Early morning bearishness quickly turned to a choppy morning session that rather suddenly rocketed up in a big afternoon surge with rather low volume. DIA, SPY, and QQQ all closed at new record highs as traders showed tremendous confidence heading into big tech reports and an FOMC decision. After the bell, we will get the highly anticipated reports from MSFT, GOOGL, and AMD. Plan for a substantial gap Wednesday morning as a result so plan your risk accordingly also keeping in mind the pending FOMC decision. Buckle up for some potentially wild and challenging price action.

Overnight Asian markets closed mixed but mostly lower with Hong Kong and Shanghai leading the selling in reaction to the Evergrande liquidation order adding more uncertainty to China’s real-estate decline. However, across the pond, the European markets are green across the board this morning celebrating a stagnating GDP instead of slipping into recession. U.S. futures point to a slightly bearish open ahead of big tech reports and pending rate decisions on the horizon.

The Big Tech companies are in the spotlight, as they reveal their earnings for the latest quarter. Microsoft and Alphabet will announce their results on Tuesday after the bell, while Meta Platforms, Apple, and Amazon will follow on Thursday. Investors are expecting robust performance from these behemoths, which boosted their share prices to new highs on Monday. The rally in Big Tech lifted the S&P 500 to a new record – and its first close above 4,900. The Dow Jones Industrial Average also reached a new peak at the end of the day.

The eurozone economy showed signs of resilience in the last quarter of 2023, according to the preliminary data released by the EU’s statistical office on Tuesday. The bloc managed to dodge the mild recession that was predicted by a Reuters survey of economists after its GDP shrank by 0.1% in the third quarter. The euro zone’s GDP, adjusted for seasonal variations, did not change from the previous quarter and grew by a meager 0.1% from a year ago.

Neuralink, the brain-computer interface company founded by Elon Musk, announced that it had successfully implanted its device in a human for the first time on Sunday. The patient, whose identity was not disclosed, is “doing well” after the surgery, according to a post on X, a social media platform for scientists and researchers. Neuralink started enrolling patients for its first human trial in the fall, after getting the green light from the FDA in May. The trial is part of Neuralink’s ambitious goal to bring its technology to the market and enable people to control computers and machines with their minds.

Reed Hastings, the co-founder and executive chairman of Netflix, has donated two million shares of the online video service, as per a regulatory filing. The shares are worth more than $1.1 billion at the current market price. Hastings, who has a net worth of $6.6 billion, according to the Bloomberg Billionaires Index, holds a large stake in Netflix, which he helped create in 1997.

With a big afternoon surge the DIA, SPY, and QQQ closed at new record highs, ahead of a hectic week for the macro economy. The Russell 2000 index, worked to catch up action and was the best performer, gaining about 1.4% on the day. The NASDAQ, of course, also did well, increasing by more than 1% as the tech titans continued to stretch higher in anticipation of earnings. Will their earning support these lofty valuations? We will soon find out. Today the FOMC will begin deliberations on interest rates and we will get their decision Wednesday afternoon at 2:00 Eastern. After the bell today we will also get the highly anticipated earnings reports from GOOGL, MSFT, and AMD. The results could create considerable price volatility on Wednesday including a substantial morning gap so plan your risk carefully my friends.

Markets opened just a touch higher on Monday. SPY opened 0.04%, DIA opened dead flat, and QQQ opened 0.09% higher. From that point, all three major index ETFs wandered sideways for 90 minutes. Then the QQQ and SPY began a modest but steady rally at 11 a.m. DIA followed starting at 1 p.m. Then at 3 p.m., the Bulls kicked it into gear so that even after a modest 20-minute pullback all three major index ETFs went out very near their highs of the day. This action gave us large, white-bodied candles in all three with SPY and QQQ being at least “Trader’s Best Friend” patterns (Doji followed by a large white candle) and QQQ even being a Morning Star signal if you are lenient on the first candle. All three remain above their T-line (8ema).

On the day, eight of the 10 sectors were in the green as Technology (+1.36%) led the way higher. At the same time, Communications Services (-0.07%) and Energy (-0.05%) were the only down sectors (barely). Meanwhile, the SPY gained 0.79%, DIA gained 0.58%, and QQQ gained 1.02%. (All three closing at new all-time high closes.) Meanwhile, VXX gained 0.41% to close at 14.59 and T2122 jumped up to the top end of its overbought territory at 94.08. 10-year bond yields dropped to 4.076% and Oil (WTI) fell 1.32% to close at $76.98 per barrel. So, markets opened just on the bullish side of flat, bided their time for 90 minutes, and then rallied the rest of the day. The last hour was the strongest move of the day. This all happened on a well-less-than-average volume in all three major index ETFs.

There was no major economic news released on Monday.

After the close, ARE, CLS, CR, FFIV, GGG, HP, NUE, SANM, SMCI, WHR, and WWD all reported beats on both the revenue and earnings lines. Meanwhile, CLF missed on revenue while beating on earnings. It is worth noting that CLS, SANM, SMCI, and WWD all raised forward guidance. However, WHR lowered guidance.

So far this morning, AOS, DHR, GM, JBLU, MDC, MPC, MPLX, MSCI, and PNR all reported beats on both the revenue and earnings lines. Meanwhile, JCI, OSK, PFE, PHM, and UPS all missed on revenue while beating on earnings. On the other side, PII beat on revenue while missing on earnings. It is worth noting that GM also raised its forward guidance.

In stock news, Reuters reported Monday that STLA has begun volume-level production of large and mid-sized hydrogen fuel cell vans. At the same time, AMZN withdrew from its $1.4 billion acquisition of IRBT. (This move was in response to opposition from EU antitrust regulators. The deal was originally valued at $1.7 billion but investigations led to delay and drove the price down.) At the time this withdrawal was announced, IRBT also announced it would lay off about 31% (350) of its employees. (IRBT plunged as much as 19% on the day, but closed down just 8.77%.) Later, the Wall Street Journal reported that GM dealers were pressuring GM corporate to launch and offer more hybrid vehicles to match demand. Elsewhere, HCMLY announced Monday that it will spin off its North American operations. (No announcement was made on a potential IPO, with NASDAQ and NYSE both courting the Swiss giant.) At the same time, WMT announced it will offer annual stock grants to its store managers in an effort to attract and retain talent. (The awards mean that the most successful store managers could earn more than $400k per year.) After the close, ALB laid off 300 employees (4% of its global workforce). This was part of a previously announced cost reduction plan. (The company expects the move to save it $50 million in 2024.) Also after the close, Reuters reported that TER (semiconductor testing equipment maker) had pulled more than $1 billion of manufacturing out of China in 2023 in order to ensure compliance with sanctions.

In stock legal, governmental, and regulatory news, the Republican Chairmen of two US House committees sent a letter to President Biden asking that the administration launch investigations into four Chinese companies involved in the F battery plant that is planned for construction in MI. Later, AAL was sued (in a potential class-action suit) for having stripped 1.1 million frequent flier miles from two customers after they doubled up using credit card mileage bonuses. The pair allege AAL wrongly accused them of fraud. Elsewhere, TM urged the owners of 50,000 2003-2005 vehicles to stop driving their cars immediately until after recall repairs on airbag inflators can be done. After the close, PHG (maker of recalled and deadly CPAP machines and masks) reached a settlement with the FDA and Dept. of Justice. Under the agreement, the company will stop selling sleep apnea machines in the US (until it meets FDA corrective actions and gets approval), which could cost the company $400 million per year. Also after the close, X agreed to a $42 million settlement of a lawsuit, including $37 million in facility improvements related to a 2018 fire. (After the fire, X operated its plant without the required desulfurizing equipment for three months, emitting huge clouds of sulfurous gas.). The settlement was with environmental groups and the Allegheny County Health Department.

Overnight, Asian markets were mostly in the red as the region reacted to Monday’s court-ordered liquidation of China Evergrande. Shenzhen (-2.40%), Hong Kong (-2.32%), and Shanghai (-1.83%) led the region lower. Meanwhile, in Europe, we see a mostly green picture at midday. The CAC (+0.47%, DAX (+0.19%), and FTSE (+0.51%) lead the region higher (with only four of the 15 exchanges in red numbers) in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing to an open just on the red side of flat. The DIA implies a -0.16% open, the SPY is implying a -0.12% open, and the QQQ implies a -0.04% open at this hour. At the same time, 10-year bond yields are down slightly to 4.064% and Oil (WTI) is flat at $76.78 per barrel in early trading.

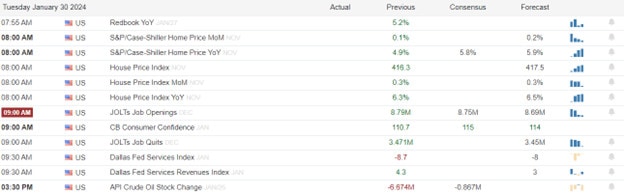

The major economic news scheduled for Tuesday includes Jan. Conf. Board Consumer Confidence and Dec. JOLTs Job Openings (both at 10 a.m.), and API Weekly Crude Oil Stocks report (4:30 p.m.). The major earnings reports scheduled for before the open include AOS, GLW, DHR, GM, HCA, HUBB, JBLU, JCI, MDC, MAN, MPC, MPLX, MSCI, OSK, PNR, PFE, PII, PHM, SYY, and UPS. Then, after the close, AMD, GOOGL, ASH, BXP, CP, CB, EA, ENVA, EQR, FBIN, GOOG, HA, JNPR, LFUS, MTCH, MSFT, MOD, MDLZ, RNR, RHI, SWKS, SBUX, SYK, TER, and UNM report.

In economic news later this week, on Wednesday, Jan. ADP Nonfarm Employment Change, Q4 Employment Cost Index, Jan Chicago PMI, EIA Weekly Crude Oil Inventories, FOMC Rate Decision, FOMC Statement, and FOMC Press Conference are reported. On Thursday, we get Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, Q4 Nonfarm Productivity, Q4 Labor Costs Index, S&P Global Mfg. PMI, Dec. Construction Spending, Jan. ISM Mfg. Employment, Jan. ISM Mfg. PMI, Jan. ISM Mfg. Price Index, and Fed Balance Sheet. Finally, on Friday, Jan Avg. Hourly Earnings, Jan. Nonfarm Payrolls, Jan. Private Nonfarm Payrolls, Jan. Participation Rate, Jan. Unemployment Rate, Dec. Factory Orders, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-year Inflation Expectations, and Michigan 5-year Inflation Expectations are reported.

In miscellaneous news, ICE reported Monday that global futures (including derivatives) have hit a record level of open interest. They reported that 87.2 million stock futures contracts traded on January 25, leaving an open interest of 61.5 million contracts. At the same time, 33 million energy futures contracts traded leaving an open interest of 56 million contracts. Elsewhere, JPM reported Monday evening that the 11 new “spot price of Bitcoin” ETFs are seeing large drops in money inflows.

In government news, after the close, a bipartisan group of Congressional negotiators reached agreement on spending levels for each of the 12 funding bills needed to keep the government open. These total to the amount previously agreed by House Speaker Johnson and Senate Majority Leader Schumer ($1.59 trillion) but below the amount originally agreed before the GOP reneged on the June 2023 deal. While Johnson could use Democratic votes to get the bills passed in the House, it is unknown whether any of the MAGA extremists would call for his ouster if he did that. (Of course, theoretically, Democrats could also override that tiny minority holding everything hostage by voting for Johnson during a “vote to vacate the chair,” but it is uncertain whether the Democrats would do that. So, we have a step toward keeping the government open. However, plenty of uncertainty remains on both sides of the aisle as to whether this step really has any meaning. Elsewhere, the Treasury Department said on Monday that it expects to borrow $760 billion in Q1, which is $55 billion below the estimate released in October. The primary reason we do not need to borrow as much is that the economy has been stronger than expected, resulting in higher tax inflows and a higher cash balance than previously forecasted.

With that background, it appears that all three major index ETFs are undecided early. All opened the premarket near their Monday close level and have put in small, black-bodied, and indecisive candles so far in the early session. All three remain above their T-line (8ema) and very, very near their all-time highs. So, the Bulls are still in control of the trend in both the short term and the longer term. In terms of extension, none of the three are too far stretched from the 8ema. However, the T2122 indicator is well into its overbought range. So, the market will again need a pause or pullback soon. Still, both sides have some slack to work with if they can gain enough momentum to do it. Even though 99% of the market knows exactly what to expect from the Fed, with the Fed announcement being tomorrow afternoon, don’t be surprised if today is a “wait and see” day. Continue to keep watching those Tech Big Dogs. (I follow 10, but somebody has coined the term “Magnificant 7” and five of those seven report this week. If those big dogs move as a group, it is basically impossible for the rest of the market to do anything but follow given their trading volumes.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Friday’s price action was highlighted by the INTC disappointment and perhaps a little worry that many of the big tech companies have been priced to perfection with several Mag7 reports pending this week. These huge company reports will be joined by a busy week of economic data that includes an FOMC rate decision on Wednesday and a Friday Employment Situation report. Traders should plan for gap up or gap down market opens on the results of Mag7 earnings, possible big point whipsaws along with overall price volatility that could prove challenging for inexperienced traders.

Overnight Asian market closed mostly higher even as one of China’s largest developers was ordered to liquidate by a Hong Kong court. European market trade mixed this morning after last week’s surge to a two-year high. U.S. futures have recovered off of overnight lows putting on a brave face ahead of a huge week of market-moving data that could create substantial price volatility. Buckle up it could be a wild week ahead.

The stock of China Evergrande, the debt-laden property developer, suffered a sharp drop of more than 20% in the morning session, triggering a temporary trading halt. The plunge came after a Hong Kong court ruled that Evergrande had to repay $260 million to a group of bondholders who had sued the company for defaulting on its obligations. The court decision added to the woes of Evergrande, which had been hoping to reach a last-minute agreement with its foreign creditors over the weekend to restructure its $300 billion debt. However, the talks reportedly broke down, leaving Evergrande on the brink of collapse.

The future of some of the world’s biggest pharmaceutical companies is uncertain, as they face the looming threat of patent cliffs in the next decade. Patent cliffs are the periods when the exclusive rights to sell one or more of their top-selling drugs expire, allowing generic rivals to enter the market and undercut their prices. Bristol Myers Squibb, Merck, and Johnson & Johnson are among the companies that could lose tens of billions of dollars in sales by 2030 due to patent cliffs. However, some of these companies have taken steps to mitigate the impact of patent expirations, such as developing new drugs, acquiring smaller biotech firms, or expanding into new markets.

China is reportedly planning to transfer the control of three of its largest state-owned asset management companies to its sovereign wealth fund, China Investment Corp, in a bid to bolster its financial stability. According to Xinhua Finance, the move would affect China Cinda Asset Management, China Orient Asset Management, and China Great Wall Asset Management, which were established in the late 1990s to deal with bad debts from the banking sector. The plan comes as China faces a severe stock market slump and a mounting debt crisis in its property sector, which has triggered fears of a systemic collapse. By handing over the asset managers to China Investment Corp, Beijing hopes to improve its governance, efficiency, and profitability, as well as to diversify its business scope and reduce its reliance on the domestic market.

Oil prices rose sharply after a series of missile attacks by Iran-backed militants in the Middle East. The attacks targeted a fuel tanker in the Red Sea, causing a fire and a large oil spill, and a U.S. military base in Jordan, killing three U.S. soldiers and wounding several others. The attacks were carried out by unmanned aerial drones, which Iran has been supplying to its allies in the region. The escalation of tensions in the oil-rich region sparked fears of a wider conflict and disrupted the global oil supply.

The U.S. stock market edged down Friday with the INTC disappointment, ending a six-day winning streak. Technology stocks have been leading the rally, lifting the main indexes to record levels, but after Intel reported weak earnings the QQQ is perhaps showing a little worry about the elevation in the tech giants ahead of earnings. Focus this week with be the several Mag7 earnings reports along with the general ramp of earnings numbers. Along with likely earnings volatility, we have a big week of market-moving economic reports that include an FOMC rate decision and the Employment Situation coming Friday. All these things combined with the very high prices in big tech could make for a wild week of price action. Expect big morning gaps, and watch for the possibility of substantial point whipsaws as investors react to all the data.

The market started out quite bullish again on Thursday. SPY gapped up 0.45%, DIA opened 0.23% higher, and QQQ gapped up 0.60%. All three major index ETFs then ground sideways for a while. DIA was the first to break lower, selling off from 10:30 a.m. until noon. SPY and QQQ followed at noon with SPY reaching its lows (not quite recrossing the morning gap) by 2:10 p.m. QQQ sold off most sharply, recrossing its gap by 1:20 p.m. and reaching the low of the day at 2:10 p.m. From that point, all three put in a modest rally that lasted the rest of the day. DIA went out on the highs, putting in a white-bodied candle that bounced up off its T-line (8ema) and putting it back at the top of its four-day consolidation. SPY printed a small, indecisive, white-bodied Hanging Man-type candle (which could also be seen as a Dragonfly Doji type). QQQ was the laggard, giving us a gap-up, black-bodied, Spinning Top that closed at yet another all-time high close.

On the day, all 10 sectors were in the green as Utilities (+1.80%) and Energy (+1.78%) were way out in front leading the gainers. At the same time, Consumer Cyclicals (+0.21%) was by far the worst-performing sector. Meanwhile, the SPY gained 0.54%, DIA gained 0.64%, and QQQ gained 0.12%. Meanwhile, VXX gained 1.31% to close at 14.64 and T2122 climbed to the top of the mid-range but remains just outside of its overbought territory at 78.52. 10-year bond yields dropped to 4.124% and Oil (WTI) spiked another 2.81% to close at $77.20 per barrel. So, markets gapped higher on strong economic data and earnings reports (with the exception of TSLA which got hit hard on its miss and lower guidance). However, at that point, traders were uncertain, took some profits and then finally started to modestly but again in the afternoon. This all happened on less-than-average volume in all three major index ETFs.

The major economic news on Thursday included Building Permits, which came in just below expectations at 1.493 million (versus a forecast of 1.495 million and well above the prior reading of 1.467 million). At the same time, Weekly Initial Jobless Claims were higher than projected at 214k (compared to a forecast of 200k and well above the prior week’s 189k). Weekly Continuing Jobless Claims also came in hot at 1,833k (versus a forecast of 1,828k and the prior week’s 1,806k). At the same time, Dec. Durable Goods Orders were flat month-on-month at 0.0% (versus a forecast of +1.1% and sharply lower than November’s +5.5%). However, when looking at only the Core Durable Goods Orders for December, the number was hitter than expected at +0.6% (compared to a forecasted +0.2% and the November +0.5% reading). In terms of Q4 GDP, it was very strong data coming in at +3.3% (versus the +2.0% forecast and still less than the Q3 +4.9%). This was mostly real growth since the Q4 GDP Price Index was up just 1.5% (compared to a +2.3% forecast and the +3.3% Q3 value). So, that data is telling us inflation is coming down sharply but GDP is still climbing briskly. The December Goods Trade Balance was just slightly better than anticipated at -$88.46 billion (versus a forecast of -$88.70 billion and trending correctly compared to the Nov. -$90.27 billion). December Retail Inventories were up a bit at +0.6% compared to the November -0.6% reading. Later, Dec. New Home Sales were better than predicted at 664k (compared to a 645k forecast and much better than November’s 615k). Finally, after the close, the Fed Balance Sheet was reported to have actually grown (for the first time in a long time) by just a touch from $7.674 trillion to $7.677 trillion (a $3 billion increase in the last week but still down $10 billion from the week before that).

In stock news, in the wake of its acquisition of ATVI, MSFT announced the layoff of 1,900 from the Activision and Xbox gaming units (their need was eliminated by the merger). The cuts represent 8% of the total employees of the post-merger gaming division. At the same time, TSLA CEO Musk said that Chinese EV-makers will “demolish global rivals” without trade barriers. This comes after BRKB’s Warren Buffett backed Chinese BYD with its substantially cheaper models compared to TSLA. Later, PYPL announced new updates to its products on Thursday. The news was not well received as the stock fell as much as 6.5% on the day before closing down 3.65%. Elsewhere, GM and HMC said they have begun delivering fuel cell systems to customers from their joint venture. The JV factory will produce 2,200 fuel cell systems per year by mid-decade. At the same time, Reuters reported that BAC will give stock awards to 97% of its workforce (employees earning $500k or less). Later, the CEO of PARA announced an unspecified number of layoffs, telling CNBC the company needs to “run leaner and spend less.” After the close, LOW said it would be cutting a “limited number” of non-customer-facing corporate positions. Also after the close, JPM shuffled several top executives as the company prepares for succession after Jamie Dimon leaves. In addition, LEVI said it would cut between 10% and 15% of its global corporate jobs. (LEVI has about 5,000 global corporate employees, which would make the cuts between 500 and 750 jobs.)

In stock legal, governmental, and regulatory news, bowing to obvious market opinion, BA CEO Calhoun said he agreed with the FAA ban on the expansion of 737 MAX 9 production following all the quality control issues identified in the wake of a fuselage panel blowing off a jet in mid-flight. (This came in a brief interview following a meeting on Capitol Hill where Calhoun was explaining to lawmakers that BA would turn things around.) At the same time, the EU’s top court ruled in favor of VLKAF in a dispute over spare parts manufacturers using similar markings to the original parts Audi logo. Later, the NRLB accused WMT of union-busting in CA, alleging the company interrogated its employees, removed pro-union flyers from break rooms, and threatened employees who distributed union literature (all being violations of US labor law). At the same time, the SEC delayed making an approval decision on BLK’s application to launch two Etherium-based spot-price ETFs (similar to the 11 Bitcoin ETFs recently approved). AAPL announced Thursday that it will begin allowing app downloads from sources outside of its own store…but only in Europe and only in reaction to the new EU law (DMA) that requires this move to avoid massive penalties. In reaction to the recent accounting investigation, shareholders filed suit against ADM and its executives. Later, GM revealed it is being probed by both the US Dept. of Justice and the SEC related to the October incident where one of GM’s Cruise self-driving cars ran over and dragged a pedestrian. GM said these investigations stemmed from a “failure of leadership” (which had tried to hide the incident initially) and vowed to “reform its culture.” After the close, the CA Public Utilities Commission approved a $45 million penalty against PCG for its part in causing the 2021 “Dixie” fire. Also after the close, the FTC announced it had ordered MSFT, GOOGL, and AMZN to provide information on their recent investments in AI companies OpenAI and Anthropic. (The companies have 45 days to provide that information.)

After the close, AJG, ASB, TBBK, INTC, KLAC, LHX, OLN, SSB, V, and WDC all reported beats on both the revenue and earnings lines. At the same time, COF, TMUS, and WAL beat on the revenue line while missing on earnings. On the other side, LEVI AND WY missed on revenue while beating on earnings. It is worth noting that INTC, LHX, and LEVI lowered guidance while WDC raised its forward guidance.

Overnight, Asian markets were mixed and leaned toward the red side. Hong Kong (-1.60%), Japan (-1.34%), and Shenzhen (-1.06%) were by far the biggest losers while Australia (+0.48%), Singapore (+0.38%), and South Korea (+0.33%) led the gainers. However, in Europe, we see strong green numbers across the board at midday. The CAC (+2.17%), DAX (+0.21%), and FTSE (+1.21%) lead the region higher in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a start on the red side of flat. The DIA implies a -0.05% open, the SPY is implying a -0.07% open, and the QQQ implies a -0.35% open at this hour. At the same time, 10-year bond yields are down slightly to 4.12% and Oil (WTI) is down 1% to $76.62 per barrel in early trading.

The major economic news scheduled for Friday includes Dec. Core PCE Price Index, Dec. PCE Price Index, and Dec. Personal Spending (all at 8:30 a.m.), and Dec. Pending Home Sales (10 a.m.). The major earnings reports scheduled for before the open include AXP, ALV, BAH, CL, FCNCA, GNTX, and NSC. There are no reports scheduled for after the close.

So far this morning, ALV, BKU, BAH, and CL have reported beats on both the revenue and earnings lines. Meanwhile, VLVLY missed on revenue while beating on earnings. On the other side, FCNCA beat on revenue while missing on earnings. Unfortunately. AXP missed on both the top and bottom lines. However, AXP and BAH both raised forward guidance.

In miscellaneous news, major private Fintech firm EquiLend reported an outage of its service on Thursday. The service, which automates the lending of shares between broker-dealers said Wednesday it had identified unauthorized access to its systems. The system manages $2.4 trillion in stock transactions each month and this outage may have temporarily impacted the ability to short some stocks. (EquiLend is partly owned by GS, JPM, BAC, and BLK among other big Wall Street names.) Elsewhere, Reuters reported that (in a sign of changed warfare) an explosive drone had a nat. gas field in Northern Iraq, doing limited damage. Earlier in the day, another drone had targeted US forces near Erbil Iraq. However, that drone was shot down by US air defenses and did no damage.

In overseas inflation news, the ECB policymakers said Thursday that they were “open to” a policy change in March (i.e. a rate cut). This was a change in rhetoric for the European Central Bank. Still, it maintained rates at its historically-high 4% rate. Later, Japan reported that its Core Consumer Price Index (for Tokyo, which is a leading indicator for the rest of the country) has fallen below the Bank of Japan’s 2% inflation target. Tokyo’s core CPI in January is just 1.6% above a year earlier, much lower than the 1.9% that was forecasted and down sharply from 2.1% in the December report.

With that background, it appears (take this with a grain of salt because TC2000 is acting up this morning) that all three major index ETFs gapped lower to start the premarket. However, all three have put in strong while candles in the early session. As a result, SPY and DIA look dead flat while QQQ is down just less than a quarter of a percent. All three remain above their T-line (8ema) and very near all-time highs. So, the Bulls are still in control of the trend in the short term and the longer term. In terms of extension, This morning’s premarket action seems to have eliminated its over-stretch from the 8ema while the SPY and DIA are within normal distance from the T-line. The T2122 indicator is near its overbought range, but remains just inside its midrange. So, once again, both sides have slack to work with if they can gain enough momentum to do it. With that said, given Thursday’s very good economic data (growth with falling inflation) the risk remains on the side of a move lower (if PCE data disappoints by coming in hot). Continue to keep watching those Tech Big Dogs. If they make a move as a group, it is almost impossible for the rest of the market to do anything but follow given their trading volumes. Finally, remember it’s Friday. Pay yourself and prepare your account for the weekend.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Wednesday gave us a gap higher and then a fade. SPY opened 0.60% higher, DIA gapped up 0.31%, and QQQ gapped up 0.96%. After that open, all three major index ETFs meandered back and forth around that open level until 1 p.m. At that point, we saw profit taking sell off the market the rest of the day. This action gave us gap-up, black-bodied candles in all three. All three had higher upper wicks than lower (DIA’s version was mostly body). While all three also remain above their T-line, DIA is not far above even as QQQ is even more stretched after that morning gap. This all happened on average volume.

On the day, seven of the 10 sectors were in the red with Energy (+1.04%) way out in front leading the gainers. At the same time, Utilities (-1.35%) and Communications Services (-1.35%) were by far the worst-performing sectors. Meanwhile, the SPY gained 0.11%, DIA lost 0.25%, and QQQ gained 0.55%. Meanwhile, VXX gained 2.63% to close at 14.45 and T2122 dropped but remained in its midrange at 35.98. 10-year bond yields spiked up to 4.18% and Oil (WTI) gained 1.36% to close at $75.38 per barrel. So, markets gapped higher on Chinese stimulus and a great earnings report (which included their report that orders have TRIPLED in the last quarter by ASML). However, at that point, traders started having second thoughts based on being extended and also on the breadth of the rally (being mostly led by the 10 big dog tech stocks).

The major economic news on Wednesday was limited to S&P Global Manufacturing PMI, which came in well above expectations at 50.3 (compared to a forecast and Dec. value of 47.9). At the same time, the S&P Global Services PMI also came in higher than was predicted at 52.9 (versus a forecast of 51.0 and the December reading of 51.4). This gave us an S&P Global Composite PMI of 52.3 (compared to the Dec. reading of 51.4). Later the EIA Crude Oil Inventories showed a much bigger drawdown than anticipated at -9.233 million barrels (compared to a forecast of -2.150 million barrels and the prior week’s -2.492 million barrels).

After the close, AMP, CNXC, CCI, CSX, IBM, LRCX, PKG, RJF, RMD, STX, NOW, URI, and WRB all reported beats on both the revenue and earnings lines. At the same time, COLB, LVS, SLM, and TSLA all beat on revenue while missing on earnings. On the other side, PLXS beat on revenue while missing on earnings. Unfortunately, CACI, HXL, KNX, LVRO, and LBRT missed on both the top and bottom line. It is worth noting that CNCX, HXL, KNX, PLXS, and SLM all lowered their forward guidance. It is also worth noting that TSLA (one of the biggest dogs in terms of dollar value of stock traded) warned of a slowdown in the year ahead.

In stock news, the Seattle Times reported Wednesday that BA (not SPR) was the one that reinstalled the panel the explosively left the ALK 737 MAX 9 jet during flight. The paper said the claims were confirmed by an anonymous whistleblower. Later, C said that the 5,000 employees it has laid off since the start of the year will be paid through April. At the same time, STLA announced it had acquired British AI technology firm CloudMade for an undisclosed amount. Later, a DAL flight using a BA 757 jet lost its nose wheel as the plane was lining up to take off in Atlanta Monday, but the FAA notice on the event was not posted until Wednesday. At the same time, CG announced it is buying a $415 million student loan portfolio from TFC. Later, Reuters reported that GM will invest $1.4 billion in Brazil over the next four years. At the same time, Reuters reported the TSN has dropped CVS as its pharmacy benefits manager in favor of a startup. (CVS, CI, and UNH currently control 80% of that pharmacy benefits market.) Elsewhere, NVDA (chipmaker) and EQIX (data center provider) announced they are partnering to offer supercomputing systems to the corporate world. (This service is meant to compete with AMZN and MSFT cloud computing offerings.) At the same time, SPOT announced they will launch in-app purchases on iPhones as soon as EU laws take effect forcing AAPL to allow this on March 7. Later, BA announced they had delivered the first 737 MAX 8 jet to China since the early 2019 grounding of those planes. After the close, F said it expects to see a $1.7 billion pre-tax loss related to employee pension and other post-retirement benefits restatements. Also after the close, TSLA said it will start making a new model of EV in the second half of 2025. The new car will be a smaller crossover aimed at the mass market. (TSLA is notorious for missing its production date promises by years.)

In stock legal, governmental, and regulatory news, LEVI filed suit against Italian luxury brand Brunello Cucinelli claiming trademark infringement. At the same time, India company Zee Entertainment urged SONY to honor their $10 billion merger agreement after SONY had announced the termination. Zee also filed suit in India, asking the court to force SONY to honor the deal and saying negotiations had taken two years. Later, the NHTSA announced that F has agreed to recall 2.24 million older Explorer SUVs (2011 – 1019 models) related to panel trim clips that were not installed properly. At the same time, court filings show that GOOGL reached a $1.67 billion AI chip patent infringement settlement with Singular Computing, just as the trial’s closing arguments were scheduled to begin. Elsewhere, EU governments and lawmakers have agreed in principle to terms that would allow them to force European companies to prioritize the production of certain key products to prevent a supply chain crisis. The laws are meant to reduce the impacts of events like the COVID pandemic or the Russian invasion of Ukraine. The European Commission would be the group vested with the power to make such decrees. Later, in details of the ADM accounting investigation, it was reported that ADM senior executives’ bonuses were tied to the performance of that company’s minor nutrition unit. (The nutrition unit contributed less than 10% of the company’s revenue.) Meanwhile, the Biden Administration urged Congress to approve the sale of LMT F-16 fighter jets to Turkey following a 20-month delay after that country’s parliament approved the entry of Sweden into NATO. At the same time, President Biden vetoed legislation that would have blocked a waiver granted for government-funded EV charging stations. (The waiver allows the stations to not be “entirely” manufactured in the US. It approves stations with more than 55% US materials and manufactured products.) After the close, the FAA lifted its restrictions on BA 737 MAX 98 planes flying, if the plane has passed inspection. This will be the first flight of the plane since the January 6 suspension. However, at the same time, the FAA halted BA production expansion for 737 MAX planes of all types until compliance and quality control procedures are resolved.

Overnight, Asian markets were mixed but leaned toward the green side led by a strong move in China. Shanghai (+3.03%), Shenzhen (+2.01%), and Hong Kong (+1.96%) led the region higher. In Europe, we see the opposite picture taking shape as all but 3 of the exchanges are in the red at midday. The CAC (-0.50%), DAX (-0.44%), and FTSE (-0.17%) are leading the region lower in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a flat start to the day (ahead of data). The DIA implies a +0.02% open, the SPY is implying a +0.06% open, and the QQQ implies a +0.13% open at this hour. At the same time, 10-year bond yields are down slightly to 4.17% and Oil (WTI) has popped up 1.13% to $75.95 per barrel in early trading.

The major economic news scheduled for Thursday includes Building Permits, Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, Dec. Durable Goods Orders, Q4 GDP, Q4 GDP Price Index, Dec. Goods Trade Balance, and Dec. Retail Inventories (all at 8:30 a.m.), Dec. New Home Sales (10 a.m.), and Fed Balance Sheet (4:30 p.m.). The major earnings reports scheduled for before the open include ALK, AAL, AIT, BX, BFH, CRS, CMCSA, CFR, DOW, EXP, HUM, HZO, MMC, MKC, MBLY, MUR, NEE, NOK, NOC, ORI, BPOP, SDVKY, SHW, LUV, STM, UNP, VLO, VLY, XEL, and XRX. Then, after the close AJG, COF, INTC, KLAC, LHX, LEVI, OLN, TMUS, V, WAL, WDC, AND WY report.

In economic news later this week, on Friday, we get the Dec. Core PCE Price Index, Dec. PCE Price Index, Dec. Personal Spending, and Dec. Pending Home Sales.

In terms of earnings reports later this week, on Friday, AXP, ALV, BAH, CL, FCNCA, GNTX, and NSC report.

In miscellaneous news, the US Navy intercepted multiple missiles fired by Yemeni Houthi rebels on Wednesday as they escorted AMKAF (Maersk) ships in the Red Sea. (The ships were carrying US military supplies according to Maersk.) Elsewhere, CSX reported a 13% drop in Q4 profits, which the company blamed on the loss of margin from its fuel surcharges (which the railroad can no longer charge now that fuel costs have fallen). Meanwhile, former St. Louis Fed President Bullard (a mega hawk) hinted in an interview Wednesday that the FOMC may cut rates in March, even if inflation has not yet hit the 2% target. (While no longer a Fed member, Bullard is widely seen as in the know and has always been hawkish. If he hints at a March cut, that may mean the Doves are being more forceful in behind-the-scenes talks.)

In Fedwatch news, Fed Funds Futures (of the probability of a first rate cut) show only a 1.6% probability of a cut next week. That probability rises to 41.9% in March, 100% by May, (oddly) back to 98.8% by June, and 99.9% by July. The other three meetings in 2024 all show a 100% probability of Fed having made its first rate cut. Of course, these are trader bets and do not necessarily match what the Fed will do.

So far this morning, ALK, AAL, AIT, BFH, CNX, DOW, EXP, MMC, NOC, BPOP, SHW, and LUV all reported beats on both the revenue and earnings lines. Meanwhile, BANC, HUM, HZO, ORI, VLY, and VIRT all beat on revenue while missing on earnings. On the other side, BX, MKC, MBLY, STM, and VLO all missed on revenue while beating on earnings. Unfortunately, MUR, NOK, SDVKY, XEL, and XRX missed on both the top and bottom lines. It is worth noting that, XRX, MBLY, HZO, and HUM lowered their forward guidance while AAL raised its guidance.

With that background, all three major index ETFs seem to be waiting on the data dump at 8:30 a.m. The SPY is giving us an “inside candle” Doji so far in the premarket while QQQ is giving us a Bullish Harami Spinning Top. DIA is the lone black body candle in the early session, but even so, it is an inside candle. All three remain above their T-line (8ema) and very near all-time highs. So, obviously, the Bulls are still in control of the trend in the short term and the longer term. In terms of extension, the QQQ is still stretched above its T-line withe the SPY getting a bit stretched and DIA just above its own 8ema. The T2122 indicator is also still in its midrange. So, both sides have room to run if they can gather the momentum to do it. With that said, the risk is of a move lower on data the disappoints. As I’ve been saying for some time, keep watching those Big Dogs. If they make a move as a group, it is almost impossible for the rest of the market to do anything but follow given their trading volumes. As of 7:45 a.m., TSLA is getting hammered after yesterday’s earnings miss. However, the rest of the Big Dogs are mixed and lean toward the green side.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Markets were undecided on Tuesday with SPY opening 0.12% higher, DIA opening 0.17% lower, and QQQ opening 0.17% higher. From that point, SPY and QQQ traded sideways, wandering back and forth across the open gap until noon. DIA also traded sideways in a very tight range along the open for 60 minutes. Then DIA sold off for 90 minutes before resuming its sideways trading. Then, at noon, all three major index ETFs made a modest (20-degree) rally the rest of the day. This left all three as indecisive candles. SPY and QQQ both printed white-bodied Inside Day Hammer candles. At the same time, DIA printed a gap-down, black-bodied Doji-type candle. All three remain above their T-line (8ema). This all happened on slightly above-average volume in DIA and QQQ and slightly below-average volume in the SPY.

On the day, seven of the 10 sectors were in the green with Communication Services (+1.30%) way out in front leading the way higher. At the same time, Financial Services (-0.14%) and Industrials (-0.10%) were the worst-performing sectors. Meanwhile, the SPY gained 0.29%, DIA lost 0.27%, and QQQ gained 0.41%. Meanwhile, VXX was off by 2.90% to close at 14.08 and T2122 climbed a bit but remained in the upper side of its midrange at 73.33. 10-year bond yields climbed back to 4.136% and Oil (WTI) fell just a bit to close at $74.50 per barrel. So, after a mixed, flat open the market was pretty much undecided and lethargic on the day. The Bulls had a slight advantage for the afternoon. (It is worth noting that the big Tech names were all green but only ranged from INTC (+1.39%) to AMD (+0.14%).

The major economic news on Tuesday was limited to the API Weekly Crude Oil Stocks report, which showed a significantly larger drawdown than expected at -6.674 million barrels (compared to a forecasted 3.000-million-barrel drawdown and the prior week’s 0.483-million-barrel increase).

In Fed news, on Tuesday, Reuters provided a summary of the FOMC voters’ most recent statements. However, note that some of these quotes are older than others. Atlanta Fed President Bostic (dove) said, “If we continue to see a further accumulation of downside surprises in the data it’s possible for me to get comfortable to advocate normalization sooner than the third quarter. But the evidence would need to be convincing.” NY Fed President Williams (centrist) said, “It will only be appropriate to dial back the degree of policy restraint when we are confident that inflation is moving toward 2% on a sustained basis.” Fed Governor Waller (centrist) has said, “The key thing is the economy is doing well. It is giving us the flexibility to move carefully and methodically.” Fed Vice-Chair Barr (centrist) has said, “The Fed is at or near the peak of interest rates.” Fed Vice-Chair Jefferson said, “We are in a sensitive period of risk management, where we have to balance the risk of not having tightened enough, against the risk of policy being too restrictive.” Fed Governor Cook (centrist) has said, “I see risks as two-sided, requiring us to balance the risk of not tightening enough against the risk of tightening too much.” San Francisco Fed President Daly recently said, “It takes patience. It takes gradualism.” Cleveland Fed President Mester (hawk) said, “March is probably too early in my estimation for a rate decline.” Richmond Fed President Barkin (hawk) said, “Getting inflation under control is critically important.” Fed Governor Bowman (hawk) said, “While the current stance of monetary policy appears to be sufficiently restrictive … I remain willing to raise the federal funds rate further at a future meeting.” Finally, Fed Chair Powell (centrist) said, “Declaring victory would be premature … But of course the question is when will it become appropriate to begin dialing back?”

After the close, CNI, EWBC, ISRG, LRN, and TXN all reported beats on both the revenue and earnings lines. At the same time, BKR missed on revenue while beating on earnings. On the other side, NFLX and STLD both beat on revenue while missing on earnings. It is worth noting that NFLX raised forward guidance while TXN lowered its guidance.

In stock news, FSR said Tuesday that it expects to deliver the remaining 5,000 vehicles produced in 2023 by the end of Q1, through its new network of 100 dealers in the US, Canada, and Europe. At the same time, in addition to its earnings, NFLX announced a $5 billion, 10-year deal to broadcast WWE’s weekly program. Later, SNY agreed to buy INBX in a stock and cash deal worth $2.2 billion. Elsewhere, GOLD announced that it is accelerating the expansion of its copper mine in Zambia. This will make that mine one of the largest copper mines in the world. At the same time, PLUG announced its Georgia “green hydrogen” (liquid hydrogen) plant is now operational. Later, LUV flight attendants voted to authorize a strike by at 98% margin. Meanwhile, UAL said it is no longer counting on BA’s 737 MAX 10 jets. This announcement comes after more BA delays and plane groundings have pushed back delivery schedules that were already years behind schedule. While UAL did not cancel its orders (at least yet), the airline has removed those planes from its internal plans, saying it believes recent production quality issues will delay certification yet another year. At the same time, Bloomberg reported that AAPL has reduced the number of features and delayed the release of its “Apple Car” until at least 2028. (AAPL had previously announced it would develop an autonomous self-driving car by 2026. The original plan was for a level 4-5 self-driving capability. The new plan is for level 2+.) After the close, SAP announced a restructuring that will “impact” 8,000 employees worldwide. Some of the job cuts will be implemented through voluntary leave programs while many other employees will be “reskilled and transferred” within the company. Also after the close, Bloomberg reported that WBA is exploring the sale of its “Shields Health Solutions” unit for roughly $4 billion. Finally, EBAY announced Tuesday evening that it will lay off 9% of its workforce or about 1,000 employees.

In stock government, legal, and regulatory news, the Dept. of Justice requested data from SIX and FUN related to their merger (announced in November). Later, the FDA asked drugmakers GILD, JNJ, BMY, LEGN, and NVS to add a serious warning label to their cancer therapies that use “CAR-T” technology. (This comes after recent reports of patients treated with genetically engineered CAR-T technologies developing different cancers than the one the drug was treating.) Later, AAPL asked a British Competition Tribunal to throw out a $1 billion class-action type lawsuit brought by more than 1,500 app developers alleging AAPL’s 30% fee and monopoly on iPhone app stores are anti-competitive. At the same time, JNJ announced it has reached a tentative settlement to resolve investigations by 42 states and the District of Columbia into whether the company misled consumers about the safety of its talc products. Later, the Wall Street Journal reported that the settlement included a $700 million payment. The CEO of ALK told NBC news that the company had reported finding many BA 737 MAX 9 planes with loose bolts to the FAA and Dept. of Transportation. At the same time, ADM was hit with an accounting probe. This caused ADM shares to plummet 24% on Monday, rebounding slightly (+1.20%) on Tuesday. Later, NMR was sued by a former employee, claiming she was paid less relative to men, and was fired for insisting that the company stop discriminating against women. After the close, CACI was awarded a US Army contract for $900 million. Also after the close, BA announced its CEO will meet with US Senators who are investigating the ALK airline mid-air panel blowout and loose bolts. Finally, an Oregon jury ordered a subsidiary of BRKB to pay $62.3 million to nine property owners whose properties were damaged by wildfires found to have been caused by the company’s negligence in dealing with power lines. (This is the first of many trials from 5,000 home and business owners whose properties were damaged by the 2020 fires.)

Overnight, Asian markets were mostly green, with Japan (-0.80%) and South Korea (-0.36%) the only red in the region. Meanwhile, Hong Kong (+3.56%), Thailand (+1.82%), and Shanghai (+1.80%) led the nine gainers. (China roared back after the PBOC announced policy easing in an attempt to boost their economy.) In Europe, we see a similar picture with only Russia (-0.59%) and Norway (-0.09%) in the red. At the same time, The CAC (+0.90%), DAX (+1.27%), and FTSE (+0.39%) lead the region higher. In the US, as of 7:30 a.m., Futures are pointing toward a gap higher to start the day. The DIA implies a +0.22% open, the SPY is implying a +0.43% open, and the QQQ implies a +0.70% open at this hour. Meanwhile, 10-year bond yields are down to 4.107% and Oil (WTI) is off a quarter of a percent to $74.18 per barrel in early trading.

The major economic news scheduled for Wednesday includes S&P Global Mfg. PMI, S&P Global Services PMI, S&P Global Composite PMI (all at 9:45 a.m.), and EIA Crude Oil Inventories (10:30 a.m.). The major earnings reports scheduled for before the open Wednesday include ABT, APH, ASML, T, BOKF, ELV, FCX, GD, KMB, EDU, PGR, SAP, TEL, TDY, and TXT. However, after the close, AMP, CACI, COLB, CNXC, CCI, CSX, HXL, IBM, KNX, LRCX, LVS, LVRO, LBRT, PKG, PLXS, RJF, RMD, STX, NOW, TSLA, URI, and WRB report.

In economic news later this week, on Thursday, Building Permits, Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, Dec. Durable Goods Orders, Q4 GDP, Q4 GDP Price Index, Dec. Goods Trade Balance, Dec. Retail Inventories, Dec. New Home Sales, and Fed Balance Sheet are reported. Finally, on Friday, we get the Dec. Core PCE Price Index, Dec. PCE Price Index, Dec. Personal Spending, and Dec. Pending Home Sales.

In terms of earnings reports later this week, on Thursday, we hear from ALK, AAL, AIT, BX, BFH, CRS, CMCSA, CFR, DOW, EXP, HUM, HZO, MMC, MKC, MBLY, MUR, NEE, NOK, NOC, ORI, BPOP, SDVKY, SHW, LUV, STM, UNP, VLO, VLY, XEL, XRX, AJG, COF, INTC, KLAC, LHX, LEVI, OLN, TMUS, V, WAL, WDC, AND WY. Finally, on Friday, AXP, ALV, BAH, CL, FCNCA, GNTX, and NSC report.

In miscellaneous news, on Tuesday, BAC analysts reported that hedge funds were net buyers of stocks last week for the first time in 10 weeks. The analysis said that the net was $554 million of stock added to hedge fund portfolios. Elsewhere, bond icon Bill Gross told Bloomberg that the Fed needed to end Quantitative Tightening and begin cutting rates soon. Gross said the window to do this (to preserve the soft landing) was this year. Later, Bloomberg reported that India’s stock market has surpassed Hong Kong’s market (by $4.33 trillion versus $4.29 trillion). This makes India the fourth largest stock market globally, behind the US, China, and Japan. (Hong Kong, France, and the UK follow those top four.) Finally, TM Chairman Toyoda told an interview Tuesday that he believes electric-only vehicles will reach a maximum of 30% of the market, with the rest of the market made up of hybrid, hydrogen, and traditional-fuel cars. Part of his reasoning was explained that 1 billion people in the world still live without electricity (and many, many more without reliable electricity), which makes EV cars a non-starter for that portion of the world.

So far this morning, ABT, ASML, ELV, EDU, and SF all reported beat on both the revenue and earnings lines. Meanwhile, T and SAP both beat on revenue while missing on earnings. On the other side, TXT, TDY, and TEL missed on revenue while beating on earnings. Unfortunately, KMB and GD missed on both the top and bottom lines. It is worth noting that ELV and EDU both raised forward guidance while ASML, T, and KMB lowered guidance.

With that background, all three major index ETFs gapped higher to start the premarket session. All three are also printing white-bodied candles, which although small, are at the top of their range so far in the early session. The SPY, DIA, and QQQ remain above their T-line (8ema) and sitting at (or near in the case of DIA) all-time highs. So, obviously, the Bulls are in control of the trend in the short term. In the longer term, we are also clearly bullish in all three. In terms of extension, the QQQ is stretched above its T-line after the premarket gap, while the other major index ETFs are still inside the normal range. The T2122 indicator is also still sitting in its midrange. So, both sides have room to run if they can gather the momentum to do it. As I’ve been saying for some time, keep watching those Tech Big Dogs. If they make a move as a group, it is almost impossible for the rest of the market to do anything but follow given their trading volumes. As of 7:45 a.m., all of them are looking to gap higher and all but two of them are printing white-bodied premarket candles.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Equity markets ended the day mixed but mostly higher with the DIA finishing lower while SPY and QQQ shook off some early selling to resume the push higher. A strong showing on Netflix after the bell sets the stage for yet another gap to open the scoring tech sector. Today we have Mortgage Apps, PMI, Petroleum, and bond auctions as well as a significant increase in earnings events so expect heightened price volatility as traders react. Also, keep in mind we have the possibility of some big point moves with key economic data coming Thursday and Friday before the bell so carefully plan accordingly.

Overnight Asian markets closed mixed but mostly higher as Hong Kong surged 3.56% and the Shanghai exchange enjoyed a needed relief rally. European markets are decidedly bullish this morning in reaction to PMI data showing an improvement in economic activity. The strong NFLX report after the bell yesterday sets up another gap open as index futures push higher ahead of earnings and economic reports.

Netflix warned its users and investors that it will increase its prices in the future, according to its quarterly investor letter. The company said that it needs to raise its prices to invest more in original and licensed content, as well as to improve its technology and user experience. Netflix also announced that it signed a deal to add 10 years of WWE’s Raw, a popular wrestling show, to its content library. Netflix has not changed the price of its ad tier, which costs $6.99 per month, since it introduced it in 2022. The company reported strong growth in its subscriber base in the fourth quarter of 2023. The company added 13.1 million new subscribers, beating its forecast of 11.5 million. The company now has 260.8 million paid subscribers worldwide, up 18% from a year ago. Netflix also exceeded Wall Street’s revenue estimates, posting $9.9 billion in revenue, up 21% year-on-year. The company attributed its success to its diverse and high-quality content offerings, as well as its global expansion strategy.

Despite surpassing market forecasts on both revenue and profit, ASML, the world’s leading supplier of lithography machines for chipmaking, warned that its sales growth would stall in 2024. The Dutch company, whose products are essential for producing the most advanced semiconductors, has been affected by the escalating tensions between the U.S. and China over technology trade and security. Earlier this month, ASML revealed that the Dutch government had restricted its exports of its latest NXT:2050i and NXT:2100i models to China last year, amid pressure from the U.S. to limit China’s access to cutting-edge chip technology.

The Federal Aviation Administration (FAA) has initiated a probe into Boeing’s aircraft manufacturing practices after a serious incident involving an Alaska Airlines flight. A door panel detached from the plane’s fuselage during the flight, causing a loud bang and a loss of cabin pressure. No one was injured, but the flight had to make an emergency landing. FAA Administrator Mike Whitaker said that the agency had sent several inspectors to Boeing’s factories to conduct a thorough examination of its quality control and safety standards. He said that the FAA was moving away from relying on Boeing’s self-audits and towards a more hands-on approach.

The stock market ended the day mixed but mostly higher, as the tech titans shook off early selling to resume the chase higher. The sectors of consumer goods and telecoms led the gains in the S&P 500, thanks to the impressive quarterly results of P&G and Verizon. The gap between the long-term and short-term Treasury yields widened today, as the 10-year yield climbed to about 4.14% and the 2-year yield dropped to 4.38%. Today the number of earnings ramped up significantly so expect some price volatility as traders react the the substantial amount of data. For the first time this week, we will also have the economic calendar providing some inspiration for the bulls or bears, with Mortgage Apps, PMI Composite, Petroleum Status, Business Uncertainty, and bond auction results. That said keep in mind Thursday morning brings us a slew of market-moving economic reports before the bell so plan your risk accordingly as big point moves are possible.

Wanting to follow through with Friday’s record-breaking surge, Monday began with another substantial gap as the chase higher continues. However, the momentum seemed to fad rather quickly with investors perhaps showing a little caution with key inflation data coming Thursday morning. Today will be all about the earnings results as the number of reports ramps up which will capped by the highly anticipated Netflix report after the bell. Be prepared as price volatility typically picks up during the bulk of earnings and there are some big point moves possible so plan carefully.

While we slept Asian markets reversed early losses to close mostly higher as China mulls a massive stock market rescue package as disinflation and consumer weakness grow. European markets trade flat to slightly bearish this morning resting after recent gains. U.S. markets also suggest a mixed but rather flat open coming off of overnight lows with a busy day of earnings ahead.

China’s economic outlook is bleak, according to Shaun Rein, founder of the China Market Research Group, who has been living in China for 27 years. He told CNBC on Monday that he has never seen such low confidence among consumers and businesses in China. He predicts that China will go through at least another 3-6 months of economic hardship, as it struggles to rebound from the impact of Covid-19. China, the second-largest economy in the world, has failed to meet its growth expectations in 2023, despite lifting pandemic restrictions.

The Fed’s Office of Inspector General released a report on Monday that criticized the trading activities of two former regional presidents, Robert Kaplan of Dallas and Eric Rosengren of Boston. The report found that their trades, which involved stocks, bonds, and futures, created conflicts of interest that compromised their independence and integrity as central bank officials. The report also said that their actions violated the Fed’s code of conduct and ethics policies, and undermined the public’s trust in the Fed.

The SEC, the U.S. regulator of the securities markets, revealed that a SIM swap attack was behind the hacking of its official account on X, a social media platform. On Jan. 9, a hacker managed to take over the @SECGov account and posted a false message saying that the SEC had approved the first spot bitcoin ETFs, which are funds that track the price of bitcoin and trade on the spot market. The hacker was able to do this by swapping the SIM card of the phone number linked to the account and resetting the password. The SEC admitted that it did not have two-factor authentication enabled, which would have added an extra layer of security to the account.

The stock market kicked off the week bullish with another substantial gap up but then struggled to continue the upward perhaps acknowledging the uncertainty of the inflation data later this week. Bond yields have also nudged higher suggesting some concern and caution by investors about the pending Thursday data. The Nasdaq has gained about 2.0% since the start of the year, mostly due to the Magnificent 7 stocks (Apple, Microsoft, Google, Amazon, Tesla, NVIDIA, and Meta) which have increased by an average of 3.9%. However, the Russell 2000 small-cap stock index has fallen by over 3.0% this year, even though it had more strength at the end of 2023. With very little to nothing on the economic calendar today investors will be looking to the growing list of earnings reports for inspiration. The Netflix report will be of particular interest after the bell today. Earnings typically mean a ramp up of price volatility so plan your risk accordingly.

All that pushing and shoving by the tech giants finally got the job done as the S&P 500 broke out joining the DIA and QQQ with nothing but blue sky above. Unfortunately, the IWM does not benefit from big tech and continues to lag way behind the other indexes still in a short-term downtrend. That said with a light day on the earnings and economic calendars I would expect the fear of missing out trade to push indexes higher. However, keep in mind that the Thursday GDP and Friday Core PCE nears, bullish momentum could fade into some uncertainty ahead of the data.

Overnight Asian markets traded mixed with Japan hitting 33-year highs as China led the selling down 2.68%. European markets started the week off bullishly mostly green following the Friday surge higher. U.S. futures also point to bullishness wanting to extend the Friday break out with the tech titans leading the way with great anticipation of their pending earnings.

Economic Calendar

Earnings Calendar

Notable reports for Monday include AGYS, AGNC, BRO, IBTX, TFII, UAL, & ZION.

News & Technicals’

Buy now, pay later, a service that allows online shoppers to split their purchases into interest-free installments, boosted online sales to a new high during the holiday season, growing by 14% compared to the previous year. However, many consumers are facing difficulties in paying off their bills, as they are already burdened by record-high credit card debt and rising delinquency rates. The frequency of buy now, pay later defaults is not clear, but the users of the service are more prone to miss payments on other credit products, such as car loans or mortgages.

Moody’s Investors Service has a pessimistic view of the credit quality of APAC countries in 2024, as China’s economic growth decelerates and funding and geopolitical challenges increase. The credit rating agency said that China’s growth slowdown has a large impact on APAC economies, as they are closely linked to China’s role in global trade. It also said that the global liquidity situation, which depends on the Fed’s policy stance, is another factor that affects the credit outlook. The agency expects the Fed to keep its policy tight until the middle of the year, which could limit the availability of funds for APAC countries.

The new year has brought more job losses for many workers, even as the economic indicators show signs of improvement. Inflation has eased, unemployment has fallen, and recession fears have faded, but many big companies are still downsizing their workforce. However, the layoff strategies vary among different companies. Some companies are opting for a one-time, large-scale cut, while others are preferring a gradual, phased-out approach. The reasons for these different methods may depend on the company’s financial situation, industry outlook, and employee morale.

The stock market closed with a huge surge, as the S&P 500 broke out and finally reached a new all-time high joining the DIA and QQQ. However, the IWM continues to lag substantially behind without the benefit of the tech giants. The technology sector was the best performer, with semiconductor stocks boosting the sector after Taiwan Semiconductor Manufacturing Corp. (TSMC), a major chipmaker, posted better-than-expected results, and its shares jumped more than 6%. Today we have a very light economic calendar with a few notable reports but I would expect the fear of missing out on trade to continue this upside breakout at least until we get the next reading on the GDP on Thursday morning. Stay with the trend and enjoy the ride but keep in mind that valuations are very frothy so watch for hints of trouble along the path.

The Bulls were in control from the jump on Friday. SPY gapped up 0.26%, DIA opened 0.28% higher, and QQQ gapped up 0.51%. From that point, all three major index ETFs rallied steadily higher before plateauing in the last 90 minutes of the day, near their highs. This action gave us gap-up, large, white-bodied candles in the SPY, QQQ, and DIA. All three closed at new all-time high closes after printing new all-time highs during the day. SPY and QQQ have almost no wicks while DIA had some wick on both ends. That meant that all three were above their T-lines (8ema). This all happened on slightly above-average volume in DIA and QQQ and slightly below-average volume in the SPY.

On the day, all 10 sectors were in the red with Utilities (-1.36%) out in front leading the way lower. At the same time, Consumer Defensive (-0.40%) and Financial Services (-0.46%) held up better than the other sectors. At the same time, the SPY lost 0.56%, DIA lost 0.25%, and QQQ lost just 0.56%. Meanwhile, VXX gained 3.65% to close at 15.92 and T2122 dropped even further into the oversold territory at 6.25. 10-year bond yields climbed to 4.102% and Oil (WTI) rose 0.60% to close at $72.83 per barrel. So, after a significant gap lower, Mr. Market was indecisive with a very modest bias toward the bullish side. This happened on less-than-average volume in the SPY, and average volume in both the QQQ and DIA.

On the day, nine of the 10 sectors were in the green with Technology (+2.00%) way out in front leading the way higher. At the same time, Consumer Defensive (-0.29%) was by far the worst-performing sector and the only one in the red. Meanwhile, the SPY gained 1.25%, DIA gained 1.01%, and QQQ gained 1.98%. Meanwhile, VXX fell 2.53% to close at 15.00 and T2122 climbed back up into the upper side of its midrange at 69.04. 10-year bond yields spiked to 4.13% and Oil (WTI) fell 0.50% to close at $73.71 per barrel. So, after a significant gap higher at the open, Mr. Market was dead set on achieving that all-time high in the SPY, led by the AI-crazed Tech big dogs (AMD was up 7.11%, NVDA up 4.17%, INTC up 3.03%, GOOGL up 2.02%, META up 1.95%, AAPL up 1.55%, MSFT up 1.22%, and AMZN up 1.20%). Even beleaguered TSLA gained 0.15%.

The major economic news on Friday included December Existing Home Sales, which came in a bit lower than expected at 3.78 million (versus a forecast and November value of 3.82 million). On a month-on-month basis, that was a 1.0% decline compared to a forecasted +0.3% and the prior month’s +0.8%. At the same time, Michigan Consumer Sentiment was stronger than anticipated at 78.8 (versus a 70.0 forecast and December’s 69.7). Meanwhile, Michigan Consumer Expectations also far exceeded the predictions at 75.9 (compared to a 67.0 forecast and a 67.4 December reading). At the same time, the Michigan 1-Year Inflation Expectations were down at 2.9% (versus the forecast and prior value of 3.1%). On a 5-year outlook, the Michigan Consumer Inflation Expectations also came in lower than expected at 2.8% (compared to a 3.0% forecast and the previous reading of 2.9%).

In Fed news, San Francisco Fed President Daly said Friday that she believes FOMC policy “is in a good place” now and that risks have become more balanced. She said, “We have to calibrate very carefully to ensure that we continue to bring inflation down and we ensure that we do it gently, as gently as we possibly can.” Daly went on to say, “The risks to the economy are balanced, and the risks to both sides of our mandate are balanced.” She concluded by saying, “So while I think it’s appropriate for us to look forward and ask when would policy adjustments be necessary so we don’t put a stranglehold on the economy, it’s really premature to think that that’s (speaking of rate cuts) around the corner.”