Earnings and Fed Speakers On Tap Today

Markets opened modestly higher Friday, with the SPY gapping up 0.41%, DIA gapping up 0.32%, and QQQ gapping up 0.53%. At that point, all three major index ETFs gave us a 20-minute rally (follow through) followed by a 20-minute selloff to fade the gap, and then a steady rally that took us to the highs of the day at 12:45 pm. However, then the Bulls headed out the door and the Bears lead a stronger, steady selloff that drove all the way into the close. This action gave us large, black-bodied candles with sizable upper wicks in the SPY, DIA, and QQQ. It also produced Bearish Engulfing signals in the SPY and DIA. All three major index ETFs also retested and failed their T-line during the day as well as falling through a minor support level.

On the day, six of the 10 sectors were in the red with Utilities (-0.76%) again leading the way lower while Basic Materials (+0.20%) and Communications Services (+0.18%) were the only sectors appreciably in the green. At the same time, the SPY lost 0.45%, DIA lost 0.38%, and QQQ lost 0.47%. The VXX climbed 3.57% to 25.83 and T2122 again climbed toward the center of the mid-range to 48.25. 10-year bond yields fell to 4.042% while Oil (WTI) jumped 1.34% to close at $82.64 per barrel. This happened on slightly above average volume in the QQQ and DIA as well as average volume in the SPY. So, we ended the week on a fourth-straight down-day in the SPY and QQQ, resulting in the worst week since March.

The major economic news reported Friday included the July Average Hourly Earnings, which came in above expectations at +4.4% year-on-year (compared to a forecast of +4.2% but in line with the June reading of +4.4%). The July Average Hourly Earnings month-on-month was also a bit above what was anticipated at +0.4% (versus the June +0.3% but again right in line with the June value of +0.4%). At the same time, July Nonfarm Payrolls were reported below the predicted level at +187k (compared to a +200k forecast but just above the June reading of +185k). On the private side, July Private Nonfarm Payrolls were also light at +172k (versus a forecast of +179k but well above the June value of +128k). The July Participation Rate remained steady at 62.6% (with the forecast and June reading also being 62.6%). This all resulted in a July Unemployment rate that fell to 3.5% (compared to a forecast of 3.6% which was also the June value). What all of this Payroll data means is that a soft landing seems more likely as job addition is declining but remains positive even as recent data has shown inflation is falling. Apparently, the Fed has (at least so far) threaded the needle.

SNAP Case Study | Actual Trade

In stock news, shipping giant Maersk warned Friday, saying there has been a steep decline in demand for global sea shipping containers. This implies importers and exporters like LOW, WMT, TGT, HD, UL, ADM, QCOM, NKE, PG, etc. could also be suffering significant demand declines. Elsewhere, GOOGL said Friday that is has unloaded 90% of its position in HOOD, leaving the online ad giant with 612k shares. At the same time, Reuters reported YELL’s Friday bankruptcy filing is now considering a sale of assets and real estate as part of its reorganization. Meanwhile, AMZN announced it will dip into the finance market by offering a credit card in Brazil in partnership with MA. Then, after the close, GM said it will be adding headcount in 2024. Also after the close, AAPL, HPE, and SSGFF all halted shipments to India after PM Modi ordered all imports of electronics to require a license (in order to discourage foreign purchases instead of Indian-manufactured products).

In stock legal, regulatory, and government news, AMZN was cited again Friday by the Dept. of Labor OSHA agency for more hazardous conditions including unreasonable worker quotas and improper medical care. OSHA said it has recommended $15,615 in new penalties (maximum allowed by law) against the AMZN Logan Township, NJ warehouse. (AMZN has 15 days to pay or appeal the fines.) Elsewhere, COIN asked a federal judge to throw out the SEC’s lawsuit that accused it of violating securities laws by trading cryptocurrency the SEC classifies as securities. During the afternoon, the FDA approved the first oral postpartum depression treatment from SAGE and BIIB. (The injectable version required a two-day IV drip.) The condition affects 1 in 8 mothers and could become a major revenue generator based on convenience when the pills hit the US market by year-end. Meanwhile, after the close, the major banks released the amounts they expect to be charged as part of the “special assessment” to replenish the FDIC deposit insurance fund. JPM expects $3 billion, WFC projects $1.8 billion, BAC anticipates $1.9 billion, GS expects $400 million, PNC is planning on $468 million, MS expects $270 million, TFC projects $460 million, and C anticipates $1.5 billion. Finally, the antitrust case against GOOGL brought by the Dept. of Justice and 38 states was narrowed Friday as the judge threw out some claims. This was a significant win for GOOGL, with the case alleging the GOOGL search engine results favor GOOGL and disadvantage competitors like YELP and EXPE heading to trial on September 12.

So far this morning, DK, ELAN, KKR, THS, and VTRS all reported beats on both the revenue and earnings lines. Meanwhile, BRKB and CCO beat on revenue while missing on earnings. On the other side, HSIC missed on revenue while beating on earnings. It is worth noting that THS raised its forward guidance. It is also worth noting that BRKB missed on earnings while still reporting a record quarterly profit.

Overnight, Asian stocks were mixed in modest trading. South Korea (-0.85%), Shenzhen (-0.83%), and Shanghai (-0.59%) paced the six losing exchanges. On the other side, Taiwan (+0.90%), Singapore (+0.53%), and India (+0.41%) led the six gainers. Meanwhile, in Europe, the bourses are leaning heavily to the red side at midday. The CA (-0.48%), DAX (-0.65%), and FTSE (-0.65%) lead the region lower with only Russia (+1.47%) appreciably higher in early afternoon trade. In the US, as of 7:30 am, Futures are pointing toward an open on the green side of flat. The DIA implies a +0.14% open, the SPY is implying a +0.24% open, and the QQQ implies a +0.39% open at this hour. At the same time, 10-year bond yields are surging higher to 4.107% and Oil (WTI) is down one percent to $82.00 per barrel in early trading.

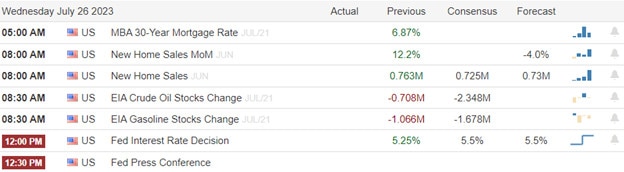

The major economics news scheduled for Monday is limited to two Fed speakers (Harker at 8:15 am and Bowman at 8:30 am). The major earnings reports scheduled for before the opening bell include BRKB, BTNX, CCO, DK, ELAN, HE, HSIC, KKR, THS, TSN, and VTRS. Then, after the close, ACM, AEL, ARKO, BKD, CBT, CE, COMP, CTRA, CAPL, PLUS, WTRG, ICUI, IFF, ITUB, JELD, KMPR, KD, MTW, MRC, OKE, PLTR, PARA, PRI, PRIM, RNG, SWKS, and STRL report.

In economic news later this week, on Tuesday we get June Imports, June Exports, June Trade Balance, and API Weekly Crude Oil Stocks Report. Then Wednesday, EIA Crude Oil Inventories are reported. On Thursday, we get July CPI year-on-year, July CPI month-on-month, Weekly Initial Jobless Claims, July Federal Budget Balance, and the Fed Balance Sheet. Finally, on Friday, July PPI month-on-month, Preliminary Michigan Consumer Sentiment, Preliminary Michigan Consumer Expectations, Preliminary Michigan 5-year Inflation Expectations, and the WASDE Ag report are delivered.

In terms of earnings reports, on Tuesday, we hear from AHCO, ADT, ARMK, ATKR, GOLD, BR, CPRI, CEIX, DDOG, DUK, LLY, ENR, FOXA, GFS, HNI, HZNP, INGR, LCII, LI, NFE, NYT, NXST, NRG, OGN, PRGO, PLTK, RPRX, QSR, SEE, SEAS, STGW, TDG, UAA, UPS, VRTV, WMG, ZTS, AKAM, AMC, BHF, CLOV, CPNG, DAR, EDR, FG, FLT, FNF, FNV, GNW, GO, IAC, IOSP, JXN, LILA, LYFT, DOOR, QGEN, QDEL, RXT, RIVN, SLF, SMCI, TTWO, TOST, MODG, and TWLO. Then Wednesday, BERY, BHG, BCO, BAM, CRL, GEO, HMC, NOMD, OGE, PENN, RBLX, SONY, SWX, SLVM, UWMC, VTNR, VSH, WEN, APP, CACI, CANO, CENX, CDE, CPA, CRGY, ENS, G, ILMN, JAZZ, MFC, NGL, PAAS, TTEK, VSAT, DIS, and WYNN report. On Thursday, we hear from AQN, BABA, AIT, AZUL, TAST, HBI, KELYA, EYE, NVO, ACDC, RL, USFD, WWW, ASTL, BAP, and NWSA. Finally, on Friday, ACDVF reports.

In miscellaneous weekend news, late Friday night META CEO Zuckerberg announced that the new Twitter competitor Threads will have new search and web features within a few weeks. Then on Saturday, Fed Governor (and voter) Bowman (a hawk) said she expects more rate hikes. Bowman went on to say, “We should remain willing to raise the federal funds rate at a future meeting if the incoming data indicate that progress on inflation has stalled.” Elsewhere Saturday, BRKB released record-breaking Q2 results, which showed a 6.6% increase in earnings (versus Q2 of 2022) to $10.043 billion and a $17 billion increase in cash on hand (to nearly $150 billion). Again, this was BRKB’s biggest quarterly profit ever. However, they missed on earnings. Meanwhile, WFC announced Saturday that its system glitch, which had caused many customers’ direct deposits to not be credited to their accounts, had been fixed and account balances were now corrected. (The issue had begun Thursday when WFC began getting social media backlash once again.)

With that background, it looks like markets are giving us a gap-up, black-bodied candle in all three major index ETFs this morning. (Meaning they are well off the pre-market highs.) Inside candles for sure, but trying a modest premarket move. The DIA retested (and failed) its T-line in the early session with the other two just hanging out inside Friday’s candle. All three remain below their T-line (8ema) and the short-term trend is bearish. However, the longer-term trend remains Bullish. As far as extension goes, all of them are close to T-line and T2122 is dead-center in its mid-range. So, both sides of the market have plenty of room to run…if they can find momentum. We only have Fed speakers in terms of scheduled news today. In fact, this should be a light news week until CPI on Thursday.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service