DIA futures rose by 36 points, or approximately 0.1%, while S&P 500 and Nasdaq 100 futures also saw gains of 0.1% as the small cap rotation continues. This follows a strong performance on Monday, where the Dow advanced to record levels, and both the S&P 500 and Nasdaq posted gains. However, the rally has quickly become very extended with the T20 indicators suggesting the odds of a little rest or pullback have grown.

By 11:17 a.m. London time, the pan-European Stoxx 600 had declined by 0.39%, with all sectors and major bourses experiencing losses. Mining stocks were the hardest hit, dropping 1.89%, followed by the insurance sector, which fell by 1.12%.

Asia-Pacific markets exhibited mixed performance on Tuesday, influenced by a series of political and economic updates from the United States. Investors are also keenly observing China’s Third Plenum, where discussions are expected to focus on addressing high local government debt and promoting advanced manufacturing.

Economic Calendar

Earnings Calendar

Notable reports for Tuesday before the bell include BAC, MS, PNC, PGR, STT, & UNH. After the bell include FULT, HWC, IBKR, JBHT, OMC, & PNFP.

News & Technicals’

President Biden expressed regret over his use of the phrase “put Trump in the bulls-eye,” which he mentioned to donors in a private call shortly before an attempted assassination of Donald Trump. Several Republican lawmakers have criticized Democratic campaign rhetoric, including Biden’s comment, for potentially inciting the incident. Biden clarified that he has never intended to incite political violence, emphasizing what he perceives as a stark contrast to Trump’s approach.

Apple has unveiled a preview version of its upcoming iPhone update, iOS 18. This beta version, available ahead of the official fall release, allows Apple enthusiasts and developers to explore and test the latest features. Notably, this year’s most significant new service, Apple Intelligence, is not included in the public beta. Apple has announced that users will have the opportunity to try out Apple Intelligence later this summer, adding to the anticipation surrounding the new update.

Federal Reserve Chair Jerome Powell highlighted that central bank policy operates with “long and variable lags,” explaining why the Fed would not wait for its inflation target to be fully achieved before taking action. Powell emphasized that the central bank seeks “greater confidence” that inflation will return to the 2% level. The Fed’s next policy meeting is scheduled for the end of July, where further decisions on monetary policy will be discussed.

As tech tensions between the U.S. and China escalate, vast networks of underwater cables have emerged as a new point of contention in international relations. These subsea cables, which carry 99% of the world’s data traffic, are crucial to the global internet infrastructure. The U.S. government has reportedly cautioned tech giants like Google and Meta about the potential vulnerability of undersea cables in the Pacific to Chinese espionage. This development underscores the growing complexities and security concerns in the digital age.

As we ramp up in earnings expect price volatility to continue to expand and the small cap rotation to continue. Keep in mind we have a major distraction over the next two days due to Prime day shopping events across many retailers. This at times create choppy market conditions so plan accordingly.

Markets jumped higher to start the week. SPY gapped up 0.37%, DIA gapped up 0.57%, and QQQ gapped up 0.40% to start the day. From there, SPY and QQQ rallied steadily to follow-through and reach the highs of the day at about 11:25 a.m. After that, both sold back off steadily into the gap again at 2:15 p.m. At that point, both SPY and QQQ made a modest rally back above the opening level before selling sharply the last 30 minutes of the day. Meanwhile, after its gap higher, DIA sold off for 30 minutes before following the two broader major market index ETFs higher until noon. Then it followed the others, selling back into the gap and reaching the lows at 1:40 p.m. before rallying back above the open. DIA finally got in-sync with its broader brothers selling off hard the last 30 minutes of the day. This back-and-forth action gave us indecisive, black-bodied Doji candles in all three major index ETFs. SPY and DIA both printed new all-time highs and new all-time high closes. QQQ retested its T-line (8ema) from above and passed the test.

On the day, the 10 sectors were split evenly Monday with five in the green and five in the red. Financial Services (+1.35%), Energy (+1.19%), and Industrials (+1.12%) led the gainers while Utilities (-1.99%) was by far (by more than 1.20%) paced the losers. At the same time, SPY gained 0.28%, DIA gained 0.51%, and QQQ gained 0.27%. (It is worth noting that for the third day in a row, IWM (+1.90%) was well out in front of the three major index ETFs. VXX gained 1.48% to close at a still extremely low at 10.31. T2122 fell just a bit again, but remains in the top end of its overbought territory at 95.61. On the bond front, 10-year bond yields popped to 4.23% and Oil (WTI) fell just a bit to close at $81.92 per barrel. So, Monday was the volatile day where markets all gapped higher, rallied to the highs in the morning, sold off to the lows in the afternoon only to bounce the last few minutes. This happened on above-average volume in DIA, average volume in the QQQ, and below-average volume in the SPY.

The major economic news scheduled for Monday was limited to NY Empire State Mfg. Index, which came in slightly lower than expected at -6.60. Compare this to a forecast of -5.50 and the June reading of -6.00.

In economic speak news, on Monday, Fed Chair Powell indicated that the recent CPI data had boosted FOMC confidence that inflation is falling. When asked about Fed confidence, Powell said, “What increases that confidence in that is more good inflation data, and lately here we have been getting some of that.” Powell went on to say that he does not expect the Fed to wait until inflation reaches the 2% target before cutting rates, because that could undercut economic expansion. He said, “The implication of that is that if you wait until inflation gets all the way down to 2%, you’ve probably waited too long.” Powell was also questioned about whether he will serve out his term, given the questioning of FOMC policies during his tenure. Powell bluntly answered “Yes” (indicating he will serve his entire term). Later, San Francisco Fed President Daly echoed Powell’s remarks on confidence. She said, “Confidence is growing that we are getting nearer a sustainable pace of getting inflation back down to 2%.” She continued, “I’m not going to tell you when the rate cut is, how many rate cuts might come,” … “Over time, as inflation comes down and the labor market slows, we have to make sure that we’re holding rates high enough that we don’t lose that inflation fight, but not hold them too long and risk worsening the labor market to a point where it’s challenging for people to get jobs.”

In stock news, on Monday, CLF announced it is acquiring Canadian steel company Stelco for $2.5 billion. At the same time, SEDG announced it would lay off 400 (7% of workforce) employees in Israel as it tries to improve profitability. Later, M announced it had ended acquisition talks with two private equity firms. (The talks had been ongoing for months.) After the close, the Wall Street Journal reported that a “hacktivist” group (Nullbulge) has obtained and leaked data from DIS’s internal communication system. The released data included everything from computer code, to excerpts from financial reports, to assessments of job candidates, to photos of employee dogs. At the same time, GM declined to reiterate its 2025 forecast of producing 1 million electric vehicles.

In stock legal and governmental news, on Monday, the French competition authority confirmed that it is investigating NVDA related to “anti-competitive practices.” At the same time, UBER lost an appeal of its lower court victory (which had ruled UBER rival taxi operators would be charged a 20% tax on profits). Later, PYPL was fined $27.3 million by the Polish antitrust agency for failing to spell out which activities may cause consumers to be fined (ambiguous contract fine print). At the same time, VRTX sued the US Dept. of HHS, seeking a court declaration that the company’s financial support for some patients does not violate US anti-kickback laws.

Overnight, Asian markets had seven of 12 exchanges in the green. However, Hong Kong (-1.60%) was the biggest mover while Shenzhen (+0.86%) led the gainers. In Europe, the bourses lean heavily to the red side at midday with 12 of 15 exchanges in the red. The CAC (-0.79%), DAX (-0.48%), and FTSE (-0.29%) are leading the region lower in early afternoon trade. Russia (+1.39%) is again an outlier. Meanwhile, in the US, as of 7:15 a.m., Futures are pointing to a modestly green start to the day. The DIA implies a -0.10% open, the SPY is implying a +0.15% open, and the QQQ implies a +0.21% open at this hour. At the same time, 10-Year bond yields are down sharply to 4.18% and Oil (WTI) is off just over one percent to $80.94 per barrel in early trading.

The major economic news scheduled for Tuesday includes June Import Price Index, June Export Price Index, June Core Retail Sales, and June Retail Sales (all at 8:30 a.m.), May Business Inventories and May Retail Inventories (both at 10 a.m.), and API Weekly Crude Oil Stocks report (4:30 p.m.). The major earnings reports before the open include BAC, SCHW, MS, PNC, PGR, STT, and UNH. Then, after the close, IBKR, JBHT, and OMC report.

In economic news later this week, on Wednesday, June Building Permits, June Housing Starts, June Industrial Production, EIA Crude Oil Inventories, and Fed Beige Book are reported. Fed Governor Waller also speaks. Then Thursday, we get Weekly, Initial Jobless Claims, Weekly Continuing Jobless Claims, Philly Fed Mfg. Index, US Leading Economic Indicators Index, Fed’s Balance Sheet. We also hear from Fed member Daly and Fed Governor Bowman. Finally, on Friday, Fed members Williams and Bostic speak.

In terms of earnings reports later this week, on Wednesday, ALLY, ASML, CFG, ELV, FHN, JNJ, NTRS, PLD, SYF, USB, AA, CCI, DFS, EFX, KMI, LBRT, STLD, SNV, UAL, and WTFC report. On Thursday, ABT, ALK, BX, CTAS, CHI, DPZ, HXL, INFY, KEY, MTB, MAN, MMC, NOK, NVS, SNA, TSM, TXT, AIR, ISRG, NFLX, PPG, and SCHL report. Finally, on Friday, AXP, ALV, CMA, EEFT, FITB, HAL, HBAN, RF, SDVKY, SLB, TRV, and WIT report.

So far this morning, BAC and UNH have reported beats on both their revenue and earnings lines. Meanwhile, PNC missed on revenue while beating significantly on the earnings line. (SCHW, MS, PGR, and STT report closer to the opening bell.)

In miscellaneous news, Reuters reported Monday that the cost to transport a standard 40-foot shipping container from Shanghai to New York is pushing $10k ($9,387). This is more than double the rate in February but still well below the early pandemic high of almost $16k. The increase in costs is mostly attributed to attacks from Yemeni Houthi rebels (which have caused longer routes around the horn of Africa). This increase in shipping costs will either pressure company margins, contribute to inflation, or both as the Israeli invasion of Gaza shows no signs of an Israeli withdrawal yet. Elsewhere, the CDC sent a field team to CO to help the state deal with an outbreak of bird flu after four confirmed cases and a fifth suspected case were reported. (Based on current information, the CDC said it believes the risk to people in the public are low. However, farm workers and livestock herds are at significant risk.) Meanwhile, Bolivia announced the discovery of the largest natural gas field found since 2005. The single 1.7 trillion cubic feet field (located in northern Bolivia) is about 17.5% the size of the total US natural gas reserves. (However, bear in mind that it will take years to develop the field and build the infrastructure to transport the natural gas to global markets from the land-locked nation.)

With that background, it looks as if the SPY and QQQ are bullish again this morning while DIA is much more undecided. SPY and QQQ both opened the premarket slightly lower, but have put in white-bodied candles with only lower wick since that point. Meanwhile, DIA also opened slightly lower and also ran higher before backing down again to have a high-wick, Doji candle at this point. All three major index ETFs remain above their T-line (8ema). So, regardless of your timeframe, the market trend (short-term, mid-term, or longer-term) remains very bullish. In terms of extension, DIA remains the only one of the three that can be said to be stretched above its T-line. However, the T2122 indicator still remains in the top end of its overbought range. Therefore, the market may be in need of some rest or a pullback. With regard to those 10 big dog tickers, nine of the 10 are in the green this morning. TSLA (+1.29%) is again the biggest mover and also leading the market in premarket dollar volume traded. Only MSFT (-0.02%) is below break-even among those market-moving stocks.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Stock futures gap higher as the bulls continue to run after investors assessed the implications of the assassination attempt on former President Donald Trump and prepared for a significant week of corporate earnings reports. The Dow Jones Industrial Average futures increased by 204 points, or 0.51%, while S&P 500 futures rose by 0.43%, and Nasdaq 100 futures gained 0.5%. This uptick reflects cautious optimism in the market despite the political turmoil.

European declined to begin the week by 0.12%, with all major indexes and most sectors experiencing losses. Utilities were the hardest hit, dropping 0.91%, while basic resources followed closely with a 0.83% decrease. This broad-based downturn reflects widespread market challenges across Europe.

China’s economy experienced a growth rate of 4.7% in the second quarter, falling short of the 5.1% expansion forecast by Reuters and marking a decline from the 5.3% growth recorded in the first quarter. Meanwhile, Australia’s S&P/ASX 200 index achieved a historic milestone by surpassing the 8,000 mark for the first time, closing at 8,017.6 with a 0.73% increase.

Economic Calendar

Earnings Calendar

Notable reports for Tuesday before the bell include BLK, & GS. After the bell include CFB, FBK, & SFBS.

News & Technicals’

Goldman Sachs is set to release its second-quarter earnings before the market opens on Monday. Analysts surveyed by LSEG anticipate earnings per share of $8.34 and revenue of $12.46 billion. Following the earnings release, company executives will hold a call with analysts at 9:30 a.m. ET to discuss the results and provide further insights into the financial performance and outlook.

Google is reportedly in advanced negotiations to acquire the cybersecurity firm Wiz for $23 billion, according to sources cited by The Wall Street Journal. If finalized, this acquisition would mark Google’s largest ever, underscoring its strategic push into the cybersecurity sector. The deal is expected to be completed soon, reflecting Google’s commitment to enhancing its security capabilities amid growing digital threats.

Burberry announced that if the current trading slowdown persists, it anticipates an operating loss for the first half of the year and a full-year operating profit below the current consensus. As a result, shares of the 168-year-old British luxury brand plummeted by 15.4% as of 9:54 a.m. London time. In response to these challenges, the company suspended its dividend and appointed Joshua Schulman, formerly of Michael Kors and Coach, as the new CEO, with Jonathan Akeroyd stepping down immediately.

Swatch Group reported a significant decline in first-half sales and earnings on Monday, attributing the downturn to weaker demand for luxury goods in China, including Hong Kong and Macau. Despite the overall slump, the Swatch brand managed to defy the trend, achieving a 10% increase in sales in China. This performance highlights the brand’s resilience amid challenging market conditions, even as the broader company faces headwinds in one of its key markets.

As we look ahead to a busy week as the earnings season ramps up the bulls continue to run pointing to a substantial gap up open. Gapping to new record highs can create some big point whipsaws so plan your risk accordingly. Expect volatility to increase over the next several weeks as the market reacts to all the earnings data coming our way.

The Bears just couldn’t stand their success from the day prior and let the Bulls run on Friday. SPY gapped up 0.23%, DIA gapped up 0.30%, and QQQ opened up by 0.12%. From there, all three major index ETFs rallied sharply until 11:30, took a one-hour rest and then rallied again to the highs of the day at 1:55 p.m. At that point, we saw very modest profit-taking and a sideways grind until 3:30 p.m. However, traders took profits hard the last 30 minutes, giving back half or more of the day’s gains. This action gave us gap-up, white-bodied candles in all three with large upper wicks. SPY and QQQ printed Bullish Harami candles with QQQ crossing back above its T-line (8ema). SPY also printed another new all-time high. Meanwhile, DIA also printed a new all-time high and new all-time high close. This happened on well above-average volume in DIA, as well as just below-average volume in the SPY and QQQ.

On the day, all 10 sectors were in the green with Consumer Cyclical (+1.17%) out in front leading the rest of the sectors higher. Meanwhile, Energy (+0.31%) was the laggard sector. At the same time, SPY gained 0.61%, DIA gained 0.68%, and QQQ gained 0.59%. VXX fell 1.74% to close at an extremely low at 10.16. T2122 fell just a bit to remain in the top end of its overbought territory at 96.34. On the bond front, 10-year bond yields dropped to 4.181% and Oil (WTI) was down almost half a percent to close at $82.24 per barrel. So, Friday was the Bull’s day all day with significant profit-taking the last 30 minutes giving back a fair amount of the daily gains. It is worth noting that INTC (+2.96%), IBM (+2.55%), and AMGN (+1.77%) led the DIA to its new all-time highs…but it was a broad-based move with 22 of the 30 DIA tickers in the green. Meanwhile, 401 of 501 of the SPY were green and 81 of 101 of the QQQ were above break-even.

The major economic news scheduled for Friday included June Core PPI, which came in hotter than expected at +0.4% (compared to a +0.2% forecast and May’s +0.3%). This led to a June PPI of +0.2% (versus a forecasted +0.1% and May’s 0.0% value). Later, Preliminary July Michigan Consumer Sentiment was lower than predicted at 66.0 (compared to the 68.5 forecasted and June’s 68.2 reading). At the same time, the July Preliminary Michigan Consumer Expectations were also lower than anticipated at 67.2 (versus the 69.8 forecast and June’s 69.6 value). On the forward-outlook side, the July Michigan 1-Year Inflation Expectations were 2.9% (in-line with the forecast and a tick better than June’s 3.0% number). In the longer term, July’s Michigan 5-Year Inflation Expectations were better than predicted, also at 2.9% (versus a 3.0% estimate and June reading).

The US Dept. of Agriculture WASDE report also came out Friday. It raised estimates for US corn production and reduced the soybean production estimate. (Forecasts of large US crops in both have pushed both commodity prices down since the Spring. The USDA also lowered its US national corn inventory (not growing, in storage) estimate by 8.4% from June. (This could mean short-term prices may increase, which is what Friday’s market saw.)

In stock news, on Friday, LUV and ACHR announced they have agreed to mutually develop operational plans for electric air taxis in CA and TX airports. At the same time, Reuters reported exclusively that EADSY (Airbus) has launched a cost cutting program that includes a headcount freeze aimed tackling a problem with increased per jet cost of production. (No layoff plans were reported, but “all costs” were on the table per the article.) Meanwhile, the Financial Times reported that UL is planning massive layoffs in Europe, with layoffs of a third of officer workers (roughly 3,200) taking place between now and the end of 2025. Later, T announced (after an SEC filing revealed) that it had suffered a massive hack, losing data from 109 million customer accounts (nearly all of its cellular or landline customers) text and calls from six months in 2022. (The FBI is investigating and at least on person has been arrested so far.) After the close, Reuters reported that BHP and LUNMF are in talks about making a joint bid for copper miner FLMMF. Then, on Sunday, the Wall Street Journal reported that GOOGL is near to striking a deal to acquire cybersecurity firm Wiz for roughly $23 billion. (If completed, it would be GOOGL’s largest acquisition ever.)

In stock legal and governmental news, on Friday, India’s antitrust regulator said AAPL exploited its position in the app market. Later, Reuters reported that BG and GLNCY (Glencore)-backed Viterra have offered to sell off their assets in two EU countries in order to get European Commission approval of their $34 billion merger. At the same time, a US District Court of Appeals rejected appeals made by DISH and an amateur astronomer group, upholding the lower-court decision in favor for FCC approval for SpaceX to deploy thousands (up to 7,500) of Starlink satellites. Later, C asked a judge to dismiss a conservative racial discrimination lawsuit that alleged the bank violated civil rights law by waiving ATM fees for customers of minority-owned banks. At the same time, Bloomberg reported that federal prosecutors are investigating ABR over allegations (that were made by short sellers) of lending practices and financial disclosures. Later, a US Appeals Court has temporarily put the FCC’s reinstatement of net neutrality rules on hold until August 5. The court will consider appeals by the telco companies. (The rule which was set to go back into effect July 22 requires internet service providers to treat all network traffic equally, rather than throttling some and charging higher rates for certain types of traffic.) At the same time, a NY Federal Judge ruled AMZN must comply with an EEOC subpoena related to its investigation into allegations that company discriminated against pregnant workers.

Overnight, Asian markets were evenly mixed, but the biggest movers were to the red side. Japan (-2.45%) and Hong Kong (-1.52%) led half of the region lower. In Europe, the bourses are much more bearish with only four of 15 exchanges in the green at midday. Russia (+1.39%) is a notable outlier. The CAC (-.044%), DAX (-0.21%), and FTSE (-0.23%) are leading the region lower in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a gap higher. The DIA implies a +0.56% open, the SPY is implying a +0.43% open, and the QQQ implies a +0.49% open at this hour. At the same time, 10-Year bond yields are up to 4.221% and Oil (WTI) is off slightly to $82.13 per barrel in early trading.

The major economic news scheduled for Monday is limited to NY Empire State Mfg. Index (8:30 a.m.). However, Fed Chair Powell speaks at noon and Fed member Daly speaks at 4:35 p.m. The major earnings reports before the open include BLK and GS. Then, after the close, there are no major reports scheduled.

In economic news later this week, on Tuesday we get June Import Price Index, June Export Price Index, June Core Retail Sales, June Retail Sales, May Business Inventories, May Retail Inventories, and API Weekly Crude Oil Stocks report. On Wednesday, June Building Permits, June Housing Starts, June Industrial Production, EIA Crude Oil Inventories, and Fed Beige Book are reported. Fed Governor Waller also speaks. Then Thursday, we get Weekly, Initial Jobless Claims, Weekly Continuing Jobless Claims, Philly Fed Mfg. Index, US Leading Economic Indicators Index, Fed’s Balance Sheet. We also hear from Fed member Daly and Fed Governor Bowman. Finally, on Friday, Fed members Williams and Bostic speak.

In terms of earnings reports later this week, on Tuesday we hear from BAC, SCHW, MS, PNC, PGR, STT, UNH, IBKR, JBHT, and OMC. Then Wednesday, ALLY, ASML, CFG, ELV, FHN, JNJ, NTRS, PLD, SYF, USB, AA, CCI, DFS, EFX, KMI, LBRT, STLD, SNV, UAL, and WTFC report. On Thursday, ABT, ALK, BX, CTAS, CHI, DPZ, HXL, INFY, KEY, MTB, MAN, MMC, NOK, NVS, SNA, TSM, TXT, AIR, ISRG, NFLX, PPG, and SCHL report. Finally, on Friday, AXP, ALV, CMA, EEFT, FITB, HAL, HBAN, RF, SDVKY, SLB, TRV, and WIT report.

So far this morning, GS reported beats on both the revenue and earnings lines. BLK missed on revenue while beating handily on earnings.

In miscellaneous news, Reuters reported that rating agencies (MCO and Fitch) said Friday that office and other commercial real estate loan delinquencies ticked up in June. The report said that overall commercial mortgage-backed loans delinquency rate rose to 2.45% (from 2.42% in May). (This is the rate of loans with payments at least 30-days in arrears.) Elsewhere, Israeli PM Netanyahu reversed (reneged) on a previous major point in ceasefire negotiations with Hamas. Israel now says it demands to control the flow of Palestinians back to the North during any ceasefire versus a prior concession of “free Palestinian movement” during a ceasefire. This essentially ended the talks for now as Netanyahu tries to shore up his extreme right-wing alliances. On Sunday, CNP (the main electric provider in the Houston area) said half a million residences and businesses remain without power going into the new week.

In way too early earnings season news, Friday saw the early reporting big bank stocks punished, despite all of them reporting beats versus consensus estimate. For example, WFC closed down 6.02%, C down 1.81%, and JPM down 1.21%. Some analysts attributed this to the constituent details of the reports. (For instance, WFC reported less interest income than expected although it did beat over overall revenue estimates by $440 million.) Other analysts said they believed it had to do with forward outlook such as JPM’s Jamie Dimon warning that inflation and interest rates may stay higher than the market expects and may hurt the overall economy. However, still others said it was pure profit-taking. Whatever the reason, it was worth noting that only Energy underperformed the Financial Services sector on Friday, despite reports that were good at first glance.

With that background, it looks as if the Bulls want to run this morning. All three major index ETFs gapped higher to start the premarket and have printed white-body candles with no wicks since that start. DIA is testing Friday’s all-time high again in the early session. All three remain above their T-line (8ema). So, regardless of your timeframe, the market trend (short-term, mid-term, or longer-term) remains very bullish. In terms of extension, DIA is now the only one of the three major index ETFs stretched above its T-line. However, the T2122 indicator is in the top end of its overbought range. Therefore, the market may be in need of some rest or a pullback. With regard to those 10 big dog tickers, eight of the 10 are in the green this morning. TSLA (+4.07%) is the biggest mover and also leading the market in premarket volume. Only MSFT (-0.12%) and META (-0.21%) are below break-even among those market-moving stocks.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Thursday was a profit-taking day in the markets. After, good CPI data, SPY opened +0.02%, DIA opened +0.09%, and QQQ opened +0.06%. However, at that point we saw divergence with the broader SPY and QQQ selling off briskly before bobbling near the lows to close out the say. Meanwhile, DIA rallied and sold off and meandered sideways in positive territory the rest of the day. This action gave us large, black-body Bearish Engulfing candles in the SPY and QQQ. QQQ also crossed back below its T-line (8ema) for the first time in nine days. (SPY did print another all-time high, but not all-time high close.) At the same time, DIA printed a modest gap-up, large-legged Doji. This happened on above-average volume in QQQ and DIA, as well as modestly below-average volume in the SPY.

On the day, nine of the 10 sectors were in the green with Basic Materials (+2.07%) out in front leading almost all of the rest of the sectors higher. Meanwhile, Technology (-1.34%) was by far (by more than 1.80%) the weakest sector as we may have seen some rotation out of the big dog tech names that have led the market for a long, long time. At the same time, SPY lost 0.86%, DIA gained 0.09%, and QQQ lost 2.19%. VXX gained a little most than half a percent to close at a still extremely low at 10.34. T2122 spiked for the second-straight day into extreme overbought territory at 97.97. On the bond front, 10-year bond yields were down again to 4.207% and Oil (WTI) gained 1.08% to close at $83.00 per barrel. So, Thursday was a major profit-taking day or rotation on good CPI news. (Perhaps traders think the CPI data foreshadows a rate cut and/or change in economic cycle position.) Regardless of the cause, all 10 of the big dog names were down more than 1% for the day, led by TSLA (-8.44%), NVDA (-5.57%), and META (-4.11%).

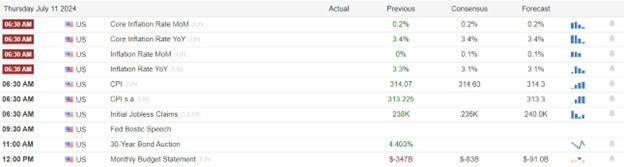

The major economic news scheduled for Thursday included June Core CPI (month-on-month), which fell and was below expectations at +0.1% (compared to a forecast and May reading of +0.2%). On a Year-on-Year basis, June Core CPI was also down at +3.3% (versus a forecast and May value of +3.4%). On the headline number, June CPI (month-on-month) actually fell and was below predictions at -0.1% (compared to a forecast of +0.1% and a May reading of 0.0%). On the Year-on-Year basis, June CPI was also down and below what was anticipated at +3.0% (versus a +3.1% forecast and a May +3.3% number). At the same time, Weekly Initial Jobless Claims were notably down at 222k (compared to a 236k forecast and a 239k previous week reading). For the Weekly Continuing Jobless Claims, number was also down at 1,852k (versus a 1,860k forecast and the prior week’s 1,856k value). Later, the June Federal Budget Balance was a bit better than expected at -$66.0 billion (compared to a forecast of -$71.2 billion and drastically down from May’s -$347.0 billion). Then, after the close, the Weekly Fed Balance Sheet showed a modest increase of $2 billion at $7.224 trillion (versus the prior week $7.222 trillion).

In economic speak news, on Thursday, San Francisco Fed President said that the recent better inflation data area relief. She said, “With the information we have received today, which includes data on employment, inflation, GDP growth, and the outlook for the economy, I see it as likely that policy adjustments, some policy adjustments, will be warranted.” At the same time, St. Louis Fed President Musalem indicated that Thursday/s CPI data was encouraging. He said, “The June Consumer Price Index points to encouraging further progress toward lower inflation.” Later, Chicago Fed President Goolsbee told a group interview, “My view is, this is what the path to 2% looks like.” He also indicated yesterday’s report was “excellent news” that indicate the stronger than expected May CPI data was just “a bump in the road.” He went on to say, “The reason to be as restrictive as that and the reason to tighten in real terms would be if you thought the economy was overheating. This is not in my view what an overheating economy looks like.”

In stock news, on Thursday, MSTR announced it will undergo a 10-for-1 split for the holders of record on August 1. Later, PFE announced it will move ahead with a pill form of its GLP-1 weight loss drug. This comes after a 20-person study showed concerns over side effects from the pills. At the same time, RTX was awarded a $1.2 billion contract to provide additional Patriot missile systems to Germany. Later, QS said it has signed a strategic partnership with VLKAF (Volkswagen) to develop new battery technologies. (QS closed up 30.50% on the day on this news.) At the same time, BCSF announced it will buy ENV for $4.5 billion. Later, IBATF announced it has become the first company to commercialize a lithium extraction technology, selling a license to its filtration technology to private miner US Magnesium. (Beating RIO and SLI to this milestone.) At the same time, GM announced plants to invest $900 million to retool an MI plant to build electric vehicles. Meanwhile, Bloomberg reported that TSLA will delay the launch of its robotaxis until October. (This was yet another delay from the previously announced August 8 unveiling.)

In stock legal and governmental news, on Thursday, the EU antitrust regulator said AAPL has agreed to open its “tap-and-go” payments system to rivals in order to avoid sanctions under one of three ongoing EU antitrust investigations of the company. This came even as the head of the agency said “so far is that we have not seen a change in behavior on Apple’s side when it comes to our preliminary findings.” Later, the Dept. of Energy awarded GM and STLA nearly $1.1 billion in grants to build electric vehicles and components. Meanwhile, CVX and HES announced they expect the FTC to review their proposed merger in Q3. (This announcement came after Bloomberg reported the FTC would delay its decision on the merger until Q4.) At the same time, the EPA and Dept. of Justice announced MRO had agreed to a $241 million settlement (including a $64 million fine) for violations of the Clean Air Act. Later, DG agreed to pay a $12 million penalty to the Dept. of Labor for alleged safety violations.

Overnight, Asian markets were mixed but leaned toward the green side. Hong Kong (+2.59%) was by far the biggest gainer. Meanwhile, Japan (-2.45%) and Taiwan (-1.94%) were by far the biggest losers, following Thursday’s US Tech selloff. In Europe, we see mostly green at midday. The CAC (+0.69%), DAX (+0.41%), and FTSE (+0.31%) lead the region higher in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a mixed, flat start to the morning. The DIA implies a +0.09% open, the SPY is implying a +0.01% open, and the QQQ implies a -0.09% open at this hour. At the same time, 10-Year bond yields are back up a bit to 4.217% and Oil (WTI) is up almost another percent to $83.37 per barrel on hopes for economic stimulus from the Fed.

The major economic news scheduled for Friday include June Core PPI and June PPI (both at 8:30 a.m.), Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-Year Inflation Expectations, and Michigan 5-Year Inflation Expectations (all at 10 a.m.), and the WASDE Ag report (noon). The major earnings reports before the open include BK, C, ERIC, FAST, JPM, and WFC. However, there are no major reports scheduled for after the close.

In miscellaneous news, following Thursday’s CPI data, the CME Fedwatch tool shows that 8.8% of fed fund futures trades expect a rate cut at the July 31 meeting, but 91.2% expect no cut. However, for the September 18 meeting, Fed Fund futures indicate a 92.7% probability of a rate cut. Elsewhere, more than 1.2 million residences and businesses remain without power in South TX following hurricane Beryl and officials said 500k will remain without power into next week. Finally, the EU said early Friday that Elon Musk’s former Twitter deceives users and breaches EU online content rules. If confirmed, X (Twitter) could face a fine up to 6% of global annual turnover.

So far this morning, BK, JPM, and WFC all reported beats (easily) on both the revenue and earnings lines. Meanwhile, FAST missed slightly on revenue while coming in in-line of earnings. On the other side, ERIC beat easily on revenue while missing on the earnings line. (C reports at 8 a.m.)

With that background, it looks as if markets have all moved modestly, but indecisively bullish in the premarket. SPY and DIA are printing Doji in the early session while QQQ has put in a white-body candle that recovered from a premarket opening gap lower. The SPY and DIA remain above their T-line (8ema) while QQQ seems just about ready to retest its own T-line from below this morning. So, regardless of your timeframe, the market trend (short-term, mid-term, or longer-term) remains very bullish despite yesterday’s big black candle. In terms of extension, DIA is now the only one of the three major index ETFs stretched above its T-line. However, the T2122 indicator is in the top end of its overbought range. Therefore, oddly after yesterday’s candle, the market may be in need of more rest or a pullback. With regard to those 10 big dog tickers, they are split 50-50 this morning with 5 in the green and 5 in the red. META (-1.76%) is the biggest mover while TSLA (-0.91%) has traded the most dollar volume in the early session. NVDA (+0.49%) is just behind TSLA in dollar-volume this morning.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

U.S. stock futures edged slightly lower early Thursday, with a cautious stance as traders as braced for the inflation report. The high anticipation centers around the June consumer price index and the ramifications it will have on future interest rate decisions. Economists polled by Dow Jones have set their expectations for a modest increase of 0.1% month-over-month. On an annual basis, the CPI is projected to rise by 3.1% compared to the same period last year.

European markets rallied Thursday morning, with indices across the region climbing as investors anticipate the forthcoming U.S. inflation data. The upbeat mood was bolstered by flash figures indicating that the U.K. economy expanded by 0.4% in May, a welcome recovery following a stagnant April and surpassing the modest 0.2% growth anticipated by analysts. This economic uptick was mirrored in the currency market, where the British pound appreciated by 0.21%, reaching its highest valuation against the U.S. dollar in the past four months.

The Japanese market saw significant gains, with the Nikkei 225 index climbing 0.94% to close at 42,224.02. This surge was largely attributed to a strong performance by technology stocks. Similarly, the broader Topix index also rallied, rising 0.69% to reach a new peak of 2,929.17. South Korea, the Kospi index increased by 0.75%, as the Bank of Korea maintained its interest rate at 3.5%. The tech-centric Kosdaq index modestly rose by 0.11%.

Economic Calendar

Earnings Calendar

Notable reports for Tuesday before the bell include DAL, & PEP. After the bell we have no notable reports.

News & Technicals’

PepsiCo’s financial performance in the second quarter presented a mixed picture, as the company fell short of Wall Street’s revenue expectations. This shortfall was primarily due to a decrease in volume across its three North American business units. In light of these results, PepsiCo has adopted a more conservative stance regarding its sales forecast for the entire year, signaling a cautious approach amid uncertain market conditions. Despite the revenue setback, the company managed to surpass earnings estimates for the quarter, indicating that while sales volume may have declined, profitability metrics and cost management strategies could have yielded better-than-expected outcomes. This divergence between revenue and earnings highlights the complex challenges and operational efficiencies within PepsiCo’s business operations.

The U.S. Treasury Department and the Internal Revenue Service (IRS) have reported a significant milestone in tax collection efforts, having recovered over $1 billion in tax debt from high-income individuals in the past year. This achievement underscores the government’s intensified focus on ensuring tax compliance among the wealthy. In a strategic move to bolster these efforts, the IRS announced in September its intention to heighten scrutiny on individuals earning in excess of $1 million per year who have substantial tax debts exceeding $250,000. This initiative represents a concerted push to enhance the integrity of the tax system and address the tax gap by targeting those with the highest earning brackets and significant outstanding tax obligations. The announcement serves as a reminder of the IRS’s commitment to fair tax enforcement and the importance of compliance with tax laws.

In a landmark decision, EU antitrust regulators have endorsed a set of commitments from Apple, marking a significant shift in the tech giant’s approach to its contactless payment technology. This development paves the way for competitors to access Apple’s tap and go payment system, potentially altering the landscape of digital payments in Europe. EU antitrust chief Margrethe Vestager highlighted the move as a pivotal change that promises to enhance competition and consumer choice. This announcement follows the European Commission’s initiation of an antitrust probe concerning Apple Pay back in 2020, reflecting the EU’s ongoing efforts to ensure fair competition in the digital market. The acceptance of these commitments by Apple indicates a willingness to comply with regulatory standards and could set a precedent for other tech companies operating within the EU.

The highly anticipated inflation report and the jobless claims with likely set the tenor for today’s trading. Will the reaction follow-though with the bullish surge the ended the Wednesday session or, will the bears find reason to whipsaw the indexes back down? Buckle up we will soon find out so plan your risk carefully.

Wednesday was a bullish freight train and the Bears were tied to the track. The SPY gapped up 0.23%, DIA opened flat, and QQQ gapped up 0.42%. From there, all three major index ETFs ground sideways in a very tight range for 90 minutes. However, then the fuse was lit and all three rallied steadily for the rest of the day. They all went parabolic the last half hour with only five minutes of profit taking at the end keeping all three from ending on their highs. This action gave us large white-bodied candles with smaller wicks on both ends across the board. SPY and QQQ once again printed new all-time highs and gave us new all-time high closes (the 37th of the year). Meanwhile, after a successful retest of its T-line (8ema) the DIA rallied to break out of its trading range dating back to May and closed less than a percent from its own all-time high. This happened on below average volume in SPY and QQQ as well as above-average volume in DIA.

On the day, all 10 sectors were in the green with Basic Materials (+1.51%) way out front leading the rest of the market higher. Even the laggards, Consumer Cyclicals (+0.61%), Energy (+0.62%), and Consumer Defensive (+0.64%) were up significantly. At the same time, SPY gained 0.99%, DIA gained 1.08%, and QQQ gained 1.04%. VXX fell just a tad and remains extremely low at 10.27. Meanwhile, T2122 spiked up to the top half of its mid-range at 69.68. On the bond front, 10-year bond yields were down a bit to 4.281% and Oil (WTI) gained 1.24% to close at $82.42 per barrel. So, Wednesday was a bullish day in a strong bullish trend. SPY and QQQ have closed at a new all-time high close each of the last five sessions, led by the Tech Big Dogs like NVDA (+2.70%), AMD (+3.87%), and AAPL (+1.88%). In fact, the only one of the 10 Tech Big Dogs that was down was NFLX (-1.18%) and it only traded $1.8 billion in stock on the day. So, if traders were waiting on CPI data…they have a funny way of showing it.

The major economic news scheduled for Wednesday were limited to EIA Weekly Crude Oil Inventories, which showed a much larger drawdown than expected at -3.443 million barrels (compared to a forecasted build of 0.700-million-barrels but far less than the prior week’s -12.157 million barrels).

In economic speak news, on Wednesday, Fed Chair Powell testified again, this time in front of the House. Powell said the Fed does not need to reach the 2% target figure prior to cutting rates. In addition, he said the Fed will cut rates “when and as needed,” regardless of the election. Powell said, “Our undertaking is to make decisions when and as they need to be made, based on the data, the incoming data, the evolving outlook and the balance of risks, and not in consideration of other factors, and that would include political factors.” (For the second day in a row, GOP lawmakers pressed (begged?) Powell not to announce any rate cuts until after the November 5 election.) When asked about the path of inflation, Powell indicated he did have some confidence that inflation is headed back below 2%. However, when asked if the bar for a rate cut had been cleared, Powell said “”I am not ready to say that yet.” He continued, “There is a path to getting back to full price stability while keeping the unemployment rate low, … We’re on it. We’re very focused on staying on that path.”

After the close, PSMT and WDFC reported beats on both the revenue and earnings lines.

In stock news, on Wednesday, WBD announced its CNN unit will cut 100 jobs (2.8% of its workforce) and also launch a new CNN.com subscription service later this year. At the same time, INTU announced plans to layoff 1,800 employees (10% of workforce) in cost-cutting moves, citing that AI is transforming the company. Later, HON announced they have signed a deal to buy APD’s LNG pretreatment unit for $1.81 billion. At the same time, AMD announced they have agreed to buy Silo AI (private) for $665 million. Later, TLSA raised the prices of its Model 3 in Europe by about $1.622 after the EU imposed tariffs on EVs made in China. (The Model 3 is made in China.) Meanwhile, Bloomberg reported that GOOGL has walked away from its pursuit of purchasing HUBS. Later, Bloomberg reported that AAPL is expecting 10% growth in iPhone sales compared to 2023 according to internal sources it cited. (However, 2023 was a down year for iPhone shipments.) At the same time, the Athletic reported that AMZN. CMCSA, and DIS have finalized a $76 billion deal to broadcast NBA basketball games for 11 seasons. (However, the report said current NBA partner WBD still has the option to match the deal.) After the close, COST announced it will hike membership fees starting in the fall. Elsewhere, MSFT announced it will drop its “observer seat” on the OpenAI board to head off antitrust inquiries in the US and UK. AAPL followed MSFT’s lead giving up its own newly-acquired “board observer” seat.

In stock legal and governmental news, on Wednesday the NHTSA announced that STLA is recalling 332k 2017-2025 Alfa Romeo, Jeep, and Fiat vehicles in the US over faulty seatbelt sensors. At the same time, the same agency announced BMWYY was recalling 394k vehicles in the US due to faulty airbag inflators. Later, HE stock spiked on a report saying that a “massive settlement” related to the Maui wildfires could be unveiled as soon as next week. No other details were released, but 451 lawsuits (covering 1,800 individual plaintiffs as well as 425 business entity plaintiffs) related to those wildfires are in the courts now. At the same time, MSFT completed a $21.7 million deal to settle cloud licensing practices to avoid EU antitrust action. (The deal was with the main complainant to the EU about those practices.) GOOGL announced it will explore other options to fight MSFT cloud licensing practices after the settlement. Later, JBLU asked the Dept. of Transportation to disqualify the UAL proposal from winning one of the five new round-trip flight slots up for bid from Washington Reagan airport.

Elsewhere, a federal judge in CA dismissed most of the FCBN $1 billion lawsuit against HSBC for “poaching” 40 employees after the collapse of Silicon Valley Bank in March of 2023. Later, the CEO of BA was hauled before the NTSB and forced to apologize for violating its NTSB rules. After the apology, the BA CEO refused other comment. At the same time, NSC agreed to implement the series of safety recommendations made by the NTSB following the February 2023 train derailment in East Palestine OH. Later, the FTC announced plans to sue UNH, ESRX, and CVS over their negotiating practices (collusion) on drugs including insulin following a two-year investigation. After the close, the former CEO of WORX was convicted of securities fraud related to statements about the company becoming the major supplier of rapid COVID-19 tests, despite knowing the claims were untrue. At the same time, the Fed and Office of the Comptroller fined C $136 million after the bank was found to have made insufficient progress addressing data management issues. (The bank was fined $400 million in 2020 for the same deficiencies.)

Overnight, Asian markets were nearly green across the board. Only India (-0.03%) was below break-even. Meanwhile Hong Kong (+2.06%), Shenzhen (+1.99%), and Taiwan (+1.60%) led broad and strong gains in the region. In Europe, we see the same picture taking shape at midday with only Denmark (-0.03%) on the red side of flat. However, the CAC (+0.32%), DAX (+0.19%), and FTSE (+0.22%) lead modest gains ahead of US data. In the US, as of 7:30 a.m., Futures are pointing toward a start just below Wednesday’s close. The DIA implies a -0.17% open, SPY is implying a -0.11% open, and QQQ implies a -0.08% open at this hour. At the same time, 10-Year bond yields are up slightly to 4.281% and Oil (WTI) is up three-tenths of a percent to $82.35 per barrel in early trading.

The major economic news scheduled for Thursday include June Core CPI, June CPI, Weekly Initial Jobless Claims, and Weekly Continuing Jobless Claims (all at 8:30 a.m.), June Federal Budget Balance (2 p.m.) and Weekly Fed Balance Sheet (4:30 p.m.). Fed member Bostic also speaks at 11:30 a.m. Earnings season begins again Thursday as Thursday, CAG, DAL, and PEP report before the open. However, there are no major reports scheduled for after the close.

In economic news later this week, on Friday, June Core PPI, June PPI, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-Year Inflation Expectations, Michigan 5-Year Inflation Expectations, and the WASDE Ag report are delivered.

In terms of earnings reports later this week, Friday, BK, C, ERIC, FAST, JPM, and WFC report.

So far this morning, DAL beat on revenue while missing on earnings by a penny. On the other side, PEP missed on revenue while beating on earnings.

With that background, it looks as if markets are slightly, but undecidedly bearish in the premarket. All three major index ETFs started the early session flat, but have put in small, black-bodied candles since then. Still, regardless of your timeframe, the market trend (short-term, mid-term, or longer-term) remains very bullish. In terms of extension, QQQ is stretched above its T-line and SPY is also pushing its extension. The T2122 indicator is back up above the center of its mid-range. Therefore, the market still has room to run in either direction, but the Bears still have more slack to work with today. (We are in need of rest or pullback in the QQQ and SPY.) With regard to those 10 big dog tickers, eight of the 10 are in the red early this morning on modest moves. However, the biggest dog, NVDA (+0.36%) is also the best performer of that group on price move and volume.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service