GM and MCD Beat as Fed Watch Starts

Markets gapped down Monday (0.73% in the SPY, 0.34% in the DIA, and down 1.21% in the QQQ). All three major indices rallied for 45 minutes but then began a selloff that lasted the rest of the day. We closed very close to the lows. This action gave us gap-down black-bodied candles with upper wicks. It would be possible to call the SPY and DIA Inverted Hammer candles, with both of them sitting on the T-line (8ema). The DIA is also sitting on its 50sma again after the session. This all happened on average volume in the SPY and QQQ while DIA had lower-than-average volume.

On the day, nine of the 10 sectors are in the red as Technology (-2.02%) leading the way lower and Communications Services (+0.03%) holding up better than the other sectors. At the same time, the SPY was down 1.25%, the DIA was down 0.75%, and QQQ was down 2.02%. Meanwhile, the VXX was up 2.48% to 11.56 and T2122 dropped out of the overbought territory to 76.04. 10-year bond yields were up to 3.542% and Oil (WTI) was down almost 2.5% to $77.81 per barrel. So, on the day, we saw a gap-down bearish candle that closed near the lows.

In stock news, SNY has fired all employees at two vaccine manufacturing plants in India after the company failed to win a UNICEF contract. At the same time, Reuters reported that CFG cut back on auto lending last year and now plans to further reduce its exposure to this segment of the business as a risk management move. The plan is to reduce the auto loan portfolio to $5 or $6 billion (from a $14.5 billion peak). A bit later in the day, UL announced a new CEO (former Heinz exec) Hein Schumacher. Meanwhile, F announced they are cutting prices on their “Mustang Mach-E” by as much as $5,900. This follows the lead of TSLA and is the harbinger of an EV price war according to industry analysts. Not to be outdone, TSLA also announced it is now offering more new discounts and added feature incentives to entice buyers. Elsewhere, Reuters reported that BA will be adding a third production line for 737 Max planes in mid-2024. In union news, 8,200 UAL Teamster members have ratified a new two-year contract. Then, after the close, JBLU pilots also approved a two-year contract extension.

SNAP Case Study | Actual Trade

In stock legal and regulatory news, a US court has rejected the JNJ attempt to offload liability from tens of thousands of talc product lawsuits via the Chapter 11 Bankruptcy of its healthcare subsidiary. Meanwhile, in Philly, the US Third District Court of Appeals has ruled that drug manufacturers can limit healthcare providers use of outside pharmacies for dispensing drugs under a federal discount program. The ruling is a win for SNY, NVO, and AZN. At the same time, the NHTSA has hit VLVLY (Volvo) with a $130 million civil penalty after an investigation found the company failed to recall defective vehicles in a timely fashion.

In energy news, Natural Gas dropped another 6% Monday, falling to nearly a two-year low at $2.646/mmBtu. This is despite forecasts calling for East Coast temperatures below freezing this week (and nearing 10 degrees Friday). Meanwhile, Oil (WTI) fell almost 2.5% as analysts are expecting a Wednesday rate hike, which should make the Dollar stronger and therefore lower commodity prices. Another factor is that despite the European ban and the G-7 price cap, oil analysts say Russian exports remain strong.

In miscellaneous news, Bloomberg reported that last week was the first week where more than 50% of workers returned to the office across all major US cities. Meanwhile, US Treasury Sec. Yellen told an interview Monday that “persistently low inflation” is likely to return as a long-term challenge for the economy once the pandemic-era distortions are worked out. Finally, both the US and Germany said they will not be supplying fighter jets to Ukraine. However, according to LMT announced the US will continue to supply the planes to European countries (who in-turn may supply the F-16s to Ukraine). For example, Poland said Monday it was willing to supply F-16s in coordination with other European allies.

After the close, SANM, ARE, GGG, HP, and CADE all posted beats on the revenue and earnings lines. Meanwhile, WHR and PFG both missed on the revenue line while beating one the earnings line. On the other side, NXPI and WWD both beat on revenue while missing on earnings. It is worth noting that WHR and SANM both raised their forward guidance.

Overnight, Asian markets were red across the board with the sole exception of India (+0.07%) which clung to the green. Meanwhile, Taiwan (-1.48%), Hong Kong (-1.03%), and South Korea (-1.00%) led the region down. In Europe, markets are mixed but lean heavily to the downside at midday. The FTSE (-0.85%), DAX (-0.56%), and CAC (-0.53%) lead the region lower while only Russia (+0.33%) is appreciably in the green in early afternoon trade. As of 7:30 am, US Futures are pointing to a down start to the day. The DIA implies a -0.27% open, the SPY is implying a -0.30% open, and the QQQ implies a -0.44% open at this hour. At the same time, 10-year bond yields are down to 3.523% and Oil (WTI) is off 1.16% to $76.99/barrel in early trading.

So far this morning, MPC, GM, UBS, MCD, IP, PHM, GLW, DOV, AOS, LII, ST, KEX, and MSCI have all reported beats on both the revenue and earnings lines. Meanwhile, XOM, UPS, PFE, PII, MCO, and PNR missed on revenue while beating on earnings. On the other side, PSX, CAT, MPLX, OSK, and MDC all beat on revenue while missing on earnings. Unfortunately, SPOT missed on both the top and bottom lines. It is worth noting that GM, SPOT, PII, and DOV all raised their forward guidance. However, UPS, PFE, GLW, and OSK all lowered their forward guidance.

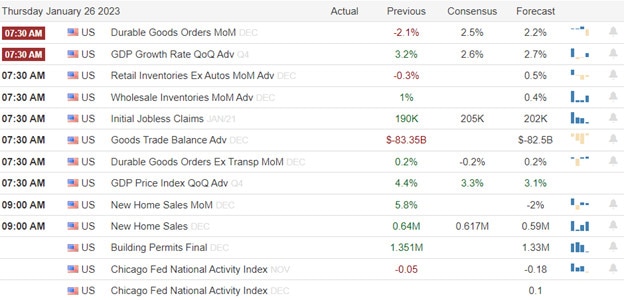

The major economic news events scheduled for Tuesday we get Q4 Employment Cost Index (8:30 am), Chicago PMI (9:45 am), Conference Board Consumer Confidence (10 am), and the API Weekly Crude Oil Stocks Report (4:30 pm). Major earnings reports scheduled for the day include AOS, CAT, GLW, DOV, XOM, GM, HUBB, IMO, IP, KEX, LII, MDC, MAN, MPC, MCD, MCO, MPLX, MSCI, NYCB, OSK, PNR, PFE, PSX, PBI, PII, PHM, ST, SPOT, SYY, UBS, and UPS before the opening bell. Then, after the close, AMD, DOX, AMGN, ASH, BXP, CP, CENT, CENTA, CB, EW, EA, HA, HLI, JNPR, MTCH, MDLZ, OI, RNR, SNAP, SYK, SMCI, UNM, and WDC report.

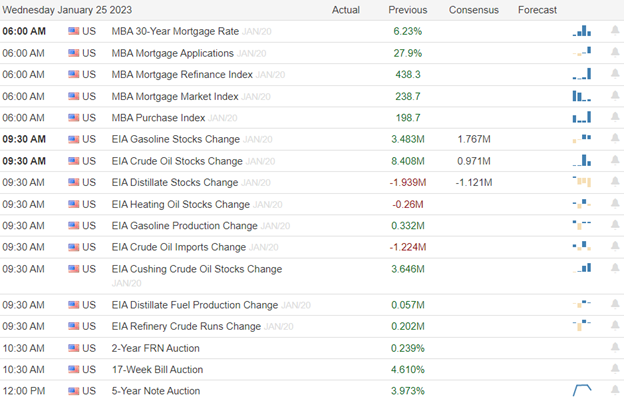

In economic news later in the week, on Wednesday, ADP January Nonfarm Employment Change, Jan. Mfg. PMI, ISM Mfg. PMI, Dec. JOLTs, EIA Crude Oil Inventories, the FOMC Rate Decision, FOMC Statement, and FED Chair Press Conference are reported. On Thursday, we get Weekly Initial Jobless Claims, Q4 Nonfarm Productivity, Q4 Unit Labor Costs, and December Factory Orders. Finally, on Friday, Jan Avg. Hourly Earnings, Jan. Nonfarm Payrolls, Jan. Participation Rate, Jan. Unemployment Rate, Services PMI, and ISM Non-Mfg. PMI are reported.

In terms of earnings later this week, on Wednesday, we hear from MO, ABC, ATKR, BSX, EAT, GIB, EPD, EVR, FTV, GSK, HUM, IEX, JCI, MHO, NVS, ODFL, OTIS, PTON, SMG, SR, TMUS, TMO, WRK, WM, AFL, ALGN, ALGT, ALL, AFG, AVT, BHE, CHRW, CCS, CTVA, DXC, ENVA, GL, THG, HOLX, LSTR, LFUS, MCK, MTH, META, MET, MAA, MOD, MUSA, QRVO, RRX, TTEK, and VSTO. On Thursday, FLWS, ABB, WMS, APD, ALFVY, ATI, AME, APTV, ARCO, ARW, ABG, AVY, BALL, BCE, BCX, BERY, BMY, BR, BIP, BC, CAH, CMS, CNHI, COP, DB, LLY, EL, RACE, FCFS, HBI, HOG, HSY, HON, ITW, ICE, LANC, LAZ, LEA, MMP, MKL, MRK, NJR, PH, PENN, DGX, RCI, SBH, SNDR, SIRI, SNA, SONY, SWK, TT, GWW, WNC, WEC, GOOGL, AMZN, AAPL, TEAM, BSMX, BZH, BYD, CVCO, CRUS, CLX, CTSH, COLM, DECK, F, GEN, GILD, GOOG, HIG, HUBG, KMPR, LPLA, MEOH, MCHP, MTX, OTEX, POST, QCOM, RGA, SIGI, SKX, SKYW, SBUX, and X report. Finally, Friday, we hear from AON, ARCB, AVTR, SAN, BSAC, BBU, BEPC, BEP, CBOE, CHD, CI, LYB, MOG.A, NFG, REGN, SAIA, SNY, and ZBH.

The main talk on financial news this morning is the fact GM blew away expectations. The company also told wall street it is expecting a stronger year in 2023 than industry analysts had been predicting. This would seem to bolster the idea of a consumer stronger than we thought in Q4 and perhaps a soft landing this year. Still, at the same time, MCD also easily beat expectations on both lines. They cited increased business in what it thinks is a sign of inflation-wary consumers opting for fast food rather than fine dining. Of course, that would point to a consumer under pressure.

With that background, it looks like all three major indices are retesting their T-line (8ema) for support during the premarket. DIA is also retesting its 50sma and the QQQ is falling further from its 200sma (which failed as support on Monday). The trend is still bullish in the QQQ and SPY. Meanwhile, the sideways meander inside a wedge continues in the DIA. Even though more than 99% of futures bets are expecting a 0.25% rate hike (i.e. the market is certain it knows what the FOMC will do), do not be surprised if we drift on lower volumes today and early on Wednesday. (There isn’t much advantage to be had “doubling down,” even when you are sure you know what will happen when everybody else in the market believes the same thing.)

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: No Trade Ideas today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service