Earnings Lead the Way This Morning

Markets gapped down Tuesday and while the large-caps were more sideways after that, all three major indices closed not too far up off their lows. This left us with gap-down Black candles to start the week. On the day, SPY lost 1.76%, DIA lost 1.45%, and QQQ lost 2.49%. The VXX climbed more than 7.6% to 19.86 and T2122 dropped into the oversold area at 14.15. 10-year bond yields spiked massively to 1.875% and Oil *WTI) soared another 2.41% to $85.85 on middle-eastern and Russia/Ukraine war fears.

The big business news on the day was MSFT acquiring ATVI in a $68.7 billion all-cash deal. MSFT will pay $95/share in the deal, which will make it the number three company in that space. It also gets ATVI out from under massive clouds around their corporate culture and legal issues around sexual discrimination and harassment suits filed by employees and the State of CA. Oddly, ATVI spiked as high as $93 in premarket, opened at $86.68, and closed back down to $82.31…which was still up almost 26% on the day. MSFT closed down 2.43% on the day.

In other business news, PTON hired consulting company McKinsey to “evaluate their cost structures.” This almost always results in mass layoffs, store closures, and even business offering rationalization. PTON closed down 3.51% on the day after the announcement. Elsewhere, for the second time in less than a year, JPM announced it is raising salaries across a broad group of employees in an effort to keep and attract talent.

On the earnings front, so far today UNH, FAST, PG, and CFG have all reported beats on both lines. BAC, MS, and ASML reported beats on earnings but came in light versus revenue estimates. However, USB missed on both lines.

Overnight, Asian markets were mostly strongly lower, with a couple of very minor exceptions. Japan (-2.80%) was an outlier, but New Zealand (-1.58%), Shenzhen (-1.28%), and Australia (-1.03%) were representative of the regional trend. In Europe, stocks are mixed, but mostly modestly higher at mid-day. Russia (+4.43%) is an outlier and is snapping back from a terrible Tuesday (war fear). However, the FTSE (+0.27%), DAX (+0.31%), and CAC (+0.70%) are leading most of the region higher in early afternoon trade. As of 7:30 am, US Futures are pointing toward a modestly green open. The DIA implies a +0.22% open, the SPY is implying a +0.28% open, and the QQQ implies a +0.31% open at this hour. Bond yields continue to rise at 1.886% and Oil (WTI) is up another 1.29% in early trading.

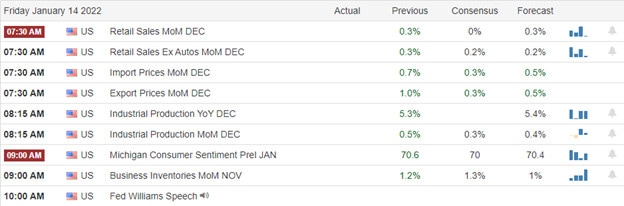

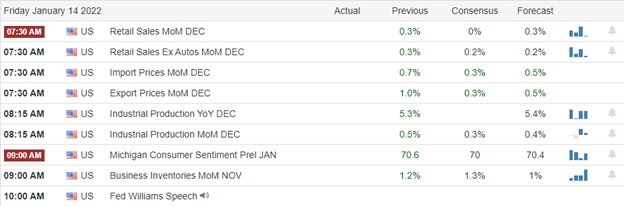

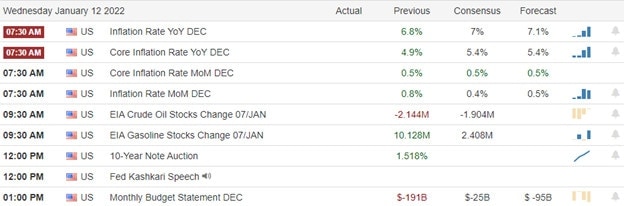

The major economic news scheduled for release Wednesday is limited to Dec. Building Permits and Dec. Housing Starts (both at 8:30 am). Major earnings reports scheduled for before the market include: ASML, BAC, CFG, CMA, FAST, MS, PG, PLD, STT, USB, UNH. Then, after the close, AA, DFS, FUL, KMI, and UAL report.

Earnings, inflation, and fear over the acceleration of the Fed’s hawkish turn continue to be the major drivers in the market. The question of the day is whether we have found a little support OR the earnings news is just a setup for another “gap and crap.” The bears clearly still have all the momentum so far this week (and year). The wild ride in Oil since the beginning of December shows no sign of letup. However, one has to ask whether this is a bull trap as extended as the commodity and the major names are at this point. So, be careful in that space. Keep in mind that even though the direction is bearish, intraday whipsaw volatility remains likely. In short, trade carefully.

Stick to your trading rules and on managing the things you can control. Don’t chase, trade with the trend, keep consistently taking profits when you have them, and move your stops in your favor. And keep in mind that the first rule of making a lot of money in the market is to not lose a lot of money in the market. So, don’t be stubborn. When you’re wrong, just admit it and take your loss. (That’s why we set stops.)

Ed

Swing Trade Ideas for your consideration and watchlist: BEKE, CECE, SCCO, TECK, EBAY, NEM, AMGN, HSY, RWM, UNG, QID. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service