China Stim Helps Bulls As We Await Powell

Markets opened flat on Wednesday before making a morning run up to the highs at noon. Then the whipsaw kicked in and all 3 major averages sold off back down near the open shortly after 1:30 pm. From there we saw an oscillating sideways grind in a tight range. However, Mr. Market gave us one last rally and then selloff starting at 3 pm which left us mid-way between the open and highs as of the close. This action gave us a white-bodied, Spinning Top type of candle in all the major indices. The QQQ and DIA both held their 34ema as support on the day.

All 10 sectors were in the green, with the Energy, Healthcare, and Consumer Cyclical sectors leading the way higher. On the day, SPY gained 0.31%, DIA gained 0.24%, and QQQ gained 0.29%. The VXX fell 1.69% to 19.80 and T2122 is back in the mid-range at 51.77. 10-year bond yields climbed to 3.111% and Oil (WTI) is up another 1.71% to $95.34/barrel. All-in-all, this was another indecisive, low-volume day where markets have held support but haven’t really started back up yet.

In economic news, July Durable Goods Orders came in below consensus forecasts at dead flat. This was below the +0.6% forecast and well below June’s +2.0% number. July Pending Home Sales were also down. However, the -1.0% was well above the -4.0% forecast and much better than June’s -8.9% number. EIA Crude Oil Inventories came in down 3.282 million barrels (on increased exports, hitting a new all-time high) and this was a far bigger drawdown than the -0.933 million barrels forecast, but still much better than the previous week’s 7.056-million-barrel drawdown. Also, during the day, President Biden announced the administration will forgive $20,000 in student loan debt for Pell Grant recipients and $10,000 in federal loan debt for others with income of less than $125,000.

SNAP Case Study | Actual Trade

In another blow to the stock, the TWTR whistleblower mentioned in yesterday’s blog is now scheduled to speak before the US Senate on September 13. This can’t help but lead to attacks from Senators eager to reign in big tech (as well as those just wanting to make headlines less than 2 months prior to the mid-term election). In other big tech news, AAPL invited the press to a “big announcement” on September 7. It has been y rumored the company will announce its new iPhone 14 line on that day. Elsewhere, GOOGL is launching an ad campaign to fight disinformation in parts of Europe. The pilot program spots (which will run on GOOGL search, TWTR, META, and TikTok) aim to help people identify emotional manipulation, scapegoating, and fake information in posts and media reports. Initially, the campaigns will run in Poland, Slovakia, and the Czech Republic.

In energy and consumer news, Bloomberg reported Wednesday that 20 million US homes (1 in 6 homes) are behind in payments of their energy bills. This has been caused by surging electricity, natural gas, and fuel oil prices. This is expected to get worst as we head into colder months. Specifically, California’s PCG has seen a 40% rise in residential delinquencies and New Jersey’s PEG reports a 30% rise in customers who are more than 90-days late…just since March. Meanwhile, as mentioned above, US exports of Oil and distillates hit an all-time high of more than 11 million barrels per day last week. This is especially interesting since a fire at the main US LNG export terminal will keep that facility (and thus US exports of LNG) offline until November.

After the close Wednesday, CRM, WSM, NTAP, ADSK, and SPLK all reported beating on both the revenue and earnings lines. Meanwhile, VSCO missed on revenue while beating on the bottom line. On the other side, GES and SNOW both beat on revenue while missing on earnings. However, NVDA missed on both the top and bottom lines. It is also worth noting that SPLK raised forward guidance while CRM and NVDA both lowered their forecasts.

So far this morning, TD, DG, CM, COTY, and TITN all reported beats on both the top and bottom lines. At the same time, BURL missed on revenue while beating on earnings. However, PTON and HAIN missed on both the top and bottom lines. It is worth noting that BURL and PTON also lowered their forward guidance.

Overnight, Asian markets leaned heavily to the green side. Hong Kong (+3.63%) was an outlier, up hard after being halted in the morning for a typhoon warning and later resuming trade in the afternoon. However, Malaysia (+1.92%), South Korea (+1.22%), and Shanghai (+0.97%) led the region higher. In Europe, stocks are nearly green across the board at mid-day. Only Switzerland (-0.01%) shows any red at all. Meanwhile, the FTSE (+0.19%), DAX (+0.28%), and CAC (+0.06%) are leading the region higher in early afternoon trade. As of 7:30 am, US Futures are pointing toward a green start to the day. The DIA implies a +0.28% open, the SPY is implying a +0.53% open, and the QQQ implies a +0.71% open at this hour. 10-year bond yields are down slightly to 3.098% and Oil (WTI) is flat in early trading.

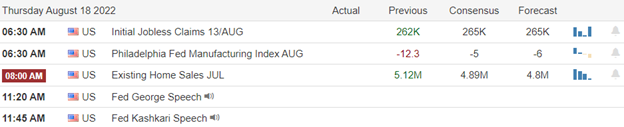

The major economic news events scheduled for Thursday include Q2 GDP Revision and Weekly Jobless Claims (both at 8:30 am), and the Jackson Hole Central Banker Symposium begins (at 9 am). However, Fed Chair Powell does not speak until Friday. The major earnings reports scheduled for the day include ANF, BURL, CM, COTY, DG, DLTR, GFI, GOGL, HAIN, PTON, and TD before the open. Then, after the close, DELL, FTCH, GPS, MRVL, ULTA, VMW, and WDAY report.

In economic news later this week, on Friday, we get July PCE Price Index, July Personal Spending, July Trade Goods Balance, July Retail Inventories, Michigan Consumer Sentiment, and the Jackson Hole Central Banker Symposium continues with Fed Chair Powell Speaking. On the earnings front, JKS reports before the open Friday.

As markets grind toward getting their clue from Fed Chair Powell, the Jackson Hole Conference starts today with other Central Bankers speaking. New Chinese stimulus, in the form of government spending (which will amount to almost 1% of Chinese GDP), has given bulls an overnight shot in the arm. However, as stated before, don’t be surprised with a “wait and see” attitude in the market until Powell speaks on Friday. Premarket prices look like we will be gapping higher and may retest the T-line in the major indices. However, those prices have also fallen back from earlier highs as traders remembered they were waiting on Powell. There is no denying that it looks like the pullback has paused and just maybe started to reverse. There is potential support levels below, the broken mid-term trend was bullish, and the broken longer-term trend was bearish. So, caution is in order, and volatility is to be expected. However, China is giving us a little lift early today.

Demonstrate patience and wait for confirmation. Remember that trading is our job. So, do the work and follow the process. Stick with your trading rules, trade with the trend, and take those profits when you have them. Don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. When price does move in your direction, always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all OUR MONEY!). Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: ACAD, DM, CGC, AA, ALB, MRO, OKE, X, SNOW. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service