AMZN Partial Miss Reinforced Econ Data

Markets opened basically flat on Thursday before putting in a slow morning rally and a slow afternoon fade. So, generally, it was a sideways nothing day that continued the consolidation in all 3 major indices. All 3 indices put in upper wicks and small bodies, but you would NOT call any of them Shooting Star candles. On the day, SPY gained 0.40%, DIA gained 0.42%, and QQQ gained 0.18%. All 3 indices are very near all-time highs again. The VXX fell to 29.49 and T2122 rose just into the edge of the overbought territory at 81.99. 10-year bond yields rose back to 1.266% and Oil (WTI) was up 1.5% to $73.53/barrel.

During the day Q2 GDP came in far below expectation. While we still saw 6.5% GDP growth for the quarter, analysts had estimated the growth would be 8.5%. Weekly Jobless claims also came in a bit above expectation (400k vs. 380k est.). Then mid-morning June Pending Home Sales shrank 2%. However, markets shrugged off this news and traded as if everything was fine.

After hours, AMZN reported a massive beat on earnings and over $113 billion in sales for Q2, but still missed on revenue by over $2 billion. This comes as the pandemic “stay at home shopping” boost fades. The stock was hammered hard in post-market trading, down 6.5%. Almost all the other after-hours earnings reports were beats on both lines. PINS beat on both lines, but obliterated in post-market trading, down 21% as of 4:30 pm after reporting that it lost users during the quarter.

This morning the incredibly strong earnings season continued. Almost all reports came in as beats on both lines. The only misses reported were NWL missing on revenue and JCI barely missing (by 4/100 of a cent) on earnings. CHTR, AON, LYB, VFC, CPRI, PG, and CVX in particular reported significant beats. A few buyback plans, such as CVX were announced. Another great day on reports of the quarter past.

Overnight, Asian markets were red across the board. Japan (-1.80%) and Hong Kong (-1.35%) led the region lower. In Europe, there are a few minor exchange exceptions, but in general the continent is also in the red as of mid-day. The FTSE (-0.82%), DAX (-0.74%), and CAC (-0.09%) are pretty typical of the spread among European bourses. As of 7:30 am, US Futures are also pointing to a gap lower at the open. The DIA is implying a -0.33% open, the SPY implying a -0.66% open, and the QQQ implying a 1.04% open following the AMZN disappointment. 10-year bond yields and commodity prices are also down, perhaps unrelated to the dollar which is showing only tepid strength this morning.

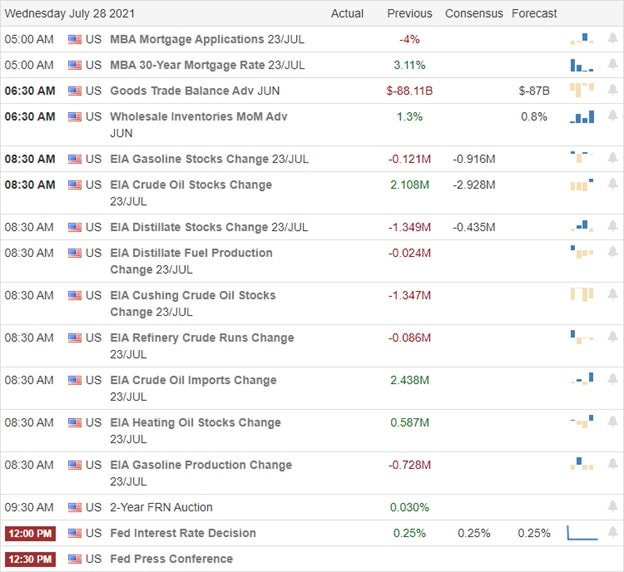

The major economic news scheduled for release on Friday is limited to June PCE Price Index, Q2 Employment Cost, and June Personal Spending (all at 8:30 am), Chicago PMI (9:45 am), and Michigan Consumer Sentiment (10 am). Fed member Brainard also speaks long after the close (8:30 pm). The major earnings reports scheduled for the day include ABBV, AXL, AON, AVNT, BBVA, BLMN, BAH, COG, CPRI, CRI, CAT, CERN, CVX, CHD, CNHI, CL, DAN, XOM, HRC, HUN, ITW, IMO, JCI, LAZ, LIN, LYB, NWL, PBR, POR, PG, QSR, TU, TIXT, VFC, GWW, and WY all before the open. Then after the close, there are no major reports scheduled.

It looks like AMZN reporting just their third-ever $100 billion quarter of revenue, but missing by over $2 billion, was the tipping point for fear. Earlier missed economic reports had not moved markets. Still, after a night of reflection, world markets are moving lower so far today. Remember that we are still very near all-time highs and the bullish trend remains in place. So, don’t get too far out on a bearish limb over a pullback. Also, keep in mind that it is Friday and month-end. So, be ready for the weekend new cycle, lightening up, evening up, and hedging as appropriate.

Don’t let a gap or loss get you down. It happens. Remember, trading success is not made in one trade, one day, or one week. Success is all about batting average and adding up those singles and doubles. So, manage your current positions first. Don’t chase, predict turns on one candle, and stick to your trading rules. Discipline will see you through. Focus on the process and managing what you can control. Finally, Friday is payday. So don’t forget to pay yourself.

Ed

Swing Trade Ideas for your consideration and watchlist: No Tickers Today. Rick is out but the RWO Room is open. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service