Tariff Pause Rethink, Earnings, and JOLTS Today

The market was volatile Monday, seemingly over-reacting to Trump’s tariffs and then bouncing hard (perhaps in an over-reaction to Trump calls with Mexico and Canada and pushing back Mexican tariffs a month). SPY gapped down 1.51%, DIA gapped down 1.28%, and QQQ gapped down 1.76%. All three major index ETFs did a momentary bound and then followed through to the downside, reaching the lows of the day at 10:20a.m. At that point, all three spiked hard to the upside for about 20-25 minutes before starting a sideways chop with a slight bullish trend. That slight bullish trend lasted until 3 p.m. when we saw a modest selloff across SPY, DIA, and QQQ the last hour. This action gave us huge gap-down white-body candles with significant wicks on both ends of the candles. All three gapped below their T-line (8ema) with only DIA retesting from below and failing its retest. SPY and QQQ also gapped down below their 50sma, retested from below and closed just above and below that level respectively.

On the day, six of the 10 of the sectors were in the red with Consumer Cyclical (-1.29%), Industrials (-1.23%), and Technology (-1.18%) out front leading the market lower. On the other side, Communications Services (+0.46%) held up better than the other sectors. At the same time, SPY lost 0.67%, DIA lost 0.25%, and QQQ lost 0.80%. Meanwhile VXX gained another 2.15% to close at 45.07 while T2122 dropped all the way back into the top of its oversold range to close at 18.52. On the bond side, 10-Year Bond yields closed at 4.563% and Oil (WTI) gained 0.32% to close at $72.76 per barrel. So, Monday was all about market reaction to Trump’s tariffs and then talks and pushing them off temporarily. This all happened on above-average volume in SPY, DIA, and QQQ.

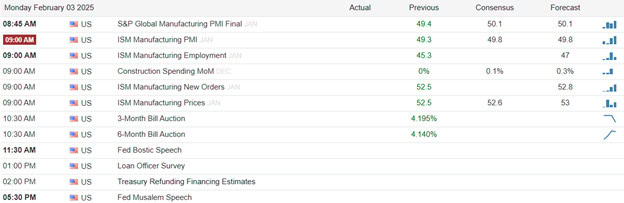

The major economic news on Monday includes S&P Global Mfg. PMI came in higher than expected at 51.2 (compared to a 50.1 forecast and a December 49.4 reading). A few minutes later, Dec. Construction Spending also came in stronger than predicted at +0.5% (versus a +0.3% forecast and November’s +0.2%). At the same time, ISM Mfg. PMI was strong at 50.9 (compared to a 49.3 forecast and the December 49.2 value). On jobs, ISM Mfg. Employment were up strongly to 50.3 (versus a 47.8 forecast and a 45.4 December reading). In terms of prices, the ISM Mfg. Price Index were also up to 54.9 (compared to a 52.6 forecast and December’s 52.5 value).

In Fed news, on Monday Atlanta Fed President Bostic said the FOMC may need to wait “for a while” on any further rate cuts as the new Administration’s policies make the economic outlook much less certain. Bostic said, “I want to be cautious and I don’t want to have our policy lean in one direction based on an assumption the economy is going to evolve a certain way, then have to turn it around.” He also cited waiting on seeing what impact 2024’s (one percent) cut will have, saying, “I want to see what the reduction that we did at the end of last year translates to in terms of the economy, and it could—depending on what the data are—mean that we are waiting for a while.” Elsewhere, Boston Fed President Collins told CNBC, “The kind of broad-based tariffs that were announced over the weekend, one would expect to have an impact on prices … with broad-based tariffs, you actually would not only see increases in prices of final goods, but also a number of intermediate goods.” However, she went on to point out that there isn’t a lot of experience with broad-based tariffs in the modern economy (because administrations from both parties have realized they don’t work and are both a tax on US citizens and inflationary for at least 85 years). Both emphasized with the unpredictable and unstable policy approach of the Trump administration, the extent of the inflationary impact is unknowable until we learn how tariff implementation, US competitor pricing response, and counter-tariff responses play out.

After the close, ACM, BRBR, CLX, EQR, FN, NXPI, PLTR, and DOC reported beats on both the revenue and earnings lines. Meanwhile, EG beat on revenue while missing on earnings. On the other side, KD and WWD missed on revenue while beating on earnings. However, CBT missed on both the top and bottom lines.

Overnight, Asian markets were mixed with half the exchanges green and half red. Hong Kong (+2.83%) and India (+1.62%) paced the gains while Shenzhen (-1.33%) was by far the biggest loser. In Europe, we a similar picture taking shape at midday but slightly more of the bourses lean toward the red side. The CAC (+0.22%), DAX (-0.04%, and FTSE (-0.12%) lead the region on volume in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a mixed, flat open after Trump back-tracked on tariffs for both Mexico and Canada and announced he will hold a similar call with China’s President Xi. The DIA implies a -0.18% open, the SPY is implying a dead flat open, and the QQQ implies a +0.21% open at this hour. At the same time, 10-Year Bond yields are back up to 4.577% and Oil (WTI) has dropped 2.17% to $71.57 per barrel in early trading.

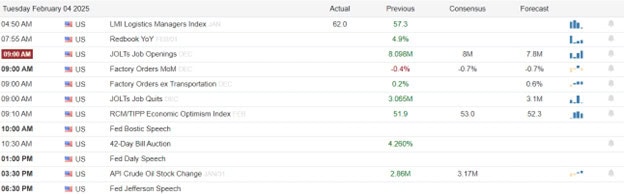

The major economic news scheduled for Tuesday are limited to Dec. Factory Orders and Dec. JOLTs Job Openings (both at 10 a.m.), and the API Weekly Crude Stocks Report (4:30 p.m.) and we hear from Fed members Bostic (11 a.m.) and Daly (1:15 p.m.). The major earnings reports scheduled for before the open include AMCR, AME, APO, ARMK, ADM, ATI, ATKR, AXTA, BALL, BERY, CNC, CNH, CMI, ENR, EPD, EL, RACE, FOXA, IT, GPK, HUBB. INGR, J, KKR, LANC, MPC, MRK, MPLX, PYPL, PNR, PEP, PFE, REGN, SPOT, TDG, UBS, WEC, WTW, and XYL. Then after the close, AMD, ALGT, GOOGL, DOX, AFG, AMGN, ATO, CSL, CRUS, COLM, DXC, EA, ENVA, FMC, GOOG, THG, JKHY, JNPR, LUMN, MTCH, MAT, MOD, MDLZ, NOV, OI, OMC, OSCR, PRU, SPG, SKY, SNAP, UNM, and WU report.

In economic news later this week, on Wednesday, ADP Nonfarm Employment Change, Dec. Exports, Dec. Imports, Dec. Trade Balance, S&P Global Services PMI, S&P Global Composite PMI, ISM Non-Mfg. PMI, ISM Non-Mfg. Price Index, EIA Weekly Crude Oil Inventories are reported and we hear from Fed member Bowman. On Thursday, we get Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, Preliminary Q4 Nonfarm Productivity, Preliminary Q4 Unit Labor Costs, Fed Balance Sheet, and we hear from Fed members Waller and Daly. Finally, Friday, Jan. Avg. Hourly Earnings, Jan. Nonfarm Payrolls, Jan. Private Nonfarm Payrolls, Jan. Participations Rate, Jan. Unemployment Rate, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-Year Inflation Expectations, Michigan 5-Year Inflation Expectations, and Dec. Consumer Credit are reported.

In terms of earnings reports later this week, Wednesday, ARCC, ARES, BSX, BG, CPRI, CDW, COR, EMR, EQNR, EVR, FSV, FI, GSK, GFF, HOG, IEX, ITW, JCI, NYT, NVO, ODFL, PFGC, REYN, RXO, SR, SWK, TROW, TKR, TM, UBER, VSH, DIS, AFL, ALGN, ALL, ARM, ASGN, AVB, EQH, BV, CENT, CTSH, COHR, CPAY, CTVA, CCK, DLX, ENS, ENSG, NVST, PLUS, F, GL, HI, HOLX, ITUB, KMPR, MCK, MET, MAA, MOH, MUSA, NWSA, ORLY, CNXN, PTC, QGEN, QCOM, RRX, SWKS, STE, SNEX, SU, TTMI, UHAL, UGI, VLTO, WFRD, and WEX report. On Thursday, we hear from WMS, AGCO, APD, AB, APTV, MT, ARW, AZN, BCE, BDX, BDC, OWL, BWA, BMY, CX, CMS, CIGI, COP, DAR, LLY, ENTG, EFX, GTES, HP, HSY, HLT, HON, HII, NSIT, ICE, IQV, ITT, K, KVUE, LH, LEA, LNC, LIN, MKL, MMS, MDU, NVT, PATK, PTEN, BTU, PTON, PM, RL, RITM, RBLX, SNA, SPB, TPR, TEX, TRI, UAA, WMG, XEL, XPO, YUM, YUMC, ZBH, AMRK, AFRM, AMZN, ATR, BYD, CNO, EHC, EXPE, LION, FTNT, FBIN, G, HUBG, ILMN, MTD, MCHP, MTX, MHK, MPWR, NBIX, OTEX, PINS, POST, PFG, RGA, SKX, SONO, SSNC, TTWO, VSAT, and WERN. Finally, on Friday, AVTR, CBOE, ROAD, FLO, FTV, ULCC, GPRE, KIM, NWL, PAA, PAGP report.

So far this morning, APO, AXTA, CNC, ENR, EL, IT, INGR, J, KKR, MPC, MRK, PYPL, PNR, PFE, PJT, REGN, TDG, UBS, and XYL all reported beats on both the revenue and earnings lines. Meanwhile, AMCR, AME, ARMK, ATKR, BALL, EPD, MPLX, PEP, and WTW all missed on revenue while beating on earnings. On the other side, SPOT beat on revenue while missing on earnings. However, CNH, GPK, and WEC missed on both the top and bottom lines.

With that background, it looks like the market is rethinking the tariff selloff and rebound. All three major index ETFs are more flat this morning, printing smaller premarket candles and reversing their initial early session move. DIA is just below and looking to retest its T-line while QQQ did retest and then backed off. As a result, all three remain below their 8ema. So, the short-term trend remains bearish. The mid-term downtrend (if you want to call it a trend) remains a mess. In terms of extension, as mentioned, all three are back close below their T-line. Meanwhile, T2122 is just inside of its oversold territory. So, both sides have room to work today if they can find momentum, but the Bulls may have a little more slack to work with today. In terms of the Big Dogs, nine of the 10 are in the green with AMA (+1.38%) out in front leading the pack higher. On the other side, AAPL (-0.42%) is the laggard and only one of the 10 in the red. As far as liquidity goes, TSLA (+0.44%) and NVDA (+0.38%) are neck-and-neck and both have traded about 4.5 times as much as the next most liquid ticker. However, take note that it is a very light premarket volume overall.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service