Some of the shine of the relentless bullish rally quickly faded yesterday as the inflation report surprised to the upside dashing hopes of rate cuts early this year. Treasury yields surged higher with 10-year coming near this year’s high spiking the VIX sharply as investors grappled with high stock valuations in light of the new data. Plan for price volatility to be high as we deal with a significant number of earnings reports, Mortgage Apps, Petroleum Status, and Fed Speakers. With a very busy economic calendar on Thursday and the uncertainty of the pending PPI Report on Friday be prepared for challenging price action as we head for a 3-day weekend.

Overnight Asian markets that were not closed for the Lunar Holiday closed lower in reaction to the U.S. inflation data. However, European markets trade modestly higher this morning after the U.K. reported their inflation of 4% even with their last reading. The U.S. futures also look higher this morning trying to relive some of the painful decline of yesterday ahead of earnings and economic data.

Lyft, a ride-hailing company, saw its stock price surge by 16% in premarket trading on Wednesday after it reported better-than-expected results for the fourth quarter of 2023. However, the company also admitted that it made a serious mistake in its press release, which overstated its earnings outlook for 2024. The company initially said that it expected its adjusted earnings margin to grow by 5% in 2024, but later corrected it to 0.5%. The company apologized for the error and said it was due to a typo.

Airbnb, the online platform for renting and booking accommodation, delivered a strong performance in the fourth quarter of 2023, surpassing analysts’ expectations. The company reported $2.22 billion in revenue, up 22% year-over-year, and said that its guest demand was robust despite the pandemic. Airbnb also expressed confidence in its outlook for the first quarter of 2024, projecting a revenue growth of 25% to 30%. The company attributed its success to its resilience, innovation, and diversification of its offerings.

The U.K. inflation rate remained unchanged at 4% in January, as the cost of furniture and household goods, food, and non-alcoholic drinks eased. However, the core CPI measure, which strips out the volatile components of food, energy, alcohol, and tobacco, was still high at 5.1%, slightly below the expected 5.2%. According to Marion Amiot, a senior European economist at S&P Global Ratings, this reflects the tightness of the labor market, which is driving up wages and inflation, especially in the service sector.

The stock market plunged on Tuesday, but recovered some losses by the end of the day, as the January U.S. CPI inflation report surprised to the upside. Annual inflation was 3.1%, higher than the expected 2.9%, and disappointing the market, crushing rate cut anticipations. Treasury bond yields were up sharply, with the 10-year Treasury yield rising by 0.13% to around 4.31%, close to its yearly peak. This also weighed on stock indexes, which fell by more than 1% each. The Nasdaq, which has more technology stocks, trailed the wider S&P 500, dropping by about 1.8%. The VIX volatility index, which measures Wall Street’s “fear level,” jumped by about 18% to around 16.5. Today traders and investors will have a slew of earnings to navigate along with Mortgage Apps, Fed Speakers, Petroleum Status, and a short-term Bill Auction. However, traders should keep in mind we have a very busy economic calendar on Thursday as well as the uncertainty of the pending PPI report on Friday. Plan for volatility to be high and expect big whipsaws as the market tries to come to grips with the economic reality of the longer-than-hoped-for inflation fight.

The markets opened flat on Monday. SPY opened dead flat, DIA opened down 0.08%, and QQQ opened down 0.03%. From there, all three major index ETFs ground to the side in a tight range for an hour. Then all three rallied modestly for 60 minutes before grinding sideways again for two hours. At that point, all three sold off for 90 minutes (with QQQ giving the steepest selling) only to end the day with another hour of sideways drift in a tight range. This action gave us new all-time highs in all three with DIA also giving us a new all-time high close. However, all three had large upper wicks. The DIA printed a Bullish Engulfing, QQQ printed a Bearish Harami, and SPY gave us a Shooting Star without the gap up. With that said, to me, the biggest thing to take note of were those large upper wicks and far less than average volume in all three of the major index ETFs.

On the day, nine of the 10 sectors were in the green as Energy (+1.16%) and Utilities (+1.14%) led the way higher while Technology (-0.19%) was the only sector lagging in the red. Meanwhile, the SPY lost 0.04%, the DIA gained 0.36%, and QQQ lost 0.39%. VXX gained 2.14% to close at 14.32 and T2122 spiked into the top end of overbought territory at 96.60. 10-year bond yields rose a bit to 4.179% and Oil (WTI) was flat at +0.13% to close at $76.94 per barrel. So, Monday was a dead day in the market with long periods of flat trading and offsetting rises and declines. There were warning signs of exhaustion in the rally with very low volumes and those high wicks. However, an argument can be made that traders were just waiting on the CPI data.

The major economic news released Monday was limited to NY Fed 1-Year Consumer Inflation Expectations, which came in flat from January at 3.00%. Later, the January Federal Budget Balance came in much better than expected at -$22 billion (compared to a -$39.3 billion forecast and December’s massive -$129.0 billion).

In Fed news, Atlanta Fed President Bostic said Monday afternoon that he anticipates that inflation will be near “the low twos” by the end of 2024. Bostic continued, “With that outlook, I really see the first move (rate cut) coming sometime in the summer.”

After the close, ANET, SCI, WTS, and WM all reported beats on both the revenue and earnings lines. Meanwhile, CAR, CDNS, GT, JHX, MEDP, and PFG all missed on revenue while beating on earnings. Unfortunately, BHF and TSE missed on both the top and bottom lines. It is worth noting that MEDP raised its forward guidance while PFG lowered guidance.

In stock news, GILD announced that it had reached an agreement to acquire CBAY for $32.50 per share. (GILD expects the deal to close this quarter.) Later, FANG said it had agreed to buy Endeavor Energy (private) for $26 billion in cash and stock. The deal would make FANG the third-largest oil and gas producer in the Permian Basin (behind XOM and CVX). At the same time, VINO announced it is starting a “strategic asset liquidation” plan. The move is intended to head off what it says is a plan by other companies to drive down their stock price ahead of a takeover bid. Later, MLM said it had agreed to acquire 20 operations in the Southeast US from Blue Water Industries for $2.05 billion. Elsewhere, drivers from UBER, LYFT, DASH, and others announced Monday that they will go on strike on Valentine’s Day to demand fair pay. Later, BB announced it had concluded 200 job cuts in Q4 and is targeting $100 million in added profit from cost savings (from unspecified means) in 2024. At the same time, JBLU shares jumped 15% when reports stated that Carl Icahn had taken a 10% stake in the airline, saying that the stock was “undervalued.”

In stock legal, governmental, and regulatory news, on Monday a federal judge ordered Elon Musk to testify in the SEC probe of his takeover of Twitter (now X). Later, KTOS was awarded a $877 million contract with the “Space Systems Command” (Space Force). At the same time, a federal judge ruled that WMT and ENR must face a lawsuit alleging they violated antitrust laws by conspiring to raise the prices of disposable batteries. Later, the NHTSA said it had closed an investigation into F 2010 Fusion cars related to power steering issues. At the same time, AWK filed an appeal contesting a December ruling. The decision could change the management of water in CA’s Monterey County. Later, in Germany, a ban went into effect against importing, making, or selling INTC server chips which had been found to violate the patent rights of R2 Semiconductors. (This impacts INTC, DELL, HPQ, HPE, etc. who sell INTC server chips in Germany.) At the same time, BRKB-owned Jazwares filed suit against BBW alleging that BBW based its new line of plush animals are knockoffs that infringe on its intellectual property rights. Later, a federal judge blocked an OH law that prevented the access of children 16 and under to META’s Facebook, TikTok, GOOGL’s YouTube, and X without prior parental consent. After the close, the Attorney General of KY filed suit against KR, claiming the company’s pharmacies contributed to the state’s opioid addiction crisis with more than 11% of all opioid pills in the state prescribed by the retailer.

Note that the Chinese markets were closed for Lunar New Year and will stay closed all week as well. Meanwhile, Japan (+2.89%), Malaysia (+1.26%), and South Korea (+1.12%) led the rest of the region higher. In Europe, we see the opposite picture taking shape with all but two of the 15 bourses in the red. The CAC (-0.46%), DAX (-0.57%), and FTSE (-0.30%) lead the region lower in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a gap lower to start the day (ahead of CPI). The DIA implies a -0.20% open, the SPY is implying a -0.46% open, and the QQQ implies a -0.86% open at this hour. At the same time, 10-year bond yields are back to 4.16% and Oil (WTI) is up 0.73% to $77.47 per barrel in early trading.

The major economic news scheduled for Tuesday is limited, but important with Jan. Core CPI and Jan. CPI (both at 8:30 a.m.), and Weekly API Crude Oil Stocks (4:30 p.m.). The major earnings reports scheduled for before the open include AN, BIIB, BRKR, KO, DDOG, ECL, FELE, GFS, HAS, HRI, HWM, INCY, JHX, LCII, LDOS, MAR, TAP, MCO, QSR, SHOP, TRU, WSO, WCC, KLG, and ZTS. Then, after the close, ABNB, AKAM, ALSN, AMX, AIG, BFAM, DVA, ENTG, EQT, GDDY, GXO, IAC, IOSP, CART, INVH, LYFT, MCY, MGM, MRC, NGD, PRI, QDEL, REZI, SSNC, MODG, WCN, WELL, and ZG report.

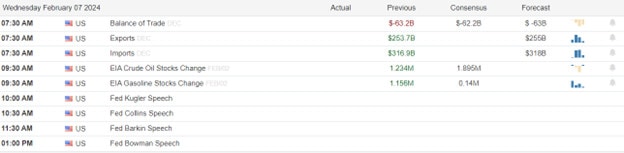

In economic news later this week, on Wednesday EIA Crude Oil Inventories are reported. On Thursday, we get Initial Weekly Jobless Claims, Weekly Continuing Jobless Claims, Jan. Core Retail Sales, Jan. Retail Sales, Jan. Import Price Index, Jan. Export Price Index, NY Empire State Mfg. Index, Jan. Industrial Production, Dec. Business Inventories, Dec. Retail Inventories, the Fed Balance Sheet, and Fed member Bostic speaks. Finally, on Friday, Jan. Building Permits, Jan. Housing Starts, Jan. Core PPI, Jan. PPI, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-Year Inflation Expectations, Michigan 5-Year Inflation Expectations, and Fed member Daly speaks.

In terms of earnings reports later this week, on Wednesday, we hear from AVTR, AVNT, GOLD, BGC, CAE, CRL, CHEF, CME, CNHI, DBD, ES, GNRC, GPN, IQV, KHC, LAD, LPX, MLM, NHYDY, OC, PSN, R, SITE, SAH, SUN, TMHC, WAB, WMB, ALB, ATUS, AWK, AR, APP, ACGL, CF, CC, CSCO, CW, ET, EQIX, HLF, HUBS, KGC, MTW, MFC, OXY, PTEN, CNXN, ROL, SON, SUM, TWLO, TYL, VTR, and WFG. On Thursday, HOUS, ARCH, CBRE, CVE, CRBG, CROX, DE, DNB, EPAM, GTX, GPC, GEO, HBI, H, NSIT, KELYA, KNF, LH, LECO, DNOW, OGN, PBF, PENN, RS, RPRX, SABR, SN, SO, SPTN, STLA, SLVM, TRGP, USFD, VNT, WEN, WST, YETI, ZBRA, AEM, AL, LNT, AMN, AMAT, BIO, BE, ED, DLR, DASH, DKNG, DBX, GLOB, IR, LBTYA, MERC, OPEN, ROKU, TXRH, TOST, TTD, and TROX report. Finally, on Friday, we hear from ACDVF, AXL, CNK, POR, PPL, TRP, THS, and VMC.

In miscellaneous news, C told its bond trading customers to be cautious in their bets on the Fed’s rate easing. The bank recommended trades take a hedged approach to such investments, warning we could see something akin to 1998 when the FOMC did a quick succession of cuts. However, they warn traders to not be surprised if there is a rate hike in the mix. Elsewhere, Bitcoin closed above $50,000 for the first time in two years on Monday. At the same time, a survey by BNPQY (BNP Paribas) found that hedge funds (in particular multi-strategy funds) are now returning just $0.41 to their clients for every $1.00 the fund makes. This is reflecting a new trend where popular funds now have a blank check for expenses. Finally, the US Senate approved a $95 billion bill to provide aid to Ukraine, Israel, and Taiwan. (This is the same bill as a week ago but stripped of the border policy and appropriates that the GOP wants but that the MAGA types don’t want to pass so they can preserve the issue to run on in 2024.) The bill passed 70-29 with strong bipartisan support. However, the House GOP caucus is such a mess that passage in the House remains in serious doubt. (The MAGA types there have said they won’t pass aid without the border components, but killed the earlier bill that gave them what they wanted because their boss wants the issue more than a solution. So, they are in a “damned if you do and damned if you don’t” situation of their own making related to passage of the needed bill.)

So far this morning, AN, BRKR, KO, DDOG, GFS, HWM, LDOS, TAP, QSR, SHOP, and TRU all reported beats on both the revenue and earnings lines. Meanwhile, MAR missed on revenue while beating on earnings. On the other side, INCY, MCO, and ZTS beat on revenue while missing on earnings. Unfortunately, BIIB, HAS, HRI, LCII, WSO, and WCC missed on both the top and bottom lines. It is worth noting that DDOG, GFS, MAR, and MCO lowered their forward guidance. (ECL, FELE, JHX, and KLG report at 8 a.m.)

With that background, it looks like the Bears are in control this morning, energized by those high wicks from Monday. Ahead of the CPI print, the Bears are pressing especially hard in the QQQ giving a gap lower to start the premarket and a large red-body candle that is now near a retest of its T-line (8ema) from above. Still, all three major index ETFs remain above their T-line (8ema). So, the Bulls still have control of the trend in both the long and short term. In terms of extension, none of the three is too far from their 8ema yet. However, T2122 is deep into that indicator’s overbought territory. This means the market still has slack to work with if either side of the market gains traction, but the Bears have more room to work with. As I have been saying for months, keep an eye on those 10 huge tech stocks. If they walk in lock-step, whatever direction they decide to go is very likely to call the tune for the rest of the market. And so far in this early session, they are all flashing bright red.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Yesterday indexes finished mixed as the Russell 2000 surged higher hinting at a possible rotation for the high-flying tech sector to small-cap names. The afternoon selling raised some caution leaving behind some shooting star patterns on the Nasdaq and SP-500 charts with VIX moving higher diverging from the overall market. Of course, this action was not a surprise with all eyes on the CPI data pending and the uncertainty that brings to the minds of traders. We also have a big day of earnings reports so I think it’s fair to say that anything is possible today. Stay with the trend but continue to raise your stops in case the bears find a reason to attack because big-point moves are possible.

Overnight with many Asian markets still closed, the Nikkei touched 38,000 and nears an all-time high. However, European markets trade lower across the board this morning with cautiousness as they wait on U.S. inflation data. U.S. futures also suggest a lower open as we wait on the CPI data that could move the market substantially in either direction. Buckle up it could be a wild and price action morning.

JetBlue Airways, a low-cost airline based in New York, is facing pressure from activist investor Carl Icahn, who disclosed a 9.9% stake in the company on Monday. Icahn believes that JetBlue is undervalued and has the potential to grow its market share and profitability. He has expressed his interest in joining the board of directors and influencing the company’s strategy and governance. JetBlue, which has been struggling to recover from the pandemic and the failed merger with Spirit Airlines, has been implementing cost-cutting measures and operational improvements to boost its performance and competitiveness.

Nvidia, a leading chipmaker and technology company, has seen its stock price soar to record highs, sparking fear of missing out (FOMO) among investors. According to Julian Emanuel, a senior managing director at Evercore ISI, many of his clients, who have experienced the dot-com bubble and burst, are more concerned about not having enough exposure to Nvidia than having too much. He said this is the first time he has seen this sentiment since 2021, which he views as a warning sign. He also expects a 13% correction in the stock market this year, which he thinks is normal in a non-recessionary environment.

The perception of China and Russia as threats to the West has decreased in the past year, according to a new survey that reveals the growing awareness of non-conventional risks. The survey, conducted among G7 countries, shows that mass migration caused by war or climate change and the spread of radical Islam are now the most feared risks among Western populations. The survey also indicates that most Westerners expect China and the Global South to gain more influence and power in the next ten years, while the West will face stagnation or decline.

The stock market was mixed on Monday, with the S&P 500 falling slightly, while the Dow added about 120 points and the Russell 2000 surged higher, gaining about 2%. The best-performing sectors were energy, utilities, and materials, while information technology and consumer discretionary trailed behind. Treasury yields were stable, with the 10-year yield ending around 4.17%. Oil prices did not change much, closing at about $77 a barrel. This morning the Small Business Optimism Index missed expectations showing a decline disappointing the market sending premarket futures lower. Before the market opens the Inflation data will be the main focus for markets, with the CPI report, and could create significant price volatility considering the very extended condition of the indexes. Beyond that, we have a large number of earnings that will keep traders gambling on the next big mover. Buckle up anything seems possible today.

The Bulls were in charge again on Friday. SPY opened up 0.06%, DIA opened down 0.05%, and QQQ gapped up 0.27%. At that point, the SPY and QQQ continued on slow, steady rally until 3 p.m. with some very modest profit-taking the last hour. At the same time, DIA sold off slowly until noon, rallied slowly until 3 p.m. (just reaching the open level) and then took profits more strongly than the other indexes the last hour. This action gave us large white-bodied candles with small upper wicks in the SPY and QQQ. Meanwhile, DIA printed a black-bodied Doji candle. SPY and QQQ printed yet another new all-time high and new all-time high close. (SPY closed above 5000 for the first time.) Again, this happened on very low volume in all three major index ETFs.

On the day, eight of the 10 sectors were in the green as Technology (+1.38%) again was well out in front leading the market higher. At the same time, Energy (-0.73%) and Consumer Defensive (-0.61%) were the only sectors in the red. Meanwhile, the SPY gained 0.57%, the DIA lost 0.16%, and QQQ gained 0.98%. VXX gained 0.72% to close at 14.02 and T2122 climbed again but remained in the mid-range (just outside of the overbought area) at 78.12. 10-year bond yields rose a bit to 4.173% and Oil (WTI) gained 0.42% to close at $76.54 per barrel. So, the bulls ended the week again on its fourth higher close in the SPY. However, that’s the least of the streaks. SPY, DIA, and QQQ are all on a five-week winning streak…and 14 out of 15 weeks closing higher.

There was no major economic news released on Friday. However, the Bureau of Labor Statistics did revise downward the CPI data for December. The new CPI data showed a +0.2% increase for December, down from the earlier +0.3% estimate. However, at the same time, BLS revised the November number up from 0.1% to 0.2%.

In Fed news, Dallas Fed President Logan said Friday that risks are more balanced now and this gives the FOMC room to be patient on rate cuts. Logan said that there had been “tremendous progress” on bringing down inflation, but she still wants to see more evidence before starting rate cuts. She said, “The risks that I’m seeing in the economy are becoming more in balance, but I do think we need to take time here to continue to look at the data…I’m really not seeing any urgency to make any additional adjustments at this time.”

In stock news, ASTL (Canadian steelmaker) reported a significant “incident” at its north Casthouse blast furnace complex. The incident affected 12 workers with at least five requiring medical treatment. At the same time, STLA’s Chrysler brand announced it will unveil a new concept car on Tuesday that will be a “sustainable design” and be the basis for a fully electrified Chrysler future. Later, BTTR announced it had acquired AIMFF in a move that positions it well for developing a weight-loss supplement for pets. (This will compete with PFE who made a similar acquisition to move into the same segment.) At the same time, ATR and BIIB announced a partnership to build digital health solutions for neurological diseases. Later, DIS announced a new AI tool designed to match advertiser commercial messages to the mood created by specific program scenes. At midday, ASML announced they are gearing up the production line for a new $350 million “High NA EUV” chipmaking machine. The product will enable TSM, NVDA, INTC, and AMD to make new high-end, higher-density chips. At the same time, Reuters reported an exclusive the CSCO will announce a restructuring plan that will include laying off thousands of employees. The report said a public announcement is likely to come at CSCO’s earnings call on Feb. 14. Later, AXP announced that its 2023 restructuring-related costs amounted to $277 million. Elsewhere, HUBB finalized its divestiture of its residential lighting unit to KWAC for an undisclosed sum. At the same time, APLD announced it will take a revenue hit from the loss of revenue due to an ongoing power outage (since January 18) data center. Then, on Saturday, Reuters reported that AMZN founder Bezos sold $2 billion worth of AMZN stock last week per regulatory filings. (Bezos said a week ago that he would sell roughly 50 million shares by the end of January 2025.) Later Saturday, TSLA announced temporary 2% – 2.3% price cuts on Model Y cars in the US (valid until Feb. 29).

In stock legal, governmental, and regulatory news, on Friday, the FDA granted “orphan drug” status to IRON’s DISC-3405 investigational therapy. This grants the company development assistance, tax credits, fee waivers, and 7 years of market exclusivity. At the same time, the FAA accepted the propulsion system certification plan from JOBY. This sets a clear path to commercial passenger use of JOBY’s electric air taxi vehicles. Later, the FDA approved Phase 2 clinical trials of OKYO’s ocular investigational drug. At the same time, a proposed class-action suit was filed against AMZN for allegedly violating consumer protection laws by steering consumers to higher-priced products by hiding lower-price options. Later, the SEC announced Wall Street firms have agreed to pay $81 million in fines for record-keeping failure. The violators include USB and OPY. After the close, AAPL made a court filing indicating it plans to settle a lawsuit that alleged it had stolen trade secrets from startup Rivos. (Just another in a long line of firms that AAPL has “allegedly” stolen technology from.) Also after the close, Reuters reported that FAA Chief Whitaker and other top administrators of the agency will be in Seattle to meet with BA executives early this week.

Note that most Asian markets were closed for the Lunar New Year and will stay closed all week as well. In Europe, the bourses are mostly green at midday with just four of the 15 in the red. The CAC (+0.32%), DAX (+0.32%), and FTSE (-0.14%) lead the region on volume as usual in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a start to the week just on the red side of flat. The DIA implies a -0.08% open, the SPY is implying a -0.02% open, and the QQQ implies a -0.01% open at this hour. At the same time, 10-year bond yields are down a touch to 4.16% and Oil (WTI) is off 1.16% to $75.94 per barrel in early trading.

The major economic news scheduled for Monday is limited to NY Fed 1-Year Consumer Inflation Expectations (11 a.m.) and Jan. Federal Budget Balance. However, we also hear from Fed member Kashkari (1 p.m.). The major earnings reports scheduled for before the open are limited to TRMB. Then, after the close, ANET, CAR, BHF, CDNS, GT, MEDP, PFG, SCI, TSE, WTS, and WM report.

In economic news later this week, on Tuesday we get Jan. Core CPI, Jan. CPI, and Weekly API Crude Oil Stocks. Then, Wednesday EIA Crude Oil Inventories are reported. On Thursday, we get Initial Weekly Jobless Claims, Weekly Continuing Jobless Claims, Jan. Core Retail Sales, Jan. Retail Sales, Jan. Import Price Index, Jan. Export Price Index, NY Empire State Mfg. Index, Jan. Industrial Production, Dec. Business Inventories, Dec. Retail Inventories, the Fed Balance Sheet, and Fed member Bostic speaks. Finally, on Friday, Jan. Building Permits, Jan. Housing Starts, Jan. Core PPI, Jan. PPI, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-Year Inflation Expectations, Michigan 5-Year Inflation Expectations, and Fed member Daly speaks.

In terms of earnings reports later this week, on Tuesday, AN, BIIB, BRKR, KO, DDOG, ECL, FELE, GFS, HAS, HRI, HWM, INCY, JHX, LCII, LDOS, MAR, TAP, MCO, QSR, SHOP, TRU, WSO, WCC, KLG, ZTS, ABNB, AKAM, ALSN, AMX, AIG, BFAM, DVA, ENTG, EQT, GDDY, GXO, IAC, IOSP, CART, INVH, LYFT, MCY, MGM, MRC, NGD, PRI, QDEL, REZI, SSNC, MODG, WCN, WELL, and ZG report. Then Wednesday, we hear from AVTR, AVNT, GOLD, BGC, CAE, CRL, CHEF, CME, CNHI, DBD, ES, GNRC, GPN, IQV, KHC, LAD, LPX, MLM, NHYDY, OC, PSN, R, SITE, SAH, SUN, TMHC, WAB, WMB, ALB, ATUS, AWK, AR, APP, ACGL, CF, CC, CSCO, CW, ET, EQIX, HLF, HUBS, KGC, MTW, MFC, OXY, PTEN, CNXN, ROL, SON, SUM, TWLO, TYL, VTR, and WFG. On Thursday, HOUS, ARCH, CBRE, CVE, CRBG, CROX, DE, DNB, EPAM, GTX, GPC, GEO, HBI, H, NSIT, KELYA, KNF, LH, LECO, DNOW, OGN, PBF, PENN, RS, RPRX, SABR, SN, SO, SPTN, STLA, SLVM, TRGP, USFD, VNT, WEN, WST, YETI, ZBRA, AEM, AL, LNT, AMN, AMAT, BIO, BE, ED, DLR, DASH, DKNG, DBX, GLOB, IR, LBTYA, MERC, OPEN, ROKU, TXRH, TOST, TTD, and TROX report. Finally, on Friday, we hear from ACDVF, AXL, CNK, POR, PPL, TRP, THS, and VMC.

In miscellaneous news, climate researcher Michael Mann (University of PA) was awarded $1 million for libel and defamation by two right-wing, climate-denying writers. It took Mann 12 years of legal work, but just like the defamation suit that FOX settled last year, it is another small step in favor of truth. Elsewhere, Reuters reported Friday that Chinese banks issued a new all-time high record ($683.7 billion) in loans during January. This was more than four times the amount loaned in December and came as the Chinese central bank provided more support measures to banks. Meanwhile, in the US, the Washington Post reported that OpenAI CEO Altman is seeking $7 trillion in funding (yes, trillion) to begin creating and supplying the company’s own AI semiconductor chips. This is a massive effort. (For reference, “only” $527 billion worth of chips were sold globally in 2023, in total.) In addition, this would create a direct competitor to the two main suppliers of chips to all AI users (NVDA and AMD). Nonetheless, Altman is meeting with various Silicon Valley venture capitalists and had meetings with the UAE and Saudi Arabian sovereign funds last week. He has also met with SoftBank (majority owners of ARM) and the world’s largest chipmaker TSM. (It is worth keeping in mind that Altman has the backing of MSFT.) The Washington Post reported Friday he was also in contact with the US government related to where to build semiconductor Fabs (factories). Finally, Bloomberg reports that the National Assn. for Business Economics survey released today found that 21% of economists feel the Fed policy is “too restrictive.” (It is worth noting that the survey was conducted just before the last FOMC meeting.) This is the most disagreement with the Fed policy from those economists since 2011.

In geopolitical news, on Friday Israeli PM Netanyahu ordered his military to prepare a plan to evacuate Rafah. (Rafah is the Southernmost and largest city in the Gaza Strip that has not yet been occupied by Israeli ground troops. It is also the main border crossing into Egypt through which the vast majority of humanitarian aid flows.) The media speculates this is a precursor to seizing what is left of that city. (Rafah is already under air and artillery attacks.) This led to more Oil market fear of an expanded conflict. Then, on Saturday, Reuters reported that a US-led coalition) air defenses (including Kurdish forces, who suffered six dead in the incident) stopped a six-drone attack on a COP oil field in Syria. The report claimed the attack came from an Iranian-backed militia in Syria. On Sunday, the Israeli PM told US morning news shows that his military was being very careful and that the ratio of dead civilians to dead Hamas fighters was 1-to-1. If that were somehow true (very, very unlikely) Hamas had a much larger militia than anyone had ever realized since a little over 28,000 Palestinians are confirmed dead and almost 68,000 injured.

With that background, it looks like the Bulls are rebounding slightly after the Bears started the premarket with a modest lead in their race. All three major index ETFs are printing small, white-body candles in the early session and are little changed from Friday’s close. All three also remain above their T-line (8ema). So, the Bulls remain in control of the trend in both the long and short term. In terms of extension, none of the three is too far from their 8ema yet and the T2122 indicator remains just outside of overbought territory at the top of its midrange. This means the market still has slack to work with if either side of the market gains traction. As I have been saying for months, keep an eye on those 10 huge tech stocks. If they walk in lock-step, whatever direction they decide to go is very likely to call the tune for the rest of the market.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The bulls celebrated as the SP-500 crossed 5,000, a psychological level that can serve as a significant level of support or resistance. The Nasdaq led the rally pushed by the tech giants that continued their parabolic rise. This week anything is possible with a CPI report on Tuesday, a slew of reports grouped into Thursday, and then a PPI report on Friday as we slide into a 3-day weekend. Of course, we will toss in a bunch of earnings reports and some Fed speeches to keep the price volatility challenging.

Many of the Asian markets were closed to their extended celebration of the Lunar New Year. However, European markets traded mostly higher this morning with only the FTSE moving slightly lower. Ahead of a Tuesday CPI, U.S. futures suggest a flat maybe slightly bearish open perhaps resting after the record highs made on Friday. Buckle up it could be a wild week as the data is revealed.

Economic Calendar

Earnings Calendar

Notable reports for Monday include ANET, CAR, BLKB, BHF, CDNS, FRT, GT, HPP, LSCC, MNDY, MEDP, & OTTR.

News & Technicals’

Russia’s economy is expected to grow faster than previously anticipated, according to the International Monetary Fund (IMF). The IMF revised its projection for Russia’s GDP growth in 2024 from 1.1% to 2.6%, citing improved domestic demand and higher oil prices. However, Russia’s economic recovery is also driven by its massive military spending, which has increased sharply since the outbreak of the war. The IMF’s managing director, Kristalina Georgieva, warned that Russia’s economic model is unsustainable and resembles the Soviet era, with heavy reliance on state-owned enterprises and low diversification.

Elon Musk, the billionaire entrepreneur and founder of Tesla and SpaceX, is facing a legal battle with the U.S. Securities and Exchange Commission (SEC) over his takeover of Twitter in 2022. A U.S. judge has ordered Musk to appear in court and answer questions about his acquisition of the social media giant, which the SEC suspects was a case of securities fraud. The SEC claims that Musk manipulated the stock price of Twitter by buying shares before announcing his intention to buy the company with borrowed money. Musk, who has a history of clashing with federal regulators, denies any wrongdoing and argues that he has the right to challenge the SEC’s authority.

Germany, the largest economy in Europe, is facing a bleak economic outlook for 2024. The latest data shows that the country’s GDP contracted by 0.2% in the fourth quarter of 2023, marking the second consecutive quarter of negative growth. Economists warn that Germany may slip into a technical recession this year, as the recovery from the pandemic is hampered by various challenges. These include the impact of trade tensions, rising energy costs, and political instability both at home and abroad. While some economists hope that the worst is behind, they remain pessimistic about the prospects of robust growth in 2024.

The EU, which claims to be a leader in environmental protection, is facing a backlash from its citizens over its climate policies. Farmers across Europe have been protesting against the EU’s plans to reduce pesticide use and greenhouse gas emissions, arguing that they would harm their livelihoods and competitiveness. As a result, the European Commission, the EU’s executive branch, has decided to abandon its proposal to cut pesticide use by half. Moreover, the Commission has also excluded the agricultural sector from its ambitious goal of slashing greenhouse gas emissions by 90% by 2040. These moves have raised doubts about the EU’s commitment and credibility in tackling the climate crisis.

The U.S. stock market mostly rose on Friday with the Dow lagging slightly, as the S&P 500 crossed 5,000, reaching new record highs. Big round numbers like this tend to serve as strong psychological support levels if prices hold above but also tend to serve as strong resistance levels if prices happen to fall below. Small-caps, consumer discretionary, and technology sectors led the market, as oil prices also increased. The 10-year Treasury yield edged higher on Friday, continuing the rise in interest rates since last week, as bond markets delayed their expectations for Fed rate cuts. This week will be highlighted by a CPI number on Tuesday followed by a reading on PPI Friday which just happens to be the February option expiration before a 3-day weekend. Of course, we will continue to have notable earnings events to add to the price action volatility. Stay with the upside trend but continue to raise your stops should the market stumble on one of these data points.

Thursday was a sideways day from the start. SPY opened “up” 0.01%, DIA gapped up 0.19%, and QQQ opened 0.05% higher. From that point, SPY wandered back and forth across that “gap” for the rest of the day. At the same time, DIA sold off modestly back down across its gap by 10:15 a.m. and reached its lows at 11:30 a.m. Then it started a modest rally crossing back up into the gap by 2 p.m. and slowly drifting back up toward its opening level. Meanwhile, QQQ very slowly rallied after the open, reaching its highs at 11 a.m. and trading sideways in a tight range the rest of the day. This gave us indecisive candles in all three major index ETFs. Both SPY and QQQ printed white-bodied Spinning Top candles while DIA printed a long-legged Doji. All three gave us yet another new all-time high close with QQQ and SPY also giving us new all-time highs. This happened on a very low volume compared to the average.

On the day, six of the 10 sectors were in the green as Technology (+1.10%) again was well out in front leading the market higher. At the same time, Communications Services (-1.53%) was again by far the laggard sector. Meanwhile, the SPY gained 0.04%, the DIA gained 0.18%, and QQQ gained 0.19%. VXX fell by 0.57% to close at 13.92 and T2122 climbed but remained in the mid-range at 71.06. 10-year bond yields climbed to 4.156% and Oil (WTI) spiked 3.61% to close at $76.53 per barrel. So, again strong earnings led to optimism but there was no news to lead to a follow-through. The bulls were not willing to put more money in at these high levels and the bears have gotten run over enough times that they aren’t going to be on reversal yet either. (Hence, the very low volume.) This led to a day of drift and micro moves that amounted to a nothing burger.

The major economic news released Thursday was limited to Weekly Initial Jobless Claims, which came in a bit below expectation at 218k (compared to a forecast of 221k and the prior week’s 227k). At the same time, Weekly Continuing Jobless Claims also came in a bit below the anticipated level at 1,871k (versus a forecast of 1,878k and the prior week’s 1,894k). Finally, after the close, the Fed Balance Sheet rose $1 billion on the week, coming in at $7.631 trillion (compared to $7.630 trillion last week).

In Fed news, Richmond Fed President Barkin said Thursday that he is skeptical of recent economic data, citing the difficulty of seasonal adjustments at the start of each year. Barkin said, “The data has been remarkable across the board,” … “But I am always cautious about numbers around the turn of the year, there’s big seasonal adjustments…I am not sure I am going to take too much out of any one month.” He went on to say the Fed should be patient in making rate changes. Later, Boston Fed President Collins said she thinks the Fed will cut rates by three-quarters of a percent in 2024. Collins told a radio interview Thursday, “I do expect that before the end of the year, it will be appropriate for us to carefully begin easing rates.” She went on to echo other Fed members by saying she would need to see additional evidence before voting for rate cuts, but that inflation is clearly falling and the economy remains resilient.

In stock news, UL announced a $1.6 billion share buyback program Thursday. Later, ICE (parent company of NYSE) said it saw strong growth in trading volumes, especially in energy and commodity markets last quarter. ICE attributed part of the increased volume to an increase in market volatility (which usually leads to more volume as traders adjust positions). At the same time, GOOGL rebranded its AI chatbot from Bard to Gemini on Thursday and launched it as a $19.99/mo. subscription service that comes with two terabytes of cloud storage (normally a $9.99/mo. offering). (Gemini is intended to compete with MSFT’s co-pilot subscription available in MS Word and MS Excel.) Later, Reuters reported that APO is negotiating for a minority stake in 2,000 SBUX locations across 13 countries in the Middle East, North Africa, and Central Asia. The 30% stake is said to be valued between $4 billion and $5 billion. At the same time, Reuters reported that DVN is in talks to acquire ERF to strengthen its positions in the Bakken (ND) and Marcellus (PA) shale fields. Later, HSBC announced it had partnered with GOOGL and will provide financing to GOOGL-chosen climate technology firms that join GOOGL’s “Cloud-Ready Sustainability” program. Elsewhere, VLKAF (Volkswagen) told Reuters that despite competitors like GM pulling back on EV plans, it is sticking with its plan to launch 25 electric vehicle models in North America by 2030. However, the company hedged its bets by saying it is ready to adjust as the market shifts. At the same time, BA announced it had received an order for 45 of its 787 jets from Thai Airways. (No delivery dates were announced, but typically the lead time is several years.) Later, Reuters reported that part of the reason TSLA is now considering layoffs is that TSLA trails both GM and F in “revenue per employee.” GM generates over $1 million per employee, F generates $937,000, and TSLA makes just under $690,000 per employee.

In stock legal, governmental, and regulatory news, the FAA announced it has begun an investigation into two JBLU planes that collided on the tarmac in Boston Thursday. (No injuries were reported.) Later, AMZN and BMWYY (BMW) won a lawsuit in Spain against four sellers of counterfeit BMW merchandise sold through AMZN. Elsewhere, Reuters reported that the CFTC has opened an investigation into GS and has sent the company subpoenas for information about fees charged for certain block trades in the futures market. (GS paid $50 million in 2023 to settle three other CFTC cases.) Later, the FAA formally mandated inspections of all 737 MAX airplanes looking for loose bolts on rudder control systems. (This was a follow-up to BA itself “recommending” that its customers inspect those bolts after identifying quality control issues in December.) At the same time, a US Senate Committee voted to boost funding of the FAA (so that it can increase the number of on-the-ground inspectors at BA and its suppliers like SPR) and also rejected the proposal to increase the pilot retirement age from 65 to 67. Both of these positions are in line with FAA requests but are in opposition to House as well as airlines (AAL, DAL, LUV, and UAL) positions on the matters. Later, a group of religious investors (the group represents $4 trillion in assets) sent a letter urging XOM to drop its lawsuit against climate activists. At the same time, EU antitrust regulators have now set a March 13 deadline for whether to approve the CSCO $28 billion acquisition of SPLK. Later, Reuters reported that UBER, DROOF, and other similar companies that use online workers reached a deal with EU lawmakers over the rights of gig workers. The deal removes the matter from the national government’s purview in favor of collective bargaining and case law. However, it also puts the burden of proof on the company in any dispute over whether a person is an employee or contractor.

After the close, AFRM, BYD, DXCM, EXPE, G, PEAK, ILMN, LEG, MHK, MSI, TEX, and TFII all reported beats on both the revenue and earnings lines. Meanwhile, ATR, FE, FLO, NGL, and PINS missed on revenue while beating on earnings. On the other side, TTWO beat on revenue while missing on earnings. Unfortunately, CPRI and MTD missed on both the top and bottom lines. It is worth noting that AFRM and MTD raised forward guidance. However, G, LEG, MHK, and TTWO lowered guidance.

Note that Asian markets were closed for Lunar New Year and will stay closed all of next week as well. In Europe, markets lean the green side at midday with 10 of the 15 bourses modestly in positive territory. The CAC 9-0.15%), DAX (+0.05%), and FTSE (+0.02%) lead the region slightly higher in early afternoon trade. In the US, as of 7:15 a.m., Futures are pointing toward a slightly green start to the day. The DIA implies a +0.05% open, the SPY is implying a +0.13% open, and the QQQ implies a +0.31% open at this hour. At the same time, 10-year bond yields have climbed to 4.172% and Oil (WTI) is down slightly to $76.23 per barrel in early trading.

There is no major economic news scheduled for Friday. The major earnings reports scheduled for before the open include AMCX, CTLT, ENB, FTS, MGA, NWL, PEP, PAA, PAGP, and TIXT. There are no earnings reports scheduled for after the close.

So far this morning, AMCX and NWL reported beats on both the revenue and earnings lines. Meanwhile, FTS, PEP, and TIXT missed on revenue while beating on earnings. On the other side, MGA beat on revenue while missing on earnings. Unfortunately, ENB and UI missed on both the top and bottom lines. It is worth noting that NWL and TIXT lowered forward guidance. However, also note that PEP raised its guidance.

In miscellaneous news, Maersk said Thursday that there is too much container chipping capacity and this would impact their profits for 2024. The shipping giant downplayed the impact of Red Sea disruptions (which cause longer shipping routes meaning more container ships are needed to maintain the same flow of trade). The signal that this was a real warning was that the company also suspended its share buyback program. Maersk is often seen as a barometer of global trade and therefore global GDP. Elsewhere, the US Dept. of Transportation reported that driving in the US set a new yearly record in 2023 of 3.263 TRILLION miles driven. (This was the first time a new record has been set since prior to COVID-19.) Meanwhile, US trade data released earlier this week shows that Mexico exceeded China to become the largest trading partner of the US. Mexican trade included $476 billion in imports and $323 billion in exports from the US for a total of $799 billion in 2023. (US-China trade for 2023 was just $575 billion.) Finally, Treasury Sec. Yellen told the Senate Banking Committee that she expects more commercial real estate stress, but that the problem is not a systemic banking risk. Yellen said, “Valuations are falling. And so it’s obvious that there’s going to be stress and losses that are associated with this, … exposure of the largest banks is quite low, but there may be smaller banks that are stressed by these developments … I hope and believe that this will not end up being a systemic risk to the banking system.”

In global-related news, Israel rejected the Hamas proposal (itself a response to earlier negotiations) for a “cease-fire and humanitarian aid in exchange for hostages” deal. (This was the primary cause of the spike in oil prices Thursday as Israel, Hamas, and the Houthi rattled sabers after Israel’s announcement.) Later, Ukrainian President Zelenskyy replaced their Armed Forces chief in favor of the head of their ground forces. In related news, after the GOP killed the combined Border-Ukraine-Israel-Taiwan package they had demanded, the US Senate pushed forward a smaller $95 billion aid bill just covering Ukraine and Israel aid. This came after the GOP caucus split and 17 of them voted with the Democratic majority to get past the high hurdle by a 67-32 vote. House action on this bill is completely uncertain since the House Speaker is one of the MAGA types (but also backed away on Thursday from his demand to split this into separate Israel and Ukraine aid bills so that they could vote down Ukraine aid to appease their party’s Russian-supporting candidate and wing) and MAGA lobbying and threats is what killed the broader Senate bill in the first place.

With that background, it looks like all three major index ETFs are looking to open a bit higher but in a pretty undecided manner. All three are giving us small, white-body candles in the premarket. All three also remain above their T-line (8ema). So, the Bulls remain in control of the trend in both the long and short term. In terms of extension, none of the three is too far from their 8ema yet and the T2122 indicator remains in its midrange. This means the market still has plenty of slack to work with if either side of the market gains traction. As I have been saying for months, keep an eye on those 10 huge tech stocks. If they walk in lock-step, whatever direction they decide to go is very likely to call the tune for the rest of the market. Finally, remember that it’s Friday. So, pay yourself and prepare your account for the weekend by lightening up, moving stops, and/or hedging.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The rally was back on Wednesday across the market. SPY gapped up 0.46%, DIA gapped up 0.33%, and QQQ gapped up 0.63%. At that point, all three major index ETFs pulled back into the top of their gap area to bide time for half an hour. Then all three rallied sharply for 30 minutes. From there, all three drifted sideways within a fairly tight range the rest of the day. This action gave us white-bodied candles with larger lower and smaller upper wicks. SPY and QQQ could be said to have printed white-bodied Spinning Top candles while DIA gave us a White Doji-like candle. All three printed new all-time high closes while SPY and QQQ also gave us new all-time highs. This happened on less-than-average volume (especially in the DIA).

On the day, five of the 10 sectors were in the green as Technology (+1.25%) was way out front leading the market higher. At the same time, Communications Services (-1.18%) lagged very far behind the other sectors. Meanwhile, the SPY gained 0.83%, the DIA gained 0.41%, and QQQ gained 1.03%. VXX fell slightly to close at 14.00 and T2122 dropped a bit but remained in the center of its mid-range to 51.95. 10-year bond yields climbed to 4.115% and Oil (WTI) rose 1.05% and close at $74.08 per barrel. So, once again strong earnings led to a pop at the open. From that point, it felt like a game of “wait and see” with traders looking for the next news event on the horizon.

The major economic news released Wednesday included Dec. Exports, which were up to $258.20 billion (compared to November’s $254.30 billion value). At the same time, Dec. Imports were also up to $320.40 billion (versus the Nov. $316.20 billion reading). This gave us a December Trade Balance of $62.20 billion, which was in line with the $62.20 billion forecast and the November $61.90 billion value. Later, Weekly EIA Crude Oil Inventories showed a much higher build than expected at +5.520 million barrels (compared to the +1.700 million barrels forecast and the prior week’s +1.234 million barrels build). Later, the Dec. Outstanding Consumer Credit number was dramatically lower than anticipated at $1.56 billion. Compare this to a $14.90 billion forecast and the massive $23.48 billion November reading. (However, remember that Consumer Credit numbers are often subject to big revisions.)

In Fed news, the NY Fed released a report showing that wealth inequality continues to grow. The report covered the period from 1/1/19 to 9/30/23. It showed white family’s net worth rose 28% over the period while the Hispanic family’s net worth increased 20%. However, black family net worth actually decreased by 1.5% over the period. Elsewhere, Boston Fed President Collins said if the economy meets her expectations, the FOMC will be able to lower rates “at some point this year.” Collins said, “The unexpected strength in recent GDP and labor market data exemplifies the ongoing resilience of demand, and highlights that the anticipated slowdown in activity may take some time.” She continued, “I believe it will likely become appropriate to begin easing policy restraint later this year.” Collins also said that the Fed does not need to wait until the Fed’s 2% inflation target is met, saying she “totally agrees” that if they wait until then, “that’s waiting too long.” Later, Fed Governor Kugler said she was optimistic that inflation will continue to decline. She went on to agree with the recent statements of Fed Chair Powell, saying, “The job is not done yet.” However, she also said, “March, May, June — every meeting from now until the end of the year and moving forward will be live (for rate cuts).” Meanwhile, on CNBC, Minneapolis Fed President Kashkari said, “Sitting here today I would say two to three cuts would seem to be appropriate for me right now…that’s my gut based on the data we have so far.”

After the close, NLY, ARM, ASGN, CENTA, CENT, CPA, CXW, COTY, EHC, EFX, GL, MMS, MCK, MKSI, MOH, NWSA, OSCR, PYPL, SGU, STE, SLF, UVV, DIS, and WYNN all reported beats on both the revenue and earnings lines. Meanwhile, ALL, BKH, ENS, EG, MAA, MUSA, ORLY, and RRX missed on revenue while beating on earnings. Unfortunately, NVST, FAF, FLT, MAT, and UHAL missed on both the top and bottom lines. It is worth noting that ARM, MPWR, OSCR, and DIS raised their forward guidance. However, ENS, EFX, MAA, PYPL, and RRX lowered their guidance.

In stock news, PRU announced it has taken over the $4.9 billion pension risks of SHEL as part of its deal to manage the pension benefits. At the same time, Bloomberg reported that only a single TSLA was sold in South Korea in January due to various safety concerns, high prices, and inadequate charging infrastructure. Later, FOX reported a 20% decline in revenue, citing a fall in political ad sales. At the same time. MSFT announced it has launched its Microsoft 365 Copilot internally in an attempt to boost AI adoption by its programmers. Later, MPWR announced it will acquire Axign (a Netherlands-based fabless semiconductor maker). At the same time, DIS told CNBC it will be taking a $1.5 billion minority stake in Epic Games (Fortnite publisher). Later, ADESY (Airbus) announced it delivered 30 jets in January (up 50% from the same month in 2023). The company also recorded 31 jet orders during the month. Elsewhere, BA said that the FAA investigation findings will likely cause delays in the production schedule of its 737 jets. Later, SPXC announced the acquisition of Ingenia (a Canadian firm) for $300 million, which included acquired real estate. Meanwhile, after the close, TSLA asked its managers to define which of their employees are critical to operations, stoking fears of layoffs to come.

In stock legal, governmental, and regulatory news, the FDA put a hold on trials of a GILD blood cancer drug, citing an increased risk of death in some previous studies. Later, a German court ruled against INTC in a patent dispute with tiny CA-based R2 Semiconductors. At the same time, GCI was ordered to pay $25 million in damages after losing a defamation lawsuit. Later, GOOGL’s Waymo autonomous driving unit was hit with a notice of regulatory review by the CA Dept. of Motor Vehicles after one of its driverless cars hit a cyclist, on Tuesday, causing minor injuries. At the same time, Reuters reported that MSFT is in negotiations with a trade group (CISPE), which does include AMZN which is a direct competitor, in an attempt to end the group’s complaint filed with the EU’s antitrust regulators over MSFT cloud computing licensing practices. In other MSFT news, the FTC clammed MSFT on Wednesday for violating its promises by laying off 1,900 gaming employees after saying no such layoffs would happen when it was seeking approval for its acquisition of ATVI (which the agency is still appealing to block). Later, a US court nullified EPA approval of certain agricultural weedkillers from BAYRY (Bayer) and BASFY (BASF) used on soybean and cotton crops. Elsewhere, the NHTSA announced it had closed its investigation into 3 million vehicles from HYMTF (Hyundai) and Kia related to potential engine fires. The agency determined the companies had issued eight recalls that addressed the issues that had caused the fires prompting the investigation. At the same time, META filed a challenge to an EU “supervisory fee” aimed at deferring the regulator’s costs for monitoring compliance with EU content laws. The fee amounts to 0.05% of META’s global net income and the fee amount is related to a social media’s average monthly active users. The fee also applies to GOOGL, AAPL, and other social network giants. Meanwhile, AAPL won the dismissal of a shareholder lawsuit that alleged the company had overpaid CEO Cook by tens of millions of dollars. After the close, CVS was fined $250k by the state of OH for understaffing the pharmacy of one of its stores risking employee safety, and causing extreme delays for patients seeking prescriptions. (The case stems back to a 2021 investigation.)

Overnight, Asian markets were mixed but leaned toward the green. Japan (+2.06%), Shenzhen (+1.29%), and Shanghai (+1.28%) led the region higher while Hong Kong (-1.27%), India (-0.95%), and Thailand (-0.82%) lagged. In Europe, we see a similar mixed picture at midday with 5 of the 15 bourses in the red. The CAC (+0.62%), DAX (+0.36%), and FTSE (+0.01%) lead the region higher in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a start just on the red side of flat. The DIA implies a -0.01% open, the SPY is implying a -0.14% open, and the QQQ implies a -0.15% open at this hour. At the same time, 10-year bond yields are up to 4.139% and Oil (WTI) is up another percent to $74.65 per barrel in early trading.

The major economic news scheduled for Thursday includes Weekly Initial Jobless Claims and Weekly Continuing Jobless Claims (both at 8:30 a.m.), WASDE Ag report (noon), and Fed Balance Sheet (4:30 p.m.). The major earnings reports scheduled for before the open are include WMS, APO, MT, ARES, ARW, ABG, AXTA, BAX, BCE, BDC, BWA, CCJ, CX, CIGI, COP, DTE, DUK, GTES, HOG, HSY, HMC, NSP, ICE, IPG, ITT, K, KVUE, LNC, MAS, MDU, NFG, PATK, BTU, PM, RL, RXO, SPGI, SNA, SPB, SAVE, TROW, TPR, TPX, THC, TRI, TDG, UA, UAA, WMG, WEX, and ZBH. Then, after the close, AFRM, ATR, BYD, CPRI, BAP, DXCM, EXPE, FE, FLO, G, PEAK, ILMN, LEG, MTD, MHK, MSI, NGL, PINS, TTWO, TEX, and TFII report.

In economic news later this week, on Friday there is no major news planned.

In terms of earnings reports later this week, on Friday, AMCX, CTLT, ENB, FTS, MGA, NWL, PEP, PAA, PAGP, and TIXT report.

So far this morning, WMS, APO, ARES, AXTA, BAX, BCE, BDC, CRARY, HOG, ICE, IPG, ITT, KIM, MAS, RNECY, SPB, TROW, TPR, THC, TDG, WEX, and ZBH all reported beats on both the revenue and earnings lines. Meanwhile, ABG, CCJ, CIGI, and SPGI beat on revenue while missing on earnings. On the other side, COP, DTE, GTES, HSY, KVUE, LNC, RXO, SNA, TRI, UA, and UAA all missed on revenue while beating on earnings. Unfortunately, MT, BWA, DUK, PM, and TPX missed on both the top and bottom lines. It is worth noting that WMS, CIGI, DT, MAS, TPR, TRI, and ZBH all raised their forward guidance. However, BWA, HSY, KVUE, KIM, PM, and SPGI all lowered their guidance.

In miscellaneous news, the USDA released its latest forecast Wednesday, saying that it expects a plunge in crop prices (to multi-year lows) along with a surge in production costs. The result is that the agency expects enough of a drop in farm incomes to cause ripples across the broader economy. Specifically, the USDA forecasts a 25.5% drop in net farm profits in 2024 after a drop in 2023 from the record high in 2022. Elsewhere, Bloomberg reported that a former Citadel employee has said the fund was one of the clients MS had leaked upcoming trades to when it was punished for the practice. The names of the recipients had been redacted as part of MS’s $249 million settlement to end the SEC investigation. Meanwhile, in a surprise move, China replaced the head of its securities regulator in a move meant to help restore confidence in the markets. (The man replaced had gained the nickname “the broker butcher” for cracking down on traders.)

With that background, it looks like all three major index ETFs are undecided in the premarket. All three are giving us small candles with DIA printing an early session white body and both SPY and QQQ giving us a small red body. None are far removed from Wednesday’s close and all three remain above their T-line (8ema). So, the Bulls remain in control of the trend in both the long and short term. In terms of extension, none of the three is too far from their 8ema yet and the T2122 indicator remains in the center of its midrange. This means the market has plenty of slack to work with if either side of the market gains traction. As I have been saying for a long time, keep an eye on those 10 huge tech stocks. On Wednesday it was META, NVDA, MSFT, AMD, and TSLA leading the pack. If they walk in lock-step, whatever direction they decide to go is very likely to call the tune for the rest of the market.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The bull trend continues despite the rate of uncertainty fueled by earnings results and a remarkable willingness to chase the very extended tech titians higher. I think we can expect more of the same as we roll out a huge number of earnings reports through the end of the week. That said, manage your positions closely because the bears are beginning to act a bit more aggressively, and if the bulls stumble or run out of energy an attack could begin quickly. Plan for considerable price volatility as the market reacts to all the pending reports.

While we slept Asian markets closed mixed but mostly higher as China pushed hard to stimulate buying confidence as manufacturing and real-estate woes continue. European markets trade modestly lower across the board this morning as the rate uncertainty continues. Although U.S. futures traded lower overnight once again they are working hard in the premarket to recover losses as earnings results roll out.

Snap, the maker of the popular social media app Snapchat, reported a modest increase in its fourth-quarter revenue, while its net loss shrank from a year ago. However, the company’s revenue and forecast fell short of the market expectations, sending its shares lower. Snap blamed the Middle East conflict for slowing down its growth, as it said in a letter to investors on Tuesday that the geopolitical turmoil hurt its advertising business.

Chipotle, the fast-casual Mexican restaurant chain, reported strong earnings and revenue for the fourth quarter, exceeding the market forecasts. The chain’s same-store sales, which measure the performance of its existing locations, also surpassed expectations, showing healthy growth. Chipotle attributed its success to the increase in its customer traffic, which defied the general decline in the restaurant industry. Chipotle said that its digital and delivery initiatives, as well as its menu innovations, helped attract more customers and boost its sales.

Ford, one of the leading car manufacturers in the world, is revising its plans for investing in electric vehicles (EVs). According to its CEO Jim Farley, the company is facing challenges in making EVs affordable and profitable for the average customer. While Ford remains optimistic about the future of EVs, it has decided to reduce its spending on this segment by $12 billion. This move reflects the uncertainty and complexity of the EV market, which is still evolving and developing.

Despite beating analysts’ estimates for its fourth-quarter performance, CVS Health delivered a disappointing outlook for 2024. The healthcare giant blamed rising medical expenses for its lower earnings guidance, which reflects the challenges faced by the insurance sector amid the pandemic. CVS Health, which operates pharmacies, clinics, and health plans, said it expects to earn at least $8.30 per share in 2024, down from its previous projection of at least $8.50 per share.

Earnings results continue to help the indexes push higher to close mostly in the green on Tuesday. The S&P 500 and the NASDAQ, edged up by about 0.2% and 0.1%, respectively. However, after the morning pop, the market largely chopped sideways on relatively low volume. The best-performing sectors in the S&P 500 were real estate and materials, each gaining about 1.5%. After dropping by about 2% in the previous two days, U.S. small-cap stocks bounced back by about 0.6%. Today traders will look for inspiration in the huge number of earnings reports as well as Mortgage Apps, International Trade, Petroleum Status, several Fed speakers, and bond auctions. The trend remains bullish but the hint of uncertainty could bring the bears in quickly so continue to manage your positions carefully to protect profit if the bull begins to stumble.

Tuesday saw stocks open slightly higher and then diverge with large-caps chopping sideways and QQQ selling off before starting its own chop to the side. SPY gapped up 0.19%, DIA opened 0.09% higher, and QQQ gapped up 0.27%. At that point, SPY meandered sideways, recrossing its gap several times. Meanwhile, DIA chopped to the side above its open and QQQ immediately recrossed the gap up and sold off until 12:30 p.m. before meandering along the lows. Then, during the last 30 minutes of the day, all three major index ETFs rallied. This action gave us a white-bodied Spinning Top in the SPY, a large-bodied, white-bodied Bullish Harami in the DIA (that bounced up off its T-line), and a black-bodied Spinning Top in the QQQ (which also bounced up off its 8ema).

On the day, nine of the 10 sectors were in the green as Healthcare (+1.30%) and Consumer Cyclical (+1.20%) led the way higher. Meanwhile, on the other end of the spectrum, Communications Services (-0.22%) was the only sector that stayed in the red. At the same time, the SPY gained 0.29%, the DIA gained 0.39%, and QQQ lost 0.20%. VXX fell another 2.43% to close at 14.05 and T2122 spiked back up into the center of its mid-range to 55.74. 10-year bond yields dropped back down to 4.09% and Oil (WTI) rose 0.92% and close at $73.45 per barrel. So, good premarket earnings led to a nice start to the day. However, from that point forward we mostly saw drift and indecision as traders wait for a more broad-based read on earnings season (or more news and/or Fed opinions).

The major economic news released Tuesday was limited to Weekly API Crude Oil Stocks, which showed a smaller-than-expected increase of 0.674 million barrels (compared to a forecasted build of 2.133 million barrels but better than the prior week’s 2.500-million-barrel drawdown). Elsewhere, the EIA released its short-term Energy Outlook. The report says it expects US electricity use to rise to records in both 2024 and 2025. (The US used 3,994 billion kWh in 2023 with 2024 demand projected at 4,112 billion kWh and 2025 at 4,123 billion kWh).

In Fed news, Cleveland Fed President Mester said Tuesday that she is open to rate cuts if it is clear inflation is still slowing. Mester said, “Monetary policy is in a good place from which to assess and respond” … “I don’t want to put a particular calendar date on it (rate cuts) – it really is dependent on the state of the economy.” She added, “There’s no rush.” Later, Philly Fed President Harker said that a soft landing was in sight for the US economy. Harker said, “The data point to continued disinflation, to labor markets coming into better balance, and to resilient consumer spending — three elements necessary for us to stick to the soft landing we remain optimistic to achieve.” He went on to say “real progress” is being made toward (getting back to) the Fed’s 2% target.

After the close, AB, AFG, AMGN, AIZ, CSL, CMG, CINF, CRUS, CNO, EW, F, FTNT, IEX, JKHY, LUMN, OI, OMC, OXBC, SONO, SNEX, VLTO, VOYA, WFRD, WU, and YUMC all reported beats on both the revenue and earnings lines. At the same time, ASTL, AMCR, EQH, CTSH, EXEL, and SNAP all missed on revenue while beating on the earnings lines. On the other side, GILD, KD, PRU, QGEN, VSAT, and WERN all beat on revenue while missing on earnings. Unfortunately, AMRK, DOX, ATO, PLUS, NBR, and VFC missed on both the top and bottom lines. It is worth noting that PLUS and GILD lowered guidance. However, JKHY, KD, and VLTO raised their forward guidance.

In stock news, USB announced it will resume share buybacks and plans to find $3 billion more in cost savings related to integrating its acquisition of CS. (UBS says it now expects to save $13 billion total by the end of 2026 from the CS purchase.) Later, the UAW announced that more than 50% of the workers at VLKAF (Volkswagen) TN plant have signed requests to join the union. (UAW previously announced it will seek recognition once that number reaches 70%.) At the same time, DD announced a new $1 billion stock buyback program and hiked its dividend by 6%. Later, KSS stock jumped as hedge funds (major shareholders) urged the company to sell itself. (KSS rejected a $64/share offer in 2022, holding out for a $70/share offer that never arrived. KSS closed at $26.80 on Tuesday.) At the same time, AMZN announced it will cut 115 jobs from its healthcare services unit (which has 400 employees). Elsewhere, DIS (ESPN and ABC), FOX, and WBD announced a revolutionary sports-centric subscription streaming service to be launched in the fall of 2024. This will target non-cable, sports fan subscribers.