Futures tied to the Nasdaq-100 declined as investors scrutinized Nvidia’s earnings report. Despite Nvidia surpassing third-quarter expectations and providing robust guidance, its shares dropped 3% in premarket trading. This reaction highlights the heightened expectations surrounding Nvidia, as noted by Aswath Damodaran, a finance professor at New York University’s Stern School of Business. He remarked on CNBC’s “Closing Bell: Overtime” that Nvidia not only needs to exceed analyst estimates but must do so by a significant margin, around 10%, to satisfy market anticipations.

European stocks flattened out due to weak global market sentiment. British sports retailer JD Sports saw its shares plummet over 14% in early trading after cautioning that its annual profits would likely hit the lower end of its forecast. Conversely, Zurich Insurance shares climbed 2% following the announcement of a new three-year plan. The overall market sentiment was further dampened by investor reactions to the crucial earnings report from artificial intelligence leader Nvidia.

Asia-Pacific markets experienced a downturn as investors closely monitored tech shares and developments surrounding Indian stocks linked to billionaire Gautam Adani. The chair of Adani Group, along with others, faced an indictment in a New York federal court over a significant bribery and fraud scheme. This news contributed to a decline in several key indices: India’s Nifty 50 dropped by 0.72%, Japan’s Nikkei 225 fell by 0.85%, and Hong Kong’s Hang Seng index decreased by 0.32%. In contrast, mainland China’s CSI300 saw a slight gain of 0.09%. Meanwhile, markets in South Korea and Australia ended the day marginally lower.

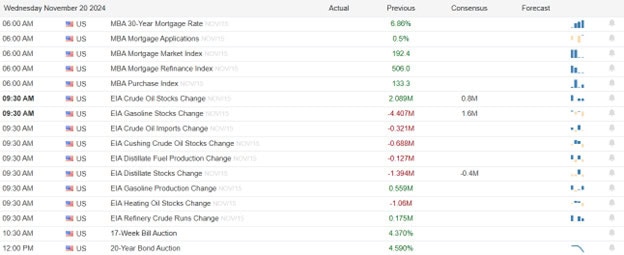

Economic Calendar

Earnings Calendar

Notable reports for Wednesday before the bell include AKTR, BJ, BEKE, DE, SCVL, VSTS, & WMG. After the bell reports include CPRT, ESTC, GAP, INTU, ROST, & UGI.

News & Technicals’

Ukraine reported that Russia launched an intercontinental ballistic missile (ICBM) overnight, targeting Dnipro city in the central east of the country. If confirmed, this would mark the first use of such a missile by Moscow in the ongoing conflict. Although the range of an ICBM seems excessive for a strike against Ukraine, these missiles are typically designed to carry nuclear warheads. The deployment of an ICBM would underscore Russia’s nuclear capabilities and signal a potential escalation in the conflict. The attack resulted in injuries to two individuals and caused damage to an industrial facility and a rehabilitation center for people with disabilities, according to local officials.

Gautam Adani, one of the world’s wealthiest individuals, was indicted in a New York federal court on charges related to an alleged bribery and fraud scheme. A spokesperson for Adani Group dismissed the allegations from the U.S. Department of Justice and the U.S. Securities and Exchange Commission against directors of Adani Green Energy as “baseless and denied.” Following the indictment, shares of companies within India’s Adani Group plummeted, with Adani Green Energy — the company at the heart of the allegations — experiencing a significant drop of 17.9%.

Chinese tech giant Baidu reported a 3% year-over-year decline in third-quarter revenue, totaling $4.78 billion for the quarter ending September 30. Despite this drop, the company exceeded market expectations, driven by growth in its AI cloud segment. Net income for the period increased by 14%, reaching $1.09 billion. However, Baidu’s U.S.-traded shares fell nearly 4% in premarket trading following the release of these results.

The Department of Justice is urging a federal judge to mandate that Google divest its Chrome internet browser as a remedy in the ongoing antitrust case. According to the filing, this action is intended to “permanently stop Google’s control of this critical search access point.” This push follows an August ruling by a U.S. judge that determined Google holds a monopoly in the search market. The proposed divestiture of Chrome aims to address and mitigate the competitive harms identified in the case.

Although NVDA was down during the night the US futures this morning have decided it was good enough to push for a gap up open. Keep in mind the rest of the world seems to have a slightly different opinion. Today we will look for clues to inspire the bulls or the bears in earnings and economic data while keeping an eye on the rising geopolitical tensions. The bond yields continue to a concern as well the oil prices rising sharply today due to the escalating conflict.

Stock futures edged higher on Wednesday as investors anticipated a crucial earnings report from tech giant Nvidia, which is set to release its results after the market close. Market participants are particularly interested in the demand for Nvidia’s Blackwell AI chips. Given Nvidia’s substantial market capitalization of $3.6 trillion, its performance could significantly influence the S&P 500 and Nasdaq Composite for the remainder of the week. Additionally, retailers Target and TJX are scheduled to report their earnings on Wednesday morning. Investors will also be paying close attention to remarks from Federal Reserve Governors Lisa Cook and Michelle Bowman, along with Boston Fed President Susan Collins.

European markets opened on a positive note early Wednesday, with the pan-European Stoxx 600 rising by 0.5% in early trading. Most sectors were in the green, except for the automotive sector. The FTSE 100 started flat but gained 0.2% following the release of data showing U.K. inflation surged to 2.3% in October, surpassing expectations. On the Stoxx 600, Sage Group emerged as the top performer, with its shares soaring nearly 17%, while national lottery operator La Française des Jeux (FDJ) was the worst performer, dropping by 5%.

Asia-Pacific markets experienced mixed performance in volatile trading on Wednesday, influenced by escalating geopolitical tensions between Ukraine and Russia. Investors closely analyzed Japan’s October trade data, which showed a year-over-year export growth of 3.1%, a significant improvement from the 1.7% decline in September. Import growth also exceeded expectations at 0.4%, although it was lower than the previous month’s 2.1%. Japan’s Nikkei 225 index dipped by 0.16%, while Hong Kong’s Hang Seng Index edged up by 0.24%. South Korea’s Kospi gained 0.42%, but the Kosdaq fell by 0.47%. Meanwhile, Australia’s S&P/ASX 200 dropped by 0.57%.

Economic Calendar

Earnings Calendar

Notable reports for Wednesday before the bell include BERY DY, GLBE, NIO, SR, TGT, TJX, & WIX. After the bell reports include CPA, JACK, MMS, NVDA, PANW, SNOW, & SQM.

News & Technicals’

The U.S. closed its embassy in Kyiv on Wednesday, citing specific intelligence about a potential significant air attack amid escalating tensions with Russia. In a statement, the U.S. Embassy announced the closure as a precautionary measure and advised embassy staff to shelter in place. Additionally, the embassy urged U.S. citizens to be ready to take immediate shelter if an air alert is issued.

Comcast is advancing with plans to spin off its cable network channels, according to sources cited by CNBC on Tuesday. The process is anticipated to take about a year, with an official announcement possibly coming as soon as Wednesday. This strategic move aims to provide cable networks with flexibility to merge with other networks or be sold to private equity. The decision comes as millions of customers shift from traditional pay TV bundles to streaming services. Over the next year, Comcast will determine necessary licensing agreements and decide if MSNBC and CNBC will continue their collaboration with NBC News.

U.S. Treasury yields rose on Wednesday as investors weighed the geopolitical tensions and recent economic data. The yield on the 10-year Treasury increased by nearly 5 basis points to 4.426%, while the 2-year Treasury yield climbed by over 2 basis points to 4.297%. The market’s focus was on the escalating conflict between Russia and Ukraine, which has intensified tensions between the U.S. and Russia. In response to the heightened threat, the U.S. closed its embassy in Kyiv, warning of a potential significant air attack.

Target reported disappointing third-quarter earnings and revenue, falling short of analysts’ estimates and prompting the company to lower its full-year guidance. Despite efforts to boost sales by cutting prices on thousands of items, Target struggled to attract customers. This underperformance stands in stark contrast to Walmart, which exceeded Wall Street expectations and raised its outlook just a day earlier.

Despite the dangerous geopolitical situation, the market continues with high anticipation of the crucial earnings from NVDA after the bell today. Obviously, this report could set the sentiment of the market for the rest of the week so be prepared for a substantial Thursday morning gap. The question is will it be up or down? Plan your risk carefully and while keeping in mind a significant air strike out of Russia could occur at any time escalating the conflict.

Tuesday brought us a gap-down (on Putin nuke threat) bullish action day. SPY gapped down 0.58%, DIA gapped 0.80% lower, and gapped down 0.53%. From there, DIA made a small detour lower, but then followed the SPY and QQQ in a consistent rally by all three major index ETFs until 2 p.m. Then they all three sold off for 40 minutes before drifting modestly higher the rest of the day. This action gave us white candles in the SPY, DIA, and QQQ. SPY gave us a large, gap-down, white-bodied outside day candle that retested its T-line (8ema) from below…and closed right on the average (to the penny). Meanwhile, DIA printed more of a gap-down, white-bodied fat Spinning Top. Finally, QQQ gave us a gap-down, large, white-bodied candle with a small upper wick. QQQ came close, but did not quite retest its T-line from below. This all happened on below-average volume in all three major index ETFs. (Well below-average in QQQ.)

On the day, seven of the 10 sectors were green as Technology (+1.11%) and Utilities (+0.83%) were way out front leading the rest of the market higher. On the other side, Communications Services (-0.53%) was by far the worst-performing sector. At the same time, SPY gained 0.37%, DIA lost 0.31%, and QQQ gained 0.69%. VXX climbed 3.32% to close at 46.38 and T2122 climbed slightly, but remains in the bottom half of its mid-range to close at 46.38. Meanwhile, 10-Year bond yields fell to 4.392% while Oil (WTI) gained 0.61% to close at $69.58 per barrel. So, Tuesday was a day marked by Putin’s bellowing that led the West to knee-jerk into fear of nuclear war. However, almost as soon as the market opened, traders regained their senses to realize that like everything in life, it’s not as bad a feared (or as good as hoped). So, we rallied off the lows in a steady pace until some mid-afternoon profit-taking.

The major economic news scheduled for Tuesday was limited, but included Preliminary October Building Permits, which came in a bit lower than expected at 1.416 million (compared to a forecast of 1.440 million and a September reading of 1.425 million). At the same time, October Housing Starts were also a little light at 1.311 million (versus a forecast of 1.340 million and the September 1.353 million value). Then, after the close, the API Weekly Crude Oil Stocks report showed a larger inventory build than predicted at +4.753 million barrels (compared to a forecasted 0.800-million-barrel build and the prior week’s 0.777-million-barrel drawdown).

In Fed news, on Tuesday, Kansas City Fed President Schmid said, “The decision to lower rates is an acknowledgement of the … growing confidence that … inflation is on a path to reach the Fed’s 2% objective. A confidence based in part on signs that both labor and product markets have come into better balance in recent months.” Schmid continued, “(It) remains to be seen how much further interest rates will decline or where they might eventually settle.” He went on to warn against worrying about inflation from too much government spending, saying, “Large fiscal deficits will not be inflationary because the Fed will do its job. … However, that could mean persistently higher interest rates.” (A back-handed warning about too much spending and cutting of taxes.)

After the close, KEYS, LZB, QFIN, and SNEX reported beats on both the revenue and earnings lines. At the same time, ZTO missed (massively) on revenue while beating on earnings.

Overnight, Asian markets were mixed again. Shenzhen (+0.78%) and Shanghai (+0.66%) were the biggest gainers while Taiwan (-0.70%) was by far the biggest loser on the day. In Europe, with two minor exceptions, we see green across the board at midday. The CAC (+0.13%), DAX (+0.25%), and FTSE (-0.07%) lead the region higher on volume in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a modestly green start to the day. The DIA implies a +0.23% open, the SPY is implying a +0.18% open, and the QQQ implies a +0.24% open at this hour. At the same time, 10-Year bond yields are back up to 4.43% and Oil (WTI) is up 0.65% to $69.84 per barrel in early trading.

The major economic news scheduled for Wednesday is limited to EIA Weekly Crude Oil Inventories (10:30 a.m.). However, we also hear from Fed Governor Bowman at 12:15 p.m. The major earnings reports scheduled for before the open include RERE, BERY, DY, NIO, TGT, TJX, WSM, YSG, and ZIM. Then, after the close, BBAR, SQM, CPA, MMS, NVDA, PANW, and SNOW report.

In economic news later this week, on Thursday, we get Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, Philly Fed Mfg. Index, Philly Fed Mfg. Employment, October Existing Home Sales, US Leading Economic Index, and the Fed Balance Sheet. Finally, on Friday, Preliminary November S&P Global Mfg. PMI, Preliminary November S&P Global Services PMI, Preliminary November S&P Global Composite PMI, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan Consumer 1-Year Inflation Expectations, Michigan Consumer 5-Year Inflation Expectations are reported.

In terms of earnings reports later this week, on Thursday, we hear from ATKR, BIDU, BJ, ROAD, DE, IQ, BEKE, PDD, VSTS, WMG, CPRT, GAP, INTU, NTAP, ROST, and UGI. Finally, on Friday, there are no major reports scheduled.

So far this morning, RERE, DY, TJX, and ZIM all reported beats on both the revenue and earnings lines. However, NIO and TGT missed on both the top and bottom lines.

With that background, it looks like the market is indecisively positive so far this morning in the premarket. All three major index ETFs made a small gap higher to start the early session, but all three have printed Doji-like candles since that start. SPY and QQQ are above their T-line (by virtue of the gap and only barely) while DIA remains below. So, the short-term trend is indeterminant-to-bearish. Still, the mid-term and longer-term trends remain bullish. In terms of extension, none of the major index ETFs are stretched from their T-lines and the T2122 indicator is now back in center of its mid-range. So, there is plenty of room to run for either the Bulls or Bears, if either can get some momentum. In terms of the 10 Big Dogs, exactly half are in the green and the other half in the red so far this morning. NFLX (+0.69%) is leading the way for the gainers while AMZN (-0.31%) is the worst laggard. In a reversion to the way things were prior to the election, NVDA (+0.44%) is the leader in dollar-volume traded this morning, having traded about 1.5 times as much stock as TSLA (-0.18%).

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Stock futures dipped early Tuesday, influenced by rising geopolitical tensions and investor anticipation of key earnings reports from major retailers and Nvidia. The market’s cautious sentiment followed a stark warning from Russian President Vladimir Putin, who indicated a lowered threshold for nuclear weapon use under Russia’s new doctrine. This doctrine suggests that Russia might resort to nuclear weapons if faced with conventional threats that jeopardize its sovereignty or territorial integrity. Amid these tensions, traders are particularly focused on Walmart’s upcoming earnings report, expected later on Tuesday, which could provide valuable insights into consumer health and spending trends.

European markets declined on Tuesday amid renewed concerns over Russia. Most sectors and major regional bourses saw pullbacks, with the automotive sector dropping 2.1%, while utility stocks edged up by 0.2%. Additionally, the final reading of the annual euro zone inflation showed an increase from September’s 1.7% to a higher rate. Core inflation, which excludes volatile items like food, energy, alcohol, and tobacco, was reported at 2.7%. These developments reflect the market’s cautious stance in response to geopolitical tensions and inflationary pressures.

Asia-Pacific markets experienced gains on Tuesday, buoyed by Tesla’s positive impact on Wall Street the previous night and investor analysis of Chinese financial policymakers’ remarks at an investment summit in Hong Kong. Australia’s S&P/ASX 200 saw a rise of 0.89%, Japan’s Nikkei 225 closed 0.51%, South Korea’s Kospi increased by 0.12%, Hong Kong’s Hang Seng Index advanced 0.40%, and the Topix climbed 0.68%. These movements reflect a cautiously optimistic market sentiment in the region.

Economic Calendar

Earnings Calendar

Notable reports for Tuesday before the bell include AS, ENR, J, LOW, MDT, OCSL, VIK, VIPS, WB, & WMT. After the bell reports include ALC, AZEK, DLB, GBDC, KEYS, LVB, POWL, VREX, & ZTO.

News & Technicals’

Stock futures dipped early Tuesday following a stark warning from Russian President Vladimir Putin to the United States. Putin’s statement, which lowered the threshold for a nuclear strike, came shortly after reports that the Biden administration had permitted Ukraine to launch American missiles deep into Russia. According to Russia’s new doctrine, a nuclear strike would be considered if Russia or its ally Belarus faced aggression involving conventional weapons that posed a critical threat to their sovereignty or territorial integrity. The doctrine also stated that any aggression against Russia or its allies by a non-nuclear state, supported by a nuclear state, would be viewed as a joint attack.

Lowe’s exceeded third-quarter earnings and revenue expectations on Tuesday and raised its outlook, although it still anticipates a decline in full-year sales compared to the previous year. Meanwhile, its competitor Home Depot has observed that customers are postponing major projects despite the Federal Reserve’s interest rate cuts. In August, Home Depot also lowered its full-year forecast, citing anticipated weak demand for home improvement in the latter half of the year due to high interest rates. These trends highlight the ongoing challenges in the home improvement sector amid fluctuating economic conditions.

Super Micro announced on Monday that it has appointed BDO as its independent auditor. Following this news, the company’s stock, which had significantly declined since its peak in March, surged by 37% in extended trading, continuing its upward momentum from earlier in the day. Additionally, Super Micro confirmed that it will remain listed on Nasdaq, subject to the exchange’s review of its compliance plan. This development marks a positive turn for the company amid its recent challenges.

Investors are trying to focus on the WMT earnings this morning but rising geopolitical tensions and the threat on nuclear weapons use by Russia is obviously tempering bullish spirits. Of course, the highly anticipated NVDA earnings on Wednesday could quickly tip the scales of market sentiment the bulls or the bears depending on the results. That said, plan your risk carefully to avoid overtrading due to the likely volatile price action these news events may create.

Markets mostly moved sideways on the day with a little more bullish energy in the Tech sector. SPY opened up 0.08%, DIA opened down 0.08%, and QQQ gapped up 0.31%. From there, SPY and QQQ followed through to the upside until 11:45 a.m. before they gave back about a third of their post-open gains in a long, slow, mostly sideways slide that lasted the rest of the day. Meanwhile, DIA meandered sideway back and forth across its opening “gap” all day. This action gave us indecisive candles in all three major index ETFs. SPY and QQQ both printed white-bodied Spinning-Top, Bullish Harami candles that remained below their T-line (8ema) without testing. For its part, DIA printed a Doji candle that retested and failed its own T-line. This happened on well below-average volume in all three major index ETFs.

On the day, nine of the 10 sectors were green as Energy (+1.50%) and Basic Materials (+1.24%) were way out front leading the market higher. On the other side, Healthcare (-0.13%) was the only sector below break-even. At the same time, SPY gained 0.41%, DIA lost 0.07%, and QQQ gained 0.69%. VXX fell 3.65% to close at 44.89 and T2122 popped up out its oversold territory into the bottom half of its mid-range to close at 40.82. Meanwhile, 10-Year bond yields fell to 4.414% while Oil (WTI) popped 3.27% to close at $69.21 per barrel. So, Monday was a divergence day the Big Dogs of Tech, like TSLA (+5.62%), AMD (+2.99%), NFLX (+2.80%), etc., dragged the broader index ETFs higher while the mega-cap DIA lagged.

There was no major economic news scheduled for Monday.

After the close, ACM, BRBR, SYM, and TCOM reported beats on both the revenue and earnings lines. At the same time, ADM missed on revenue while coming in in-line on earnings.

Overnight, Asian markets were nearly green across the board. Only Malaysia (-0.11%) was in the red. Meanwhile, Shenzhen (+1.89%) and Taiwan (+1.34%) led the gainers. However, in Europe, we see the opposite picture with red across the board at midday. The CAC (-1.16%), DAX (-1.14%), and FTSE (-0.43%) lead the region lower in early afternoon trade. In the US, as of 7:15 a.m., Futures are pointing toward a down start to the day. DIA implies a -0.52% open, the SPY is implying a -0.27% open, and the QQQ implies a -0.14% open at this hour. At the same time, 10-Year bond yields are down to 4.373% and Oil (WTI) is down two-thirds of a percent to $68.71 per barrel in early trading.

The major economic news scheduled for Tuesday is limited to October Building Permits and October Housing Starts (both at 8:30 a.m.), and API Weekly Crude Oil Stocks report (4:30 p.m.). The major earnings reports scheduled for before the open include AS, ESLT, ENR, FUTU, LOW, MDT, VIK, VIPS, WMT, and XPEV. Then, after the close, QFIN, KEYS, LZB, SNEX, and ZTO report.

In economic news later this week, on Wednesday, EIA Weekly Crude Oil Inventories are reported. On Thursday, we get Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, Philly Fed Mfg. Index, Philly Fed Mfg. Employment, October Existing Home Sales, US Leading Economic Index, and the Fed Balance Sheet. Finally, on Friday, Preliminary November S&P Global Mfg. PMI, Preliminary November S&P Global Services PMI, Preliminary November S&P Global Composite PMI, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan Consumer 1-Year Inflation Expectations, Michigan Consumer 5-Year Inflation Expectations are reported.

In terms of earnings reports later this week, on Wednesday, RERE, BERY, DY, NIO, TGT, TJX, WSM, YSG, ZIM, BBAR, SQM, CPA, MMS, NVDA, PANW, and SNOW report. On Thursday, we hear from ATKR, BIDU, BJ, ROAD, DE, IQ, BEKE, PDD, VSTS, WMG, CPRT, GAP, INTU, NTAP, ROST, and UGI. Finally, on Friday, there are no major reports scheduled.

So far this morning, AS, ESLT, J, LOW, MDT, VIK, VIPS, and WMT have all reported beats on both the revenue and earnings lines. Meanwhile, ENR, FUTU, and XPEV missed on the revenue line while beating on earnings.

With that background, the broader markets seem be remaining indecisive relative to the last two closes. Both SPY and QQQ gapped up modestly to start the premarket, but have sold down since that point (although it is worth noting that both candles have significant lower wicks, meaning they are well up off the early session lows at this point). For its part, DIA opened the premarket modestly lower and has followed through to the downside since then, showing it is more decisively bearish. All three major index ETFs remain below their T-line (8ema), so, the short-term trend is bearish (although we don’t yet have a lower high and lower low to complete a true bear trend). Still, the mid-term and longer-term trends remain bullish. In terms of extension, none of the major index ETFs are stretched from their T-lines and the T2122 indicator is now back in its mid-range. So, there is plenty of room to run for either the Bulls or Bears, if either can get some momentum. In terms of the 10 Big Dogs, nine of the 10 are in the red this morning. GOOGL (-0.45%) is leading the way lower while NVDA (+1.57%) is holding up best. As has been the case since the election, TSLA (-0.10%) is out front leading the dollar-volume traded by about 1.5 times over NVDA.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Friday saw the market open lower. SPY gapped down 0.61%, DIA gapped down 0.40%, and QQQ plummeted 1.11% at the open. From there, all three major index ETFs sold off. DIA sold off until 12:30 p.m. and then meandered sideways along the lows the rest of the day. Meanwhile, SPY and QQQ sold until 2 p.m. before following the DIA in sideways meanders the rest of the day. This action gave us gap-down, large black-body candles in the SPY and QQQ. At the same time, DIA printed a gap-down, black-body Spinning Top candle. All three major index ETFs gapped down through and closed below their T-line (8ema). This happened on above-average volume in the QQQ and slightly below-average volume in the SPY and DIA.

On the day, seven of the 10 sectors were red as Healthcare (-2.44%) and Technology (-2.22%) way out in front, like 1.30% out in front, leading the market lower. On the other side, Utilities (+1.03%) was the far-and-away the strongest sector for the day. At the same time, SPY lost 1.28%, DIA lost 0.73%, and QQQ lost 2.38%. VXX spiked 7.15% to close at 46.59 and T2122 dropped into the top half of the oversold territory to close at 15.49. Meanwhile, 10-Year bond yields fell just a bit to 4.445% while Oil (WTI) dropped 2.55% to close at $66.95 per barrel. So, Friday was a bearish day from before the open. It continued South after the open and only found support mid-afternoon (or maybe traders just took off early for the weekend).

The major economic news scheduled for Friday included October Core Retail Sales, month-on-month, which came in lower than expected at +0.1% (compared to a forecast of +0.3% and far below September’s +1.0% value). On the headline side, October Retail Sales (month-on-month), which were stronger than expected at +0.4% (versus a forecast of +0.3% and well down from September’s +0.8% reading). At the same time, the October Export Price Index was much higher than predicted at +0.8% (compared to a forecasted -0.1% and September’s -0.6% number). On the other side, the October Import Price Index was also higher than anticipated at +0.3% (versus a forecasted -0.1% and September’s -0.4% reading). Meanwhile, the NY Empire State Mfg. Index was MUCH stronger than predicted at 31.20 (versus a -0.30 forecast and a October -11.90 value). Later, October Industrial Production was improved but down at -0.29% compared to September’s -0.73% number. Then, September Business Inventories (month-on-month) grew less than expected at +0.1% (compared to a +0.2% forecast and an August +0.3% value). Finally, September Retail Inventories increased less than predicted at +0.2% (versus a +0.3% forecast but up from August’s +0.1% number).

In Fed news, on Friday, Boston Fed President Collins warned about the risks of “technology developments.” She said, “We must all be attuned to the very real risks and challenges (of technical innovations).” Later, Collins also spoke to Bloomberg, where she said, “I certainly wouldn’t take (a rate cut in) December off the table. But again, we’re not on a preset path and so we’ll have a look carefully at the data and see what makes sense when we get to that meeting.” Later, Chicago Fed President Goolsbee told Bloomberg, “I think we are going to be looking at rates coming down over the next year along the line the dot-plot said.” He went on to indicate that he sees a quarter point cut in December and another full percentage cut in 2025. (This was a much more open and dovish stance than other Fed members, especially given the Trump inflationary tariff plans.)

Overnight, Asian markets were mixed with six or the region’s 12 exchanges in red and the other 6 in green. South Korea (+2.16%) was the biggest gainer while Shenzhen (-1.91%) paced the losses. However, in Europe, we see a much bleaker picture with 13 of that region’s 14 bourses in the red. The CAC (-0.16%), DAX (-0.26%), and FTSE (+0.06%) lead the region in early afternoon trade. In the US, as of 8 a.m., Futures are mixed on modest trading. The SIA implies -0.08% open, the SPY is implying a +0.11% open, and the QQQ implies a +0.38% open at this hour. At the same time, 10-Year bond yields are up to 4.481% and Oil (WTI) is up half a percent to $67.40 per barrel in early trading.

There is no major economic news scheduled for Monday. There are also no major earnings reports scheduled for before the open include. However, after the close, BRBR and TCOM are scheduled to report.

In economic news later this week, on Tuesday we get October Building Permits, October Housing Starts, and API Weekly Crude Oil Stocks report. Then Wednesday, EIA Weekly Crude Oil Inventories are reported. On Thursday, we get Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, Philly Fed Mfg. Index, Philly Fed Mfg. Employment, October Existing Home Sales, US Leading Economic Index, and the Fed Balance Sheet. Finally, on Friday, Preliminary November S&P Global Mfg. PMI, Preliminary November S&P Global Services PMI, Preliminary November S&P Global Composite PMI, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan Consumer 1-Year Inflation Expectations, Michigan Consumer 5-Year Inflation Expectations are reported.

In terms of earnings reports later this week, on Tuesday, we hear from AS, ESLT, ENR, FUTU, LOW, MDT, VIK, VIPS, WMT, XPEV, QFIN, KEYS, LZB, SNEX, and ZTO. Then Wednesday, RERE, BERY, DY, NIO, TGT, TJX, WSM, YSG, ZIM, BBAR, SQM, CPA, MMS, NVDA, PANW, and SNOW report. On Thursday, we hear from ATKR, BIDU, BJ, ROAD, DE, IQ, BEKE, PDD, VSTS, WMG, CPRT, GAP, INTU, NTAP, ROST, and UGI. Finally, on Friday, there are no major reports scheduled.

With that background, markets seem indecisive in a more volatile way early. The SPY and QQQ both gapped higher to start the early session, but both have printed decent-sized black candles since then, moving back toward flat. Meanwhile, DIA gapped lower to start the premarket, but has rallied back toward flat from the other side. All three remain below their T-line (8ema), so, the short-term trend has turned down. However, the mid-term and longer-term trends remain bullish. In terms of extension, none of the major index ETFs are stretched from their T-lines, but the T2122 indicator is now back in the upper part of its oversold territory. So, there is room to run for either the Bulls or Bears, if either can get some momentum. In terms of the 10 Big Dogs, seven of the 10 are in the green this morning. Again, TSLA (+5.65%) is way out front leading the gainers while NVDA (-2.65%) and NFLX (-2.05%) are far being the reset of the dogs. It is worth noting that TSLA is again the leader in terms of dollar-volume traded with 1.5 times as much money changing hands on that ticker as NVDA, which itself has traded 11 times as much as the next closest ticker.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Stock futures showed mixed results on Monday as Wall Street braced for a week of major earnings reports, following a challenging period for the three main benchmarks. Investor concerns about the trajectory of interest rates remain high, especially after Federal Reserve Chair Jerome Powell indicated on Thursday that the central bank is not in a rush to cut rates due to the economy’s robust growth and strong labor market. Currently, most investors are anticipating a year-end overnight lending rate between 4.25% and 4.50%. This week’s key market driver will be Nvidia’s earnings report, scheduled for release on Wednesday.

European markets experienced a downturn on Monday as investors shifted their focus to upcoming regional inflation data. The European Stoxx 600 index fell by 0.22%, with most major regional bourses and sectors seeing declines. Retail stocks were the hardest hit, dropping by 0.73%, while food and beverage stocks managed a modest gain of 0.29%. This week, market participants are keenly awaiting several significant data releases, including the latest U.K. inflation figures on Wednesday and the final reading of the euro zone consumer price index. Additionally, a series of purchasing managers’ index reports from various regions are scheduled for Friday.

Asia-Pacific stocks showed a mixed performance on Monday, reflecting a cautious market sentiment ahead of key economic data releases this week. In China, the loan prime rate (LPR) announcement on Wednesday is anticipated to remain unchanged, with the one-year rate at 3.1% and the five-year rate at 3.6%, according to ING. Japan is set to release its trade data on Wednesday, followed by October’s headline inflation figures on Friday, which will provide insights into the country’s economic health. Additionally, the Reserve Bank of Australia will publish the minutes from its recent meeting on Tuesday, offering further clues on the central bank’s policy direction.

Economic Calendar

Earnings Calendar

Notable reports for Monday before the bell include BRC, & TWST. After the bell reports include ACM, BRBR, & SYM.

News & Technicals’

Tencent Cloud is strategically utilizing the WeChat ecosystem to differentiate itself from other cloud service providers, according to CEO Dowson Tong. He noted that numerous Tencent clients are eager to develop their own mini programs within WeChat’s network to draw in the app’s extensive user base. This unique integration with WeChat, Tong emphasized, sets Tencent Cloud apart from many other online platforms. Meanwhile, the cloud service market is dominated by Microsoft Azure, Amazon Web Services, and Google Cloud Platform, which collectively hold 68% of the market share.

Tesla shares surged on Monday after reports emerged that President-elect Donald Trump’s transition team plans to prioritize creating a federal framework for regulating self-driving vehicles within the U.S. Transport Department. Elon Musk, a prominent advocate for Trump’s return to the White House during the recent elections, has been appointed by Trump, along with former Republican presidential candidate Vivek Ramaswamy, to head the newly established Department of Government Efficiency. This development has bolstered investor confidence in Tesla, reflecting optimism about the future regulatory environment for autonomous vehicles.

The boxing match between Jake Paul and Mike Tyson made history, with Netflix reporting that 60 million households tuned in, reaching a peak of 65 million concurrent streams. According to Most Valuable Promotions, gate receipts for the event exceeded $18 million, marking the highest revenue for a fight held outside of Las Vegas. This record-breaking event highlights the immense popularity and commercial success of the bout.

Spirit Airlines’ CEO reassured customers that they can continue booking tickets despite the company’s recent challenges. Following a failed acquisition attempt by JetBlue Airways, a significant engine recall by Pratt & Whitney, and weaker-than-expected sales, Spirit has been grappling with mounting losses. Additionally, the airline is under pressure to renegotiate $1.1 billion in debt payments due next year. Despite these hurdles, the CEO’s statement aims to maintain customer confidence and stability in the airline’s operations.

Although the earnings season is winding down, we still have some major earnings reports this week that could determine if the bulls can hold on to the upper hand or if the bears find an opening to attack. Tuesday, we get WMT and but the most anticipated will be the report from NVDA on Wednesday. This report could shake the market out of the postelection hangover we experienced last week. On the other hand if the report disappoints the bears could push to fill the index gaps below.

Markets opened mostly flat on Thursday. SPY opened up 0.02%, DIA opened 0.19% higher, and QQQ opened down 0.07%. However, after that start, all three major index ETFs slowly walked a stair-step trend lower all day long. That action gave us large, black-bodied candles in all three. SPY printed what could be called a “Bearish Trader’s Best Friend” signal (Doji followed by a gap-down large black candle). It retested its T-line (8ema) from overhead and managed to close just above the average. Meanwhile, DIA printed a Doji Continuation Pattern (two large black candles separated by a Doji in between), which is also sometimes called a Doji Sandwich. It did not quite retest its T-line. At the same time, QQQ printed a Bearish Trader’s Best Friend like SPY. QQQ also retested (from above) and passed the test of its T-line. Once again, this happened on below-average volume in all three major index ETFs.

On the day, nine of the 10 sectors were red with Healthcare (-1.74%) and Industrials (-1.48%) way out in front leading the market lower. On the other side, Energy (+0.81%) was the only sector to hang onto green territory for the day. At the same time, SPY lost 0.64%, DIA lost 0.48%, and QQQ lost 0.69%. VXX was just on the red side of flat to close at 43.48 and T2122 dropped but remains just outside of oversold territory at the bottom of its mid-range to close at 24.73. Meanwhile, 10-Year bond yields climbed again to 4.455% while Oil (WTI) was just up 0.31% to close at $68.67 per barrel. So, Thursday saw a flattish open and then an all-day tepid, step-like selloff that continued the pullback. With that said, all three major ETFs remain above their T-line (8ema) and that means the trend is bullish, if only modestly.

The major economic news scheduled for Thursday included the Weekly Initial Jobless Claims, which came in a bit better than expected at 217k (compared to a forecast of 224k and the prior week’s 221k reading). On the on-going side, Weekly Continuing Jobless Claims were also down a touch to 1,873k (versus a 1,880k forecast and the 1,884k previous week value). At the same time, October Core PPI (Month-on-Month) was up a tick as predicted at +0.3% (compared to a +0.3% forecast and the September +0.2% reading). For the headline number, the October PPI (Month-on-Month) was also up a tick as anticipated to +0.2% (versus a +0.2% forecast and +0.1% September number). Later, EIA Weekly Crude Oil Inventories showed a larger-than-expected inventory build of 2.089 million barrels (compared to a forecasted +0.400 million barrels and in-line with the previous week’s +2.149 million barrels reading). After the close, the Fed’s Balance Sheet showed a $27 billion decline from the prior week, down to $6.967 trillion.

In Fed news, on Thursday, Fed Governor Kugler told an Economist conference that the FOMC has made good progress toward both of its mandates. Kugler said, “The United States has seen considerable disinflation while experiencing a cooling but still resilient labor market.” However, she continued, “(a combination of) continued but slowing trend in disinflation and cooling labor markets means that we need to continue paying attention to both sides of our mandate.” She went on, “If inflation doesn’t retreat further it would be appropriate to pause our policy rate cuts. But if the labor market slows down suddenly, it would be appropriate to continue to gradually reduce the policy rate.” At the same time, Richmond Fed President Barkin said high union wage settlements (thinking of the BA deal) and incoming President Trump’s broad and high tariffs are among the reasons the FOMC must be cautious.

Barkin told a Real Estate Roundtable, “Being thoughtful, gradual, systemic, methodical …in terms of declaring victory…is not a bad judgment, because you may have cost pressures coming for things like wages or tariffs or whatever happens…On the other hand you can’t ignore things that are disinflationary.” Later, Fed Chair Powell said that the FOMC doesn’t need to be in a hurry to cut rates. Powell said, “The economy is not sending any signals that we need to be in a hurry to lower rates. The strength we are currently seeing in the economy gives us the ability to approach our decisions carefully.” He continued, “We know that reducing policy restraint too quickly could hinder progress on inflation. At the same time, reducing policy restraint too slowly could unduly weaken economic activity and employment.”

After the close, AMAT, GLOB, and POST all reported beats on both the revenue and earnings lines.

Overnight, Asian markets were mostly red with only four of the 12 regional exchanges above break-even. Shenzhen (-2.62%) and Shanghai (-1.45%) were by far the biggest losers while Australia (+0.74%) was far-and-away the biggest gainer. In Europe, we see a similar picture with just four of 14 bourses in the green at midday. The CAC (-0.13%), DAX (-0.11%), and FTSE (+0.07%) lead the region in mixed and modest early afternoon trade. Meanwhile, in the US, as of 7 a.m., Futures are pointing toward a down start to the day. The DIA implies a -0.41% open, the SPY is implying a -0.54% open, and the QQQ implies a -0.80% open at this hour. At the same time, 10-Year bond yields are back “down” to 4.437% and Oil (WTI) is off a third of a percent to $68.45 per barrel in early trading.

There is major economic news scheduled for Friday include October Core Retail Sales, October Retail Sales, October Export Price Index, October Import Price Index, and NY Empire State Mfg. Index (all at 8:30 a.m.), October Industrial Production (9:15 a.m.), September Business Inventories and September Retail Inventories (both at 10 a.m.). We also hear from Fed member Williams at 1:15 p.m. The major earnings reports scheduled for before the open include BABA and SPB. Then, after the close, there are no reports scheduled.

So far this morning, BABA and SPB both beat on revenue while missing on earnings. (SPB missed by more than 14% on revenue that was 4.5% higher than expected.)

With that background, the Bears seem in control of the market early. SPY and QQQ both gapped down through their T-line (8ema) to start the premarket and have printed indecisive Doji-type candles since then. At the same time, DIA opened the early session above its T-line but has sold off to be retesting that average now, being just below it but not on the premarket low. That being the case, the short-term trend has turned down or, at best, may be flat in the case of the DIA. However, the mid-term and longer-term trends remain bullish. (We would do well to remember that we are less than 2% from the all-time high in all three major index ETFs.) In terms of extension, none of the major index ETFs are stretched from their T-lines and the T2122 indicator is now back in the lower part of its mid-range. So, there is room to run for either the Bulls or Bears, if either can get some momentum. In terms of the 10 Big Dogs, nine of the 10 are in the red this morning. INTC (-0.96%) paces the losses while TSLA (+0.50%) is holding up better than the others. It is worth noting that TSLA is again the leader in terms of dollar-volume traded with 4.5 times as much money changing hands on that ticker as NVDA (-0.27%), which itself has traded 7.5 times as much as the next closest ticker. Finally, remember it’s Friday. So, prepare your account for the weekend by lightening up positions or hedging if appropriate.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

U.S. stock futures saw a slight increase as investors aimed to regain momentum that had previously driven major averages to record highs. Market participants are currently debating whether this upward trend has further potential. Key economic indicators are on the horizon, with the October producer price index set for release on Thursday and the retail sales report due on Friday. Additionally, Fed Chair Jerome Powell is scheduled to speak in Dallas, Texas, which could provide further insights into the economic outlook.

European stocks traded higher as investors assessed the latest U.S. inflation data. Despite the overall positive movement, most sectors experienced a pullback, with tech stocks falling by 1.2%. In contrast, oil and gas stocks saw a gain of 1.3%. The markets are currently focused on reversing recent declines, with significant attention on upcoming data releases and corporate earnings reports.

Asia-Pacific markets experienced a general downturn, with Hong Kong’s Hang Seng index leading the losses, dropping by over 2% by the final hour of trading. This decline extended a multi-day losing streak, resulting in a 4% loss for the week as of Wednesday’s close. Mainland China’s CSI 300 also saw a significant drop of 1.73%, while Japan’s Nikkei 225 fell by 0.48%. In contrast, Australia’s S&P/ASX 200 emerged as a rare bright spot, gaining 0.37%. South Korea’s Kospi ended nearly flat with a marginal gain, whereas the Kosdaq Index declined by 1.17%.

Economic Calendar

Earnings Calendar

Notable reports for Thursday before the bell include AAP, BILI, DIS, JD, NTES, NICE, NOMD, SBH, TLN, & ZK.

After the bell reports include AMAT, ESE, GLOB, MITK, & POST.

News & Technicals’

Disney reported its fiscal fourth-quarter earnings on Thursday, narrowly surpassing analyst estimates, driven by growth in its streaming services which bolstered the entertainment segment. The company reported adjusted earnings per share of $1.14, slightly above the expected $1.10. Revenue also exceeded expectations, coming in at $22.57 billion compared to the anticipated $22.45 billion. Net income rose to $460 million, or 25 cents per share, up from $264 million, or 14 cents per share, in the same quarter last year. However, revenue for Disney’s sports segment, primarily ESPN, remained flat, with ESPN’s profit declining by 6%.

Cisco’s latest quarterly results exceeded expectations, leading the company to raise its full-year revenue target. Despite this positive development, revenue for the quarter ended October 26 dropped by 6% to $14.7 billion compared to the previous year. Net income also declined, falling to $2.71 billion, or 68 cents per share, from $3.64 billion, or 89 cents per share, in the same quarter last year. Additionally, networking revenue saw a significant decrease of 23%, reaching $6.75 billion, which was slightly below the $6.8 billion consensus estimate by analysts surveyed by StreetAccount.

On Thursday, Treasury yields remained relatively stable as investors kept a close watch on new economic data and a series of speeches from Federal Reserve policymakers. The 10-year Treasury yield edged slightly lower to 4.449%, while the 2-year Treasury yield also dipped to 4.282%. Federal Reserve Chair Jerome Powell is set to discuss the U.S. economic outlook in Dallas, Texas, later in the day. Additionally, remarks from Fed Governor Adriana Kugler, Richmond Fed President Tom Barkin, and New York Fed President John Williams are anticipated, which could provide further insights into the economic landscape.

The bulls still want to celebrate the election working to regain momentum this morning. However, we still have a pending PPI report with a consensus estimate that suggests higher producer costs. Should the number come in hot, expect the bond yields and the dollar continue to gain strength. In that event watch for the possibility of a whipsaw. On the other hand if the number weakens expect the bullish celebration to continue with more record highs into the end of the week.

Wednesday saw the market open flattish and meander back and for the around the gap. SPY opened 0.08% higher, DIA opened 0.12% higher, and QQQ opened 0.09% lower. As mentioned, after that open, all three major index ETFs meandered back and forth below and above that initial “gap” all day. This action gave us indecisive, Spinning Top or Doji-like candles in all three, which all also remain above their T-line (8ema). This all happened on below-average volume in all three major index ETFs.

On the day, all 10 sectors were red with Basic Materials -1.79%) and Healthcare (-1.59%) out in front leading the market lower. On the other side, Technology (-0.03%) and Consumer Defensive (-0.28%) held up much better than the other sectors. At the same time, SPY lost 0.33%, DIA lost 0.82%, and QQQ lost 0.18%. VXX fell slightly to close at 44.52 and T2122 dropped all the way down into the lower half of its mid-range to close at 40.64. Meanwhile, 10-Year bond yields spiked again to 4.426% while Oil (WTI) was just on the red side of flat to close at $68.03 per barrel. So, Tuesday gave us a morning selloff followed by a more modest bounce and then a drift lower the last hour of the day. For the first time in five days, none of the major index ETFs printed a new all-time high. With that said, we still look a little toppy with all three major ETFs well above their T-line (8ema).

The major economic news scheduled for Wednesday included October Core CPI (Month-on-Month), which came in exactly as expected at +0.3% (compared to a forecast and September reading of +0.3%). On an annualized basis, October Core CPI (Year-on-Year) also came in just as expected at +3.3% (versus a forecast and September value of +3.3%). At the same time, the headline October CPI (month-on-month) was also as anticipated at +0.2% (compared to a forecast and September reading of +0.2%). On an annualized basis, October CPI (Year-on-Year) was +2.6% (versus a forecast of +2.6% and the September reading of +2.4%). Later, the October Federal Budget Balance showed a significantly higher than expected deficit of $257.0 billion (compared to the $226.4 billion forecast and far higher than the September $64.0 billion shortfall). Then, after the close, the API Weekly Crude Oil Stocks report showed a unexpected drawdown of 0.777 million barrels (versus a predicted 1-million-barrel increase and the previous week’s 3.132-million-barrel increase).

In Fed news, Minneapolis Fed President Kashkari told Bloomberg, “I’ve got confidence about that (inflation heading down toward 2%), but we need to wait.” He continued, “We’ve got another month or six weeks of data to analyze before we make any (more rate cut) decisions.” Later, St. Louis Fed President Musalem told a Memphis Economic conference that the Fed is in the “last mile” of the inflation fight and the FOMC can now afford to be deliberate. Musalem said, “In my baseline scenario, based on current information, I expect inflation to converge toward 2% over the medium term … but recent information suggests to me that the risk of inflation ceasing to converge toward 2%, or moving higher, has risen, while the risk of an unwelcome deterioration in the labor market has remained unchanged or possibly fallen.”

Meanwhile, Kansas City Fed President Schmid expressed growing confidence that inflation is headed back to 2%. Schmid said his confidence is “based in part on signs that both labor and product markets have come into better balance in recent months.” He continued, “While now is the time to begin dialing back the restrictiveness of monetary policy, it remains to be seen how much further interest rates will decline or where they might eventually settle.” Speaking about the deficit, Schmid said, “As an optimist, my hope is that productivity growth can outrun both demographics and debt … But as a central banker, I will not let my enthusiasm get ahead of the data or my commitment to the Fed’s dual mandate of price stability and full employment.” (In other words, he basically ducked the question.) At the same time, Dallas Fed President Logan said, “I anticipate the FOMC will most likely need more rate cuts to finish the journey” (meaning bringing inflation down to 2%).

After the close, BZH, CSCO, HI, SARO, and TTEK reported beats on both the revenue and earnings lines. Meanwhile, AGRO and NU missed on revenue while beating on the earnings line. On the other side, BV, GPCR, and HP beat on revenue while missing on earnings.

Overnight, Asian markets were mixed, but leaned toward the red with four exchanges above break-even and eight below-water. Shenzhen (-2.83%) Hong Kong (-1.96%), and Shanghai (-1.73%) were by far the biggest movers. In Europe, with the exception of Athens (-0.3%) we see green across the board at midday. The CAC (+1.08%), DAX (+1.32%) and FTSE (+0.40%) lead the region higher in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a modestly green start to the morning. DIA implies a +0.25% open, the SPY is implying a +0.13% open, and QQQ implies a +0.07% open at this hour. At the same time, 10-Year bond yields are up to 4.443% and Oil (WTI) is up 0.70% to $68.91 per barrel in early trading.

There is major economic news scheduled for Thursday includes Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, October Core PPI, and October PPI (all at 8:30 a.m.), EIA Weekly Crude Oil Inventories (11 a.m.), and Fed’s Balance Sheet (4:30 p.m.). We also hear from Fed Chair Powell (3 p.m.) and Fed member Williams (4:15 p.m.). The major earnings reports scheduled for before the open include AAP, AZUL, BILI, EFXT, JD, NTES, NICE, NOMD, SBH, TLN, DIS, and ZK. Then, after the close, AMAT, GLOB, and POST report.

In economic news later this week, on Friday, October Core Retail Sales, October Retail Sales, October Export Price Index, October Import Price Index, Ny Empire State Mfg. Index, October Industrial Production, September Business Inventories, September Retail Inventories are reported.

In terms of earnings reports later this week, on Friday BABA and SPB report.

So far this morning, BN, EXFT, JD, NTES, NICE, SIEGY, and have all reported beats on both the revenue and earnings lines. Meanwhile, NOMD, SBH, DIS, and ZK all missed on revenue while beating on earnings. On the other side, BILI beat on the revenue line while missing on earnings. However, AAP missed on both the top and bottom lines.

With that background, markets seem tepid to modestly bullish and perhaps trying to put in a bottom to their three-day pullback. All three major index ETFs opened the premarket slightly higher. Since that point they have put in small candles with SPY and QQQ printing small, Doji-like candles and DIA giving us a small, white, Marubozu candle. All three remain above their T-line (8ema). So, the short, mid-term, and long-term trends remain bullish. In terms of over extension, none of the SPY, DIA, or QQQ are stretched above their T-lines and the T2122 indicator is now back in the lower half of its mid-range. So, there is room to run for either the Bulls or Bears, if either can get some momentum. In terms of the 10 Big Dogs, seven of the 10 are in the green this morning. AMD (+0.99%) is the biggest price mover (on overnight news of a 4% global layoff). Meanwhile, TSLA (-0.47% on $280 million traded) is the leader in dollar-volume traded. (Again, this is the post-Trump win norm, but NVDA had been in that leader spot for 18 months prior to the election.)

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service