The market faces some complex challenges this week with the rising pandemic concerns in China, crypto market uncertainties, and rising U.S. layoffs as we slide toward a holiday shutdown. With earnings inspiration winding down, only one day of market-moving economic reports, expect news sensitivity, choppy conditions, and declining volume this week. Plan your risk carefully, as holiday weeks typically suffer declining volume as traders and investors head out for holiday plans.

Asian markets mostly declined while we slept, even as China held steady benchmark lending rates with pandemic concerns rising. European markets trade red across the board this morning as recession worries persist. U.S. futures point to a modestly bearish open as earnings inspiration declines and holiday travel sets the stage for choppy market conditions.

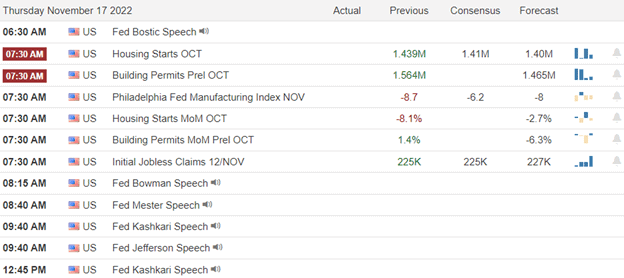

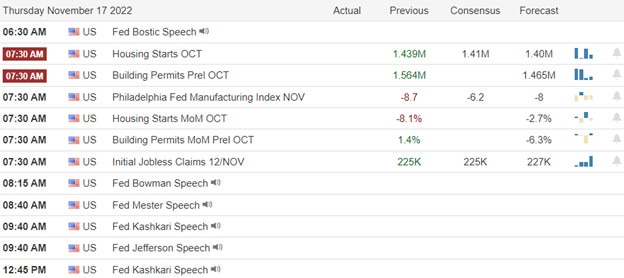

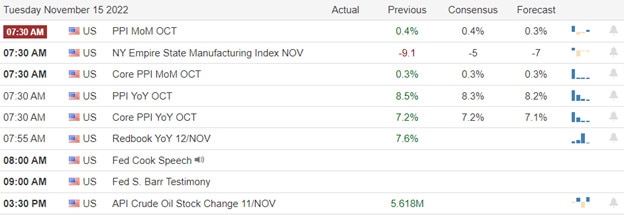

Economic Calendar

Earnings Calendar

Though the bulk of 4th quarter earnings has passed, we still have a few each day as the theme of retail reports continues. Notable reports include A, DELL, SJM, J, LI, URBN, WEBR, & ZM.

News & Technicals’

Bob Iger is back as CEO of Disney. Bob Chapek was named CEO in February 2020 and came under fire for various decisions. Shares of Dow 30 component Disney jumped in premarket trade Monday. Bob Iger has disapproved of several of Bob Chapek’s changes to Disney despite handpicking him as his successor in early 2020, sources have told CNBC. Disney shares have fallen more than 40% this year, including slumping on weak fiscal fourth-quarter results earlier this month. The biggest point of contention may be Chapek’s reorganization of the company, which established a new division called Disney Media and Entertainment.

Bitcoin hovered around a one-week low on Monday, and other major cryptocurrencies fell sharply as the impact of the dramatic collapse of FTX continued to ripple through the market. The cryptocurrency market has come under pressure over the last two weeks as problems at major exchange FTX came to light. From Nov. 6 — the day Binance CEO Changpeng Zhao said his exchange would liquidate its FTT tokens — the crypto market has lost more than $260 billion of value.

The latest NFIB monthly small business confidence and jobs reports show that Main Street is still looking to hire even as economic sentiment continues to decline. But the vast majority of open positions (90%) are seeing few to no qualified applicants apply even as layoffs mount throughout the economy. In addition, higher wages get harder for business owners to offer as inflation increases as a margin pressure amid a lower sales outlook. Still, other work benefits and perks can be used to attract talent.

As the Thanksgiving shutdown approaches, the market faces some complex challenges, with layoffs rising in the U.S., and new pandemic issues in China, while the crypto market uncertainty continues. As a result, expect exchange volumes to decline sharply this week as traders and investors head out for holiday plans. Chop may be the word of the week as earnings inspiration dwindles and all the potential market-moving economic reports bunched up on Wednesday morning. Holiday weeks can be very news-sensitive, so plan your risk accordingly.

Markets diverged at the open again Friday as the SPY gapped up 0.87%, DIA gapped up 0.37%, and QQQ gapped up 1.10% to start the day. However, at that point, all 3 got back in-step and sold off the first 40 minutes with all 3 having recrossed their gaps by 10:10 am. Then 3 major indices diverged again with QQQ continuing its selloff, DIA going sideways back and forth inside its morning gap in waves, and the SPY bouncing along on both sides of the Thursday close. This lasted until 3:30 pm, when a broad-based rally took all 3 indices back up a bit. All this action is giving us black-bodied candles that retested and held the T-line in all 3 major indices. The DIA was more of an indecisive Doji candle while the SPY was more of a Black Hammer, and the QQQ was just a black candle with a large lower wick.

On the day, seven of the ten sectors are in the green, with Utilities sector (+2.00%) leading the winners by a large margin while the Energy Sector (-0.67%) fared worst. Meanwhile, the SPY gained 0.45%, the DIA gained +0.38%, and the QQQ was dead flat at day end. The VXX fell 1.03% to 16.41 and T2122 climbed back into the low end of the overbought territory at 85.71. 10-year bond yields have climbed back up to 3.824% and Oil (WTI) plunged another 1.90% to $80.09 per barrel. So, overall Friday was a gap-up day where that turned indecisive as the bulls could not follow through and the bears were able to fade the gap, but ultimately could not drive prices lower as the late-day rally turned markets modestly green.

In stock news, CVNA announced Friday they are cutting another 1,500 jobs (another 8% of the workforce) after cutting 2,500 earlier in the fall. In other Auto industry news, EVGO announced a deal to become the preferred EV charging partner of Subaru with buyers of some of Subaru’s EV offerings receiving a $400 credit to use EVGO fast charging stations nationwide in the US. Elsewhere, HON agreed to pay $1.3 billion to end asbestos-related lawsuit claims against a former business unit. On Saturday, TSLA recalled 321,000 cars over rear light problems. Finally, in a shocker, the CEO of DIS (Chapek) was ousted Sunday night and replaced with former DIS CEO, Bob Iger. Iger returns to the job after a 3-year hiatus.

In miscellaneous news, the CFTC reports the that US Dollar is in a “net short” position for the first time since July 2021. Former Theranos CEO Elizabeth Holmes was sentenced to 11 years in prison Friday after the close for her defrauding of investors. In economic news from Friday, the October Existing Home Sales came in a bit higher than expected at 4.43 million (compared to the forecasted value of 4.38 million, but worse than the September value of 4.71 million). In China-related news, the bull’s hopes that China was pivoting from its “Zero Covid” policy evaporated over the weekend as the city was rumored to be a test case for loosening instead closed schools, locked down universities and ordered its residents to stay at home for 5 days. So, no loosening yet.

In Ecological news, the COP27 conference reached a deal to pay the poor countries for all the environmental damage caused by climate change due to the industrialized nations’ emissions. However, no more progress was made on getting the industrialized nations (especially the US and China) to actually meet their previously agreed commitments to reduce emissions.

So far this morning, J and SJM both beat on the revenue and earnings lines.

Overnight, Asian markets leaned heavily to the downside, but on mostly modest moves. Hong Kong (-1.87%) was by far the biggest loser while South Korea (-1.02%), and India (-0.88%) rounded out the biggest red numbers. On the upside, only Japan (+0.16%), and Thailand (+0.09%) managed to stay green on the day. Meanwhile, in Europe, we see a similar picture taking shape at midday. The FTSE (-0.05%), DAX (-0.67%), and CAC (-0.20%) are typical of the region in early afternoon trade, with only 2 small exchanges managing to stay modestly green so far. As of 7:30 am, US Futures are pointing toward a red start to the day. The DIA implies a -0.25% open, the SPY is implying a -0.57% open, and the QQQ implies a -0.82% open at this hour. At the same time, 10-year bond yields are up to 3.831% and Oil (WTI) is off eight-tenths of a percent to $79.40/barrel in early trading.

There are no major economic news events scheduled for Monday. The major earnings reports scheduled for the day are FUTU, SJM, J, and NIU before the open. Then, after the close, A, CENTA, CENT, DELL, MMS, SNEX, URBN, ZM, and ZTO report.

As you would expect on a holiday week, this week will be light on economic news. On Tuesday we get the API Weekly Oil Stock report as well as 3 Fed speakers (Mester, George, and Bullard). Then Wednesday, October Building Permits, October Durable Goods, Weekly Initial Jobless Claims, Mfg. PMI, Services PMI, Michigan Consumer Sentiment, October New Home Sales, EIA Weekly Crude Oil Inventories, and FOMC Meeting Minutes are reported. Thursday and Friday have no economic news due to the holiday.

In earnings reports later this week, on Tuesday, we hear from ANF, AEO, AMWD, ADI, BIDU, BBY, BURL, CAL, CSIQ, CHS, DKS, DLTR, DY, IQ, MDT, VIPS, WMG, ADSK, GES, HPQ, and JWN. Then on Wednesday, DE and LU report. There are no reports on Thursday or Friday due to the holiday.

The shortened holiday week is shaping up to be light on news and lighter on earnings than in recent weeks. Still, we will get some more retail and miscellaneous earnings reports (mostly Tuesday). In the short term, the trend remains bullish and over-extension has been addressed with last week’s pullback and hold to the T-line and support. With this background, what we know for sure is that the probabilities in the near term lie in the Bull’s favor. However, continue to be cautious about chasing. Finally, expect the volume to lighten up as we get closer to the holiday (and we can expect Friday’s half-day to be a dead market).

As always, be deliberate and disciplined…but don’t be stubborn. Remember it’s 100 times more important to avoid big mistakes than it is to pick big winners. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: GRWG, DDD, AAPL, NKE, FSM, TSLA, NOK You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The theme of the week continued with Thursday producing another big point whipsaw as robust economic data encouraged more hawkish statements from Fed members. Though the recovery rally left a lot of bullish engulfing patterns across charts, index volumes remained noticeably low with significant overhead resistance that the bulls have yet to breach. As you plan forward, keep in mind the holiday week ahead, and the likelihood of choppy light volume as traders hit the airports and byways.

After Japan reported the highest inflation in 40 years, the Asian markets closed the day mixed and relatively flat. However, European markets trade decidedly bullish this morning as rate hikes and recession worries linger. The U.S. futures point to another morning gap up, hoping to capitalize on yesterday’s recovery rally with housing data ahead as we slide into the weekend and toward the Thanksgiving holiday. Expect the volatility to continue.

Economic Calendar

Earnings Calendar

The Friday earnings calendar only has eight confirmed reports. Notable reports include BKE, FL, & JD.

News & Technicals’

Swedish and Danish investigators are investigating a flurry of detonations on the Nord Stream 1 and 2 pipelines on Sept. 26 that sent gas spewing to the surface of the Baltic Sea. The explosions triggered four gas leaks at four locations — two in Denmark’s exclusive economic zone and two in Sweden’s exclusive economic zone. The Swedish Prosecution Authority said in a statement that “residues of explosives have been identified on several of the foreign objects seized,” according to a translation.

St. Louis Fed President James Bullard noted that “the policy rate is not yet in a zone that may be considered sufficiently restrictive.” Using the so-called Taylor Rule for monetary policy, Bullard suggested the proper zone for the fed funds rate could be in the 5%-7% range, higher than current market pricing and unofficial Fed forecasts indicate.

Internal Slack messages shared with CNBC showed engineers and other employees posting goodbye messages to a “watercooler” chat group during the 5 p.m. ET Thursday deadline that Musk set just a day earlier. Hundreds of salute emojis (which convey the message “thank you for your service”) streamed by, along with dozens of goodbye messages. Amazon will continue to lay off employees in the coming year, CEO Andy Jassy wrote in a memo to workers on Thursday. The company began informing workers this week that they were being let go. “I’ve been in this role now for about a year and a half, and without a doubt, this is the most difficult decision we’ve made during that time,” Jassy wrote.

Thursday proved to be just another big point whipsaw, with the Dow swinging more than 350 points from low to high, reacting to better-than-expected economic data and hawkish Fed statements. However, after gapping sharply lower at the open, it was nothing but buying the rest of the day, leaving behind a lot of bullish engulfing patterns in the charts. Unfortunately, the index volumes were markedly low, and bulls still have significant overhead yet to breach. So, take caution over overtrading as we head into the weekend, remembering subsequent week volumes are likely to decline sharply due to the holiday.

Again or still…for the second day in a row. However you say it, it’s the same story as Thursday.

Markets gapped down strongly Thursday after Wednesday’s Hawkish Fed statements. The SPY opened down 1.27%, DIA gapped down 1.00%, and QQQ jumped down 1.59% at the open. However, from that point, the bulls started a slow, wavy, rally that took us to the highs of the day about 1:20 pm. At that point, a slow, steady selloff started that took us back down into the morning gap, before rallying hard the last 30 minutes. During the session, price tested and held the T-line (8ema) in all 3 indices (SPY, DIA, and QQQ). This action gave us gap-down white candles with upper wicks in all 3 major indices.

On the day, eight of the ten sectors are in the red, with the Utilities sector (-1.53%) leading the losses while the Communications Services (+0.16%) and Consumer Defensive (+0.14%) sectors held up the best. Meanwhile, the SPY lost 0.31%, the DIA was flat at +0.01%, and the QQQ lost 0.22%. The VXX fell 0.96% to 16.58 and T2122 dropped back into the center of the mid-range at 56.25. 10-year bond yields have climbed to 3.769% and Oil (WTI) plunged 4.26% to $81.94 per barrel. So, overall Thursday was a gap-down day where the bulls immediately rejected the gap as the bulls and bears then fought to an overall standstill by day’s end.

In economic news, October Building Permits came in above the forecast at a number of 1.526 million (compared to 1.512 million expected, but still below the September value of 1.564 million). October Housing Starts also beat the forecasted value, coming in at 1.425 million (compared to the forecasted 1.410 million, but again still below the 1.488 million in September). Weekly Initial Jobless Claims also beat expectations, coming in at 222k (compared to a forecasted 225k and last week’s value of 226k). However, the November Philly Fed Mfg. Index came in far below expectations at -19.4 (compared to the forecasted -6.2 and October’s value of -8.7). In other economic news, Bloomberg reported that US mortgage rates saw the biggest drop in over 41 years this week, with the US avg. 30-year, fixed-rate mortgage dropping to 6.61% (lowest level in two months). In Fed news, Fed speakers gave us more hawkish comments Thursday. St. Louis Fed Pres. Bullard said that the rate hikes, so far, have only had limited effects on inflation. He suggested rates will have to be hiked further than expected to effectively bring down inflation. While he did not say how high, he used a chart that showed a range of 5%-7% (and we are currently between 3.75% and 4%). Later, Minneapolis Fed President Kashkari said he wants to be sure inflation has stopped climbing before he would support stopping interest rate hikes, and “it’s an open question how far we have to go with the interest rate (hikes).”

In stock news, Reuters reported that HAS is looking to sell its TV production business unit eOne. Meanwhile, the FAA said it does not expect to certify the BA “737 Max 7” plane this year. This means the plane will need to be reworked to meet new cockpit safety alert standards that come into effect on December 27. However, BA is still seeking a waiver from those safety standards from Congress, but no progress has been reported on that front yet. Elsewhere, GM subsidiary Brightdrop said it expects to reach $1 billion in revenue. Also on Thursday, workers at 100 SBUX stores held a 1-day walkout to protest “illegal retaliation against workers who tried to organize unions.” Elsewhere, after hours, DNUT settled US Dept. of Labor charges that it failed to pay overtime to several hundred workers by paying a $1.19 million fine. Finally, AMZN CEO Jassy said the company would continue cutting jobs into 2023, but did not detail the additional cuts.

In energy news, the EIA said on Thursday that in October, Heating Oil costs for US households were 65% more than in the same month of 2021. In part, this was due to the US importing 38% less distillate fuel than it has in recent years as well as by a fire that has taken the largest East Coast distillate refinery (in Philadelphia) offline permanently. In other energy news, the cause of Thursday’s selloff in oil is being attributed to bad covid news out of China. The Chinese new case total has risen to the highest level since April with the majority of new cases coming from the heavy manufacturing region of Guangzhou. However, the hawkish talk from Fed members also stoked fear of a rate-hike-induced economic slowdown in the US, which did not help oil prices.

After the close, AMAT, ROST, GPS, POST, UGI, KEYS, PANW, WWD, and STNE all reported beats on both the revenue and earnings lines. Meanwhile, WSM beat on the revenue line while missing on the earnings line. Unfortunately, FTCH missed on both the top and bottom lines. It is worth noting that ROST, KEYS, and PANW raised their forward guidance. However, GPS, UGI, WWD, and STNE all lowered their forward guidance.

So far this morning, JD and FL have both reported beats on the revenue and earnings lines. However, SPB reported misses on both the top and bottom lines.

Overnight, Asian markets were mixed on modest moves. New Zealand (+0.76%) was by far the largest gainer while Shanghai (-0.58%), Singapore (-0.42%), and Shenzhen (-0.37%) paced the losses. Meanwhile, in Europe, with the exception of Russia (-0.65%), the entire region is in the green at midday. The FTSE (+0.92%), DAX (+1.00%), and CAC (+1.20%) are leading a broad-based rally in early afternoon trade. As of 7:30 am, US Futures are pointing toward a green start to the day. The DIA implies a +0.56% open, the SPY is implying a +0.76% open, and the QQQ implies a +0.93% open at this hour. 10-year bond yields are moving higher at 3.799% and Oil (WTI) is off fractionally to $81.37/barrel.

The major economic news events scheduled for Friday, are limited to October Existing Home Sales are reported at 10 am. It is also important to note that today is Options Expiration Friday and Bloomberg reports we have $2 Trillion of options expiring today. The major earnings reports scheduled for the day are FL, JD, and SPB before the open. However, there are no major reports scheduled for after the close.

The retail industry continues to show strong earnings, implying that consumers (at least last quarter) had not yet rolled over into recession mode. However, hawkish Fed comments (especially from the most hawkish, Bullard) are telling markets not to get ahead of themselves. (Bullard implied that the end of hikes may not come until 2% higher than analysts and Fed futures have priced in. If that were to happen, it is not yet priced into markets.) So, once again, beauty and the market outlook is in the eye of the beholder. There is something to hang your hat on regardless of how you feel about market direction in the longer term.

However, in the short term, there is no question that the trend is bullish and we have seen a healthy pullback to rest in the upward move. All 3 major indices tested and held the T-line yesterday. So, extension is no problem at all (either in terms of the T-line or T2122). In addition, we held support levels in all 3 major indices. With this background, what we know for sure is that the probabilities in the near term lie in the Bull’s favor. With that said, continue to be cautious about chasing and remember it is Friday (time to get paid and “get ready for the weekend news cycle” day). This is also Options Expiration Friday, with Bloomberg reporting more than $2 Trillion in options ending at the close (really Saturday, but effectively at the close). So, we could always see some kind of price action where somebody tries to pin the price in or out of the money depending on their option position. Just be aware if there is a large open interest near price.

As always, be deliberate and disciplined…but don’t be stubborn. Remember it’s 100 times more important to avoid big mistakes than it is to pick big winners. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: no trade ideas today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

With some confusing and contradictory data on Wednesday morning, the dollar bounced, and bond yields rallied as thoughts of recession danced in traders’ minds. The QQQ, SPY, and IWM felt some selling pressure while the Dow chopped in a frustrating 160-point range. In a time when good economic numbers are bad and bad numbers are good, how we react to today’s housing, jobless, and manufacturing numbers is anyone’s guess. The one constant we can seem to count on is the price volatility so plan your risk carefully!

While we slept, Asian markets struggled to close the day primarily red. European markets waiting on U.K. budget details trade mixed but mostly lower this morning. Finally, after a mix of post-market earnings results, U.S. futures point to a lower open ahead of earnings and economic data that could quickly reverse or worsen the open. Be prepared for more big-point price whips and challenging price action as the market reacts to the data.

Economic Calendar

Earnings Calendar

We have about 40 companies on the Thursday calendar; however, many are small-cap names. Notable reports include BABA, AMAT, BJ, DOLE, FTCH, GPS, KSS, M, NTES, PANW, ROST, STNE, PLCE, UGI, VIPS, & WB.

News & Technicals’

Markets were buoyed last week after U.S. inflation came in below expectations for October, prompting investors to bet that Federal Reserve policymakers would soon have to slow or stop the monetary policy tightening measures they have deployed to bring down inflation. Though surging stocks suggest markets are reaffirming hopes of a soft landing from the Fed, BlackRock’s top strategists disagreed and remained underweight developed market stocks.

Amazon sent out “voluntary severance” offers to some employees this week as it looks for ways to rein costs beyond the announced massive layoffs. Employees have until Nov. 29 to agree to resign, and their last day of employment will be Dec. 23, according to documents viewed by CNBC. In addition, more than 100 unionized Starbucks locations plan to strike on one of the chain’s biggest sales days of the year, Red Cup Day. At the 113 striking locations, the union will be distributing its own version of the reusable red cup that features the Grinch’s hand holding an ornament with the logo of Starbucks Workers United. The action comes after contract negotiations between Starbucks Workers United and the company broke down.

Nvidia reported fiscal third-quarter results on Wednesday for the period ending in October, with sales beating analyst expectations but earnings per share coming in light. Analysts and investors closely watch Nvidia as a leading indicator for the health of the technology industry because it sells chips and software to many PC makers and cloud providers. Cisco reported fiscal first-quarter results on Wednesday that beat analysts’ estimates on the top and bottom lines. The company cited an “easing supply situation” and lifted its guidance for fiscal 2023. Revenue increased 6% from a year earlier.

With a mix of confusing and contradictory data, Wednesday morning bond yields rose, the dollar bounced, and Dow chopped sideways in a 160-point range. Though the QQQ, SPY, and IWM experienced some selling pressure, no technical damage occurred. However, a mix of earnings results after the bell, with Fed members remaining hawkish, has many thinking about recession with 4th quarter rally hopes diminishing. This morning we face housing data, Jobless Claims, Philly Fed numbers, and a parade of Fed speakers to keep traders guessing what comes next. While there is a lot of uncertainty about the path forward, there is one thing that seems inevitable, challenging price volatility.

Markets diverged a bit at the open Wednesday as QQQ gapped down 0.80%, SPY gapped down 0.40%, and DIA gapped down just 0.20%. From there, the SPY and QQQ ran sideways in waves within a not-too-large range below the open all day while the DIA did the same back and forth back across the prior close level all day. This action gave us smaller candles today, with the SPY and QQQ printing black-bodied Spinning Top candles while the DIA printed a white-bodied Inverted Hammer-type candle. This action relieved extension from the T-line (8ema) as well.

On the day, nine of ten sectors were in the red, with the Technology sector (-2.24%) leading the losses while the Utility sector (+0.47%) held up best. Meanwhile, the SPY lost 0.76%, the DIA gained 0.04%, and the QQQ lost 1.36%. The VXX fell 2,67% to 16.74 and T2122 dropped back into the mid-range at 67.57. 10-year bond yields fell down to 3.692% and Oil (WTI) fell 1.82% to $85.34 per barrel. So, overall Wednesday was a rest day where we saw a modest pullback in the bullish trend.

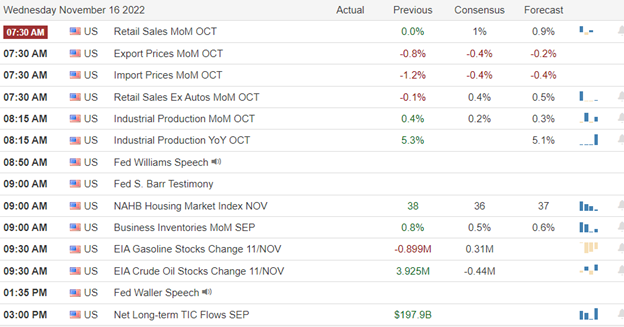

In economic news, October Import Price Index fell by 0.2% (compared to a drop of 0.4% that was forecast and the September drop of 1.1%). On the other side, October Export Price Index fell 0.3% (compared to a forecast drop of 0.4% and the September drop of 1.5%). Meanwhile, October Retail Sales grew by 1.3% (much more strongly than the forecast +1.0% and the September dead flat value at +0.0%). Later, October Industrial Production grew 3.28% showing some slowing compared to the September 4.96% growth. Elsewhere, September Business Inventories grew less than expected at +0.4% (compared to +0.5% forecasted and the August +0.9% growth). At the same time, September Retail Inventories fell 0.1% which was exactly what was forecasted and better than the August growth of 0.6%. Finally, EIA Weekly Crude Oil Inventories followed the API move by having a 5.400-million-barrel drawdown (compared to an expected 440k barrel drawdown and last week’s 3.925-million-barrel build in stocks).

In stock news, UAL said Wednesday that they expect the busiest travel day since the start of Covid-19 over the Thanksgiving weekend. They forecast a 12% increase in passengers over the holiday weekend compared to 2021. Meanwhile, COST says it has reached a deal with activist investors to cut its greenhouse emissions to new meet a new target by the end of next year. 70% of COST shareholders voted in favor of a resolution for COST to cut emissions back in January. At the same time, a Washington state court has ruled that the $4 billion dividend payment by ACI, scheduled to be paid today will remain on hold pending the close of the KR buyout. Reuters reports that regulators have said they received “good access” to Chinese firms’ financial records during their 7-week audit in Hong Kong. BABA and YUMC were among the 200 companies whose records were audited in hope of saving the US listings for those companies. Elsewhere, TSLA reported 2 new fatal car crashes involving their self-driving systems on Model 3 cars to the NHTSA Wednesday.

In miscellaneous news, despite constant talk of heavy inflation, Coffee prices have been collapsing recently, due in part to great weather in Brazil. Coffee futures fell from $239 at the end of August to $158 (per 237,000 pounds of beans) currently. This represents a 34% drop in 2.5 months. Elsewhere, three environmental groups sued the state of LA over its issuing of a permitting exemption to an LNG Terminal run by an unlisted firm. However, this terminal would impact several listed companies such as KMI, ATO, and XOM. Finally, in Fed news, San Francisco Fed President Daly said that “a pause is off the table” while Fed Governor Waller said the Fed “has a ways to go” on rate hikes and we will still need increases into next year (although he added that data is making him more comfortable with a 0.50% increase in December).

After the close, CSCO, BBWI, HP, and HI all beat on both the top and bottom lines. At the same time, NVDA and CPRT beat on revenue while missing on earnings. On the other side, CPA missed on revenue while beating on earnings.

So far this morning, BABA, SIEGY, M, KSS, BJ, NTES, and FORTY all posted beats on both the revenue and earnings lines. Meanwhile, DOLE, BV, and WB all missed on revenue while beating on earnings. On the other side, PLCE beat on revenue while missing on earnings. It’s worth noting that BJ and M both raised their forward guidance while KSS removed its forward guidance altogether, citing a volatile retail environment.

Overnight, Asian markets were mostly in the red on modest moves. South Korea (-1.39%) and Hong Kong (-1.15%) led the region lower while Singapore (+0.61%), Australia (+0.19%), and Malaysia (+0.06%) were the only three exchanges that managed to stay green. In Europe, exchanges are red across the board as of midday. The FTSE (-0.53%), DAX (-0.05%), and CAC (-0.71%) are typical of the region with a couple of the smaller exchanges managing to be down more than one percent in early afternoon trading. As of 7:30 am, US Futures are pointing toward a down start to the day. The DIA implies a -0.60% open, the SPY is implying a -0.67% open, and the QQQ implies a -0.63% open at this hour. 10-year bond yields are back up to 3.721% and Oil (WTI) is off 1.79% to $84.06/barrel in early trading.

The major economic news events scheduled for Thursday, we get October Building Permits, October Housing Starts, Weekly Initial Jobless Claims, and Philly Fed Mfg. Index (all at 8:30 am). We also have a few Fed speakers (Bullard at 8 am, Bowman at 9:15 am, and Mester at 9:40 am). The major earnings reports scheduled for the day are BABA, BJ, BV, DOLE, KSS, M, NTES, and WB before the open. Then, after the close, AMAT, FTCH, GPS, KEYS, PANW, POST, ROST, WSM and WWD report.

In economic news later this week, on Friday, October Existing Home Sales are reported. Meanwhile, in earnings reports later this week, on Friday, we hear from FL, JD, and SPB.

With retail earnings continuing to show strong consumers (last quarter) and some expectations (HD, LOW, WMT, M, BJ) for this quarter, and Hawkish Fed members telling the market not to expect a pause in rate hikes, we get ready for another day in the market. Traders seem cautiously pessimistic in the Premarket. At any rate, retail earnings have shown that there is a clear split between strong management teams (WMT, M, BJ, etc.) and the weak ones TGT (which was punished yesterday).

With this background, what we know for sure is that the trend is bullish continues and it looks like stocks are going to retest the T-line today in all 3 major indices. So, over-extension is no problem at all today. We are also now coming back down into a potential support level for the SPY, DIA, and QQQ. So, continue to be cautious if you are thinking of chasing a move (bearish or bullish).

Be deliberate and disciplined…but don’t be stubborn. Remember it’s 100 times more important to avoid big mistakes than it is to pick big winners. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to remember the “Legend of the man in the green bathrobe“…in that situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! And there is absolutely no reason to keep raising your bet (risk) just because you’ve had a win. Finally, keep in mind that trading is not a hobby. It’s a job. The money is real. So, you have to treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: VALE, CSCO, TLT, DIS, INTC, AAPL, EGHT, AFRM, NAIL, NTR. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

A smaller-than-expected rise in producer prices and geopolitical concerns served up another whipsaw day as the Dow shifted more than 600 points from high to low. The substantial overhead resistance and uncertainty of the market-moving economic reports we face this morning also played a role. Despite the volatility, the bulls remain in control, and although very dangerous to the trader, the huge point intraday swings have not technically damaged the index charts. However, plan carefully, as a busy day of earnings and economic reports could quickly produce another wild, emotionally driven ride today.

Asian markets closed mostly lower overnight. With U.K. inflation topping a 40-year high and the geopolitical tensions of the Poland missile strike, European markets are trading red across the board this morning. With a mix of early morning earnings results and the uncertainty of market-moving economic reports before the open, U.S. futures suggest a flat to slightly bearish open. However, anything is possible after the data is revealed, so plan carefully.

Economic Calendar

Earnings Calendar

On the Wednesday earnings calendar, we have nearly 30 companies confirmed, but many are non-market-moving small-cap names. Notable reports include CSCO, LOW, NVDA, BBWI, HP, KLIC, MANU, SONO, TGT, TJX, VSCO, & WSM.

News & Technicals’

Crypto.com CEO Kris Marszalek has taken to Twitter, YouTube, and the airwaves to reassure customers that their deposits are safe and the company is on solid footing. However, in the last few months, the company has reportedly cut over one-quarter of its staff, and concern has mounted since FTX’s collapse last week. “I understand that right now in the market, you’ve got a situation where everyone is done taking peoples’ word for anything,” Marszalek told CNBC on Tuesday.

Lowe’s reported third-quarter earnings Wednesday, beating analyst expectations. However, the home improvement retailer also lowered the top end of its full-year revenue guidance. Lowe’s reported results a day after rival Home Depot’s earnings topped expectations. In addition, Amazon has begun laying off employees in its corporate and tech workforce. CEO Andy Jassy has moved aggressively to cut costs across Amazon, and the company previously said it would freeze hiring in its corporate workforce.

Economists polled by Reuters had projected an annual increase in the consumer price index of 10.7%, and October’s print marks an increase from the 40-year high of 10.1% seen in September. “Indicative modeled consumer price inflation estimates suggest that the CPI rate would have last been higher in October 1981, where the estimate for the annual inflation rate was 11.2%,” the ONS said.

Tuesday served traders another whipsaw day, surging in the morning on a smaller-than-expected rise in PPI but pulling back by the close facing an uncertain Retail Sales report. Geopolitical-political concerns also played a role, with the Dow dangerously swinging more than 600 points from the day’s high to the low. Along with a busy economic calendar that will reveal the October retail numbers, we also have several big retailers fessing up to quarterly results. Index charts remain bullish; however quite dangerous due to the substantial point whips and the uncertainty of the path forward. I suspect with all the data coming our way today, wild price gyrations are likely to continue, so avoid overtrading and plan your risk carefully.

Markets gapped strongly higher at the open Tuesday (+1.50% in the SPY, +0.82% in the DIA, and a whopping +2.48% in the QQQ) after PPI and the NY Fed Mfg. Index both came in much better than expected (from a market perspective). From there, all 3 major indices waffled sideways in a fairly tight range until just before noon. At that point, a slow selloff took us slowly to the lows of the day (as of then) at about 1 pm. Then at 1:10 pm, 2 missiles (presumed Russian and likely intended for Ukraine) struck a Polish village a few kilometers inside Poland, killing 2 Polish civilians. Poland called an emergency National Security Council meeting to talk about their response. This caused a strong and immediate selloff across all 3 major indices as traders feared escalation of the war to involve NATO. This hard selloff recrossed the morning gap and reached the lows of the day by 2 pm when a bounce kicked in that regained about two-thirds of the losses seen in the afternoon by 3:30 pm and then ground sideways into the close.

On the day, this action is giving us gap-up, black-bodied Spinning Top type candles across all 3 major indices. (With a little larger body in the QQQ.) Nine of ten sectors were in the green, led by the Technology sector (+2.57%) while Communications Services (-0.73%) lagged. At the same time, the SPY gained 0.85%, the DIA gained 0.13%, and the QQQ gained 1.38%. The VXX rallied 1.3% to 17.20 and T2122 spiked back up into the overbought territory at 91.70. 10-year bond yields fell down to 3.777% and Oil (WTI) spiked 1.21% to $86.91 per barrel. So, overall Tuesday was a volatile day punctuated by premarket economic news (which is taken as good by the market under the assumption it will cause the Fed to ease up) and bad afternoon geopolitical news (which the market briefly took as bad under fear of war expanding in Europe).

In economic news, the NY Empire State Manufacturing Index came in at +4.50, which was significantly higher than the forecasted value of -5.00 and very much improved from the October reading of -9.10. This positive value indicates improving business conditions. At the same time, October PPI came in at +8.0% (year-on-year) which, like CPI last week, was well below the forecasted value of +8.3% and much better than the September reading of +8.4%. More importantly, the Core PPI (stripping out energy and food) was up just +6.7%, a full half percent below the forecast of +7.2% and much lower than the September value of +7.1%. Again, this indicates the growth of inflation is easing by a considerable amount, which led traders to believe the Fed may reduce the size of the rate hike it does in December. In the afternoon, the Fed reported that US Household Debt rose at the fastest pace in 15 years during Q3 (+$351 billion). This increase was mostly due to credit card usage and mortgage balances.

In energy news, TRP announced after the close that it has declared Force Majeure and will be required to reduce the volume of oil shipped through the Keystone pipeline (that ships oil to the Midwestern US) due to recent severe weather events. No details were given on the amount of the reduction or the duration of the slowdown. However, industry analysts said the reduction was about 7% of the normal 622,000 barrels per day volume. The API reported after the close that US oil inventories dropped much more than expected last week (a 5.8 million barrel drawdown, compared to a forecast 400k barrel drawdown). However, gasoline inventories rose by 1.7 million barrels and distillate stocks increased 850k barrels.

In stock news, activist investors TCI Fund publicly urged GOOGL to cut headcount to lower losses at the company’s Waymo self-driving unit after noting that this unit had increased headcount 20% per year since 2017. Elsewhere, AN announced Tuesday that it has acquired a 6.1% stake in automotive digital marketplace TRUE. Meanwhile, Jim Farley, CEO of F, said the company will need to bring much more work in-house (eliminating the need for many suppliers) in order to preserve jobs. The underlying problem for the F workforce is that it takes 40% less labor to build an electric vehicle and the underlying problem for F is that paying profit to suppliers reduces margins in comparison to TSLA (which makes most of its own parts). In regulatory news, the SEC has delayed its decision on whether to approve an Ark21 (spot Bitcoin) ETF until Jan. 27. In the late afternoon, Reuters reported that CG is in talks trying to form a partnership to acquire HPN for between $8-$10 billion. Finally, in legal news, INTC was hit with a $949 million judgment by a Texas court Tuesday for infringing the patents of Softbank subsidiary VLSI. Earlier in the day, it was reported that GS paid $12 million to a former partner over the charge of creating a “toxic workplace for women” including vulgar remarks by the CEO. The settlement took place two years ago but was hidden by a nondisclosure agreement.

In miscellaneous news, the New York Fed announced it is starting a 12-week pilot project for the “digital dollar.” The pilot will include participation by C, MA, and WFC among other financial institutions. Elsewhere, Consumer Reports ranked TSLA worst out of 24 brands of electric vehicles in terms of reliability in the US. In currency news, the missile strikes in Poland caused very volatile Forex trading Tuesday. The Euro was down dramatically against all pair partners and the USD swung wildly against the Yen and British Pound. Finally, in Supply Chain news, the Port of Los Angeles reports that October volumes at the busiest US seaport fell to the lowest level since 2009. The imports were down 28% from a year earlier and empty container handling fell more than 25% during the month.

After the close, AAP reported a beat on revenue while missing on earnings. The company also lowered its forward guidance. Meanwhile, GSM reported misses on both the top and bottom lines. So far this morning, LOW, ARCO, and ZIM have reported beats on both the revenue and earnings lines. Meanwhile, TGT beat on the revenue line while missing on earnings. On the other side, TJX missed on revenue while beating on earnings. It is worth noting that LOW raised its forward guidance and ZIM lowered its own forward guidance.

Overnight, Asian markets were mostly in the red on mostly modest moves while the second day of the G-20 summit continued in that region. Shenzhen (-1.02%), Thailand (-0.58%), and Hong Kong (-0.47%) led the way lower. Meanwhile, only Japan (+0.14%) and India (+0.03%) managed to hang on to green territory. In Europe, we see a very similar picture taking shape at midday. After it was decided the missiles in Poland were likely caused by Ukrainian Air Defense misses (trying to shoot down Russian missile attacks), things have settled a bit. The FTSE (-0.03%), DAX (-0.95%), and CAC (-0.48%) are typical of the region. However, a couple of the smaller exchanges are down more than 1% in early afternoon trade. As of 7:30 am, US Futures are now pointing toward an open just on the red side of flat. The DIA implies a -0.08% open, the SPY is implying a -0.11% open, and the QQQ implies a -0.19% open at this hour. At the same time, 10-year bond yields are down to 3.768% and Oil (WTI) is off just a fraction at $86.77/barrel in early trading.

The major economic news events scheduled for Wednesday include October Retail Sales and October Import/Export Price Indexes (both at 8:30 am), October Industrial Production (9:15 am), September Business Inventories and Sept. Retail Inventories (both at 10 am), and EIA Weekly Crude Oil Inventories (10:30 am). We also have a Fed speaker (Williams at 9:50 am). The major earnings reports scheduled for the day are ARCO, LOW, TGT, TCEHY, TJX, and ZIM before the open. Then, after the close, BBWI, CSCO, CPA, HP, HI, NVDA, and SONO report.

In economic news later this week, on Thursday, we get October Building Permits, October Housing Starts, Weekly Initial Jobless Claims, and Philly Fed Mfg. Index. Finally, on Friday, October Existing Home Sales are reported.

In earnings reports later this week, on Thursday, we hear from BABA, BJ, BV, DOLE, KSS, M, NTES, WB, AMAT, FTCH, GPS, KEYS, PANW, POST, ROST, WSM, and WWD report. Finally, Friday, we hear from FL, JD, and SPB.

With yesterday afternoon’s immediate threat (expanding war in Europe) mostly lessened, US markets turn back toward earnings and the economy. This morning, TGT warned it sees a weak holiday coming this year, but this is likely due to it having large inventories that will need to be discounted heavily in order to be sold. On the other hand, just like competitor HD, LOW raised its Q4 guidance saying that it expects a strong Q4. (Maybe more of Santa’s gifts are coming from the hardware store this year.) Also, yesterday we saw more evidence that inflation may be slowing (which could mean the pace of hikes by the Fed also eases up…and the market would love that). At any rate, tensions have eased a bit and retail earnings up to this moment are mixed at worst.

With this background, what we know for sure is that the trend is bullish and yesterday’s pullback did not break the recent range, let alone the trend. However, it did lessen extension from the T-line (8ema) just a bit. We also know that price moves in a lightning bolt, zig-zag pattern. And, once again, our zig is still in need of a zag if we are going to sustain a bullish move higher. Can Mr. Market overcome that need, sure…but only in the short-term. So, even if the bulls rule the day, don’t expect this to be a vertical rally. Normal rallies need pullbacks and there are also a lot of bears out there that still believe Q1 and Q2 will be terrible and the market should fall more to account for this fact. In addition, we still have more retail name (lesser ones) reports coming later this week. So, caution is still warranted, but so far it is looking like the consumer may still hold up (at least through year-end).

So, continue to be deliberate and disciplined…but don’t be stubborn. Remember it’s 100 times more important to avoid big mistakes than it is to pick big winners. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to remember the “Legend of the man in the green bathrobe“…in that situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! And there is absolutely no reason to keep raising your bet (risk) just because you’ve had a win. Finally, keep in mind that trading is not a hobby. It’s a job. The money is real. So, you have to treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: PLUG, EL, GOLD, META, SBLK, VALE, and GFI. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

During the morning session on Monday, the bulls tried pushing higher, but the uncertainty of the PPI report inspired the profit-takers to reduce risk heading into the close. As a result, the indexes whipsawed, leaving behind shooting star patterns near price resistance levels but creating no technical damage to the charts. However, big-name earnings reports from HD and WMT and the reaction to the producer prices will likely create significant pre-market volatility. Unfortunately, we’ve yet to discover that it will inspire the bulls or the bears!

While we slept, Asian markets mostly rallied despite disappointing Chinese activity data as Hong King surged 4.11%. However, European markets are taking a more cautious stance this morning, trading flat as they wait on inflation data. On the other hand, U.S. futures push for a bullish open in the pre-market pump ahead of the producer price numbers that will likely set the tone for the day.

Economic Calendar

Earnings Calendar

We have about 20 companies confirmed on the Tuesday earnings calendar. Notable reports include HD, WMT, ARMK, AAP, ENR, AQUA, HUYA, DNUT, SE, & TME.

News & Technicals’

Americans grew more worried about inflation in October, with fears emanating primarily from an expected burst in gasoline prices. A New York Fed survey showed inflation expectations for the year ahead rose to 5.9%, while the three-year outlook increased to 3.1%. Home prices were expected to rise by 2%, tied for the lowest since June 2020. Home Depot reported third-quarter earnings on Tuesday, beating analyst expectations. The retailer reported revenue increased by nearly 6% to $38.87 billion. Wall Street is watching how rising costs and other macroeconomic headwinds affect the retailer.

Last week, when it filed for Chapter 11 bankruptcy protection, FTX indicated that it had more than 100,000 creditors. But in an updated filing Tuesday, lawyers for the company said: “In fact, there could be more than one million creditors in these Chapter 11 Cases.” In addition, over the past 72 hours, the lawyers wrote that FTX has been in contact with “dozens” of regulators in the U.S. and overseas.

At the 2022 Web Summit tech conference, startup founders and investors warned fellow entrepreneurs it was time to rein in costs and focus on fundamentals. “The multiples last year are not the same as this year,” said Guillaume Pousaz, CEO of London-based payments firm Checkout.com. Instead, multibillion-dollar unicorn companies will collapse in “spectacular failures,” Par-Jorgen Parson, partner at venture capital firm Northzone, told CNBC.

Monday’s price action tried to put on a brave face early in the day, but the uncertainty of the PPI report brought out the profit takers. Although the Dow swung more than 400 points from high to low, leaving behind shooting star patterns on all the index charts. That said, the move showed respect for overhead resistance, index charts suffered no technical damage despite the volatility. How things go from here will depend on the reaction to the PPI report and the earnings results from WMT and HD. We should plan for substantial pre-market gyrations; the results likely set the day’s tone. Will it be the bulls or the bears that find inspiration? Buckle up; we are about to find out!

Stocks gapped down modestly on Monday (-0.69% in the QQQ, -0.45% in the SPY, and -0.31% in the DIA). The three major indices rollercoastered their way sideways until about 12:30 pm. At that point, all 3 of those indices rallied up above the gap to new highs of the day at 2 pm. Then a slow, protracted selloff took us back down to Friday’s close by 2:45 pm before accelerating into a hard selloff the last 30 minutes. This took us out to a close very near the lows of the day. This action gave us black-bodied candles with long upper wicks and small lower wicks. (In other words, black Inverted Hammer candles in the DIA, SPY, and QQQ.) It is worth noting that all 3 major indices are still extended above their T-line (8ema), especially the QQQ and SPY.

On the day, all ten sectors were red after the late selloff with the Financial Services sector (-1.28%) leading the losses and Communications Services (-0.17%) holding up best. Meanwhile, the SPY lost 0.78%, the DIA lost 0.60%, and the QQQ lost 0.88%. The VXX rallied to close dead flat at 16.98 and T2122 dropped and fell just outside the overbought territory at 77.88. 10-year bond yields rose a bit to 3.874% and Oil (WTI) plunged 4.22% to $85.21 per barrel. So, all-in-all, Monday was a pause day that ended up with very modest pullbacks across the market.

In Fed news, Fed Vice-Chair Brainard gave us a study in contradiction Monday when she said that she “thinks it will probably be appropriate soon to move to a slower pace of (rate) increases.” However, later in the speech, she said “Inflation is very high in the United States and abroad” and “Monetary policy will need to be restrictive for some time to have confidence that inflation is moving back to target…For these reasons, we are committed to avoiding pulling back prematurely.” In other words, there was a little something for both sides of the debate and the listener will interpret her words to support the position they held before she started talking.

In stock news, Reuters reported Monday that AMZN is planning to lay off 10,000 employees from corporate and technology positions. Elsewhere, Investing.com reports that VLKAF (Volkswagen) has reached its goal of delivering 500k electric vehicles more than a year earlier than they had forecast. (For reference, TSLA, the leader in electric cars, has delivered 3.2 million cars total since 2015.) After the close, Reuters reported that FDX (specifically the freight division) is furloughing an unspecified number of employees due to business conditions that are hurting shipping volumes. In addition, ILMN announced after hours that it is cutting 5% of its global workforce. At the same time, activist investor Ancora Holdings said Monday that it will fight the sale of IAA (in which Anchora holds a 4% stake) to RBA for $7.3 billion (which was a 19% premium on the IAA price at the time of the deal). Ancora claimed it was a poorly structured deal that resulted from a weak sale process that was not in the best interest of the shareholders. Finally, GOOGL paid nearly $400 million to settle the allegations brought by 40 states that the tech giant illegally tracked users’ locations back in 2014 (action brought in 2018).

In BRKB (Warren Buffet) news, Monday filings of 13F documents show that Berkshire has taken a 60 million share position in TSM. They also took a 5.75 million share in LPX and a 434k position in JEF. In the oil industry, Berkshire added to its holdings of both CVX and OXY. Among other big names, BRKB maintained its holdings in AAPL ($133 billion) and BAC ($38 billion). Finally, Berkshire increased its holdings of PARA by 13 million shares. All the stocks in which a new Berkshire position was announced were trading higher in the post-market session.

In energy news, Reuters reports that CVX is sending crews to cap old wells that are leaking methane and other gases. This action is ahead of new regulations coming in CO after voters set limits on unused wells. CVX estimates it will cost between $80k and $100k per well to cap each of the 500 wells in that state, each of which produces as much emissions as 22,000 cars each year. Elsewhere, on Monday afternoon, executives at DUK and AEP told Bloomberg that they see the recently passed “Inflation Reduction Act” as significantly reducing their customer’s energy bills. They went on to say that the law will shift the majority of those savings onto the top 1% of taxpayers. However, they had not fully analyzed the dollar value of potential savings of their customers.

So far this morning, MT, BAM, AZN, USFD, RWEOY, BDX, NIO, DDS, TDG, KELYA, SBH, SLVM, and NICE all posted beats on both the revenue and earnings lines. At the same time, AEG, WRK, TPR, EPC, and EYE all missed on revenue while beating on the earnings line. On the other side, PRMW beat on revenue while missing on earnings. Unfortunately, WE and SIX missed on both the top and bottom lines. It is worth noting that USFD and PRMW raised their forward guidance. However, BDX, NIO, TPR, SBH, WE, and YETI all lowered their forward guidance.

Overnight, Asian markets leaned heavily to the upside. Hong Kong (+4.11%), Taiwan (+2.64%), and Shenzhen (+2.14%) led the region higher as tech stocks soared on the optimism caused by the Biden-Xi talks and joint statements (and despite Chinese Industrial Production and Retail Sales data disappointing). Meanwhile, in Europe, stocks are much more mixed and even lean to the red side at midday. The FTSE (-0.03%), DAX (-0.05%), and CAC (+0.31%) lead the region showing more red than green in early afternoon trading. However, as of 7:30 am, US Futures are pointing toward a gap higher to start the day. The DIA implies a +0.33% open, the SPY is implying a +0.70% open, and the QQQ implies a +1.12% open at this hour. 10-year bond yields are back down to 3.812% and Oil (WTI) is off seven-tenths of a percent to $85.27/barrel in early trading.

The major economic news events scheduled for Tuesday include October PPI and NY Empire State Mfg. Index (both at 8:30 am), and API Weekly Crude Oil Stocks report (4:30 pm). The major earnings reports scheduled for the day are ARMK, BERY, ENR, AQUA, HD, SE, TME, VVV, and WMT before the open. Then, after the close, AAP and GSM report.

In economic news later this week, on Wednesday, October Retail Sales, October Import/Export Price Indexes, October Industrial Production, September Business Inventories, EIA Weekly Crude Oil Inventories, and a Fed speaker (Williams) report. On Thursday, we get October Building Permits, October Housing Starts, Weekly Initial Jobless Claims, and Philly Fed Mfg. Index. Finally, on Friday, October Existing Home Sales are reported.

Inearnings reports later this week, on Wednesday, ARCO, LOW, TGT, TCEHY, TJX, ZIM, BBWI, CSCO, CPA, HP, HI, NVDA, and SONO report. Then on Thursday, we hear from BABA, BJ, BV, DOLE, KSS, M, NTES, WB, AMAT, FTCH, GPS, KEYS, PANW, POST, ROST, WSM, and WWD report. Finally, Friday, we hear from FL, JD, and SPB.

So far this morning, WMT, HD, SE, TME, VVV, ENR, and AQUA all posted beats on both the top and bottom lines. (WMT and HD in particular posted significant beats on both revenue and earnings.) Meanwhile, ARMK beat on revenue while missing on earnings. It is also worth noting that WMT raised its forward guidance.

With that background, premarkets are very bullish, in part because WMT says sales are stronger than expected and its inventory glut has been significantly reduced. Between this and the HD revenue beat, traders seem to be reading through that the consumer is in much better shape than the bears had been suggesting. Still, we do have the PPI data at 8:30 am, and while it tends to follow in line with the CPI data, there is still a chance that we get a premarket shock later this morning. Be careful chasing any bullish moves. We know that price moves in a lightning bolt, zig-zag pattern. And, once again, at the moment, our zig is in need of a zag if this is going to be a sustained move higher. Can good news overcome the need, sure…but only in the short-term. So, even if the bulls rule the day, don’t expect this to be a vertical rally. In addition, we have more big retail names coming up later this week. There is no guarantee they will have had the same results that WMT and HD had last quarter. Finally, remember that we get another read on the US consumer this week as the big retail names all report.

So, continue to be deliberate and disciplined…but don’t be stubborn. Remember it’s 100 times more important to avoid big mistakes than it is to pick big winners. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to remember the “Legend of the man in the green bathrobe“…in that situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! And there is absolutely no reason to keep raising your bet (risk) just because you’ve had a win. Finally, keep in mind that trading is not a hobby. It’s a job. The money is real. So, you have to treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: IGT, TWOU, ELF, VRT, ANET, KGC, HZNP, GOLD. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service