Tuesday proved to be a day of frustrating low-volume chop as the market waited for NFLX earnings after GS dampened early bullishness missing expectations. Bond yields rose yesterday and look to extend higher this morning with the U.K. reporting a 10.1% inflation rate above estimates. Today we have a light day on the economic calendar but we ramp up the earnings data with MS this morning and TSLA this afternoon we should expect another day of challenging price action.

Asian markets finished the day mixed but mainly lower worried about rate hikes and possible recession. The surprise U.K. inflation rate and uncertainty of the Fed’s next rate decision have European markets seeing red across all indexes this morning. As investors digest earnings miss from GS and NFLX, the U.S. point to bearish open as we ramp up the number of reports with confidence in the results slightly fading. Be watchful for big-point intraday whipsaw or full-on reversals as traders react to the data.

According to the Office for National Statistics, the consumer price index rose by an annual 10.1% in March 2023 in the UK. This is above a consensus projection of 9.8% in a Reuters poll of economists. The inflation rate remained in double digits as households continued to grapple with soaring food and energy bills. This is a slight dip from the unexpected jump to 10.4% in February, which broke three consecutive months of declines since October’s 41-year high of 11.1%.

Netflix released its first-quarter 2023 financial results on April 18th, 2023. The company outperformed expectations for the first quarter financial results, delivering a 16% positive surprise in earnings per share ($0.94 vs. $0.80 anticipated) and a 5% positive surprise in revenues ($26.39 billion vs. $25.19 billion). Netflix said it was pushing back the broad rollout of its password-sharing crackdown. Originally, Netflix wanted the rollout to take place late in the first quarter, but on Tuesday it said it would do it in the second quarter. The company said it saw its subscriber growth impacted in the international markets where it has already rolled out such initiatives.

On Wednesday, U.S. Treasury yields climbed after another sticky inflation report in the U.K. raised concerns global central banks would need to stay the course with their tightening campaigns. The yield on the 10-year Treasury was up by over 6 basis points to .63%. The yield on the 2-year Treasury was last trading at 4.28% after rising by 8 basis points.

Equity markets were mixed on Tuesday, as the S&P 500 closed higher after a frustrating day of low-volume chop. Forecasts still call for -6.5% earnings growth year-over-year in the first quarter. The S&P 500 overall is up about 8.0% in 2023, still driven largely by growth sectors like technology and communication services. More recently, we have seen better performance from defensive sectors, like consumer staples and health care, and cyclical sectors, including energy and materials. This comes as Treasury yields have moved higher, with the 2-year U.S. Treasury yield up by nearly 0.46% since its recent lows to 4.22% 1. The VIX volatility index has also moved lower, down about 9% in April thus far. Index technicals remain bullish but once again over-extended according to the T2122 indicator.

Markets opened flat and ground sideways for the first hour in all three major indices. The bears then stepped in to drive a modest selloff that lasted until 12:30 pm. At that point, again all three major indices ground sideways along the lows. However, at about 2 pm, markets began a rally (slightly stronger than the morning selloff) which continued all the way into the close. This action gave us white-bodied candles with lower wicks and also inside day candles. You might even say the QQQ printed a Hammer that also retested its T-line. So, all three major indices remain in a bullish average stack (3ema > 8ema > 17ema > 50sma > 200sma).

On the day, nine of the 10 sectors were in the green with Financial Services (+0.77%) leading the way higher while Energy (-0.83%) lagged behind the other sectors. At the same time, the SPY gained 0.36%, DIA gained 0.32%, and QQQ gained 0.08%. VXX fell 2.73% to 39.50 and T2122 climbed back into the overbought territory to 90.22. 10-year bond yields continued to shoot higher to close at 3.602% while Oil (WTI) lost 1.85% to $80.99 per barrel. So, Monday was sort of a meandering day that saw price drift lower in the morning and higher in the afternoon but all within a fairly tight range (inside Friday’s candles in all three major indices).

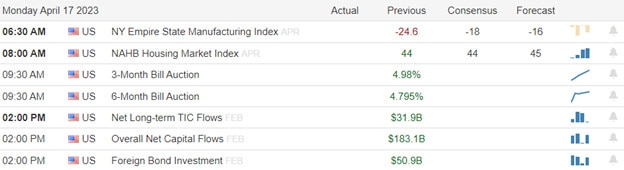

In economic news, on Monday NY Fed’s Empire State Manufacturing Index came in far above expectation at 10.80. This is compared to a forecast of -18.00 and the March reading of -24.60. The 10.80 was the strongest reading since July of 2022. Meanwhile, in political news, US House Speaker McCarthy traveled to Wall Street Monday to pitch the same idea that he has proposed for months. Namely, the GOP will pass a one-year debt ceiling increase (paying debts already incurred, money already spent), in exchange for Democrats and the President agreeing to cut spending back to 2022 levels, reversing some of President Biden’s policies, and then only increasing spending a maximum of 1% per year going forward. The proposal continues to be a non-starter for Democrats and would also require significant cuts to everything else in the budget unless McCarthy’s fellow Republican, Senate Minority Leader McConnell, gives up his (and others) proposed Defense spending increases (which added $118 billion to President Biden’s last Defense budget request of $740 billion). So, the US default versus Debt Ceiling increase (and whatever else rides along with that passage) debate is not likely to get serious until May when pressure builds. This will give financial news more fodder to discuss the implications of a US default on its debt.

In stock news, LLY announced it will invest $1.6 billion in two Indiana manufacturing plants in order to support the production of its recently approved cancer drug Jaypirca. At the same time, TSLA got bad public relations buzz after the company cut the bonuses of 20,000 employees at its Shanghai factory over the weekend. As a result, employees took to social media to ask the Chinese people to rally behind them and to ask TSLA CEO Elon Musk to override the decision. (These are the same workers he praised in tweets last year for “burning the 3 am oil” to keep operations running during the city’s COVID-19 lockdown.) In other auto-industry news, RNLSY (Renault) announced it is reviewing prices worldwide for its electric vehicles after the latest round of price cuts by TSLA. Elsewhere, PCRFY (Panasonic), which supplies batteries to TSLA, said Sunday that it is considering building a battery plant in Oklahoma after the state passed laws to allow the Governor to offer the company more incentives to do so. Meanwhile, MRK announced a deal to acquire RXDX for $200/share. After the close, it was reported Samsung (SSNLF) is considering replacing GOOGL’s Google with MSFT’s Bing as the default search engine for its phones and tablets. This would be a significant hit to GOOGL’s search ad business.

In stock legal and regulatory news, ILMN settled a patent infringement suit (related to genetic testing patents) brought against it by Ravgen Inc. The settlement details were not disclosed. Elsewhere, the $1.6 billion defamation lawsuit brought against FOX for allegedly defaming Dominion Voting Systems was delayed one day. It is widely believed this delay was to allow FOX to seek settlement terms from Dominion (which has already been granted summary judgment on the facts that FOX knowingly and purposefully published lies about Dominion and that those lies caused Dominion harm). In related news, Reuters reported after the close that a group of FOX investors has now demanded company files and part of the Dominion case discovery as they consider filing suit against FOX directors and executives for the damage they have suffered as a result of the company’s false narrative and fraudulent reporting (and presumably any settlement or judgments) have or will have on their stock value. Meanwhile, the US Treasury Department announced Monday that VLKAF (Volkswagen), BMWYY (BMW), NSANY (Nissan), RIVN, HYMTF (Hyundai) and VLVLY (Volvo) electric vehicles would lose access to a $7.500 tax credit. TSLA Model 3 vehicles will see their eligibility cut to $3,750 while other TSLA models retain the full $7.500 credit. Most F and STLA electric vehicles will also see their tax credit cut to $3,750. GM Bolt, Bolt EUV, Cadillac Lyriq, Chevy Equinox EV and Blazer EV will all still qualify for the $7.500 tax credit. Over at the US Supreme Court, justices declined to hear a GM appeal seeking to revive a racketeering lawsuit against STLA (or more precisely its Fiat division). In other Supreme Court news, the justices did hear an appeal by WORK (owned by CRM now) seeking to have a shareholder lawsuit dismissed. The case accuses WORK of misleading statements prior to the “self-listing” when WORK was offered. At the same time, the SEC filed charges against another cryptocurrency exchange (Bittrex) for operating an unregistered securities exchange. After hours, nine more US states joined the US Dept. of Justice lawsuit against GOOGL that alleges the company broke antitrust law with its digital advertising business (by abusing its dominance).

In banking news, Bloomberg reported that WFC execs are privately concerned that efforts to unionize its bank employees will soon result in union victories. However, the executives say they have plans to spend millions of dollars to address employee “pain points” and defeat organizing efforts. Elsewhere, a report showed that the average regional bank has reported only a 3% reduction in deposits since before the “banking crisis” began. However, there are exceptions, such as SCHW which saw an 11% reduction in deposits. Meanwhile, AAPL has announced a high-yield 4.15% savings account (via partner GS) for users of its Apple Card as it seeks to draw users away from traditional banks.

Overnight, Asian markets leaned heavily to the red side. Only Japan (+0.51%), Shanghai (+0.23%), and Shenzhen (+0.04%) managed any green. Meanwhile, Hong Kong (-0.63%), Taiwan (-0.59%), and New Zealand (-0.44%) led the rest of the region lower. In Europe, the mirror image of Asia is taking shape at midday. Only Russia (-0.21%) and Spain (-0.24%) are in the red. Meanwhile, the CAC (+0.67%), DAX (+0.64%), and FTSE (+0.21%) lead the rest of the region higher in early afternoon trade. In the US, as of 7:30 am, Futures are pointing toward a green start to the day. The DIA implies a +0.39% open, the SPY is implying a +0.41% open, and the QQQ implies a +0.63% open at this hour. At the same time, 10-year bond yields are back down to 3.577% and Oil (WTI) is off 0.20% to $80.69/barrel.

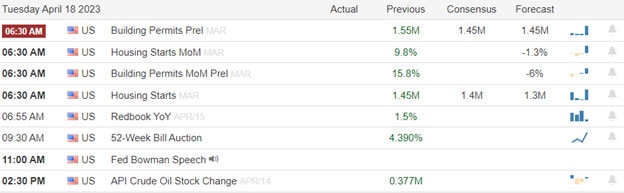

The major economic news events scheduled for Tuesday are limited to March Building Permits and March Housing Starts (both at 8:30 am) and API Weekly Crude Oil Stock Report (4:30 pm) and Fed member Bowman speaks at 1 pm. The major earnings reports scheduled for the day include BAC, BK, ERIC, GS, JNJ, LMT, and PLD before the open. Then, after the close, FHN, IBKR, ISRG, NFLX, OMC, UAL, and WAL report.

In economic news later this week, on Wednesday, EIA Crude Oil Inventories and Fed Beige Books are reported and Fed member Williams speaks. On Thursday, Weekly Initial Jobless Claims, Philly Fed Mfg. Index, and March Existing Home Sales are reported and we get two Fed speakers (Waller and Bowman). Finally, on Friday, Mfg. PMI, S&P Global PMI, and Services PMI are reported.

In terms of earnings reports later this week, on Wednesday we hear from ABT, ALLY, ASML, BKR, CFG, ELV, LAD, MS, NDAQ, EDU, SYF, TRV, USB, AA, CCI, FDS, EFX, FFIV, IBM, KMI, LRCX, LVS, LBRT, STLD, TSLA, WTFC, and ZION. On Thursday, ALK, T, AN, BX, CMA, DHI, EWBC, FITB, GPC, HRI, HBAN, KEY, MAN, MMC, NOK, NUE, PM, POOL, RAD, SNA, SNV, TSM, TFC, UNP, WSO, and WBS report. Finally, on Friday, ALV, FCX, HCA, PG, RF, SDVKY, SAP, and SLB report.

After the close, JBHT reported misses on both the revenue and earnings lines. So far this morning, BAC, JNJ, LMT, ERIC, BK, and CBSH all beat on both the revenue and earnings lines. Meanwhile, GS missed on revenue while beating on earnings. A couple of notes of interest, BAC’s revenue was a 58% larger beat than analysts expected and BK’s revenue was also a 63% upside surprise. At the same time, ERIC’s earnings beat was double the analyst-expected number. It is also worth noting that JNJ has raised its forward guidance.

One last miscellaneous story of note. Bloomberg reports this morning that investors are the most underweight stocks (versus bonds) that they have been since early 2009. This may mean nothing significant for short-term traders. However, for longer-term traders and investors, it means there is a ton of money sitting on the sideline earning almost nothing. That flood of cash back into the market as FOMO kicked in is what led to the massive rally that began in 2009 and continued essentially unbroken until the pandemic in 2020 (or if we throw out that one-off event until the top in 2022). It is just something to keep in mind moving forward.

With that background, it looks like the bulls are trying to break out of the recent range (going back to the start of the month in the case of QQQ) this morning. The bullish trend continues with the moving averages stacked. Over-extension does not appear to be a problem in terms of the T-line (8ema) for any of the major indices. Yet a case can be made that we are getting extended to the upside according to the T2122 indicator. We should also realize we are up against a potential resistance line in the SPY and not too far below on in the DIA. QQQ might be called at “resistance” but it is definitely a weaker or less obvious level. Once again, if we can put aside fear and prediction, the chart is telling us to maintain a long bias on a swing trading horizon while keeping a sharp eye out for trend breaks. So, be careful and go with the flow.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Despite the last-minute surge the SP-500 finished the day little changed in an overall choppy low-volume session as we waited on the market-moving reports from BAC and GS Tuesday morning with NFLX coming after the bell. We will also get a reading on the health of the housing sector with a starts and permits report before the opening of trading. Bond prices continue to be problematic but interestingly the market seems happy to ignore it as the VIX continues to fall and the T2122 indicator presses back into the overbought region. The morning session could be wild so watch for some big gaps and possible big point whipsaws as the investors react.

Overnight Asian markets closed mixed even as China beat first-quarter GDP expectations. However, European markets see nothing but green with earnings data on the horizon and the ECB signaling a possible 50 basis point rate increase. As we wait on big bank reports the U.S. futures push for a gap up open that could move dramatically as results come into the light.

Economic Calendar

Earnings Calendar

Earnings begin to pick up today through Thursday then get really busy next week. BAC, BK, ERIC, FHN, FULT, GS, IBKR, ISRG, JNJ, LMT, NFLX, OMC, PLD, UAL, & WAL.

News & Technicals’

Apple opened its first store in India, called Apple BKC, in Mumbai. The company is also opening another store in Delhi. Apple CEO Tim Cook has long held a bullish view on India and now the company is ramping up sales and manufacturing of its flagship iPhone in the country. This highlights the importance of the Indian market to Apple’s future.

House Speaker Kevin McCarthy spoke at the New York Stock Exchange. He opened a new phase in the debt ceiling fight by saying House Republicans would pass their stand-alone debt ceiling hike with spending cuts and stricter work requirements. However, such a bill would be dead on arrival in the Democratic-controlled Senate and in Democratic President Joe Biden’s White House.

The S&P 500 was little changed after an up week that pushed it near the year’s highs. Small-caps outperformed. Earnings remain the area of focus, with 60 S&P 500 companies scheduled to report this week, including Charles Schwab and State Street today. Bank of America, Goldman Sachs, Netflix, and Tesla are due to deliver results later this week. House Speaker McCarthy is expected to outline Republican demands for spending cuts and other concessions regarding the debt ceiling. Treasury yields were higher as investors are starting to rethink the likelihood of the Fed cutting rates later this year.

Bank stocks led the gains on Friday while overall the indexes struggled as rising bond yields and worries about tightening credit weighed on investors’ minds. Today we will hear from Schwab which has been challenged by substantial capital outflows in the recent banking scare. The results could be market-moving with the warnings from Jamie Dimon and Warren Buffet of more bank failures to come. Also ahead will be the Empire State MFG and Housing Market Index reports which have shown a weakness in the sectors.

Asian market closed Monday trading with modest gains despite the surge in Hong Kong up 1.68%. European markets also trade with modest gains hoping to shake off recession worries as earnings ramp up. As I write this report U.S. futures point to modest gains as bond yields rise ahead of earnings and economic reports that could bring more bullish inspiration or embolden the bears. Plan for just about anything as the market reacts.

Economic Calendar

Earnings Calendar

Notable reports for Monday include SCHW, ELS, JBHT, MTB, PNFP, & STT.

News & Technicals’

Google CEO Sundar Pichai has warned that society is not prepared for the rapid advancement of AI. In an interview with CBS’ “60 Minutes” that aired Sunday, he said that laws that guardrail AI advancements are “not for a company to decide” alone. He also warned of consequences, saying that AI will impact “every product of every company.”

U.S. Treasury Secretary Janet Yellen has said that banks are likely to become more cautious and may tighten lending further in the wake of recent bank failures. This could negate the need for further Federal Reserve interest rate hikes. “Banks are likely to become somewhat more cautious in this environment,” Yellen said in the interview, which is scheduled to air on Sunday. “We already saw some tightening of lending standards in the banking system prior to that episode, and there may be some more to come.” She said that would lead to a restriction in credit in the economy that “could be a substitute for further interest rate hikes that the Fed needs to make.”

Indexes struggled to finished slightly lower Friday after Thursday’s sharp rally that helped push global indexes to their highest close in 10 weeks while rising bond yields and tightening credit worried investors. Bank stocks led the gains, with shares of JPMorgan jumping after the company reported strong earnings results. Government bonds yields rose after the Fed’s Waller urged more monetary-policy tightening to reduce still high inflation, pressuring some of the rate-sensitive sectors. Elsewhere, oil prices rose after the International Energy Agency (IEA) said it expected global demand to rise this year on the back of a recovery in Chinese consumption and warned that output cuts announced by OPEC+ producers could exacerbate an oil-supply deficit. As earnings ramp up plan for price volatility to remain challenging in the days and weeks ahead.

Again, on Thursday, markets gapped higher after PPI came in lower than expected. The SPY gapped up 0.27%, DIA gapped up 0.13%, and QQQ gapped up 0.63%. We then saw 30 minutes of figuring out the direction in all three major indices. This led to a long, slow, steady rally that ran all day in the large-cap indices as well as a sharper 20-minute rally before the long, slow steady follow-through rally in the QQQ. These rallies lasted until 3 pm when a sideways grind in a very tight range took hold in all three major indices. This action gave us large-bodied, white candles in the SPY, DIA, and QQQ. The two large-cap indices broke out of their recent pullback while the QQQ broke above its consolidation range dating back to 4/5 but did not break out of the pullback that began at the start of the month.

On the day, all 10 sectors were in the green with Healthcare (+1.75%) leading the way higher while Utilities (+0.20%) lagged behind the others. At the same time, the SPY gained 1.33%, DIA gained 1.12%, and QQQ gained 1.96%. VXX fell 3.64% to 41.34 and T2122 climbed back well into the overbought territory at 93.45. 10-year bond yields rose to close at 3.449% while Oil (WTI) was down 1.02% to $82.39 per barrel. So, markets liked the PPI data falling more than expected and didn’t give the bears an inch all day long Thursday. It was a risk-on day with the tech big dogs (AMZN, NFLX, AAPL, TSLA, and META) taking markets higher. This happened on just less-than-average volume in SPY and QQQ with the mega-cap DIA trading a bit less than the other two indices (relative to average).

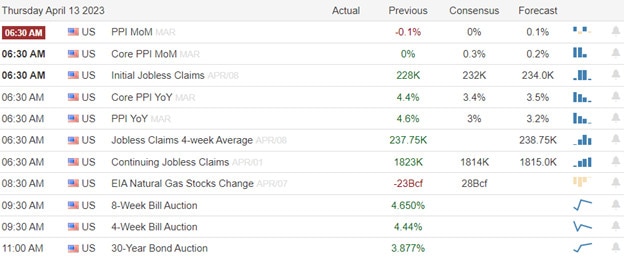

In economic news, the March Producer Price Index surprisingly came in well below expectations at -0.5% month-on-month (compared to a forecast of +0.1% and also well below the Feb. reading of +0.0%). More importantly, the March year-on-year PPI value came in at 2.7%, below the forecast of +3.0% and far below the February value of 4.9%. At the same time, Weekly Initial Jobless Claims were above the anticipated at 239k (versus a forecast of 232k and well above the prior week’s reading of 228k). Later in the day, Fed data was released showing that of the week ending April 12, bank borrowing from the Fed Discount window fell again to $67.6 billion/day (average) from $69.7 billion/day the prior week. At the same time, the total banks borrowed from the new Fed Bank Term Funding Program also fell to $71.8 billion (total for the week) from $79.02 billion in the prior week. This data points to the liquidity problems and turmoil in the banking sector easing, albeit in a modest way.

In stock news, AMZN joined the AI race on Thursday, announcing its Cloud Computing division has released a suite of tools aimed at helping other companies develop their own chatbots and image-generation services powered by artificial intelligence. These services will be powered by AMZN chips as well as AI chips from NVDA. Midday, it was reported by Reuters that XOM raised its CEO pay by 52% in 2022. This came as the pay (median) for XOM workers actually fell by 9%. For reference, the pay of competitors, such as the CEO of CVX rose 4%, the pay of OXY’s CEO rose 35%, and the CEO of COP saw his pay fall 16% (all versus the prior year). Meanwhile, LCID announced the start of a nationwide tour aiming to allow consumers in 40 US cities to get a chance to experience and drive the company’s Air luxury electric vehicle at “pop-up studio locations” in the cities. Separately, LCID announced they produced 2,314 and delivered 1,406 vehicles in Q1 (ending March 31). Elsewhere, S&P reported after the close that hedge funds thought the recent “banking crisis” was a buying opportunity. The report said hedge funds increased their regional bank stock exposure by 5.5%. As an example, Citadel (one of the most profitable hedge funds) bought a 5.3% stake in WAL while it was being battered. After the close, Reuters reported that BBVA, BAC, and SAN will jointly fund a $6 billion deal allowing Mexico to purchase power plants from IBDRY. Finally, BA announced after the close that it has stopped deliveries of 737 MAX planes as new quality problems (possibly stretching back to 2019) were identified with parts from their supplier SPR.

In stock legal and regulatory news, across the pond, the Swiss parliament rejected the Swiss government’s $121 In stock legal and regulatory news, mid-afternoon Thursday, GOOGL’s attorneys were grilled by a US District Court judge as the company sought to get a US Dept. of Justice antitrust case thrown out. The suit alleges that GOOGL illegally paid billions of dollars each year to AAPL, MSI, VZ, LG, Samsung and others to keep Google as the default search engine on their phones. Interestingly, the main alleged victim in the lawsuit is MSFT, who the Dept. of Justice successfully sued for antitrust violations in 1998. At the same time, STLA told Bloomberg it is leaning toward expanding production of a Peugeot electric vehicle in Spain. This has caused France to directly pressure the CEO of STLA and Slovakia (where the vehicle is now produced) is formulating a strategy to keep or add jobs. Meanwhile, KR asked a US federal judge to dismiss an antitrust case that had been filed by consumers, in hopes of blocking the acquisition of ACI. Across the pond, the EU said that Ireland has one month to create an order blocking META from doing transatlantic data flows. This would be the finalization of a ban on META from sharing and using European user data. Elsewhere, the US Dept. of Justice said ADBE has agreed to pay $3 million to settle allegations the company paid kickbacks to companies that convinced the federal agencies to buy ADBE software.

In miscellaneous news, the downward spiral of Natural Gas prices continued as the front-month Natty contract closed at $1.997/mmBtu on Thursday. This was the lowest close since June 2020 (amidst national lockdowns). Prior to that, this low level had not been seen since January 2016. Thursday’s move came as the EIA announced its natural gas storage data for the week. This week saw the first inventory build of the year for Nat Gas, but it was a smaller increase than expected at +25bcf (compared to a forecast of +28bcf). In other news, the Supreme Court has decided not to halt a legal settlement that erases $6 billion in debt that was owed by former students of (mainly for-profit) colleges who had been misled about school academics and job prospects. Meanwhile, a group representing Southern CA seaports (the Pacific Maritime Assn.) claimed Thursday that the largest union of longshoremen on the West Coast is disrupting the busiest seaport in the US for the second week in a row. This slowdown comes as negotiations over a new contract covering 22,000 West Coast dockworkers near the one-year milestone (with no major progress apparent). Major shippers like WMT and HD have been diverting cargo ships to ports on the Gulf of Mexico and East Coast to avoid potential work stoppages.

Overnight, Asian markets leaned heavily to the green side. Only New Zealand (-0.42%) and Thailand (-0.28%) were in the red. Meanwhile, Japan (+1.20%), Taiwan (+0.79%), and Shanghai (+0.60%) led the region higher. In Europe, we see a similar picture taking shape at midday. The CAC (+0.43%), DAX (+0.39%), and FTSE (+0.59%) are leading that region higher in early afternoon trade. In the US, as of 7:30 am, Futures are pointing toward a mixed open ahead of news. The DIA implies a +0.07% open, the SPY is implying a -0.06% open, and the QQQ implies a -0.44% open at this hour. At the same time, 10-year bond yields are rising to 3.467% and Oil (WTI) is up half of a percent to $82.57/barrel in early trading.

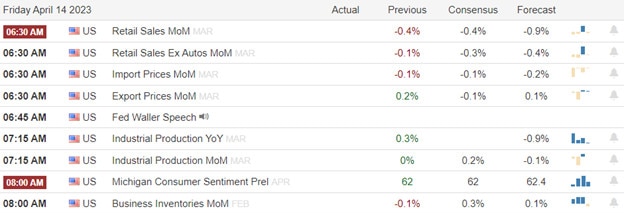

The major economic news events scheduled for Friday include March Retail Sales and March Import/Export Price Indexes (both at 8:30 am), March Industrial Production (9:15 am), Feb. Business Inventories, Michigan Consumer Sentiment, and Feb. Retail Inventories (all at 10 am). We also have a Fed Speaker (Waller at 8:45 am). The major earnings reports scheduled for the day include BLK, C, JPM, PNC, UNH, and WFC before the open. There are no major earnings reports scheduled for after the close.

So far this morning, UNH, JPM, WFC, PNC, and BLK all reported beats to both the revenue and earnings lines. (It is worth noting that on the revenue line, JPM surprised by 52% while PNC surprised by 37%, and WFC surprised by 33%.) C reports at 8 am. So far, only PNC has changed forward guidance, lowering its outlook.

With that background, at least at this point, it looks like the market’s “wait and see” stance remains intact. The QQQ is making the biggest premarket move…and it is only showing an inside candle move that has yet to go back down to retest the T-line (8ema). I suppose traders could be hanging tight until they see Retail Inventories or even Industrial Production. Still, that seems less important than the big banks starting us off with good reports this morning with record revenues, big deposit increases, and the benefit of higher rates (rate margins) as a tailwind. With that said, all three major indices remain in their bullish trends. The 3ema is still above the 8ema, which is above a rising 17ema, which is above the 50sma and that is above the 200sma for all of them. Over-extension does not appear to be a problem either in terms of the T-line but the T2122 indicator is back in the overbought area. This is what the chart tells us now. So, again, putting aside fear and prediction, the chart is telling us to maintain a long bias on a swing trading horizon while keeping a sharp eye out for trend breaks. However, also remember that it’s Friday. So, don’t forget to pay yourself and prepare for the weekend news cycle when you cannot react to changes until Monday.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The bull ran hard Thursday on better-than-expected economic data surging through resistance with no regard to the uncertainty that lies before the market today. It would seem that the market has full confidence that the big banks will report strong enough to support current prices and that the pending economic data will also be rosy. If they are correct look for more upside but watch for possible whipsaws from this short-term extended condition. However, if the data disappoints be prepared for a substantial bear attack that could quickly change market sentiment. Anything is possible so plan carefully.

Asian markets closed green across the board overnight responding to the bullish U.S. prices surge on better-than-expected inflation data. European markets trade with modest gains this morning as they wait and hope for bullish bank reports to support current market pricing. However, after yesterday’s buying spree the U.S. futures point to a slightly bearish open but that could all change as investors react to all the market-moving data ahead.

Economic Calendar

Earnings Calendar

The day the market has been waiting for is here, the kick-off of 2nd quarter earnings begins today. Notable reports for Friday include JPM, BLK, C, PNC, WFC, & UNH.

News & Technicals’

The health of Europe’s commercial real estate market is causing concerns among investors. Some are questioning whether it could be the next sector to blow. Following March’s banking crises, fears have arisen of a so-called “doom loop,” in which a potential bank run could trigger a property sector downturn. According to Morningstar Direct data, European funds invested directly in real estate recorded outflows of £172 million ($215.4 million) in February. Some analysts now see real estate stocks falling by 20%-40% by next year. However, it’s important to note that the situation is not the same across all countries in Europe. Some countries are doing better than others. For example, according to a report by Savills, the UK commercial property market is expected to grow by 3% in 2023. It’s also worth noting that the real estate market is cyclical and downturns are not uncommon. However, these downturns are usually followed by periods of growth.

Chinese President Xi Jinping’s signature foreign policy idea, the Belt and Road Project, was announced in 2013. The ambitious plan aimed to build infrastructure trade links across Eurasia and beyond. However, observers say that a decade after the project’s rollout, it is losing steam. Xi reportedly invited President Vladimir Putin to travel to China for the third Belt and Road Forum this year in an attempt to inject new momentum into the massive endeavor.

The bull ran hard on Thursday as producer price index (PPI) inflation data surprised to the downside. The PPI came in at 2.7% YoY for March, well below last month’s 4.9% reading. This comes after headline U.S. consumer price index (CPI) inflation in March also moved lower for the ninth consecutive month. In addition, jobless claims inched higher this week, up to 239,000, another sign that the labor market may be starting to soften. Markets are still pricing in about a 70% probability of a 0.25% Fed rate hike at its May meeting, although they expect a pivot to rate cuts by the second half of the year*. In our view, the Fed likely has one additional rate hike ahead of it, followed potentially by a longer pause in its rate-hiking cycle. However, today is a big day of data that could keep the bullish party going or dramatically shift sentiment. Prepare for a wild morning of price gyrations and watch out for big point whipsaws from these short-term overbought conditions.

The better-than-expected CPI brought out the bulls with a big gap up open but investors exhaled closing the indexes lower as rising bond yields raised recession concerns. Adding to the uncertainty looking forward both Jerome Powell and Warren Buffett warned that more banking troubles are likely on the horizon. Expect some price volatility this morning as investors react to the PPI and Jobless Claims figures but don’t be too surprised if low-volume chop rules the rest of the day as we wait for the huge day of market-moving data Friday morning.

Asian markets traded mixed overnight reacting to the Fed’s warning of recession as a result of the banking crisis. European markets also trade mixed this morning as recession uncertainty weighs on investors’ minds. At the time of writing this report U.S. Futures trade near the flatline ahead of jobless numbers and producer inflation data after the Fed signaled a recession on the horizon.

Economic Calendar

Earnings Calendar

Just one more day to wait until we begin 2nd quarter’s earnings with several big banks ramping up the volatility. Notable reports for Thursday include DAL, FAST, FRC, & PGR.

News & Technicals’

SoftBank sold $7.2 billion worth of shares in Alibaba via prepaid forward contracts. Three years ago, SoftBank maintained a nearly 25% stake in Alibaba worth over $100 billion. SoftBank and its Vision Fund have been posting huge quarterly losses amid a slowdown in the tech sector that has hammered valuations.

According to a survey by the International Association of Credit Portfolio Managers, 81% of fund managers see defaults picking up in the next 12 months, compared with 80% in the survey last December. For North American corporates, 86% of respondents see defaults rising, while 91% see defaults rising in Europe.

Oil traded near a five-month high as falling US inventories and surging Chinese imports added to signs of a tightening global market. West Texas Intermediate futures held above $83 a barrel after gaining 4.4% over the past two days.

According to Federal Reserve documents released Wednesday, the fallout from the U.S. banking crisis is likely to tilt the economy into recession later this year. Though Vice Chair for Supervision Michael Barr said the banking sector “is sound and resilient,” staff economists said the economy will take a hit.

Stocks opened higher on Wednesday, as investors exhaled after the latest read on inflation failed to produce any worrisome surprises. That enthusiasm faded somewhat as the trading day went on, with the S&P 500 closing 0.4% lower while the Dow shed 38 points. Interest rates responded by moving lower, with the 10-year Treasury yield falling back near 3.4%, while shorter-term rates fell more amid some relief on the Fed rate-hike outlook. Today traders will get more inflation data from the PPI report and the data on the jobs front with the jobless claims. Shortly after attention will turn to the big bank earnings Retail Sales and Industrial Production figures out Friday morning.

Markets gapped higher on Wednesday after good CPI data. SPY gapped up 0.52%, the DIA gapped up 0.50%, and the QQQ gapped up 0.64%. However, again we saw divergence at that point with the large-cap indices meandering sideways for an hour before selling off for 45 minutes, recrossing the gap in the process. Meanwhile, QQQ had faded the gap-up within 20 minutes of the open and then kept heading lower until 11:15 am. At that point, all three major indices put in a long, slow rally that lasted until just after 2 pm. Then, the selloff was on with the bears driving prices lower the rest of the day. This action gave us large-body, black candles in all three major indices. This included an Evening Star signal in the SPY, a Dark Cloud Cover in the DIA, and a big, black, outside day candle in the QQQ. QQQ also crossed back below its T-line while the other two major indices held above their own 8ema.

On the day, seven of the 10 sectors were in the red with Consumer Cyclical (-1.77%) leading the way lower while Industrials (+0.32%) held up best. At the same time, the SPY lost 0.39%, DIA lost 0.09%, and QQQ lost 0.88%. VXX gained 0.61% to 42.90 and T2122 fell back out of the overbought territory to 72.44. 10-year bond yields fell to close at 3.402% while Oil (WTI) was up 2.11% to $83.24 per barrel. So, markets liked the CPI data falling more than expected, following the Fed’s preferred path. However, as soon we got the three-week-old Fed takes from the day following the SBNY bank, the bears roared as (at that time) Fed members said they expected the banking crisis to push the economy into recession sometime this year. This happened on less-than-average volume in the large-cap indices and slightly above-average volume in QQQ.

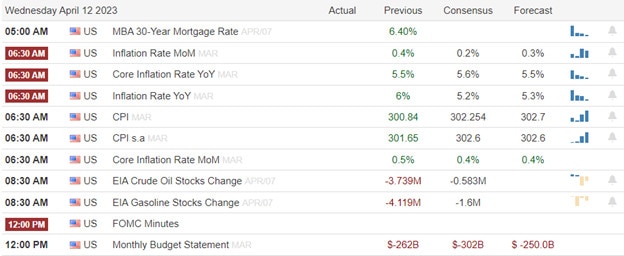

In economic news, the March Consumer Price Index came in below expectations at 5.0% year-on-year (versus a forecast of 5.2% and the February reading of 6.0%). This was the ninth consecutive monthly decline. Later in the morning, the EIA Crude Oil Inventories came in above expectation with a build of 0.597-million-barrels (compared to a forecasted drawdown of 0.583-million-barrels and far higher than the prior week’s 3.739-million-barrel drawdown). Then at 2 pm, the March Federal Budget Balance was larger than anticipated at -$378.0 billion (versus a forecast of -$302.0 billion and significantly worse than the February reading of -$262.0 billion). At the same time, the FOMC Minutes basically followed Fed Chair Powell’s remarks from the March 22 press conference. There was a broad consensus to raise rates by a quarter percent at that point. However, the terminal level of the Fed Funds Rate was also tamped down by the banking crisis going on then. Four of the regional Fed Presidents did not want any hike. The other big news was that Fed Staff (not the voters) put forth that their base case was then expecting a “mild recession later this year” given their assessment of the impact of the banking turmoil on available credit. Elsewhere, San Fran Fed President Daly told an audience Wednesday that more rate hikes may not be needed to tame inflation, saying “there are good reasons to think that policy may have to tighten more to bring inflation down.”

In stock news, a day prior to competitor DAL’s earnings report, AAL announced it is forecasting profits below market expectations. AAL specifically cited high labor and fuel costs. In other transport news, GOOGL got some bad press when some of their Waymo self-driving vehicles pulled over due to heavy fog in San Francisco Tuesday night, causing traffic problems during rush hour. Meanwhile, WBD announced it is combining HBO Max and Discovery+ content to create a new streaming service called “Max” as the company attempts to compete with DIS, NFLX, AMZN, and PARA. At the same time, the world’s largest luxury brand (LVMH, not US-listed) reported a 17% rise in sales in Q1 and specifically notes a strong rebound in the Chinese market. In the electric market, an industry insider reported Wednesday that TSLA is about to launch a third generation of its home battery pack, named Powerwall 3. (No pricing or specs were yet available since the equipment has not yet been approved for connection to the electric grid.) Elsewhere, EMR agreed to buy NATI for $8.2 billion ($60/share). Elsewhere, the Teamsters union told UPS it won’t begin national contract negotiations as (previously scheduled to start next week) until after regional supplemental contracts are completed. 30 supplemental contracts remain unsettled and the national contract expires July 31.

In stock legal and regulatory news, across the pond, the Swiss parliament rejected the Swiss government’s $121 billion aid package that had been part of UBS’s buyout of failing CS. (That government commitment cannot be overturned, but the vote signals that the large house of parliament is not happy with the deal.) Meanwhile, the US Dept. of Labor (in cooperation with other federal agencies) sent a letter to meat companies TSN, JBSAY, and 16 other meat companies Wednesday, ordering those companies to inspect their supply chains in order to root out illegal child labor. The letter said the Dept. of Agriculture is exploring enforcement mechanisms and will take action in the near future. At the same time, US Senator Wyden called for an investigation by Congress and the Administration following a Reuters report that Russia is using facial recognition technology based on chips from NVDA and/or INTC to identify and detain political dissenters. Russian customer records showed that NVDA products continued to arrive in Russia at least through Oct. 31, 2022. (NVDA responded by saying that if it finds a customer who violated US Export Laws, it will cease doing business with that customer.) Elsewhere, a Del. Superior Court Judge imposed sanctions on FOX for withholding evidence in the $1.6 billion defamation case brought against it by Dominion Voting Systems. No fine dollar amount was mentioned, but the cost of added legal work by Dominion following newly the disclosed information will be borne by FOX. In banking news, head of the National Economic Council (and former Fed Vice-chair) Brainard told reporters Wednesday the banking crisis now has eased in terms of deposit outflows. However, she also called for stronger stress testing (liquidity) requirements that include regional banks. Finally, CO became the first state to pass “right to repair” legislation for farmers on Wednesday. The bill will force farm machinery makers like DE and CNHI to provide manuals, diagnostic equipment, and parts to farmers who want to repair (or have local mechanics repair) their farm machinery. Other states are now expected to follow suit and similar legislation may impact other consumer electronics (like phones, tablets, Mac computers, etc.).

In miscellaneous news, Wednesday evening, CNBC reported that a Univ. of Florida finance professor (Lopez-Lira) told them that he used Chat-GPT to predict the next day’s market directions (based on analyzing all news headlines). Reportedly, the results were “much better than random chance.” The professor’s paper has not yet been peer-reviewed. However, Lopez-Lira said his research suggests AI could be trained to predict stock movements. (For what it is worth, this research was done using the older ChatGPT 3.5 model. The professor found less than a 1% chance the model could have achieved the results it attained by mere chance.) Elsewhere, Bloomberg announced overnight that it will integrate a “ChatGPT-style” AI into its Bloomberg Trading Terminal. No timeline was mentioned.

Overnight, Asian markets were mixed in very uneven trading. Shenzhen (-1.21%) and Taiwan (-0.80%) were by far the largest losers. Meanwhile, South Korea (+0.43%) was the biggest gainer. Still, the green exchanges outnumbered the red exchanges in the region. Over in Europe, we see a similarly mixed picture taking shape, but most of the bourses lean toward the green side at midday. The CAC (+0.93%), DAX (-0.08%), and FTSE (+0.01%) lead on volume as usual in early afternoon trading. In the US, as of 7 am, Futures are pointing toward a flat to green start to the morning (ahead of PPI data). The DIA implies a +0.01% open, the SPY is implying a +0.10% open, and the QQQ implies a +0.24% open at this hour. At the same time, 10-year bond yields are back up to 3.424% and Oil (WTI) is down half a percent to $82.86/barrel.

The major economic news events scheduled for Thursday are limited to March PPI and Weekly Initial Jobless Claims (both at 8:30 am). The major earnings reports scheduled for Thursday include DAL, FAST, INFY, and PGR before the open. There are no major earnings reports scheduled for after the close.

In economic news later this week, on Friday, March Retail Sales, March Import/Export Price Indexes, March Industrial Production, Feb. Business Inventories, Michigan Consumer Sentiment, and Feb. Retail Inventories are reported.

In terms of earnings reports later this week, on Friday, BLK, C, JPM, PNC, UNH, and WFC report.

So far this morning, FAST beat on both the revenue and earnings lines. Meanwhile, DAL beat on revenue while missing on earnings. Unfortunately, INFY missed on both the top and bottom lines. (PGR is scheduled to report at 8:15 am.)

With that background, at least before the PPI data release, traders seem to be continuing their “wait and see” stance. All three major indices are starting to form tiny Bull Harami-type inside candles, staying within the recent consolidation range. Little has changed in the large-cap indices. The 3ema is still above the 8ema, which is above a rising 17ema, which is above the 50sma and that is above the 200sma. The QQQ has nearly the same bullish moving average stack. However, the QQQ 3ema has fallen below the T-line, perhaps giving an indication that the bullish trend has cracks. We also have to recognize that all three major indices are sitting on a potential support level. Over-extension does not appear to be a problem either in terms of the T-line or T2122 indicator. So, the consolidation continues, but the bullish trend has not yet broken. New data or news could change that picture in a heartbeat. However, this is what the chart tells us now. So, again, putting aside fear and prediction, the chart is telling us to maintain a long bias on a swing trading horizon while keeping a sharp eye out for trend breaks.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Ahead of inflation readings investors saw fit to push the indexes into price resistance levels with the Vix showing no fear of the pending data. The T2122 indicator stretched into the short-term overbought range adding some risk of a quick market reversal should the CPI numbers disappoint. Plan for some substantial price volatility after the open as we hear from more Fed members and wait for the FOMC minutes. Anything is possible so plan carefully.

Asian markets closed mostly higher overnight with only the Australian index suffering losses. European markets appear to have substantial confidence in a softer CPI reading this morning seeing nothing but green. U.S. futures also suggest a bullish open ahead of the key inflation data but as soon as the data is revealed it could get much better if inflation indeed declined, however, if the opposite occurs, prepare for a bear attack.

Economic Calendar

Earnings Calendar

Notable reports for Wednesday include APOG, BBBY, & SPWH.

News & Technicals’

According to Chris Harvey at Wells Fargo & Co., the resilience of US equities this year will be short-lived. He expects the S&P 500 to suffer a 10% correction in the next three to six months. That would take the American stock benchmark to around 3,700, which is near the November lows. However, Wells Fargo maintained its year-end price target of 4,200 — or about 2% above Monday’s close.

According to John Flood, a partner at Goldman Sachs Group Inc., this week’s lull in the US stock market is likely to end with Wednesday’s consumer price index report. He wrote in a note Tuesday that investors should expect the S&P 500 to drop at least 2% should the year-over-year inflation rate come in above the previous reading of 6%. However, stocks are likely to go higher if CPI meets or trails 5.1%, which happens to be the consensus estimate from economists in a Bloomberg survey.

The U.S. Environmental Protection Agency has proposed new tailpipe emissions limits that could require as much as 67% of all new vehicles sold in the U.S. by 2032 to be all-electric. This would surpass President Joe Biden’s previous commitment to have EVs make up roughly 50% of cars sold by 2030 and accelerate the country’s clean energy transition. According to Kelley Blue Book data, EV sales accounted for only 5.8% of all the 13.8 million new vehicles sold in the country last year, an increase from 3.1% the year before.

Stocks closed higher on Tuesday as investors await U.S. inflation readings and the start of earnings season later this week. After moving substantially lower in March, government bond yields have stabilized more recently. For example, the 2-year Treasury yield is back above 4.0% after falling to 3.75% over the past few weeks. Market forecasts for a 0.25% rate hike at the Federal Reserve’s May meeting have now increased to a 70% probability. The VIX continues to show no fear and the T2122 indicator has reached the bearish reversal zone adding to the risk of today’s CPI report. Anything is possible so expect volatility and possible big-point whipsaws as we wait for the FOMC minutes this afternoon.

On Tuesday, markets opened flat in all three major indices. At that point, we saw a divergence with the SPY meandering slightly lower until 10:45 am and then starting a long, slow, and modest rally. At the same time, the DIA just started a long, slow, modest rally after the open. Meanwhile, QQQ sold off until 11 am and bobbed around until noon when it also started a slow, steady rally. However, a selloff in the last 30 minutes gave back most of the day’s gains. This action gave us small-body, indecisive candles in both the SPY and DIA, as well as a Bearish Harami candle in the QQQ. Again, this all happened on very low volumes in all the major indices.

On the day, nine of the 10 sectors were in the green with Basic Materials (+1.70%) leading the way higher while Technology (-0.30%) lagged and was the only sector in the red. At the same time, the SPY gained 0.03%, DIA gained 0.28%, and QQQ lost 0.64%. VXX fell almost 1% again to 42.64 and T2122 climbed into the extreme end of the overbought territory at 96.46. 10-year bond yields climbed to close at 3.43%. Meanwhile, Oil (WTI) was up 2.19% to $81.49 per barrel. So, on Tuesday we divergence as Technology languished while the rest of the market slowly rallied, only to give back most of the progress during the last half hour of the day.

In economic news, on Tuesday, NY Fed President Williams (FOMC voter) toed the company line by saying that future the interest rate path will be data-dependent. However, he also said that one more hike in May and then a pause is a “reasonable starting point.” He went on to say that as of now, “the banking system has really stabilized” and that, while the Fed will watch for negative shocks, “right now we’re not seeing any of those effects.” In a separate event, the NY Fed released a report predicting the Fed’s path for shrinking its balance sheet will take several more years. (And I guess the Fed ought to know what the Fed’s going to do better than anybody.) The report forecasts that the Fed balance sheet will only have shrunk from $8.7 trillion to about $6 trillion by the summer of 2025 and will then hold steady for about a year. Elsewhere, Chicago Fed President Goolsbee (FOMC voter) urged “prudence and patience” (caution) by his fellow FOMC members so that the Fed doesn’t raise rates too aggressively. After the close, the API Weekly Crude Stocks Report showed an unexpected inventory build of 0.377 million barrels (compared to a forecasted drawdown of 1.300 million barrels and far different than the prior week’s 4.346-million-barrel drawdown).

In stock news, BABA demonstrated its generative AI model named Tongyi Qianwen (which means “truth from a thousand questions”) Tuesday and promised the company will integrate the model into all of the company’s apps soon. This public demo came just hours before the Chinese government published draft rules covering the way that generative AI services should be managed. Meanwhile, F said it will invest $1.3 billion to retool a Canadian plant to transform the SUV assembly plant into one that produced multiple models of electric vehicle as well as battery packs. Completion of the plant conversion is scheduled for late 2024. In other EV news, HMC announced Tuesday that its goal is to become one to the world’s top three EV manufacturers by 2030. To get there, the company will invest $18 billion and expects to produce more than 3.64 million electric vehicles per year by the end of the decade. Elsewhere, Reuters reported that multiple sources tell it ERJ will sign a deal to sell 20 jets to a Chinese airline during this week’s trip to China by Brazilian President Lula da Silva. At the same time, GLNCY revised its unsolicited bid for TECK, adding a cash component. TECK management responded that the offer was largely unchanged and rejected it as still decreasing the value to TECK shareholders.

In stock legal and regulatory news, the US Dept. of Energy proposed reducing the credit (rating) automakers get for electric vehicles towards meeting government fuel economy requirements (CAFÉ or Corporate Avg. Fuel Economy). For example, under the new rules, an F-150ev which currently is credited at 237.1 mpg would only be rated at 67.1 mpg. This would mean F would need to sell a much higher percentage of hybrid and electric vehicles to maintain an average above the standard. For reference, STLA paid just $152 million for missing the standard in both 2016 and 2017. However, the NHTSA more than doubled the fines for missing CAFE standards in 2022. Elsewhere, in India, a group of startups asked an Indian court to suspend the new GOOGL “in App billing fee system” (scheduled to go live on April 26) until it can be reviewed by the Indian antitrust body. Meanwhile, a US appeals court gave MRNA a win by affirming the decision to throw out an ABUS lawsuit over patent infringement related to MRNA’s COVID-19 vaccines. At the same time, a group of video gamers has filed a new legal challenge to the MSFT acquisition of ATVI. This came after a US judge rejected an earlier version of the suit last month. After the close, a US appeals court ruled a lawsuit against HPQ alleging shareholders were defrauded should be revived, overruling a lower court’s dismissal. (The SEC has already fined HPQ $6 million over the practices in question in September 2020.)

In miscellaneous news, BAC reported Tuesday evening that its clients pulled roughly $2.3 billion from equities markets last week. That was the second consecutive week of overall stock market outflows according to the BAC note. This week’s equities outflow was led by money leaving real estate sector stocks (-$451 million). Interestingly, at nearly the same time, BX announced it had raised $30.4 billion for its latest global real estate fund. Elsewhere, Bitcoin climbed above $30,000 Tuesday, for the first time since June 2022. This puts Bitcoin up 82% on the year. This comes as G7 members are discussing cryptocurrency standards and how they should be regulated ahead of the next G7 meeting at the end of June. Meanwhile, the EIA released a forecast saying that US electricity use will fall 1% in 2023 (down from a record high in 2022) mostly due to a warm winter. In addition, the Dept. of Energy said the use of coal in electric generation is set to fall significantly again this year. In 2022, 20% of electricity was generated through burning coal, and this year that is on track to be 17%. Finally, BA took over the top spot (for the first time since mid-2018), delivering slightly more planes in Q1 (3 more jets) than its main competitor EADSY (Airbus).

Overnight, Asian markets were mixed but there was more green on the board than red. Hong Kong (-0.86%) had by far the biggest losses. Meanwhile, Japan (+0.57%), India (+0.51%), and Australia (+0.47%) led the majority of the region higher. In Europe, the bourses are mostly green at midday. The CAC (+0.45%), DAX (+0.30%), and FTSE (+0.64%) lead nine other exchanges higher in early afternoon trade while only three of the smaller markets are in the red. In the US, as of 7:00 am, Futures are pointing toward a flat to mildly green start to the day (ahead of major data). The DIA implies a +0.23% open, the SPY is implying a +0.16% open, and the QQQ implies a +0.03% open at this hour. At the same time, 10-year bond yields are back up to 3.451% and Oil (WTI) is on the red side of flat at $81.49/barrel in early trading.

The major economic news events scheduled for Wednesday include March CPI (8:30 am), EIA Crude Oil Inventories (10:30 am), March Federal Budget Balance and the FOMC Meeting Minutes release (both at 2 pm). There are no major reports scheduled for Wednesday.

In economic news later this week, on Thursday, March PPI and Weekly Initial Jobless Claims are reported. Finally, on Friday, March Retail Sales, March Import/Export Price Indexes, March Industrial Production, Feb. Business Inventories, Michigan Consumer Sentiment, and Feb. Retail Inventories are reported.

In terms of earnings reports later this week, on Thursday, we hear from, DAL, FAST, INFY, and PGR. Finally, on Friday, BLK, C, JPM, PNC, UNH, and WFC report.

In mortgage news, interest rates fell to a two-month low last week, causing homebuyer mortgage demand to rise. Specifically, the national average 30-year, fixed-rate, 20% down, mortgage rate fell from 6.40% to 6.30% last week. (Loan origination points also fell from 0.59 to 0.55.) As a result, demand for new purchase mortgages jumped 8% on the week. It is worth noting that demand for refinance loans was flat on the week, and overall mortgage demand was still far lower than it was one year prior. Also, even though the weekly average was reported, it was a sharp one-day decline mid-week that likely drew the increased application volumes.

With that background, at least in the premarket, once again it looks like the market is in “wait and see” mode. The large-cap indices are both just on the green side of flat while the Tech-heavy QQQ is just on the red side. However, the 3ema is still above the rising T-line (8ema), which is above a rising 17ema, which is above the 50sma and that is above the 200sma in all the major indices. So, any way you slice it, the trend remains bullish and we can best be described as in a pullback or Bull Flag inside that bullish trend. (With that said, we do have to recognize we are sitting on potential support in the QQQ, and up against a potential resistance level in the DIA and SPY.) Over-extension is certainly not a problem in terms of the T-line. However, the T2122 indicator is deep into the overbought territory. It’s absolutely true that new data or news could change the picture in a heartbeat. However, that is what the chart tells us now. So, putting aside fear and prediction, the chart is telling us to maintain a long bias and keep a sharp eye out for trend breaks.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service