October Unemployment Data This AM

The major indices gapped down at the open Thursday (about 1% in the SPY and QQQ and about two-thirds of a percent in the DIA). At that point, the large-cap indices started a sideways rollercoaster action with a slightly bullish trend. Meanwhile, the QQQ gave us a move dead sideways and a more volatile rollercoaster ride. The DIA had managed to fade the morning gap by 12:20 pm and continued to bob around the level of that previous close the rest of the way. However, the SPY remained in the gap and the QQQ bobbed around its opening level, not even attempting to fill the gap until the final 30 minutes. This all ended with a strong selloff in the last 20 minutes of the day across all 3 major indices. This action gave us indecisive, gap-down, Spinning Top candles in the SPY and DIA with the QQQ tending more toward a gap-down, black Inverted Hammer candle. It is worth noting that the QQQ is now VERY extended from its T-line.

On the day, six of the ten sectors were in the red with Technology (-2.05%) leading the way lower and Energy (+1.53%) lagging the move. Meanwhile, SPY fell 1.02%, DIA fell 0.45%, and QQQ fell 1.95%. It’s worth noting that the SPY and QQQ did this on average volume while the SPY did not quite reach average. Elsewhere, the VXX was down 2.23% to 17.54 and T2122 remained in the mid-range at 43.83. 10-year bond yields rose to 4.149% and Oil (WTI) was down 2.14% to $88.06/barrel. So, the market was still scared of the Fed at the open but quickly became undecided. Meanwhile, the heavier volume (relative to average) in the DIA indicates money continues to flee to the safety of mega-caps.

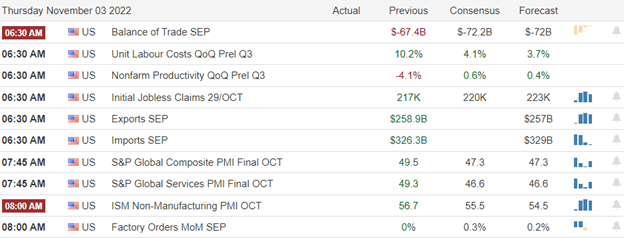

In economic news, September Exports came in a little over a $1 billion less than the prior month while Sept. Imports came in $4.8 billion above the prior month. The net September Trade Balance was larger than expected at -$73.30 billion (compared to the forecast $72.20 billion). Weekly Initial Jobless Claims were lower than expected at 217k (versus the forecast of 220k and last week’s 218k number). Q3 Nonfarm Productivity was up, but up less than expected at +0.3% (compared to the forecast of +0.6% but at least far better than Q2’s number of -4.1%). Q3 Unit Labor Costs were up less than expected at +3.5% (versus +4.1% forecast and Q2’s reading of +8.9%). October PMI came in better than expected at 47.8 (versus the 46.6 forecast but worse than the Sept. reading of 49.3). However, September Factory Orders came in as expected at +0.3%, which was slightly better than the prior month’s +0.2%. Finally, October ISM Non-Mfg. PMI came in below expectation at 54.4 (versus a forecast of 55.5 and the September reading of 56.7).

SNAP Case Study | Actual Trade

In stock news, TEVA agreed to pay $523 million to the state of NY to settle opioid lawsuits. Elsewhere, LYFT confirmed it is cutting its staff by 13% (6883 employees). In addition, BA announced the launch of its first crewed Starliner capsule to carry humans has slipped to 2023. Meanwhile, AMZN announced they are pausing all new corporate hiring. At the same time, STLA is urging owners of 286,000 2005-2010 Chrysler cars after airbag deployment deaths. ERIC subsidiary Vonage has agreed to pay $100 million to the FTC to settle a lawsuit over failing to provide a simple method for customers to cancel and imposing “junk” fees. After the close, GIS announced they are following suit with GM and pausing advertising on Twitter. Finally, Bloomberg reports AXL has drawn takeover interest from BWA and DANA as well as British firm Melrose Industries.

In miscellaneous news, early Thursday, the Bank of England raised interest rates by the most since 1989 by following the US in doing a 0.75% rate hike. Back on this side of the pond, the SEC and DOJ announced they are launching probes into company executives gaming the “pre-arranged stock sales” system to do insider trading. SIEN acknowledged it has been subpoenaed related to CEO trading and in September CMCM CEO and Former President were both charged with insider trading using the 10b5-1 prearranged sale trading plans. The government is expanding the investigation to other companies. In Canada, the government cut its 2023 GDP forecast to +0.7%, but also cut its deficit forecast by 30% and said that the Canadian economy would narrowly avoid recession.

After the close, AMGN, PYPL, RGA, DXC, SQ, ED, LYV, CTVA, MSI, BECN, MELI, AEE, MCHP, SWKS, ILMN, TKC, VTR, MTD, IHRT, FND, OTEX, TWLO, DBX, EXAS, CTRA, SVC, ED, ATSG, AMN, TS, and CVCO all reported beats on the top and bottom lines. Meanwhile, SBUX, HVRRY, MNST, GDDY, CNXN, COLD, ZEUS, AL, MTZ, KWR, TDS, and WBD all reported misses on revenue while beating on earnings. On the other side, EOG, RKT, EXPE, CWK, OPEN, DASH, USM, CE, LFG.A, FRG, TEAM, AGL, SEM, and USX all reported beats on revenue while missing on earnings. Unfortunately, CVNA, COIN, AVB, and NVST all missed on both the revenue and earnings lines.

So far this morning, CAH, AES, ADNT, HSY, LAMR, ASIX, and CNK have all reported beats on the revenue and earnings lines. Meanwhile, ITOCY, PBR, TEF, HUN, EVRG, AMCX, and TIXT all missed on revenue while beating on earnings. On the other side, DUK, QRTEA, IEP, and NFG all beat on revenue while missing on earnings. Unfortunately, MGA, FLR, SYNH, GTN, and AMRX all missed on both the top and bottom lines. It is worth noting that SYNH and GTN both lowered their forward guidance. However, PNM raised its forward guidance.

Overnight, Asian markets were very strongly green, with the sole exception of Japan (-1.68%). Hong Kong (+5.36%), Shenzhen (+3.20%), and Shanghai (+2.43%) led the region higher again on rumors the Chinese government would move away from its “Zero Covid” lockdown strategy. (Oddly, these rumors come as China reported its highest number of new cases in more than six months.) In Europe, we see a similar picture at midday with only Portugal (-0.41%) in the red. The FTSE (+1.38%), DAX (+1.76%), and CAC (+2.26%) are all strongly green on a very broad-based rally that sees none of the other exchanges up less than one-half of one percent in early afternoon trading. As of 7:30, Futures are pointing toward a green start to the day in the US as well. The DIA implies a +0.62% open, the SPY is implying a +0.80% open, and the QQQ implies a +0.85% open ahead of data. 10-year bond yields are up again at 4.163% and Oil (WTI) is surging up 3.5% to $91.28/barrel in early trading.

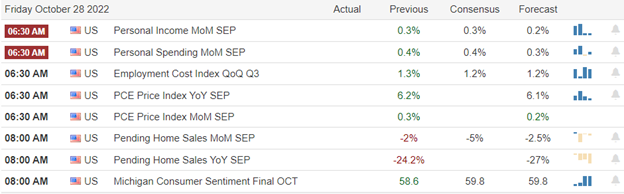

The major economic news events scheduled for Friday include Avg. Hourly Earnings, Oct. Nonfarm Payrolls, Oct. Participation Rate, and Oct. Unemployment Rate (all at 8:30 am). We also have a Fed speaker (Rosengren at 10 am). The major earnings reports scheduled for the day include ADNT, AES, AMCX, AXL, AMRX, BEP, CAH, CNK, D, DUK, ENB, EOG, EVRG, FLR, GTES, GLP, HSY, HUN, IEP, KOP, LAMR, LSXMA, MGA, PBR, PPL, SYNH, TEF, TIXT, and VST before the open. There are no major reported scheduled for after the close.

As markets wait on the October Employment data this morning, the rest of the world seems to be buoyed by the hope that the second-largest economy (China) may open up by loosening covid restrictions and lockdowns. That may be the case, but so far there is no official word of such a policy shift and that country is at a six-month high in terms of new covid cases. (Moreover, the Chinese vaccine is ineffective against the now dominant Omicron variants meaning the only tools that government has available are lockdowns or “let it go and hope unrest over mass deaths does not get bad before you reach herd immunity.” The point is, despite market hopes, and rumors, I would not bet money based on just hopium. On this side of the world, all the news seems to revolve around the now-private TWTR. It seems Musk has begun laying off up to half of the company staff and has already been sued for doing so without providing advanced notice.

With that background and as we wait on the employment data, it is clear the bullish trend is broken and the premarket bounce would still have a long way to go to print a Morning Star-type signal in any of the 3 major indices. Extention from the T-line (8ema) is only a factor in the beleaguered QQQ at this point. However, T2122 says we have room to run since we are still in the mid-range. Once again, be very careful about chasing these morning gaps. This is not only a very bearish market, but also very volatile. Any move higher could “rip your face off” by reversing hard. So, strongly consider letting the panic settle out before taking any new trades. Emotions will kill a trader! Control your FOMO and your fear in general. I promise you, there will be plenty of money to make after the knee-jerks ease up. Also, remember that this is Friday…with a long weekend news cycle to get through before we can adjust or close any trades.

This morning, I am reminded of Warren Buffet’s first rule of making a lot of money in the market: “Do not lose a lot of money in the market” (and his second rule is “remember rule #1”). So, be deliberate and disciplined, but don’t be stubborn. Remember that it is 100 times more important to avoid big mistakes than it is to pick big winners. If you have a loss, admit you were wrong and take the loss before it gets out of hand. And when price does move in your direction, always move your stops in your favor and take a little profit off the table. (You have to remember the “Legend of the man in the green bathrobe“…in that situation, it is NOT HOUSE MONEY you’re betting, it’s all OUR MONEY!). Finally, trading is not your hobby. It’s a job. The money is real. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. I know the Powerball is huge right now, but give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service