With the deadline drawing near the rhetoric and political gobblygook woke up the bears on Friday as bond yields continue to rise adding pressure to a stressed regional banking sector. Despite the bearish move, no technical damage occurred in the indexes. This the market faces some big economic reports, lots of political wrangling over the debt ceiling, and few market-moving earnings reports. That said, we could experience some big point moves in the market and I would not rule out substantial head fakes and whipsaws to keep traders and investors guessing.

Asian markets traded mostly higher overnight after China leave loan rates unchanged with the tech-heavy HSI leaning the way up 1.17% at the close. However, European markets are taking a more cautious approach this morning as they monitor the debt ceiling negotiations trading slightly bearish this morning. With a light day of earnings and a morning filled with Fed speakers, U.S. futures suggest a flat open to begin another week as we wait and hope for a deal out of Congress and some potential market-moving economic report later this week.

Economic Calendar

Earnings Calendar

Although earnings season is winding down we will still have some substantial market-moving reports over the week. Notable reports for Monday include GLBE, HEI, NDSN, & ZM.

News & Technicals’

The leaders of the Group of Seven (G7), an intergovernmental organization of wealthy Western nations have issued a joint statement that signals their intention to balance their economic ties with China and their security concerns over its actions. The statement says: “We are not decoupling or turning inwards. At the same time, we recognize that economic resilience requires de-risking and diversifying.” This follows the remarks of U.S. Treasury Secretary Janet Yellen, who urged the G7 countries to cooperate in addressing the challenges posed by China at a meeting earlier this month. Some analysts, such as Goldman Sachs economists Hui Shan and Andrew Tilton, expect more measures to come from the G7, especially with the Committee on Foreign Investment in the United States (CFIUS), a body that reviews foreign investments for national security risks.

Meta, the parent company of Facebook, has been hit with a record-breaking fine by the European Data Protection Board (EDPB) for violating the privacy rights of its EU users. The EDPB, which oversees the implementation of the General Data Protection Regulation (GDPR) in the bloc, has ordered Meta to pay 1.2 billion euros ($1.3 billion) for transferring EU user data to the U.S. without adequate safeguards. The EDPB has also given Meta five months to stop any future data transfers to the U.S. and six months to cease processing any EU user data that was previously transferred in breach of GDPR. Meta said it would appeal the decision and the fine, claiming that it was “singled out” and that the ruling “sets a dangerous precedent” for other companies.

Rising bond yields added pressure to the already stressed regional banking sector and the political gamesmanship on the debt ceiling woke up the bears on Friday. However, other than some possible bearish candle patterns no technical damage was created. According to Goldman’s report, the CTA”s are maxed out but that doesn’t necessarily mean selling in the market if corporate buy-backs and retail continue to buy. But, beware, if the profit-taking begins the sell side could quickly gain some momentum so be prepared. With more political wrangling, some big economic reports, Fed speak, and a few random market-moving earnings reports throughout the week the potential for big price swings traders will have to stay on their toes and be ready for just about anything.

Friday saw a very modest gap higher (up 0.24% in the SPY, down 0.03% in the DIA, and up 0.06% in the QQQ). This led to a sideways grind until 11 am in all three major indices. However, at that point we saw a sharp selloff across the board for 40 minutes. From that point, the rest of the day saw an undulating sideways move the entire rest of the day in all three indices. This action gave us indecisive, black-bodied Spinning Top candles in the QQQ, SPY, and DIA (although the DIA body was admittedly larger than the other two indices). The DIA also closed just below its T-line (8ema) while the other two major indices remain comfortably above their own. This all happened on average volume in the DIA and less-than-average volume in the SPY and QQQ.

On the day, seven of the 10 sectors were in the red with Consumer Cyclical (-1.15%) leading the way lower as Healthcare (+0.64%) held up better than the other sectors. At the same time, the SPY lost 0.15%, DIA lost 0.23%, and QQQ lost 0.56%. VXX gained 2.5% to 35.77 and T2122 dropped back to the center of the mid-range at 56.95. 10-year bond yields spiked up to 3.682% while Oil (WTI) fell a quarter of a percent to end the day at $71.67 per barrel. So, Friday saw an intraday whipsaw that really amounted to an indecisive stalemate between the bulls and bears with the Bears having just a bit of the upper hand on the strength of a 40-minute mid-day selloff.

The only economic news Friday was talking. On the Fed front, Gov. Bowman again pleaded the case on behalf of banks. She criticized the Fed for using the collapse of SIVB, SBNY, and FRC as a “pretext” for considering what she termed “radical reform of the bank regulatory framework…as opposed to targeted changes to address identified root causes of banking stress.” She went on to say the new regulation being considered is simply “incompatible with the fundamental strength of the banking system.” At the same time, NY Fed President Williams told a conference that he refuses to tie Fed policy to his recently published research that shows major global economies are still fundamentally in a low-interest rate world. Later, Fed Chair Powell spoke and said that recent banking system troubles (causing tighter credit conditions) mean that “our policy rate may not need to rise as much as it would have otherwise to achieve our goals.” He went on to give what Bloomberg called a clear signal he is open to pausing interest rate increases next month. Powell said, “We’ve come a long way in policy tightening and the stance of policy is restrictive and we face uncertainty about the lagged effects of our tightening so far and about the extent of credit tightening from recent banking stresses … Having come this far we can afford to look at the data and the evolving outlook to make careful assessments.”

In other talking news Friday, Treasury Sec. Yellen told bank CEOs that more bank mergers may be necessary. Specifically, she told Reuters “Pressures on U.S. regional bank earnings may lead to more concentration in the sector and regulators will likely be open to such mergers.” Elsewhere, the proximate cause of the mid-day slump in markets was that GOP negotiators walked out of the Debt Ceiling talks. However, on Friday evening (once the GOP had made their headlines), they returned to the table and negotiations resumed after a six-hour pause. Progress was reported over the weekend and another meeting between President Biden and Speaker McCarthy is scheduled for today after a call from the President (from Airforce One) to McCarthy which the Speaker called “productive.” At this point, it definitely seems like an agreement is a done deal but the two sides will wrestle for political points until the last minute. So, be prepared for news from the Monday meeting (likely bad news to stoke fear).

In stock news, the Wall Street Journal reported Friday that Samsung (which has a little over 27% of smartphone market share) has decided it will not change its default search engine from GOOGL to the MSFT Bing engine. The company had been considering a switch for a couple of months. (GOOGL earns $3 billion per year from its contract with Samsung, in addition to ad revenue.) Meanwhile, CTLT slashed its forecast and again delayed the release of its quarterly results (the third postponement) after replacing several financial directors and naming a new CFO last month. At the same time, Reuters reports that META will release a text-based app to compete with Twitter in June. The news outlet reports META is already testing the service with influencers and content creators. Elsewhere, the CEO of MS announced he will step down sometime in the next 12 months. In the auto industry, TSLA began offering more discounts ($1,300 this time) on some Model 3 cars in the US and even heavier discounts in Europe. Finally, in a funny story, the Wall Street Journal reported Friday that AAPL has issued an internal edict to employees forbidding them from using ChatGPT. This is interesting because it comes less than a day after AAPL announced they are offering a ChatGPT app for iPhones and less than a week since the company hinted that it is working on its own AI offering (when it touted the fact it has been designing AI chips for years). So, AI is good as a product to sell…just not good enough a product for “us” to use.

In stock legal and regulatory news, a driver for startup Revel is suing TSLA over a crash at the end of January. The driver claims his TSLA “suddenly and automatically” took accelerated, forcing the driver to need to crash the vehicle in order to get it to stop. Elsewhere, EU antitrust regulators questioned MSFT competitors about the type of data their contracts with MSFT require them to turn over. The watchdog asked if MSFT may have used the required data to go directly to the competitors’ customers. In somewhat related news, the same EU antitrust agency finalized its record fine of META (reported here last week) to be a whopping $1.3 billion for transferring EU customer data from European to US servers. Later, the US FDA approved a KRYS gene therapy used to treat skin disorders. At the end of the day, the US Forest Service told a federal court it is not sure when it would be able to approve a land swap that would allow RIO and BHP to develop a new copper mine in AZ. (Native American groups have opposed the swap and mine.) The Biden Administration (Bureau of Land Mgmt.) on Friday issued a decision supporting a $6.6 billion pipeline proposed by ETRN. (Earlier last week, Energy Sec. Granholm also had backed the pipeline.) Meanwhile, a US judge ruled Friday that AAL must end its alliance with JBLU in a victory for the Biden Administration which had claimed their agreement would reduce competition and raise consumer prices. Finally, the Wall Street Journal reports that the NHTSA is making an official demand and will take legal action against ARCW after the company refused the agency’s request that it recall 67 million airbag inflators after nine of them exploded during deployment, killing two people. While ARCW has been defiant, GM proactively recalled all vehicles with those inflators. However, this recall would cut across F, TM, STLA, VLKAF (Volkswagen), and HYMLF (Hyunda/Kia) and could threaten ARCW solvency.

Overnight, Asian markets leaned heavily toward the green side, with only three of the region’s exchanges in the red. New Zealand (-0.88%) saw the worst of the losses as Hong Kong (+1.17%), Thailand (+0.95%), and Japan (+0.90%) led the region higher. Meanwhile, in Europe, the bourses are leaning the opposite direction at midday. The CAC (-0.35%), DAX (-0.33%), and FTSE (flat) lead the region lower with two notable exceptions (Greece +7.06% and Denmark +1.23%) in early afternoon trade. (Greece skyrocketed as its ruling conservative party won the most seats in the Greek election and will now enter talks with other smaller parties about forming a government.) In the US, as of 7:30 am, Futures are pointing to a start just on the red side of flat. The DIA implies a -0.07% open, the SPY is implying a -0.10% open, and the QQQ implies a -0.15% open at this hour. At the same time, 10-year bond yields are down 3.663% and Oil (WTI) is just on the green side of flat at $71.58/barrel.

The major economic news events scheduled for Monday are limited to just three Fed speakers (Bullard at 8:30 am, Barking at 10:50 am, and Bostic at 10:50 am). The major earnings reports scheduled for the day are limited to RYAAY and ZIM before the open. Then, after the close, HEI, NDSN, and ZM report

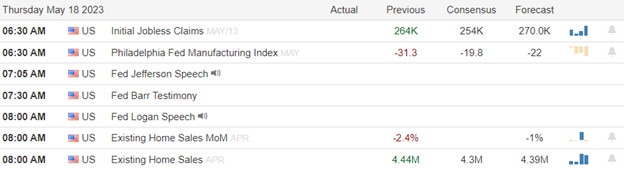

In economic news later this week, on Tuesday we get Building Permits, Preliminary May Mfg. PMI, Preliminary May S&P Global Composite PMI, Preliminary May Services PMI, April New Home Sales, and API Weekly Crude Stocks Report. Then Wednesday, EIA Weekly Crude Oil Inventories, FOMC May Minutes, and Treasury Sec. Yellen speaking are on tap. On Thursday, we get Preliminary Q1 GDP, Preliminary Q1 GDP Price Index, Weekly Initial Jobless Claims, April Pending Home Sales, the Fed Balance Sheet, and Bank Reserve Balances with the Fed. Finally, on Friday, April Durable Goods Orders, April Goods Trade Balance, Aprile PCE Price Index, April Personal Spending, April Retail Inventories, and Michigan Consumer Sentiment are reported.

In terms of earnings reports later this week, on Tuesday, we hear from AZO, BJ, DKS, HIS, LOW, VIPS, WSM, A, INTU, PANW, TOL, URBN, and VFC. Then Wednesday, ANF, ADI, BMO, BNS, DY, KSS, WOOF, XPEV, UHAL, AEO, ENS, PLUS, GES, MOD, NVDA, SNOW, and SPLK report. On Thursday, we hear from AMWD, BBY, BURL, CM, DLTR, GCO, HEPS, MDT, NTES, RL, RY, TD, TITN, ADSK, COST, DECK, GPS, MRVL, RH, ULTA, and WDAY. Finally, on Friday, BIG, BAH, and HIBB report.

So far this morning, RYAAY beat on both the revenue and earnings line. Meanwhile, ZIM missed on both the top and bottom lines.

In miscellaneous news, after the close Friday, the Fed reported that deposits at US banks edged lower on the week ending May 10, falling to $17.10 trillion (from $17.16 trillion the week prior). At the same time, the Fed reported that bank-provided credit fell from $17.37 trillion to $17.32 trillion. Meanwhile, at the G-7 Summit, President Biden changed course and approved the transfer of F-16 fighter-bomber jets (from US allies, not the US directly) to Ukraine. The US will provide Ukrainian pilot training on the jets after having already trained two for the purposes of determining what topics would need to be covered and to what extent. LMT and GD make the F-16 and it is now being speculated that orders will be placed to replace the jets given to Ukraine by US allies. (The most recent sale of F16s averaged a price of $350 million per jet after add-ons, accessories, and spare parts were figured in…$4.21 billion for 12 jets in 2022.) The number of jets to be provided is unknown, however, military analysts say 50 or more may be the fleet size required for combat effectiveness across all of Ukraine. So, there is a strong potential for large orders of spare parts and maintenance supplies at the very least…and the possibility of large orders for F16 or F35 planes to replace the jets going to Ukraine.

With that background, it looks like traders are still undecided early on Monday. DIA seems to be retesting its T-line while the other two major indices are just sitting inside Friday’s candle just below their closes. SPY may be getting some support from the 2/2 and 5/1 highs level. Meanwhile, QQQ still has to deal with its next resistance level it failed Friday (which has caused multiple reversals back into early 2021. Over-extension from the T-line is not a problem although QQQ remains a bit stretched. The T2122 indicator also sits in its mid-range (telling us we have at least a little room left to run). With this all said, it does not pay to fight the tape and the trend remains bullish at the moment in the SPY and especially QQQ. DIA, on the other hand, is a choppy, slightly bearish mess.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

With disappointing economic data and Fed speakers remaining hawkish on their battle with inflation but in a late-day surge investors whipsawed the indexes with the Dow reversing more than 350 points from low to high in the last 30 minutes of the day! The SPY broke out above resistance to joining the QQQ while the DIA and IWM remain range bound after the 2-day rally. Only a handful of the tech giants provide the majority of the rally. Today with a light earnings calendar the focus will likely be on the economic calendar dominated by Fed speakers including Jerome Powell.

Though Japanese stocks reached their highest level since 1990 Asian markets closed mixed with Hong Kong down 1.40%. European markets trade green across the board this morning as G-7 leaders commit to more Russian sanctions. U.S. futures suggest a modest open on Friday with Jerome Powell’s comments following committee member comments likely to dominate today’s market sentiment.

Economic Calendar

Earnings Calendar

We have a very light day on the earnings calendar. Notable reports for Friday include DE & FL.

News & Technicals’

Leaders in the G-7 have committed to more Russian sanctions. “We will starve Russia of G-7 technology, industrial equipment, and services that support its war machine,” the G-7 said in a statement released late Friday. The G-7 added, “We will continue our joint effort to support Ukraine’s repair of its critical infrastructure, recovery, and reconstruction.” The United Kingdom separately imposed further sanctions on Russia’s diamonds, an industry worth $4 billion in exports in 2021.

The Walt Disney Co. has scrapped its plans to build a new campus in Lake Nona, Florida, and relocate 2,000 employees from California to work in digital technology, finance, and product development. The company cited “changing business conditions” as the reason for the decision. The move comes amid a bitter feud between Disney and Florida Gov. Ron DeSantis over a state law that bans classroom lessons on sexual orientation and gender identity in early grades. Disney filed a First Amendment lawsuit against DeSantis and other officials last month. The new campus was expected to cost $1 billion and create 13,000 jobs over the next ten years.

Investors whipsawed the indexes on Thursday, despite the uncertainty over Fed rate comments and the debt-limit talks in Washington. Hotter-than-expected jobless claims and a very weak economic outlook in the Philly Fed report started the day sharply lower but surged sharply higher in the last 30 minutes of the day with the Dow moving more than 350 points from low to high. The good news is that the late-day surge finally broke the resistance in the SPY with the tech giants doing most of the lifting. However, the DIA and IWM remain range bound although looking improved with the 2-day rally. We have a light day on the earnings calendar and the economic calendar will be dominated by Fed speakers with Jerrome Powell speaking at 11:00 AM Eastern.

Markets started the day dead on Thursday (“gapping” up 0.06% in the SPY, up 0.11% in the QQQ, and down 0.25% in the DIA). The large-cap indices both then proceeded to be dead money for 30 minutes. However, the Bulls had other plans in the QQQ as a strong rally kicked in at the open and did not let up until noon. After their 30-minute wake-up call, the SPY and DIA followed QQQ higher until 11 am before resting for an hour. From noon until 2 pm all three major indices sold off a bit (with DIA even crossing back through its open to new lows at 2 pm). Yet the Bulls would have none of this and led a strong rally across the board the last two hours of the day, taking all three of the major indices out very near the highs. This action gave us large, white-bodied candles in the SPY and QQQ with essentially no lower wick and a tiny upper wick. Meanwhile, the DIA printed a white-bodied candle with a longer lower wick and a tiny upper wick.

On the day, six of the 10 sectors were in the green with Technology (+1.83%) leading the way higher as Communications Services (-0.71%) lagged behind the other sectors. At the same time, the SPY gained 0.96%, DIA gained 0.43%, and QQQ gained 1.86%. VXX fell another 4% to 34.90 and T2122 climbed back up outside of the oversold territory to 75.61. 10-year bond yields spiked up to 3.651% (as a flood of money came out of bonds) while Oil (WTI) fell 1.18% to end at $72.03 per barrel. So, Thursday saw the large caps unsure but the “big dog” tech names like NFLX, NVDA, AMD, AMZN, and AAPL dragged the rest of the market to new highs. This happened on close to average volume in all three major indices.

In economic news, Weekly Initial Jobless Claims came in below expectations at 242k (compared to a forecast of 254k and the prior week’s 264k number). However, it must be noted that three-quarters of the decline from last week was due to the stopping of massive fraudulent claims coming from the state of MA. At the same time, the Philly Fed Manufacturing Index came in better than expected (but still negative) at -10.4 (versus a forecast of -19.8 and far better than the April reading of -31.3). Later in the morning, April’s Existing Home Sales were just shy of the anticipated value at 4.28 million (compared to a forecast of 4.30 million but well below the March value of 4.43 million). This represented a 3.4% month-on-month decline. After the close, the Fed Balance Sheet was reported at $8.457 trillion, which is down $46 billion from one week ago. Meanwhile, Bank Reserve Balances at the Federal Reserve were up to $3.280 trillion (from last week’s $3.225 trillion).

In Fed talk, Fed Governor Jefferson (also Vice-Chair nominee) told a conference that inflation may be slowing but it is too early to judge the full impact of the rapid rate increases the Fed instituted in the last 15 months. He said “By some measures, progress has been slowing” and “Outside of energy and food, the progress on inflation remains a challenge,”. However, Dallas Fed President Logan seemed to be in the other camp, saying “The data in coming weeks could yet show that it is appropriate to skip a meeting.” However, uber-hawk St. Louis Fed President Bullard told the Financial Times “(the slow progress on taming inflation) may warrant taking out some insurance by raising rates somewhat more to make sure that we really do get inflation under control.”

In stock news, Reuters reported Thursday that in the wake of the failures of SBNY, SVB, and FRC, banks now see social media as a serious threat rather than a potential marketing channel. Reuters says banks, especially the majors like JPM and C, have set up teams to monitor social media, contact any complaining customers to resolve issues quickly, and also nip any reputational risks in the bud. (Unstated, but implied, is the big banks using bots to post counter-messaging to any concerns over liquidity.) In a related story, SCHW (who was a brokerage mentioned among the bank deposit run stories) raised $2.5 billion through a debt offering on Thursday. Elsewhere, the NYSE and NASDAQ said they will nullify premarket trades of CDW (made between 4 am and 4:22 am Eastern) after share prices briefly plunged 96%. Meanwhile, Reuters reported SONY is considering spinning off its finance unit in an IPO just three years after taking full control of that line. Also, in the afternoon, META shared new details on its AI work, including a custom AI chip being developed in-house. The company claimed it has been developing AI chips since 2020 and their chips use a fraction of the electricity of market-leading NVDA’s AI chips. In political spat news, DIS has canceled plans to build a $1 billion office campus in Florida, announced the closing of a luxury hotel there, and also canceled the relocation of 2,000 high-paid employees (averaging $120k) to that state amidst the company’s fight with the Florida Governor. The fight is over the Governor’s retaliation against the company for publicly stating opposition to his 2022 cultural agenda law. The impact on DIS of these decisions is unknown although it has already lost its self-controlled zoning and tax district and will spend a large amount suing the state for breaking related contracts. On the FL side of the equation, these moves will cost the state billions of dollars in lost taxes, jobs, and development in the next few years.

In stock legal and regulatory news, a US district judge issued a temporary restraining order preventing AMGN from closing its $27.8 billion purchase of HZNP until after the suit brought by the FTC to block that deal has been heard in court. Meanwhile, the US Supreme Court refused to take up an appeal of a lower court decision to throw out a lawsuit against GOOGL. The case challenged the so-called “Section 230” liability protection of social media companies for content posted by their users. This caused a sigh of relief across all major tech names. In another case, the Supreme Court ruled 9-0 against AMGN in its bid to revive patents in an infringement case the company had brought against SNY and REGN. Elsewhere, GOOGL agreed to pay the state of WA $39.9 million to settle a lawsuit claiming the company had misled users about its location tracking practices. (The company had previously paid $391.5 million to settle a suit from 40 states last November and another $80+ million to settle with AZ in October over the same issue.) Later, the NHTSA announced that F is recalling 422k SUVs because the video from rearview cameras may fail even after a prior recall repair. This recall includes 2020-2023 Ford Explorers and Lincoln Navigators.

After the close, AMAT, ROST, FTCH, and GLOB all reported beats on both the revenue and earnings lines. Meanwhile, DXC, FLO, and CVCO all missed on revenue while beating on earnings. Unfortunately, QFIN missed on both the top and bottom lines. There were no guidance changes announced.

Overnight, Asian markets leaned heavily to the green side. Hong Kong (-1.40%), Thailand (-0.77%), and Shanghai (-0.42%) were the only red in the region. Meanwhile, New Zealand (+1.03%), South Korea (+0.89%), and Japan (+0.77%) led the more numerous gainers. In Europe, we see a similar story taking shape at midday. The CAC (+0.65%), DAX (+0.57%), and FTSE (+0.43%) lead all but three bourses higher with only Denmark (-0.53%) showing any appreciable loss in early afternoon trade. In the US, as of 7:30 am, Futures are pointing toward a very modest green start to the day. The DIA implies a +0.12% open, the SPY is implying a +0.17% open, and the QQQ implies a +0.05% open at this hour. At the same time, 10-year bond yields are flat at 3.65% and Oil (WTI) is up 1.14% to $72.76/barrel in early trading.

The major economic news events scheduled for Friday is limited to hearing from three Fed speakers (Williams at 8:45 am, Bowman at 9 am, and Chair Powell at 11 am). The major earnings reports scheduled for the day are limited to DE, CTLT, and FL before the open. There are no earnings reports scheduled for after the close.

So far this morning, DE beat on both the revenue and earnings lines. Showing solid growth in revenue (+30% which was a 17.2% upside surprise) and earnings (+42%, which was a 12.6% upside surprise). However, FL missed on both the top and bottom lines. It is worth noting that DE also raised its forward guidance while FL lowered its guidance at the time of reporting. (CTLT was scheduled to report at 7 am but has been delayed for some reason.)

In miscellaneous news, after the close, the US and Taiwan reached a trade agreement covering customs procedures, regulatory practices, anti-corruption measures, as well as small business issues. The deal is not expected to impact any tariffs. This deal was really just a “make-up” deal because Taiwan had previously been excluded from the Indo-Pacific Economic Framework to avoid conflicts with China. Elsewhere, G7 countries unveiled new sanctions and export controls that target Russia. The measures added 70 entities to a blacklist prohibiting them from receiving any exports from G7 countries as well as 300 sanctions against individuals, entities, vessels, and aircraft considered facilitators. The Russian energy-extracting industry was also targeted. Meanwhile, in Kansas, a Wheat industry group announced the results of its survey of the state’s winter wheat crop. The survey expects Kansas (the largest wheat-producing state) to have the lowest crop yield since 2000. They expect a crop of 178-million-bushels (compared to a USDA forecast of 191.4-million-bushels and 2022’s 244.2-million-bushel winter wheat crop). If this new estimate is correct, expect pressure on food prices related to wheat despite the recent extension of the Russia-Turkey-Ukraine grain export deal.

With that background, it looks like DIA is pushing up against resistance at yesterday’s closing level. However, SPY and QQQ are looking to push higher this morning. In addition, all three major indices are up off the premarket lows and are now at the top of their premarket range. Just be aware that QQQ (the market leader) is close to retesting its next resistance level above and it is really a relative handful of massive tech names dragging QQQ (and the rest of the market) higher. Over-extension from the T-line is also a problem for QQQ and to a lesser extent for SPY. However, the T2122 indicator is still in (the top of) its mid-range telling us we have at least a little room left. All of this is taking place on a Friday after a nice up week (especially in QQQ). So, profit-taking and rest for the market seem in order. Don’t get caught off-guard by some Friday selling. Still, we can’t fight the tape and the trend remains bullish at the moment.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The bulls were energized on Wednesday triggering a short squeeze when both the President and Speaker came out with statements saying they are working together for a deal on the debt ceiling. Unfortunately, the rally didn’t break the trading range of the DIA, SPY, and IWM which has kept indexes trapped for more than one and a half months. Today along with WMT earnings we will get Jobless Claims, the Philly Fed numbers, Existing Home Sales, and more Fed member chatter to add the potential for price volatility.

Asian markets took a cue from the U.S. surge closing the day with gains across the board with the Nikkei leading the way up 1.60%. European markets are also decidedly bullish this morning reacting to the debit ceiling progress hopes. U.S. futures reversed overnight losses to once again suggest a bullish open ahead of potentially market-moving earnings and economic data.

The global debt has reached a near-record level of $305 trillion, according to the Institute of International Finance (IIF). This is an increase of $45 trillion since the start of the pandemic, driven by unprecedented fiscal and monetary stimulus measures. However, as central banks start to raise interest rates to curb inflation, the debt servicing costs have also risen, creating a “crisis of adaptation” for borrowers and lenders. The IIF warned that the high leverage in the financial system poses significant risks to financial stability and economic growth.

The tech giants are dominating the stock market in 2023, as they continue to grow their profits and expand their businesses. Apple, Alphabet, Amazon, and Microsoft have all increased their share prices by more than 30% since January, while Meta has more than doubled its value. These five companies are outperforming the rest of the market by a wide margin, as the Dow Jones Industrial Average has barely moved in the same period. The tech sector is showing its resilience or is this an irrational move indicating a growing tech bubble?

Target is facing a serious problem of organized retail crime, which is costing the company more money and putting its stores at risk. The company expects to lose $500 million more in 2023 than in 2022 because of theft and damage by criminal groups. Target’s CEO Brian Cornell said the company is taking steps to protect its products and employees and to keep its stores open for customers. Other retailers have also complained about the increase in retail crime and blamed online platforms that allow criminals to sell stolen goods.

The market saw a substantial short squeeze after lawmakers said they are nearing a debt ceiling deal. Both sides said they don’t want to miss the deadline of early June and are working hard to a compromise. The earnings season is wrapping up with reports from big retailers like Walmart and TJX companies later this week. We will also get data from Jobless Claims, Philly Fed, and Existing Home Sales with more Fed speakers throughout the morning. The big question for the day is; Can the bulls follow through with another day of bullishness as the data rolls out? Buckle up for another day where anything is possible!

Wednesday was the Bulls’ Day. The SPY gapped up 0.52% and the DIA gapped up 0.54%. Then after a modest 30-minute pullback, those bulls started running in a long, steady rally that took us to the highs of the day at about 2 pm. Meanwhile, the QQQ was more muted, gapping up 0.34% and then recrossing the gap before the Bulls stepped in to drive that same long, steady rally to the highs at 2 pm. From there, we saw very modest profit-taking and a sideways grind into the close near the highs in the SPY, DIA, and QQQ. This action gave us large-bodied, white candles with larger lower than upper wicks in all three major indices. The SPY and DIA both crossed back above their T-line (8ema) and DIA crossed back above its 50sma while QQQ continues its rally and is starting to get a bit extended above its own T-line.

On the day, nine of the 10 sectors were in the green with Financial Services (+2.29%) leading the way higher as Utilities (-0.11%) was the only red sector and lagged the rest. At the same time, the SPY gained 1.19%, DIA gained 1.30%, and QQQ gained 1.21%. VXX fell 3.32% to 36.36 and T2122 jumped back up out of the oversold territory to 66.67. 10-year bond yields spiked up to 3.581% while Oil (WTI) jumped up 2.62% to end at $72.72 per barrel. So, Wednesday saw the three major indices get back “in sync” as the bulls ran and then modest profits were taken to end the day. While volume was less-than-average, all three indices were closer to average volume than has been the case for several days.

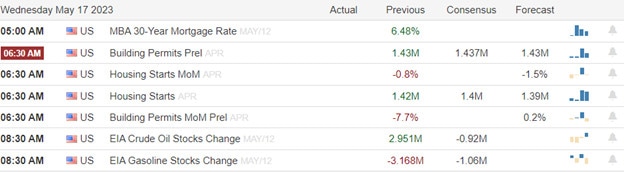

In economic news, Preliminary April Building Permits came in a bit shy of expectations at 1.416 million (compared to a forecast and prior month reading of 1.437 million). This was a 1.5% month-on-month decline, which was improved from March’s 3.0% month-on-month decline. However, at the same time, April Housing Starts were very slightly above expectation at 1.401 million (versus a forecast of 1.400 million and the March value of 1.371 million). Later in the morning, EIA Weekly Crude Oil Inventories showed a much larger than expected inventory build of +5.040-million-barrels (compared to an expected drawdown of 0.920-million-barrels or the prior week’s 2.951-million-barrel increase in inventories). With all that said, the main economic news came from the Debt Ceiling front. Both President Biden and Speaker of the House McCarthy told the press (separate events) that the two sides are making progress and neither thinks the US will default on its debt.

In stock news, WAL gave an update on their deposits saying that they continue to rise in May after the March and early April spate of withdrawals. Elsewhere, the CEO of FSR told an automotive conference in Germany that the company is actively pursuing partnerships with rivals PSNY and an EV maker supported by Mercedes. The partnerships are intended to allow the small EV companies to get to scale and work together to solve supply chain challenges that companies like TSLA can solve on their own. Later, in other EV news, TM announced they are partnering with SZKMY (Suzuki) and Tokyo-listed Daihatsu on a mini-electric commercial van. Each partner will release their own branded version of the vehicle later this year. At the same time, PFE announced it is planning to raise $31 billion through its largest-ever debt offering. PFE intends to use the proceeds to complete its $43 billion deal to acquire SGEN. The debt offering is expected to close on May 19. As the economy weakens, many grocery and household product makers are adding to their low-cost products and smaller-size packages specifically for dollar stores like DLTR and DG. Among these, according to Reuters, are EPC, KHC, HSY, CAG, PG, and SJM, who all have dedicated dollar-store units or teams. This falls in line with a Tufts University study that found dollar stores to be the fastest-growing US food and household goods retailers. Meanwhile, FDX pilots voted overwhelmingly in favor of a strike if needed as the pilots union and company enter the final stages of negotiations. (However, pilots cannot strike until after given permission by the National Labor Relations Mediation Board and after a cooling-off period if and when an impasse is reached.) Finally, the Wall Street Journal reported that TPG and Francisco Partners are collaborating on a $5 billion bid to acquire NEWR.

In stock legal and regulatory news, Reuters reports that Qatar’s sovereign wealth fund (the second-largest shareholder of CS prior to its forced sale) is seeking legal help in an attempt to recover the haircut it took when CS was sold to UBS at “a fraction of its value.” At the same time, according to multiple sources, Reuters reported META is set to face an unspecified but claimed to be the largest fine ever levied by the EU. The fine is a result of META failing to comply with warnings and deadlines from a top EU court and continuing to transfer European user data from EU-based servers to US-based servers. (The prior record fine levied was $821.2 million levied against AMZN.) In Congress, a bipartisan group of lawmakers introduced legislation making it illegal for automakers (including GM, F, STLA, TSLA, and VLKAF) from eliminating AM radios from new models of their vehicles. The bill would direct the NHTSA to mandate that new cars include AM radio at no additional charge. Elsewhere, AVGO has offered “interoperability remedies” in order to address EU antitrust concerns over its deal to acquire VMW for $61 billion. The EU Antitrust Agency recently extended the deadline for its final decision to July 17. Meanwhile, the FAA is forecasting a 4.5% increase in flights over the Memorial Day holiday period, expecting the total to be just shy of the pre-pandemic peak. (DAL expects a 17% increase in passengers from 2022 while AAL and UAL both expect unspecified increases over last year.) Then, after the close, WBA reached a $230 million settlement with the city of San Francisco over its role in the city’s opioid epidemic.

In miscellaneous news, on Wednesday, the NY Fed published a report that said the downside risk to the economy “eased a bit so far this year, but remains elevated.” At the same time, a Reuters poll of 116 economists found that 60% believe rates are at the same level they will be at year-end. Interestingly, 26% predict no hike and at least a 25-basis-point rate cut before year-end. Only 14% are expecting another rate hike by the end of the year. Meanwhile, the Fedwatch Tool tells us markets (futures) are pricing in a 29% chance of a quarter-point hike in June. However, those futures also see a 43% chance of a rate cut in September, a 79% probability of a cut in November, and a 95% chance of a rate cut in December. So, somebody is (or somebodies are) wrong. The question is whether it is the market, the majority of economists, the Fed, or some combination of the three.

After the close, CSCO, SNPS, CPRT, STNE, and TTWO all reported beats on both the revenue and earnings lines. Meanwhile, VSAT and ZTO both missed on revenue while beating on earnings. It is worth noting that CSCO, SNPS, and STNE all raised their forward guidance. Meanwhile, TTWO lowered its forward guidance.

Overnight, Asian markets leaned heavily to the green side. Japan (+1.60%), Taiwan (+1.11%), and Hong Kong (+0.85%) led the region higher while only India (-0.28%) and Shenzhen (-0.12%) showed any red. Meanwhile, in Europe, the bourses are mixed at midday with the big exchanges rallying. The DAX (+1.68%), CAC (+0.92%), and FTSE (+0.55%) are leading the region higher in early afternoon trade. In the US, at 7:30 am, Futures are pointing toward a modestly green start to the day. The DIA implies a +0.09% open, the SPY is implying a +0.22% open, and the QQQ implies a +0.27% open at this hour. At the same time, 10-year bond yields are rising again at 3.6% and Oil (WTI) is flat at $72.80/barrel in early trading.

The major economic news events scheduled for Thursday include Philly Fed Mfg. Index and Weekly Initial Jobless Claims (both at 8:30 am), April Existing Home Sales (10 am), Fed Balance Sheet and Bank Balances with the Fed (both at 4:30 pm). We will also have testimony from Fed Vice Chair (for Bank Supervision) Barr at 9:30 am. The major earnings reports scheduled for the day include WMS, BABA, BBWI, CSIQ, DOLE, GRAB, BEKE, MSGE, and WMT, before the open. Then, after the close, AMAT, CVCO, DXC, FTCH, FLO, GLOB, and ROST report.

In economic news later this week, on Friday, we hear from two Fed speakers (Chair Powell and Williams). In terms of earnings reports later this week, Friday, we hear from DE and FL.

So far this morning, WMT, BEKE, CSIQ, WMS, MSGE, and EXP all reported beat to both the revenue and earnings lines. Meanwhile, BABA, DOLE, and BBWI all missed on revenue while beating on earnings. It is worth noting that BEKE and WMT have raised forward guidance while WMS lowered its guidance. It is also worth noting the MSGE has a 132% upside earnings surprise, BEKE posted a 100% upside surprise on earnings, CSIQ posted a 95% upside surprise on earnings, DOLE posted a 79% upside surprise on earnings, and WMS had a 56% upside surprise on earnings. So, the sandbagging remains strong.

With that background, it looks like all three major indices are running up to test the next potential resistance level in premarket trading. DIA is also retesting its recent downtrend line. However, it is the QQQ (and the handful of massive tech names) that are leading this march higher, until yesterday’s good news gave financials a boost. Over-extension from the T-line is not a problem in general. However, QQQ is getting stretched. Still, the T2122 indicator sits in the mid-range telling us we have at least a little room to move. Be careful of chop and watch for rotation if traders start to think we are overcooked and look to start locking in profits. We still cannot say we have a nicely trending market anywhere except for the QQQ.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Tuesday turned out to be a rough day for the DIA, SPY, and IWM after the Home Depot miss and a retail sales report that came in short of expectations. Of course, the debit ceiling negotiation cloud hanging over the market didn’t help the overall sentiment but now it seems there has been some progress with the President seeming willing to negotiate. Expect a market reaction if a deal is finally struck. Target’s earning report seems to have left a mixed reaction as evidence of a slowing economy continues to grow. Mortgage Apps, Housing, and Petroleum figures are on deck with several earnings reports that could be market-moving.

Overnight Asian markets traded mixed in reaction to economic data and monitoring debit ceiling negations. However, European markets trade flat to mostly lower this morning with Commerzbank down 6%. On the other hand, U.S. futures seem to have a very different opinion pushing for a bullish open and working to recover some of yesterday’s losses.

According to reports, there was some progress made in the negations of the debit ceiling between the President and the Speaker of the house. This continues to weigh on the mind of the market and as information rolls out on this issue expect it to have market ramifications.

Kraft Heinz is introducing HEINZ REMIX™, a digital sauce dispenser that lets customers create their customized condiments. The dispenser has a touchscreen that offers a choice of four bases and four enhancers, with three intensity levels, resulting in over 200 possible combinations. The company aims to attract consumers who want more variety, spiciness, and sweetness in their sauces and to use the data from the dispenser to inform its future product launches in grocery stores. The innovation is part of Kraft Heinz’s turnaround strategy that focuses on its away-from-home segment.

Target reported better-than-expected earnings for the first quarter of fiscal 2023, despite a slight decline in sales. The retailer earned $1.89 per share, beating the consensus estimate of $1.40 by 35%. However, its revenue fell 0.8% year over year to $25.37 billion, as consumers became more cautious about their spending amid inflation and recession fears. Target’s comparable sales also dipped 0.5% in the quarter. The company said it was focused on investing in its stores, digital capabilities, and merchandise assortment to gain market share and drive long-term growth.

Equities fell on Tuesday after Retail sales missed estimates and Home Depot disappointed on earnings guiding lower for the next quarter. Markets were disappointed by weak consumer-spending data and worried about the debt-ceiling deadline. Small-cap stocks suffered more today, signaling a gloomier economic outlook. This was also reflected in sector performance, with cyclical sectors like energy, real estate, and industrials among the worst performers. Treasury yields edged up slightly on the day with Fed speakers suggesting they will hold the line on rates and still willing to raise them if necessary to achieve their 2% target. Today markets will have Mortgage Applications, Housing Starts, and Peterleum numbers along with several earnings reports with a retail theme for the day.

On Tuesday, markets saw a modest gap lower at the open (down 0.27% in the SPY, down 0.30% in the DIA, and down 0.21% in the QQQ). However, those three major indices diverged at the point, with the QQQ immediately rallying (recrossing the gap within 5 minutes and continuing higher at 1 pm), the SPY trading sideways along its opening level, and the DIA selling off until 10:15 am and then trading sideways until about 1 pm. At about 1 pm, all three got back in sync by starting a wavy selloff that lasted into the close. This action gave us a white-bodied candle with a large upper wick in the QQQ, a black-bodied candle with a significant upper wick in the SPY, and a large-bodied black candle in the DIA. The SPY fell down through its T-line (8ema) while the DIA failed a retest of its 50sma after holding up above the previous three days.

On the day, all 10 sectors were in the red with Utilities (-2.11) leading the way lower as Technology (-0.25%) held up significantly better than any other sector. At the same time, the SPY lost 0.67%, DIA lost 1.02%, and QQQ gained 0.11%. VXX was up more than 3% to 37.61 and T2122 climbed dropped back down into the oversold territory at 14.79. 10-year bond yields spiked up to 3.541% while Oil (WTI) fell 0.76% on the day to end at $70.57 per barrel. So, Tuesday was a divergent day that saw the mega-cap DIA fall out of its recent range, large-cap SPY stay at the lower end of its recent range, and QQQ stay inside the top of its recent range. This came on very divergent moves in the QQQ as AMD, AMZN, and GOOGL essentially held up that index on their own. Once again, this happened on well less-than-average volume across all three of the major indices.

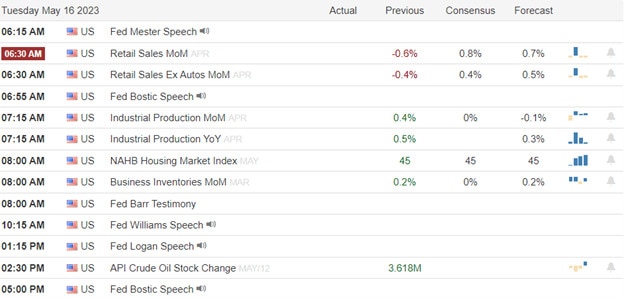

In economic news, April Retail Sales came in much lower than was expected at +0.4% (compared to a forecast of +0.8% but also far better than the March reading of -0.7%). Later, April Industrial Production month-on-month came in much better than expected at +0.5% (versus a forecast of -0.1% and the March reading of +/- 0.0%). On an annual basis, Industrial Production was up 0.24% (and last year had been up 0.07% versus the 2021 reading). March Business Inventories were a bit lower than expected at -0.1% (compared to the forecast of +0.1% and the February value of +0.2%). In addition, March Retail Inventories also grew less than expected at +0.3% (versus the forecast and February reading which were both +0.4%). Finally, after the close, the API Weekly Crude Oil Stocks report showed a 3.690-million-barrel inventory build (compared to an expected drawdown of 1.300-million-barrels but in line with the prior week’s value of a 3.618-million-barrel inventory build).

In Fed talk, Cleveland Fed President Mester said Tuesday that she does not think the FOMC is at a point where it can hold rates steady for a period of time. Specifically, she said, “Have we gotten to that rate yet? At this point, given the data we’ve gotten so far, I would say no.” Later Richmond Fed President Barkin told Bloomberg “I do want to learn more about what’s happening with all these lagged effects. But I also want to reduce inflation…and if more increases are what’s necessary…I’m comfortable doing that.” However, NY Fed President Williams told a university audience he was more comfortable with a “pause and see” approach, telling them “We know it takes a while for our decisions to fully affect the economy” … “We’ve got to make our decisions and then watch what happens, get that feedback, see how the economy’s behaving.” Then Dallas Fed President Logan told a Fed conference “(Changing rates in) smaller, less frequent steps can make it less likely that FOMC monetary policy causes US financial instability.”

In stock news, CNBC (citing sources) reported that CMCSA is likely to sell its 33% stake in the Hulu streaming platform to DIS between now and early next year. Later, an investing consortium including BX and TRI released a term sheet stating that it is going to sell $3 billion worth of stock in the London Stock Exchange, which would be approximately 5.5% of the exchanges voting shares. Mid-day, the CEO of OpenAI (creator of ChatGPT) and IBM both told US Senators that artificial intelligence needs to be heavily regulated…but also that we shouldn’t stifle innovation or the great benefits AI could offer. Testimony from the two raised fears of AI spreading misinformation, influencing elections, infringing copyrights, and upending the economy by replacing swaths of jobs. (Needless to say, MSFT, GOOGL, and many others companies that have gone “full speed ahead” on AI were likely not pleased by the news.) Also in the afternoon, a German Automobile Club study found that TSLA Model 3 vehicles dominated its internal combustion engine competitors in terms of reliability for cars older than three years finding that just 1.1 out of every 1,000 2020 TSLA Model 3 broke down annually. (6.9 breakdowns per 1,000 was the average for gas vehicles and 4.9/1000 was the EV average.) Elsewhere, after the close, NYCB announced that the FDIC is selling shares of the bank that were acquired during the seizure of SBNY in what amounts to a secondary share offering. Meanwhile, NOW announced its first-ever stock buyback program of up to $1.5 billion. Finally, it was announced that the new entity created by the combination of WWE and EDR will trade under the ticker TKO (TKO Group).

In stock legal and regulatory news, the FTC said Tuesday that it will sue to prevent the proposed AMGN $27.8 billion purchase of HZNP which would give AMGN monopoly positions in the treatments in certain diseases. Meanwhile, the NHTSA announced that STLA is recalling 219,000 2014-2016 Jeep Cherokee SUVs over fire risks due to electrical shorts in the power liftgate. Later in the day, Reuters reported that WFC has agreed to pay $1 billion to settle a lawsuit that accused the company of defrauding shareholders by misinforming them about its progress in recovering from a series of scandals.” A US District judge has granted preliminary approval to an all-cash settlement of the suit, but the deal will not be final until a hearing in early September. Elsewhere, Reuters reports that JNJ has set aside $400 million in a separate fund to resolve State AGs claims that it violated state unfair business practices and consumer protection laws as part of its second attempt to settle 38,000 lawsuits over talc product liability. (JNJ’s second bankruptcy plea offered $8.9 billion to settle the 38,000 cases.) At the same time, a US Appeals Court has ruled in favor of GE, HD, and Ikea and against the University of CA, which had sought to ban the import of light bulbs that infringe on the university’s patents. (Lawsuits against AMZN, WMT, and TGT had also been paused waiting on the outcome of this ruling.) After the close, MAR settled with the state of TX and agreed to “prominently display all resort fees” to increase price transparency. This comes a day after the TX State AG filed suit against H for misleading consumers with marketing and hidden fees.

Overnight, Asian markets were mixed but leaned toward the red side. Hong Kong (-2.09%) and Thailand (-1.25%) were by far the biggest losers while Taiwan (+1.60%), Japan (+0.84%), and South Korea (+0.58%) were the only appreciable gainers on the day. Meanwhile, in Europe, the bourses lean heavily to the red side at midday. The DAX (+0.43%) is an outlier while the CAC (-0.01%) and FTSE (-0.07%) are typical of the small losses being registered across most of the region in early afternoon trade. In the US, as of 7:30 am, Futures are pointing toward a green start to the day. The DIA implies a +0.41% open, the SPY is implying a +0.37% open, and the QQQ implies a +0.23% open at this hour. At the same time, 10-year bond yields are back down to 3.519% and Oil (WTI) is up a half of a percent to $71.23/barrel in early trading.

The major economic news events scheduled for Wednesday are limited to April Building Permits and April Housing Starts (both at 8:30 am), and EIA Crude Oil Inventories (10:30 am). The major earnings reports scheduled for the day include ARCO, TGT, and TJX before the open. Then, after the close, SQM, CSCO, STNE, SNPS, TTWO, VSAT, and ZTO report.

In economic news later this week, on Thursday we get Weekly Initial Jobless Claims, Philly Fed Mfg. Index, April Existing Home Sales, Fed Balance Sheet, and Bank Balances with the Fed. Finally, on Friday, we hear from two Fed speakers (Chair Powell and Williams).

In terms of earnings reports later this week, Thursday, WMS, BABA, BBWI, CSIQ, DOLE, GRAB, BEKE, MSGE, WMT, AMAT, CVCO, DXC, FTCH, FLO, GLOB, and ROST report. Finally, on Friday, we hear from DE and FL.

After the close, KEYS and KD both reported beats to both the revenue and earnings lines. It is worth noting that KEYS raised its forward guidance while KD lowered it own guidance. So far this morning, TCEHY and ARCO have reported beats to both the revenue and earnings lines. Meanwhile, TGT and TJX both missed on revenue while beating on earnings. (This includes a 50% upside earnings surprise from ARCO and an 18% upside earnings surprise by TGT.)

With that background, it looks like the SPY is retesting its T-line and the QQQ continues its march higher, at least as of the premarket. Even DIA is trying to climb back above its 50sma (and back into the recent trading range). Over-extension is not a problem yet in terms of distance from the T-lines. However, the T2122 indicator is back in the oversold region. Be careful of the chop and watch for rotation given the divergence of short-term attitudes of the SPY, DIA, and QQQ. We still do not have a nicely trending market anywhere except the QQQ.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The indexes finished the day about where they began the day with modest gains in another day of chop despite a truly awful Empire State MFG report showing a massive decline in the sector. The capacity for the market to continue to ignore these data points is remarkable and makes one wonder if its actual market strength or complacency. With an earnings miss from HD this morning we have Retail Sales, Industrial Production, Inventories, the Housing Index, and several Fed speaker to keep traders on edge. Plan for yet another day of uncertainty while hoping something happens to end the range-bound chop.

As we slept Asian market traded mixed with modest gains and losses after China reported better-than-expected retail sales activity. European markets trade with modest gains this morning as they monitor the U.S. debt ceiling negotiation progress and economic data. Ahead of a big morning of earnings and economic reports along with Fed speakers while wrangling over the debt ceiling continues, futures suggest a bearish open.

Economic Calendar

Earnings Calendar

Notable reports for Tuesday include AGYS, BIDU, HUYA, KEYS, KD, HD, SE, SSYS, TME, & TUP.

News & Technicals’

The debt limit crisis is looming over Washington as President Joe Biden and House Speaker Kevin McCarthy are set to meet again on Tuesday with other top lawmakers. The meeting comes after a week of daily negotiations between staff from both parties, but with no clear sign of a breakthrough. The federal government could face a default on its obligations as soon as early June if Congress does not raise the debt ceiling, which limits how much the government can borrow to pay its bills. Biden and McCarthy have been at odds over how to address the issue, with Biden calling for a bipartisan solution and McCarthy insisting that Democrats act alone.

Home Depot, the largest home improvement retailer in the U.S., reported disappointing results for the fiscal first quarter of 2023. The company missed analysts’ estimates for revenue and lowered its outlook for the full year, citing weaker demand for big-ticket items and smaller home improvement projects. Home Depot’s Chief Financial Officer Richard McPhail said that customers are spending less on items such as patio sets and grills, which typically drive sales in the spring season. He also attributed the lower revenue to colder weather and falling lumber prices, which reduced the average ticket size.

China’s crackdown on due diligence consultancies, such as Capvision, has raised concerns among foreign investors about the country’s openness and transparency. Capvision is the latest firm to be accused of violating national security laws by providing sensitive information to overseas clients. This follows the recent restrictions on foreign access to China’s data and information platforms, which have hampered the ability of investors to conduct research and analysis. Some experts argue that China’s enforcement of its anti-espionage law is arbitrary and vague, as the term “national security” is not clearly defined or delimited.

Despite a terrible Empire State Mfg. number the indexes experienced another day of chop ending the day slightly positive about exactly where they began the day. Retail giants, HD, Target, and Walmart prepare to report their earnings and lawmakers will meet this afternoon hoping to reach a deal on the debt limit. The Nasdaq led the gains among the major indexes, while the S&P 500 Index and Dow Jones also advanced. Treasury yields edged up, with the 2-year Treasury yield approaching 4.0% again. However, yields are still well below their early March peaks. The market expects the Fed to lower rates by September but that thought process does not seem to be shared by the voting members of the Fed. We shall see! Oil prices also rose slightly, with WTI crude oil recovering above $71, but still down by about 11% this year. Today before the bell we have the market moving Retail Sales figures followed by Industrial production, Inventories, Housing Market along with several Fed speakers.