If the choppy price action of late has been frustrating, the wait is over, and let the volatility begin. Not only do we have the CPI and Jobless Claims, but we also kick off the wild speculation and price manipulation of the 4th quarter earnings season. While companies may hit substantially lowered earnings estimates, the guidance forward and the commitment to stock buybacks will likely be most important for the future direction of the stock prices. Expect the challenging price action to continue with the path forward, which is looking so uncertain at this time.

Asian markets declined across the board as investors traded cautiously ahead of U.S. inflation data. European markets, however, show some willing bulls as they brace for the coming numbers. This morning looks like a repeat of yesterday’s premarket pump, pointing to a bullish open ahead of earning and economic report results. I guess the question to be answered is, with this pump-up speculation be successful, or will it result in another disappointing pop and drop? Buckle up; we’re about to find out!

Economic Calendar

Earnings Calendar

We’ve made it to the official kick-off day of the 4th quarter earnings. Notable reports include BLK, CMC, DAL, FAST, PGR, TSM & WBA.

News & Technicals’

Belgium’s central bank chief told CNBC that the European Central Bank needs to raise interest rates into positive territory when considering inflation, despite recession fears. “My bet would be it’s going to be over 2%, and I would not be surprised if we have to go to above 3% at some point,” said Pierre Wunsch, governor of the National Bank of Belgium. However, he said that September’s hike in the ECB’s benchmark deposit rate to 0.75% meant rates were still negative in real terms.

Cash, one of the most hated corners of the market for years, is getting some newfound love from money managers as the Federal Reserve’s firm commitment to rate hikes roiled nearly every other asset class. Global money market funds saw $89 billion of inflows for the week ending Oct 7, the largest weekly injection into cash since April 2020, according to Goldman Sachs’ trading desk data. Meanwhile, the data said that mutual fund managers also hold a record amount of cash.

The Office for National Statistics estimated Wednesday the U.K. economy shrank by 0.3% in August, potentially beginning what economists expect will be a lengthy recession through the winter. In addition, postal workers, rail workers, and public barristers have all carried out strikes recently to protest pay and conditions, as wages fail to keep up with inflation running at around 10%. A worst-case scenario laid out by national electricity system operator the National Grid warned that households and businesses might face three-hour power outages over winter. Asia’s biggest economic problems next year will stem from rising interest rates. These will put increasing pressure on debt servicing in Asia and heighten capital flight from the region: IMF The U.K. bond crisis will have limited impact on Asian markets, although “anything that creates financial market turbulence will find a way” to upset other economies: IMF. As many Asian economies, such as Japan and Hong Kong, open up, increased human mobility will generate economic activity and stall a slowdown.

The wait is over, so let the volatility begin. After the disappointing PPI number, the dollar rose, the bond yields surged, and the FOMC minutes say the hawkishness is not yet over! That made for a choppy Wednesday as traders pondered the CPI, Jobless Claims, and what earnings reports might reveal. Once again, the overnight futures are working to pump up a bullish open but will it be just another pop and drop to punish those rushing in hoping to pick the bottom? We sure could use a rally with the indexes in a short-term oversold condition, but it may not be a tough sell if inflation remains resilient. As earnings number ramp up, expect wild speculation and price volatility to do the same. I think the company’s guidance and stock buyback levels will be more important this season than hitting the substantially lowered estimates. So be careful jumping in too soon and wait for the conference call before making your decision. Likely challenging times lie ahead, so plan your risk carefully.

Markets opened little changed Wednesday and then chopped sideways in a fairly small range. The only exception to this was the SPY which plunged the last 15 minutes of the day to get back near the lows. The DIA did retest its T-line (8ema), but failed, while the other 2 major indices didn’t even come close. This action is giving us Indecisive, Inside Day candles in all 3 of the major indices. The Spy printed more of an Inverted Hammer candle while the DIA gave us a Doji and the QQQ printed a Spinning Top. Overall, just a volatile, sideways day that seems to be coiling up as we wait for another shoe to fall.

On the day, seven of the 10 sectors are in the red with Utilities (-2.99%) being by far the biggest losing group. On the other side, Consumer Cyclical (+0.27%), Consumer Defensive (+0.24%), and Energy (+0.20%) were the gaining sectors. Meanwhile, SPY was down 0.32%, DIA was down 0.04%, and QQQ was down 0.03%. The VXX was off 1.01% to 21.54 and T2122 remains oversold at 15.81. 10-year bond yields backed off to 3.898% and Oil (WTI) was down 2.5% to $87.12/barrel.

In economic news, September PPI came in twice as hot as expected at +0.4% (versus +0.2% forecasted and actual in August). For what it is worth, the September Core PPI (with food and energy prices stripped out) came in as expected at +0.3%, which was also the same as August. In the afternoon, the September FOMC Meeting Minutes did not give us any new information. Just as Fed speakers have been telling us since the meeting, the FOMC expects rate hikes to continue at a higher pace and a higher final interest rate level for a longer period than originally expected since inflation is showing little sign of abating yet. After the close the API reported a 7.054-million-barrel crude oil inventory increase this week, dramatically reversing last week’s 1.770-million-barrel drawdown. Finally, Treasury Sec. Yellen expressed concerns about liquidity in the bond market as many of the largest buyers have gone away. Sovereigns, Japanese and European insurance and pension funds, etc. all have their own financial problems and are not looking to add US bonds. As a result, as the supply of Treasuries has climbed, a lack of liquidity has driven average yields higher and caused outsized volatility. (I’m not sure that is news, because that is how I was taught that free markets work…when supply goes up and demand goes down, the price falls, meaning in this case the yield rises. Nonetheless, she said it, and the financial media all thought it was newsworthy enough to report.)

In stock news, Wednesday afternoon, it was announced that CCJ (a uranium supplier) and BEP (a utility) are teaming up to acquire Westinghouse from BBU (a holding company affiliated with BEP). The $7.9 billion deal will give CCJ a 49% ownership interest in the Westinghouse venture as nuclear power becomes more popular again. Across the pond, the EU approved the deal where CE will buy DD’s “Mobility and Materials” business unit for $11 billion. After the close, CLF announced the USW union had ratified a new 4-year labor contract covering 12,000 of its employees. At the same time, AMAT announced it was cutting its Q4 revenue estimate, citing new export regulations as a headwind. Meanwhile, the NRLB cited SBUX for having called the police to disperse employees that were pro-union at a Kansas store. Finally, AMZN announced that it is switching rockets for the upcoming launch of its prototype satellites (intended to compete with Elon Musk’s Starlink of satellite-based high-speed internet system). The new rocket is from UAL (a joint venture by BA and LMT).

In Energy news, Oil was down in great part to a very strong dollar. (The Euro fell further below parity to $0.97 while the Dollar rose to a 24-year high of 146.91 Yen.) In company-related news, XOM announced that its new carbon emissions reduction business, called Low Carbon Solutions unit, had signed CF (the world’s largest ammonia manufacturer) as its first client. At the same time, they signed a second deal with ENLC (an oil pipeline network). After he close the EIA (US Energy Information Administration) said that consumers can expect to pay 28% more (compared to last year) to heat their homes this coming winter. This is based on Natural Gas (half of all homes) prices up 28% year-over-year, Electricity (40% of homes) up 10% over last year, and Heating Oil (9% of homes) up 27% on the year.

So far this morning, WBA, TSM, and FAST all beat on both the revenue and earnings lines. (As mentioned above, even though TSM beat, it also drastically cut new capital spending for the rest of the year…even while raising guidance.) Meanwhile, BLK and CMC missed on revenue while beating on earnings. On the other side, DAL beat on revenue while missing on earnings. However, DAL did raise guidance after reporting a major surge in summer travel. Finally, DPZ missed on both lines.

Overnight, Asian markets were red across the board. Taiwan (-2.07%), Hong Kong (-1.87%), and South Korea (-1.80%) led the red tide, perhaps aided by TSM (the world’s largest chipmaker) cutting 2022 capital spending by 10% in a major warning shot fired across the bow of tech companies. Meanwhile, in Europe, stock exchanges are mixed but lean to the green side at midday. The FTSE (+0.04%), DAX (+0.87%), and CAC (+0.40%) are leading the move with four of the smaller exchanges lagging and still red in early afternoon trade. As of 7:30 am, US Futures are pointing toward a modestly green open ahead of consumer inflation data. The DIA implies a +0.58% open, the SPY is implying a +0.55% open, and the QQQ implies a +0.30% open at this hour. 10-year bond yields remain at 3.89% and Oil (WTI) is also little moved at $87.40/barrel in early trading.

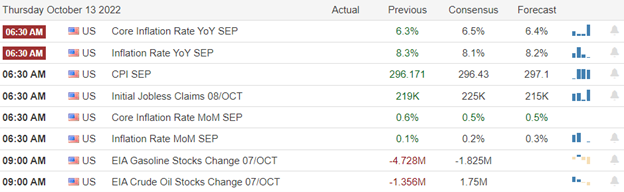

The major economic news events scheduled for Thursday include September CPI and Weekly Initial Jobless Claims (both at 8:30 am), EIA Weekly Crude Oil Inventories (11 am), and the Federal Budget Balance (2 pm tentative). The major earnings reports scheduled for the day include BLK, CMC, DAL, DPZ, FAST, INFY, PGR, TSM, and WBA before the open. There are no major reports scheduled for after the close.

In economic news later this week, on Friday we get September Retail Sales, September Import/Exports, August Business Inventories, Mich. Consumer Sentiment, and August Retail Inventories.

In earnings reports later this week, on Friday, the big banks really kick off earnings season as C, FRC, JPM, MS, PNC, USB, UNH, and WFC all report.

Markets will be focused on CPI data in at least the pre-market this morning, even though we have had some generally good earnings reports. For what it is worth, Moody’s Chief Economist said overnight that his analysis leads him to expect a significant inflation reduction within 6 months. However, just from a read-through of the PPI data, we should expect a very hot inflation number today. Don’t be surprised if we see more whiplash as markets overreact early, rethink and whip back in the other direction. However, at the moment we appear stuck between this week’s low and the T-line.

With this backdrop, the premarket action seems to show some optimism ahead of the CPI data. The market remains a bit extended in terms of T2122, but not extremely so. Watch the T-line levels for resistance if we bounce on the CPI data. Once again, the one thing we know is that the strong bear trend is still in place and markets have been indecisive the last two days…as if waiting. So, don’t predict a bottom, but keep a watchful eye on market price action.

Don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. When price does move in your direction, always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all OUR MONEY!). Also, keep in mind that trading is a job. It’s not a hobby. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Demonstrate patience and wait for confirmation. Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: WBA, APA, HALO, BA, RCL, MO, UPST. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The bulls tried to get upside price action going, but all at once, the bears returned with a vengeance producing a nasty whipsaw to punish the dip buyers. As a result, the QQQ closed at a new 2022 low, while the other indexes managed to hold Monday’s low. Before the bell today, we will get the Producer price report and then deal with the FOMC minutes this afternoon. In addition, we will have to keep a close on rising bond yields and fluctuating currency after the BOE deadline warning to pension plans. Finally, no matter the market reaction, keep in mind the CPI numbers come out before the bell Thursday, so plan your risk carefully!

Asian markets traded mixed as the Yen continued to weaken to 146 to 1 against the dollar. European market trade mixed in a choppy session, waiting for U.S. inflation data. However, the U.S. futures push for a bullish open ahead of the PPI number. How the market reacts after the number is anyone’s guess. Perhaps the futures premarket pump will signal a relief rally, or perhaps they are just trying to put lipstick on a pig.

Economic Calendar

Earnings Calendar

With the official kickoff of 4th quarter earnings beginning tomorrow, we have another light day of reports. Notable reports include PEP & DCT.

News & Technicals’

Tobias Adrian, director of monetary and capital markets at the International Monetary Fund, told CNBC Jamie Diamon’s call that U.S. stocks could tumble another 20% was “certainly possible.” He said sentiment had so far held up relatively well, but a shift in this could spark a further downturn. Adrian also warned financial stability risks are very elevated, with the global economy in a “very, very stressed moment.” Sridhar Ramaswamy, who led Google’s advertising business from 2013 to 2018, has launched a Web3 company called nxyz. Nxyz trawls blockchains and their associated applications for data on things like NFTs and crypto wallets and then streams it to developers in real time. The company raised $40 million in a funding round led by crypto-focused venture fund Paradigm, with additional backing from Coinbase, Sequoia, and Greylock.

The U.S. Department of Commerce introduced sweeping rules to prevent China from obtaining or manufacturing key chips and components for supercomputers. Analysts said that this is likely to hobble China’s domestic chip industry. In addition, Washington’s export rules could touch other parts of the supply chain that use American technology, highlighting the wide-ranging nature of the latest restrictions.

Unbelievable

“I don’t think there will be a recession. If it is, it’ll be a very slight recession. That is, we’ll move down slightly,” Biden told CNN’s Jake Tapper in a Tuesday interview. On Monday, JPMorgan Chase CEO Jamie Dimon told CNBC there would likely be a recession in six to nine months. In September, the U.S. central bank raised benchmark interest rates by three-quarters of a percentage point —the Fed’s third consecutive hike. Treasury Secretary Janet Yellen said the U.S. is doing well amid global economic uncertainty. Yellen said the U.S. economy has slowed after a strong recovery, but job reports indicate a resilient economy. The Treasury Secretary reiterated that lowering inflation is a priority of the Biden administration.

Yesterday proved to be another choppy day as the bulls finally pushed off the lows only to have the bears produce a nasty whipsaw, driving indexes down in a quick move. The QQQ made a fresh 2022 low after the BOE set a deadline for pension plans to make adjustments as central bank interventions end. Today we face the latest reading on Producer Prices, more Fed speak, and we will get the minutes of the last FOMC meeting. I think the market is looking for any hope to relieve the short-term oversold condition of the indexes. Still, traders must remain aware of the currency liquidity issues and bond yield gyrations. As you make trading decisions, remember we get the CPI number before the bell on Thursday and begin the 4th quarter earnings with the big bank reports. Plan for a heavy dose of price volatility.

The DIA diverged from the SPY and QQQ at the open Tuesday. Both SPY and QQQ gapped down half of a percent and then both followed through strongly for 30 minutes to lows where SPY was down 1.20% and QQQ was down 1.75% at 10 am. Meanwhile, DIA gapped down just 0.25 percent and then traded sideways in a very tight range for the first 30 minutes. However, at 10 am, all 3 got back in lock-step as the bulls started a strong rally that lasted until 1 pm, where we found the highs of the day. After a little less than 2 hours of grinding slightly lower, the bears really kicked into high gear at about 2:40 pm and drove us to new lows for the day in all 3 major indices at 3:20 pm. Then the chop continued as the bulls stepped back in to bounce us up off those lows the last 40 minutes of the day. This action gave us gap-down, indecisive, candles with large upper wicks and smaller lower wicks. In other words, Spinning Top type candles in all 3 indices. The DIA retested its T-line (8ema) and failed the test earlier in the day.

On the day, eight of the 10 sectors are in the red with Consumer Defensive (+0.60%) leading the gains and Technology (-1.89%) being by far the sector showing the largest loss. Meanwhile, SPY lost 0.65%, DIA gained 0.11%, and QQQ lost 1.37%. The VXX was up 1.5% to 21.76 and T2122 remains in the oversold territory at 12.50. 10-year bond yields rose to 3.937% and Oil (WTI) fell 2.75% to $88.64/barrel. Overall, it has been a volatile, choppy, and indecisive day across the market. It may be that markets were really just waiting on inflation and earnings data later this week.

In FOMC news, on Tuesday, Philly Fed President Harker again told an audience he believes the central bank can reduce inflation without triggering a deep recession and causing high unemployment. However, he did not give additional clues about the size of rate hikes he feels appropriate to do that inflation fight or how long they will continue. Later, Cleveland Fed President Mester told a NY Economic Club audience the Fed needs to continue raising rates. She reiterated that “at some point, as inflation comes down, then my risk calculation will shift. But at this point, my concern lies more on the fact we haven’t seen progress on inflation.” She continued, “Given current economic conditions and the outlook, in my view, the larger risks come from tightening too little.” (She thus implied that she continues to favor at least 0.75% hikes.)

In stock news, BK announced it will join COIN and BLK in offering cryptocurrency custody services. Meanwhile, UBER, LYFT, and DASH all slumped Tuesday after a Dept. of Labor proposal was announced that would require any contractor that was “economically dependent” on a company to be classified as an employee by that company. This would dramatically raise costs. In union news, AMZN workers in Southern CA have filed a petition with the National Labor Relations Board to have a union election. At the same time, the voting started in the AMZN upstate NY union vote. Elsewhere, the US Supreme Court heard arguments on whether or not to overturn a CA law prohibiting the sale of meat (pork) from animals that were kept in tightly confined spaces (which is true for hogs (pork) and chickens and could even be argued for cattle). Companies that will be directly impacted include TSN, BRFS, HRL, IBA, PPC, and SAFM. Finally, in “sale news,” AMZN, WMT, and BBY kicked off the holiday sales season with major online sales events (which follow the success of AMZN Prime Day). Those 2-day sales started Tuesday.

In European economic news, Tuesday afternoon (US time), BoE Governor Baily told UK fund and investors that they had 3 days to get their portfolios fixed before the central bank will withdraw its bond-buying support from the market. The BoE has stepped in the last 2 weeks with emergency buying to prevent UK bonds from reaching a “self-reinforcing fire sale” situation. He also implies that this emergency action will delay quantitative tightening by the BoE (which was scheduled to start Oct. 31) until later this year. Elsewhere, the ECB announced it will wait until interest rates are back close to 2% before it begins to shrink its own balance sheet.

So far this morning, PEP beat on both the revenue (by over $1.13 billion) and earnings (by 7%) lines. The company also raised its 2022 annual forecast for revenue by 20% (from +10% to +12% for the year). The company said its revenue rose 20% for Q3 (through price increases) despite a small decline in product volume sold. This indicates that the “inflation story” has given the company cover to increase prices by significantly more than costs rose and that the consumer is willing to accept these higher prices.

In mortgage news, home loan applications fell 2% for the week as the interest rate on a 30-year, fixed-rate, conforming loan went from 6.75% to 6.81%. However, as rates have risen, there has been renewed interest in adjustable-rate mortgages (which has been a dead niche for years). (ARMs used to make up less than 3% of loans and now are up to 12% of all new home loans.) This shift comes as home buyers have become accustomed to very low rates and either expect rates to come back down or are betting that they will have moved again before the rate adjusts up. The rate for a 5/1 ARM (rate is set for 5 years) is just 5.56%.

Overnight, Asian markets were mixed again but more evenly split today. Shenzhen (+2.46%) and Shanghai (+1.53%) were by far the strongest markets. Meanwhile, it was Hong Kong (-0.78%), New Zealand (-0.76%), and Singapore (-0.70%) that paced the region’s losses. In Europe, the bourses are mixed on mostly modest moves at midday. The FTSE (-0.10%), DAX (+0.20%), and CAC (+0.11%) show indecision at this point. At the same time, smaller exchanges are showing greater moves (in both directions) in early afternoon trading. As of 7:30 am, US Futures are pointing toward a green start to the day. The DIA implies a +0.49% open, the SPY is implying a +0.67% open, and the QQQ implies a +0.89% open at this hour. At the same time, 10-year bond yields are up strongly again to 3.958% and Oil (WTI) is up one-half of a percent at $89.79/barrel in early trading.

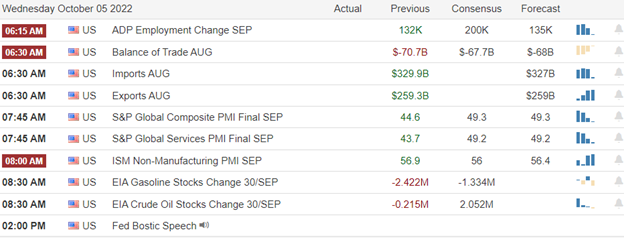

The major economic news events scheduled for Wednesday include September PPI (8:30 am), WASDE Ag Report and EIA Short-Term Energy Outlook (both at noon), September Fed Meeting Minutes (2 pm), and the API Weekly Crude Oil Stocks report (4:30 pm). We also have a Fed speaker scheduled (Bowman at 6:30 pm). The major earnings reports scheduled for the day are limited to PEP and WIT before the open. There are no major reports after the close.

In economic news later this week, on Thursday, September CPI, Weekly Initial Jobless Claims, EIA Weekly Crude Oil Inventories, and the Federal Budget Balance are reported. Finally, on Friday, we get September Retail Sales, September Import/Exports, August Bus. Inventories, Mich. Consumer Sentiment, and August Retail Inventories.

In earnings reports later this week, Thursday, we hear from BLK, CMC, DAL, DPZ, FAST, INFY, PGR, TSM, and WBA. Finally, on Friday, C, FRC, JPM, MS, PNC, USB, UNH, and WFC all report.

This morning all eyes will be on the PPI numbers during the pre-market. After that, some may look ahead to the Fed Minutes in the afternoon. However, we already know what FOMC Chair Powell said that day and have had an absolute chorus of Fed speakers reiterating the same story since. So, the meeting minutes may be a non-story. So, I think the inflation data (and read-through to out-guessing when the Fed will lighten up) will be the main market driver today. Don’t be surprised if we see some market “dead time” as some traders decide to wait on CPI and the real start of the Earnings Season before placing many bets. Overall then, look for morning volatility and a potentially dead market once we get past that knee-jerk and “second thought.”

With this backdrop, the premarket action seems to show some optimism ahead of the PPI data. The market is a bit extended in terms of T2122, but not extremely so. Watch the T-line levels for resistance if the bounce gets that far. Once again, the one thing we know for sure is that the strong bear trend is still in place and that has to be the main directional indicator we heed. So, don’t predict a bottom. If you are going long the market, be sure you are either quick or in it for the long term because a resumption of the down move is the most likely scenario for now.

Don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. When price does move in your direction, always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all OUR MONEY!). Also, keep in mind that trading is a job. It’s not a hobby. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Demonstrate patience and wait for confirmation. Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: EOG, COP, DVN, SLB, OXY, MRO, VLO, PSX. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Though the semiconductor sector attracted the majority of the bearish activity on Monday, the overall market experienced a chop fest as we waited for the uncertainty of inflation numbers and the earnings season kick-off. Unfortunately, we see bond yields surging higher this morning with little else in the earnings or economic calendars to inspire as we again wait. Watch for sensitivity to the news cycle as geopolitical tensions grow, and earnings warnings are seemingly on the rise.

While we slept, Asian markets mostly declined, with Taiwan stocks down 4% as TSMC plunged 8%. European markets see only red this morning as the dollar’s strength and weakening global growth worries persist. With another day of waiting ahead and bond yields surging, U.S. futures suggest a bearish open, with the QQQ leading the selling.

Economic Calendar

Earnings Calendar

We have five verified reports on Tuesday, but only two qualify as somewhat notable. They are AZZ and PNFP.

News & Technicals’

The Bank of England intervenes in the bond market again today. “Dysfunction in this market and the prospect of self-reinforcing ‘fire sale’ dynamics pose a material risk to UK financial stability,” the Bank of England warned. The move marks the second expansion of the central bank’s extraordinary rescue package in as many days after it increased the limit for its daily gilt purchases on Monday ahead of the planned end of the purchase scheme. Israel and Lebanon reached a historic agreement to resolve a long-running maritime border dispute following months of negotiations guided by the United States. “This is a historic achievement that will strengthen Israel’s security, inject billions into Israel’s economy, and ensure the stability of our northern border,” Israel’s Prime Minister Yair Lapid said in a statement. His comments came after Lebanon received the final draft of the U.S.-brokered agreement with Israel.

“I hope Musk cleans up Twitter,” JPMorgan CEO Jamie Dimon said in a CNBC interview. The remarks are Dimon’s first on the Musk-Twitter deal, revived last week after a fresh bid from Musk to buy the company. Dimon echoed Musk’s concerns about spam accounts and said Twitter should give users more control over its recommendation algorithms. Delta will have an exclusive five-year partnership with Joby operating electric vertical takeoff and landing aircraft, or eVTOLs, as part of the Delta network. As a result, Delta CEO Ed Bastian envisions moving passengers to and from airports quicker and with less hassle.

Two subsea pipelines connecting Russia to Germany are at the center of international intrigue after a series of blasts caused what might be the single largest release of methane in history. Many in Europe suspect the incident resulted from an attack, particularly during a bitter energy standoff between the European Union and Russia. However, the Kremlin has repeatedly dismissed claims it destroyed the pipelines, calling such allegations “stupid” and “absurd.”

As mentioned in Monday’s report, the hurry-up and wait in the market evolved into a chop fest as we ponder on inflation data and the beginning of the earnings season. The semiconductor attracted the most bear activity due to the new U.S. chip regulations temporally pushing the QQQ to a new 2022 low. Though we saw a reprieve from bond yield worries, they are back with a vengeance this morning, with the 2-year climbing to 4.32% in early Tuesday. In addition, the national average gas price continues to rise at $3.92, adding worries that the core inflation rate could rise despite the rapid rate-increasing efforts of the FOMC. Unfortunately, we face another day of waiting with little on the earnings and economic calendars to inspire. Plan for markets to be sensitive to early earnings warnings and geopolitical events and keep a close eye on support challenges as the bears continue to drive sentiment.

Markets gapped modestly higher Monday (+0.33% in the SPY, +0.45% in DIA, and +0.10% in the QQQ). However, the bears immediately stepped in to sell off the market to reach the lows of the day at about 1:15 pm. At that point, we reversed on a dime as the bulls took over to lead a strong rally for 45 minutes. Finally, we started a sideways roller-coaster ride of smaller moves for the last 2 hours of the day. This action has left us with black-bodied, Hammer Type candles with long, lower wicks in all 3 of the major indices. It is also worth noting that all 3 indices are also getting a little extended below their T-line (8ema) and both the SPY and QQQ are testing the breakout area of their Dreaded-h patterns.

On the day, 3 of the 10 sectors are in the green, but none of them were significantly higher. Consumer Defensive (+0.21%) was the largest gaining sector while Energy (-1.95%) and Technology (-1.94%) paced the losses. Meanwhile, the SPY was down 0.72%, DIA was down 0.34%, and QQQ was down 1.08% (to a 2-year low). The VXX was up just less than 2.49% to 21.43 and T2122 was up, but remains in the oversold area at 13.38. 10-year bond yields remain at 3.888% since the bond market was closed and Oil is down 2% to $90.75/barrel. Overall, it was an indecisive down day.

In economic news, midday, Chicago Fed President Evans continued to chorus from the Fed, saying that fighting inflation is still the top priority, even if it means job losses. At roughly the same time, JPM CEO Jamie Dimon told CNBC that said that the US economy is “actually doing very well” at the moment. However, he sees a “very, very serious” combination of headwinds that are likely to push the US and global economies into recession in the next six to nine months. He went on to say that Europe is already in recession and blamed the Fed for waiting too long to fight inflation and then doing too little. His opinion stands in contrast to others like Ark Investors CEO Cathie Wood who released an open letter to the Fed Monday warning that their tight policy could very well cause deflation if they don’t ease. Elsewhere, in the afternoon, the union that represents workers who build and maintain rail tracks voted to reject the offer made by the committee representing the major freight rail carriers. This brings the total to date to only four of 12 unions that have voted to accept the offer. However, the parties have agreed to a “cooling off period.” So, no rail strike is immediately imminent and negotiations will resume.

In stock news, Bloomberg reported Monday afternoon that XOM is considering buying DEN. No final decisions have been reached, but DEN has been seeking strategic options. BA rival Airbus (an OTC stock) increased deliveries in September, delivering 55 aircraft to bring the YTD total to 437. BA will announce its own numbers Tuesday. The Wall Street Journal reported that BIO is in talks to merge with QGEN. Elsewhere, the European Commission has informed TEVA that its preliminary view is that the company has breached European Union antitrust rules. Relate to climate and green initiatives, HON announced it has a new technology that can convert ethanol into jet fuel. This would reduce emissions and help airlines comply with standards that can let them qualify for incentives as laid out in the US Inflation Reduction Act. Finally, after-hours LEG cut its 2022 guidance by between $100 million and $200 million. LEG stock was down 8% in after-hours trading.

In Russian news, on Monday, the Putin regime retaliated for the weekend bombing of his bridge over the Kerch straight (to Crimea). Russia launched well over 100 cruise missiles, 30 kamikaze drones, and more than 40 rockets. About half of the missiles and nearly all of the drones were shot down by Ukrainian forces. However, that left about 50 missiles and 40 smaller rockets that hit their non-military targets, many of which were not even of an infrastructure nature. The G-7 will hold an emergency meeting to discuss responses to the Russian attacks today and Ukrainian President Zelenskyy will speak. Elsewhere, pro-Russian hackers briefly took airport websites in Chicago, Los Angeles, Atlanta, and New York offline Monday.

The Bank of England was forced to step into UK bond markets again Tuesday. A day after it extended its emergency measures to backstop pension funds, the BoE said it was seeing “fire sale dynamics” in the UK bond market as it began buying inflation-tied bonds (in addition to its other bond buying). One of the important UK financial think tanks (IFS) said it estimates the new UK government will need to come up with $66 billion in spending cuts before the new budget is announced (a month early to shore up markets) on October 31.

Overnight, Asian markets were mixed again, but leaned heavily to the downside. Taiwan (-4.35%), Japan (-2.64%), and Hong Kong (-2.23%) led the region lower on fears of economic slowdown and the impacts of President Biden’s chip export (to China) bans. Meanwhile, Shenzhen (+0.53%), New Zealand (+0.35%), and Shanghai (+0.19%) managed to stay green. In Europe, with the exception of Russia (+1.42%), stock exchanges are red across the board at midday. The FTSE (-0.94%), DAX (-0.87%), and CAC (-0.54%) lead the region lower in early afternoon trade. As of 7:30 am, US Futures are pointing a down start to the day. The DIA implies a -0.52% open, the SPY is implying a -0.62% open, and the QQQ implies a -0.60% open at this hour. 10-year bond yields are up to 3.924% and Oil (WTI) is off 2.34% to $88.96/barrel in early trading.

There major economic news events scheduled for Tuesday are limited to a pair of Fed speakers (Harker at 11:30 am and Mester at noon). Once again, there are no major earnings reports scheduled for the day.

In economic news later this week, on Wednesday we get September PPI, the WASDE Ag Report, September Fed Meeting Minutes, and the API Weekly Crude Oil Stocks report and Fed member Bowman speaks. Thursday, September CPI, Weekly Initial Jobless Claims, EIA Weekly Crude Oil Inventories, the Federal Budget Balance are reported. Finally, on Friday, we get September Retail Sales, September Import/Exports, August Business Inventories, Mich. Consumer Sentiment, and August Retail Inventories.

In earnings reports later this week, on Wednesday, PEP and WIT report. Thursday, we hear from BLK, CMC, DAL, DPZ, FAST, INFY, PGR, TSM, and WBA. Finally, on Friday, C, FRC, JPM, MS, PNC, USB, UNH, and WFC all report.

Markets seem very fragile amidst the global recession fears, new chip export to China bans (TSM was down 8% in Taiwan overnight), and the Russian War caused energy crisis (and OPEC’s support of Russia and higher oil prices through production cuts). With Inflation data coming both Wednesday (PPI) and Thursday (CPI) as well as Earnings Season kicking off again with Big Banks on Friday, it is hard to see a catalyst for any bullish turn other than a “hopium knee-jerk reaction” to some data point. So, the mood is glum and the market bias will remain bearish overall for at least the short-term.

With this backdrop, the premarket action seems pretty tame, down a half of a percent overall. (Again, perhaps because Mr. Market is waiting on another shoe to drop.) The market SPY and especially the QQQ are extended (to the downside) from their T-Lines, but the DIA remains within 1.3% in premarket and T2122 is oversold, but not extremely. So, a bounce is not set up technically. As has been true for quite a while, the one thing we know for sure this morning is that the strong bear trend is still in place and again that should be the main directional indicator we heed. The large-cap indices MAY find some support at their Dreaded-h pattern breakout levels. However, remember that level did nothing to help the QQQ bulls hold up.

Keep in mind that trading is our job. It’s not a hobby. So, treat it that way. Do the work and follow the process. Stick with your trading rules, trade with the trend, and take those profits when you have them. Demonstrate patience and wait for confirmation. Don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. When price does move in your direction, always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all OUR MONEY!). Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: SRTY, MARA, WDC, MMM, QQQ, NFLX, DASH, RIVN. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Today the market may breathe a sigh of relief with the bond market closed for Columbus Day, providing a break from the rising yields. Unfortunately, with no earnings or economic reports today, we could see a choppy day as we wait for the inflation reports and the kick-off of the 4th quarter silly season. The hopefulness of the so-called Fed pivot fell apart on Friday with the strong jobs report suggesting another 75 basis point increase is possible. Watch for earnings warnings and possible downgrades as the economic challenges continue.

Asian markets fell across the board during the night, with tech stocks taking the biggest hit due to the new U.S. chip regulations. European markets traded in a choppy session this morning with flat to slightly bearish results. U. S. futures recovered substantially from overnight losses, but at the time of this report suggests an uncertain and flat open. Expect choppy price action and a sensitivity to the news cycle as we hurry up and wait.

Economic Calendar

Earnings Calendar

Although we have eight companies listed on the Monday earnings calendar, there are no confirmed reports today.

News & Technicals’

The U.S. announced Friday that new U.S. rules require companies to apply for a license if they want to sell certain advanced computing semiconductors or related manufacturing equipment to China. Notably, the changes also mean foreign companies will need a license if they use American tools to produce specific high-end chips for sale to China. “The U.S. has been abusing export control measures to block and hobble Chinese enterprises wantonly,” the Chinese Ministry of Foreign Affairs Spokesperson said.

Allianz Chief Economic Adviser Mohamed El-Erian said he predicts headline inflation “will probably come down to about 8%,” but that core inflation “is still going up.” El-Erian said an increase in core inflation means “we still have an inflation issue.” On Monday, the Bank of England announced that it would introduce further measures to ensure an “orderly end” to its purchase scheme on October 14. Following last month’s unprecedented spike in gilt yields, LDIs — which hold substantial quantities of gilts and are owned predominantly by final salary pension schemes — were receiving margin calls from lenders.

The bears could breathe a sigh of relief today because the bond market is closed for Columbus Day, which aided the Friday selling as yields surged. However, the challenging price volatility will remain due to the uncertainty of the 4th quarter earnings season beginning Thursday, FOMC minutes, a CPI, PPI, and retail sale report. Moreover, the narrative of a Fed pivot that created last week’s nasty whipsaw hurt a lot of speculation retail bounce traders. It may soon usher in a capitulation event if earnings begin to disappoint and fear turns to panic. That said, be ready for big price swings but stay focused and follow the trend because there will be plenty of opportunities to profit.

On Friday, markets gapped lower on the better-than-expected September Payroll data (which leads traders to conclude that what the Fed has been saying is true…and the Fed will not be easing up on rate hikes anytime soon). SPY gapped down 1.1%, DIA gapped down 0.9%, and QQQ gapped down 1.75%. After that, the Bears followed up with a strong selloff in the first 30 minutes before starting a much slower downtrend that has lasted all the way into a small bounce in the last 30 minutes of the day. This action has given us gap-down, large black candles with small lower wicks that are starting to get just a little extended below the T-line (8ema). The QQQ is even nearing the breakout of its bearish “Dreaded h” pattern.

On the day, all 10 sectors are in the red. Technology (-4.13%) is leading the way lower while Energy (-0.62%) is the laggard in the decline. At the same time, SPY was down 2.81%, DIA is down 2.08%, and QQQ is down 3.81%. The VXX is up 4% to 20.91 and T2122 has dropped back into the oversold territory at 8.54. 10-year bond yields are up to 3.883% and Oil (WTI) has spiked 4.76% to $92.66/barrel after a strong Payrolls Report seemed to tell the market demand will remain high while production will go down (based on the upcoming OPEC+ production cuts). So, it was a “good news is bad news” day that has all 3 major indices working on another dreaded-h pattern.

In economic news, September Nonfarm Payrolls came in above expectation (at +263k versus +250k forecasted and +315k in August). However, September Avg. Hourly Earnings came in lower than expected at +5.0% versus +5.1% forecasted and +5.2% in August. That may be partially responsible for the September Participation Rate falling slightly to 62.3% (from 62.4% in August). With that said, the September Unemployment fell to 3.5% (from 3.7% forecasted and 3.7% in August). So, both of the headline numbers fall into the category of “things that will not give the Fed reason to start easing their rate hikes.”

In stock news, on Friday, BP announced that it has boosted spending by $500 million in the North Sea and US Shale Basin in response to oil and gas shortages. However, it does not expect any of those projects to increase production for months. PEP also said it expects to receive the first of 100 TSLA semi tractors on Dec. 1. (The trucks have been on order since 2017 and PEP will be the first company to receive the new TLSA Semi.) NIO announced that it will only lease (not sell) its electric vehicles when they go to market in Europe later this year. The average lease will be $1,200/month. Elsewhere, the NHTSA announced it has closed a safety investigation (started in 2017) into tired from GT. Finally, RIVN has recalled almost all of the vehicles they have built over safety concerns stemming from a bolt that appears not fully tightened during production (on nearly every car).

In warning news, an FDX internal memo reported by Reuters showed that the company is significantly lowering its holiday package volume forecast. The memo did not give the new number but warned contractor delivery companies to expect a downward adjustment to forecasts soon as major shippers have told FDX executives they are adjusting their own forecasts lower. On Saturday, SSGFF (Samsung) warned that its profits will take up to a 32% hit for the year due to a slowdown in memory chip sales, meaning its customers like INTC, AMD, NVDA, LNVGY, AAPL, HPE, and DELL must be buying less and their own forecasts could be in jeopardy.

In international news, on Saturday, Russia seized the Sakhalin-1 Oil and Gas Project, which leaves US, Japanese, and Indian investors at risk as the order puts a Russian Operator in charge and authority over whether foreign investors can retain their stakes given to the Russian government. XOM has/had a 30% stake in the project, while Japan’s Sodeco had a 50% stake. Elsewhere, also Saturday, Taiwan signaled that it will follow President Biden’s new export controls (issued Friday) which limit the export of semiconductor chips made anywhere in the world using US chipmaking equipment. This will end exports from TSM (and much smaller UMC) to China. In France, strikes at oil refineries and storage facilities owned by TOT and XOM have more than 21% of gas stations closed for lack of supply. TOT announced it will begin wage negotiations with the union this month. The French government said it has a plan to ration fuel, but the situation has not yet reached that point.

Overnight, Asian markets were red across the board. Hong Kong (-2.95%), Shenzhen (-2.38%), and Shanghai (-1.66%) led the region lower. In Europe, markets are mixed but lean to the red side in midday trading. The FTSE (-0.31%), DAX (+0.64%), and CAC (-0.07%) lead the market, with Russia (-3.21%) being an outlier in early afternoon trading. As of 7:30 am, US Futures are pointing toward a modestly red start to the day. The DIA implies a flat -0.06% open, the SPY is implying a -0.15% open, and the QQQ implies a -0.25% open at this hour. 10-yeat bond yields are at 3.888% and Oil (WTI) is down eight-tenths of a percent to $91.90/barrel in early trading.

There are no major economic news events scheduled for Monday (Columbus Day). Bond markets are closed (although stock markets are open). However, we do have a Fed speaker (Brainard at 1 pm). There are no major earnings reports scheduled for the day.

In economic news later this week, on Tuesday we have another pair of Fed speaker (Harker and Mester). Then on Wednesday we get September PPI, the WASDE Ag Report, September Fed Meeting Minutes, and the API Weekly Crude Oil Stocks report and Fed member Bowman speaks. Thursday, September CPI, Weekly Initial Jobless Claims, EIA Weekly Crude Oil Inventories, the Federal Budget Balance are reported. Finally, on Friday, we get September Retail Sales, September Import/Exports, August Business Inventories, Mich. Consumer Sentiment, and August Retail Inventories.

The silly season begins again later this week after a couple of days of reprieve. There are no reports scheduled for Monday or Tuesday. Then, on Wednesday, both PEP and WIT report. On Thursday, we hear from BLK, CMC, DAL, DPZ, FAST, INFY, PGR, TSM, and WBA. Finally, on Friday, the banks really kick off the season with C, FRC, JPM, MS, PNC, USB, UNH, and WFC all report.

With September Payrolls behind us and the Fed chorus continuing to beg us to believe that they will not be easing up on rate hikes anytime soon, dejected traders will start watching for earnings evidence to support their preconceived ideas. The weekend has probably taken care of the Payrolls Report volatility. However, good old-fashioned everyday volatility is likely to remain. Also, keep an eye on Ukraine as Putin is a sore loser and has lost face after 2 lanes of his Kerch Bridge were blown up on Saturday. It appears he is moving another large group of soldiers toward Belarus again, perhaps planning to take another run at Kyiv.

With this backdrop, the premarket action seems pretty mild. (Again, perhaps waiting on earnings to begin.) The market extension (to the downside) is a modest issue but we’ve seen far worse recently. So, I will start to watch for (but not expect today) a consolidation or relief rally. The one thing we know for sure this morning is that the strong bear trend is still in place and again that should be the main directional indicator we heed.

Keep in mind that trading is our job. It’s not a hobby. So, treat it that way. Do the work and follow the process. Stick with your trading rules, trade with the trend, and take those profits when you have them. Demonstrate patience and wait for confirmation. Don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. When price does move in your direction, always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all OUR MONEY!). Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: TOST, TWTR, SNOW, RBLX, AAPL, META, SBUX, TSLA, and PYPL. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The 3 major indices gapped modestly lower at the open Thursday. Then, initial volatility kicked in for the first hour of the day, reaching the day’s highs and lows in that hour. After that, stocks meandered sideways in a tight range in the lower half of the day’s range until 2:45 pm (when the bears pushed us lower into new lows for the day. This action left us with black-bodied, long-wick, indecisive candles in all 3 major indices. All 3 still remain above their T-line (8ema). This can also be seen as a Bearish Harami candle in the QQQ and SPY indices.

On the day, 9 of the 10 sectors are in the red. Energy (+0.74%) was the lone green sector while Utilities (-2.90%) was by far the lagging sector. Meanwhile, the SPY was down 1.04%, DIA down 1.16%, and QQQ down 0.79%. The VXX was up 2.92% to 20.09 and T2122 fell but remains in the mid-range at 42.25. 10-year bond yields spiked to 3.822% and Oil was up 1.44% to $89.02/barrel. Overall, this made Thursday a day of consolidation, perhaps as the market waits on today’s September Payrolls reports.

In economic news, the Weekly Initial Jobless claims came in higher than expected at 219k (versus 203k forecast and last week’s 190k reported). Meanwhile, among Fed speakers, Minneapolis Fed President Kaskari said the Fed has “more work to do on bringing down inflation” and that the Fed is “quite a way away from being able to pause aggressive rate hikes. At the same time, Chicago Fed President Evans said that the Fed’s rate policy is likely headed to 4.5% – 4.75% by Spring 2023, saying the Fed has “further to go” (on rate hikes). New Fed Governor Cook said that inflation “remains stubbornly and unacceptably high and the data over the last few months show that inflationary pressure remains broad-based.” She went on to say “we (Fed) will keep at it until the job is done.” So, once again, every Fed speaker has told us that there is no letup in sight on Fed rate hikes (despite Fed Fund Futures pricing in a rate cut next year).

In stock news, during the day, a French court substantially lowered the fine that had been levied against AAPL (from $1.1 billion to $366 million) for anti-competitive behavior. While the court agreed that AAPL had abused retailers economic dependency on the company, it also overruled the guilty charge of price-fixing as unproven. Elsewhere, TM announced that is resuming production of its first electric vehicle (which had been halted for 3 months while new safety measures were designed and implemented related to the batteries). HMC also announced its first electric SUV, which will hit the market for the 2024 model year. Meanwhile, the Executive Chairwoman of FFIE resigned (Oct. 3 but announced Thursday), citing death threats she has received during the ongoing fight for control of the company’s board. In addition, BRY stock jumped during the late afternoon when Reuters reported the company is exploring “strategic options including a potential sale.” Finally, Elon Musk again asked for a postponement of the TWTR litigation and said that he expects the original deal to close on or about Oct. 28.

In profit warning news, after the close, LEVI missed on revenue and beat on earnings. However, it also cut its full-year forecast. LEVI also warned on profits citing inflation and a consumer shift away from higher-end products. Elsewhere, AMD issued its Q3 preliminary results (it is scheduled to officially report November 1, after the close). The company said results are likely to come in well below forecast on both weaker demand and supply chain issues. The company expects gross margins of about 50% (versus the previous forecast of 54%). Meanwhile, Bloomberg reports that its sources indicate CS may lose $2 billion this year. In related news, CS is trying to bring in an unnamed outside investor to purchase its advisory and investment banking units as the main part of CEO Koerner’s restructuring plan. Finally, this morning CS announced it will be buying back just over $3 billion of its own debt and selling the bank-owned Savoy Hotel (located in the Swiss Financial district) in an attempt to fight off a falling share price and ever-increasing bets against the company’s credit default swaps.

In pot news, President Biden pardoned thousands of people with federal convictions for simple marijuana possession. He also initiated a new review of how the drug is classified. (Currently marijuana is classified as “schedule 1” or the most dangerous class of drug. This is a higher classification, meaning harsher penalties, than fentanyl or methamphetamine.) The President also went on to put pressure on state and local officials by saying nobody should be in jail solely for marijuana possession and urged governors to follow his lead on the matter. Cannabis tickers like TLRY and CGC jumped more than 20% on the news.

Overnight, Asian markets were red across the board. Hong Kong (-1.51%), Taiwan (-1.37%), and Shenzhen (-1.29%) led the region lower. Meanwhile, in Europe, stocks are mixed on modest moves at midday. The FTSE (+0.14%), DAX (-0.08%), and CAC (+0.16%) lead the region on volume, per normal, in early afternoon trade. However, it appears the region is waiting on the US September Payrolls Reports as a read-through to economic slowing (and perhaps Fed actions). As of 7:30 am, US Futures are pointing toward a mixed, flat start to the day. The DIA implies a +0.22% open, the SPY is implying a +0.06% open, and the QQQ implies a -0.25% open at this hour (pre-news). 10-year bond yields are up again to 3.845% and Oil (WTI) is up 1% to $89.35/barrel in early trading.

The major economic news events scheduled for Friday include Sept. Avg. Hourly Earnings, Sept. Payrolls, Sept. Participation Rate, and Sept. Unemployment Rate (all at 8:30 am). We also have a Fed speaker (Williams at 10 am). There are no major earnings reports scheduled for the day.

With September Payrolls data coming today, do not be surprised if a beat is bad for markets (as traders assume the Fed will keep on the path of over-sized rate hikes) and visa-versa (a miss may cause traders to jump to the conclusion that the Fed will ease up). The average estimate is for a gain of 255k jobs in September. In either case, we can probably expect the market reaction to be an overreaction and a short-lived one at that. In other words, we are likely to see a swing back the other way very soon. On top of that, there has been no indication whatsoever from Fed members that they are even considering an easing. In fact, most true Fed Watchers are of the opinion they will not change course until something in the economy breaks.

With this backdrop, the premarket action seems to be waiting on the news. Market extension is not an issue as the premarket action has us sitting on the T-line (8ema) in all 3 major indices. The one thing we know for sure this morning is that the strong bear trend has not been broken and that is the main directional indicator we should heed. As mentioned, expect significant volatility today, especially in the premarket as the Payrolls data is released. So, in general, unless you are very quick or very comfortable in high volatility, this could be a day to sit on your hands and “wait and see” at least in the morning.

Keep in mind that trading is our job. It’s not a hobby. So, treat it that way. Do the work and follow the process. Stick with your trading rules, trade with the trend, and take those profits when you have them. Demonstrate patience and wait for confirmation. Don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. When price does move in your direction, always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all OUR MONEY!). Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: No tickers today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The narrative of a Fed pivot kept the bulls inspired Wednesday despite the economic data showing the battle against inflation is not over. Moreover, the decision of OPEC to cut production by two million barrels a day adds pressure to the inflation fight as oil and gas prices surge. With few notable earnings reports, Jobless Claims, and several Fed speakers, we should expect another wild of price volatile as we wait for the Friday Employment Situation numbers.

While we slept, Asian markets traded mixed in reaction to the OPEC decision. European market markets struggle in a choppy morning session turning modestly bearish as the rally momentum fades. As I write this report, U.S. futures have reversed overnight gains suggesting a lower open ahead of earnings and economic reports. With 4th quarter earnings just a week away, uncertainty remains high, so plan for the challenging price action to continue.

Economic Calendar

Earnings Calendar

Just one week before the official kick-off of 4th quarter earnings, we have a few noteworthy stocks on the calendar today. Notable names include ANGO, CAG, STZ, LEVI, & MKC.

News and Techniclals’

Energy analysts believe deep production cuts from OPEC+ could backfire for U.S. ally Saudi Arabia. OPEC and non-OPEC allies, often referred to as OPEC+, agreed on Wednesday to reduce oil production by 2 million barrels per day from November. The move is designed to spur a recovery in oil prices, which had fallen to roughly $80 a barrel from more than $120 three months ago. However, Washington sees OPEC+’s decision as political interference and a “blow” against U.S. President Joe Biden, said Dan Yergin, vice chair of S&P Global. Secondly, it’s seen as somehow political interfering in the U.S. election, although the cut doesn’t go into effect until November,” he said. “There seems to be a mini battle between [Strategic Petroleum Reserve] releases in the White House and what’s going on with OPEC+,” said Bill Perkins, CEO of Skylar Capital Management.

Analysts said Apple’s next iPhone would likely be equipped with USB-C charging rather than its proprietary Lightning system. It comes after lawmakers in the European Parliament approved a law requiring electronics sold in the European Union to be equipped with a USB Type-C charging port by the end of 2024. Indeed, there are rumors that Apple is exploring USB-C for the iPhone 15, which is what the next device could be called if the traditional naming convention continues. Analysts said Apple’s change to USB-C will likely be for the global market, including the U.S., rather than just the EU.

Ford is increasing the entry-level price of its electric F-150 Lightning pickup by $5,000 for the 2023 model year due to rising costs and supply chain issues. As a result, the starting price of the 2023 Lightning Pro model will be $51,974 – up nearly 11% and a 30% increase from the truck’s $39,974 price in May 2021. However, the company said the price increase would not impact current retail order holders and commercial and government customers with scheduled orders. Treasury yields rallied slightly in early Thursday trading as inflation worries and hawkish Fed policies continue.

The wild price action continues as the hope of a Fed pivot inspires buyers to recover the Wednesday morning gap that temporarily produced gains on the day. Unfortunately, bond yields and the dollar’s strength continue to inhibit bullish sentiment. Add in the OPEC decision that’s quickly raising oil and gas prices and fanning the flame of inflation, thickening the dark cloud hanging over the weakening economy. Today we get the latest read on Jobless claims and more Fed speeches for the market to process as we move toward the Friday Employment Situation report. Plan carefully and expect the volatile uncertainties to continue.