economic Calendar

Earnings Calendar

We have a little lighter day on the earnings calendar with under 175 companies listed. Notable reports include DIS, AWH, BYND, BMBL, CNFR, CPNG, WATT, GPRK, DNUT, NGMS, PAAS, PAYS, PAAS, PRGO, RIVN, SONO, TAK, TM, COOK, WEN, WWW & YETI.

News & Technicals’

Investors are eyeing what could be a pivotal consumer price index report for April, anticipating that the data shows inflation has already reached its height. Economists warn that prices could remain elevated. The issue is how fast inflation could decline when determining how the Federal Reserve will respond with interest rate hikes. CPI is expected to rise 0.2% in April or 8.1% on an annualized basis. That’s compared with a 1.2% monthly increase or 8.5% gain year-over-year in March. UST, a so-called stablcoin meant to maintain a $1 peg, was trading at less than 50 cents Wednesday. Sister token luna dived more than 80%, as the creator said he is close to announcing a recovery plan. According to a J.D. Power survey published Wednesday, packed planes and more expensive tickets drove down customer satisfaction with airlines over the past year for the first time in a decade. Customer satisfaction dropped among travelers across all the ticket classes. According to Adobe data, in March, domestic U.S. airfares were 20% higher than in 2019. ON TUESDAY, Gas TSO of Ukraine (GTSOU) announced force majeure – unforeseeable circumstances that prevent the fulfillment of a contract – the first declaration of its kind since the Russian invasion. From Wednesday, it will not accept through its Sokhranivka entry point, which delivers Russian gas to Europe. TTF European natural gas prices were up more than 6.4% by around 9:15 a.m. London time on Wednesday, according to Refinitiv data. Lagarde was cementing market expectations that the ECB will raise its policy rate for the first time in over a decade in July to tame record-high eurozone inflation — the result of surging energy prices spilling over to other goods. Most other central banks have already raised borrowing costs, but the ECB, which had fought too low inflation for a decade, is still pumping cash into the financial system via bond purchases. Treasury yields pulled back again in early Wednesday trading, with the 10-year declining to 2.94% and the 30-year dipping to 3.08%.

Tuesday trading was a rollercoaster ride of uncertainty as analysts worked to convince investors that inflation peaked last month even as food and energy prices surged to new records. National average gas prices jumped to $4.40 a gallon, and diesel increased to $5.55, punishing Americans on everything they buy, sell or do. As a result, all eyes will be on the CPI number coming out before the bell, so although the futures indicate a hopeful outcome, expect considerable price volatility as the market reacts. The T2122 indicator suggests that we are overdue for a relief rally; however, the bears are likely to attack if the CPI comes in hotter than expected. On the other hand, should the CPI come in better than expected, the bulls could trigger a short squeeze rally. There is a lot at stake with the SP-500 clinging to 4000 and the QQQ trying to hold 3000 price levels. We also get the Petroleum Statis number and have a 10-year bond auction to keep an eye on today. As you plan forward into Thursday, remember the PPI number will also be critical to investor sentiment. Ready or not, here it comes!

Stocks gapped up 1.5% Tuesday in what appeared to be a relief rally in the making. However, it was a Bull Trap that the Bears sprung immediately leading to a steady selloff that lasted all morning, more than filling the gap before flattening out near the lows by lunchtime. Still, the whipsaw was not done. So, stocks reversed and a strong rally kicked in about 12:30 pm, followed by another selloff, and then another rally, etc. This action gave us indecisive, big wick, black candles that both printed new 52-week lows and look to be ending in the green in the QQQ and SPY. The technology and healthcare sectors led on the day with Utilities lagging. On the day, SPY was up 0.23%, DIA closed down 0.26%, and QQQ rose 1.21%. The VXX fell 3.4% to 27.05 and T2122 remained deeply oversold at 1.33. 10-year bond yields fell but then rebounded to close just below 3% at 2.993% and Oil (WTI) fell 3.45% to $99.56/barrel.

After the close, OXY, GFS, FNF, HRB, RXT, GO, ALC, SCSC, DAR, and ADV all reported beats on both revenue and earnings. Meanwhile, ELY missed on revenue while beating on earnings. On the other side, WELL reported beating the estimates on revenue but missed on the bottom line. Finally, EA, COIN, RBLX, WYNN, YELL, RKT, OSCR, GSM and DBD reported misses on both lines.

Cryptocurrency markets are in turmoil as twice in the last 2 days a major “stablecoin” has decoupled from its supposed dollar pegging. The idea behind a stablecoin is that a computer algorithm maintains a 1:1 peg to the dollar by buying/destroying digital assets. (This would be like the dollar under the gold standard, but with a computer printing/burning dollars in an attempt to maintain the dollar-gold exchange rate.) The first to decouple was Luna, which dove more than 80% in value. Then UST dropped as far as to 31 cents and is now trading at 50 cents on the dollar. Both stablecoin are part of the same project Terra. Terra creator Do Kwon (who has also amassed billions of dollars’ worth of bitcoin) said Tuesday he is close to announcing a plan to recover and return to a 1:1 dollar peg. The moral of the story is that stablecoins aren’t.

On the Russian invasion story, Finland’s Foreign Minister Haavisto said his country is now just days away from applying for NATO membership. Meanwhile, the war may be expanding as Belarus moved their special forces to the border of Ukraine claiming that the US and its allies are increasing their presence on that country’s border. Ukraine said that it will turn off natural gap pipelines from Russia to Europe as Russia’s forces have disrupted operations at several facilities. This pipeline accounts for a third of Russian gas exports to Europe and this may well reduce supplies for EU countries.

The economic news coming later this week includes Apr. PPI, Weekly Initial Jobless Claims, the WASDE Report, and a Fed speaker on Thursday. Then on Friday, we see Apr. Imports/Exports, Michigan Consumer Sentiment, and a couple more Fed speakers.

The talk in financial markets seems to be all expecting a Fed “overshoot.” In other words, they are assuming that inflation has now peaked and the Fed is behind the curve, tightening into a slowing economy. That would lead to a so-called hard landing. This is all just US-focused, but there are and will be impacts on global markets from the Russian aggression and Western responses with the CIA reporting Putin is preparing for a very long-term conflict. For example, food prices will be raised when the supply of grain is reduced a significant amount. And oil prices cannot help but be impacted as the West is at least nominally banning Russian oil while Saudi Arabia and the UAE are warning about a lack of capacity to expand production to offset those reductions. My point is that markets tend to front-run the economy by 3-9 months and it is impossible to forecast something when the future environment is not known. So, watching the chart is much better than predicting the market in months-long positions.

Overnight, Asian markets were mixed again but on more muted moves than earlier this week. Shenzhen (+1.80%), Hong Kong (+0.97%), and Shanghai (+0.75%) led the gains while Thailand (-0.58%), India (-0.45%), and Taiwan (-0.35%) paced the losses. This came as Chinese Consumer Prices rose by 2.1% in April, the fastest increase since November. Meanwhile, in Europe, markets are mostly in the green despite a spike in natural gas prices on the Russian pipeline news. The FTSE (+1.11%), DAX (+1.29%), and CAC (+1.94%) are leading the region higher in early afternoon trading. As of 7:30 am, US Futures are pointing toward a gap up to start the day once again. The DIA implies a +0.86% open, the SPY is implying a +1.13% open, and the QQQ implies a +1.48% open ahead of key inflation data. 10-year bond yields are down again to 2.93% and Oil (WTI) is up almost 3.5% to $103.22/barrel in early trading.

The major economic news scheduled for release on Wednesday includes Apr. CPI (8:30 am), Crude Oil Inventories (10:30 am), 10-year Bond Auction (1 pm), and Apr. Fed. Budget Balance (2 pm). There is also another Fed speaker (Bostic at noon). Major earnings reports scheduled for the day include ICL, NOMD, PFGC, PRGO, SLVM, TM, WEN, and WWW before the open. Then after the close, DOX, APP, CPA, CPNG, PAAS, STE, and DIS report.

So far this morning WWW, OCPNY, and ICL have reported beats on both revenue and earnings. Meanwhile, NOMD, ADRNY, PCRFY, BRTHY, and EC all missed on revenue while beating on earnings. On the other side, BRDCY, SGIOY, AJINY, MNBEY, and PRGO have reported beating the estimates on revenue but missed on the bottom line. Finally, TM, TAK, FUJIY, AGESY, SMTOY, ATC, and WEN have reported misses on both lines.

Premarkets are up significantly and most analysts are saying that they expect the April CPI to show that inflation has now peaked (expecting an +8.1% print versus last month’s +8.5% number). This means that the risk this morning is on the downside as an unexpectedly hot print could reverse overnight gains and shock markets. Either way, there is no reason to panic and chase the open Futures are backing off earlier highs. Regardless of the number, the Fed is still very likely to raise rates by half a percent in June and it would take a significant shock one way or the other to move them off that amount of hike. This means that markets will still have several weeks to adjust before the Fed regardless of today’s number. Again, no need to panic or experience FOMO. So, once again the question is whether the implied gap up is a “dead cat” bounce or the beginnings of a reversal. The smart money remains in the “relief rally at best, bull trap at worst” camp given the strong bear trend and current over-extension. So, if you are bound to go long in this move, be very cautious and extremely nimble. The bears still have all the momentum.

Stick with your trading rules and manage the things that you can control while trying not to worry about the things you have no control over at all. Trade with the trend, don’t chase, keep consistently taking profits when you have them, and move your stops in your favor. Remember that the first rule of making big money in the market is to not lose big money in the market. So, don’t be stubborn, and protect yourself from yourself. You also don’t need to be in the market all the time. If this isn’t a market condition you thrive in, then get out of the way. It will settle out at some point and it’s far better to wait and have money the market condition you prefer than to force trades now and be busted when things do turn. Keep in mind that nobody is right all the time. If you’re wrong, just admit it and take your loss. Focus on your process and enjoy yourself.

Ed

Swing Trade Ideas for your consideration and watchlist: VMD, NXPI, OXY, MCK, WDC, HPQ, ABC, EPAM, JPM, MRK, VLO, VZ, CHRW, GSK, EXPD, PVH. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Inspired by selling pressure around the world, the bears continued to drive the indexes lower, pushing the SPY below 4000 and the QQQ below 3000 at the close of the day. Today, we have another busy day of earnings data, a Fed speakers parade, and a 3-year bond auction. Indicators suggest a short-term oversold condition, but traders will need to remain nimble with key inflation numbers coming Wednesday and Thursday. So, plan your risk carefully with challenging price action expected in the days ahead!

Asian markets traded mostly lower as we slept, with Hong Kong extending Monday’s losses by another 1.84%. European markets see green across the board this morning rebounding to relieve some selling pressure though the indexes remain in downtrends. U.S. futures also look ready for a bit of relief in the selling this morning, pointing to a gap up open ahead of a busy day of earnings. AS you plan forward, remember the CPI number coming out before the market opens on Wednesday.

Economic Calendar

Earnings Calendar

Tuesday is a busy day with nearly 250 companies listed on the earnings calendar. Notable reports include OXY, BIRD, ARMK, BHC, SKIN, BLDR, ELY, CHH, COIN, CRON, EA, FOXA, FTCI, GFS, GMED, HL, IIVI, KGC, LI, LBTYA, MTTR, NXST, KIND, PTON, PLNT, RXT, REAL, RBLX, RKT, SOFI, SU, SWCH, SYY, TDW, TTD, U, VERX, WMG, WELL, FREE, WKHS, XL & XPEL.

News & Technicals’

According to new data from Realtor.com, the supply of homes for sale is finally showing signs of improvement. In April, inventory was 12% lower than the year-earlier month, the smallest year-over-year decline since 2019. The shift in supply is likely due to a slower sales pace stemming from the recent increase in mortgage rates, making expensive homes even pricier. However, the number of active listings is still down 67% from pre-pandemic levels. The most valuable publicly traded company, Apple, had seen its market capitalization trimmed by over $200 billion since Wednesday when the Fed raised interest rates by a half percentage point. However, like Campbell Soup, General Mills and J.M. Smucker, Staples have outpaced Big Tech in three trading days. Moscow last week made payments to holders of two dollar-denominated Russian sovereign bonds, maturing in 2022 and 2042 and worth a collective $650 million. Russia has benefited from an exemption in U.S. sanctions that allows bond payments to be made on Russian sovereign debt from sources authorized by the Treasury on a case-by-case basis. However, this exemption expires on May 25, and MSCI suggested that unless extended, it could trigger a default event when several Russian bond payments are due on May 27. Crypto project Terra is buying billions in bitcoin to support UST, a controversial stablecoin. Its creator Do Kwon believes bitcoin can become the “reserve currency” of the Terra ecosystem. However, that belief is being tested as UST falls below its $1 peg. Amazon recently fired two employees involved in the organizing effort at a Staten Island warehouse, where workers voted to join a union last month. Tristan Dutchin and Matt Cusick, who are part of the Amazon Labor Union’s organizing committee, said they were fired by Amazon last week. Treasury yields pulled back in early Thursday trading, with the 10-year trading at 3.02% and the 30-year declining to 3.13%.

The bears continued to drive the indexes lower Monday, with the SPY closing below 4000 and the QQQ ending the day below 3000. The Dow set a new 2022 low by a few ticks as the IWM pushed sharply lower. Interestingly even as the VIX rose, it seemed somewhat controlled, with the indexes largely chopping in a range most of the afternoon. The T2122 indicator is in a short-term oversold condition suggesting a relief rally may be possible soon. However, with a big day of earnings data and the tense geopolitical events, traders will have to stay focused on watching for intraday whipsaws. With the CPI number out Wednesday morning, get ready for another dose of volatility that could squeeze out short traders if there is an improvement or quickly inspire the bears to keep pushing for new market lows. So, buckle up as the wild ride continues!

Markets gapped down more than 1.5% today and then followed through until the SPY managed to find some support at the 500sma around 11:30 am. Despite an hour-long mid-day attempt to bounce, the bears stepped back in to take all 3 major indices back to their lows by 2 pm and continue sliding toward the lows of the day. The QQQ was clearly the ugliest of the major indices, with the SPY not far behind while the DIA benefitting from the safety trade printing a gap-down black Spinning Top that bounced up off the February low (probably on safety trades). Every sector was in the red, with Energy leading the charge lower. This left us at new 52-week lows in all 3 of the major indices. On the day, SPY lost 3.16%, DIA lost 1.89%, and QQQ lost 3.86%. The VXX rose 3.5% to 28.01 and the only possible silver lining for the Bulls is that the market is now very oversold with the T2122 falling to 1.33. 10-year bond yields fluctuated wildly during that day, reaching the high since 2009 (3.185%) but fell back to 3.04% by day end. Oil (WTI) fell a whopping 6.4% to $102.75/barrel.

After the close, SPG, IFF, EQH, AMC, XPO, CLOV, HI, MRC, VRM, UNVR, and MCHP all reported beats on both revenue and earnings. Meanwhile, ICUI, DNB, missed on revenue while beating on earnings. On the other side, IAC, CAPL, SWX, VVV, and RNG reported beating the estimates on revenue but missed on the bottom line. Finally, NVAX, ZNGA, and PRIM reported misses on both lines.

Realtor.com reports that the supply vs. demand balance of the real estate market has started to improve. April home for sale inventory was down just 3%-12% from the same time in 2021 and this was the smallest year-over-year drop since 2019. The data suggest that the rapid rise in interest rates, which has made housing bubble prices even more expensive for buyers is slowing the pace of sales, despite listings being down 67% from pre-pandemic levels.

On the Russian invasion story, MSCI research said they are now expecting Russia to default on bond payments on May 27. Since late February, the US Treasury Dept. has been approving (on a case-by-case basis) Russian payment on bond debt. The exemption to sanctions that allowed that flexibility expires May 25 and the firm does not believe the US will renew the exemption. Elsewhere, NBC reports that more than 1 million Ukrainians have been forcibly relocated to Russia. Meanwhile, the European Bank for Reconstruction and Development estimates the Russian economy will only shrink 10% in 2022 (mostly due to the huge increases in exported energy prices largely offsetting the loss of domestic activity), while the Ukrainian economy will shrink by 30%. To me, a contraction of only 30% is nearly miraculous. With an active war ongoing, many of the major centers of industry in ruins, all ports closed, one-third of the population now being refugees, and only half of the crops able to be planted, it is hard to see how the country’s output could be down only 30%. Finally, the US has suspended the 25% tariff on Ukrainian steel for a year. (That said, it is unclear how much steel can make it from Ukraine to the US given most steel production is in the South-Eastern parts of the country and would normally ship through the closed ports.

The Fed warned of tightening financial market liquidity overnight. Meanwhile, the market waits on more inflation data tomorrow as well as President Biden speaking on the subject at 11:30 am today…and inflation has been the key market driver for a while now. Oil markets have slumped the last two days as traders see the EU softening its sanctions on Russian oil in the face of Pro-Putin Hungary’s veto power on the ban. (The problem with the EU is that it requires unanimity to act.)

The economic news coming later this week includes Apr. CPI, Crude Oil Inventories, 10-year Bond Auction, and Apr. Fed. Budget Balance on Wednesday. Then on Thursday, we get Apr. PPI, Weekly Initial Jobless Claims, the WASDE Report, and a Fed speaker. Finally, Friday we see Apr. Imports/Exports, Michigan Consumer Sentiment, and a couple of Fed speakers.

Overnight, Asian markets were mixed. Shenzhen (+1.37%), Thailand (+1.14%), and Shanghai (+1.06%) led the gainers. Meanwhile, Hong Kong (-1.84%), New Zealand (-1.34%), and Singapore (-1.25%) paced the losses. (Hong Kong’s bad day may in part be the result of a new “pro-reintegration-to-China” leader who has taken over. In Europe, stocks are rebounding from Monday’s terrible day as of mid-day. The FTSE (+0.67%) lags as the “Queen’s Speech” was delivered in absentia and focuses on the high cost of living. However, the DAX (+1.44%) and CAC (+0.96%) are typical of the region in early afternoon trading. As of 7:30 am, US Futures are pointing toward a gap higher to start the day as stocks try to recover some of Monday’s losses. The DIA implies a +0.77% open, the SPY is implying a +0.87% open, and the QQQ implies a +1.32% open at this hour. 10-year bond yields have dropped sharply but remain above 3% at 3.024% and Oil (WTI) is off another 1.7% to $101.41/barrel in early trading.

Once again, there is no major economic news scheduled for release on Tuesday. However, there are 5 Fed speakers scheduled (Williams at 7:40 am, Bostic at 8:30 am, Waller and Kashkari, both at 1 pm, Mester at 3 pm, and Bostic again at 7 pm). Major earnings reports scheduled for the day include FOX, AHCO, ARMK, AVYA, BHC, BCO, BLDR, CCO, XRAY, DBD, DSEY, EPC, FOXA, H, IAA, IIVI, IGT, LCII, LI, LDI, MIDD, EYE, NXST, NCLH, PTON, PLTK, REYN, SONY, SYY, TDG, UWMC, and WMG before the open. Then after the close, ADV, ALC, ELY, COIN, DAR, EA, GSM, FNF, GFS, GO, HRB, JXN, LBTYA, LNW, OXY, OSCR, RXT, RBLX, RKT, SCSC, WELL, WYNN, and YELL report.

So far this morning BAYRY, DKILY, ITOCY, BLDR, MIDD, IIVI, IAA, IGT, LCII, ARMK, and NXST have all reported beats on both revenue and earnings. Meanwhile, SONY, NTDOY, SSUMY, TYOYY, EYE, AZUL, and SU all missed on revenue while beating on earnings. On the other side, HGV has reported beating the estimates on revenue but missed on the bottom line. Finally, NPSCY, XRAY, NCLH, PTON, RICOY, AVYA, DBD, BHC, and KWHIY have reported misses on both lines.

Futures are backing off earlier highs. However, it appears we will still see a bounce at the open. The question is whether that is a “dead cat” bounce or the beginnings of a reversal. The smart money remains in the “relief rally only” camp given the strong bear trend and current over-extention. So, if you are bound to go long in this move, be very cautious and extremely nimble. The bears still have all the momentum and this would be an excellent place for a Bull trap. As always, don’t get caught chasing moves, and be quick to take profits when you have them.

Stick with your trading rules and manage the things that you can control while trying not to worry about the things you have no control over at all. Trade with the trend, don’t chase, keep consistently taking profits when you have them, and move your stops in your favor. Remember that the first rule of making big money in the market is to not lose big money in the market. So, don’t be stubborn, and protect yourself from yourself. You also don’t need to be in the market all the time. If this isn’t a market condition you thrive in, then get out of the way. It will settle out at some point and it’s far better to wait and have money the market condition you prefer than to force trades now and be busted when things do turn. Keep in mind that nobody is right all the time. If you’re wrong, just admit it and take your loss. Focus on your process and enjoy yourself.

Ed

Swing Trade Ideas for your consideration and watchlist: SHW, TSLA, NVDA, MSFT, AMZN, NFLX, JPM, FB, AAPL, BBIG, ADM, PEP, C, WFC, GILD, SPXS, UVXY, SQQQ . You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service