Last Friday as we headed into a 3-day weekend the six-day winning streak broke with a modest decline. Is this a temporary pause or could we be at or near a summer market high as we wait for the next round of earnings? Currently, the SP-500 10-year P/E ratio is 29.8 which is 47.4% above the modern-ear market average of 20.2 suggesting an overbought condition. However, investor enthusiasm for risk may still push the index toward a 4500 print. We have a light day on both the earnings and economic calendar with a bit of follow-through selling pressure showing up in the pre-market.

Asian markets traded mixed with modest gains and losses, however, the tech-heavy HSI fell 1.54%. European markets trade red across the board this morning following Monday’s declines. Ahead of a light day of earnings and economic reports U.S. Futures point to a lower open to begin our holiday-shortened week.

Economic Calendar

Earnings Calendar

Notable reports for Tuesday FDX & LZB.

News & Technicals’

The situation in Ukraine has escalated as Russian forces continue to launch air strikes on several cities and towns. The Ukrainian government has declared a state of emergency and activated its air defense systems. However, it admits that its counteroffensive is proving challenging due to the overwhelming number of Russian troops and aircraft. The international community has condemned the Russian aggression and called for an immediate ceasefire and dialogue.

The Bank of England faces a difficult decision as it prepares to announce its latest policy stance on Thursday. The central bank has to balance the risks of rising inflation and labor shortages against the uncertainties of the post-pandemic recovery and the potential impact of new variants of the coronavirus. The latest inflation data, due on Wednesday, is expected to show a further increase in consumer prices, adding to the pressure on the Bank to tighten monetary policy sooner rather than later.

The S&P 500 six-day winning streak broke on Friday which had lifted it to new highs for the year closing only slightly in the red. The big question is, have we put in a top or is this just a short-term pause in the overall rally? Investors have high hopes that the Fed is done raising rates despite the fact the committee suggested their terminal rate is 50 basis points higher as they work for the 2% target. The rally was more broad-based recently with more sectors and stocks joining the upward trend, but the Nasdaq still led the way, posting its best weekly performance since late January. Hopes of more stimulus from China and a weaker dollar also helped the bullish mood. Asian markets followed suit, as the Bank of Japan kept rates steady. Meanwhile, government bonds fell as the 10-year Treasury yield climbed to 3.77%.

Friday was a profit-taking day ahead of the long weekend and after a blisteringly strong week. SPY gapped 0.08% higher, DIA gapped up 0.11%, and QQQ gapped strongly higher, opening up 0.60%. However, after that open the Bears were in control although from 10 am until 1 pm it was more of a sideways grind. All three major index ETFs closed near their lows. This action gave us black candles with tiny wicks on both ends. There were no candle signals according to a strict reading of the chart. However, the SPY could be seen as having a Dark Cloud Cover sentiment (just missing by an open not above the prior high). All three remain above their T-line (8ema) and only QQQ could be said to still be over-extended to the upside.

On the day, nine of the 10 sectors were in the red as Communications Services (-0.80%) led the market lower and Utilities (+0.21%) was the only sector to manage to stay in the green. At the same time, SPY lost 0.71%, DIA lost 0.53%, and QQQ lost 0.63%. The VXX fell 3.53% to 27.30 and T2122 pulled back modestly but remains in the overbought territory at 87.64. 10-year bond yields climbed to 3.767% while Oil (WTI) gained 1.16% higher to close at $71.44 per barrel. So, overall, as said above, it was a day for profit-taking. This can be seen by the very heavy volume in the QQQ (the market leader all year and especially during the week) while SPY and DIA had a bit less-than-average volume, even on a triple witching day.

For the week, QQQ was up 3.79%, SPY was up 2.22%, and DIA (laggard all year) was up 1.08% even after Friday’s profit-taking. During those five days, QQQ and SPY had above-average volume while DIA was just above average. However, none of them had enough volume to call them a “blowoff top.”

In major economic news on Friday, Michigan Consumer Sentiment came in above the expected number at 63.9 (compared to a forecast of 60.0 and a May reading of 59.2). At the same time, Michigan Consumer Expectations were significantly higher than was expected at 61.3 (versus a forecast of 56.5 and a May value of 59.2).

In stock news, TSP completed its first unmanned road test (39 miles) of its heavy-duty truck in China. Elsewhere, TSLA also offered new short-term incentives in China for its Model 3 cars. The incentives offer buyers between June 16 and June 30 discounted interest rates as well as cash subsidies for the customer’s auto insurance. In other TSLA news, CEO Musk told a French audience that autonomy (full self-driving) was the primary driver of the company’s value. (Quite an interesting statement given the myriad of legal trouble TSLA faces over claims its “full self-driving” is not autonomous and has failed causing deaths, injuries, and property damage.) Also on Friday, HUM echoed the UNH Thursday warning about a spike in medical costs due to higher-than-expected demand for surgery. Later, LLY reported that its migraine drug (which had been approved by the FDA in 2018 for preventative migraine treatment) has failed to prove statistically superior to the competing drug sold by the BVHN and PFE partnership. Meanwhile, GM continued its “internal combustion investment tour” by announcing it would invest nearly $1 billion in the expansion of production at an OH plant making heavy-duty truck engines. Construction will begin immediately and will quadruple the plant’s production capacity. Later, Reuters reported that BALL is now exploring the sale of its aerospace and defense unit for $5 billion with bidders including BAESF, TXT, and private equity firms. (The goal is to focus on beverage packaging production.) Finally, Bloomberg reports that MU is very close to signing a deal to build a $1 billion chip packaging plant in India. This dela may be announced during Indian PM Modi’s state visit to Washington this week.

In stock legal and regulatory news, GOOGL sued a CA man on Friday, charging that he had created 350 fake accounts on its platforms and sold them to real businesses for the purposes of creating 14,000 fraudulent product and service reviews. Elsewhere, CUBI announced it had bought $631 million worth of loans (formerly belonging to SBNY) from the FDIC at a 15% discount from book value. Later, WHR announced it had agreed to drop a lawsuit against one of their former Italian executives (whom they had accused of stealing trade secrets when he left to work for a competitor). At the same time, a US District judge ruled that JPM CEO Dimon will not need to submit to a second deposition related to the US Virgin Island’s lawsuit over the bank’s work for Jeffrey Epstein. In a tangentially-related story, a US judge preliminarily approved the DB $75 million settlement with the victims of Jeffrey Epstein. Meanwhile, a federal court in Louisiana dismissed a TSLA complaint against the state restriction on the direct sale of automobiles. Late Friday the FDA advised COVID-19 vaccine makers (MRNA, PFE/BNTX, NVAX, etc.) to develop new vaccine candidates targeted at the XBB1.5 variant currently circulating. In fine news, TWNK was fined just under $300,000 by the US Dept. of Labor for safety and training failures that resulted in a preventable partial finger amputation of an employee in December. Finally, after he close, BMS sued the US Dept. of Health and Humans Services asking the court to declare US government negotiations over drug prices to be unconstitutional. The specific drug in question is their Eliquis blood thinner. The ridiculous thing about the suit (and peer suits) is that US patients pay an average of $440 for a dose of Eliquis while the same dose cost $162 in Zurich, $96 in Berlin, and $65 in Johannesburg. (It’s good to own politicians.)

In overnight news, BABA announced a six-way restructuring, replacing its chairman in the process with an insider (a long-time confidant of Jack Ma). Elsewhere, Bloomberg reports UBS is facing large fines (maybe $300 million) from the Fed as well as others from UK regulators (maybe $128 million). These fines related to CS dealings with Archegos Capital prior to its implosion.

Overnight, Asian markets were mixed but leaned (on movement size) toward the red. Hong Kong (-1.54%) and Thailand (-1.24%) paced the gainers while Australia (+0.86%), India (+0.33%), and New Zealand (+0.33%) led the gainers. Meanwhile, in Europe, we see a different story taking shape with just two exchanges barely hanging onto the green at midday. The CAC (-0.26%), DAX (-0.56%), and FTSE (+0.01%) lead the way on volume but most of the smaller bourses have moved more to the downside in early afternoon trade. In the US, as of 7:30 am, the Futures are pointing to a surprisingly similar start to the week among the major indices. The DIA implies a -0.31% open, the SPY is implying a -0.33% open, and the QQQ implies a -0.34% open at this hour. At the same time, 10-year bond yields are down to 3.763% and Oil (WTI) is up a bit to $72.09 per barrel in early trade.

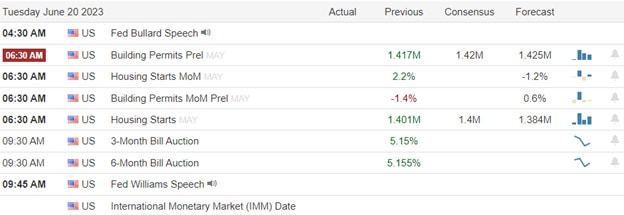

The major economic news events scheduled for Tuesday are limited to May Building Permits and May Housing Starts (both at 8:30 am), and two Fed Speakers (Bullard at 6:30 am and Williams at 11:45 am). The only major earnings reports scheduled for Tuesday are FDX and LZB after the close.

In economic news later this week, on Wednesday, API Weekly Crude Oil Stocks are reported and we two more Fed Speakers (Chair Powell and Mester). On Thursday, we get Q1 Current Account, Weekly Initial Jobless Claims, May Existing Home Sales and three Fed Speakers (Waller, Bowman, and Mester). Finally, on Friday, Manufacturing PMI, Services PMI, and S&P Global Composite PMI are reported while we hear from three Fed speakers (Bullard, Bostic, and Mester).

In terms of earnings reports, on Wednesday we hear from PDCO, WGO, ASTL, KBH, and SCS. Then Thursday, CAN, CMC, DRI, FDS, and GMS report. Finally, on Friday, we hear from KMX.

In miscellaneous news, the US Dept. of Energy received two ransom requests at a nuclear waste disposal site and Oak Ridge Laboratories on Friday. This followed the MOVEit security flaw recently found in PRGS software. Despite this, the Russian hacker group responsible for the hacks posted on their website “WE DON’T HAVE ANY GOVERNMENT DATA” saying that if they mistakenly did get government data “WE STILL DO THE POLITE THING AND DELETE ALL.” Elsewhere, on Saturday, Bloomberg reported that T recently told 60,000 managers to return to the office. The catch was that they have sharply reduced the number of offices. So, many of those ordered back to the office would be required to relocate or quit. (Bloomberg says sources tell this was seen as a way to reduce the costs of severance incurred had they been forced to lay off many of those people.) Finally, Sec. of State Blinken met with Chinese leaders, including Chinese President Xi over the weekend. Both sides made nice, saying a stable relationship is important and inviting Blinken’s Chinese counterpart to Washington for a reciprocal meeting. However, there were no deals made or changes announced for example related to US sanctions or Chinese policies.

With that background, it looks like the Bears are looking to follow through early on Friday’s pullback. The DIA looks headed to retest its T-line (8ema) as support. However, all three major index ETFs remain above their T-lines at this point. So, the market trend remains bullish. In terms of over-extension, none of the major index ETFs are too far above their T-line but the T2122 indicator remains in the lower half of the overbought territory. So, both the Bulls and the Bears have some room to run if they can manage the momentum.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Thursday was the Bulls’ Day almost from start to finish. The SPY gapped down 0.17%, DIA opened flat, and QQQ gapped down 0.35% at the open. However, at that point, it was all Bulls, all the time until 3 pm. The strongest rallies were from 9:30 am to 10 am, 10:30 am to 11:45 am, and 2 pm to 3 pm. Then, the last hour of the day saw very modest profit-taking as price drifted lower into the close. This action gave us big white candles with small upper wicks and no lower wicks in all three of the major index ETFs. The DIA bounced up off its T-line while printing a Bullish Engulfing candle and breaking out of its one-candle pullback. The SPY Bullishly Engulfed a Doji and by day’s end, both the SPY and QQQ were again extended above their 8emas. To say the trend remains bullish is an understatement.

On the day, all 10 sectors were in the green as Communications Services (+1.52%) led the market higher and Consumer Defensive (+0.95%) was the “laggard” sector. At the same time, SPY gained 1.24%, QQQ gained 1.19%, and DIA gained 1.28%. The VXX gained 2.65% to 28.30 and T2122 climbed back up into the overbought territory to end at 91.60. 10-year bond yields plummeted to 3.72% while Oil (WTI) shot 3.38% higher to close at $70.58 per barrel. So, overall, the Bulls simply ran the Bears off after the post-Fed indecision from Wednesday afternoon. It is interesting to note that for the first time in a long time, all three major index ETFs gave us above-average volume with QQQ printing significantly greater-than-average volume. However, none of them gave us so much volume that I would say we need to fear it was a “blowoff top.”

In major economic news on Thursday, the May Export Price Index was far below the expected value at -1.9% (compared to a 0.0% forecast and the April -0.1% value). At the same time, the May Import Price Index was also down but in line with expectations at -0.6% (versus the -0.6% forecast but well below the April +0.3% reading). Weekly Initial Jobless Claims came in above the anticipated level at 262k (compared to a 250k forecast but right in line with last week’s 262k value). Meanwhile, perhaps the oddest data was the divergence in Fed Mfg. Indices. The NY Fed Empire State Mfg. Index came in far above expectations at +6.60 (versus a forecast of -16.00 and massively above the May reading of -31.80). However, a relatively short distance away, the Philly Fed Mfg. Index came in slightly worse than anticipated but still down at -13.7 (versus the forecast calling for -13.5 but still a bit better than the May reading of -10.4). So, both of the Manufacturing Indices were improved but the NY one was greatly improved and positive while Philly was still negative. (Maybe the May NY reading was an anomaly?) Meanwhile, May Retail Sales also came in better than expected at +0.3% (compared to a forecast of -0.1% but was slightly down from the April +0.4%). Later, May Industrial Production Year-on-Year was reported significantly lower than anticipated at +0.23% (versus a +1.30% forecast and even less than the April +0.37% value). The same was true on a Month-on-Month basis where the change was -0.2% (compared to a +0.1% forecast and an April value of +0.5%). So, Industrial Production is slowing. Later still, April Business Inventories came in line with expectations at +0.2% (compared to a +0.2% forecast and growing from the April -0.2% reading). At the same time, April Retail Inventories came in below what was predicted at -0.2% (versus the -0.1% forecast and well better than the March +0.3% value).

In stock news, reacting to corporate boycotts, MDLZ continues to refuse to stop doing business in Russia. However, the company announced Thursday it will try to avoid the stigma by saying that they have stopped making new capital investments in Russia and hope to move all its Russian operations into a separate, stand-alone unit by the end of the year. Elsewhere, MBGAF (Mercedes Benz) announced Thursday that a 3-month test program in the US will begin today (6/16), in which ChatGPT can be given partial control over car systems so that system responses to voice commands will be (hopefully) better and more natural sounding. As a follow-on to Thursday’s Retail Sales report, Reuters says both GM and F reported that consumers unexpectedly bought more cars than the companies had forecast. Meanwhile, DAL announced it will resume paying quarterly dividends, which had been stopped in March 2020 due to the pandemic. (The dividend will be $0.10 per share for holders of record on July 17, paid August 7.) Later, the Wall Street Journal reports that TSLX is considering bidding on some of the bankrupt retailer BBBY’s assets, using more than $500 million of debt it lent to BBBY as at least part of the bid. At the same time, Reuters reports that SPCE will launch its commercial space tourism service late this month when they take three passengers into space June 27-30. In addition, Reuters also reported that within a day of its blowout earnings report, ORCL laid off hundreds of employees and rescinded job offers within its Health unit on Thursday. (That unit includes CERN, which ORCL acquired in December.)

In stock legal and regulatory news, BAYRY (Bayer) and its US subsidiary MON have reached an agreement to pay NY state $6.9 million to settle claims of misleading ads claiming that Roundup weedkiller was environmentally safe. Elsewhere, Bloomberg reported Thursday that GS has paid “millions” to settle an internal complaint after an executive “accidentally” sent a sexually explicit video recording of himself to a female junior staffer. (This complaint was deemed so sensitive that it was handled at the C-suite level and overseen by CEO Solomon.) In the opposite of government regulation, Reuters has reported that INTC and the German government are very close to a deal whereby the chipmaker will receive a $10.83 billion subsidy (up 50% from the amount originally agreed) in return for INTC building a chip-making Fab plant in Magdeburg Germany. (A deal is expected to be signed Monday.) Meanwhile, AMAT sued CA company Mattson (owned by Chinese company) of a 14-month effort to steal technologies and trade secrets used to AMAT’s chipmaking equipment. Later, the Wall Street Journal reported that both the Dept. of Justice and SEC are investigating GS’s role in the final days of SIVB.

In IPO news, exuberance returned to the market as FOMO drove action on the new issue CAVA. The company had priced its IPO at $19-$20 Wednesday night, but the stock opened Thursday at $42 and reached a high of $47.89 before closing at $43.78. That amounted to a tidy 118+ percent one-day gain for those (institutions, insiders, and others) who had got in at the IPO price. The bottom line is that first, CAVA really caught the right day to list and second, the appetite for IPOs seems to have returned to markets. (Some would say that may be a sign we are nearing a top.)

After the close, ADBE beat on both the revenue and earnings lines. This included quarter-on-quarter growth of both lines. ADBE also raised its forward guidance.

Overnight, Asian markets were heavily green with only Taiwan (-0.27%) in the red. Meanwhile, Shenzhen (+1.11%), Hong Kong (+1.07%), and New Zealand (+0.96%) led the rest of the region higher. In Europe, we see the same picture taking shape at midday with only Russia (-0.28%) in the red. The CAC (+0.90%) is out front leading the region while the DAX (+0.30%) and FTSE (+0.38%) also are driving optimism in early afternoon trade. In the US, as of 7:30 am, Futures are pointing toward a flat start to the day. The DIA implies a -0.03% open, the SPY is implying a +0.04% open, and the QQQ implies a +0.15% open at this hour. At the same time, 10-year bond yields are up slightly to 3.732% and Oil (WTI) is off a quarter of a percent to $70.44 per barrel in early trading.

The major economic news events scheduled for Friday are limited to the Michigan Consumer Sentiment Report (10 am) and a pair of Fed Speakers (Bullard at 3 am and Waller at 7:45 am). There are no major earnings reports scheduled for Friday. Still, it is worth remembering that today is Triple Witching Day (the simultaneous expiration of monthly stock options, stock index futures, and stock index futures options), which causes heavy volume, especially at the end of the day. Also, remember that Monday is a market holiday (Juneteenth).

In miscellaneous news, Bloomberg reported that markets need to prepare for more uncertainty around soon to begin flowing “economic disaster” news coming out of Washington. On Thursday, and in spite of claims that they had no such plans earlier this year, a 176-member group of the GOP House members proposed cuts to Social Security in the form of raising the retirement age to 69. The group’s plan would also subsidize private alternatives to Medicare. (This would apparently be a precursor to eliminating that government program at some later time.) The group’s plan (appropriation bills proposals) calls for 30% cuts to all the non-defense areas of the budget…and also for another $5.1 trillion round of tax cuts. (All of these measures are contrary to what they agreed to and was signed into law by the debt ceiling deal just two weeks ago.) So, this is the start of what will clearly be another round of GOP brinksmanship. This time, instead of threatening a default of US debt, they will threaten a government shutdown, leading up to the September fiscal year-end. So, be prepared for coming daily market swings (chop or volatility) based on a series of “the world is ending” and “I’m the most XXX and the other side are all YYY” proclamations from every politician, economist, pundit, Tom, Dick, and/or Harry. In other government news, several US federal agencies joined a growing list of companies (SHEL as one example) and governments hit by a global hacking campaign known as MOVEit. This attack took advantage of a flaw in PRGS company software that is widely used (globally) in information infrastructures.

With that background, it looks like the large-cap indices are looking to start Friday with a little rest (modestly lower open). However, QQQ is near premarket highs at this point and the Bulls seem to want to keep running in the tech-heavy index. All three major index ETFs remain above their T-lines (8ema). So, at least at this point, there is no way to see the market except in a bullish trend. In terms of over-extension, the QQQ is far above its 8ema as of this moment while the premarket action has allowed SPY to get some extension relief. The T2122 indicator is back inside of the overbought territory, but only midway into that measure of overextension. A few other things to keep in mind. First, we have had a hell of a bullish run-up this week. So, profit-taking would seem to be in order (don’t be surprised if we see it by the market overall today). Secondly, the first point is especially true ahead of the upcoming 3-day weekend (and you also need to prepare your account for that off period…take profits, hedge, lighten up, move stops, etc.). Finally, it is “triple witching” (the fourth witch stopped trading in 2020). So, we should expect heavy volume today…particularly at day end…with the possibility of “pinning” or even increased volatility in spots. (Triple witching does not tend to increase volatility overall…but you can drown in a river that viewed overall is only a quarter inch deep.)

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Although the Fed skipped a month in raising rates their hawkish look forward added uncertainty to the path forward. The Dow experienced a huge whipsaw while a handful of tech stocks managed to hold the QQQ in the green for the close. This morning traders face a busy morning of economic data that could move the market substantially as investors react to a complex summer outlook. Bond yields surged higher after the Fed decision pressuring an already strained financial sector. Whipsaws and price volatility are expected to remain challenging as the data rolls out this morning.

While we slept Asian markets traded mixed in reaction to the Fed decision but the tech-heavy HSI surged 2.17%. European market trade was mostly lower this morning expecting a rate increase from the ECB. Ahead of a busy morning of economic reports U.S. futures trade modestly lower but as the data is revealed anything is possible depending on the possible inspiration of the bulls or bears.

Economic Calendar

Earnings Calendar

Notable reports for Thursday include ADBE, JBL, and KR.

News & Technicals’

After two weeks of labor unrest that disrupted trade at 29 West Coast ports, a tentative agreement was reached on Thursday night between the Pacific Maritime Association and the International Longshore and Warehouse Union. The six-year deal covers 22,000 workers who handle about half of the nation’s cargo. The terms of the agreement were not disclosed, but both sides expressed relief and gratitude for the assistance of Acting U.S. Secretary of Labor Julie Su. The port congestion caused by worker slowdowns and stoppages is expected to take several days to clear out.

The war in Ukraine has escalated as Russian mercenaries clashed with the Kremlin over their role and strategy in the conflict. The leader of the Wagner Group, Yevgeny Prigozhin, has refused to sign a contract with the Russian Defense Ministry, which wants more control over the volunteer formations. Meanwhile, Ukraine and its allies are holding a meeting in Brussels to discuss how to bolster Kyiv’s air defenses and artillery against Russian aggression. The meeting comes after Ukraine launched a counteroffensive last week to reclaim some of the territory occupied by Russia. The war has killed at least 10 people and wounded dozens more in Kyiv’s hometown of Kryvyi Rih, where Russian missiles hit civilian buildings.

The Federal Reserve’s decision added uncertainty keeping rates unchanged while raising the terminal rate expectations. The Fed suggested, however, that it might hike rates two more times, as its latest “dot plot” showed a higher fed funds rate target of 5.6%, up from 5.1% in March. Chair Powell said in his remarks that he hoped inflation would start to ease soon, as he saw some signs of a cooling in the labor market. It was a mixed day for stock markets on Wednesday, as the S&P 500 and Nasdaq managed to end the day higher, while the Dow Jones finished lower. Meanwhile, bond yields rose after the Fed meeting, as markets wondered if the Fed would tighten more than expected. The 2-year Treasury yield jumped by 0.10% to 4.68%, almost 1.0% above its lows in mid-May. Today we have a very busy economic calendar filled with possible market-moving reports. Plan for substantial volatility, whipsaws, and big point moves as the traders react to the data.

Markets diverged again today as DIA continued to be a laggard and contrary to the two other major index ETFs. SPY opened very modestly higher (up 0.08%), while QQQ opened up 0.04% higher, but DIA gapped down 0.34%. After the open, SPY and QQQ rallied all morning, reaching the highs of the day at 11:25 am. At that point, they both began a slow selloff that lasted until 2 pm. Meanwhile, DIA ground sideways in a tight range until 2 pm after its gap lower. However, the Fed statement at 2 pm caused the major index ETFs to “sync up” as the market crashed hard for 30 minutes, rallied hard for 30 minutes, and then fell a little less violently during the last hour of the day. However, the SPY and QQQ did rebound in the last 5 minutes much more than the DIA. This action gave us indecisive candles in all three major index ETFs. The SPY printed a long-legged Doji, the DIA a gap-down black-bodied Spinning Top, and the QQQ a white-bodied Hammer or Hanging Man.

On the day, seven of the 10 sectors were in the red as Healthcare (-0.82%) led the market lower, while Consumer Defensive (+0.49%) and Technology (+0.47%) held up much better than other sectors. At the same time, SPY gained 0.12%, QQQ gained 0.73%, and DIA fell 0.65%. The VXX fell almost 3% to 27.57 and T2122 dropped back to just outside the overbought territory to 77.19. 10-year bond yields fell to end at 3.796% while Oil (WTI) lost 1.04% to end the day at $68.69 per barrel. So, overall, it was a divergent day punctuated by the volatility caused by the FOMC. Still, all three index ETFs remain above their T-lines (8ema) even as DAI retested and held its T-line during the day. This all happened on well-above-average volume in the QQQ, slightly above-average volume in the DIA, and average volume in the SPY.

In major economic news, the May PPI (month-on-month) came in better than expected at -0.3% (compared to a forecast of -0.1% and much better than the April value of +0.2%). At the same time, May Core PPI was reported in line with expected values at +0.2% (exactly matching the forecast and April reading, which were both +0.2%). Later in the morning, the EIA Weekly Crude Oil Inventories came in well above the anticipated level at a build of 7.919-million-barrels (versus a forecast calling for a build of 1.482-million-barrels and far above the previous week’s 0.451-million-barrel drawdown). However, the main news of the day came from the FOMC. In terms of Fed Funds rate projections (dot plot), the Fed’s Q2 forecast expects current rates to top out at 5.6% (was 5.1%) this year, one year from now they expect to be at 4.6% (was 4.3%), and two years out they now anticipate the rate to be set at 3.4% (was 3.1%). Clearly, these were all increases from the projections in the Q1 forecasts. Their longer-term projection is for rates to fall to 2.5% (the same as it has been since 2019). With that said, the FOMC did pause rate hikes for the first time in 10 meetings or 18 months, holding rates at the previous 5.00% to 5.25% level.

In terms of Fed speak, as noted above the FOMC statement expects Fed Funds rates to top out at 5.6% later this year. This implies two more quarter-point hikes spread out across the four remaining 2023 meetings. (This hawkish stance was unexpected by the market and caused the big 2 pm knee-jerk downward.) They were more upbeat about the 2023 economy, expecting the job market to endure only “small job losses” (compared to a much more somber March statement) as they project the Unemployment Rate will rise to 4.1% before year-end. At the same time, they see inflation on a very similar path to what they had projected in March. For example, they expect PCE (their preferred inflation measure) to fall to 3.2% later this year. (They had forecasted it would only fall to 3.4% this year at the March meeting). Nonetheless, they still anticipate Fed Fund rate cuts (about 1%) to begin in 2024 in order to stimulate growth because they expect Unemployment to reach 4.5% in 2024.

As for Chair Powell himself, in addressing the pause, he said, “We’ve covered a lot of ground, and the full effects of our tightening have yet to be felt.” Later, he tried to “walk back” the Fed Funds rate forecast by saying he thinks rate cuts are “about a couple of years out” (as opposed to one). However, he also said “I would almost say that the conditions that we need to see in place to get inflation down are coming into place.” (He later defined that progress to mean “growth meaningfully below trend.”) The Chair also said that good financial conditions are likely to allow the Fed to push hard on the reduction of its balance sheet (which itself will act as a means of taking liquidity out of the market). Finally, Powell pushed back against the idea that the FOMC had already made a decision about what they would do in July. Specifically, he said “I would say two things: One, a decision hasn’t been made. Two, I do expect that it will be a live meeting.” With that said, as of 5:30 pm Wednesday the CME Fedwatch Tool says that is a 64.5% probability of a quarter-point hike in July (the other 35.5% bet on no hike at that meeting).

In stock news, health insurance companies took a hard hit Wednesday when UNH announced its costs were rising due to an increase in surgeries by older adults. (HUM took the worst hit plummeting 11.24%, CVS dropped 7.76%, ELV fell 6.89%, UNH itself was down 6.4%, and CI fell “just 3.11%.) In better (shareholder) news, SHEL said it will increase shareholder distribution to 30%-40% of cash flow (up from the current 20%-30%). This includes a 15% boost in dividends as well as an increase in the size and pace of share buybacks. This comes as the new CEO said the company is doubling-down on its “oil and gas” units shifting away from previous efforts to grow “renewables and low-carbon” businesses. Elsewhere, VLKAF said on Wednesday that it expects to realize $10.83 billion in savings from cost-cutting and operational efficiency gains by 2026. At the same time, in boycott news, BUD’s Bud Light beer lost its spot as the top-selling beer in the US (for the week ending June 3) to STZ’s Modelo Especial brand following the backlash from conservatives who did not like BUD doing a social media promotion with transgender influencer Dylan Mulvaney. (Modelo had 8.4% of US beer sales while Bud Light came in second at 7.3% after Bud Light experienced a 24.6% decrease in sales.) Meanwhile, GOOGL announced it is launching two new AI-powered features for advertisers designed to automatically find the best ad placements across GOOGL platforms. Later, SCHW announced it is now forecasting a 10%-11% drop in Q2 revenue due to interest effects and soft trading activity. (SCHW said it has had to rely on more expensive funding sources than had been expected.)

In stock legal and regulatory news, the FAA said Wednesday that all new passenger aircraft will be required to have a secondary barrier to prevent flight deck intrusions. The rule will not take effect until two years from the “effective date” which itself will not be until August. This comes as plane manufacturers (BA and EADSY), unions, and the major airline trade group have fought the rule for years. (The rule was originally supposed to be adopted in 2019. However, industry interest groups have been very successful in dragging out the implementation as lobbying money and lawyers carry a big stick in Washington. In other air industry news, in a nod to airline labor shortage problems, the US House voted to raise the mandatory pilot retirement age from 65 to 67 as part of the FAA reauthorization bill expected to be taken up by the whole House next month. Elsewhere, in Canada, the country’s budgetary watchdog now estimates that the subsidies (tax credits) paid to VLKAF in order to obtain a battery plant will cost their government $1.8 billion (US) more than forecast. This news comes as tense negotiations are underway between Canada and STLA over the subsidies given to garner its own battery plant. Meanwhile, President Biden vetoed a bill that would have scrapped limits on the pollution produced by heavy trucks and buses. This leaves in place EPA rules cutting emissions by 2032 despite GOP and transportation industry objections to the reductions which they say will be too costly to implement over 9 years.

After the close, LEN beat (significantly) on both the revenue and earnings lines. (The homebuilder posted more than a 12% upside revenue and a 27% upside earnings surprise.) It is worth noting that the company also raised its forward guidance.

Overnight, Asian markets were mixed. Hong Kong (+2.17%) and Shenzhen (+1.81%) were by far the biggest gainers while losses were modest, led by South Korea (-0.40%) and India (-0.36%). Meanwhile, in Europe, the bourses are mostly lower at midday. The CAC (-0.83%), DAX (-0.70%), and FTSE (+0.04%) lead the way on volume and market cap as usual. However, Norway (+0.75%) is the biggest of the four gainers in early afternoon trade. In the US, as of 7:30 am, Futures are pointing toward a down start to the day. The DIA implies a -0.22% open, the SPY is implying a -0.41% open, and the QQQ implies a -0.73% open at this hour. At the same time, 10-year bond yields are back up to 3.829% and Oil (WTI) is up just over 1% to $68.98 per barrel in early trading.

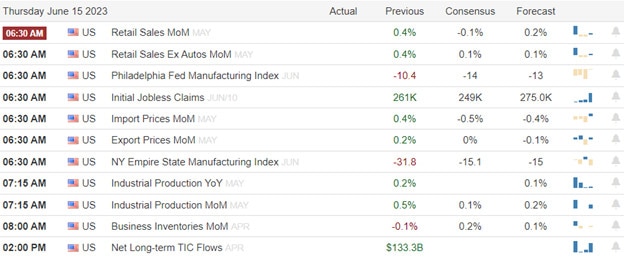

The major economic news events scheduled for Thursday include May Retail Sales, May Imports, May Exports, Weekly Initial Jobless Claims, NY Empire State Mfg. Index, and Philly Fed Mfg. Index (all at 8:30 am), May Industrial Production (9:15 am), April Business Inventories and April Retail Inventories (both at 10 am). The major earnings reports scheduled for Thursday are limited to KR, JBL, and WLY before the open. Then, after the close, ADBE reports.

In economic news later this week, on Friday, we Michigan consumer Sentiment, and a Fed Speaker (Waller at 7:45 am).

In terms of earnings reports, there are no reports scheduled for Friday.

In miscellaneous news, the ECB is expected to raised rates to the highest level in 22 years and leave the door open to more rate increases at 8:15 am today. Unlike the US, even as the Euro Zone economy flags, the ECB is fighting against the highest inflation in the ECB’s 25-year history (now 6.1%). Still, this increase is only expected to take ECB rates to 3.5% (nearly two full percent below the US Fed Funds rate). On this side of the pond, UPS and Teamster negotiators have agreed to one of the key sticking points in their ongoing contract negotiations. UPS will install air conditioning in its entire fleet of 95,000 delivery vans. Finally, CAVA priced its IPO last night at $22 per share with 14.4 million shares on offer as of sometime today. (IPOs typically open after the opening bell as opposed to with the bell.)

With that background, it looks like the Bears are trying to open markets near the lows of the premarket prices. All three major index ETFs remain above their T-lines (8ema). So, at least at this point and by that measure we remain in a bullish uptrend and the move is nothing but a minor pressure relief after five very strong days (at least in the QQQ and SPY). However, the ECB Rate decision or (more likely) the large US data dump at 8:30 am may change that premarket outlook. Expect there to be some volatility now that markets have had a little time to digest the Fed data and words from yesterday. In terms of over-extension, none of the major index ETFs are too far from their T-line as of premarket and the T2122 indicator has dropped back outside of the overbought territory. So, the bulls have some slack if they gather the momentum and, of course, the bears have plenty of room if they want to make a charge.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The lowest CPI reading in 2 years inspired the bulls and investors cheered pricing the market with an expectation the Fed will pause hoping this is the end of the rate hiking cycle. Today at the 2 PM announcement and the following press conference we will find out if the hawks have left the building or not. Before that excitement keep in mind we have Morage Apps, PPI, and Petrolem numbers likely adding to the emotional volatility of the day. Be prepared it could get wild if Powell surprises the market or continues to suggest the rate hike cycle may not be over just yet.

Asian market closed mixed with we slept with the Nikkei hitting fresh new highs and the HSI leading the sellers in the tech-heavy index. However, European markets trade higher across the board this morning with the FTSE MIB leading the way up 1.38% at the time of this writing this report. With a light day of earnings and a busy day on the economic calendar U.S. futures currently trade mixed but could and will likely change significantly based on the pending data reaction. Buckle up, emotions are high so plan for significant volatility.

Economic Calendar

Earnings Calendar

The only notable report for Wednesday is LEN.

News & Technicals’

Advanced Micro Devices (AMD) has revealed its new A.I. chip, the MI300X, which is designed to challenge Nvidia’s dominance in the fast-growing artificial intelligence market. The MI300X is AMD’s most advanced graphics processing unit (GPU), the category of chips that are used to build cutting-edge AI programs such as ChatGPT. The MI300X can use up to 192GB of memory, which means it can fit even bigger AI models than other chips. AMD said the MI300X will start shipping to some customers later this year and will be more meaningful in 2024. AMD’s CEO Lisa Su said AI is the company’s “largest and most strategic long-term growth opportunity” and that GPUs are enabling generative AI.

Vodafone and CK Hutchison have agreed to merge their UK mobile businesses, creating the country’s largest mobile operator with more than 27 million subscribers. The deal, which was announced on Wednesday, will give Vodafone a 51% stake and CK Hutchison a 49% stake in the combined group. The new group will be led by Vodafone UK’s current CEO Ahmed Essam and will invest £11 billion over 10 years to build “one of Europe’s most advanced standalone 5G networks”. The merger is expected to face scrutiny from competition regulators, who have previously blocked a similar deal between Three and O2 in 2016.

Investors cheered as the latest inflation data showed a slowdown to 4% in May, the lowest rate in over two years and in line with expectations. The market is priced for the belief that the Fed will keep rates unchanged at today’s rate announcement at 2 PM Eastern. Although Powell is not known for surprising the market, if he should do so and raise rates expect a very disappointed market that may unleash the bears. Cyclical sectors and small-cap stocks led the gains, while bond yields rose. Asian markets also got a boost from hopes of more stimulus from China. Oil prices bounced back 3% after a sharp drop on Monday.

Tuesday was another day in the Bulls’ column right from the start after a cooler-than-expected CPI number. The SPY gapped 0.34% higher, DIA gapped 0.17% higher, and QQQ gapped 0.78% higher at the open. At that point, both of the large-cap index ETFs followed through for the first 15 minutes before selling off back down to the Opening level by 10:15 am. At that point, both the SPY and DIA rallied back to the highs of the day shortly before 2 pm. Then we saw an hour of selloff back near the open and an hour of mild rally to end the day in both of those large-cap index ETFs. Meanwhile, at the open, QQQ almost immediately sold off completely recrossing the opening gap by 10:15 am. It then rallied back to the open level by 11:30 am and chopped along that level until 1:50 pm. At that point, the QQQ sold off for 45 minutes and then rallied the last hour of the day to close very near where it opened. This action gave us gap-up, indecisive candles across all the major indices. QQQ printed a Doji, SPY printed a white-bodied Spinning Top, and the DIA printed a white-bodied candle with a large upper wick.

On the day, eight of the 10 sectors were in the green as Basic Materials (+1.79%) led the market higher, while Utilities (-0.11%) and Communication Services (-0.10%) were the lagging sectors. At the same time, SPY gained 0.66%, DIA gained 0.43%, and QQQ gained 0.77%. The VXX fell slightly to 28.42 and T2122 climbed even further into the overbought territory to 96.27. 10-year bond yields climbed briskly to end at 3.821% while Oil (WTI) gained 3.02% to end the day at $69.16 per barrel. Overall, all three index ETFs remain well above their T-lines (8ema) with the QQQ and SPY now extended from it. This all happened on average volume in all three (slightly below average in the SPY and slightly above average in the QQQ). So, Tuesday was the Bulls’ Day again but there was indecision. Perhaps this was a nod to the FOMC announcements ahead or maybe to a lack of drama at the Miami courthouse. Either way, we go into Wednesday up against potential resistance in the DIA, a bit below it in the SPY, and with room to run in the QQQ.

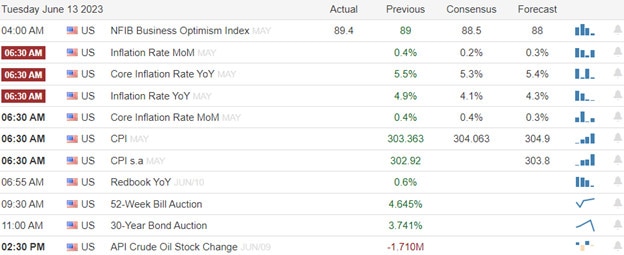

In major economic news Tuesday, May CPI came in below expectations on a month-over-month basis at +0.1% (compared to a forecast of +0.2% and significantly better than April’s +0.4% reading). On a year-on-year basis, May CPI also came in better than was anticipated at +4.0% (versus the forecast of +4.1% and much better than the April +4.9% value). If you look deeper, May Core CPI came in just as expected at +0.4% (month-on-month) and +5.3% (year-on-year). It is worth noting that the year-on-year value was down two-tenths of a percent from the April reading. So, overall, this tells us inflation is cooling but remains well above a 2% target. If you are a hawk, you would say there is a long way to go and the Fed should hike rates more and faster. On the other side, if you are a dove, you’d say inflation has fallen dramatically (more than 5%) in the last year and the Fed probably should pause to give what they’ve done already a little more time to work (in order to reduce the risk of a hard landing). Later, after the close, API Weekly Crude Oil Stocks reported an unexpected inventory build of 1.024-million-barrels (versus the expected 1.291-million-barrel drawdown and last week’s 1.710-million-barrel drawdown).

In stock news, AMD announced a new AI chip that will compete with NVDA’s chips in the same market, starting in Q4. The AMD chip will have more memory and be more power efficient than NVDA’s current offerings. However, NVDA will still have the absolute single-chip computing power lead. At the same time, BA announced that it has delivered 50 737 MAX jets in May (13 less than Airbus but still a 43% improvement over May 2022) as production recovered from the discovery of a defective part. Elsewhere, Reuters reported that AMZN is now excluding the Chinese rival site Temu (which is owned by PDD) from its “competitive price checks” algorithm. This could mean that suppliers could sell the same product on Temu at a lower price than AMZN without incurring the online giant’s wrath. (AMZN is betting it doesn’t have to match/beat Temu prices because buyers won’t check other sites to compare thus raising margins.) Later, UAL announced that it expects the new contract it is offering pilots to add more than $8 billion in costs over four years (if the deal is approved by the union). For reference, the deal DAL reached with its pilots in March is expected to add $7 billion to that airline’s costs over the same period. At the same time, IN Gov. Holcomb announced that GM and Korean manufacturer Samsung will build a $3 billion EV battery plant in the state (planned to begin production in 2026). Later in the day, FSLY disclosed new pricing and product packages. FSLY shares jumped 8.42% on the news. Meanwhile, TSN announced that it will terminate 228 corporate employees in Chicago who have refused to relocate to the company’s AR headquarters. (This is identical to the action taken for employees at the TSN location in SD.)

In stock legal and regulatory news, STLA recalled 354,000 Jeeps from 2021 to 2023 model years according to the NHTSA. The recall was over rear coil springs that might fall off while driving after faulty installation. Elsewhere, Sky News in the UK reports that CNNWQ (Cineworld), who is the primary rival of AMC, is preparing to file for the British version of bankruptcy (administration). For their part, AMC tells Reuters it is still on track to emerge from US bankruptcy in July. Later, the state of NY fined BRKa’s Geico insurance unit for violating the state’s law about timely reporting of the vehicle insurance status of vehicles registered in the state. Late in the day, the NHTSA released a report saying that TSLA Autopilot software has been involved in 736 crashes resulting in 17 fatalities since 2019. (This was a dramatic increase from the same report in June 2022 when the software had only been linked to three deaths.) Meanwhile, MMM appealed the dismissal of its subsidiary bankruptcy case in an effort to avoid liability from 260,000 pending lawsuits claiming hearing loss from defective military earplugs. At roughly the same time, a US appeals court partially revived a shareholder lawsuit (alleging the company concealed a life insurance policy reserves shortfall) against PRU. That shortfall caused a 10% drop in share price when it was announced in November 2019. At the close, the NHTSA sided with automakers by issuing a letter to those automakers telling them not to comply with a MA “Right to Repair” law requiring that they release auto telemetry data to independent repair facilities. The excuse used was that the MA law would pose a safety concern. Also after the close, it was announced that GOOGL must postpone the planned release of its Bard AI in the EU (formerly planned for this week) due to privacy concerns raised by the Irish Data Protection Commission. Finally, a US Patent Office tribunal sided with INTC in its bid to invalidate a patent held by VLSI Technology. The invalidation will cancel out a $1.5 billion patent infringement verdict delivered against INTC in 2021.

In mortgage news, last week the 30-year, fixed-rate, conforming loan rates fell to an average of 6.77% (down from 6.81% the prior week). As a result, home refinance loan applications rose 6% (but were still 41% lower than the same week in 2022). New home purchase loan applications climbed 8% for the week. However, they remain 27% below the same week during the previous year. Overall, this led to a 7.2 increase in mortgage application volume for the week.

Overnight, Asian markets were mostly in the green. Japan (+1.47%) was by far the biggest winner with Singapore (+0.90%), and Malaysia (+0.35%) rounding out the top gainers. Meanwhile, South Korea (-0.72%) and Hong Kong (-0.58%) gave us the only significant losses in the region. In Europe, the bourses lean heavily to the upside at midday with only two spots of red among 13 green exchanges. The CAC (+0.84%), DAX (+0.57%), and FTSE (+0.55%) are leading Europe higher in early afternoon trade. In the US, as of 7:30 am, Futures are pointing toward a mixed and modest start to the day ahead of data. The DIA implies a -0.11% open, the SPY is implying a +0.19% open, and the QQQ implies a +0.14% open at this hour. At the same time, 10-year bond yields are up slightly to 3.827% and Oil (WTI) is climbing up 1.3% to $70.33 per barrel in early trading.

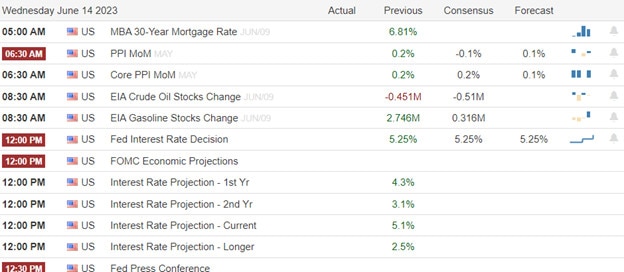

The major economic news events scheduled for Wednesday include May PPI (8:30 am), EIA Crude Oil Inventories (10:30 am), Q2 Fed Interest Rate Projections Current year, 1st year, and 2nd year, FOMC Economic Projections, FOMC statement, and Fed Interest Rate Decision (all at 2 pm), and the Fed Chair Press Conference (2:30 pm). The major earnings reports scheduled for Wednesday are limited to LEN after the close.

In economic news later this week, on Thursday, May Retail Sales, May Imports, May Exports, Weekly Initial Jobless Claims, NY Empire State Mfg. Index, Philly Fed Mfg. Index, May Industrial Production, April Business Inventories, and April Retail Inventories are reported. Then, on Friday, we Michigan consumer Sentiment, and a Fed Speaker (Waller at 7:45 am).

In terms of earnings reports later this week, on Thursday, KR, JBL, WLY, and ADBE report. Finally, there are no reports on Friday.

In late-breaking news, the MSFT $69 billion acquisition of ATVI hit another snag on Tuesday evening as a CA federal judge placed a restraining order on the deal to give the FTC challenge time to be heard in the courts. Elsewhere, Bloomberg reports this morning that the ECB is calling in $540 billion in loans to European banks (pandemic emergency loans) at one time. This will be a real stress test, especially for smaller banks and especially the ones in Italy and Greece. Finally, as reported here earlier, the EU has now charged GOOGL with anticompetitive practices in their ad business. In a preliminary conclusion the European Commission that GOOGL advertising tech is dominant in the European ad buying/publishing market and is abusing that position to harm competitors. The commission suggested GOOGL may be forced to break up, removing its ad marketplace platform from its ad-selling unit.

With that background, it looks like the Bulls in the QQQ and SPY are tentatively looking to make another push at the open today but also that the DIA remains unsure of this move and is leaning downward. All of this is subject to change based on the PPI numbers. However, those are usually less influential than the CPI data we got yesterday. The pivotal data of the day will obviously come from the Fed at 2 pm and 2:30 pm. Expect there to be at least two jolts at that point. (Usually, we get a knee-jerk reaction…and then a counter-reaction. Sometimes even followed by a re-reaction.) QQQ (and to a lesser extent SPY) is extended away from its T-line at this point. Meanwhile, the T2122 indicator is also deep in the overbought territory. So, rest or a pullback is in order regardless of outside data. So, just be prepared for the volatility in what is otherwise a bullish market.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The bull run continued on Monday with high hopes the pending CPI number will weaken enough to give the Fed cover to pause rate increases Wednesday afternoon. Be prepared for a big potential move in the indexes particularly if the number happens to disappoint due to the tremendous anticipation. Interestingly the VIX rallied yesterday indicating an increase in fear even as the indexes surged higher. With no notable earnings reports to inspire bulls or bears, all eyes will key off the economic calendar reports.

Asian markets rallied led by Japan surging 1.80% and topping 33.000 at the close. European markets trade cautiously flat this morning as they wait on the central bank rate decisions. U.S. futures tick higher this morning as we wait on the results of the consumer price index that is highly anticipated to support at Fed rate pause.

Economic Calendar

Earnings Calendar

There are no notable earnings reports for Tuesday.

News & Technicals’

Investors cheered as stocks rose on Monday amid expectations that the Federal Reserve will pause its aggressive rate hikes at its next meeting on Tuesday. The Fed has raised its key interest rate 10 times since last year to combat inflation, which has soared to its highest level in decades. However, some economists believe that the Fed will signal that it is not done tightening monetary policy and that more rate increases are likely in 2023. The S&P 500 and Nasdaq Composite gained 0.93% and 1.53%, respectively, closing at their highest level in 13 months. The Dow Jones Industrial Average added 189.55 points, or 0.56.

Many are hopeful that the US consumer price index report on Tuesday will reveal a slowdown in inflation that will allow the Fed to skip a rate hike on Wednesday. This would be the first time they do not raise the key rate after 10 straight hikes since March 2022.

The U.K. saw its short-term borrowing costs soar to their highest level since the financial crisis on Tuesday after strong labor data fueled expectations of more interest rate hikes by the Bank of England. The yield on two-year government bonds, which influences mortgage rates, climbed above 4.75%, surpassing the peak reached during the market turmoil triggered by the former government’s “mini-budget” last year. The labor report showed that wages excluding bonuses grew by a record 7.2% in the February-April quarter, while employment hit a record high. The Bank of England is under pressure to raise interest rates further to rein in inflation, which stood at 8.7% in April.

The bull run continued around the world on Monday, with Japan and Europe leading the way, as investors anticipated a break in the Fed’s rate hike cycle. Growth-oriented sectors such as technology, communication services and consumer discretionary outperformed, extending their year-to-date rally. Bond markets were calm, with little movement in interest rates. The 10-year Treasury yield stayed close to 3.75%. The market mood improved as the day went on, as hopes grew that the Fed will skip a rate hike at its meeting on Wednesday.

Monday was another Bullish day starting with higher opens. (SPY gapped 0.23% higher, DIA gapped 0.13% higher, and QQQ gapped 0.48% higher.) At that point, all three major index ETFs chopped sideways in a volatile way. At 11 am, the SPY and QQQ started a strong rally that lasted the rest of the day. Meanwhile, DIA finally began to follow at noon, sold off again from 1:20 pm until 3 pm, and then followed higher again the last hour of the day. This action gave us gap-up strong white candles with small lower wicks and almost no upper wick. SPY broke through a resistance level not tested since mid-August 2022 while QQQ is back at levels not seen since March 2022. All three index ETFs remain above their T-line (8ema) as the trend remains Bullish.

On the day, seven of the 10 sectors were in the green as Technology (+1.99%) led the market higher, while Energy (-1.16%) was by far the lagging sector. At the same time, SPY gained 0.91%, DIA gained 0.56%, and QQQ gained 1.69%. The VXX gained a half of a percent again to 28.49 and T2122 climbed back into the overbought territory to 89.41. 10-year bond yields fell slightly to end at 3.742% while Oil (WTI) plummeted 4.45% to end the day at $67.05 per barrel. So, Monday was the Bulls’ Day again. We took out resistance levels and pushed on up with technology leading the way higher. However, it should be noted that this all happened on well-below-average volume in all three major index ETFs.

The only major economic news on Monday was the May Federal Budget Balance which came in a bit worse than expected with a $240.0 billion deficit (compared to a forecast for a $236.0 billion deficit and much worse than the April reading of a $176.0 billion surplus). The primary cause of the deficit is that revenues were down 21% from a year earlier (mostly coming from a decline in high-end tax returns). However, spending was up too, with a tripling of the cost of the Medicare program driving much of the increase. Elsewhere, the NY Fed released a survey Monday which found American inflation expectations have fallen to the lowest level in two years. The May Survey of Consumer Expectations found that respondents project inflation a year from now will be at 4.1% (down from 4.4% in the prior month’s survey). The same respondents expect inflation to be at 3.0% in three years (slightly up from April’s 2.9% average).

In stock news, the Wall Street Journal reported Monday that VZ is looking for a new CFO who would also become the CEO-in-waiting to succeed current CEO Vestberg. At the same time, LMT and GFS announced a partnership to secure a domestic supply of semiconductors for defense systems. The partnership aims to garner part of the $52 billion provided by the Chips Act from the previous Congress. Elsewhere, CAVA released details of their IPO scheduled for later this week. The offering will be 14.4 million shares with a planned price range between $19 and $20 per share. In boycott news, MDLZ is facing growing boycotts by corporate entities in the Nordic region over its continued operation in Russia. Several airlines, railways, hotel chains, retailers, and even the Norwegian Football Assn. are among those who announced they will stop selling MDLZ products in the last few days. In the auto space, following on the heels of similar stories at other locations (MI and TX), GM announced they will invest $632 million to expand its Ft. Wayne IN internal combustion truck plant capacity. In other auto news, TSLA sent emails to Canadian customers canceling the customers’ orders for US-built “Model Y Long Range” vehicles. The email offered those affected the option to instead select Chinese-built “Model Y Long Range” vehicles. After the close, CB announced it has authorized a $5 billion stock repurchase program effective July 1.

In stock legal and regulatory news, it was announced Monday that GOOGL settled with composer Maria Schneider on Sunday, a day before her case against the company for enabling piracy of her works was scheduled to begin. Terms of the settlement were not released. Elsewhere, Reuters reported AVGO is set to win conditional approval for its $61 billion purchase of VMW from the EU Antitrust regulator. The approval will be tied to remedies relating to interoperability with rival products (such as those from MRVL). The official decision is not due until July 17, but Reuters says multiple sources have leaked the outcome to them early. However, in the US, the FTC filed a motion to seek a court order to block the MSFT acquisition of ATVI. (Antitrust experts say the FTC faces an uphill battle because MSFT has already offered voluntary concessions to allay fears it could dominate the online gaming market.) JPM has agreed to settle with the victims of Jeffrey Epstein for $290 million. The settlement still requires the approval of the federal judge overseeing the case. In the afternoon, US District Judge Sorokin delayed the effective date of the permanent injunction blocking the “effective merger” of AAL and JBLU in the Northeast. Originally scheduled to be effective June 20, the revision will make the injunction effective 21 days after his final ruling. This comes after the airlines petitioned for him to not block their “mutual frequent flyer and codeshare arrangements” late last week. At the end of the day, a jury found BRK.A subsidiary PacifiCorp is liable in a $1.6 billion class action lawsuit over wildfires in Oregon. At the same time, Bloomberg reported GOOGL will be hit with a formal antitrust complaint to be announced Wednesday. The new suit targets GOOGL’s ad business model which targets individuals based on information gained by tracking them.

In real estate news, Bloomberg reports that office occupancy in New York has increased. Their survey found that occupancy is above 50% for the first time since before the pandemic. This is welcome news for some as the city estimates that remote work has been costing the New York economy $12 billion a year. However, the same survey found that other major cities such as Washington DC and San Francisco remain below 50% office occupancy.

After the close, ORCL reported beats on both the revenue and earnings lines. The company also raised forward guidance after reporting jumps in the company’s cloud services revenue growth.

Overnight, Asian markets leaned heavily to the green side with only two exchanges in the red. Japan (+1.80%), Taiwan (+1.54%), and Shenzhen (+0.76%) led the gainers. Meanwhile, in Europe, the picture is more mixed at midday. Seven of the 15 European exchanges are in the red with the CAC (-0.08%), DAX (+0.08%), and FTSE (-0.16%) leading on volume. Sadly, Russia (+1.39%) is the biggest positive mover on the day as of early afternoon. In the US, as of 7:30 am, Futures are pointing to a mixed and modestly positive start to the day. The DIA implies a -0.01% open, the SPY is implying a +0.12% open, and the QQQ implies a +0.33% open at this hour. At the same time, 10-year bond yields are down a bit to 3.736% and Oil (WTI) is up 1.94% to $68.43 per barrel in early trading.

The only major economic news events scheduled for Tuesday are May CPI (8:30 am) and API Weekly Crude Oil Stocks (4:30 pm). There are no major earnings reports scheduled for either before the open of after the close.

In economic news later this week, on Wednesday, May PPI, EIA Crude Oil Inventories, Q2 Fed Interest Rate Projections for the current year, 1st year, and 2nd year, FOMC Economic Projections, FOMC statement, Fed Interest Rate Decision, and Fed Chair Press Conference are reported. On Thursday, May Retail Sales, May Imports, May Exports, Weekly Initial Jobless Claims, NY Empire State Mfg. Index, Philly Fed Mfg. Index, May Industrial Production, April Business Inventories, and April Retail Inventories are reported. Then, on Friday, we get Michigan consumer Sentiment, and a Fed Speaker (Waller at 7:45 am).

In terms of earnings reports later this week, on Wednesday, we hear from LEN. Then Thursday, KR, JBL, WLY, and ADBE report. Finally, there are no reports on Friday.

In miscellaneous news, overnight TM announced plans for a new EV unit that will offer a full lineup of “extended range” electric vehicles in 2026. The company also announced it plans to achieve annual sales of 3.5 million all-electric vehicles by 2030. Finally, the ex-President with a persecution complex has called on his backers to show up to support for him and denounce his indictment today as he is arrested, booked, and arraigned in Miami. Worse yet, some of his right-wing Congressional and social media supporters have stoked that fire by falsely claiming the 37-count indictment to be a political attack and calling for everything from the abolition of the FBI and Dept. of Justice to actual militant action. (Rep. Higgins of LA called for the taking of bridges and knowing the points of attack on the maps. Later, he said there is a “3% militia solution” to the indictments.) As a result, this will undoubtedly be the top news story by day-end Tuesday (probably sooner) and has the potential to throw markets into turmoil based on the action taken by “those people” who show up to protest…and whether authorities are prepared to respond appropriately if they step out of line.

With that background, it looks like the Bulls are looking to make another modest push at the open today but also that the DIA remains the laggard (and mostly undecided this morning). The SPY looks like it wants to retest the Mid-April 2022 lows while QQQ seems to be looking to chasing the March 2022 high level. DIA lags, but has a little room before reaching a strong resistance level starting at the May 1, 2023 high. The main takeaway from this for me is that the bulls have all the momentum this morning. However, QQQ is back to being a bit over-extended from its T-line at this point and it would not take a huge move for SPY to join it in that condition. Meanwhile, the T2122 indicator is back up mid-way into the overbought territory. So, we do have some room to run, but we are also a bit stretched. Obviously CPI this morning will drive early action. Expectations are for the report to show modestly moderating inflation (giving fuel to the Fed Doves for a pause in hikes tomorrow). However, as I said above, the situation in Miami has the potential to cause a massive jerk in the market. So, we might see extreme volatility or a reversal of trend, depending on what the MAGA types do and how authorities react. Just be prepared.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Friday was another Bullish and yet hesitant or indecisive day. The SPY gapped 0.19% higher, QQQ gapped 0.47% higher, and DIA was the contrarian again, opening down 0.06%. At that point, SPY and QQQ put in strong rallies while the DIA put in a milder rally over the first hour of the day. At that point SPY and QQQ sold off with intermittent relief rallies reaching Thursday’s closing level at about 12:45 pm. Meanwhile, DIA trod water until about 11:20 am when a sharp, short rally had it back at Thursday’s close by 11:35 am. From there DIA ground sideways in a very tight range until 1:30 pm. Then the last rally of the day took DIA two-thirds of the way back to the highs before grinding sideways into the close from 2:30 pm onward. SPY’s last rally started at 12:45 pm and lasted until 2:30 pm before drifting into the close. At the same time, QQQ rallied more strongly from 12:45 pm until 2:25 pm before selling off into the close.