As the bulls push for new record market highs this morning, it seems there is no price too high for some stocks with 3rd quarter earnings set to begin this week. With Covid-19 infections rising, some areas have reported hospitals are at capacity. Still, the market seems confident that no matter the impacts, the Fed and the Congress will cover the costs with more debt to keep the market going up. Expect the wild volatility to continue in the week ahead.

Asian markets rose sharply overnight, with the NIKKEI closing up nearly 2.25%. European markets are full-on bullish across the board this morning up more than 1.3%. US futures opened positive and continue to push higher this morning with a gap up open that will set new NASDAQ record highs at the open. Go bulls!

Economic Calendar

Earnings Calendar

This week we begin the 3rd quarter earnings season with the big bank beginning to report on Tuesday. We start the week with a light day with just 9-companies reporting with only one notable report coming from PEP this morning.

News and Technical s

I’m not sure it makes any difference to write about the impacts of coronavirus as the country continues to soar in new infections. As states require the wearing of masks such as Florida after reporting more than 15,000 new infections, protests broke out from groups saying that infringes on their rights. You can’t make this stuff up! If I were writing a novel, it would be so unbelievable it would not sell. Several areas in the country reporting that hospitals are at capacity treating Covid-19 patients, and the death toll in the US is back on the rise. Approaching earings, the market appears to have little to no concern about the pandemic with the expectation that the Fed and Congress will continue to escalate the deficit to keep the market going higher. With the national debt over 26.5 Trillion, the consequences of such spending are apparently irrelevant in today’s society.

Futures began trading last night seeing only bullishness, and that sentiment has only grown as we near the open of the day. The NASDAQ is poised to set another new all-time high at the open, and the SPY will gap above the island reversal that has recently served as resistance. The DIA, which has struggled with the resistance its 200-day average, will gap above it this morning at the open. Gaping to new record highs always carries with it the risk of a potential pop and drop, but with the bulls relentlessly willing to pay any price for stocks ahead of earnings, I would not rule out a big short squeeze sending indexes even higher. Expect wild price action to continue in the week ahead. Stay focused and flexible.

After a modestly lower open and a half-hour of volatility, the bulls stepped in and rallied the entire rest of the day closing near the highs. This left the SPY ending the week where it began after 5 days of consolidation. However, the QQQ continued its massive rally, with TSLA, NFLX, and GOOG pulling markets higher. On the day DIA was up 1.39%, SPY was up 1.02%, and QQQ was up 0.68% to yet another all-time high close. VXX fell to 32.15 and T2122 remains toward the high side of the mid-range at 73.53. 10-year bond yields rose to 0.641% as it was a risk-on day and Oil (WTI) rose back to $40.52/barrel.

In weekend trade developments, late Friday President Trump said the US-China relationship is severely damaged and as a result phase two of a trade deal is not a priority. In fact, he said “he isn’t even thinking about it.” Then on Saturday, the administration announced new tariffs of 25% on French goods (i.e. wine, cheese, cookware, cosmetics, soap, etc.). These tariffs are in retaliation for France not ending its new 3% tax on revenue earned from online sales to French users as the US had demanded. The tariffs are timed to not take effect until January, with the stated reason of giving time for negotiations. However, this move also comes days after Treasury Sec. Mnuchin canceled negotiations on the tax issue and warned retaliation on any country that imposes taxes on American tech giants (GOOG, AMZN, FB, etc.).

In the US, the virus numbers show we have 3,414,105 confirmed cases and 137,787 deaths. As of the weekend, only 3 states are seeing a reduction in the new case rate, while 14 are holding relatively steady, and 33 are increasing. Friday saw a record of 71,000 new cases. On Saturday, that number was 62,000. Then Sunday we saw a 5th straight day over 60,000 new cases. This includes FL reporting a massive 15,300 (4,000 more than the previous 1-day high). In South Carolina, they reported they are now seeing over 22% of all tests coming back positive.

Globally, the number of cases has reached 13,062,360 confirmed cases and 572,214 deaths. On Sunday, the W.H.O. reported 230,000 new cases. In Brazil, they reported 72,000 cases Sunday (on about two-thirds the US population). India reported a record number of cases 5 days in a row as of today. They also announced their 3rd largest city will lock-down for a week starting Tuesday. Meanwhile, in the UK, the government is now making a major push for economic recovery. Sunday, they encouraged workers to go back to the office (as opposed to working from home) if at all possible in an effort to stir retail activity. The MP (Gove) who announced this also said it should be up to individuals, not the government, as to whether people wear masks in shops, bars, and restaurants.

Overnight, Asian markets were mostly strongly green, with a couple of minor red exceptions being Thailand and Singapore. Shenzhen was up almost 3.5% and the NIKKEI up 2.22%. In Europe, we’re seeing a similar story with only Russia and Greece below flat. The big 3 bourses (FTSE, DAX, CAC) are all up about 1.3% at this point in their day. As of 7:30am, US futures are all pointing to a gap higher of about 0.80% at the open.

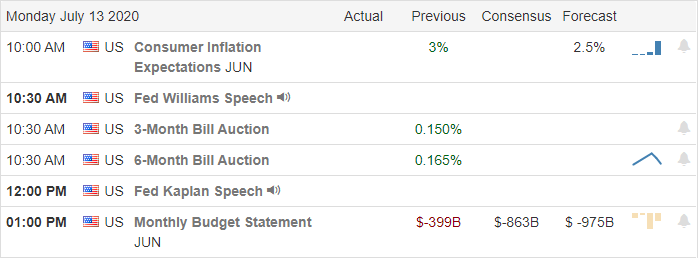

The only major economic news for Monday is the June Federal Budget Balance (2 pm). The only major earnings report for the day was PEP before the open and they reported a 3.1% revenue fall for the quarter, but beat on earnings ($1.32 vs 1.25). There was also a deal announced with chipmaker ADI buying MXIM in an all-stock deal.

Friday’s candles were very Bullish, albeit within a consolidation in large-caps (SPY). However, the QQQ continues to rip. Are the QQQs extended? Absolutely. However, that doesn’t mean they must reverse today. And the bulls look like they want to run again this morning with absolutely no fear of the pandemic. Still, keep an eye on those “canary in the coalmine” FAANG stocks. If they were to break, so will the market. If they maintain their rally, there is nothing the rest of the bears can do to fight that momentum. So, watch the short-term chart and don’t chase, don’t predict, and take profits as you go. And also keep in mind that Earnings Season starts again Tuesday.

Ed

The Daily Trade Ideas have been moved back to this space at the request of members. Today’s trade ideas are HD, PBR, XHB, VALE, LULU, CNP, XRT, GLW, CWH, MGA. Trade your plan, take profits along the way, and smart. Also, don’t forget to check for upcoming earnings. Finally, remember that the stocks/ETFs we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

As we head into the weekend, the tech giants continue to lead the way setting new records while DIA, SPY, and IWM experience some selling pressure. At the same time, 18 million Americans remain unemployed as more than 1.3 million files for benefits. That nearly doubles the number we experienced in the depths of the 2008 and 2009 depression. The VIX continues to display the uncertainty the market faces as a select few stocks continue to rise to new price highs.

Asian markets closed the day lower across the board as virus infections weigh on recovery hopes. However, European markets are bullish this morning in reaction to hopeful Italian data. US Futures have recovered from overnight lows suggesting modest declines at the open ahead of a very light day of earnings reports and pending PPI data.

Economic Calendar

Earnings Calendar

On Friday’s earnings calendar, we have a light day with just 11 companies stepping up to quarterly results. The report from SJR is the only particularly notable report I see. Remember, the official kick-off to the 3rd quarter earnings season begins next week.

News and Technical’s

Another day of records with the NASDAQ reaching out to new highs while at the same time coronavirus infections in the US topped 63,000 for the first time. More than 1.3 million filed for unemployment last week, and the concern is that the numbers may now start to grow as states struggle in their efforts to recover with the recent surge in the pandemic infections. It’s interesting to note that even at 1.3 million, the number is double the worst numbers we experienced in the depression of 2008 and 2009. A day after the Supreme Court rules against the President, his competitor calls for an end of the era of shareholder capitalism, suggesting higher corporate taxes. Tensions continue to grow as following the impositions of sanctions of three local Chinese officials of China’s ruling Communist party over human rights abuses. China vows to retaliate.

As we head toward the weekend, the imbalance between the tech giants continues with the QQQ holding on to a strong uptrend while the DIA, SPY, and IWM experience selling pressure. I have to wonder what happens to the market if or when profit taking begins in the tech sector. The VIX continues to suggest a considerable uncertainty exists as it seesawed between a low of 26 and a high of 31 handles yesterday. Facing a light day on both the economic and earnings calendar, the market could be sensitive to the news cycle, and price action is likely to remain volatile. Next week begins the 3rd quarter earnings season, which is likely to keep the wild price action going into the near future. Stay focused and flexible, carefully considering the risk you carry into the weekend.

Markets opened modestly higher Thursday on slightly better than expected Initial Jobless Claims. However, this was met with an immediate and strong selloff that took us to the lows by 11:30 am. While bulls rallied up off these lows, they were never able to climb back to flat. The NASDAQ closed at yet another record high close as AMZN, AMD, and NVDA almost single-handedly held markets up. At the close, SPY was down 0.50%, DIA down 1.32%, and, as noted, QQQ up 0.84%. The VXX also climbed a bit to 33.06 and T2122 (4-week New High/Low Ratio) edged closer to overbought territory at 73.75. 10-year bond yields fell sharply to 0.607% as money chased bond safety. And Oil (WTI) also sold off to $39.48/barrel.

Treasury Sec. Mnuchin told CNBC Thursday that the White House will not back the kind of sweeping coronavirus relief they supported before. Instead he said they would only accept a smaller, narrower package. As often happens in the Administration, this seems to be at odds with the President’s own words from a week ago (when he said he wanted to give away more money than the Democrats, but just “to do it right”). However, it does line up with consistent statements out of Senate Republicans. Either way, Congress will return in just under two weeks to resume negotiations and votes.

In other political-market news, Democratic Presidential nominee Biden laid out his “Moderate plans for an economic recovery.” Among other things, he said that “(the wealthy investor class) don’t need me.” The plans he announced include the raising of corporate tax rates to 28% (the mid-point between prior corporate rates and the current 21% rate President Trump pushed through.)

In the US, the virus numbers show we now have 3,220,559 confirmed cases and 135,828 deaths. This includes another record of over 62,000 new cases reported nationally. A dozen states reported a record-high number of new cases Thursday. Among them, CA, FL, and TX all reported record virus-related deaths on the day. In FL, Miami-Dade County recorded a 33% positive result rate on all tests processed Thursday. Meanwhile, Dr. Fauci (NIH) told the Wall Street Journal “any state that is having a serious problem, that state should seriously look at shutting down.”

Globally, the number of cases has reached 12,420,723 confirmed cases and 558,091 deaths. In a huge case of stating the obvious, the W.H.O. reported “the pandemic is getting worse” on a day when the world reported a record number of new cases (227,000). Among the countries reporting record-high new case counts were the US and Mexico, both of which reported a daily record in both cases. However, even though Brazil did not report a record number of new cases, Mexican numbers still pale in comparison to Brazil who reported almost 43,000 new cases and over 1,200 deaths on the day.

Overnight, Asian markets were red across the board with the lone minor exception of Malaysia. In Europe, markets are mixed, but mainly green at this point in the day. The big 3 bourses (FTSE, DAX, CAC) are all up half a percent. As of 7:30am, US futures are all pointing to a modestly lower open.

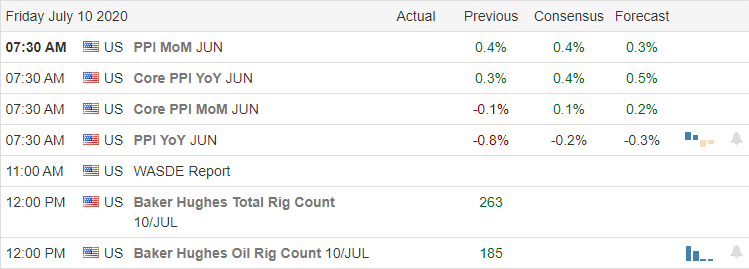

The only major economic news for Friday is June Producer Price Index (8:30 am). The only major earnings report for the day are GBX before the open and SJR after the close.

Thursday’s candles were fairly ugly, with a Bearish Engulfing signal in SPY and DIA. However, despite this, a consolidation pattern is all we can point to in those two indices, especially since the mega-cap techs continue to pull the entire market higher. Are the QQQ extended? Absolutely. However, that doesn’t mean they must reverse today.

Keep an eye on those “canary in the coalmine” FAANG stocks. If they break, so will the market. If they maintain their rally, there is nothing the rest of the bears can do to fight their momentum. So, keep an eye on the short-term chart and don’t chase, don’t predict, and take profits as you go. Also, remember its payday. Take some profits off the table and/or hedge you positions in front of the weekend.

Ed

Daily trade ideas have been moved to the trading room and the Members-Only Phone App. Trade your plan, take profits along the way, and smart. Also, don’t forget to check for upcoming earnings. Finally, remember that the stocks/ETFs we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

As the Nasdaq prints, another record high the US also sets a new national record of Covid-19 infections and health officials as calling for a federal policy to curb the spread. While on the surface, the market appears to have absolutely no concerns, yet the VIX remains quite elevated, and the Absolute Breadth Index continues to decline. An interesting dichotomy that could produce a bullish short squeeze or an attack by the bears as recovery concerns mount. Stay focused and flexible as the market grapples with what comes next.

Asian markets continue their bullish run with week lead by China, which rose 1.39%. European markets have seesawed between gains and loss this morning as they cautiously monitor pandemic numbers and the challenging recovery. Ahead of a light day of earnings and another round of jobless claims US futures point to a slightly lower open.

Economic Calendar

Earnings Calendar

On the Thursday earnings calendar, we have just 11 companies reporting quarterly results. Notable reports include WBA, BNED, FC, HELE, PSMT, & WDFC.

News and Technical’s

The bulls refuse to lose continuing to buy up the big tech giants with NASDAQ setting another record high lead by AAPL, which also closed the day at a record high. As the market continues to surge, so does the pandemic infections, hitting a new national record of 60,000 new cases reported in a single day. Health officials are calling for a federal policy action to curb the spread of the virus, suggesting another shutdown may be necessary. A new study warns of a potential wave of brain damage as an aftereffect of Covid-19 infections. The research shows patients suffering from temporary brain dysfunction, strokes, nerve damage, or other serious brain effects. A scary thought considering the US is now dealing with more than 3 million that have already been affected by the virus. According to reports, there is already a noticeable pullback in driving activity as people choose to stay home rather than risking infection. United Airlines warns that half of its workforce may be furloughed, suggesting up to 36,000 people could see their jobs cut as recovery hopes fade in the recent weeks. Bed Bath & Beyond announced they would close 200 stores after reporting a sharp sales decline of nearly 50%, and the Pier One said it would not reopen retail stores in their bankruptcy reorganization moving to online sales only.

Technically speaking, the DIA, SPY, and IWM indicate a possible higher low could be forming after yesterday’s rally, yet at the same time struggling with overhead resistance and potentially bearish candle patterns. Adding to the confusion is the fact that the VIX remains elevated, and the Absolute Breadth Index continues to decline. I see the potential for a bullish short squeeze and, at the same time, see the possibility that the bears could soon attack at any time due to growing recovery concerns. It’s also odd to see indexes setting new records while at the same time precious metals continue rally sharply. Ahead of weekly jobless numbers, the futures currently point to a slightly lower open. Stay focused on price action and remain flexible and prepared for just about anything.

Stocks gave us another volatile day, but the bulls came out on top again. All 3 major indices closed at or near the highs as AMZN, AAPL, FB, and MSFT led markets higher with new all-time high closes. However, the large-caps did not eliminate the lower-high possibility. On the day, SPY was up 0.76%, DIA up 0.65%, and QQQ up 1.32%. The VXX sold off a little to 32.55 and T2122 climbed back into the mid-range at 51.65. 10-year bond yields rose to 0.666% and Oil (WTI) also rose slightly to $40.88/barrel.

In the aviation industry, late in Wednesday’s session BA competitor Airbus reported a third straight month of zero plane sales (new orders). Earlier in the day, UAL had warned 36,000 front-line employees (more than a third of their staff) of potential layoffs and furloughs in 60 days (federal law requires that much notice). It was also reported (rumors, not announcement) that the 5 largest airlines had reached a deal with the Treasury Dept. for massive loans. So, aviation names may be worth watching.

After the close, St. Louis Fed President Bullard said in an interview that he is predicting unemployment will fall back to 7% by year-end. (His previous estimate was over 10%.) This came as part of a mostly optimistic outlook that downplayed the problems facing the economy. (This stands in contrast to 3 of his counterparts who emphasized the risks facing the economy on Tuesday.) He also said he expects another major fiscal stimulus bill, giving the economy “plenty of resources.” So, there are diverging opinions of the economy among Fed members, perhaps as should be expected, but all of them are saying that more stimulus is needed and will likely happen. Stocks will like that.

In the US, the virus numbers show we now have 3,159,514 confirmed cases and 134,873 deaths. For Wednesday, the new case count was 58,000 and 820 deaths. CA Governor Newsom said Wednesday that the state has the capacity to treat 50,000 virus patients. (For reference the state now has a 7-day average of over 8,000 new cases/day, though obviously not all cases require hospitalization.) In partially related news, BBBY reported they will close 200 stores over the next 2 years in an effort to get back toward profitability in the Covid-19 era.

Globally, the number of cases has reached 12,196,923 confirmed cases and 552,771 deaths. In Asia, Tokyo reported a record-high number of new cases and Hong Kong also reported a new outbreak (though still not the highest they’ve seen). Australia’s case surge continues and, alarmingly, only a small percentage of new cases have been traced to a known case or location (implying the virus has spread more widely than previously thought).

Overnight, Asian markets were mixed but mostly green with only smaller markets like New Zealand, Singapore, Malaysia and Indonesia in the red. In Europe, markets are even more broadly mixed, but on smaller moves either direction. Among the major European bourses, FTSE is down, DAX is up, and the CAC is flat at this point. As of 7:30am, US futures are also mixed and closer to flat, likely waiting on the Jobless claims to push one way or the other.

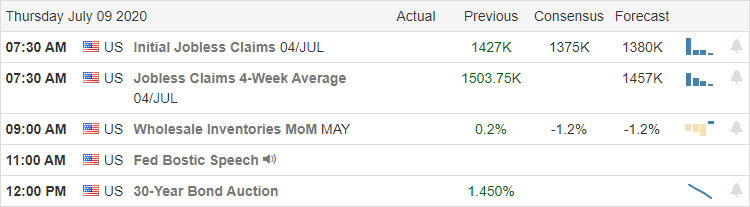

The only major economic news for Thursday is Weekly Initial Jobless Claims (8:30 am). The only major earnings report for the day is WBA before the open.

Wednesday’s candles showed once again that the bulls have strength. However, they did not signal a massive rally surge. Instead, it still seems like the bulls have paused to take a breath after last week’s rally. The short-term consolidation remains in place for the large-caps. However, the mega-cap tech names have been pulling markets (especially the QQQ) higher for quite some time. The “canary in the coal mine” is going to be those FAANG stocks. If they break, so will the market. If they maintain their rally, there is nothing the rest of the market can do but follow. So, keep an eye on those tickers and don’t chase, don’t predict, and take profits as you go.

Ed

Daily trade ideas have been moved to the trading room and the Members-Only Phone App. Trade your plan, take profits along the way, and smart. Also, don’t forget to check for upcoming earnings. Finally, remember that the stocks/ETFs we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

With coronavirus surging around in many US states, the business remains under tremendous pressure with additional closures and further delays of reopening of the economy. The huge back to the school shopping season is also in question as school districts and parents grapple with the difficult decisions of reopening and child safety. Yesterday’s mild selloff left more questions with bearish candle patterns appearing on the index charts at possible highs or near resistance levels. With the VIX rising in yesterday’s close expect price volatility to remain high and extreme sensitivity to news events.

Asian markets closed mixed but mostly higher, with Shanghai rising 1.74%. European markets are seeing modest declines across the board this morning as the surge in pandemic infections worries investors. US Futures chop around the flat-line this morning with a light day of earnings and economic news.

Economic Calendar

Earnings Calendar

On the Hump day earnings calendar, we have just 14 companies expected to report quarterly results. Notable reports include BBBY, MSM & SMPL.

News and Technical’s

US coronavirus infections have topped 3-million cases with states reporting more than 55,000 instances yesterday and 993 deaths. Arizona has seen a 26% increase in infections with the WHO suggesting just a 5% increase is troubling. In response to rapidly rising cases and hospitalizations, Texas canceled the state fair while San Francisco delays reopening indoor dining. It’s no wonder that parents have concerns about sending their children back to school this fall, and retailers worry about the back to the school shopping season. The President is suggesting he will do all he can to pressure schools to reopen. Tensions between the US and Chiana continue to grow after the FBI Director slammed their government for the use of espionage and cyberattacks against the United States. He said the stakes could not be higher, and the potential economic harm to American business as a whole almost defies calculation. These comments come on the heels of the Secretary of State threatening to ban Chinese social media apps.

After a gap down open, the bulls once again attempted a rally to test resistance levels but found resistance and ultimately selling off by the close. Potential bearish candle patterns such as an abandoned baby pattern or evening star patterns were left behind on the DIA, SPY. The QQQ left behind the uncertainty of a shooting star pattern, and the VIX rose above a 29 handle. Declining issues far outpaced advancing issues after the Schwab pointed out that 90% of the current market rally is attributed to just the top 10% of companies. This colossal imbalance raises the question, what happens to the market should these tech giants begin to selloff? An interesting question to ponder as we head for a relatively flat open with a light day of earnings and economic news.

Stocks gapped down half a percent perhaps following Europe and perhaps in profit-taking after the recent run-up. In either case, there was a morning rally to fade that gap and take markets higher. However, then an all-afternoon selloff took over with prices closing near the lows. This brings the possibility of a new “lower high” in charts of the large-caps, but the QQQ remains solidly bullish in trend. On the day, SPY fell 1.03%, DIA fell 1.51%, and QQQ fell 0.69%. VXX gained 3% to 33.39 and T2122 fell near oversold territory at 22.46. The 10-year bond yield fell to 0.64% as money bought up bonds and Oil (WTI) fell slightly to $40.49/barrel.

During the afternoon, FB reportedly had a bad call with the organizers of the advertising boycott they are suffering. Multiple outlets report the call “didn’t go well” as the company failed to address any of the boycott’s 10 demands. So, no change in the positions of the sides, but FB is apparently unfazed since their top advertisers aren’t participating in the boycott and the stock is trading near all-time highs. This all came as a 2-year audit of FB civil rights record (commissioned by FB and carried out by a former ACLU executive) found shortcomings and a mixed record at best as outlined in a 100-page report released this morning.

Three Fed speakers (Bostic, Mester, Daly) also spoke Tuesday and all said problems remain in the economy. More importantly they see a leveling or even slowing in the recovery over the last week or two. All three said additional fiscal stimulus is needed from Congress and the White House. They also all reiterated that they don’t foresee Fed tightening or any reduction of monetary stimulus until at least 2022-2023.

In the US, the virus numbers show we now have 3,097,538 confirmed cases and 133,991 deaths. This includes 60,000 new cases on Tuesday as 36 states are reporting at least a 5% increase in their 7-day average of new cases. Among them, TX reported more than 10,000 new cases on Tuesday (a record) as their positive test rate sits at 13.5%. FL is also seeing a huge spike in test positivity with 16.3% of tests coming back positive. However, there has seen a little decrease in actual new cases, which was welcome as 78% of the state’s hospital beds and 83% of the state’s ICU beds are filled. In NJ, movie theatre chains AMC and CNK have filed a lawsuit against the state, claiming that keeping theatres closed is unconstitutional. Meanwhile, Dr. Birx (White House Task Force) told Bloomberg she praises those governors who have mandated masks despite the President’s resistance, citing TX Governor Abbott specifically.

Globally, the number of cases has reached 11,980,389 confirmed cases and 547,321 deaths. In Spain, there was a blow to hopes for those who support the idea of “herd immunity.” A study has found that only 5% of the Spanish population has antibodies, despite being one of the countries hit hardest in the percentage of population contracting the disease. (For reference, experts say 70% would need antibodies to provide effective herd immunity). The surge in cases also continues in Latin America, with Mexico, Brazil, and several other countries South of the Border reporting record increases.

Overnight, Asian markets were mixed again. China was up almost 2% and Hong Kong was also solidly green. However, Japan, Australia, and India were all solidly red while South Korea was down a quarter of a percent. In Europe, markets are red across the board, but on smaller moves. The minor exceptions to that rule are Greece and Norway, which are just on the green side of flat at this point of the day. As of 7:30am, US futures are all just on the green side of flat at this point.

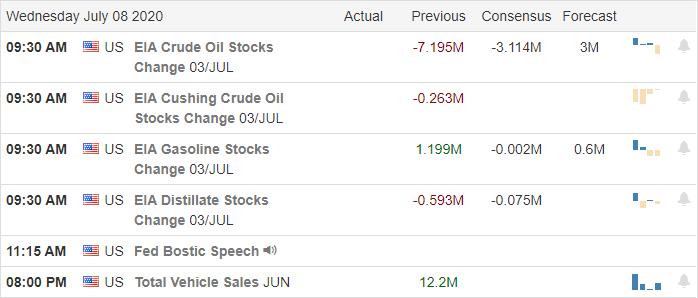

The only major economic news for Wednesday is Crude Oil Inventories (10:30 am). The only earnings reports for the day are MSM before the open and BBBY after the close.

Tuesday’s candles were ugly. However, the bears still showed no teeth with no panic or heavy selling pressure coming in. Instead, it just seemed like the bulls paused to take a breath rather than actually showing fear of the virus surge. With that said, we have to respect the lower-high if we get follow-through today by the large-caps. So, take care of getting too bullish, but also remember the only bearish traders that have not been punished in recent months are those that are fast and obey their stops. Keep an eye on the short-term chart. Don’t chase, don’t predict, and don’t be greedy (take profits and move your stops as you go).

Ed

Daily trade ideas have been moved to the trading room and the Members-Only Phone App. Trade your plan, take profits along the way, and smart. Also, don’t forget to check for upcoming earnings. Finally, remember that the stocks/ETFs we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The NASDAQ lept higher yesterday, setting new records while the Dow, SP-500, and Russell struggled to find follow-through to break price resistance levels. In a pattern that’s becoming all too familiar of late, the big morning gap struggled to find buyers or sellers as it chopped sideways the majority of the day. This morning with the EU forecasting an 8.3% economic slump and the US states beginning more business shutdowns, it looks as if the big gap this morning will be down trapping those that chased in yesterday.

Asian markets closed mixed but mostly lower overnight. European markets fall on concerning economic data with the DAX, FTSE, and CAC down 1% or more this morning. US Futures in reaction to virus-related business uncertainty suggest a substantial gap down at the open ahead of a light day of earnings and economic reports.

Economic Calendar

Earnings Calendar

On the Tuesday earnings calendar, we have 10-companies fessing up to quarterly earnings. Notable reports include LEVI and PAYX.

News and Technical’s

We have reached nearly 3 million coronavirus cases in the United States, with several states doubling infection rates in just two weeks. Florida is once again closing restaurants, health clubs, and group party venues, and some areas in Texas are reaching hospital capacity. Australia closed interstate borders in an attempt to slow the spread of the pandemic, and the Governor of California asks indoor business to close. With more and more states adding to shutdown orders and mulling future restrictions, it would seem the economic recovery continues to face considerable challenges. As tensions grow with China, the US is conducting war games in the South China Sea and, at the same time, looking at banning social media apps such as TikTok. During the night, the EU cut its economic forecasts for the region and is now projecting an 8.3% decline in the economy this year.

Yesterday’s big morning gap struggled to find follow-through buyers spending most of the day chopping sideways. The DIA, on a last-minute surge at the end of the day, breached the resistance of its 200-day average. Although the SPY tried hard to break the resistance of the early June island reversal pattern, it closed the day, failing to breakthrough. The QQQ lept higher with the tech giants leading the way while the IWM closed the day lower once again, unable to reach its 200- day average. With a light day of earnings and economic news, the market seems to have turned its attention to the impacts of the viral surge that is prompting business shutdowns in several states. As of now, the US futures are pointing to a gap down open that has the potential to create abandoned baby patterns at resistance in the DIA and SPY. With the VIX remaining elevated, expect the wild price volatility to continue today.

Markets gapped higher Monday, following Europe and Asia in follow-through to the pre-holiday rally. After a volatile session (volatile above the gap), prices closed not too far from the highs. The mega-cap tech names led the way with AMZN up almost 6%, leading to another all-time high close in the QQQ. On the day, SPY closed up 1.53%, DIA up 1.77%, and QQQ up 2.46%. The VXX closed down just slightly to 32.28 and T2122 remains in the mid-range at 63.46. 10-year bond yields closed up to 0.678% and oil was up slightly to $40.65/barrel.

After the close, Fitch reported that commercial mortgages posted the largest increase in delinquencies ever in June, with 3.6% of all commercial mortgages now delinquent. Unsurprisingly, hotels (11.49% delinquent) and retail (7.86% delinquent) lead the list. Retail consultancy ShopperTrak also told CNBC that consumers have begun to retreat again as virus cases surge. The last two weeks of their retail store surveys show a decline in shopper traffic for the first time since the first week of April.

Last night, Secretary of State Pompeo told Fox News that the US is looking at banning TikTok (who cooperates with Chinese authorities) and Chinese social media apps in a clear attempt to ratchet tensions. What is unclear is how the US would legally do that and what benefit the US gains from such action. For that matter, it’s unclear how such a move would negatively impact China. However, what is obvious is that US-companies like FB, TWTR, GOOG and other social platforms will be in the cross-hairs from the Chinese side if any such measures are taken by the US.

In the US, the virus numbers show we’ve now topped 3 million cases at 3,041,129 confirmed cases and 132,993 deaths. We recorded another 50,500 cases Monday with 32 states reporting an increasing rate of new infections. However, the daily death count continues to fall with the 7-day average just over 500/day. In TX, the military deployed medical personnel at the request of FEMA as hospitals around San Antonio are feeling the strain of virus cases. Still, at least at this point, this is a very small deployment compared, for example, to the military support sent to New York in April. In CA, Governor Newsom “asked” more of its counties to close indoor venues and businesses as the stat’s positive result rate has climbed to 6.8%.

Globally, the number of cases has reached 11,770,153 confirmed cases and 541,490 deaths. In Europe, the EU cut its GDP forecast from an already abysmal 7.4% contraction (May forecast) to an 8.3% contraction for 2020. In Brazil, their President has canceled all his events for the week and was taken to hospital for coronavirus testing after “feeling unwell” and showing a high fever. He was released, but was wearing a mask and told people to stay away from him as a safety measure upon release.

Overnight, Asian markets were mixed. China was well into the green, but Japan, Hong Kong, and South Korea were all well into the red. In Europe, their own economic data and fear over the US virus surge has markets red across the board. The big 3 bourses are all down over 1.1% at this point in their day. As of 7:30am, US futures are looking to follow Europe, pointing toward a gap down between half a percent (QQQ) and 1.05% (DIA).

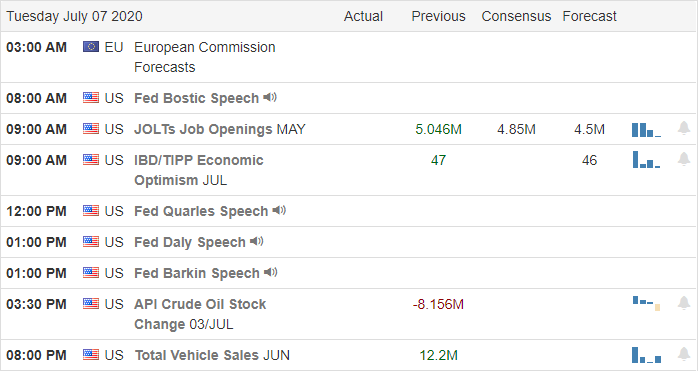

The major economic news for Tuesday is limited to May JOLTS (10 am). However, there are 3 FOMC speakers, Bostic (9 am), Quarles (1 pm), and Daly (2 pm). The only earnings report for the day is PAYX before the open.

The bulls have shown no fear of bad economic or the virus surge. Along those lines, the bears have shown no teeth recently either. With that said, markets may need a rest (especially the QQQ). So, an inside day might not be a bad thing at all. Either way, continue to be careful, but don’t buck the bullish trend unless you are fast. Don’t chase, don’t predict, and don’t be greedy (take profits and move your stops as you go).

Ed

Daily trade ideas have been moved to the trading room and the Members-Only Phone App. Trade your plan, take profits along the way, and smart. Also, don’t forget to check for upcoming earnings. Finally, remember that the stocks/ETFs we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service