U.S. futures point to a mixed bag this morning, with the QQQ gapping higher after the strong earnings performance from MSFT, while the Dow points to a substantial gap down. Although AMD and TXN topped earnings expectations, they indicate a lower this morning. With a big day of earning and economic data that includes an FOMC announcement, traders should prepare for just about anything to occur in price action. It would not be a surprise to see more index gaps tomorrow with AAPL, TSLA and FB reported after the bell today.

Asian markets closed overnight with mixed results after the IMF raised the global economic growth forecast. However, European markets trade decidedly bearish this morning as they keep an eye on earnings results. U.S. indexes face a mixed open ahead of a blizzard of market-moving data. Buckle up it could be a wild ride for the next couple of days.

Economic Calendar

Earnings Calendar

As the number of earnings ramp-up, the Wednesday calendar adds more market-moving tech reports. Notable reports include TSLA, ABT, AMP, ANTM, AAPL, T, ADP, BX, ADP, BX, BA, EAT, CP, GLW, CREE, CCI, DRE, FB, GD, HES, LRCX, LVS, LEVI, MKTX, NDAQ, NSC, NG, PKG, NOW, SYK, TER, VFC, & WHR.

News & Technicals’

A strong round of tech earnings after the bell sees the QQQ popping higher as MSFT add sales surprised the market. However, we face a mixed bag of index reactions this morning. As you would expect, MSFT is indicated sharply higher at the open but, the good vibes seem to stop there with AMD, and TXN indicated lower despite topping expectations. President Biden orders an additional 200 million doses of vaccine and suggests that things are likely to worsen before getting better. He went on to say an expectation of half a million deaths by the end of February is possible after yesterday’s death toll topped 4000 once again. Goldman Sachs CEO David Solomon will see his pay cut by 10 million after the company admitted wrongdoing in the 1Malysia Development Berhad scandal. That’s roughly 36% of his yearly salary, and, of course, no one will go to jail.

Today we traders face a blizzard of data beginning with Durable Goods Orders and FOMC Announcement and a huge round of earnings that will include APPL, TSLA & FB after the bell. Futures are all over the place this morning, with the Dow indicating a gap down of 200 points while QQQ points to a gap higher. Expect the wild volatility to continue, but don’t be too surprised if price action becomes choppy after the open as we wait for Powell and the highly anticipated reports after the close. Anything is possible, so stay focused and flexible as the drama unfolds.

Markets gapped up slightly on Tuesday, but then ground sideways with a slight bearish lean. This action resulted in Dark Cloud Cover candles in the SPY and DIA and a Doji in the QQQ (which also closed at yet another all-time high close). However, overall, it was a flat day in which SPY lost 0.16%, DIA lost 0.08%, and QQQ gained 0.15%. VXX rose less than a percent to 17.20 and T2122 fell back further into the mid-range at 63.01. 10-year bond yields were flat at 1.033% and Oil (WTI) was also flat at $52.75/barrel.

After the close, AMD and MSFT both posted beats on both the top and bottom line. In fact, AMD revenue was up 45% for the year in 2020 and said they expect 37% revenue growth in 2021. For its part, MSFT revenue rose 17% on an annual basis (up from 12% the prior quarter). Meanwhile, SBUX beat earnings estimates despite a 5% drop in same-store sales for the quarter as the company announced its COO is leaving to take a CEO role elsewhere. However, the company missed on the earnings line.

Weekly mortgage demand fell again by 4%, but remain 16% higher than a year ago. This comes as 30-year fixed rates rose from 2.92% last week to 2.95% in the most recent week. However, the housing boom price inflation is being reflected in the size of mortgages. This is reflected in the average new loan amount being at a record $395,200.

Related to the virus itself, US infections continue to rage as the US. The totals have risen to 26,011,222 confirmed cases and 435,452 deaths. The number of new cases fell in 47 states again as the average new cases has fallen to 171,270 new cases, but deaths rose again and remain high at 3,417 per day. In fact, with 5 days left, January is already the deadliest month so far in terms of the virus. President Biden announced the purchase of 200 million more doses of vaccine and set a goal of American life returning to normal by the end of summer. This new purchase includes 100 million doses from each PFE-BTNX and MRNA. In addition, the administration announced that next week the shipments to states will increase from 8.6 million doses/week to 10 million (a 16% increase), to be distributed based on state populations. Finally, JNJ says it is optimistic that Phase 3 trial result data on their own vaccine will be available to be submitted next week.

Globally, the numbers rose to 100,929,027 confirmed cases and the confirmed deaths are now at 2,169,680 deaths. In good news, the world’s average number of new cases is down again to 585,431 per day, but deaths remain high at 14,331 new deaths per day. Ireland extended its national lockdown until March 5. In Germany, the capital city of Berlin will now require two tests instead of one for everyone being tested in an effort to detect new variants earlier and prevent the closure of any more hospitals. In an effort to prevent a situation like the AZN vs EU tension over vaccine delivery, French drugmaker Sanofi has struck a deal to license the PFE-BTNX vaccine and will make 125 million doses of the vaccine exclusively for the EU.

Overnight, Asian markets were mixed on moderate moves. Japan (+0.31%), Shenzhen (+0.28%), and Taiwan (+0.27%) were among the winners. South Korea (-0.57%), Hong Kong (-0.32%), and Australia (-0.65%) were among the losers. India (-1.91%) was a outlier to the downside. In Europe, markets are strongly red across the board. The big 3 bourses show FTSE (-1.00%), DAX (-1.72%), and CAC (-1.27%) as of midday. At 7:45 am, US Futures are also pointing toward a significant gap down. The DIA is implying a -0.88% open, the SPY implying a -1.02% open, and the QQQ implying a -0.66% open.

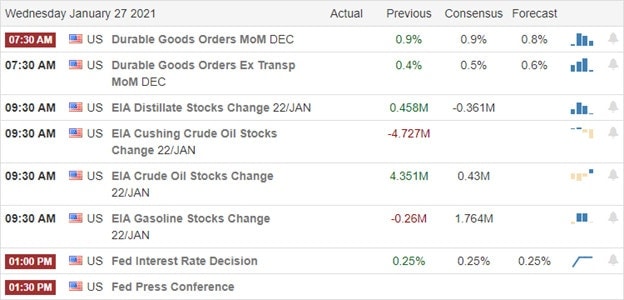

The major economic news for Wednesday includes Dec. Durable Goods Orders (8:30 am), Crude Oil Inventories (10:30 am), FOMC Rate Decision and FOMC Statement (2 pm), and the FOMC Press Conf. (2:30 pm). Major earnings reports on the day include ABT, APH, ANTM, T, ADP, BX, BA, EAT, GLW, GD, HES, KNX, NDAQ, NSC, OSK, PGR, TEL, TDY, TXT, and VFC before the open. Then after the close, AMP, AAPL, AVT, CACI, CP, CCI, EW, FB, HOLX, LRCX, LSTR, LVS, LEVI, and MTH report.

Despite strong earnings from major players, markets seem poised to drop at the open, perhaps on profit-taking new all-time highs or maybe on fear over what the Fed will do. Regardless, watch your longs closely and be cautious chasing any new positions at the moment.

There will be another day and another trade. Don’t feel like you have to trade every day. That’s one of the benefits of trading. We can take a day off when conditions (or our mood) warrants. As always, follow the trend, respect support and resistance, and don’t chase the moves you missed. Lock in your profits when you achieve trade goals and stick to your discipline. Remember, trading is a long-term game. We don’t have to try to get rich every day.

Ed

Swing Trade Ideas for your consideration and watchlist: AAOI, SIG, MJ, AG, FCEL, BLNK, SRNE, PLUG. You can find Rick’s review of those tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

We started the week with a nasty price action whipsaw in the indexes that kicked the VIX briefly above a 26 handle. Let it serve as a reminder of just how quickly and punishing a market reversal can be when indexes with indexes so elevated as earnings season ramps up. The bulls ultimately won the day defending price support and trends, but note that the bears are starting to show a bit more aggression as of late. Today, we will hear from our first tech giant, MSFT, after the bell. Prepare for the possibility of substantial morning gaps as a result.

Asian markets closed in the red across the board last night, with the HIS retreating 2.55%. However, the European markets are in bullish mode this morning despite vaccine challenges focused on earnings hopes. U.S. Futures point to modest gains this morning ahead of earnings and the latest reading on Consumer Confidence at 10 AM Eastern. Expect price volatility to continue and plan your risk carefully with market-moving reports after the bell and FOMC decision Wednesday afternoon.

Economic Calendar

Earnings Calendar

On the Tuesday earnings calendar, we a busy day and dig in the tech giants’ reports after the bell. Notable reports include SBUX, MSFT, MMM, AMD, ALK, AXP, ADM, CHRW, CNI, COF, CIT, DHI, FFIV, FCX, GE, IVZ, JNJ, LMT, NAVI, NEE, NVS, CAR, PII, PLD, RTX, ROK, TXN, UBS, VZ, & XRX.

News & Technicals’

Yesterday’s market price action delivered a couple of whipsaws, creating some fear with the VIX popping over above 26 but closing the day above a 23 handle. Today, we a big round of earings that includes the first of the tech giants, MSFT, reporting after the bell. Traders should prepare for the possibility of substantial overnight gaps or reversals as these market-movers report. Janet Yellen, confirmed by the Senate, becomes the first woman to lead the U.S. Treasury Department. The U.S. House delivers the article to impeach former President Trump for a second time in an attempt to bar him from holding office ever again. The trail begins in early February. Minnesota confirms the first known U.S. case of the more contagious Covid variant discovered first in Brazil. A record spike in infections sparks fears of new lockdown restrictions in Dubai, which relies heavily on tourism.

Though the bears showed some aggression yesterday, the bulls ultimately won the day defending price supports and holding trends. However, as we ramp up earnings activity, the bearish aggression is worth noting, keeping us focused, flexible, and prepared. With price to earings valuations so high, an earnings miss is likely to create some punitive price action by the offending stock. Should one of the tech giants stumble, it could prove painful for the overall market. Have a plan to protect your capital should a stumble come to pass but until then, stick with the bullish trend but avoid overtrading or chasing already extended stocks.

The large-caps started the week not far on either side of flat, but he QQQ gapped 1% higher at the open. However, after the open, all 3 major indices ground sideways in an indecisive manner, while closing near the top of their range. This left the SPY and DIA printing Hammers (or Hanging Men depending on your perspective) with the QQQ printing a long-legged Doji with a bit more upper wick than a Hanging Man candle would have shown. However, that was another all-time high close for the SPY and QQQ. VXX gained over 4% to close at 17.08 and T2122 was down just slightly, but remains near Overbought Territory at 76.82. The 10-year bond yield was off a bit toe close at 1.031% and Oil (WTI) rose almost 1% to $52.78/barrel.

New Sec. of Treasury Yellen said Monday that she supported the idea of large tech companies paying a larger share of their revenues in taxes in the countries where they operate. This change from the previous administration’s approach was hailed by the French Finance Minister, who said he thought a global tax agreement for online businesses could be reached as soon as this Spring. Obviously, this would have major implications for the online giants like AMZN, GOOG, FB, AAPL, and any other multinational that has shifted revenue to a low-tax country to avoid taxes up to now

A new study by Moody’s Analytics finds that 18% of renters are significantly behind on their rent as of January 1. The average amount delinquent is $5,600 (4 months of rent plus late fees and utilities). While President Biden extended the moratorium on most evictions through the end of March, a huge reconning lies just ahead. The President’s proposed relief plan includes $25 billion for renters and landlords. However, that is less than 50% of the $57.3 billion currently owed to landlords…and the stimulus plan is now being fought by Senate Republicans as being too expensive as-is. Obviously, this is major problem brewing for REITS, Real Estate ETFs, and sooner or later bank stocks.

Related to the virus itself, US infections continue to rage as the US. The totals have risen to 25,861,597 confirmed cases and 431,392 deaths. The number of new cases fell in 47 states again as the average new cases has fallen to 175,021 new cases, but deaths remain high at 3,238 per day. CA has lifted its statewide stay-at-home order, which will allow restaurants, gyms, and other high-density public businesses to reopen. Elsewhere, after days of strong pushback against his reiteration of a fall goal of 100 million vaccinations in his first 100 days in office, President Biden has now said the goal should be 1.5 million vaccinations per day.

Globally, the numbers rose to 100,359,319 confirmed cases and the confirmed deaths are now at 2,151,697 deaths. In good news, the world’s average new cases is down to 592,753 per day (the first time below 600k this year), but deaths remain high at just under 14,114 new deaths per day. Later today the UK is expected to announce new travel quarantine measures that will use hotels to lockdown travelers entering their country. In the Netherlands, a third night of riots, violence, and looting against curfews has led to more than 180 arrests. In Germany, the Health Minister came out in support of limits to exports of vaccines produced in the EU. This stems from disagreements with AZN, who says Europe’s first doses of the AZN vaccine will not arrive before the end of the first quarter, while other locales are already using the vaccine.

Overnight, Asian markets were mostly in the red. Hong Kong (-2.55%), South Korea (-2.14%), and Shenzhen (-1.98%) led the losses. Only Australia (+0.36%) and Thailand (+0.75%) managed to stay on the green side. In contrast, Europe is mostly strongly green so far today. The FTSE (+0.80%), DAX (+1.84%), and CAC (+1.26%) lead the way with only Portugal (-0.64%) and Denmark (-0.61%) on the red side of flat at this point in the day. As of 7:30 am, US Futures are pointing to a flat open. The DIA is implying a +0.20% open, the SPY implying a +0.08% open, and the QQQ implying a +0.04% open.

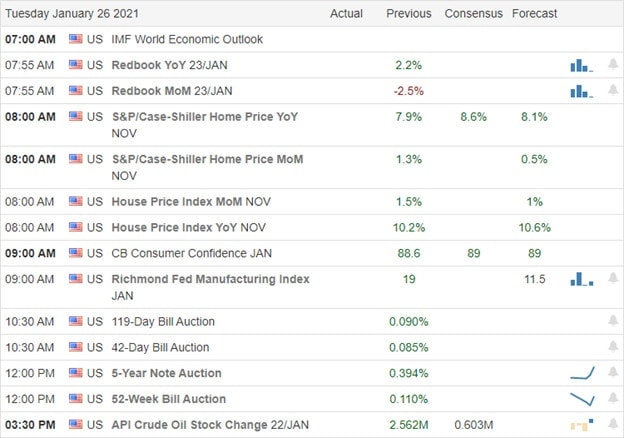

The major economic news for Tuesday is limited to Conf. Board Consumer Confidence (10 am). Major earnings reports include ALK, ADM, ALV, AXP, DHI, FCX, GE, IVZ, JNJ, LMT, MMM, NEE, NVS, PCAR, PII, PLD, RTX, ROK, VZ, and XRX all before the open. Then, after the close, AMD, BXP, CHRW, CNI, COF, EHC, MSFT, SLGN, SBUX, TXN, VAR, and WRB report.

With major earnings starting to roll (5 DIA components today), most eyes will be on the reports in the market this morning. Of course, the fight over what stimulus is needed and what is fiscally responsible may also take a good slice of Mr. Market’s mind. This comes as former President Trump’s second Impeachment Trial gets underway with the swearing-in of Senators today. We sit at all-time highs, with earnings uncertainty and tomorrow’s Fed decision still hanging overhead. So, be a little cautious and don’t get too giddy chasing the bulls.

As always, follow the trend, respect support and resistance, and don’t chase the moves you missed. There will be another trade. Lock in your profits when you achieve trade goals and stick to your discipline. Focus on the overall market, the specific chart, and your own trading process. Remember, trading is a long-term game. We don’t have to try to get rich every day.

Ed

Swing Trade Ideas for your consideration and watchlist: XBI, MDRX, XLU, XLV, GTHX, MOMO, MPC, MRVL, OVID. You can find Rick’s review of those tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

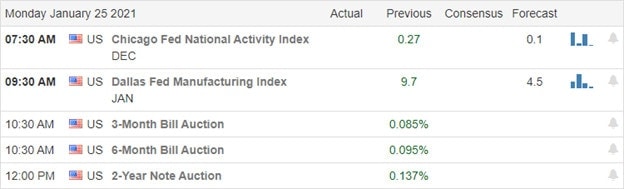

Between the earnings and economic calendar, traders and investors will have a lot of data to digest this week. Plan for the considerable price volatility and be prepared for the possibility of overnight reversals with the after the bell giant tech reports with substantial gaps at the open. With P/E ratios already extended, can companies produce earnings results to support these prices? We’re about to find out, so stay focused, flexible, and ready for just about anything.

Asian markets traded very bullishly overnight, with the HSI leading the way up a whopping 2.41%. However, European markets trade in the red across the board, and the U.S. futures that were quite bullish overnight now point to a mixed open. With so much data coming our way, be prepared for considerable price volatility in reaction earnings and economic news.

Economic Calendar

Earnings Calendar

We have a busy week of earnings that will include market-moving giant tech reports. Notable reports include AGNC, BRO, CR, ELS, KMB, & STLD.

News & Technicals’

Traders and investors will have a lot of data to digest this week with a busy economic calendar and an earings calendar brimming will market-moving reports. The futures were quite bullish during the night but have moderated considerably this morning, pointing to flat open. However, with so much data coming our way, anything is possible. Treasury yields are falling this morning as investors keep watch on the Biden 1.9 Trillion stimulus plan. The President restricted travel from the U.K., Brazil, and South Africa to mitigate risk from new virus strains that may be vaccine-resistant. In another executive action, Biden extended the student loan freeze for another eight months, and new data shows loans in forbearance are risings, adding pressure to the banking sector.

Although we saw a little selling last week, trends remain bullish, though mainly in a choppy consolidation. The week ahead could prove rather challenging as the market processes a big round of earnings. With P/E ratios already very extended, can companies produce earnings results that support these elevated prices? We will soon see, but traders should expect substantial volatility with the possibility of overnight market reversals and opening gaps as a result. Before making any new trade decision, make sure you’re checking the company’s earnings date as big price moves are possible. Focused, flexible, and agile traders with well-planned trades that carefully manage risk can do well in this environment. Buckle up!

Markets gapped down on Friday, but then printed an indecisive Doji-like candle. On the day, SPY lost 0.35%, DIA lost 0.61%, and QQQ lost 0.29%. While all 3 major indices closed down, they are just off their all-time highs. The VXX gained a little over a percent to 16.40 and T2122 fell just outside of the overbought territory at 77.85. 10-year bond yields fell to 1.086% and Oil (WTI) load over 2% to close at $51.98/barrel. For the week, large-caps were up about 2% and the QQQ up 4.35%.

GOP opposition to the price of President Biden’s $1.9 trillion stimulus plan has started to gel. With Republicans saying that more stimulus may well not be needed and that they oppose any more government borrowing unless the expense is proven to be absolutely necessary. However, the head of the National Economic Council, Brian Deese, held a call with a bi-partisan group of moderate Senators (8 Democrat and 8 GOP) on Sunday to make the case for the bill. This comes as Bloomberg reports that rate traders are also very anxious to hear Fed Chair Powell forcefully reiterate that FOMC bond purchases will continue through 2021 without easing. (In other words, that stimulus will not let up for at least the coming year.)

In a stunning admission, new CDC Director Walensky told Fox News that the government does not know how many of doses the two Covid-19 vaccines the US has in hand. And if she doesn’t know, she can’t tell Governors, state health systems or individual hospitals how much they will get or when. This is part of what has led thus far to a hap-hazard and slow push for vaccinations. In a shot (pun intended) at the Trump Administration, she said this was the situation they were handed.

Related to the virus itself, US infections continue to rage as the US. The totals have risen to 25,702,125 confirmed cases and 429,490 deaths. The number of new cases fell in 47 states again as the average new cases has fallen to 173,753 new cases, but deaths remain high at 3,182 per day. MRK shut down its vaccine program after trial data showed poor efficacy. Elsewhere, President Biden has banned all incoming travelers who were recently in South Africa (to stop the new variant from that country). It also formalized the rescinding former-President Trump’s last-minute lifting of bans on travelers from Ireland, the UK, much of Europe, and Brazil.

Globally, the numbers rose to 99,839,954 confirmed cases and the confirmed deaths are now at 2,140,489 deaths. In good news, the world’s average new cases is down to 588,519 per day (the first time below 600k this year), but deaths remain high at just under 14,000 new deaths per day. Over the weekend, the US CDC and UK Health Ministry discussed new data that suggests that the “UK Variant” of the virus is not only 50% more contagious, but also could have a higher mortality rate. On Sunday, Israel banned international flighted (in/out) for at least a week. Austria also made N95-grade masks mandatory in public and a German hospital in Berlin has been quarantined after finding 14 patients and 6 staff members infected with the newer UK variant of the virus.

Overnight, Asian markets were mixed, but leaned slightly to the bullish side. Hong Kong (+2.41%) and South Korea (+2.18%) far outpaced all other exchanges. To the downside, Malaysia (-1.26%), India (-0.93%) and Indonesia (-0.77%) paced the losses. In Europe, markets are mixed, but lean heavily to the red side so far today. Among the big 3 bourses, the FTSE (-0.71%), DAX (-0.97%), and CAC (-0.90%) are all well down at mid-day. As of 7:30 am, US Futures are also mixed. The DIA is implying a down open of 0.29%, the SPY on the green side of flat implying +0.13%, and the QQQ implies a pop higher of 0.93%.

There is no major economic news for Monday. Major earnings reports include ALLY, FHN, HBAN, KSU, RF, and SLB before the open. Major earnings reports on the day include KMB before the open. Then after the close, AUY, FUL, STLD, and XLNX report.

We have a full week of economic data and heavy earnings highlighted by the Fed statement and press conference on Wednesday. On top of this, the wrangling over another relief package continues and markets may wait until they are sure they’ll get another hit of stimulus before taking major decisions. It looks like the bulls want to run in the high-tech space this morning, but large-caps seem undecided as of now. So, bear in mind we’re at all-time highs with an indecisive market.

As always, follow the trend, respect support and resistance, and don’t chase the moves you missed. There will be another trade. Lock in your profits when you achieve trade goals and stick to your discipline. Focus on the overall market, the specific chart, and your own trading process. Remember, trading is a long-term game. We don’t have to try to get rich every day.

Ed

Swing Trade Ideas for your consideration and watchlist: CLX, WOR, SYX, BYND, APPS, BE, AG. You can find Rick’s review of those tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Yesterday’s insipid price action and declining volume suggested the market needed a rest after the hard bullish partying earlier this week. With the futures currently suggesting an overnight gap down at the open today, we are reminded that bears still exist. Now the question to be answered, do the bears have teeth, or will the dip crowd have the energy to defend trends and price supports as we slide into the weekend? Recent evidence and hope for another 1.9 trillion stimulus seem to give the bulls the upper hand.

Asian markets closed in the red across the board, with the HIS leading the way, dropping 1.60%. European markets retreat as well this morning as the virus spread and economic data damper recovery enthusiasm. Ahead of earnings and several possible market-morning economic reports, U.S. futures point to a gap down open within bullish index trends. Prepare for an extra dose of volatility as we head into the weekend.

Economic Calendar

Earnings Calendar

On the Friday earnings calendar, we have 22 companies fessing up to quarterly results. Notable reports include ALLY, HBAN, KSU, RF, & SLB.

News & Technicals’

While mostly bullish, the market’s price action seemed a bit insipid while still squeaking out new records in the SPY and QQQ. The energy and financial sectors experienced a notable weakness, while the big tech growth names garnered most the bullish attention. Whitehouse adviser Dr. Fauci says new data shows vaccines appear to be less effective against some newly identified strains. President Biden plans to sign more executive orders today but has reportedly come under pressure to scale back his 1.9 Trillion stimulus package. INTC stock surged just minutes before the close yesterday when an infographic related to the coming earnings report was leaked. The stock sold off after the bell and the release of the earnings. The company says it’s investigating the situation. Have I mentioned, I’m not too fond of earnings and the price manipulation it creates.

Technically speaking, trends remain bullish all-be-it quite stretched with volume declining even as new record highs occurred. However, this morning futures point to a gap down open, reminding us that bears still exist. We have a lighter day on the earnings calendar but several possible market-moving economic reports to keep us busy. As long as overall trends and support hold in this morning’s pullback, this is healthy market price action. However, it might be a bit painful from this elevated position for those overtrading. Plan your risk carefully as we head into the weekend.

Once again markets opened higher and after a day of indecisive trading, all 3 major indices closed an another all-time high close. As mentioned, all 3 put in indecisive Doji-like candles on the session. For the day, DIA was flat at +0.03%, SPY gained just 0.09%, but QQQ made a nice gain of 0.80%. The VXX lost eight-tenths of a percent to 16.18 and T2122 fell slightly, but remains in the overbought territory at 84.30. 10-year bonds rose to 1.109% and Oil (WTI) fell half a percent to $53.05/barrel.

On the report front after the close, IBM revenue missed on a continued slide for the fourth consecutive quarter. However, INTC reported a beat on top and bottom lines on a massive 33% surge in PC sales in the quarter. On the downside, INTC’s incoming CEO committed to the company continuing to do their own chip manufacturing. This is problematic because Intel have suffered years of manufacturing delays and operate at a higher cost than other chipmakers (like TSM).

In International trade news, the data shows that China purchased only 58% of the US goods they agreed to buy as part of former-President Trump’s “Phase One” settlement to the trade war. Meanwhile, in the UK, more post-Brexit trade news came out. This time a report finds that UK–EU freight traffic has dropped by 30% (both directions) since the first of the year. At the same time, logistics costs have risen 50% versus one year ago. Among the major issues is the new red tape. For example, the number of truck shipments rejected by the UK at the border has risen 168% versus January 2020. In addition, there are constant virus testing procedures on both sides of the border which cause delays.

Related to the virus itself, US infections continue to rage as the US. The totals have risen to 25,196,086 confirmed cases and 420,285 deaths. The number of new cases fell in 46 states Thursday as the average new cases has fallen to 191,652 new cases, but deaths remain high (4,363 on Thursday) at 3,176 per day. However, this must be taken with a grain of sale as states are suspect. MO was found to have not been reporting the results of rapid tests. This would have raised that state’s numbers by 644 just in January. Elsewhere, new CDC director Walensky contradicted the prediction of her predecessor who had said every pharmacy would have at least one of the vaccines available by the end of February. However, in good news, LLY announced that the phase 3 trial of their monoclonal antibody combination treatment was found to lower risk of contracting COVID-19 by up to 80%. While good news, the treatment is likely too expensive and scarce to use as a replacement for vaccinations.

Globally, the numbers rose to 98,188,110 confirmed cases and the confirmed deaths are now at 2,102,744 deaths. As a reference, the world average new cases is down to 631,396 per day, but deaths remain high at 13,732 new deaths per day. The UK says it is considering total border closure to contain the spread of new variants of the virus. France will now require a negative PCR test from any travelers entering from other EU countries.

Overnight, Asian markets were mixed but mostly bearish. Hong Kong (-1.60%), Indonesia (-1.66%), and Thailand (-1.03%) led, but losses were widespread. The only green was in India (+1.69%) and Shenzhen (+0.28%). Meanwhile, in Europe, so far today markets are red across the board on reports that EU economic activity has fallen to a two-month low in January, coupled with potential border closures in the UK. Among the big 3 bourses, the FTSE (-0.78%), the DAX (-0.86%), and CAC (-1.12%) are all down at mid-day. However, the biggest moves are in the smaller countries/exchanges such as Athens (-2.44%). As of 7:30 am, US futures are following Europe and pointing toward a negative open. The DIA is implying a -0.83% open, while the SPY implies a -0.75% open, and the QQQ is implying a -0.62% open.

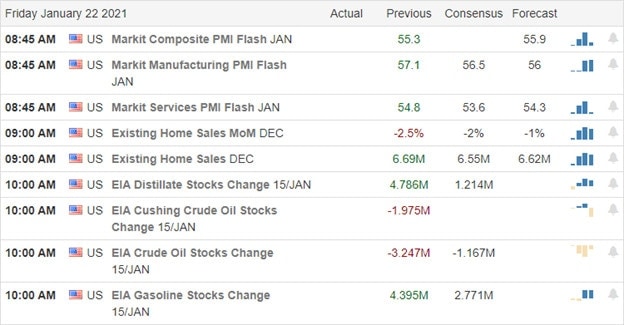

The major economic news for Friday includes Jan. Mfg. PMI and Jan. Services PMI (both at 9:45 am), Dec. Existing Home Sales (10 am), and Crude Oil Inventories (11 am). Major earnings reports include ALLY, FHN, HBAN, KSU, RF, and SLB before the open. There are no earnings reports after the close.

The markets look bearish this morning, perhaps pointing to some profit-taking at the highs or following Europe’s lead-based on virus-reduced economic activity. However, we do have a little more US data to come this morning, so don’t panic. Still, do bear in mind we are at all-time highs across the board and a bit extended to boot. The bottom line is that we need to be cautious at the highs, going into the weekend.

Lock in those profits when you achieve trade goals and stick with your discipline. As always, follow the trend, respect support and resistance, and don’t chase the moves you missed. There will be another trade. So, focus on the overall market, the specific chart, and your own trading process. Remember, trading is a long-term game. We don’t have to try to get rich every day.

Ed

Swing Trade Ideas for your consideration and watchlist: VIAC, KSS, JMIA, OSTK, SOLO, MRNA, FUBO. You can find Rick’s review of those tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service