Stock futures remained relatively stable, waiting for the FOMC minutes from the Federal Reserve’s latest policy meeting, hoping for clues about a potential interest rate cut. However, the day’s most significant release in the U.S. was a set of revisions to job figures for the year through March, which could reveal the loss of up to a million positions. This report is expected to heavily influence the tone of Federal Reserve Chair Jerome Powell’s upcoming speech at the Jackson Hole symposium, potentially impacting market sentiment and future economic policies.

European stock markets saw a cautious rebound after ending a long winning streak the previous day. In the U.K., public sector net borrowing increased to £3.1 billion ($4.037 billion) in July, a significant rise of £1.8 billion compared to the same month last year, according to the Office for National Statistics. Alex Kerr, a U.K. economist at Capital Economics, noted that this increase “continued the recent run of bad news on the fiscal position,” highlighting ongoing concerns about the country’s financial health.

In July, Japan experienced a notable increase in trade activity, with exports rising by 10.3% year-on-year and imports growing by 16.6%. These figures fell short of expectations, which had forecasted an 11.4% rise in exports and a 14.9% growth in imports. This period marked the final month of trade data before the Bank of Japan’s decision to raise interest rates at the end of July, a move that significantly strengthened the yen.

Economic Calendar

Earnings Calendar

Notable reports for Tuesday before the bell include ADI, DY, M, TGT, & TJX. After the bell include A, NDSN, SNOW, SQM, SNPS, URBN, WOLF, & ZM.

News & Technicals’

Target surpassed Wall Street’s earnings and revenue expectations, driven by increased shopper visits to both its physical stores and website. The retailer saw a boost in sales of discretionary items such as clothing. Despite this positive performance, Target adopted a cautious outlook, forecasting that comparable sales for the full year would fall within the lower range of its guidance. This tempered optimism reflects the company’s awareness of potential economic uncertainties ahead.

China’s steel rebar prices have dropped over 20% year-to-date, now standing at 3,208 Chinese yuan ($450) per ton, according to data from financial information provider Wind. This decline reflects a broader trend of disappointing demand for metals in China, as noted by Sarbin Chowdhury, head of commodities analysis at BMI. Additionally, the price of iron ore, a crucial material for steel production, has plummeted by more than 28% so far this year, based on FactSet data. These trends highlight significant challenges in the Chinese metals market.

A federal judge in Texas has struck down a Biden administration rule that aimed to ban worker noncompete agreements. On Tuesday, the judge barred the U.S. Federal Trade Commission’s rule from taking effect, which would have prohibited agreements preventing workers from joining their employers’ rivals or starting competing businesses. In her ruling, Judge Brown stated that even if the FTC had the authority to implement such a rule, the agency had not sufficiently justified the need to ban nearly all noncompete agreements. This decision marks a significant setback for the administration’s efforts to regulate employment practices.

On Wednesday, Ukraine launched one of its largest-ever drone attacks against Moscow, marking a significant escalation in the conflict. Moscow Mayor Sergei Sobyanin confirmed the scale of the attack in a Google-translated Telegram post, stating, “This is one of the largest attempts to attack Moscow with drones ever. We continue to monitor the situation.” The drone offensive coincided with Russian President Vladimir Putin’s first visit to Chechnya in 13 years, where he inspected local troops and volunteers preparing to join the war effort. This timing underscores the heightened tensions and ongoing strategic maneuvers in the region.

Although there is an anticipation for the FOMC minutes this afternoon keep a close eye out for the BLS revisions at 10AM Eastern today. According to Goldman and Wells Fargo we could see 600,000 to 1 million jobs suddenly vanish in the report. The majority of traders could be caught off guard creating the possibility of a big reversal depending on the report results. It may turn out to be a nonevent but its better to be prepared.

Markets were undecided on Tuesday. SPY opened down 0.07%, DIA opened 0.12% lower, and QQQ opened down 0.16%. At that point, SPY and QQQ rallied to recross their opening gap and reach the highs by 10 a.m. From there they sold off reaching the lows 45 minutes later and then bobbing along those lows until 1 p.m. when they rallied to recross the gap again by 2:25 p.m. and then recross it once more in a slow modest slide into the close. For its part, DIA had a similar path for the day but with much less magnitude of waves. This action gave us indecisive, black-bodied Doji-type candles in all three major index ETFs. It also gave us a higher high and a higher low than Monday by a lower open and close. Again, this happened on well-below average volume in all three major index ETFs.

On the day, nine of the 10 sectors were in the red with Energy (-2.14%) a full 1.5% out in front of the other sectors leading markets lower. On the other side, Healthcare (+0.05%) was the only sector in the green. Meanwhile, SPY lost 0.16%, DIA fell 0.13%, and QQQ lost 0.21%. VXX popped 3.92% to close at 46.17 and T2122 dropped back out of the overbought territory to close in the top end of its mid-range at 70.83. On the bond front, 10-year bond yields fell to 3.81% and Oil (WTI) dropped another 0.74% to close at $73.82 per barrel. So, Tuesday was more of a rest and/or indecision day for traders as markets wandered around the small opening gap all day. By the closing bell, markets had small black bodies. However, even at their extremes, none of the major index ETFs were more than half a percent from their Monday close.

The major economic news scheduled for Tuesday was limited to API Weekly Crude Oil Stocks after the close, which showed a 0.347-million-barrel inventory build (compared to a forecasted 2.800-million-barrel drawdown and well above the prior week’s 5.205-million-barrel drawdown).

In Fed news, on Tuesday, Fed Governor Bowman (a hawk) told an Alaska Bankers conference that she is still cautious about changing Fed policy. Bowman said, “it will become appropriate to gradually lower the federal funds rate to prevent monetary policy from becoming overly restrictive…” However, she continued, “we need to be patient and avoid undermining continued progress on lowering inflation by overreacting to any single data point (apparently a reference to July’s 4.3% Unemployment value).” Bowman noted doubts about data quality, saying “Increased measurement challenges and the frequency and extent of data revisions…make the task of assessing the current state of the economy…challenging.” This led to her conclusion, “I will remain cautious in my approach to considering adjustments to the current stance of policy.”

After the close, KEYS, LZB, PAGS, and TOL reported beats on both the revenue and earnings line. Meanwhile, ALC, JKHY and ZTO missed on revenue while beating on earnings. However, COTY missed on both the top and bottom lines.

In stock news, on Tuesday, the PARA takeover saga continued as a new suitor made his interest official, submitting a $4.3 billion bid via the acquisition of National Amusements. Later, JNJ announced they have agreed to buy V-Wave (a heart failure treatment maker) for $600 million up front and potentially an additional $1.1 billion in milestone payments (based on the development of V-Wave’s treatments). Meanwhile, GOOGL announced its Waymo robotaxi unit had doubled its “paid rides” to 100k per week over three months of operation. (Not bad considering Waymo only has 700 of its robotic taxis.) Meanwhile, WFC announced it had agreed to sell its “non-agency third-party Commercial Mortgage Servicing” unit to private firm Trimont. The terms of the sale were not disclosed. At the same time, STLA announced it was delayed its investment plans for Belvidere, IL. This came after the UAW filed grievances Monday alleging STLA has violated the terms of its November 2023 contract. STLA denied this charge. After the close, MCHP announced it had detected potentially unauthorized activity on its network systems that had disrupted operations at come facilities. (The activity was seen Aug. 17 and again on Aug. 19.) The company said it is working to bring all of its systems back online. Also after the close, BBAI (and AI company) announced it had won a contract of up to $2.4 billion over 10 years with the FAA.

In stock legal and governmental news, on Tuesday, the EU announced it would slash its previously announced additional tariffs on electric vehicles imported from China. For example, TSLA will pay an additional 9% tariff (much lower than the previously-announced 20.8%). These “punitive duties” are on top of the EU’s standard 10% tariff on imported cars. The European Commission said that the changes come after it had verified the Chinese government subsidies EV companies had received. At the same time, the FDA approved JNJ’s “chemotherapy-free” combination treatment for a type of non-small cell lung cancer. (This puts the JNJ treatment in competition with AZN’s blockbuster drug Tagrisso.) Later, DIS backed down in the face of heavy bad publicity and announced it will drop its motion to dismiss a lawsuit. Previously, DIS claimed that a user agreement accepted for a 2019 free trial of DIS+ streaming service prevented a FL widower from suing over the wrongful death of his wife. (His wife died from allergic reaction to food served at a DIS restaurant in 2023, after the couple had informed the restaurant of the allergy and the restaurant claimed to accommodate food allergies.) Instead of forced arbitration, DIS now says the case can be decided in court.

Elsewhere, the Dept. of Transportation announced the ALK acquisition of HA had been cleared by the Justice Dept. and was now under DOT review. Later, the NHTSA announced BMWYY (BMW) is recalling 721k vehicles over electrical short-circuit risk due to a faulty water pump connector seal. At the same time, the FAA has formally required the inspection of all BA 787 Dreamliner jets over the five recent “mid-air dive” reports that have been tied to pilot seat adjustment turning off the autopilot. Later, the UK competition watchdog agency announced it had accepted META’s proposed changes to the way it uses customer’s data in advertising. At the same time, a US Appeals Court revived a lawsuit against GOOGL. The class-action suit alleges that GOOGL continued to collect personal data of Chrome browser users after they chose not to synchronize their browser to Google accounts.

After the close, WBD pledged to spend at least $8.5 billion to produce movies and TV shows in Las Vegas after the company received a tax incentive package. Finally, a TX Trump-appointed federal judge struck down the FTC ban on most non-compete agreements required for employees. (The same judge had temporarily blocked the ban in July.) The ruling said the FTC does not have the authority to ban practices it deems as unfair competition methods, even though the agency was tasked by Congress is enforcing federal antitrust laws. (Appeals will very likely follow, but with the uber-Republican SCOTUS, the odds of the bans coming back into effect are long at best.)

Overnight, Asian markets were mixed again as seven of the 12 regional exchanges were in the red. Taiwan (-0.85%) and Hong Kong (-0.69%) paced the losses while Thailand (+0.73%) was by far the biggest gainer. However, in Europe, we see green across the board at midday. The CAC (+0.42%), DAX (+0.48%), and FTSE (+0.17%) lead the region higher in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a modestly green start to the morning. The DIA implies a +0.14% open, the SPY is implying a +0.19% open, and the QQQ implies a +0.22% open at this hour. At the same time, 10-Year bond yields are at 3.822% and Oil (WTI) is up by a fraction to $73.31 per barrel in early trading.

The major economic news scheduled for Wednesday is limited to EIA Weekly Crude Oil Inventories (10:30 a.m.) and July FOMC Meeting Minutes (2 p.m.). The major earnings reports scheduled for before the open include ADI, DY, M, TGT, TJX, and ZK. Then, after the close, A, CAAP, LU, NDSN, SNOW, SNPS, URBN, and ZM report.

In economic news later this week, on Thursday, Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, S&P Global Mfg. PMI, S&P Global Services PMI, S&P Global Composite PMI, July Existing Home Sales, and the Fed Balance Sheet are reported. The Jackson Hole Symposium also starts. Finally, on Friday we get July Building Permits, and July New Home Sales. The Jackson Hole Symposium also continues.

In terms of earnings reports later this week, on Thursday, AAP, BIDU, BILI, BJ, CSIQ, IQ, NTES, PTON, TD, VIK, BMA, INTU, ROST, and WDAY report. Finally, on Friday, we hear from GFI.

So far this morning, ADI, DY, M, and TGT have all reported beats on both the revenue and earnings lines. Meanwhile, ZK missed (massive miss) on revenue while staying in line on earnings (still a loss).

In miscellaneous news, on Tuesday, a research report from CBRE said that the North American datacenter capacity has jumped 70% in the last year due to the AI craze. The electrical demand of datacenters alone now stands at 3.9 gigawatts. The report said more than 500 megawatts of new datacenter demand went online in just the eight largest US markets in the first half of 2024. (For reference, that 500 megawatts adding in H1 was roughly equivalent to the entire data center capacity of Silicon Valley at the end of 2023.) Elsewhere, the SEC approved (along party lines with GOP-appointed members fighting the move) the new rules proposed in June that will allow the Public Company Accountancy Oversight to hold employees, partners, contractors, and others to be held accountable for negligence if audits are found to be in violation (fraudulent). Meanwhile, Bloomberg reported Tuesday evening that the “Carry Trade” is back on but in reverse. For many years, investors borrowed Yen in Japan at almost non-existent interest rates and “carried the money” to the US to invest in higher-yielding vehicles. With July’s Japanese rate hike and the fall in the Dollar, traders are now borrowing Dollars to put into Japanese investments. The idea is that speculators are betting that Japan will increase rates more and the US sill start cutting rates next month. (I’m not sure I buy that reporting given the relative differences in US and Japanese interest rates even after Japan’s July hike. Nonetheless, that is what Bloomberg reports.)

With that background, markets seem to be resting or indecisive again this morning. All three major index ETFs made a very modest gap higher to open the premarket, Since that point they have traded indecisively but have small white body Spinning Top candles at this time of the early session. With that said, all three remains far above their T-line (8ema) and the short-term trend is still strongly bullish. Meanwhile, the mid-term bearish trend is broken, though one could argue a new mid-term bullish trend has not formed yet (due to a lack of higher low in the run). In the long-term, we are now clearly back in a Bull trend. In terms of extension, as I mentioned all three are stretched to the upside relative to their T-line. However, the T2122 indicator has now pulled back out of its overbought territory into the top part of its mid-range. So, the market does still need a pullback or at least a rest. However, Tuesday’s candle helped some. Just remember that the market can stay overextended a lot longer than we can stay solvent predicting a reversal. So, keep the mantra “follow, don’t lead, but also don’t chase” in mind. With regard to those 10 big dog tickers, six of them are in the green, led by AMZN (+0.69%) while GOOGL (-0.60%) is the laggard. However, the biggest dog (in terms of dollar-volume traded), is NVDA (-0.01%) followed by TSLA (-0.07%), which are both undecided this morning.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

U.S. stock futures remained flat on Tuesday morning following the S&P 500 and Nasdaq Composite achieving their longest winning streaks of 2024. Investors are now turning their attention to the Federal Reserve’s annual Jackson Hole Economic Symposium, where Chair Jerome Powell is set to speak on Friday. Wall Street is eagerly anticipating his remarks, hoping for insights into the Federal Reserve’s plans for the upcoming September meeting

European stocks edged higher amid ongoing market uncertainty regarding potential interest rate cuts. The Riksbank in Sweden reduced its interest rates by 25 basis points, bringing them down to 3.50% from 3.75%, and indicated the possibility of two to three additional rate cuts within the year. Key economic data releases in Europe on Tuesday include Germany’s producer price index and the EU’s final year-on-year inflation rate, which are likely to influence market sentiment further.

China’s central bank has decided to maintain its one-year and five-year loan prime rates at 3.35% and 3.85%, respectively, aligning with market expectations. This decision reflects a steady approach to monetary policy amid current economic conditions. Meanwhile, the Reserve Bank of Australia’s August meeting minutes indicate that a rate cut in the near future is considered “unlikely,” suggesting a cautious stance on altering interest rates.

Economic Calendar

Earnings Calendar

Notable reports for Tuesday before the bell include AS, KC, LOW, MDT, PINC, & VIPS. After the bell include COTY, KEYS, LZB, TOL, & ZTO.

News & Technicals’

Alaska Airlines and Hawaiian Airlines are one step closer to finalizing their deal after the Justice Department’s investigation period ended on Tuesday without any legal action to block it. However, the completion of the deal still hinges on approval from the U.S. Transportation Department. The timeline for this approval process remains uncertain, leaving both airlines in a state of anticipation as they await the final green light to proceed.

Following Palo Alto Networks’ earnings beat on Monday, CEO Nikesh Arora discussed the company’s “platformization” strategy with CNBC’s Jim Cramer. Arora emphasized that this approach, which involves bundling the company’s products and services, is crucial for the long-term success of the cybersecurity firm. By integrating various offerings into a cohesive platform, Palo Alto Networks aims to enhance its value proposition and streamline solutions for its clients, positioning itself strongly in the competitive cybersecurity market.

Vice President Kamala Harris has proposed raising the corporate tax rate to 28%, marking her first significant initiative to increase revenues for financing her ambitious plans as president. Harris argues that this measure would ensure that billionaires and large corporations contribute their fair share to the economy. By targeting higher corporate taxes, she aims to generate the necessary funds to support various expensive programs and initiatives she envisions for the country’s future.

China’s youth unemployment rate surged to over 17% in July, marking the highest level since the new record-keeping system was implemented in December, according to the National Bureau of Statistics. This represents a significant increase from 13.2% in June. Additionally, the urban unemployment rate across all age groups rose slightly to 5.2% in July, up from 5% in June. These figures, released on Thursday, highlight growing challenges in the job market, particularly for young people.

The buying enthusiasm continued Monday as the SPY and QQQ enjoyed the longest winning streaks in 2024. However, it would be wise to raise stops and watch for clues that this parabolic relief rally finds some profit takers at this elevation.

Markets started Monday in a flat manner. SPY opened +0.08%, DIA opened up 0.13%, and QQQ opened just 0.01% higher. From there, all three major index ETFs ground sideways for the better part of an hour. At that point, all three saw a major volatility event with a 5-minute crash down followed immediately by a 5-minute spike right back up. Then the Bulls took over, leading a steady rally for the rest of the day with a bullish spike the last 10 minutes in SPY and QQQ. For its part, DIA’s rally died out at 1 p.m., after which it ground sideways with a modestly bearish trend the rest of the day until it too had a Bull spike the last 10 minutes. This action gave us large white-bodied candles in all three major index ETFs. SPY and QQQ ended the day on the highs while DIA had a small upper wick. This happened on well-below average volume in all three major index ETFs.

On the day, all 10 sectors were in the green with Healthcare (+1.98%) well out in front followed by Technology (+1.37%) leading the way higher. On the other side, Consumer Defensive (+0.43%) being the lagging sector. Meanwhile, SPY gained 0.96%, DIA was up 0.58%, and QQQ gained 1.31%. VXX fell another 1.44% to close at 44.43 and T2122 jumped back up into the top end of its overbought territory at 96.23. On the bond front, 10-year bond yields fell to 3.875% and Oil (WTI) dropped 2.86% to close at $74.46 per barrel. So, Monday was a less volatile but also quite bullish day as traders could not justify bearish trades, but were also afraid to pile in (with heavy volume) on the long side either. It is worth noting that SPY and DIA closed less than one percent below their all-time high closes. However, QQQ closed still 4.5% below its all-time high close. Interestingly, an equal-weighted version of the SPY (where all stocks have the same weight as AAPL) hit a new all-time high Monday.

The major economic news scheduled for Monday was limited to the July US Leading Economic indicators Index, which came in below expectations at -0.6% (compared to a forecast of -0.4% and a June reading of -0.2%).

In Fed news, on Monday, the Wall Street Journal reported Minneapolis Fed President Kashkari said it was appropriate to discuss potentially cutting interest rates at the FOMC meeting in September. The article quoted Kashkari as saying, “The balance of risks has shifted, so the debate about potentially cutting rates in September is an appropriate one to have.” The WSJ went on to say that Kashkari indicated progress has been made on inflation but the labor market has shown some “concerning signs.” The article quoted him as saying, “I’m still unclear how tight policy is, but the balance of risks in my view have shifted more towards the labor market and away from the inflation side of our dual mandate.” Elsewhere, Fed Governor Waller did not comment on the economy or monetary policy. However, he did address say the Fed is looking into the financial stability risks related to stablecoins and non-bank holders.

After the close, FN and PANW reported beats on both the revenue and earnings lines. It is worth noting that FN raised forward guidance while PANW lowered its guidance.

In stock news, on Monday, Reuters reported that LUV has started a campaign to fight off Elliott Investment Management’s attempt to replace two-thirds of its board members as a prelude to ousting the CEO and the LUV board Chairman. (Elliott did the same thing at SBUX in the past.) In a letter to employees, (seeking union and individual employee shareholder support) CEO Jordan said “Don’t be fooled – this is a battle for the heart of our company and our future – your future.” At the same time, Reuters reported that APA is exploring the sale of its Permian Basis oil and gas properties for roughly $1 billion. The article said APA has retained two investment banks to help facilitate a sale. Later, Reuters also reported that ANCTF (operator of the Circle-K convenience stores) has made a preliminary takeover bid for SVNDF (large Japanese 7-Eleven store operator) for roughly $38 billion.

Elsewhere, GM laid off 1,000 salaried software and services unit employees globally on Monday. (Roughly 600 of those jobs are located in MI with the rest spread around the world.) Later, the UAW union said it was filing a number of grievances against STLA and could launch a nationwide strike against the automaker. The UAW says STLA is not honoring the production (job) commitments it has made in later-2023 contract negotiations. After the close, GPRO announced it will cut about 15% of its workforce (only 139 jobs) as it seeks to restructure. At the same time, Reuters reported that BA has grounded its test fleet of 777X jets after inspections found a failure of the engine mounting structure.

In stock legal and governmental news, on Monday, the US State Department approved the sale of $100 million of Javelin missiles (produced by GD) to Australia. Later, KR sued the FTC seeking to block the regulator from reviewing its proposed $25 billion acquisition of ACI. In the suit, KR alleges that the FTC is unconstitutional. After the close, Reuters reported that two dozen state Attorney’s General have amended their lawsuit against LYV. The new filing shows that the AGs are looking for three times the damages incurred for each customer in the suit they filed in May. In related news, 10 more states joined the lawsuit Monday, bringing the total to 36 plus the District of Columbia.

Elsewhere, also after the close, PPC agreed to pay $100 million to settle claims it had conspired with rivals to reduce the pay given to chicken farmers. (TSN, SAFM, and others had previously settled the same case for much lower amounts.) At the same time, the FAA issued a airworthiness directive for BA 787 jets after receiving five reports of sudden mid-flight dives. (The dives were found to be related to movement of the captain’s seat disconnecting the autopilot without notice.) Meanwhile, IEP and its CEO Carl Icahn settled charges from the SEC of operating a “Ponzi-like scheme.” In the settlement, IEP agreed to pay $2 million.

Overnight, Asian markets were mixed with five of the 12 exchanges in the red. Japan (+1.80%) was by far the biggest gainer while Shenzhen (-1.25%) and Shanghai (-0.93%) paced the losses. In Europe, the picture is a little more red with only four of the 15 bourses in the green at midday. The CAC (+0.09%), DAX (-0.07%), and FTSE (-0.70%) are leading the region lower in early afternoon trade. Meanwhile, in the US, as of 7:30 a.m., Futures are pointing toward a mixed and flat start to the morning. The DIA implies a -0.04% open, the SPY is implying a +0.09% open, and the QQQ implies a +0.11% open at this hour. At the same time, 10-Year bond yields are at 3.873% and Oil (WTI) is just on the green side of flat at $74.42 per barrel in early trading.

The major economic news scheduled for Tuesday is limited to API Weekly Crude Oil Stocks (4:30 p.m.). Fed members Bostic (1:35 p.m.) and Vice Chair Barr (2:45 p.m.) also speak. The major earnings reports scheduled for before the open are is limited to RERE, AS, FUTU, HTHT, LOW, MDT, VIPS, and XPEV. Then, after the close, ALC, SQM, COTY, JKHY, KEYS, LZB, PAGS, TOL, and ZTO report.

In economic news later this week, on Wednesday, we get EIA Weekly Crude Oil Inventories and July FOMC Meeting Minutes. One Thursday, Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, S&P Global Mfg. PMI, S&P Global Services PMI, S&P Global Composite PMI, July Existing Home Sales, and the Fed Balance Sheet are reported. The Jackson Hole Symposium also starts. Finally, on Friday we get July Building Permits, and July New Home Sales. The Jackson Hole Symposium also continues.

In terms of earnings reports later this week, on Wednesday we hear from, ADI, DY, M, TGT, TJX, ZK, A, CAAP, LU, NDSN, SNOW, SNPS, URBN, and ZM. On Thursday, AAP, BIDU, BILI, BJ, CSIQ, IQ, NTES, PTON, TD, VIK, BMA, INTU, ROST, and WDAY report. Finally, on Friday, we hear from GFI.

So far this morning, AS, FUTU, and MDT reported beats on both the revenue and earnings lines. Meanwhile, LOW and XPEV missed on revenue while beating on earnings. On the other side, VIPS beat on revenue while missing on earnings. It is worth noting that LOW also lowered its forward guidance.

In miscellaneous news, on Monday, major US freight-forwarder CHRW announced it has begun to divert some US customer ocean cargo away from Canadian ports. This is being done in anticipation of a Canadian rale strike as soon as August 22. (Much of ocean cargo continues its journey on rail prior to switching to truck for the last leg of delivery.) Elsewhere, GS analysts cautioned their clients that next week’s US Non-Farm Payroll data revision is likely to overstate labor market weakness. GS suggests the overstatement will be due to the quarterly census of Employment which does not account for employment of illegal immigrants. Secondly, GS says even if it did take immigrants into account, that this census is consistently revised upwardly later. All told, GS believes the revision will be 300k-500k jobs too low.

With that background, it looks like traders are uncertain early this morning. All three major index ETFs gapped up modestly to start the premarket. However, all three have also sold back down printing small black-body candles in the early session. With that said, all three are still far above their T-line (8ema) and the short-term trend is clearly strongly bullish. Meanwhile, the mid-term bearish trend is broken, though one could argue a new mid-term bullish trend has not formed yet (due to a lack of higher low in the run). In the long-term, we are now clearly back in a Bull trend. In terms of extension, as I mentioned all three are stretched to the upside relative to their T-line. At the same time, the T2122 indicator is now in the top half of its overbought territory. So, the market is in need of a pullback or at least a rest. Just remember that the market can stay overextended a lot longer than we can stay solvent predicting a reversal. So, keep the mantra “follow, don’t lead, but also don’t chase” in mind. With regard to those 10 big dog tickers, seven of them are in the green, led by AMD (+1.10%) again. However, the biggest dog (in terms of dollar-volume traded), is NVDA (-0.39%), which is leading the losers in that group lower.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Traders are beginning the week with caution, following a period of renewed risk appetite last week. The market’s focus is now on potential interest-rate cuts from the Federal Reserve. The key event this week is scheduled for Friday, when Fed Chair Jerome Powell is anticipated to provide new insights into the direction of U.S. monetary policy at the central bank’s Jackson Hole economic symposium in Wyoming. This event is highly anticipated as it could offer crucial signals regarding the Fed’s future actions.

European stocks continued their positive momentum at the beginning of the new trading week, with most sectors and major bourses experiencing gains. Despite the overall upward trend, food and beverage stocks saw a slight decline of 0.15%. In contrast, mining stocks performed strongly, rising by 1.1%.

This week, traders in Asia are closely monitoring central bank announcements, including the Bank of Korea’s rate decision and the minutes from the Reserve Bank of Australia’s August meeting. In Japan, core machinery orders unexpectedly declined by 1.7% year-on-year in June, contrary to economists’ predictions of a 1.8% increase. The Nikkei 225 falling by 1.77% to close at 37,388.62, and the Topix index dropping 1.4% to end at 2,641.14. Both indexes ended their five-day winning streaks.

Economic Calendar

Earnings Calendar

Notable reports for Thursday before the bell include EL. After the bell include FN & PANW.

News & Technicals’

Ukrainian forces have reportedly destroyed a second strategically important bridge in Russia’s Kursk region as part of their ongoing incursion. Despite the scale of this cross-border operation, which involves around 5,000 Ukrainian soldiers, Moscow has yet to deliver a significant response. According to the Wall Street Journal, the incursion began nearly two weeks ago, and Kyiv claims to have seized control of 82 settlements across an area of 1,150 square kilometers (444 square miles). This ambitious operation underscores the escalating tensions and the strategic maneuvers by Ukrainian forces in the region.

Goldman Sachs has revised its forecast for the likelihood of a U.S. recession, lowering it to 20% from a recent increase to 25%, which had been raised from 15%. This adjustment follows a weaker-than-expected July jobs report that initially alarmed economists at Goldman and other institutions. However, subsequent data on retail sales and jobless claims have alleviated fears, suggesting that the world’s largest economy is not imminently heading into a recession. These recent economic indicators have provided a more optimistic outlook, easing concerns about the U.S. economic trajectory.

Retail pharmacy chains like Walgreens and CVS are shifting their strategies from continuous store expansions to closing hundreds of locations across the U.S. in an effort to boost profits. This change is driven by declining reimbursement rates for prescription drugs and various challenges affecting the front of the store, including inflation and heightened competition. Despite these hurdles, these drugstores continue to play a crucial role in the U.S. health-care system, serving tens of millions of Americans. However, to maintain their relevance and profitability, they may need to reinvent their business models.

According to the Goldman CTA report there is a renewed risk appetite largely supported by billions in corporate buybacks. There is also a massive anticipation that Jerome Powell will provide some clarity of a possible September rate cut during his Jackson Hole speech on Friday. With a light week of earnings and economic reports traders will have to stay nimble and ready for just about anything.

On Friday, the Bulls closed out a strong week with modest gain. SPY gapped down 0.32%, DIA gapped down 0.23%, and QQQ gapped +0.39%. Next, all three major index ETFs meandered back and forth across the gap until 11:30 a.m. From there, all three rallied briskly until 1 p.m. The rest of the day saw a slow and weak pullback. This action gave us white-bodied candles with modest upper wicks in the SPY, DIA and QQQ. During the day, QQQ retested and held above its 50sma. This happened on very low volume in the SPY and QQQ as well as below-average volume in the DIA.

On the day, nine of the 10 sectors were in the green again with Financial Services (+0.78%) and Communication Services (+0.72%) leading the way higher. On the other side, Industrials (-0.01%) was the only sector in the red (barely). Meanwhile, SPY was up 0.22%, DIA gained 0.21%, and QQQ gained 0.13%. VXX fell slightly to close at 45.23 and T2122 also pulled back just a bit to stay in the overbought territory at 86.11. On the bond front, 10-year bond yields fell to 3.883% and Oil (WTI) dropped 2.00% to close at $76.60 per barrel. So, Friday was a less volatile but bullish day as traders got ready for the weekend.

For the week, SPY gained 4.00%, DIA gained 2.93%, and QQQ gained 5.47%. This was the best weekly performance for the year in all three. All three major index ETFs also crossed above their Weekly T-line (8ema). In addition, DIA also closed at a new weekly high close.

The major economic news scheduled for Friday included July Building Permits, which came in light at 1.396 million (compared to a forecast of 1.430 million and a June value of 1.454 million). At the same time, July Housing Starts also were light at 1.238 million (versus the 1.340 million forecast and June’s 1.329 million reading). Later, Michigan Consumer Sentiment was better than predicted at 67.8 (compared to the 66.7 estimate and July’s 66.4 number). At the same time, Michigan Consumer Expectations were even more positive at 72.1 (versus the 68.5 forecast and July’s 68.8 value). On the inflation front, Michigan 1-Year Inflation Expectations were flat at 2.9% (compared to a forecasted 2.8% but in-line with July’s 2.9% reading). For the longer-term, Michigan 5-Year Inflation Expectations were also flat at 3.0% (versus a 2.9% forecast and the July 3.0% survey result).

In Fed news, on Friday, Chicago Fed President Goolsbee told NPR that he is leaning toward rate cuts at this point. Goolsbee said, “You don’t want to tighten any longer than you have to…and the reason you’d want to tighten is if you’re afraid the economy is overheating, and this is not what an overheating economy looks like to me.” He did decline to say whether he thought that first cut should be in September. However, he said, “If we move toward less restrictiveness, it will help ease some of these credit conditions.” He then went on to say that he thinks credit conditions appear tight now and he flagged rising unemployment as a “warning sign.” In the end though, Goolsbee signaled his support for a gradual (rather than fast) pace to rate cute. Analysts took this to mean he would support a quarter percent cut rather than a half percent.

In stock news, on Friday, UBS announced it will divest its Quantitative Investment Strategies unit to private Manteio Partners for an undisclosed amount. (The QIS unit manages about $1.5 billion in quant funds.) Later, RIVN said it has temporarily halted production of AMZN delivery vans due to a shortage of parts. (AMZN is RIVN’s largest investor, holding a 16% stake.) Meanwhile, MA announced it will cut 3% of its global headcount (about 1,000 jobs being cut) by the end of September. Later, Reuters reported that BA and LMT are in talks to sell their ULA rocket-launching joint venture to Sierra Space for between $2 billion and $3 billion. At the same time, CNBC reported on noise complaint issues made against AMZN related to its air drone delivery program in College Station, TX. The latest complaints come after AMZN asked for approval to expand its air deliveries in the city from 200 to 470 flights per day and expanding hours of air operations to 7a.m. – 10 p.m. (AMZN drones create up to 60 decibels of noise, which is half that of a chainsaw and more than one-third less than heavy equipment according to OSHA.)

In stock legal and governmental news, on Friday, the US Dept. of Commerce said that TXN will receive $1.6 billion towards the construction of three new facilities under funding approved by the CHIPS Act. At the same time, shareholders of formerly acquired German Postbank rejected a settlement offer from DB. An attorney for the shareholders said the proposal was a “crackhead offer that was dead on arrival.” Later, GSK said it would seek dismissal of an upcoming lawsuit related to Zantac causing cancer. The move followed Thursday’s court ruling in favor of GSK. At the same time, a US Appeals Court threw out Dept. of Transportation safety standards for pipeline operators. (The case was brought by the Natural Gas Assn. of America who argued the Hazardous Materials standards do not provide sufficient benefits to outweigh the costs they would incur to comply.) At the same time, the NHTSA announced that F is recalling 85k Explorer SUVs equipped with the “Police Interceptor” package due to risks of engine fire. The recall covers 2020-2022 model years.

Elsewhere, a federal appeals court narrowed an injunction that blocked enforcement of a CA law aimed at protecting children’s online safety. The court ruled that while the group suing to stop the law is likely to show the law violates the first amendment, but that the lower court failed to recognize than many provisions of the law could survive after removing first amendment concerns. (AMZN, GOOGL, and META are the hallmark members of the group that sued.) At the same time, the State Dept. approved the same of $264 million of RTX missiles to Canada. Later, the FTC filed suit against ABG, alleging that its dealerships charged Black and Latino customers higher prices and routinely added services to customer contracts without consent. Meanwhile, Reuters reported that unsealed documents from a TX court showed that TPX’s proposed $4 billion takeover of Mattress Firm was “intended to eliminate future competition.” At the same time, a US District Judge temporarily blocked the launch of a sports streaming service (joint venture) from DIS, FOX, and WBD based on antitrust claims from smaller rival FUBO.

Overnight, Asian markets were mostly green as only three of the 12 exchanges were left showing red. Japan (-1.77%) was the biggest mover in the region while Thailand (+1.56%) and Malaysia (+1.53%) paced the gains. In Europe, we see a similar picture taking shape. Only three of the 15 bourses are in the red and a couple of those are barely red. The CAC (+0.34%), DAX (+0.15%), and FTSE (-0.04%) lead the region higher in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a flat start to the morning. The DIA implies a -0.02% open, the SPY is implying a +0.01% open, and the QQQ implies a -0.02% open at this hour. At the same time, 10-Year bond yields at down to 3.875% and Oil (WTI) is off three-quarters of a percent to $76.08 per barrel in early trading.

The major economic news scheduled for Monday is limited to US Leading Economic indicators Index (10 a.m.) We also hear from Fed Governor Waller (9:15 a.m.). The major earnings reports scheduled for before the open are is limited to EL and ZIM. Then, after the close, FN and PANW report.

In economic news later this week, on Tuesday, API Weekly Crude Oil Stocks are reported. Fed members Bostic and Barr also speak. Then Wednesday, we get EIA Weekly Crude Oil Inventories and July FOMC Meeting Minutes. One Thursday, Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, S&P Global Mfg. PMI, S&P Global Services PMI, S&P Global Composite PMI, July Existing Home Sales, and the Fed Balance Sheet are reported. The Jackson Hole Symposium also starts. Finally, on Friday we get July Building Permits, and July New Home Sales. The Jackson Hole Symposium also continues.

In terms of earnings reports later this week, on Tuesday, RERE, AS, FUTU, HTHT, LOW, MDT, VIPS, XPEV, ALC, SQM, COTY, JKHY, KEYS, LZB, PAGS, TOL, and ZTO report. Then Wednesday we hear from, ADI, DY, M, TGT, TJX, ZK, A, CAAP, LU, NDSN, SNOW, SNPS, URBN, and ZM. On Thursday, AAP, BIDU, BILI, BJ, CSIQ, IQ, NTES, PTON, TD, VIK, BMA, INTU, ROST, and WDAY report. Finally, on Friday, we hear from GFI.

So far this morning, EL and ZIM reported beats on both the revenue and earnings lines.

In late-breaking news, AMD announced Monday that it will acquire server manufacturer ZT Systems for $4.9 billion (75% cash and 25% stock). This is part of the move toward offering total AI solutions rather than just selling AI Chips or AI processing cards. The industry move is toward being able to sell entire AI computing server racks to corporate clients at a higher margin. Elsewhere, China announced it had made a deal with the US to cooperate on matters of financial stability after talks in Shanghai last week. The PBOC (Chinese Central Bank) said the deal covers capital markets, cross-border payments, and the two country’s monetary policy. A statement on the deal from the US Treasury, SEC, and Fed (agencies that participated in the talks from the US) as well as the details are not yet available. However, the belief is that the talks were aimed at heading off any global systemic risk such as from the volatile and stressed Chinese bond markets.

With that background, all three major index ETFs are just on the green side of flat at the moment. For what it is worth, all three have printed small, white-body candles with lower wicks at this point. All three are still extended above their T-line (8ema) and the short-term trend is clearly strongly bullish. Meanwhile, the mid-term bearish trend is broken, though one could argue a new mid-term bullish trend has not formed yet. In the long-term, we are now clearly back in a Bull trend. In terms of extension, as I mentioned all three are stretched to the upside relative to their T-line. At the same time, the T2122 indicator is now in the lower half of its overbought territory. So, the market is in need of a rest or pullback. With that said, remember the market can remain overextended a lot longer than we can stay solvent predicting a reversal. So, keep the mantra “follow, don’t lead, but also don’t chase” in mind. With regard to those 10 big dog tickers, six of them are in the green, led by AMD (+1.98%). However, the biggest dog (in terms of dollar-volume traded), is down with NVDA (-0.14%) among the laggards.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Markets gapped strongly higher Thursday and then followed through slowly the rest of the day. SPY gapped up 1.05%, DIA gapped up 1.17%, and QQQ gapped up 1.35%. From there, all three major index ETFs rallied until 12:30 p.m. At that point pulled back slightly for 30 minutes and then resumed its rally until 3:45 p.m. Only late-day profit-taking the last 15 minutes kept us from closing at the highs. This action gave us gap-up, white-bodied candles in all three major index ETFs. DIA printed a gap-up, white-bodied, Spinning Top. Meanwhile, SPY and QQQ both gave us gap-up, white-bodied, large-body candles with small wicks on both ends. (Bear in mind, that SPY is up 8.5% in nine days, QQQ is up 12% over that time, and slow, plodding DIA is up 5.5% in the same span.) This all happened on just under average volume in all three of the major index ETFs.

On the day, nine of the 10 sectors were green with Consumer Cyclical (+2.69%) and Technology (+2.46%) out in front leading the gainers higher. At the same time, Communication Services (-0.35%) was the only sector in the red and more than 0.50% worse-performing than the next most lagging sector. Meanwhile, SPY gained 1.71%, DIA gained 1.45%, and QQQ gained 2.53%. VXX fell another 3.82% to close at 45.34 and T2122 climbed into the overbought territory at 89.26. On the bond front, 10-year bond yields spiked to 3.923% and Oil (WTI) gained 1.30% to close at $77.98 per barrel. So, Thursday was the Bulls’ day from the 8:30 a.m. data drop onward. SPY and QQQ crossed back above their 50sma. However, all three major index ETFs are now quite stretched above their T-line (8ema) indicating the need for rest, pullback, and/or profit-taking.

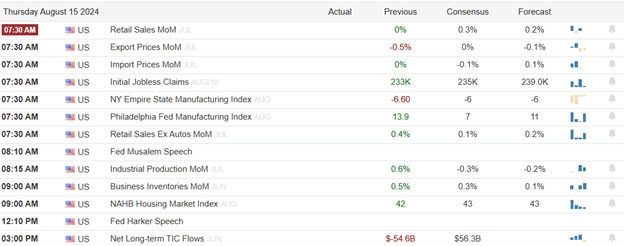

The major economic news scheduled for Thursday included Weekly Initial Jobless Claims, which came in lower than expected at 227k (compared to a 236k forecast and the prior week’s 234k). In terms of ongoing unemployment, the Weekly Continuing Jobless Claims were also down a bit at 1,864k (versus the 1,880k forecast and the prior week’s 1,871k). At the same time, July Core Retail Sales were down a tick, but much better than expected at +0.4% (compared to the +0.1% forecast and the June +0.5% reading). On the headline number, July Retail Sales were very strong at +1.0% (versus a forecast of +0.4% and much stronger than June’s -0.2% value). In terms of manufacturing, the NY Empire State Mfg. Index was bad but better than predicted at -4.70 (compared to a -5.90 forecast and the July -6.60 number). Down the road, the Philly Fed Mfg. Index was worse than anticipated at -7.0 (versus a +5.4 forecast and down sharply from July’s 13.9 reading).

In terms of Manufacturing employment, the Philly Fed Mfg. Employment Index was -5.7 (down from July’s 13.9 value). On the trade front, the July Export Price Index showed an increase of 0.7% month-to-month (compared to 0.0% forecast and June’s -0.3%). At the same time, July Import Price Index was up a tick +0.1% (versus a forecast of -0.1% and June’s 0.0% number). Later, July Industrial Production was down to -0.6% (compared to a -0.3% forecast and June’s +0.3%). Later, June Business Inventories came in as expected at +0.3% (versus a +0.3% forecast and a May +0.5% reading). At the same time, June Retail Inventories were also as predicted at +0.2% (compared to the +0.2% forecast and up a touch from May’s 0.0% value). Later, June TIC Net Long-Term Transactions showed a large increase to +$96.1 billion (versus a +$56.3 billion forecast and well up from May’s -$54.1 billion reading. Finally, after the close, the Fed Balance Sheet showed a small expansion for the week to $7.178 trillion from the prior week’s $7.175 trillion.

In Fed news, on Thursday St. Louis Fed President Musalem indicated he was more open to a rate cut than before. Speaking in KY, Musalem said his confidence (that inflation is going down) was bolstered by recent data. He continued, “It now appears the balance of risks on inflation and unemployment has shifted … the time may be nearing when an adjustment to moderately restrictive policy may be appropriate.” At the same time, in a Financial Times interview, Atlanta Fed President Bostic said he is now open to a rate cut in September (the opposite of his public expressions recently). Bostic said, “Now that inflation is coming into range, we have to look at the other side of the mandate, and there, we’ve seen the unemployment rate rise considerably off of its lows.” He continued, “…and so I’m open to something happening in terms of us moving before the fourth quarter.” Later, Philly Fed President Harker told an economic conference that a rate cut is the next step for monetary policy and the timing may be getting closer. However, he hedged on when that might take place. In response to a question implying an intra-meeting cut, Harker said, “I believe that we may be in the position to see the rate decrease this year … But I would caution anyone from looking for it right now and right away.”

After the close, AMAT, COHR, GLOB, HRB, and LNVGY all reported beats on both the revenue and earnings lines. Meanwhile, AMCR missed on revenue while beating on earnings.

In stock news, on Thursday, LMT announced it has agreed to acquire LLAP for $450 million. Later, GOOGL announced it is expanding its AI-generated summaries of searches to six new countries two months after first rolling out the feature. In addition to the US (where the feature has been available since May), Brazil, India, Japan, Mexico and Britain now have access to AI summaries. After the close, KR announced plans to cut prices by $1 billion after its $25 billion acquisition of ACI closes. (KR had previously promised $500 million in lower prices across all acquired ACI locations.)

In stock legal and governmental news, on Thursday, CVX agreed to pay $550 million to Richmond, CA in a settlement. The deal will see CVX buy the city’s withdrawal of a November ballot initiative that would have sought a tax on refineries in the city. (CVX has a refinery that produces 250k barrels per day inside the city limits.) Later, the FDA laid out new stricter goals for sodium content of packaged foods. In the announcement, the FDA said it was seeking “voluntary curbs” from packaged food makers like PEP, KHC, and CPB. However, fast-food chains such as MCD, QSR (Burger King), and YUM would also be on the hook. The cuts, with a goal of within three years, would cut sodium to 20% below the 2021 levels.

Elsewhere, TEL agreed to pay a $5.8 million fine to the Dept. of Commerce for illegally shipping electronics components to China. Later, the State Dept. approved a $5 billion sale of LMT’s Patriot missiles to Germany. In Canada, the national government rejected the request from CNI (Canadian National Railway) for imposed binding arbitration between the railroad and its Teamster Union employees. (The railroad, along with CP, have said they will lock out employees starting August 22 to avoid an employee strike.) At the same time, a second federal court (this on in FL) has blocked the FTC ban on worker noncompete agreements. Later, a federal judge in CA ruled that PEP can be sued over marketing for its Gatorade Protein bars. (The bars have more sugar than protein, which is more typical of candy bars than protein bars.) At the same time, STLA shareholders filed suit against the company, alleging fraud under the accusation the company concealed rising inventories and sales weakness prior to the company’s July 25 earnings report.

Meanwhile, in CA, Governor Newsom proposed a plan requiring refiners in the state to maintain minimum reserves of gasoline. The measure, aimed at curbing gas prices is aimed at a situation where the states refiners had less than a 15-day supply of gas in inventory 63 days in 2023. (A study found that prices spiked when refiners let inventory fall because they were taking refineries offline to increase prices.) Later, BAYRY (Bayer) won a legal fight Thursday when the US 3rd-Ciruit Court of Appeals rejected a claim by a PA landscraper which alleged the company’s Roundup weedkiller did not carry a warning label and caused his cancer sue to repeated and prolonged use. The court ruled that federal law protects the German parent company from liability from state laws requiring a cancer label.

Overnight, Asian markets were nearly all green. Only Shenzhen (-0.24%) was in the red while Japan (+3.64%), Taiwan (+2.07%), South Korea (+1.99%), and Hong Kong (+1.88%) led broad and strong gains. In Europe, the picture is more mixed with six of 15 exchanges in the red. The CAC (+0.18%), DAX (+0.52%), and FTSE (-0.46%) lead the region in early afternoon trade. Meanwhile, in the US, as of 7:30 a.m., Futures are pointing toward a start just on the red side of flat. The DIA implies a -0.08% open, the SPY is implying a -0.11% open, and the QQQ implies a -0.02% open at this hour. At the same time, 10-Year bond yields are down to 3.873% and Oil (WTI) is off 2.83% to $75.96 per barrel in early trading.

The major economic news scheduled for Friday includes July Building Permits and July Housing Starts (both at 8:30 a.m.), and then Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-Year Inflation Expectations, and Michigan 5-Year Inflation Expectations (all at 10 a.m.) The major earnings reports scheduled for before the open is limited to FLO. There are not reports scheduled for after the close.

So far this morning, missed on revenue while beating on earnings.

In miscellaneous news, on Thursday, GS lowered its Q3 GDP forecast from 2.6% to 2.4% after disappointing industrial production data for July. Elsewhere, Bloomberg reported Thursday that GS is telling clients it expects a rally based on the return of so-called systematic funds. These funds had made the largest dollar-volume selling since the pandemic over the past month, based on volatility index signals. However, now the VIX has returned to the levels seen in May-July in the last week, those funds are and will be returning to the buy-side. Meanwhile, Bloomberg also reported that ADSK is likely to face legal action. It reported internal documents from ADSK that said the company had continued using the sales strategy of offering deep discounts on multi-year deals to corporate customers who pay up front. The company pledged to investors to stop using the tactic in 2021, but internal documents say the company has continued using the strategy in order to pull forward cashflow and meet short-term financial goals.

In late-breaking news, WMT raised its guidance for the full year citing steady consumer health and the relative strength of the overall economy. WMT CFO Rainey said, “…our members and customers…remain choiceful, discerning, value-seeking, focusing on things like essentials rather than discretionary items, but importantly, we don’t see any additional fraying of consumer health.” Still, while raising its full-year 2024 forecast, the numbers do point to a second half that is not quite as strong as the first six months. They are just stronger than earlier predicted. Elsewhere, the Biden Administration released the prices for the first 10 drugs that resulted from the first-ever Medicare price negotiations. BMY, LLY, JNJ, MRK, AZN, NVS, AMGN, ABBV, and NVO are makers of those first 10 drugs subject to price negotiation and the White House says the lower prices will save Medicare $6 billion in the first year (based on 2023 drug demand data).

With that background, all three major index ETFs gapped up modestly to start the premarket. However, all three have also sold off in a more or less volatile way during the early session and are now back to just below flat so far this morning. All three are still extended above their T-line (8ema) and the short-term trend is clearly strongly bullish (even if the Bears could say they’re just in strong Bear Flag patterns). Meanwhile, the mid-term trend remains bearish, but with the downtrend line under pressure. In the long-term, we are now clearly back in a Bull trend. In terms of extension, as I mentioned all three are stretched to the upside relative to their T-line. At the same time, the T2122 indicator is now in the middle of its overbought territory. So, the market is in need of a rest or pullback. Don’t be surprised if we see some Friday profit-taking. With that said, remember the market can remain overextended a lot longer than we can stay solvent predicting a reversal. So, keep the mantra “follow, don’t lead” in mind. With regard to those 10 big dog tickers, six of them are in the green, led by NFLX (+0.46%) and the biggest dog, NVDA (+0.44%) pacing the gains. Finally, remember its Friday. So, prepare your account for the weekend news cycle and also bear in mind that today is options expiration day.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

US equity futures saw modest gains as traders anticipated a busy morning filled with economic data releases. Investors are particularly keen on the upcoming retail sales data, which will provide further insights into the economic trajectory. Additionally, Walmart’s earnings report, scheduled for release before the market opens, is expected to shed light on consumer spending patterns, making it a focal point for market watchers.

On Thursday, European stocks continued their upward trend, buoyed by cooler-than-expected inflation readings that bolstered investor confidence. This positive momentum was further supported by the latest U.K. GDP data, which revealed a 0.6% expansion in the second quarter, aligning with market expectations. The combination of these factors contributed to a generally optimistic outlook for European markets as the week progressed.

In the second quarter, Japan’s economy outperformed market expectations, with its gross domestic product (GDP) rising by 0.8% quarter-on-quarter, surpassing the 0.5% increase anticipated by economists polled by Reuters. Meanwhile, China’s retail sales experienced a year-on-year growth of 2.7%, slightly exceeding the forecasted 2.6% growth. However, the urban unemployment rate in China saw a minor uptick, climbing to 5.2% from 5% in June.

Economic Calendar

Earnings Calendar

Notable reports for Thursday before the bell include WMT, BABA, AIT, CLBT, GRAB, NICE, SPTN, & TPR. After the bell include AMCR, AMAT, COUR, HRB, & ROST.

News & Technicals’

Cisco reported its third consecutive quarter of declining revenue, marking its first full fiscal year drop since 2020. Despite this, the company’s earnings and revenue exceeded analysts’ expectations. In response to the ongoing challenges, Cisco announced a 7% reduction in its global workforce. Prior to Wednesday’s close, Cisco’s stock had fallen by 10% this year, contrasting sharply with the Nasdaq’s approximately 15% gain.

More than a week into Ukraine’s unexpected incursion into Russia’s Kursk region, the gains have likely surpassed Kyiv’s highest expectations. Ukrainian forces now control over 1,000 square kilometers of Russian territory and have captured 74 settlements, according to Ukraine’s top military commander, Oleksandr Syrskyi. While Moscow has yet to mount a significant response, it has warned of a ‘worthy’ retaliation. Analysts suggest that Ukraine faces a critical decision: whether to reinforce its troops and hold or advance its position, or to withdraw before Russia launches what is expected to be a fierce and deadly counterattack.

Starbucks has announced a substantial compensation package for its incoming CEO, Brian Niccol, who is transitioning from Chipotle. Niccol will receive $10 million in cash and $75 million in equity awards upon joining the company. His annual base salary will be $1.6 million, with the potential to earn an additional $7.2 million in cash. As he steps into his new role, Niccol faces the significant challenge of revitalizing Starbucks’ struggling business.

Payments firm Airwallex has achieved an impressive annual revenue run rate of $500 million, driven by substantial growth in its North American and European operations, according to CEO Jack Zhang. Zhang aims to prepare Airwallex for an initial public offering (IPO) by 2026. The company, which was recently valued at $5.6 billion and is backed by Tencent, is considered a strong contender among major fintech IPO candidates.

With a very busy morning of potential market-moving economic data traders should prepare for just about anything. The relief rally is starting to get a little long in the tooth and perhaps today’s data can continue to inspire the bull higher. However, we should not be surprised to see a little profit-taking begin at any time. That said, avoid chasing with the fear of missing out.