Tuesday morning, stock futures hover near the flatline following a pullback in the S&P 500 and Nasdaq Composite from their record highs. Nvidia shares declined after a Chinese regulator announced an investigation into the chip giant for potential antimonopoly law violations. Investors are also awaiting the National Federation of Independent Business’s small business survey, set to be released Tuesday morning. The key event this week is the U.S. consumer price index report, due on Wednesday, which could significantly impact the Federal Reserve’s decisions on interest rates at their upcoming meeting on December 17-18.

On Tuesday, European markets traded in negative territory, pulling back from the previous day’s mostly positive session. This retreat came as investors prepared for the upcoming U.S. inflation report. Basic resources stocks were the hardest hit, losing around 1% due to disappointing Chinese import and export figures. As a result, traders are now keenly anticipating the U.S. inflation data set to be released on Wednesday.

China stocks showed mixed performance amid overall gains in Asia-Pacific markets. Investor sentiment was buoyed by Beijing’s announcement of “more proactive” fiscal measures and “moderately” looser monetary policy for the upcoming year, aimed at boosting domestic consumption. The CSI 300 index in China rose by 0.74%, reflecting positive market reactions. However, Hong Kong’s market dipped slightly by 0.2%. In contrast, South Korea’s market saw significant gains, with the Kospi rising 2.43% and the small-cap Kosdaq surging by an impressive 5.52%. Meanwhile, Australia’s S&P/ASX 200 fell by 0.36%, and Japan’s Nikkei 225 increased by 0.53%.

Economic Calendar

Earnings Calendar

Notable reports for Wednesday before the bell include ASO, AZO, DBI, FERG, GIII, OLLI, & UNFI. After the bell reports include PLAY, GME, & STFX

News & Technicals’

China is expected to raise its budget deficit to the highest level in three decades and implement the deepest interest-rate cuts since 2015, following strong stimulus signals from its top leaders. Economists predict that next year’s fiscal deficit target could reach 4% of GDP, the widest since a significant tax reform in 1994. Historically, Beijing has maintained its budget deficit ratio at or below 3%. A larger fiscal deficit indicates that the government will increase borrowing to fund higher public expenditure, potentially boosting domestic demand as companies and households cut back on spending and investment.

Prosecutors in New York have charged Luigi Mangione, an Ivy League graduate, with the murder of UnitedHealthcare CEO Brian Thompson, according to court records. This charge was filed just hours after Mangione was arraigned in a Pennsylvania courtroom on gun and other charges following his arrest earlier Monday at a McDonald’s in Altoona, Pennsylvania. Mangione is accused of fatally shooting Thompson as the CEO was heading into an investor meeting for UnitedHealth Group, the parent company of his health insurance giant.

Oracle shares dropped by 7% in extended trading on Monday after the company reported fiscal second-quarter results that missed analysts’ expectations and provided a weaker-than-anticipated forecast. Despite this, Oracle announced a new agreement with Meta, enabling the social media giant to utilize its infrastructure for projects related to the Llama family of large language models. Even with the recent decline, Oracle’s stock has surged over 80% this year, on track for its best annual performance since 1999.

Tesla is facing a lawsuit from the family of Genesis Giovanni Mendoza-Martinez, who died in a 2023 collision involving a Model S sedan in Walnut Creek, California. The lawsuit claims that Tesla’s “fraudulent misrepresentation” of its Autopilot technology contributed to the crash. Mendoza-Martinez’s brother, Caleb, who was a passenger, sustained serious injuries. The family’s attorneys allege that Tesla and its CEO, Elon Musk, have exaggerated or made false claims about the Autopilot system for years to generate excitement about the company’s vehicles and improve its financial condition.

On Monday, the market started the day mostly flat. SPY opened 0.02% lower, opened 0.11% higher, and QQQ gapped down 0.19%. From there, all three major index ETFs traded sideways for about 20 minutes before selling off until 11 a.m. At that point, SPY and QQQ traded sideways until about 1:50 p.m. when they sold off into the close. DIA only differed in that it rallied from 11 a.m. to noon and then sold off the rest of the day. This action gave us large, black-bodied candles. SPY retested and closed just above its T-line (8ema). DIA retested and failed its T-line on a third down day. However, QQQ remains well above its T-line on a large, black-bodied candle with small wicks on both ends. This happened on well below-average volume in the major index ETFs.

On the day, seven of the 10 of the sectors were in the red again as Communications Services (-3.21%) plummeted and led the rest of the market (by 2%) lower. Meanwhile, Basic Materials (+0.79%) held up a half percent better than any other sector. At the same time, SPY lost 0.53%, DIA lost 0.48%, and QQQ lost 0.78%. VXX gained 2.27% to close at 42.71 and T2122 climbed up to the center of its mid-range to close at 47.27. On the bond side, 10-Year bond yields climbed to 4.197 while Oil (WTI) gained 1.38% to close at $68.13 per barrel. So, Monday gave us a mostly a nothing day where we saw a modest pullback. However, all three remain within one percent of their all-time high closes. Thus, it felt much more like a rest or pause day than the end of a Bull run.

The major economic news scheduled for Monday is limited to the New York Fed 1-Yr. Consumer Inflation Expectations survey, which came in up a tick at 3.0% (compared to an October reading of 2.9%).

In Fed news, we have started the Fed quiet period ahead of next week’s meeting. Still, it is worth noting this comment on the NY Fed 1-Year Consumer Inflation Expectations survey. The report noted, “the overall increase in one- and three-year-ahead inflation expectations masks a decline among those without a college degree and an increase among those with a college degree.” So, the less educated seem to believe the new administration policies will be less inflationary than those with more education.

After the close, MDB and TOL reported beats on both the revenue and earnings lines. Meanwhile, CASY missed on revenue while beating on earnings. However, ORCL missed on both the top and bottom lines.

Overnight, Asian markets were mixed again with six exchanges in green and six in the red. South Korea (+2.43%) rebounded from their post-martial law slump to lead gainers by almost 2% while Taiwan (-0.64%) paced the losses. In Europe, the picture is redder in color with 10 of the 14 bourses below water at midday. The CAC (-0.55%), DAX (+0.06%), and FTSE (-0.51%) lead the region lower in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a flat start to the morning. The DIA implies a -0.06% open, the SPY is implying a +0.06% open, and the QQQ implies a +0.14% open at this hour. At the same time, 10-Year bond yields have popped back up to 4.232% and Oil (WTI) is down 0.37% to $68.12 per barrel in early trading.

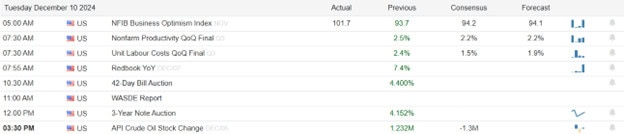

The major economic news scheduled for Tuesday include Q3 Nonfarm Productivity and Q3 Unit Labor Costs (both at 8:30 a.m.), WASDE Ag Report (noon), and the API Weekly Crude Oil Stocks report (4:30 p.m.). The major earnings reports scheduled for before the open include ASO, AZO, DBI, FERG, GIII, HEPS, OLLI, and UNFI. Then, after the close, GME reports.

In economic news later this week, on Wednesday, Nov. Core CPI, Nov. CPI, EIA Weekly Crude Oil Inventories, and the Nov. Federal Budget Balance are reported. On Thursday, we get Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, Nove. Core PPI, Nov. PPI, and the Fed Budget Balance. Finally, on Friday, Nov. Export Price Index and Nov. Import Price Index are reported.

In terms of earnings reports later this week, on Wednesday, M, REVG, ADBE, and NDSN report. On Thursday, we hear from, CIEN, AVGO, COST, and RH. There are no reports scheduled for Friday.

So far this morning, UNFI reported beats on both the revenue and earnings lines. At the same time, GIII missed on revenue while beating on earnings. However, AZO, DBI, and FERG missed on both the top and bottom lines.

With that background, stocks remain undecided in the premarket. SPY and DIA both opened the early session flat with little movement since then. (What move there has been was positive as the bulls moved SPY from slightly negative to slightly positive.) QQQ was the biggest mover, gapping down in the premarket but then immediately rallying back to just above flat. Keep in mind that the SPY, DIA, and QQQ all still sit very near all-time highs. Two of the three are also still above their T-line (8ema). So, the short-term trend is now slightly bullish. (However, to the extent we can trust TC2000 DIA data, DIA is giving me some concern coming off three straight down days and showing slightly below break-even early.) Looking further out, obviously the mid-term and longer-term trends also remain bullish sitting at or near those all-time highs. In terms of extension, none of the three major index ETFs are too stretched from their T-lines. Meanwhile, the T2122 indicator sits in the center of its mid-range. So, both sides of the market have room to move today if they can find momentum. In terms of the 10 Big Dogs, eight of the 10 are in green numbers at this point of the morning. GOOGL (+3.70%) is by far the leader in terms of price move. However, TSLA (+0.94%) is the leader in dollar-volume traded (albeit on a very light trading morning) sitting at a about 1.5 times as much traded than NVDA (-0.14%), which itself has traded almost twice as much as the next one of the big dogs.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Markets diverged Friday after a modest start. SPY opened 0.15% higher, DIA opened 0.16% higher, and QQQ opened up 0.13%. However, at that point QQQ rallied sharply the first 50 minutes before trading sideways with just a slight bullish trend the rest of the day. For its part, after its open, DIA immediately began a long slow 5-hour selloff before ending the day trading sideways in a very tight range along the lows. Meanwhile SPY was somewhere between the other two major index ETFs, grinding sideways all day after its open. This action gave us a white-bodied Spinning Top in the SPY, that delivered a new all-time high and new all-time high close. At the same time, DIA printed a big-bodied, black candle that crossed back below its T-line (8ema). Finally, QQQ printed a large, white-bodied candle that also delivered a new all-time high and new all-time high close.

On the day, seven of the 10 of the sectors were in the red as Energy (-1.99%) was far out front leading the pack lower. On the other side, Consumer Cyclical (+1.21%) was by far the strongest sector. At the same time, SPY gained 0.19%, DIA lost 0.34%, and QQQ gained 0.89%. VXX fell mor than 1.5% to close at 41.76 and T2122 dropped into the lower half of its mid-range to close at 33.33. Meanwhile, 10-Year bond yields fell again to 4.149 while Oil (WTI) dropped 1.65% to close at $67.17 per barrel. So, Friday saw some divergence in the market that is sitting at or near all-time highs. Thursday was basically a day of consolidation. That was the first such day in a while for SPY and QQQ, but a continuation of a consolidation process that has lasted 1.5 weeks in DIA. This all happened on well below-average volume in the SPY, well-below-average volume in the DIA, and average volume in the QQQ.

The major economic news scheduled for Friday included Month-on-Month November Average Hourly Earnings, which was a tick stronger than expected at +0.4% (versus a forecast of +0.3% but in-line with October’s +0.4% reading). On an annualized basis, November Average Hourly Earnings were also a tick higher than expected at +4.0% (compared to a 3.9% forecast but in-line with the +4.0% October value). At the same time, Nov. Nonfarm Payrolls were considerably stronger than predicted at +227k (versus a +202k forecast an +36k October reading). On the private side, Nov. Private Nonfarm Payrolls were also significantly higher than anticipated at +194k (compared to a +160k forecast and far stronger than October’s -2k number). The Nov. Participation Rate fell two ticks to 62.5% (versus a 62.7% forecast and even down from October’s 62.6% reading). Altogether, this led to a Nov. Unemployment Rate that was 4.2% (compared to a 4.2% forecast but up a tick from October’s 4.1%). Later, Michigan Consumer Sentiment was up to 74.0 (versus a 73.1 forecast and November’s 71.8 reading). At the same time, Michigan Consumer Expectations came in down quite a bit to 71.6 (compared to November’s 76.9). Looking further out, Michigan 1-Year Inflation Expectations were up two ticks to 2.9% (versus a 2.7% forecast and much higher than November’s 2.6% survey result). In the longer-term, Michigan 5-Year Inflation Expectations were 3.1% (compared to a 3.1% forecast and down a tick from the 3.2% November value). Later, October Consumer Credit was sharply higher at $19.24 billion (versus a $10.10 billion forecast and September’s $3.21 billion number).

In Fed news, on Friday, Fed Governor Bowman (the most hawkish voter) said she is worried about inflation. Bowman said, “I continue to see greater risks to the price stability side of our mandate, especially when the labor market continues to be near full employment.” She continued, “We’ve seen progress in lowering inflation but that progress seems to have stalled this year.” So, she concluded, “I would prefer that we proceed cautiously and gradually in lowering the policy rate, as inflation remains elevated.” Later, new (as of August) Cleveland Fed President Hammack said, “I believe we are at or near the point where it makes sense to slow the pace of rate reductions.” Hammack continued, “Moving slowly will allow us to calibrate policy to the appropriately restrictive level over time given the underlying strength in the economy.” Meanwhile, the more dovish Chicago Fed President Goolsbee said “I’m hopeful that conditions continue to evolve such that we can get in close to the (neutral, neither restrictive or expansionary rate) range.” (Goolsbee would not specifically answer on what he felt was a neutral rate, but he did say it was “around 3%” (which is 1.5%- 1.75% below the current Fed rate.)

Overnight, Asian markets were mixed but leaned toward the red side. South Korea (-2.78%) paced the losses (by 2%) after their President survived an impeachment after his failed martial law and arrests of opposition. Hong Kong (+2.76%) led the gaining exchanges by 2.5%. In Europe, the picture is much greener with 10 of the 14 bourses above break-even at midday. The CAC (+0.61%), DAX (-0.04%), and FTSE (+0.50%) lead the region higher in early afternoon trade. Meanwhile, in the US, Futures are pointing toward a mixed and slightly down start to the day. The DIA implies a +0.04% open, the SPY is implying a -0.03% open, and the QQQ implies a -0.17% open at this hour. At the same time, 10-Year bond yields set at 4.18% and Oil (WTI) is up 1.34% to $68.10 in early trading.

The major economic news scheduled for Monday is limited to the NY Fed 1-Year Consumer Inflation Expectations survey (9 a.m.). There are no major earnings reports scheduled for before the open. Then, after the close, CASY, MDB, ORCL, and TOL report.

In economic news later this week, on Tuesday we get Q3 Nonfarm Productivity, Q3 Unit Labor Costs, WASDE Ag Report, and API Weekly Crude Oil Stocks report. Then Wednesday, Nov. Core CPI, Nov. CPI, EIA Weekly Crude Oil Inventories, and the Nov. Federal Budget Balance are reported. On Thursday, we get Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, Nove. Core PPI, Nov. PPI, and the Fed Budget Balance. Finally, on Friday, Nov. Export Price Index and Nov. Import Price Index are reported.

In terms of earnings reports later this week, on Tuesday we hear from ASO, AZO, DBI, FERG, GIII, HEPS, OLLI, UNFI, and GME. Then Wednesday, M, REVG, ADBE, and NDSN report. On Thursday, we hear from, CIEN, AVGO, COST, and RH. There are no reports scheduled for Friday.

With that background, market is looking undecided in the premarket. All three major index ETFs opened the early session slightly higher, but have printed small black-body candles with more with than body so far. They all three remain close to flat. Keep in mind that the SPY, DIA, and QQQ all still sit very near all-time highs. Two of the three are also still above their T-line (8ema). So, the short-term trend is now slightly bullish. Looking further out, obviously the mid-term and longer-term trends also remain bullish sitting at or near those all-time highs. In terms of extension, QQQ is again getting a bit stretched above its T-line, but the other two are close enough. Meanwhile, the T2122 indicator is in the bottom half of its mid-range. So, both sides of the market have room to move today if they can find momentum. In terms of the 10 Big Dogs, seven of the 10 are in red numbers at this point of the morning. NVDA (-1.86%) and AMD (-1.67%) are 1.25% in front of other losers as China threatens an anti-monopoly investigation. At the same time, TSLA (+2.18%) is a full 2% ahead of the other two very modest gainers in early trading. TLSA is also leading in terms of dollar-volume traded, sitting at a about 1.5 times as much traded than NVDA, which itself has traded almost 6.5 times as much as the next one of the big dogs.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

U.S. stock futures edged lower on Monday following a strong performance by the S&P 500 and Nasdaq Composite, produced three winning weeks in a row. This cautious start to the week comes ahead of key inflation data set to be released, which will provide crucial insight into the Federal Reserve’s upcoming policy decisions. The November jobs report, which showed stronger-than-expected growth, has already influenced market sentiment. With the Fed in a blackout period before its policy-setting meeting, investors are keenly awaiting the November consumer price index (CPI) data due on Wednesday. Economists surveyed by Dow Jones anticipate a slight increase in pricing pressures, with expected monthly and yearly rises of 0.3% and 2.7%, respectively, up from the previous month’s 0.2% and 2.6%.

European markets opened the week with mixed results as investors navigated ongoing geopolitical turmoil. Major regional bourses pared back most of their earlier gains, though European luxury stocks saw a boost, with Gucci-owner Kering rising as much as 4% at one point. The market’s attention was also focused on the Middle East, where the recent ousting of Syrian President Bashar al-Assad by rebel forces has created uncertainty. Western leaders have responded cautiously to the overthrow, concerned about the potential for a power vacuum and increased instability in the region.

China’s recent announcement of “more proactive” fiscal measures and “moderately” looser monetary policy aimed at boosting domestic consumption had mixed effects on regional markets. Before the news, mainland China’s CSI 300 index saw a slight decline of 0.17%, while Hong Kong’s Hang Seng index surged nearly 3%. In South Korea, political turmoil following President Yoon Suk Yeol’s survival of an impeachment vote and the aftermath of his brief martial law declaration led to significant market drops. The Kospi index fell by 2.78%, and the small-cap Kosdaq plummeted 5.19% to 627.01 as investors remained cautious. Meanwhile, Japan’s Nikkei 225 experienced a modest increase of 0.18%, and Australia’s S&P/ASX 200 ended the day with marginal gains.

Economic Calendar

Earnings Calendar

Notable reports for Wednesday before the bell include MOMO. After the bell reports include BRZE, AI, CASY, MDB, ORCL, PHR, MTN, TOL, YEXT.

News & Technicals’

Since Donald Trump became president-elect, nearly $10 billion has flowed into U.S. exchange-traded funds (ETFs) that invest directly in Bitcoin. This surge, totaling about $9.9 billion in net inflows, reflects investor optimism that Trump’s favorable stance on the crypto sector will drive market growth. Major issuers like BlackRock Inc. and Fidelity Investments have been key beneficiaries of this trend. Additionally, Trump’s recent appointments of a digital-asset supporter as the head of the U.S. securities regulator and the first-ever White House czar for artificial intelligence and crypto have further fueled expectations of a booming crypto market.

On Monday, the 10-year U.S. Treasury yield inched up by approximately 1 basis point to 4.17%, as investors evaluated the potential impact of recent jobs data on the Federal Reserve’s upcoming interest rate decision. Similarly, the 2-year Treasury yield rose by 1 basis point to 4.11%. This slight increase comes after a dip last week. Investors are now turning their attention to key economic indicators due later this week, including fresh inflation data on Wednesday and the latest producer price index on Thursday. Additionally, business confidence and mortgage data releases are expected, although no major data points are scheduled for Monday.

President-elect Donald Trump has stated that he does not intend to replace Federal Reserve Chair Jerome Powell, whose term extends until May 2026. In an interview at Trump Tower, Trump responded to a question about Powell’s potential replacement by saying, “No, I don’t think so. I don’t see it.” He added that while Powell might comply if directly told to step down, he would likely resist if merely asked. This exchange highlights the ongoing dialogue about the Federal Reserve’s leadership as Trump prepares to take office.

Over the weekend, significant political upheavals occurred globally: Syria’s President Bashar Al-Assad reportedly fled to Russia, ending 50 years of Assad family rule; South Korea’s president survived an impeachment vote after declaring martial law for the first time in over 40 years; and France’s government collapsed following a no-confidence vote, a first in over 60 years. These events could cast a shadow over the typical year-end market rally, which usually sees markets climb. The full impact of these political developments remains uncertain, contributing to market volatility. However, positive U.S. economic data supports the case for a market rise. Traders are optimistic that the U.S. Federal Reserve will act as the market’s “Santa Claus” this year, with an 85% chance of a 25 basis points rate cut next week, according to the CME FedWatch tool, which is likely to boost markets.

Markets started off flat Thursday with DIA having the biggest move at the open. SPY and QQQ both opened less than 0.01% lower while DIA “gapped” down 0.10%. From there, both SPY and QQQ meandered sideways, re-crossing their opening level several times. Then about 1 p.m. both started a slide to the downside that lasted the rest of the day. For its part, DIA rallied after the open, reaching the high if the say at 10 a.m., and then starting a long, slow selloff that lasted the entire day. This action gave us black-bodied candles with upper wicks in all three major index ETFs. SPY and QQQ printed Bearish Harami candles, while DIA just gave us a big black candle. All three remain above their T-line (and did not ever retest that average on the day). This all happened on well below-average volume.

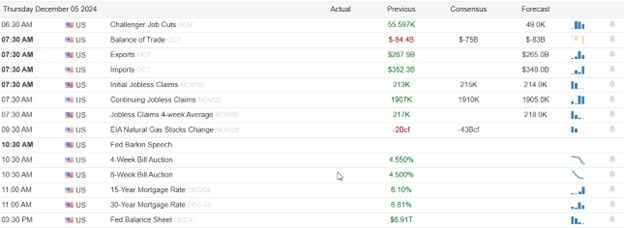

On the day, five of the 10 of the sectors were in the red and the other five in the green as Healthcare (-1.03%) was the biggest mover and led the way lower. On the other side, Consumer Defensive (+0.56%) led a far more tightly-packed group of positive sectors. At the same time, SPY lost 0.16%, DIA lost 0.50%, and QQQ lost 0.28%. VXX rose just a tad to close at 42.42 and T2122 dropped back right into the center of its mid-range to close at 53.44. Meanwhile, 10-Year bond yields fell just slightly to 4.18% while Oil (WTI) was just on the red side of flat, closing at $68.52 per barrel. So, Thursday was basically a day of consolidation. That was the first such day in a while for SPY and QQQ, but a continuation of a consolidation process that has lasted 1.5 weeks in DIA.

The major economic news scheduled for Thursday included Weekly Initial Jobless Claims, which came in higher than expected at 224k (compared to a forecast and previous week’s value of 215k). In terms of ongoing claims, Weekly Continuing Jobless Claims were well down at 1,871k (versus a forecast of 1,910k and the prior week’s reading of 1,896k). At the same time, Oct. Imports were down to $339.60 billion (compared to the September $352.30 billion number). Meanwhile, Oct. Exports were only down a touch to $265.70 billion (versus September’s $267.90 billion). Together, this gave us an Oct. Trade Balance that was down to $73.80 billion (compared to a forecasted $75.70 billion and September’s $83.80 billion reading). Later, after the close, the Fed Balance Sheet showed a $9 billion decrease for the week, falling from $6.905 trillion to $6.896 trillion.

In Fed news, on Thursday, there were no Fed speakers of note. However, the New York Fed released a study that shows tariffs during Trump’s first term hurt stock values and reduced business sales, profits, and employment. The report said, “most firms suffered large valuation losses on tariff-announcement days. We also document that these financial losses translated into future reductions in profits, employment, sales, and labor productivity.” The report continued, “because global supply chains are complex and foreign countries retaliate … Our results show that firms experienced large losses in expected cash flows and real outcomes. These losses were broad-based, with firms exposed to China experiencing the largest losses.” (The report makes no comment on Trump’s newly threatened 25% tariffs on Mexico and Canada or 10% tariff on Chinese goods. It also makes no mention of the tariffs in the last four years of the Biden Administration.)

After the close, DOCU, HPE, LULU, WOOF, ULTA, VEEV, and VSCO all reported beats on both the revenue and earnings lines. Meanwhile, COO missed on revenue while beating on earnings.

Overnight, Asian markets leaned toward the red side with eight of the 12 exchanges below break-even. That said, China had a good day with Hong Kong (+1.56%), Shenzhen (+1.48%) and Shanghai (+1.05%) making the biggest moves in the region. Japan (-0.77%), Singapore (-0.69%) and New Zealand (-0.68%) paced the losses. In Europe, we see a mixed picture taking shape at midday with seven of the 14 bourses above break-even. The CAC (+1.32%), DAX (+0.16%), and FTSE (-0.12%) lead the region in mixed early afternoon trade. In the US, as of 7:15 a.m., Futures are pointing toward an open just on the red side of flat again. The DIA implies a -0.08% open, the SPY is implying a =0.09% open, and the QQQ implies a -0.03% open at this hour. At the same time, 10-Year Bond yields are down slightly to 4.178% and Oil (WTI) is off 1.04% to $67.59 per barrel in early trading.

The major economic news scheduled for Friday we get Nov. Average Hourly Earnings, Nov. Nonfarm Payrolls, Nov. Private Nonfarm Payrolls, Nov. Participation Rate, Nov. Unemployment Rate, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-Year Inflation Expectations, Michigan 5-Year Inflation Expectations, October Consumer Credit. We also hear from Fed members Bowman and Daily. The major earnings reports scheduled for before the open are limited to DOOO and GCO. Then, after the close, there are no major reports scheduled.

With that background, market is again undecided early in the premarket session. All three major index ETFs opened close to flat and have printed very small candles with wicks on both ends up to this point of the early session. Keep in mind that the SPY, DIA, and QQQ all sit very near all-time highs. All three are also still above their T-line (8ema). So, the short-term trend is now bullish. Looking further out, obviously the mid-term and longer-term trends also remain bullish sitting at or near those all-time highs. In terms of extension, yesterday’s consolidation gave the T-line a chance to make up ground on the QQQ. So, none of the big three are too far stretched from their 8ema. The T2122 indicator ais also back in the very center of its mid-range. So, both sides of the market have room to move today if they can find momentum. In terms of the 10 Big Dogs, five of the 10 are in green numbers at this point of the morning while the other five show red. GOOGL (-0.16%) is leading a tightly packed group in modest losses. On the other side, TSLA (+1.34%) is way, way out front (by a full percent) pacing the gainers. TLSA is also leading in terms of dollar-volume traded, sitting at a about 2.5 times as much traded than NVDA (-0.12%), which itself has traded almost 4 times as much as the next one of the big dogs. Finally, remember its Friday. Prepare your account for the weekend news cycles and don’t forget to take profits. (It is payday after all.)

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Wednesday was pretty much all about the open. SPY gapped up 0.30%, DIA gapped up 0.45%, and QQQ gapped up 0.66%. From there, all three major index ETFs did some form of grinding sideways until 2 p.m. At that point, all three started a steady, but modest, rally that ran into the close. This action gave us gap-up, large-body, white body candles in all three major index ETFs. All three printed new all-time highs and closed at new all-time high closes. This happened on below-average volume in SPY and QQQ as well as average volume in the DIA.

On the day, six of the 10 of the sectors were in the red again and the other four in the green as Energy (-1.90%) was way, way out in front leading the majority of sectors to the downside. On the other side, Technology (+1.67%) far ahead of any other sector. Meanwhile, SPY gained 0.62%, DIA lost 0.68%, and QQQ gained 1.24%. VXX gained half a percent to close at 42.33 and T2122 dropped back a little more, but remains in the top part of the mid-range to close at 64.03. At the same time, 10-Year bond yields fell to 4.184% while Oil (WTI) dropped 1.73%, closing at $68.73 per barrel. What we saw Wednesday saw gaps higher across the market. That was followed by a sideways grind most of the day and then a modest rally into the close. All three major index ETFs printed new all-time highs and closed at new all-time high closes. So, the Bulls were clearly in control…even if most of the gain came on the opening gap higher.

The major economic news scheduled Wednesday included November ADP Nonfarm Employment Change, which came in with lower growth than expected at +146k (versus a +166k forecast and October’s +184k reading). Later, Nov. S&P Global Services PMI also came in light at 56.1 (compared to a 57.0 forecast, but up from October’s 55.0 value). When combined with Tuesday’s Nov. S&P Global Mfg. PMI this gave us a Nov. S&P Global Composite PMI of 54.9 (versus a 55.3 forecast, but up from October’s 54.1 number). Later, Oct. Factory Orders were lighter than predicted at +0.2% (compared to a +0.3% forecast but up significantly from September’s -0.2% reading). At the same time, Nov. ISM Non-Mfg. Employment Index was down to 51.5 (versus a 53.0 forecast and October value). Meanwhile, the Nov. ISM Non-Mfg. PMI itself was also low at 52.1 (compared to a 55.5 forecast and October’s 56.0 number). Later, EIA Weekly Crude Oil Inventories showed a much bigger drawdown than anticipated at -5.073 million barrels (versus a forecasted draw of 1.600 million barrels and the previous week’s -1.844 million barrels).

In Fed news, on Wednesday, St. Louis Fed President Musalem told Bloomberg that he expected “additional easing of moderately restrictive policy toward neutral will be appropriate over time.” However, he hedged his bets on how much or how fast, saying, “Along this baseline path, it seems important to maintain policy optionality, and the time may be approaching to consider slowing the pace of interest rate reductions, or pausing, to carefully assess the current economic environment, incoming information and evolving outlook.” Later, Fed Chair Powell told an interview, “We can afford to be a little more cautious as we as we try to find neutral rate.” Powell continued, “The economy is stronger than we thought it was going to be in September … the labor market is is better, and inflation is coming a little higher.” After his speech, Powell was asked about being undermined by a “Shadow Fed Chairman” (an idea broached by Trump’s nominated Treasury Sec.). Powell said, “I don’t think that’s on the table at all … There’s a set of institutional relationships between the Fed and every administration … I fully expect that we’ll have the same general kinds of relationships (with Trump Admin. officials). There’s got to be trust and mutual respect and acknowledgement of the different authorities and boundaries that we have.”

After the close, FIVE, PVH, and SNPS reported beats on both revenue and earnings lines. Meanwhile, AEO missed on revenue while beating on earnings. On the other side, GEF beat on revenue while missing on earnings.

Overnight, Asian markets were mostly green with just three of the 12 exchanges below the break-even level. India (+0.98%) paced the gains while Hong Kong (-0.92%) and South Korea (-0.90%) were by far the biggest losers. In Europe, we see a similar picture taking shape at midday with just four of 14 bourses in the red. The CAC (+0.12%), DAX (+0.31%), and FTSE (-0.08%) lead the region modestly higher in early afternoon trade. In the US, as of 7:40 a.m., Futures are pointing toward a start just on the red side of flat. The DIA implies a -0.02% open, the SPY is implying a -0.05% open, and the QQQ implies a -0.06% open at this hour. At the same time, 10-Year Bond yields are back up a touch to 4.217% and Oil (WTI) is back up a quarter-percent to $68.67 (after an overnight slump) in early trading.

The major economic news scheduled for Thursday includes Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, Oct. Imports, Oct. Exports, Oct. Trade Balance (all at 8:30 a.m.), and Fed Balance Sheet (4:30 p.m.). The major earnings reports scheduled for before the open are limited to BMO, BF.A, CAL, CM, CSIQ, DG, GMS, KFY, KR, PDCO, SAIC, SIG, and TD. Then, after the close, COO, DOCU, HPE, LULU, WOOF, ULTA, VEEV, and VSCO report.

In economic news later this week, on Friday, we get, Nov. Average Hourly Earnings, Nov. Nonfarm Payrolls, Nov. Private Nonfarm Payrolls, Nov. Participation Rate, Nov. Unemployment Rate, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-Year Inflation Expectations, Michigan 5-Year Inflation Expectations, October Consumer Credit. We also hear from Fed members Bowman and Daily.

In terms of earnings reports later this week, on Friday, we hear from DOOO and GCO.

So far this morning, CM, KFY, and SAIC reported beats on both the revenue and earnings lines. Meanwhile, CSIQ missed on revenue while beating on earnings. On the other side, BMO, DG, GMS, PDCO, and TD all beat on revenue while missing on the earnings line. However, CAL and SIG missed on both the top and bottom lines.

With that background, markets seem undecided early in the premarket. All three major index ETFs are just on the red side of flat. QQQ started the early session with a gap down, but has rallied to print a white-bodied candle to get nearly back to even. Keep in mind that the SPY, DIA, and QQQ sit at all-time highs. All three are above their T-line (8ema). So, the short-term trend is now bullish. Looking further out, obviously the mid-term and longer-term trends also remain bullish sitting at or near those all-time highs. In terms of extension, only QQQ is now stretched above its T-line, but SPY and DIA are still not extended. The T2122 indicator remains in the top half of its mid-range. So, both sides of the market have room to move, but the Bears may have more slack to work with today. In terms of the 10 Big Dogs, nine of the 10 are in green numbers at this point of the morning again, albeit on modest moves. GOOGL (+0.44%) is leading the way higher while AMD (-0.22%) is the only big dog in the red. In a return to post-election norm, TLSA (+0.39%) is leading in terms of dollar-volume traded, sitting at a little less than 1.5 times as much traded than NVDA (+0.10%), which itself has traded almost 9 times as much as the next one of the big dogs.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

This morning, US equity futures experienced fluctuations as investors took a breather from a record-breaking rally. Despite this pause, Bitcoin surged past $100,000 following President-elect Donald Trump’s appointment of a crypto advocate as the next head of the Securities and Exchange Commission. The S&P 500 marked its 56th record close of 2024, with the Dow and QQQ also reaching new highs, largely driven by gains in big tech. Federal Reserve Chairman Jerome Powell noted that the risks from the labor market had diminished, allowing Fed officials to cautiously lower interest rates toward a neutral level that neither stimulates nor restrains economic growth.

European stocks saw an uptick, particularly in France, following the ousting of Prime Minister Michel Barnier’s government in a no-confidence vote the previous day. The market’s positive movement was driven by gains in travel and banking stocks, although industrials and health care sectors experienced minor losses. In a significant development, Shell and Norway’s Equinor announced their intention to merge their British offshore oil and gas assets, forming a new energy company based in Aberdeen, Scotland. This merger is poised to make the new entity the largest independent producer in the U.K. North Sea.

Asia-Pacific markets showed mixed performance amid significant political upheaval. In South Korea, lawmakers moved to impeach President Yoon Suk Yeol just a day after he declared martial law, with a vote scheduled for Saturday evening, according to local reports. This political instability contributed to a 0.90% drop in the Kospi and a 0.92% decline in the Kosdaq. Meanwhile, Australia’s S&P/ASX 200 saw a modest gain of 0.1%, Japan’s Nikkei 225 rose by 0.30%, but Hong Kong’s Hang Seng index fell by 1.1%.

Economic Calendar

Earnings Calendar

Notable reports for Wednesday before the bell include CRMT, BMO, BF>B, CAL, CM, DG, GMS, SIG, & TD, After the bell reports include AGX, ASAN, COO, DOCU, COMO, GTLB, GWRE, HCP, HPE, LULU, WOOF, RBBK, IWT, SMAR, SWBI, PATH, ULTA, VEEV, VSCO, & ZIMZ.

News & Technicals’

Wednesday night, Bitcoin’s price surged past the highly anticipated $100,000 mark for the first time ever. This milestone followed new closing records for the S&P 500 and Nasdaq Composite, coinciding with President-elect Trump’s announcement of his SEC chair pick and Fed Chair Jerome Powell’s comparison of Bitcoin to gold. Bitcoin has now risen over 140% in 2024 and 48% since the election. Mike Novogratz, CEO of Galaxy Digital, remarked to CNBC that the digital asset ecosystem is on the verge of becoming a mainstream financial force.

American Eagle has revised its full-year sales forecast downward and provided holiday guidance that fell short of expectations. While the retailer experienced robust demand during the back-to-school season, it noted a slowdown in consumer spending between key shopping periods. Despite this, the Aerie brand continued to perform well, with comparable sales increasing by 5%, building on a 12% rise from the previous year.

Shell and Equinor are set to establish a joint venture in Aberdeen, Scotland, aiming to sustain fossil fuel production and ensure energy security in the U.K. The deal, expected to be finalized by the end of next year pending approvals, will create the U.K. North Sea’s largest independent producer. This strategic move underscores the companies’ commitment to maintaining a stable energy supply while navigating the evolving energy landscape.

Vivek Ramaswamy, co-leading President-elect Trump’s new Department of Government Efficiency alongside Elon Musk, announced that any “last minute spending spree” under Biden’s Inflation Reduction Act (IRA) or CHIPS Act will be closely scrutinized. He specifically mentioned the recent $6.6 billion loan to electric vehicle maker Rivian Automotive. Ramaswamy emphasized that any significant increase in spending and “dollars out the door” during the final days of Biden’s term could be considered “indefensible” and potentially a “fiduciary breach.”

After yesterday’s record-breaking rally futures hint at a possible rest as the bulls catch their breath. However, the index charts all indicate bullish patterns with no signs that the bears gaining ground. That said, the decline in the T2122, T2108, T2107 indicators as the market extends is suggesting a substantial divergence is developing. Should the bears find a reason to attack the divergence could result in a swift and substantial pullback so have a plan in pace to protect capital and profits if those profit-takers find reason to run for the door.

Tuesday saw a modest divergence at the opening bell. SPY opened 0.04% lower, DIA opened 0.10% higher, and QQQ gapped down 0.27%. From there, SPY and QQQ just meandered sideways in a tight channel before making a modest and slow afternoon rally. QQQ printed a new all-time high and new all-time high close. SPY printed a new all-time high close. At the same time, after its lower open, DIA followed-through to the downside until 11:45 a.m. Then it rallied almost back to the prior close level before meandering sideways the rest of the day. This action gave us Spinning Top candles in the SPY and DIA as well as a large-body white candle. SPY was a white-body Spinning Top and DIA was a black-body Spinning Top. This all happened on well below-average volume in all three major index ETFs.

On the day, six of the 10 of the sectors were in the red again and the other four in the green as Utilities (-0.78%) was out in front pacing the losses and leading the market to the downside. On the other side, Communications Services (+0.60%) led the gainers. Meanwhile, SPY gained 0.05%, DIA lost 0.19%, and QQQ gained 0.31%. VXX fell half a percent to close at 42.07 and T2122 dropped back a little more, but remains in the top part of the mid-range to close at 69.79. At the same time, 10-Year bond yields rose a bit to 4.226% while Oil (WTI) popped 2.76%, closing at $69.98 per barrel. So, what we saw Tuesday was basically consolidation by the SPY and DIA (even though SPY did print a new all-time high close). However, QQQ continued its rally despite a gap down to start the day. META (+3.51%), AMZN (+1.30%), AAPL (+1.28%), and NVDA (+1.18%) led that rally in the QQQ.

The major economic news scheduled for Tuesday was limited to October JOLTs which came in higher than expected at 7.744 million (compared to a 7.510 million forecast and a September 7.372 million reading). Then, after the close, the API Weekly Crude Oil Stock Report showed an unexpected inventory build of 1.232 million barrels (versus a forecasted 2.060-million-barrel drawdown and the prior week’s 5.935-million-barrel drawdown).

In Fed news, on Tuesday, FOMC members steered away from providing rate guidance ahead of December’s meeting. San Francisco Fed President Daly told Fox Business “I think we need to have an open mind here.” Later, Chicago Fed President Goolsbee said, “Over the next year it feels to me like rates come down a fair amount from where they are now, but we meet every six weeks because the conditions change.” For her part, Fed Governor Kugler simply gave backward-looking comments to a Detroit event, saying, “I view the economy as being in a good position after making significant progress in recent years toward our dual-mandate goals of maximum employment and stable prices.”

After the close, PSTG, OKTA, and MRVL reported beats on both the revenue and earnings lines. Meanwhile, CRM beat on revenue while missing on earnings.

Overnight, Asian markets were mixed with six exchanges in the red, five in the green, and one unchanged. South Korea (-1.44%) paced the losses, as expected given the political turmoil of the last 24 hours in that country. Meanwhile, Taiwan (+0.99%) led the gainers. In Europe, the bourses are mostly green at midday with four in the red and 10 in the green. The CAC (+0.52%), DAX (+1.05%, and FTSE (-0.23%) lead the region higher in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a green start to the day. The DIA implies a +0.42% open, the SPY is implying a +0.30% open, and the QQQ implies a +0.64% open at this hour. At the same time, 10-Year Bond yields are up to 4.261% and Oil (WTI) is just on the green side of flat at $70.00 per barrel in early trading.

The major economic news scheduled for Wednesday includes Nov. ADP Nonfarm Employment Change, Nov. S&P Global Services PMI, Nov. S&P Global Composite PMI, Oct. Factory Orders, Nov. ISM Non-Mfg. Employment, Nov. ISM Non-Mfg. PMI, EIA Crude Oil Inventories, and Fed Beige Book. We also hear from Fed Chair Powell. The major earnings reports scheduled for before the open are limited to CPB, CHWY, CBRL, DLTR, FL, HRL, RY, and THO. Then, after the close, AEO, FIVE, GEF, PVH, and SNPS.

In economic news later this week, on Thursday, Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, Oct. Imports, Oct. Exports, Oct. Trade Balance, and Fed Balance Sheet. Finally, on Friday, we get, Nov. Average Hourly Earnings, Nov. Nonfarm Payrolls, Nov. Private Nonfarm Payrolls, Nov. Participation Rate, Nov. Unemployment Rate, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-Year Inflation Expectations, Michigan 5-Year Inflation Expectations, October Consumer Credit. We also hear from Fed members Bowman and Daily.

In terms of earnings reports later this week, on Thursday, BMO, BF.A, CAL, CM, CSIQ, DG, GMS, KFY, KR, PDCO, SAIC, SIG, TD, COO, DOCU, HPE, LULU, WOOF, ULTA, VEEV, and VSCO report. Finally, on Friday, we hear from DOOO and GCO.

So far this morning, CPB, DLTR, and RY reported beats on both the revenue and earnings lines. Meanwhile, CHWY beat on revenue while missing on earnings. However, FL, HRL, and THO missed on both the top and bottom lines.

With that background, markets seem bullish early in the day. All three major index ETFs gapped up a bit to start the premarket and all three have printed small white-bodied candles since that point. However, it is worth noting all three have backed off just slightly from their absolute high of the early session. In addition, keep in mind that the SPY and QQQ sit at all-time highs while DIA is less than half a percent below its own all-time high. All three are above their T-line (8ema). So, the short-term trend is now bullish. Looking further out, obviously the mid-term and longer-term trends also remain bullish sitting at or near those all-time highs. In terms of extension, QQQ is now stretched above its T-line, but SPY and DIA are still not too far extended. The T2122 indicator is now back in the top half of its mid-range. So, either side has room to move, but the Bears may have more slack to work with today. In terms of the 10 Big Dogs, nine of the 10 are in green numbers at this point of the early morning session. NVDA (+1.16%) is leading the way higher while META (-0.27%) is the only big dog in the red and by far the laggard of the group. In a return to pre-election norm, NVDA is leading in terms of dollar-volume traded, sitting at a little less than 1.5 times as much traded than TSLA, which itself has traded almost 4 times as much as the next one of the big dogs.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service