The recovery rally continued Tuesday after a very turbulent start, with the Dow first sinking nearly 300 points. If you feel the price action has become challenging, buckle up with two significant inflation reports and the beginning of earnings season; the wild price volatility may become even more challenging in the days ahead. Be prepared for possible large point whipsaws and even full-on reversals that could occur overnight as the all-or-nothing market enters the silly season with valuations already extremely high.

Asian markets closed green across the board during the night, with Hong Kong advancing a whopping 2.79%. This morning, European markets are bullish, with a bit more tentativeness in price action as they wait on inflation data. Ahead of earnings and the CPI report, U.S. futures pump for more gains suggesting another gap up at the time of this report. So, let’s get ready for another wild ride!

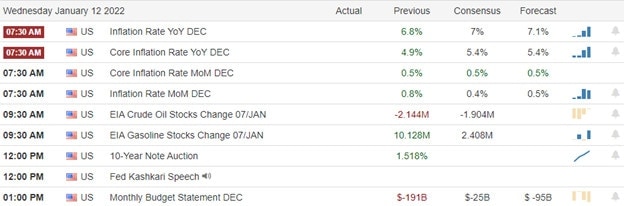

Economic Calendar

Earnings Calendar

On the Wednesday earnings calendar, we have 18 companies listed with nine confirmed reports. Notable reports include AONNY, BBCP, GHG, INFY, JEF, KBH, SJR, & VOLT.

News & Technicals’

The consumer price index is released by the Labor Department Wednesday and is expected to show headline inflation jumped by 7%, its fastest pace since 1982. The Federal Reserve is already on a path to raise interest rates to battle rising prices. So a hot number should justify the Fed’s policy shift. “It’s still hot, hot, hot, and it’s important because we’re now where the Fed worries about that 7% number getting baked into wages and getting more entrenched,” said Diane Swonk, chief economist at Grant Thornton. On Tuesday, Federal Reserve Chairman Jerome Powell said that the economy is both healthy enough and in need of tighter monetary policy. That likely will entail interest rate hikes, tapering of monthly asset purchases, and a smaller balance sheet. Powell made the comments during a confirmation hearing in which key senators indicated they would be supporting him for a second term. Russia’s dealings — or, more accurately, its clashes — with the West have focused on one country that has been a particular flashpoint for confrontations in recent years: Ukraine. This week, this has come into focus with a series of high-stakes meetings taking place between Russian and Western officials. The talks centered on trying to defuse heightened tensions between Russia and its neighbor Ukraine. Treasury yields dipped once again ahead of CPI data in early Wednesday trading, with the 10-year slightly lower at 1.7428% and the 30-year edging lower to 2.0643%.

Tuesday notched another day in the recovery rally after a bumpy start selling off nearly 300 points to begin the day. These huge point moves in this all-or-nothing market add substantial risk for the retail trader. Although we have seen a significant technical damage improvement in the DIA and SPY, the large point moves open the door for damaging whipsaws or even full-on reversals with little to no pice action support below. Since the low on Monday where the T2122 indicator nearly reached an oversold condition is now warning of an overbought condition. Indeed an all-or-nothing condition with crucial inflation data and the beginning of earnings season could quickly increase the level of price volatility, adding to the challenging environment. So stay focused, watching for potential large-point swing whipsaws and full-on reversals that could appear in the overnight session. Despite all the bullish hype, keep in mind that a Hawkish Fed typically slows economic activity. So trade wisely and avoid complacency.

Trade Wisely,

Doug

Comments are closed.