BA In Trouble Again and Big Bitcoin Week

The markets opened around the flat line on Friday. SPY opened up 0.05%, DIA started down 0.08%, and QQQ opened up 0.03%. At that point, all three major index ETFs began a rally that lasted until 10:15 a.m. in the DIA, until 11 a.m. in the SPY and until 11:20 a.m. in the QQQ. From there, all three sold off until 1:20 p.m. Then we saw a new wave up for about an hour followed by down wave down wave that lasted another hour and finally a 30 minute up wave to end the day. This action gave us White-bodied Spinning Top candles in all three major index ETFs. The DIA again retested its T-line (8ema) but failed to close above it. This happened on above-average volume in the DIA, less-than-average volume in the SPY, and average volume in the QQQ.

On the day, nine of the 10 sectors were in the green with Communications Services (+0.76%) out front leading the way higher while Consumer Defensive was the lone laggard in the red. At the same time, the SPY gained 0.14%, DIA gained 0.03%, and QQQ gained 0.12%. The VXX fell 3.30% to close at 15.55 and T2122 rose but still remained in its midrange at 45.71. 10-year bond yields rose back above four percent to 4.05% and Oil (WTI) spiked 2.4% to close at $73.92 per barrel. On the day, we saw a volatile seesaw action that really ended up not far from where Thursday had closed.

This ended a string of nine up weeks in a row in the SPY, DIA, and QQQ. On the week, SPY lost 1.55% (on average volume) and DIA lost 0.59% (on above-average volume). However, QQQ lost 3.12% (on less-than-average volume) in what seems to have been at least a short-term rotation out of the big dog tech names that have pulled markets higher for more than a year. TSLA fell 4.42%, AAPL dropped 5.90%, MSFT fell 2.20%, AMZN dropped 4.41%, AMD plummeted 5.99%, GOOGL fell 2.83%, and INTC plummeted 6.69% on the week. However, of these, only AAPL recorded even average volume for the week.

The economic news on Friday included Dec. Avg. Hourly Earnings (year-on-year) which came in higher than expected at +4.1% (compared to a forecast of +3.9% and the Nov. reading of +4.0%). On a month-on-month basis this was +0.4% (versus a forecast of +0.3% but in line with November’s +0.4% value). At the same time, Dec. Nonfarm Payrolls were much stronger than expected at +216k (compared to a forecast of +170k and the Nov. reading of +173k). On the private side, Dec. Private Nonfarm Payrolls were also much stronger than predicted at +164k (versus a forecast of +130k and the Nov. value of +136k). These resulted in a Dec. Unemployment Rate that was lower than anticipated at 3.7% (compared to a forecast of 3.8% but in line with the November reading of 3.7%). The Dec. Participation Rate was lower than predicted at 62.5% (versus a forecast and November reading of 62.8%). So, the jobs market remains strong and workers saw real wage growth (compared to inflation) again last month. Later, Nov. Factory Orders were also much stronger than expected at +2.6% (versus a +2.1% forecast and far better than the November 3.4% decline). At the same time, Dec. ISM Non-Mfg. Employment was far below predicted at 43.3 (compared to a forecast of 51.0 and the November value of 50.7). Meanwhile, Dec. ISM Non-Mfg. PMI was also below expectations at 50.6 (versus the forecast of 52.6 and November’s 52.7 reading). Finally, Dec. ISM Non-Mfg. Prices were slightly above anticipated at 57.4 (compared to a forecast of 57.3 but down from November’s 58.3 value).

In stock news, STLA announced it would not advertise during next month’s Super Bowl, citing a challenging US auto market. (GM made the same announcement in November.) STLA has often been a significant advertiser at the event. At the same time, the Wall Street Journal reported that SNPS is in advanced discussions to buy ANSS for around $35 billion in cash and stock. Later, a large US medical study was reported in the peer-reviewed journal Nature Friday, which found NVO’s hit weight-loss drugs are not linked to an increase in suicidal thoughts. Elsewhere, Reuters reported that CHK and SWN are very close to a $17 billion merger agreement. After hours, Reuters reported that the UAW has reached a tentative deal with ALSN. Meanwhile, LLY announced a new website offering telehealth prescriptions and direct-to-home delivery of drugs on Friday. This move alone may not dramatically impact the pharmacy industry but other drugmakers are expected to follow suit, which could put pressure on grocery and pharmacy chains currently filling prescriptions. At the same time, the Insurance Journal reported Friday that AUR (driverless trucking technology) along with two other competing private firms intend to drop their human copilots from their semi-truck shipments, starting in Texas. (AUR carries freight for WMT, KR, FDX, TSN, and other major shippers.) On Saturday, ALK grounded its entire fleet of 65 BA 737 MAX 9 planes after a midnight flight Friday had an entire section of the fuselage blown out, causing explosive decompression of the cabin at 16,000 feet during a flight.

In stock government, legal, and regulatory news, in China, the State Administration for Market Regulation said Friday that TSLA would be recalling and fixing all 1.62 million vehicles (all sold in the country) equipped with the full self-driving feature. (This is for the same reason as the US recall of all TSLA vehicles sold in the US in December.) Later, MSFT and OpenAI were hit with a new lawsuit in federal court in NY Friday. The suit alleges the companies misused the works of nonfiction authors to train their AI models. At the same time, Reuters reported that India’s Antitrust Regulator launched an investigation into UPS, FDX, and Germany’s DHL for alleged collusion on discounts and tariffs. Elsewhere, the FDA approved a new topical gel treatment for the highly contagious skin disease molluscum contagiosum produced by LGND. (The disease impacts 6 million Americans per year with up to 73% of patients not receiving treatment.) During the afternoon, the New York Times reported that the US Dept. of Justice is preparing an antitrust lawsuit against AAPL. (The suit purportedly attacks the way AAPL watches only work with iPhones as well as exclusivity restrictions for the iMessage app as well as distribution of iPhone apps.) At the same time, the NASDAQ announced it will delist LMDX on January 9th. Later, two groups representing the auto dealers filed a lawsuit challenging the FTC consumer protection regulations finalized in December which ban “bait and switch” advertising tactics and prohibit dealerships from charging add-on costs without prior customer approval. (The groups are supported by GM, TM, VLKAF, and other automakers.) On Saturday, following the ALK incident with a BA 737 MAX 9 jet (see above), the FAA grounded some of the same model jets nationwide and ordered the immediate inspection of all BA 737 MAX 9 jets. (There are 215 in service worldwide and the FAA order impacts 171 of them.)

Overnight, Asian markets were mixed. Hong Kong (-1.88%), Shenzhen (-1.85%), and Shanghai (-1.42%) paced the losses while Malaysia (+0.54%), Taiwan (+0.31%), and Japan (+0.27%) led the gainers. In Europe, we see a similar picture taking shape at midday with only five of the 15 bourses in the green. The CAC (-0.02%), DAX (+0.15%), and FTSE (-0.25%) are typical of the region. Athens (+1.27%) and Portugal (-1.13%) are the outliers in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a mixed open with the Dow was an outlier. The DIA implies a -0.42% open, the SPY is implying a -0.05% open, and the QQQ implies a +0.07% open at this hour. At the same time, 10-year bond yields are back up to 4.061% and Oil (WTI) is down by 2.82% to $71.75 per barrel in early trading.

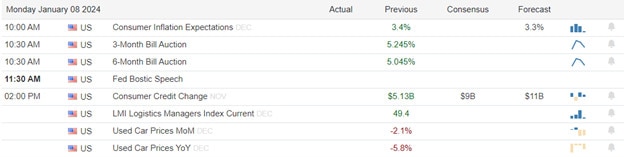

The major economic news scheduled for Monday is limited to the NY Fed 1-year Consumer Inflation Expectations (11 a.m.) and November Consumer Credit (3 p.m.). The major earnings reports scheduled for the day are limited to CMC and HELE before the open. Then, after the close, JEF reports.

In economic news later this week, on Tuesday we get Nov. Imports, Nov. Exports, Nov. Trade Balance, EIA Short-Term Energy Outlook, and API Weekly Crude Oil Stocks. On Wednesday, EIA Weekly Crude Oil Inventories are reported and Fed member Williams speaks. Then Thursday, we get Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, Dec. Core CPI, Dec. CPI, Dec. Federal Budget Balance, and the Fed’s Balance Sheet. On Friday, Dec. Core PPI, Dec. PPI, and the WASDE Ag report are delivered.

In terms of earnings reports, the main thrust does not start again until the end of the week. In the meantime, on Tuesday, AYI, ACI, MSM, SNX, PSMT, and WDFC report. Then Wednesday, we hear from KBH. On Thursday, INFY reports. Finally, on Friday, we hear from BAC, BK, BLK, C, DAL, JPM, UNH, WFC, and WIT.

In miscellaneous news, the NY Fed reported Friday that global supply chain issues eased in December. The report said the Fed’s proprietary supply chain pressure index came in a -0.15 for December, down from a November reading of +0.13. (The gauge peeked at +4.33 in December 2021.) Elsewhere, several major investment firms including BLK and FNF updated their filings Friday and hope that their Bitcoin spot price ETFs will be approved this week. This comes after the SEC asked the fund managers to submit written requests to accelerate approval.

In government funding news, the first of two cliffs (partial shutdowns) is scheduled for January 19. On Sunday afternoon, Congressional leaders (Senate Majority Leader Schumer and House Speaker Johnson) announced a $1.59 trillion agreement on the top-line spending number. The only details agreed are that this will be divided between $886 billion for Defense and $704 billion in non-defense spending. The deal does give a few more concessions to the MAGA types, allowing the GOP to renege on the June 2023 agreement. However, it doesn’t give specifics for any of the 12 appropriations bills and it is still unclear whether Speaker Johnson even has the power to get this agreement passed in his own House with the GOP majority now down to two votes (there is no tie-breaker in the House and so a tie vote fails).

So far this morning, CMC reported beats on both the revenue and earnings lines. At the same time, HELE beat on revenue while missing on earnings.

With that background, it looks like Mr. Market is indecisive so far this morning. The DIA opened the premarket with a gap lower and this has put in a small black-bodied candle that is about half wick. The other two major index ETFs are also giving no clear direction with the QQQ gapping down, but putting in the strongest whit-body of the two candles while SPY prints a true Doji type inside of Friday’s candle so far in the early session. So, the Bears remain in control of the short-term trend and the longer-term bullish daily trend lines remain broken. However, no new lower-high has presented itself in any of the three major index ETFs. (We are technically not yet in a downtrend.) In terms of extension, the two large-cap index ETFs are not far from their T-line (8ema), but the QQQ is getting a bit stretched below its T-line. At the same time, the T2122 indicator remains in its mid-range. So, both the Bulls and Bears do have room to run if they can gather the momentum to do it. Continue to keep an eye on the Tech Big Dogs. If we are seeing a rotation out of those names (which have dragged markets along for a year or more), it will be hard for markets to do anything except retreat.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Strong Labor Market

The Employment Situration report continues to not only indicate a strong labor market along with rising wages raised some worries about inflation as the dollar rallied and the 10-year bond yield rose back above 4%. We kick off the new week with a light earnings and economic calendar and it pretty much stays that way until until Thursday we we get the next reading on CPI. So as we hurry up and wait don’t be surprised to see just about anything in the price action including range bound chop as we wait in anticipation.

Asian markets closed the day mostly lower with the tech heavy Hong Kong leading the selling down 1.88% followed by Shanghai down 1.42%. Europeian markets trade mostly lower this morning with modest gains and losses in a cautious session waiting on pending inflation data. However, the U.S. futures point to a mixed open with as tech tries to bounce back with Dow under pressure due to the bad news for Boeing.

Economic Calendar

Earnings Calendar

Notable reports for Monday ACCD, HELE, & JEF.

News & Technicals’

Boeing, the aerospace giant, saw its shares plunge 8% in pre-market trading at 4:30 a.m. ET on Monday. The drop came after the Federal Aviation Administration (FAA) issued an emergency order on Saturday, requiring 171 Boeing planes around the world to undergo inspections before they can fly again. The order was triggered by an incident on Friday, when an Alaska Airlines flight suffered a blowout in one of its engines, forcing it to make an emergency landing. The National Transportation Safety Board (NTSB) is investigating the cause of the engine failure.

Audacy, a leading company in radio and podcasting, has announced that it will file for Chapter 11 bankruptcy protection to deal with its heavy debt burden. The company said that it has reached a restructuring agreement with its creditors, which will enable it to cut its total debt by 80%, from about $1.9 billion to about $350 million. The company said that the bankruptcy process will not affect its operations or its content offerings.

A $1.59 trillion spending deal was reached by congressional leaders on Sunday, as the government tries to prevent a possible shutdown. The deal sets the overall budget for the 2024 fiscal year, dividing $1.59 trillion between defense and non-defense spending, with $886 billion for the former and $704 billion for the latter. The deal shows that Johnson and Schumer, the leaders of the Senate, are cooperating, but it does not guarantee a funding agreement, as there are still policy disputes between the parties.

Cosco, a Chinese state-owned shipping company, has stopped its services to Israel via the Red Sea, amid rising conflicts in the vital waterway. The Red Sea connects the Mediterranean Sea and the Indian Ocean, and is a key route for global trade. Israeli state media reported that Cosco’s decision was based on security concerns, but did not reveal any further details. According to Globes, an Israeli financial news source, Cosco’s move could affect Israel’s imports and exports.

On Friday The U.S. employment data revealed a strong labor market, causing major indexes to swing between ups and downs. Job growth picked up, boosting the economy, but wage growth was higher than expected, raising inflation fears. The 10-year Treasury yield rose above 4%, hurting the defensive sectors, which are more affected by interest rates. However, today’s market changes were not very significant, and despite stocks finishing the first week of the year lower, only slightly correcting from the parbolic nine week bullish run. The FAA grounding sozens of 737 Max9s aircraft has the market feeling a bit bearish but little on the earnings and economic calendar anything is possible. In fact as we continue to wait for the official kickoff of earnings and the CPI and PPI reports later this week traders should consider the possibility of choppy range bound consolidations through mid week.

Trade Wisely,

Doug

December Jobs Numbers Will Call Tune

Thursday saw mixed to start the day. The SPY gapped up 0.09%, DIA opened 0.16% higher, and QQQ gapped down 0.47%. At that point, all three major index ETFs put in a morning rally that hit the highs of the day at about 11:30 a.m. This was followed by a modest selloff that lasted right into the close. That action gave all three a large high wick on a small black body. This could be seen as Gravestone Doji in the DIA and QQQ as well as an Inverted Hammer in the SPY. The DIA also retested and failed its T-line (8ema). This all happened on average volume in the DIA and below-average volume in the SPY and QQQ.

On the day, seven of the 10 sectors were in the red with Energy (-1.35%) far out front leading the market lower while Healthcare (+0.67%) was by far the strongest sector. At the same time, the SPY lost 0.31%, DIA gained 0.11%, and QQQ lost 0.51%. The VXX was just on the red side of flat to close at 16.08 and T2122 fell a bit but remains in its midrange at 36.52. 10-year bond yields rose again to 3.999% and Oil (WTI) dropped 0.43% to close at $72.39 per barrel. So, on the day, we saw a divergence at the open with the high-tech QQQ gapping down while the two large-cap index ETFs opened on the green side of flat. However, after that, the three acted in lock-step the rest of the day. So, the bullish trendlines remain broken in the DIA, SPY, and QQQ. However, the DIA is still basically consolidating while the SPY and especially QQQ continue their pullback.

The economic news on Thursday included the December ADP Nonfarm Employment Change which came in much stronger than expected at +164k (compared to a forecast of +115k and the revised November number of +101k). This was the largest gain since August. Later, Weekly Initial Jobless Claims were lower than predicted at 202k (versus a forecast of 216k and the previous week’s 220k). At the same time, Weekly Continuing Jobless Claims were also down to 1,855k (compared to a forecast of 1,883k and the prior week’s 1,886k reading). Later, Dec. S&P Global Services PMI came in better than anticipated at 51.4 (versus a 51.3 forecast and the prior 50.8 value). At the same time, Dec. S&P Global Composite PMI was slightly lower than expected at 50.9 (compared to a 51.0 forecast but still stronger than the November 50.7 value). Later, EIA Weekly Crude Oil Inventories showed a larger than predicted drawdown of 5.503 million barrels (versus a forecast calling for a 3.200-million-barrel drawdown but still not as much as last week’s 7.114-million-barrel drawdown). Finally, after the close, the Fed Balance Sheet came in $32 billion lower than the prior week at $7.681 trillion (compared to the prior week’s $7.713 trillion.

In stock news, MBLY (who sells semiconductors into the auto industry) said Thursday that it has seen a pullback in orders from customers who are clearing excess inventory. This sent both MBLY and competitors (NXPI, TXN, and WOLF) crashing lower as well as raising concerns about auto sales. At the same time, F posted its best US sales numbers since 2020, saying that sales rose 7.1% to 1.99 million units in 2023. Sales of F electric vehicles also rose 18% and now makeup 17% of total sales. Later, retail analysts reported that AMZN shored up absolute market dominance for the Christmas season. The data shows AMZN had 21% of global order volume for the Thanksgiving through Black Friday period, but jacked that up to an amazing 29% of global orders for all of Xmas season. Consumer Intelligence Research noted that AMZN’s ability to hit two-day delivery deadlines seemed to be a critical factor in winning the huge order volumes. Later, major European retailer Carrefour halted the sale of PEP products as the two companies fight over price hikes. Elsewhere, DIS subsidiary ESPN signed a $920 million, eight-year deal for an extension of the network’s exclusive media rights to 40 NCAA championships (including the lucrative college basketball postseason). This was triple the average annual amount ESPN had paid for the same rights in the past. Later, the CEO of PSX told an energy industry conference that the company would sell $3 billion worth of “non-core” assets in 2024. He gave no timelines but said discussions were ongoing. After the close, XOM signaled it will take a big hit in Q4 as it books a $2.5 billion write-down related to wells abandoned in CA as well as a hit from lower energy prices. (XOM reports February 2nd.)

In stock government, legal, and regulatory news, on Thursday the US Department of Commerce announced it will award MCHP $162 million in grants to increase the US production of microcontroller chips which are key components in both consumer and defense industries. Later, Consumer Reports issued a public letter to the FDA calling for strongly increased regulation and inspection. The consumer rights group said that 84 of 85 supermarkets and fast food restaurants it has recently tested had foods that contain plastics and in fact, 79% of the food tested contained these phthalates or BPA chemicals. (These chemicals are known to disrupt hormone production and regulation as well as pose a wide range of health risks.) At the same time, the SEC ruled that AAPL and DIS cannot avoid shareholder votes about the company’s use of AI tech. These board proposals were made by labor groups with the measures, if passed, asking for an accounting of the company’s use of AI technologies. (Both companies had argued the votes could be left off board agendas because they related to “normal business operations.” The SEC disagreed.) The EEOC filed a motion asking a federal judge to reject TSLA’s motion to pause a lawsuit alleging widespread racial bias at the company’s Fremont CA plant. (TSLA had filed a motion asking that the suit be indefinitely paused until after two other lawsuits are settled.) After the close, the NRLB ruled that GOOGL must bargain with a union representing contract workers at its YouTube Music unit.

Overnight, Asian markets were mostly in the red. Shenzhen (-1.07%), Shanghai (-0.85%), and Hong Kong (-0.66%) led the region lower. Meanwhile, in Europe, we see red across the board at midday. The CAC (-1.08%), DAX (-0.79%), and FTSE (-0.85%) lead the region lower in early afternoon trade. In the US, as of 7:30 a.m., the Futures are pointing toward a modestly down start to the day (ahead of data). The DIA implies a -0.18% open, the SPY is implying a -0.22% open, and the QQQ implies a -0.29% open at this hour. At the same time, 10-year bond yields are back above four percent at 4.036% and Oil (WTI) is up 0.82% to $72.81 per barrel in early trading.

The major economic news scheduled for Friday includes Dec. Avg. Hourly Earnings, Dec. Nonfarm Payrolls, Dec. Private Nonfarm Payrolls, Dec. Participation Rate, and Dec. Unemployment Rate (all at 8:30 a.m.), Nov. Factory Orders, Dec. ISM Non-Mfg. Employment, and Dec. ISM Non-Mfg. PMI (all at 10 a.m.). The major earnings reports scheduled for the day are limited to GBX and STZ before the open. There are no major reports scheduled for after the close.

In miscellaneous news, Reuters reported that short-sellers lost $195 billion in 2023 according to research by S3 Partners research. The report specifically noted huge losses in TLSA, NVDA, AAPL, META, MSFT, and AMZN as the largest sources of pain for the shorts. Elsewhere, Reuters reported that the Biden Administration has bought 13.82 million barrels of domestic oil to refill the strategic petroleum reserve. They have also accelerated the return of 4 million barrels that had been loaned to oil companies. (The SPR holds 354 million barrels and 180 million were released by the administration in 2022 at an average price of $95/barrel. So far, the buybacks are below the target price of $79/barrel and the buyback fund has enough to purchase another 46.5 million barrels even at that price which is higher than market.) The latest bid, put out Wed., was for another 3 million barrels for April delivery. Meanwhile, ADBE Analytics (retail analysts) issued a report Thursday saying that US shopper spending rose 4.9% for the holiday season. The report cited an increase in “Buy Now Pay Later” options and deep discounts on electronics and apparel as key factors in the increase.

So far this morning, STZ reported beats on both the revenue and earnings lines. GBX had be scheduled to report at 6 a.m. but has not done so yet.

With that background, it looks like the Bears are anticipating disappointing December Jobs Numbers this morning (or perhaps anticipating strong jobs numbers which they think will cause the Fed to hold off on the start of rate cuts). Either way, the major index premarkets all opened with a modest gap lower. Since then, all three major index ETFs have given us smaller but black-bodied candles in the early session. So, the Bears remain in control of the short-term trend and the longer-term daily uptrend lines remain broken. However, no new lower-high has presented itself in any of the three major index ETFs. (We are technically not yet in a downtrend.) In terms of extension, the two large-cap index ETFs are not too far from their T-line (8ema), but the QQQ is getting stretched below its T-line. At the same time, the T2122 indicator remains in its mid-range. So, both the Bulls and Bears do both have room to run if they can gather the momentum to do it. Continue to keep an eye on the Tech Big Dogs. If we are seeing a rotation out of those names (which have dragged markets along for a year or more), it will be hard for markets to do anything except retreat. Finally, remember this is Friday…payday. So, prepare your account for the weekend news cycles and don’t forget to pay yourself.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Jobless Claims and S&P PMI on Tap

Markets made most of their movement at the open Wednesday. SPY gapped down 0.44%, DIA gapped down 0.41%, and QQQ gapped down 0.65%. After that, all three major index ETFs traded in a tight range around the open the rest of the day. The biggest move was a selloff the last hour that took all three out near their lows. This action gave us what I would call large-body, black-body, Spinning Top candles with small upper and lower wicks. DIA also crossed below its T-line (8ema) following the SPY and QQQ in that pullback. This happened on greater-than-average volume in the DIA and a bit less-than-average in the SPY and QQQ.

On the day, eight of the 10 sectors were in the red with Consumer Cyclical (-1.85%) and Industrials (-1.80%) out front leading the way lower while Energy (+1.35%) was by far the strongest sector. At the same time, the SPY lost 0.82%, DIA lost 0.76%, and QQQ lost 1.06%. The VXX rose 3.74% to close at 16.10 and T2122 dropped but still remained in its midrange at 38.24. 10-year bond yields rose again to 3.922% and Oil (WTI) spiked 3.38% to close at $72.79 per barrel. So, on the day, most of the move was made at the open with the Bears gapping all the major indices lower. However, from there it was a sideways wobble in a tight range with a selloff the last hour taking us out near the lows. The Bullish trendlines have now been breached but SPY sits at a potential support level and QQQ has the furthest to fall before hitting potential support at about 1.35%.

The economic news on Wednesday included December ISM Mfg. Employment, which came in significantly better than expected at 48.1 (compared to a forecast of 46.5 and the November reading of 45.8). At the same time, December ISM Mfg. PMI also came in better than anticipated at 47.4 (versus a 47.1 forecast and November’s 46.7 value). Meanwhile, December ISM Manufacturing Prices came in much lower than predicted at 45.2 (compared to a forecast of 47.5 and far better than November’s 49.9 value). On the job opening front, November JOLTS Job Openings were down at 8.790 million (versus a forecast of 8.850 million and the October reading of 8.852 million). That was the lowest number of job openings since early 2021, not at a level of 1.4 openings per unemployed person. (The high was a 2:1 ratio in 2022.) Then, after the close, the API Weekly Crude Oil Stocks report showed a bigger-than-expected drawdown of 7.418 million barrels (compared to a forecasted drawdown of 2.967 million barrels and the prior week’s inventory build of 1.837 million barrels).

However, probably the most notable economic news was the release of the FOMC December Meeting Minutes. Those minutes showed that Fed members cited lower inflation risks and foresaw coming rate cuts. However, the start of and the path those cuts will take was very mixed and uncertain among members. Among the notable sections were “Participants pointed to the decline in inflation seen during 2023, noting the recent shift down in six-month inflation readings in particular.” For the first time since mid-2022, the minutes DID NOT describe inflation as “highly unacceptable” and, in fact, said the risk of renewed inflation was “diminished.” The minutes said “a few” participants saw the potential need for the Fed to switch in its tradeoff between the goal of controlling inflation and maintaining high rates of employment. Finally, the minutes noted “an unusually elevated degree of uncertainty” about the economic outlook saying that additional rate hikes are possible as are the beginning of rate cuts. This included some meeting participants floating the idea of slowing Fed balance sheet reductions, as the minutes said “several participants remarked that the Committee’s balance sheet plans indicated that it would slow and then stop the decline in the size of the balance sheet.”

In stock news, XRX announced it will cut 15% of its workforce as part of its attempt to move to a new business model and organizational structure. At the same time, TM announced its vehicle sales rose 6.6% during 2023 with strong demand for affordable sedans and SUVs. Drilling down, TM said electric vehicle sales rose 31% from the prior year, now making up 29.2% of all sales. Later, Bloomberg reported rumors that CI is close to selling its Medicare Advantage business for between $3 billion and $4 billion (that unit generated $7.9 billion in revenue in 2022). Elsewhere, INTC said it would be spinning off its AI-related business into a separate company with the help of DBRG and other investors. At the same time, Reuters reported that AIG is the lead insurer on a $130 million “all risks” policy for the A350 plane that crashed in Tokyo on Tuesday. Later, GM announced it would offer $7,500 in incentives for its electric vehicles after the company lost $7,500 in government tax incentives because the company sources batteries and other parts from China. Meanwhile, F said it would increase the price of its lowest-priced electric vehicles while cutting the price of its premium EV models by as much as $7,000. At the same time, EQNR and BP announced they have terminated an agreement to sell electricity to NY state from their proposed offshore wind farm. The companies cited higher borrowing costs and supply chain issues. Later, Bloomberg reported that GOLD has been speaking to the major investors of FQVLF to determine if there is interest in a takeover.

In stock government, legal, and regulatory news, the Dept. of Transportation reported that US airline flight cancellations fell to the lowest rate in more than a decade. Less than 1.3% of 16.3 million flights were canceled in 2023. At the same time, AAL, DAL, LUV, and UAL achieved a December on-time arrival rate between 83.7% and 99.6%. Later, Reuters reported that GOOGL and META appear to have settled their fines with the Russian government. Previous fines are no longer listed by the Russian government but the companies did not confirm or deny settlement. At the same time, the NHTSA announced that F had agreed to recall just under 113k F-150 trucks over safety concerns related to a rear axle hub bolt. Elsewhere, AAPL agreed to settle a lawsuit alleging the company knowingly let scammers use its gift cards while keeping 30% of the proceeds of the fraud. The settlement terms were not released and must still be approved by a federal judge.

After the close, the only major earnings report was from CALM, which missed on both the revenue and earnings lines.

Overnight, Asian markets leaned to the downside with seven of the 12 exchanges in the red. Shenzhen (-1.24%), Singapore (-0.79%), and South Korea (-0.78%) led the losses while Malaysia (+1.02%) and India (+0.66%) paced the gainers. In Europe, the bourses are leaning to the green side at midday. Eleven of the 15 exchanges in that region are in the green with the CAC (+0.04%), DAX (-0.04%), and FTSE (+0.06%) leading on volume. However, many of the smaller European exchanges are up more than a percent in early afternoon trade. In the US, as of 7:30 a.m., Futures are mixed and basically flat. The DIA implies a +0.11% open, the SPY is implying a -0.04% open, and the QQQ implies a -0.16% open at this hour. At the same time, 10-year bond yields are up to 3.963% again and Oil (WTI) is up 1.00% to $73.43 per barrel in early trading.

The major economic news scheduled for Thursday includes the Dec. ADP Nonfarm Employment Change (8:15 a.m.), Weekly Initial Jobless Claims and Weekly Continuing Jobless Claims (both at 8:30 a.m.), Dec. S&P Global Services PMI and Dec. S&P Global Composite PMI (both at 9:45 a.m.), EIA Weekly Crude Oil Inventories (11 a.m.), and the Fed Balance Sheet (4:30 p.m.) The major earnings reports scheduled for the day are limited to CAG, LW, RDUS, RPM, and WBA before the open. There are no major reports scheduled for after the close.

In economic news later this week, on Friday we get Dec. Avg. Hourly Earnings, Dec. Nonfarm Payrolls, Dec. Private Nonfarm Payrolls, Dec. Participation Rate, Dec. Unemployment Rate, Nov. Factory Orders, Dec. ISM Non-Mfg. Employment, and Dec. ISM Non-Mfg. PMI.

In terms of earnings reports later this week, on Friday, GBX and STZ report.

In shipping news, Reuters reported that ocean freight rates are surging after weekend attacks and US Navy retaliation in the Red Sea. The Asia-to-North America rate has more than doubled to $4,000 per 40-foot container and Asia-to-Mediterranean prices have risen to $5,175 per container. (Some carriers announced $6,000 per container Asia-to-Mediterranean rates as of mid-month.) However, it should be noted that these rates are still well below the pandemic-era rates. In addition, shipment time has risen from 7 to 20 days as ships have to reroute around Africa rather than using the shorter “Suez Canal and Red Sea” route. WMT and AMZN have already reported product delays and inventory issues at the distribution center level. (30% of East Coast import freight normally travels the Suez Canal route.)

In miscellaneous news, oil prices rose Wednesday after supply concerns surfaced following the closure of Libya’s largest oilfield. (This oil does not serve North America, but its removal impacted global oil prices, which rippled through to US oil prices.) Elsewhere, Reuters reported that US bankruptcy filings rose 18% in 2023 on the back of higher interest rates. However, it should be noted that bankruptcies are still far, far below the level seen PRIOR to the pandemic. (For example, in 2019 there were 757,816 bankruptcies. The 2023 number was 445,186 bankruptcies.) So, despite the political rhetoric and protestations of the banking industry, the number of insolvencies is DOWN more than 41% from 2019.

So far this morning, CAG and WBA have reported beats on both the revenue and earnings lines. At the same time, RPM reported misses on both the top and bottom lines.

With that background, it looks like markets are undecided so far this morning. The premarkets opened with a modest gap higher in all three major index ETFs. However, since then the trading has been indecisive with both large-cap index ETFs maintaining white-bodied candles while the QQQ and leans indecisively toward a black-bodied candle. The DIA is attempting a retest of its T-line (8ema) from below in the early session. So, while the Bulls hold on to the longer-term daily trend, we see the Bears in control of the shorter-term trend and so far today markets are undecided or waiting on news. In terms of extension, none of the three major index ETFs are truly extended but QQQ is the most extended of the group, all below their T-lines. At the same time, the T2122 indicator remains in its mid-range. So, both the Bulls and Bears continue to have room to run if they gather the momentum to do it, but the Bears should continue to be hungry given that the Bulls were firmly in control the entire two months of 2023. Lastly, continue to keep an eye on the Tech Big Dogs. If we are seeing a rotation out of those names (which have dragged markets along for a year or more), it will be hard for markets to do anything except retreat.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Down Start to Year With ISM PMI on Tap

Tuesday saw markets start the year off with a gap lower following Iran’s sending a ship into the Red Sea and AAPL caught a downgrade. The SPY gapped down 0.66%, DIA gapped down 0.55%, and QQQ gapped down 0.90%. At that point we had divergence. The DIA immediately rallied to recross the gap and slowly drifted higher until 1 p.m. Meanwhile, SPY ground sideways for an hour and then drifted higher to the highs of the day at 12:45 p.m. At the same time, QQQ sold off sharply after the open until 1:55 a.m. before recovering a portion of the selloff until 12:10 p.m. However, all three major index ETFs sold off most of the afternoon, reaching the lows at about 3:15 p.m. This culminated in a sharp rally in the last 20 minutes of the day. This resulted in a white-bodied Bullish Engulfing candle in the DIA. SPY printed a gap-down, white-bodied Doji, and the QQQ gave us a gap-down, black-bodied candle with a lower wick.

On the day, five of the 10 sectors were in the red with Technology (-2.46%) far out in front leading the losers while Healthcare (+1.04%) led the five gaining sectors. At the same time, the SPY lost 0.56%, DIA gained 0.06%, and QQQ lost 1.69%. The VXX was dead flat at 15.52 and T2122 rose but remained in its midrange at 74.59. 10-year bond yields rose slightly to 3.866% and Oil (WTI) fell to close at $71.65 per barrel. So, the Bears started off the year with a gap lower. However, the follow-through seemed to be based more on rotation out of the big dog tech names than a major change in market sentiment. It is worth noting that both the DIA (strongest index) and QQQ (by far the weakest index) had well-above-average volume while SPY came in just shy of average volume.

The economic news on Tuesday was limited to S&P Dec. Global Manufacturing PMI, which came in just shy of expectation at 47.9 (compared to a forecast of 48.2 and a Nov. value of 49.4). And November Construction Spending grew, but less than had been anticipated at +0.4% (versus a forecast of +0.5% and the October reading of +1.2%).

There have been no earnings reports yet this morning. UNF reports at 8 a.m.

In stock news, CVX announced it would take a “non-cash writedown” of between $3.5 billion and $4 billion on its oil and gas production in Q4. (This primarily covers wells in CA and the Gulf of Mexico, which were abandoned.) Later, RIVN announced that its Q4 deliveries were lower than forecasted or analyst expectations with 13,972 vehicles delivered. (This was down 10% from the prior quarter and below the average analyst estimate of 14,430.) Elsewhere, in a new year flood, companies rushed to issue new bond debt Tuesday. The $29 billion in bonds issued included TM, F, UBS, BNPQY, and others.

In stock government, legal, and regulatory news, it was a very, very slow day. However, Reuters reported that the FDA approved 50% more new drugs in 2023 than in 2022. This puts the agency back on par with historical levels.

In unusual activity news, Bloomberg reports that a Z trader picked up a pile of calls in late October, betting on the real estate rally to continue the rest of the year. They made a tidy $39 million in profit on that bet and have turned around to buy 51,000 more of the Z calls at the $65 strike expiring in May.

Overnight, Asian markets were mostly in the red. South Korea (-2.34%), Taiwan (-1.65%), and Australia (-1.37%) led the region lower with only Malaysia (+0.65%) and Shanghai (+0.17%) staying the int green. In Europe, we see a similar pattern taking shape at midday. The CAC (-1.35%), DAX (-0.94%), and FTSE (-0.85%) lead the region lower with only two minor exchanges in the green in early afternoon trade. In the US, as of 7:30 a.m., Futures point toward another gap lower to start the day. The DIA implies a -0.25% open, the SPY is implying a -0.35% open, and the QQQ implies a -0.54% open at this hour. At the same time, 10-year bonds are up to 3.978% and Oil (WTI) is just on the red side of flat at $70.36 per barrel in early trading.

The major economic news scheduled for Wednesday includes December ISM Mfg. Employment, Dec. ISM Mfg. PMI, Dec. ISM Mfg. Price Index, and Nov. JOLTs Job Openings (all at 10 a.m.), FOMC December Meeting Minutes (2 p.m.) and API Weekly Crude Stocks (4:30 p.m.). The major earnings reports scheduled for the day are limited to UNF before the open and then after the close, CALM reports.

In economic news later this week, on Thursday, Dec. ADP Nonfarm Employment Change, Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, Dec. S&P Global Services PMI, Dec. S&P Global Composite PMI, EIA Weekly Crude Oil Inventories, and the Fed Balance Sheet report. Finally, on Friday we get Dec. Avg. Hourly Earnings, Dec. Nonfarm Payrolls, Dec. Private Nonfarm Payrolls, Dec. Participation Rate, Dec. Unemployment Rate, Nov. Factory Orders, Dec. ISM Non-Mfg. Employment, and Dec. ISM Non-Mfg. PMI.

In terms of earnings reports later this week, on Thursday, we hear from CAG, LW, RDUS, RPM, and WBA. On Friday, GBX and STZ report.

In miscellaneous oil and gas news, the US was the world’s top LNG exporter in 2023, leapfrogging Qatar and Australia after the Freeport LNG terminal came back online. (The US had dropped out of the number one spot after Freeport in 2022.) US exports of LNG rose a whopping 14.7% on record gas production. Elsewhere, Bloomberg also reports that China has front-loaded its oil import quotas for 2024. Beijing has already granted permission for imports up to amounts that nearly equal all of 2023. This could lead to heavier than normal oil demand as traders try to take advantage of current lower oil prices…thereby also driving oil prices higher. (China has never issued a full year’s worth of import quotas in the past in one go. So, this may be a signal of certainty for the eyes of the Chinese economy.)

In US fiscal news, the Treasury Dept. reported that the gross national debt hit another record high, surpassing $34 trillion. (As a sidenote, a January 2020 estimate from the Congressional Budget Office had forecast that the US would reach this level of debt in 2029. So, we reached that level six and change years faster than expected. It is also interesting to note that total federal tax receipts as a percentage of GDP are down at about 16%. Of this, 67% comes from individuals, only 27% from corporations, and the rest from customs duties and excise taxes.)

With that background, it looks like Mr. Market favors the bears as the premarket session gapped a bit lower and has put in black-bodied candles in all three major index ETFs so far. DIA is just giving us a Bearish Harami and remains above its T-line (8ema) in the early session. However, both the QQQ and SPY are moving lower and threatening to take out the Tuesday low during the premarket. So, while the Bulls hold on to the longer-term daily trend, we are seeing a pullback in the SPY and QQQ as well as a consolidation in the DIA. With that said, the rally was in dire need of that rest or pullback to remain healthy as we sit very near all-time highs. In terms of extension, none of the three major index ETFs are extended at all from their T-lines. At the same time, the T2122 indicator remains in its mid-range. So, both the Bulls and Bears have room to run if they gather the momentum to do it, but the Bears should continue to be hungry given that the Bulls kept them from making any moves at all the last two months of 2023. Lastly, keep an eye on the Tech Big Dogs. If we are seeing a rotation out of those names (which have dragged markets along for a year or more), it will be hard for markets to do anything except retreat.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Iran Sends Destroyer to Red Sea

The last trading day of the year opened up flat on Friday. SPY opened 0.05% lower, DIA opened 0.04% lower, and QQQ opened dead flat. At that point, all three major index ETFs ground sideways in a very, very tight range the first hour before starting to sell off. SPY and DIA both reached their low of the day at 12:25 p.m. while did it faster by 11:35 a.m. Then all three traded sideways with a slightly bullish trend the entire rest of the day. This action gave us indecisive candles in all three. The SPY printed a black-bodied Spinning Top candle that retested and held above its T-line (8ema). DIA gave us a Doji that also retested its T-line and held above. Meanwhile, QQQ printed a large body, black-bodied Spinning Top that, again, also retested and held above its T-line.

On the day, eight of the 10 sectors were in the red with Technology (-0.66%) and Basic Materials (-0.62%) leading the way lower while Communications Services (+0.09%) and Consumer Defensive (+0.03%) being the only6 ones to hold above flat. At the same time, the SPY lost 0.29%, DIA lost 0.04%, and QQQ lost 0.43%. The VXX rose 0.26% to close at 15.52 and T2122 fell back into the midrange at 69.44. 10-year bond yields rose slightly to 3.866% and Oil (WTI) fell to close at $71.65 per barrel. So, the Bulls took the last day of the year off and the only move was some late-morning profit-taking and then drifting back toward flat.

That ended a very strong year for the stock markets. QQQ led the way higher with a huge gain of 53.79%. The SPY gained 24.29% on the year and DIA lagged the vast majority of the year, gaining 13.74%. All three major index ETFs remain very near all-time highs with QQQ and DIA having been at new all-time highs in the last few days and SPY just within a half of a percent. The US Dollar (UUP) fell 2.59% on the year, while Oil (USO) fell almost 5%. At the same time, 10-year bond yields (TNX—X) fell just 0.34% over the year.

The only economic news on Friday was December Chicago PMI, which came in lower than expected at 46.9 (compared to a forecast of 51.0 and the November reading of 55.8).

In stock news, NVDA launched a modified version of its advanced gaming 4090 chip specifically for the Chinese market. The new chip is five percent slower than the one that is banned for sale to China. Later, BA announced that all 737 MAX jets operated in China are back in service. This comes less than a week after BA announced it had made the first delivery of a 787 Dreamliner to a Chinese customer. At the same time, FSR announced it had delivered 4,700 electric vehicles (priced at $69,000) in 2023. Later, UNH announced it had agreed to sell its Brazilian operations for $515.24 million. Elsewhere, PFE, SNY, and TAK announced they plan to raise prices on 500 drugs in the US in what industry analysts say is a bargaining move aimed at stymying the Biden Administration negotiation of 10 high-cost drugs for Medicare. Later, CALM said it had agreed to buy a TSN chicken processing plant in Dexter, MO. CALM said it plans to convert the plant into an egg-grading facility. Finally, Bloomberg reports that X (formerly Twitter) is now worth less than one-third of what Elon Musk paid for the platform as advertising sales continue to plummet as right-wing Musk cannot manage to stop offending and then insulting large parts of society and advertisers in particular.

In stock government, legal, and regulatory news, GOOGL agreed to settle a $5 billion lawsuit that alleged the company secretly tracked the internet use of millions of people. The terms of the settlement were not made public but may be disclosed on the previously scheduled trial date of Feb. 24. (The lawsuit originally sought $5,000 per tracked user.) At the same time, the US Chemical Safety Board announced the findings of its long investigation of a 2020 CHK oil well explosion. The investigation found that CHK and its contractors failed to use adequate safety and control measures leading to the blast that killed three people. Elsewhere, a federal judge certified a shareholder class action lawsuit against JNJ Friday, saying the shareholders may pursue damages for JNJ allegedly fraudulently concealing how its talc products had been contaminated with cancer-causing asbestos for five years. Later, HSY was sued by an FL woman for their candies allegedly lacking the holiday details depicted in the candy’s artistic wrapper representations. At the same time, a federal judge ruled in favor of TEVA in its patent infringement lawsuit brought by CORT. Meanwhile, a US District Court upheld an FTC order preventing IQV from acquiring healthcare advertising firm DeepIntent. Later, JERT filed for Chapter 11 bankruptcy. At the same time, MCD sued a group promoting a boycott of Israeli interests in Muslim-majority Malaysia for $1.31 million, alleging the group had issued false and defamatory statements that hurt MCD operations in that country. Later, the FDA reported that RBGLY (Reckitt Mead Johnson) is voluntarily recalling batches of baby formula powder due to the possibility of contamination with bacteria. At the same time, BNPQY signed an agreement to pay $662.3 million in compensation for the misleading practices of its consumer lending unit in France. Finally, the Biden Administration is pressuring ASML to halt shipments of state-of-the-art deep ultraviolet chip lithography equipment to China. ASML agreed to be part of the sanctions set to take effect this month but had rushed to ship orders before the deadline. Now the Biden Administration is pressing hard to stop the last-minute shipments. (It is worth noting that China accounted for 75% of ASML’s Q3 sales.)

Overnight, Asian markets were mixed but leaned toward the downside. Thailand (+1.24%) was the big exception with South Korea (+0.55%) and Australia (+0.49%) rounding out the gainers. On the red side, Hong Kong (-1.52%), Shenzhen (-1.29%), and Taiwan and Shanghai (both -0.43%) led the region lower. In Europe, we see a much more evenly split leaderboard at midday. The CAC (-0.36%), DAX (-0.17%), and FTSE (-0.27%) lead nine bourses lower with six larger-moving bourses in the green in early afternoon trading. In the US, as of 7:30 a.m., Futures are pointing toward a red start to the year. The DIA implies a -0.46% open, the SPY is implying a -0.64% open, and the QQQ implies a -0.93% open at this hour. At the same time, 10-year bond yields have spiked back up to 3.959% and Oil (WTI) is surging up 2.36% to $73.34 per barrel in early trading.

The major economic news scheduled for Tuesday is limited to December S&P Global Manufacturing PMI (9:45 a.m.). There are no major earnings reports scheduled for either before the open or after the close.

In economic news later this week, on Wednesday, we get December ISM Mfg. Employment, Dec. ISM Mfg. PMI, Dec. ISM Mfg. Price Index, and Nov. JOLTs Job Openings and API Weekly Crude Stocks. Then Thursday, Dec. ADP Nonfarm Employment Change, Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, Dec. S&P Global Services PMI, Dec. S&P Global Composite PMI, EIA Weekly Crude Oil Inventories, and the Fed Balance Sheet report. Finally, on Friday we get Dec. Avg. Hourly Earnings, Dec. Nonfarm Payrolls, Dec. Private Nonfarm Payrolls, Dec. Participation Rate, Dec. Unemployment Rate, Nov. Factory Orders, Dec. ISM Non-Mfg. Employment, and Dec. ISM Non-Mfg. PMI.

In terms of earnings reports later this week, on Wednesday, UNF and CALM report. Then Thursday, we hear from CAG, LW, RDUS, RPM, and WBA. On Friday, GBX and STZ report.

In geopolitical news, in the Red Sea, US Navy shot down two anti-ship missiles fired by Yemeni Houthi rebels, which had been fired at an AMKAF (Maersk) ship Sunday. The Houthi then launched four small patrol boats to fire on the ship with small arms, but US Navy helicopters sank those boats, killing several rebels in that process. (Maersk paused Red Sea shipping after the attack despite no damage being suffered.) This Navy action is part of the US maintaining the safety of Suez-Red Sea shipping lanes while the Houthi try to stop any shipping that might aid Israel and draw attention to the Israeli war on Gaza. In a late-breaking development that has impacted oil prices, Iran has sent a destroyer to the Red Sea after the US action against its Yemeni allies.

In miscellaneous news, Supreme Court Chief Justice Roberts ignored the court’s ethics problems as well as all the massive legal decisions it faces ahead related to the ex-president. Instead, in his Sunday year-end note, Roberts focused on the pros and cons of AI technology. (Probably unrelated, this came just days after it was found that the ex-president’s legal team had used many fake AI-generated legal citations in their motions filed on his behalf in the last couple of months. Elsewhere, Chinese electric vehicle maker BYD announced it has produced more than 3 million new EVs in 2023. That very likely means it has again topped TSLA (which had produced 1.35 million in the first three quarters of 2023) as the global EV leader. In 2022, BYD outproduced TSLA by about half a million cars. BYD sold 3.02 million vehicles in 2023. Finally, in terms of starting the year off right, here are 1,000 good news stories you may have missed in 2023.

With that background, it looks like the news out of the Red Sea has markets scared that there could be further escalation of the Israeli-Hama war. All three major indes ETFs opened the premarket flat to modestly higher, but have sold off to form black-body candles that have crossed below the T-line in the SPY and QQQ and are retesting that level in the DIA. So, while the Bulls have held onto the daily trend for quite some time, this looks like a shock were the Bears will make a bid to take back control over the short-term trend. Sitting very near all-time highs, the Bulls retain control over the medium and longer-term trends. In terms of extension, none of the three major index ETFs were extended at all from their T-lines. At the same time, the T2122 indicator is now in its mid-range. So, both the Bulls and Bears have room to run if they gather the momentum to do it, but the Bears should be hungrier given that the Bulls have kept them from making any moves at all for two months.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Member e-Learning 12-21-23 – John

Member e-Learning 12-21-23 – Ed

Sharp Drop

Yesterday reminded us that bears still exist with the sharp drop at the end of the day that cascaded into traders running for the door to protect profits. Perhaps the quick selling also indicated an acknowledgment of the very overextended condition of the indexes as well as buyer exhaustion. Today as we run through a handful of notable earnings reports along with GDP, Jobless Claims, and the Philly Fed Mfg. numbers plan for an extra dose of price volatility due to the added uncertainty. Big point swings are possible and remember volumes could quickly decline as folks head out for holiday plans.

Asian markets closed the day mixed but mostly lower with the HSI and Shanghai recovering just slightly from the earlier selloff. However, European markets traded red across the board perhaps also recognizing the extended condition of the indexes. U.S. futures work to shake off yesterday’s selling indicating another gap up open trying to keep the exuberant buying spree going ahead of market-moving data. Buckle up it could be a wild morning of emotional price action.

Economic Calendar

Earnings Calendar

Notable reports for Thursday AIR, APOG, AVO, CCL, CTAS, NKE, & PAYX.

News & Technicals’

Citigroup, one of the largest banks in the world, is shutting down its global distressed-debt unit, according to CNBC. The unit, which traded bonds and loans of companies in financial trouble, was part of the bank’s markets division. The move is part of a broader restructuring plan by Citigroup’s CEO Jane Fraser, who took over in February. Fraser is aiming to improve the bank’s profitability and efficiency by exiting low-performing businesses and focusing on its core strengths.

Toyota, the world’s largest automaker, saw its shares drop sharply on Thursday after it announced a massive recall of about a million vehicles in the U.S. The recall affected certain 2020-2022 models of Toyota and Lexus, its luxury brand, due to a potential defect in the fuel pump that could cause the engine to stall. The recall was the latest in a series of quality issues that have plagued Toyota in recent years, denting its reputation for reliability and safety.

China has announced that it will impose tariffs on 12 chemical compounds imported from Taiwan, starting from Jan. 1, 2024. The move is seen as a punitive measure against Taiwan, which Beijing accuses of breaching a trade agreement. The affected chemical compounds include vinyl chloride, dodecyl benzene, and ethylene-propylene copolymer, which are used in…

The U.S. military said it intercepted 14 drones that were launched by the Houthi rebels from Yemen in the Red Sea over the weekend. The drones were part of a coordinated attack on shipping lanes in the strategic waterway, which connects the Mediterranean Sea and the Indian Ocean. The attack prompted many tankers and cargo ships to avoid the Suez Canal, which is the shortest route between Europe and Asia, and take the longer and more costly route around Africa. The Houthi rebels, who are backed by Iran, have threatened to target Israeli ships and any ships that are linked to Israel, in response to Israel’s war with Hamas in Gaza.

U.S. stocks ended Wednesday with a sharp drop as traders ran for the door in unison to protect profits in this very extended market condition. The S&P lost 1.5% and the Dow fell 476 points. The decline began with no trigger other than perhaps some exhaustion after the strong rally in the past few weeks. As a result, traders should plan for an extra dose of price volatility that could create some big point whips due to the uncertainty. Expect the GDP, Jobless Claims, and Philly Fed data to add to this morning’s emotional price sensitivity as well as the handful of notable earnings. Keep in mind after the reaction to data volume could decline into a choppy afternoon as traders extend holiday plans.

Trade Wisely,

Doug