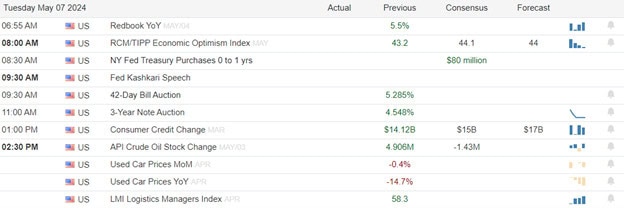

Kashkari Says There Is No Hurry to Cut

Markets opened just modestly higher Tuesday. SPY opened 0.18% higher, DIA started 0.19% higher, and QQQ opened up +0.08%. From there, all three major index ETFs ground sideways the first hour. At that point DIA started a long, very modest selloff that finally recrossed the opening gap at 2:30 p.m. From there DIA ground along the prior close level before heading back to the open level during the last hour. Meanwhile, SPY and QQQ both continued sideways until 1:30 p.m. Then, those two followed DIA but with a bit sharper selloff before grinding sideways along the previous close after 2:30 p.m. until a rally the last 15 minutes took both back up to the opening level. This action gave us, Doji candles in all three major index ETFs. SPY and DIA gapped just a bit higher before printing the Doji while QQQ opened flat and printed its own Doji. All three remain above their T-line (8ema).

On the day, seven of the 10 sectors were in the green with the Consumer Defensive (+1.01%) group leading the market higher. Meanwhile, Consumer Cyclical (-0.74%) was the weakest sector by half of a percent. VXX was flat and remains at 12.41 and T2122 pulled back a bit but remains in the overbought territory at 84.80. At the same time, 10-year bond yields fell again to 4.459% and Oil (WTI) was flat, closing at $78.56 per barrel. So, again Tuesday, it was an indecisive day across the market with no real strength from either the Bulls or the Bears. One indicator of the indecision is that the 10 big dog stocks were evenly split between green and red. However, we should note that the biggest movers among that group were on the red side and also had the heaviest dollar move. NVDA (-1.72%) traded $39.1 billion in stock and TSLA (-3.76%) traded $13.2 billion in stock. Meanwhile, AAPL (+0.38%) was the biggest gainer with $13.1 billion of stock traded.

The major economic news scheduled for Tuesday included March Consumer Credit, which came in FAR below expectations at $6.27 billion (compared to a forecasted $14.80 billion and the February value of $15.02 billion). After the close, API Weekly Crude Stocks showed an inventory build of 0.509 million barrels (versus a forecasted -1.430 million barrels and far below the previous week’s 4.906-million-barrel inventory build).

In Fed speak news, Minneapolis Fed President Kashkari said the FOMC may need to hold rates steady through all of 2024. Kashkari said, “(In order to support a rate cut) I would need to see multiple positive inflation readings suggesting that the disinflation process is on track.” However, on the other side, he did allay some fears by saying “The bar for a rate hike is quite high but it’s not infinite … There is a limit when we say, ‘OK, we need to do more.’ I think it’s much more likely we would just sit here for longer than we expect, or the public expects right now, until we see what effect our monetary policies have.”

After the close, ANET, AIZ, CRC, CHRD, GMED, GXO, HY, IAC, ICUI, KD, KGC, LYFT, MASI, MTCH, PR, RNG, SU, TOST, TWLO, and WYNN all reported beats on both the revenue and earnings lines. Meanwhile, AGL, ANDE, ARKO, BIO, BTG, BHF, JKHY, OVV, OXY, and RRR missed on revenue while beating on earnings. On the other side, AMRK, CPNG, GO, MTW, RYAM, and RIVN beat on revenue while missing on earnings. However, EA, and MCK missed on both the top and bottom lines. It is worth noting that AGL lowered its forward guidance while ANET and MASI both raised their guidance.

In stock news, on Tuesday, a Brazilian paper company (Susano) mad a bid to buy IP for $15 billion. The $42.00 per share offer was given to the IP board verbally and will be submitted in writing soon. (IP closed at $36.92 on Monday and then at $38.84 after the news Tuesday.) At the same time, AAPL held an event to announce new iPad models based on the M4 version of their in-house designed ARM processor. Later, RCL announced it is trying to recruit 10,000 new workers to staff ships and its private destinations this year. The company says the need to hire so many workers is due to record cruise demand. At the same time, META announced it has launched tools for AI image generation for advertisers. This comes after GOOGL announced the same set of tools in February. Later, PNRA announced it is phasing out its “Charged Sips” line of ultra-caffeinated drinks. (That line of products is the subject to many lawsuits claiming they caused health issues and have created significant bad PR for the chain.) Meanwhile, Bloomberg reported that JPM has started its latest round of layoffs at the Vice President and Associate level of its consumer, energy, and healthcare units.

In stock legal and governmental news, on Tuesday, a Spanish startup filed a complaint against MSFT with the Spanish antitrust regulator, related to MSFT’s cloud computing practices. Later, the US Dept. of Commerce revoked some export licenses for good such as INTC and QCOM chips that were to be shipped to China’s Huawei. At the same time, Reuters reported that four sources tell it the US has held up the shipment of BA-made munitions to Israel. (The sales will reportedly eventually go through, but are being delayed based on priorities such as shipment to Ukraine.) Later, LEVI settled its lawsuit which accused an Italian fashion brand of infringing its trademarked pocket tab. (The terms of the settlement were not disclosed.) Elsewhere, Chinese company ByteDance filed suit in the US, arguing that the recently-passed law (passed as part of the Ukraine-Israel-Taiwan aide package) is unconstitutional on a number of grounds. (The law required ByteDance to sell TikTok to a US owner in the next nine months or cease all operations in the US. TiKTok has 170 million American users according to the company.)

So far this morning, AFRM, BUD, BCO, BAM, CLVT, ELAN, EMR, GFF, LCII, LPX, TIGO, NYT, QRTEA, REYN, SHOP, SUN, and VSH all reported beats on both the revenue and earnings lines. Meanwhile, ALIT, BR, EPC, HAIN, DINO, INGR, EYE, NFE, NI, and STWD missed on revenue while beating on earnings. On the other side, TEVA and UBER beat on revenue while missing on earnings. However, SATS, KMT, MIDD, ODP, PFGC, and RCM missed on both the top and bottom lines.

Overnight, Asian markets were mixed but leaned toward the red side. Japan (-1.63%), Shenzhen (-1.35%), and Singapore (-1.08%) led the region lower. In Europe, we see the opposite picture taking shape with only three of 15 bourses in the red at midday. The CAC (+0.81%), DAX (+0.34%), and FTSE (+0.25%) lead the region higher in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a start just on the red side of flat. The DIA implies a -0.05% open, the SPY is implying a -0.15% open, and the QQQ implies a -0.20% open at this hour. At the same time, 10-year bonds are back up to 4.488% and Oil (WTI) is down more than a percent to $77.54 per barrel in early trading.

The major economic news scheduled for Wednesday is limited to EIA Weekly Crude Oil Inventories (10:30 a.m.). The major earnings reports scheduled for before the open on AFRM, BUD, BCO, BR, CLVT, SID, SATS, EPC, ELAN, EMR, FWONK, FOXA, GLP, DINO, IEP, INGR, KMT, LCII, LSXMA, LPX, MIDD, EYE, NEUE, NFE, NYT, NI, ODP, PFGC, RCM, REYN, SHOP, SWX, STWD, SUN, TGNA, TEVA, TM, UBER, VSH, and VST. Then, after the close, AE, ABNB, AMC, APP, ARM, ATO, CE, CENTA, CENT, CAKE, CCU, COMP, CPAY, CAPL, ET, EXAS, FG, FLNC, FNF, FWRD, HLI, HUBS, CART, JXN, MFC, MATV, MMS, MKSI, MRC, NWSA, NTR, PAAS, QDEL, RGLD, SBGI, SSRM, STN, STE, SNEX, RUN, TKO, MODG, TSE, TTEC, VSTO, WTS, and WES report.

In economic news later this week, on Thursday, we get Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, and the Fed Balance Sheet. Finally, on Friday, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-Year Inflation Expectations, Michigan 5-Year Inflation Expectations, the WASDE report, and April Federal Budget Balance as well as Fed members Bowman and Vice Chair Barr speak.

In terms of earnings reports later this week, on Thursday, we hear from ADV, ALE, AZUL, BERY, CSIQ, CRL, COMM, CEG, EDR, EPAM, EVRG, HBI, HGV, H, ICL, IHRT, IBP, KELYA, NXST, NOMD, PZZA, PLTK, ACDC, RPRX, RBLX, SBH, SN, SOLV, SPB, TPR, TEF, TIXT, VTNR, VTRS, WBD, WMG, AKAM, COLD, AMN, BAP, DBX, SSP, EVH, FIHL, GEN, G, HRB, IAG, IOSP, MTD, PBA, RXT, RBA, and SLF. Finally, on Friday, AQN, AMCX, CLMT, CPG, CRH, ENB, HMC, and DNOW report.

In miscellaneous news, a plague of leafhopper insects has infected Argentinian corn crops. This insect, has the ability to reduce thousands of acres of corn crop to zero yield. (While the US is the largest producer of corn, Argentina is number four behind China and Brazil. A failure of the Argentine crop would cause significant impact on global corn prices.) At the moment, Argentina is forecasting a 17% reduction in its corn production. Elsewhere, US spot electricity and natural gas prices turned negative Tuesday in TX, CA, and AZ. (Ample Western hydropower, moderate weather, and limited storage capacity were forcing many LNG producers to flare (burn off) excess gas Tuesday, rather than slow/stop well production.)

In other news, Hamas and Israeli negotiators resumed ceasefire negotiations Tuesday. However, Israel began the new session by giving a Friday deadline for a deal, saying it would halt negotiations and initiate its “real Rafah operation” if a deal has not been agreed by then. (That distinction was needed because IDF ground forces attacked and captured the Gaza border crossing between Rafah and Egypt. That crossing is where 75% of Gaza aid passed prior to the war. That crossing is now completely shut down again as famine looms in that city and the whole Gaza strip.) It’s hard to predict how this will impact oil markets, with a return to talks a soothing sign while threats and continuing Israeli attacks not so soothing.

With that background, it looks as if traders are on the bearish side this morning. The QQQ in particular shows some follow through with the larger black candle being printed in the premarket. However, the two large-cap index ETFs opened the premarket flat and are printing more “indecisive candles” since that point. All three remain above their T-line (8ema). So, the short-term trend is now bullish again. Meanwhile, the mid-term remains sideways (choppy). The longer-term market remains Bullish as all three major index ETFs have returned within a few percent of all-time highs. Overall, the character of the market is gappy, choppy, and volatile. In terms of extension, none of the three major index ETFs are “too far” extended above their T-line, but the QQQ is starting to push that level. The T2122 indicator remains in its overbought area. So, while both sides still have room to run if they can gain the momentum to do so, the Bears have more slack to play with. In terms of those 10 big dog tickers, eight of the 10 are in the red this morning putting a considerable drag on the QQQ and SPY. Again, keep in mind that this is not a heavy news week but we do have a lot of earnings reports. Perhaps more importantly, there are several Fed speakers and undoubtedly a few others will also pop off. Any of those statements could swing markets, especially as Bulls are now dreaming of Fed rate cuts again.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Higher for Longer

Fed members once again suggesting higher for longer translated into Japan’s stock market experiencing a notable downturn, leading the regional declines on Wednesday. The Nikkei 225, a benchmark index for the Japanese stock market, fell by 1.63% to close at 38,202.37. Similarly, the Topix index, which represents a broader range of stocks, also suffered a decline, closing 1.45% lower at 2,706.43.

European markets showed a cautiously optimistic picture in the mid-morning trading session. The Stoxx 600 index, which tracks a broad spectrum of companies across Europe, saw a modest increase of 0.4% by 11:15 a.m. London time. Notably, shares of Siemens Energy, a major German industrial manufacturing firm, surged by up to 12.8% following the company’s announcement of an improved outlook for 2024, buoyed by the robust performance of its power grid business.

U.S.s tock futures indicate a relatively flat to slightly bearish open as Fed comments worry investors. Meanwhile, the futures for the S&P 500 and the Nasdaq 100 remained largely unchanged, as earnings data rolled out. The highlight in the economic calendar will be the remarks of several more Fed members commenting on the ongoing inflation fight.

Economic Calendar

Earnings Calendar

Notable reports for Thursday before the bell include ACMR, AFRM, BUD, ASC, ATHM, BCO, BR, CHH, CLVT, DIN, EDIT, EMR, EVER, FOXA, GFF, HAIN, DINO, HLLY, INGR, IMXI, INSW, KMT, KRNT, LCII, MCFT, NFE, NYT, NL, ODP, PAYO, PFGC, STWD, SUN, TBLA, TEVA, TPG, UBER, PRKS, VVV, VCEL, VERX, VSH, & WWW. After the bell include ARM, ACAD, ABNB, AMC, DOX, AAP, ATO, AZEK, BGS, BYND, BKH, BMBL, CE, CAKE, CPK, CLSK, CMP, CXW, CXT, CYTK, DUOL, ECPG, ET, EXAS, FNF, FLNC, FWRD, GNK, HL, HLIO, HPK, HMN, HUBS, IIPR, CART, JXN, JRVR, KNTK, KVYO, KGS, MNKD NWSA, NUS, OSUR, PYCR, PRIM, QNST, HOOD, RGLD, SBGI, SITM, SEDG, SLF, RUN, SUPN, TTD, TKO, MODG, COOK, TTEC, VSTO, VTLE, WTS, WES, & ZD.

News & Technicals’

Investors are closely scrutinizing the remarks made by Federal Reserve officials, seeking insights into the central bank’s interest rate trajectory for the current year. The consensus among Fed representatives this week has largely reaffirmed the central bank’s monetary policy stance, as outlined at the end of their most recent meeting. This has been reflected in the Treasury yields, with the 10-year Treasury yield experiencing a slight increase of over 1 basis point, reaching 4.479% as of 6:08 a.m. ET. Similarly, the 2-year Treasury yield also edged up by just over 1 basis point, standing at 4.839%. These movements in the yields are indicative of the market’s response to the Federal Reserve’s signals and the ongoing evaluation of economic indicators by investors.

The geopolitical landscape has been increasingly strained as the United States intensifies its trade restrictions and sanctions on China, with national security as the cited rationale. This escalation has had tangible economic repercussions, particularly in the wake of the Ukraine conflict. Trade interactions between the two powers have diminished by approximately 12%, and foreign direct investments have seen a more pronounced decline of 20% when compared to the figures within their respective economic blocs. The International Monetary Fund (IMF) has projected that, should the current rifts remain unaddressed, the global economy could potentially face a contraction as severe as 7% of the world’s GDP in what could be considered an extreme fallout scenario. This forecast serves as a stark reminder of the far-reaching implications that diplomatic tensions can have on international economic stability.

The United States has taken a significant step in its ongoing strategy to limit China’s technological advancement by revoking specific licenses for chip sales to Huawei. This action, announced on Tuesday, aligns with previous measures where export licenses have been withdrawn as part of a broader regulatory process. While the Commerce Department spokesperson refrained from discussing the particulars of the licenses affected, the confirmation of the revocation underscores the U.S. government’s firm stance on export controls to Huawei. Despite these regulatory challenges, Huawei’s consumer division is experiencing a revival, particularly following the launch of its Mate 60 Pro smartphone in August, which suggests resilience and adaptability in its business operations amidst tightening restrictions.

In a remarkable turn of events for the cryptocurrency world, the majority of customers affected by the collapse of the FTX exchange have been given a beacon of hope. A recent court filing has revealed that not only are these customers poised to recover their lost funds, but they may also receive additional compensation. FTX has reported an obligation of approximately $11.2 billion to its creditors. However, the exchange has managed to secure a substantial pool of assets, ranging between $14.5 billion and $16.3 billion, earmarked for distribution among the claimants. In an unprecedented move, customers with claims of $50,000 or less are set to receive about 118% of their validated claim value. This generous reimbursement plan is expected to cover around 98% of all creditors, signaling a significant recovery operation underway within the FTX financial landscape.

Rising bond yields due to higher for longer Fed comments have given rise to a bit of caution this morning. However, with a huge number of earnings plan for price volatility and intraday whipsaws to continue.

Trade Wisely,

Doug

Generally Good Earnings Help Market

Monday was a bullish, yet mostly sideways day in the market. SPY gapped up 0.51%, DIA gapped up 0.41%, and QQQ gapped up 0.43%. From there, all three major index ETFs traded sideways in roughly a half of a percent range. The SPY and QQQ both had a slight bullish trend to that grind. Meanwhile, DIA gave us a more volatile chop to the side and had a modest bearish trend to that sideways grind. A late-day rally took all three out very near their highs of the day. This action gave us gap-up large white-body candles with small lower wicks in the SPY and QQQ. Meanwhile, the DIA printed a gap-up, white-body Doji. All three remain above their T-line (8ema). This all came on well-below-average volume in all three of those major index ETFs.

On the day, all 10 sectors were again in the green with Technology (+1.55%) once again out front leading the market higher. Meanwhile, Consumer Defensive (+0.09%) lagged well behind the other sectors. VXX dropped another 2.66% to close at 12.45 and T2122 jumped up well into the overbought territory at 90.48. At the same time, 10-year bond yields fell again to 4.489% and Oil (WTI) gained half a percent to close at $78.55 per barrel. So, once again Monday, most of the market’s move came at the open. After a significant gap, the predominate direction of all three major index ETFs was to the side. Most talking heads seem to think this is chiefly driven by hope for a Fed rate cut soon. However, it is worth noting that three-fourths of the way through earnings season, five of the six “Magnificent 7” tickers have reported beats (only TSLA has missed, but it missed on both lines). This leaves only the biggest dog of them all (NVDA) to report on Wednesday. My point is that for those who believe in those seven tickers driving the market, they’ve gotten a lot of good news recently.

There was no major economic news scheduled for Monday.

In Fed Consumer Expectations Survey news, on Monday the NY Fed released results of its survey. The report found that respondents are bracing for higher housing costs again in the next year. On average that group predicts home prices will rise 5.1% (over the next year) which is far above the +2.6% increase they expected one year ago. However, five years from now, they see home prices only up 2.7% from current. So, on average the group expects home price inflation and then deflation. In terms of rental prices, the survey found respondents expect a 9.7% increase in rent on average in the next 12 months. (That is the second-highest expectation reading in history and up from the +8.2% in early 2023.) In terms of mortgage rates, the group now expect the average mortgage to be at 8.7% in a year and 9.7% in three years. (This survey was conducted while the average 30-year fixed-rate mortgage at Fannie Mae was at 7.22%.)

In Fed speak news, NY Fed President Williams said Monday that the FOMC’s next move is likely to be a cut in rates. Williams said “Eventually we’ll have rate cuts” but for now monetary policy is in a “very good place.” Williams did not offer a timetable for when a cut (next move) may take place. He also said the Fed’s shrinking of its Balance Sheet have gone well and have not rocked the boat. Later, Richmond Fed President Barkin said that up to now the fight on inflation has been on the supply side. However, to end inflation, the US will need to take a hit on the demand side. Specifically, Barkin said, “We got a lot of benefit last year on the supply side,” … “I do tend to imagine that we’re going to need a little more edge off of demand to get all the way (back to target).” He went on to say that he was optimistic that the current Fed Funds Rate was high enough to do the job. Still, when asked where he felt the biggest risk to the economy was, Barkin replied “I still have the weight going toward inflation.” “It’s a stubborn road back…It doesn’t mean you won’t get back. It just means it takes a while…to corral price setters (businesses) into believing they don’t really have a chance (for price increases without losing sales).

After the close, ACM, ATSG, BCC, BWXT, CBT, COKE, COHR, CPS, FN, FIS, IFF, ITUB, VAC, PLTR, O, SPG, and VRTX all reported beats on both the revenue and earnings lines. Meanwhile, AL, FMC, GT, JELD, MCHP, OTTR, RRX, and WMB missed on revenue while beating on earnings. On the other side, COTY, NE, PARR, and PRI all beat on revenue while missing on earnings. However, AAN, DOOR, and OGS missed on both the top and bottom lines. It is worth noting that SPG raised its forward guidance.

In stock news, on Monday, KKR announced it will buy Indian medical device maker Healthium Medtech from UK-based Apax Partners for roughly $839 million. At the same time, Reuters reported that DIS and CMCSA are seeking to hire a third-party financial advisor to resolve their dispute over the valuation of Hulu. (DIS will acquire a 33% stake in Hulu from CMCSA according to a deal struck in 2023, but value was undecided. JPM told DIS Hulu was worth $27.5 billion while MS told CMCSA that Hulu was worth $40 billion.) Later, Chinese premium EV-maker NIO announced it will launch its first mass-market EV by the end of this month, in Europe, for under $30k. At the same time, industry publication Electrek reported that TSLA laid off more employees Monday in its Software, Service, and Engineering departments. (Employees received layoff emails on Sunday.) Later, ALE announced it would go private at a $6.2 billion valuation (including debt to be assumed). This will result in a $67/share cash offer. Elsewhere, tech publication “The Information” reported Monday that MSFT is training a new, in-house AI model named MAI-1. The model, much bigger than any MSFT has trained internally in the past, is intended to compete with GOOGL and OpenAI. (The project is being headed by the co-founder of GOOGL’s DeepMind unit.)

In stock legal and governmental news, on Monday, HOOD received notice from the SEC that its cryptocurrency unit has been “preliminarily found” to have engaged in securities violations and will likely face either “cease and desist” action, civil court injunctions, or other penalties relate to the broker’s listings and crypto transactions. Later, the highest state court in MA began hearing a challenge to ballot initiatives proposed and paid for by LYFT and UBER, which would define gig workers explicitly as contractors, not eligible for benefits, minimum wage laws, worker protection laws, and tax withholding. (No timeframe for a decision is available.) At the same time, the Wall Street Journal reported that the FAA has opened a new investigation into BA over inspections the company recently admitted its employees skipped on 787 Dreamliner planes in order to maintain production schedules. The investigation will also determine whether the documentation submitted to the FAA indicated those inspections had been made and passed (if documents were falsified). Later, a Us judge formally ended the US Dept. of Justice case against GS related to the bank’s work with corrupt Malaysian fun 1MDB, accepting the $2.9 billion in penalties GS paid. Elsewhere, Reuters reports that crypto “Super PACs” have raised more than $102 million to spend on the 2024 Congressional elections. ($54 million of this reportedly came from COIN and Ripple Labs.) Reports say much of this will be focused on defeating Democratic Senators Brown (OH) and Tester (MT) who have been critical of crypto.

Overnight, Asian markets were mixed but leaned to the bullish side with seven of the 12 exchanges in the green. South Korea (+2.16%), Japan (+1.57%), and Australia (+1.44%) were by far the biggest movers and led the region higher. However, in Europe, 13 of the 15 bourses are in the green at midday with only Russia (-0.44%) worse than flat. The CAC (+0.37%), DAX (+0.63%), and FTSE (+1.03%) are leading the region higher in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a mixed open near flat. The DIA implies a +0.07% open, the SPY is implying a dead flat open, and the QQQ implies a -0.20% open at this hour. At the same time, 10-year bond yields are down to 4.461% and Oil (WTI) is off four-tenths of a percent to $78.15 per barrel in early trading.

The major economic news scheduled for Tuesday includes the EIA Short-Term Energy Outlook (noon), March Consumer Credit (3 p.m.), and API Weekly Crude Stocks (4:30 p.m.). Fed member Kashkari also speaks (11:30 a.m.). The major earnings reports scheduled for before the open on Tuesday include GOLF, AHCO, ALGT, GBTG, ARMK, ATKR, AVNT, BLMN, BP, BLDR, CEIX, CROX, DDOG, DK, DUK, ERJ, ENR, EXPD, RACE, FTRE, GEO, GTN, HSIC, J, KVUE, NJR, NRG, OSCR, MD, PRGO, ROK, SCSC, SRE, SPR, SGRY, TPX, BLD, TDG, UBS, VVX, and DIS. Then, after the close, KLG, AMRK, AGL, ARKO, AIZ, BTG, BIO, BRFS, BHF, CRC, CHRD, CPNG, EC, EA, GMED, GO, GXO, HY, IAC, ICUI, JKHY, KGC, KD, LYFT, MTW, MASI, MTCH, MCK, OXY, OVV, PR, RYAM, RRR, RNG, RIVN, SU, VIV, TOST, TWLO, and WYNN report.

In economic news later this week, on Wednesday, EIA Weekly Crude Oil Inventories are reported. On Thursday, we get Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, and the Fed Balance Sheet. Finally, on Friday, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-Year Inflation Expectations, Michigan 5-Year Inflation Expectations, the WASDE report, and April Federal Budget Balance as well as Fed members Bowman and Vice Chair Barr speak.

In terms of earnings reports later this week, on Wednesday, AFRM, BUD, BCO, BR, CLVT, SID, SATS, EPC, ELAN, EMR, FWONK, FOXA, GLP, DINO, IEP, INGR, KMT, LCII, LSXMA, LPX, MIDD, EYE, NEUE, NFE, NYT, NI, ODP, PFGC, RCM, REYN, SHOP, SWX, STWD, SUN, TGNA, TEVA, TM, UBER, VSH, VST, AE, ABNB, AMC, APP, ARM, ATO, CE, CENTA, CENT, CAKE, CCU, COMP, CPAY, CAPL, ET, EXAS, FG, FLNC, FNF, FWRD, HLI, HUBS, CART, JXN, MFC, MATV, MMS, MKSI, MRC, NWSA, NTR, PAAS, QDEL, RGLD, SBGI, SSRM, STN, STE, SNEX, RUN, TKO, MODG, TSE, TTEC, VSTO, WTS, and WES report. On Thursday, we hear from ADV, ALE, AZUL, BERY, CSIQ, CRL, COMM, CEG, EDR, EPAM, EVRG, HBI, HGV, H, ICL, IHRT, IBP, KELYA, NXST, NOMD, PZZA, PLTK, ACDC, RPRX, RBLX, SBH, SN, SOLV, SPB, TPR, TEF, TIXT, VTNR, VTRS, WBD, WMG, AKAM, COLD, AMN, BAP, DBX, SSP, EVH, FIHL, GEN, G, HRB, IAG, IOSP, MTD, PBA, RXT, RBA, and SLF. Finally, on Friday, AQN, AMCX, CLMT, CPG, CRH, ENB, HMC, and DNOW report.

So far this morning, GOLF, AVNT, BLDR, CEIX, CROX, DDOG, ENR, RACE, GFS, GTN, J, OSCR, ROK, SGRY, TDG, UBS, VVX, and WAT all reported beats on both the revenue and earnings lines. Meanwhile, ARMK, ATKR, DK, DUK, HSIC, NJR, NRG, MD, PRGO, TPX, BLD, and DIS all missed on revenue while beating on earnings. On the other side, AHCO and GEO beat on revenue while missing on earnings. However, BLMN and BP missed on both the top and bottom lines.

In miscellaneous news, the largest physician-run hospital network in the US (Steward Health Care), which operates 31 hospitals, filed for Chapter 11 bankruptcy Monday after failing to secure a new loan from its landlord MPW. Steward has nearly 30,000 employees, including 4,500 doctors and operates 400 locations (not just the 31 hospitals). Elsewhere, the CDC said Monday that it had asked state health depts. And asked that they provide protective gear to farm workers to reduce the risk of H5N1 bird flu transmission to (and then between) humans. (There has already been one case of a farm work contracting bird flu from a dairy herd, which had been contaminated. The case was mild, similar to traditional flu.) The USDA had previously said that H5N1 had likely been circulating in poultry and dairy animals since November and was first found on March 25. So far, test have found pasteurized milk contains remnants but remains safe for human consumption.

In other news, Hamas made news Monday by announcing they had agreed to a ceasefire plan proposed by Egypt and Qatar. (Reports had said Israel had signed off on the deal before it was proposed.) However, Israel said what Hamas agreed to was nowhere close to what they could accept…implying Hamas agreed to its own counter to the deal shown to them. In the meantime, Israeli Defense Forces announced it has begun a “limited” ground offensive into Rafah (city of 1.4 million). This includes the takeover of the Rafah side of the border crossing to Egypt. While oil markets calmed on the news midday Monday, the IDF operation in Rafah (where explosions were heard Monday night) is likely to stoke oil fears again. In the meantime, Israeli negotiators said they will travel to resume ceasefire talks as both sides work to blame the other for no halt to fighting.

With that background, it looks as if traders are undecided this morning. The two large-cap index ETFs opened the premarket flat and have printed mostly wicks since that point. Meanwhile, the QQQ gapped down to start the early session and then has printed its own indecisive candle. All three remain above their T-line (8ema). So, the short-term trend is now bullish again. Meanwhile, the mid-term remains sideways. The longer-term market remains Bullish as all three major index ETFs have returned within a few percent of all-time highs. Overall, the character of the market is gappy, choppy, and volatile. In terms of extension, none of the three major index ETFs are “too far” extended above their T-line, but the QQQ is starting to push that level. However, at the same time, the T2122 indicator is now well inside of its overbought area. So, while both sides still have room to run if they can gain the momentum to do so, the Bears have more slack to play with. In terms of those 10 big dog tickers, eight of the 10 are in the red with the two biggest dogs TSLA (-1.46%) and NVDA (-1.34%) leading the QQQ (and probably overall market) lower. Again, keep in mind that this is not a heavy news week but we do have a lot of earnings reports. Perhaps more importantly, there are several Fed speakers and undoubtedly a few others will also pop off. Any of those statements could swing markets, especially as Bulls are now dreaming of Fed rate cuts again.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Positive Earnings Results

South Korean stocks surged ahead in the Asia-Pacific region on Tuesday, buoyed by the positive earnings results on Wall Street. The Kospi index, South Korea’s benchmark stock index, soared 2.16% to close at 2,734.36, marking its highest point in over a month. Meanwhile, the Kosdaq, known for its smaller-cap stocks, also enjoyed gains, albeit more modest, finishing 0.66% higher at 871.26. In contrast, the Reserve Bank of Australia maintained a steady course, holding its benchmark lending rate unchanged at 4.35% for the fourth consecutive meeting, signaling a cautious approach amidst global economic shifts.

European markets kicked off Tuesday’s trading session on a high note. The Stoxx 600, a key regional index, witnessed a 0.6% uptick by 9:30 a.m. in London. Leading the charge were financial services, which saw a notable 2.2% increase. A standout performer was the Swiss banking behemoth UBS. This positive financial revelation propelled UBS shares to climb by 8% during the morning trading hours.

U.S. stock futures displayed mixed futures results near the break-even point on Tuesday, with the Dow Jones Industrial Average poised to extend its winning streak to a fifth consecutive day amid a fresh wave of earnings reports. Dow futures edged higher by 70 points, translating to a modest gain of 0.2%. The S&P 500 futures saw a slight increase of 0.1%, reflecting cautious optimism. In contrast, the Nasdaq 100 futures experienced a minor dip, also by 0.1%, suggesting a more reserved stance among tech investors.

Economic Calendar

Earnings Calendar

Notable reports for Tuesday before the bell include DIS, AHCO, APLS, ARMK, AVNT, BLMN, BLDR, CELH, CROX, DDOG, DK, DUK, ENR, NPO, EXPD, FWRG, GFS, GOGO, HR, HSIC HLMN, IONS, J, KVUE, NJR, NRG, OSCR, PRGO, PTLO, ROK, SCSC, SERE, SPR, SQSP, TPX, BLD, TDG, UBS, WAT, WOW, & KLG. After the bell include RDDT, AWR, ANDE, ANGI, ALTM, ANET, AIZ, AGO, ALAB, ASTH, BIO, BL, BHF, CDRE, CRC, CHRD, CRUS, CFLT, CRSR, CPNG, DEI, BROS, EA, FLYW, GMED, GPRO, GO, GXO HALO, IAC, IRBT, JKHY, KTOS, KD, LAZR, LYFT, MGY, MTW, MTCH, MCK, MLNK, MYGN, OXY, LPRO, PCRX, PR, PROS, PUBM, QLYS, RDFN, RVLV, RNG, RIVN, SHLS, SONO, STAA, RGR, TOST, TRIP, TWLO, UPST, VECO, SPCE, WYNN, & ZI.

News & Technicals’

Disney has delivered a commendable financial performance, exceeding earnings estimates while achieving revenue that met analyst projections. In a notable milestone, the company’s streaming services, Disney+ and Hulu, reported a combined profit for the first time in their operational history. However, when accounting for ESPN+, the overall streaming unit faced a setback, incurring a loss of $18 million for the quarter. This contrasted with the downturn in traditional revenue streams, as both TV revenues and box office sales experienced a slump during the same period. The mixed results highlight the shifting landscape of media consumption, with streaming services gaining ground despite challenges, while conventional media formats struggle to maintain their foothold.

UBS has made a remarkable financial turnaround, reporting a significant return to profitability after enduring losses in the previous two quarters. The Swiss financial titan exceeded first-quarter expectations, largely due to a surge in wealth management revenues. Looking ahead, UBS has outlined a strategic roadmap, announcing its anticipation to finalize the merger with Credit Suisse into a unified U.S. intermediate holding company in the upcoming second quarter. Furthermore, the consolidation of its Swiss operations is slated for completion in the third quarter. This ambitious integration reflects UBS’s commitment to streamlining its global operations and fortifying its position in the competitive financial landscape.

Palantir Technologies, the data analytics firm, has delivered a robust financial performance, surpassing revenue expectations and achieving an Earnings Per Share (EPS) that aligns with analyst predictions. However, the company has tempered expectations with its projection of weaker-than-anticipated full-year guidance. Despite this cautious outlook, Palantir has consistently demonstrated profitability, marking its sixth consecutive quarter of net profit. In a significant development, the company secured a lucrative $178 million contract with the U.S. Army. This contract is aimed at advancing the Army’s technological capabilities by developing a state-of-the-art, field-deployable sensor station, which underscores Palantir’s growing influence and integral role in national defense initiatives.

BP, the oil and gas giant, has reported a dip in its first-quarter profits, which stood at $2.7 billion. This decline is primarily attributed to the downturn in oil and gas prices, coupled with a “significantly weaker” fuel margin. The trend of shrinking profits is not isolated to BP; it reflects a broader pattern within the energy industry, where companies are grappling with reduced year-on-year profits, especially impacted by the falling market gas prices. Despite these challenges, BP has reaffirmed its commitment to its shareholders by announcing share buybacks totaling $3.5 billion for the first half of 2024, signaling confidence in its financial strategy and prospects.

The market will be keenly focused and hoping for positive earnings results with little to no inspiration coming from the economic calendar. Expect whipsaws and price volatility as the reacts.

Trade Wisely,

Doug

Rate Cut Hopes

On Monday, Asia-Pacific stock markets echoed the upward trajectory of Wall Street, buoyed by a U.S. jobs report that fell short of expectations, signaling rate cut hopes. Australia’s S&P/ASX 200 index witnessed a 0.7% uplift, settling at 7,682.4 and marking its third consecutive session of advances. In a similar vein, Hong Kong’s Hang Seng index experienced a modest rise of 0.47%, while mainland China’s CSI 300 surged 1.48% to conclude at 3,657.88, as traders resumed activity after the Labor Day holiday. The collective gains across these key indices reflect a cautiously optimistic sentiment permeating the region’s markets.

European markets experienced a positive start to the week, with key indices climbing. The French CAC 40 edged up by 0.5%, while the German DAX notched a gain of 0.6%. The Italian FTSE MIB outperformed its peers with a rise of 0.9%. Meanwhile, the U.K.’s FTSE 100 was absent from the day’s trading due to a public holiday, leading to expectations of thinner trading volumes across European markets.

U.S. stock futures signaled a buoyant mood on Wall Street on Monday, as market participants geared up to extend the robust gains witnessed in the previous session. The upbeat sentiment was further bolstered by the financial update from Warren Buffett’s Berkshire Hathaway, which unveiled a remarkable nearly 40% increase in its operating earnings for the first quarter compared to the same period last year. This financial feat coincided with Berkshire’s much-anticipated annual shareholder meeting held on Saturday.

Economic Calendar

Earnings Calendar

Notable reports for Monday before the bell include AMG, BCRX, BNTX, FRPT, JLL, NSSC, NWN, PRFT, SAVE, SHO, & THUS. After the bell includes ADTN, AL, AXON, BRBR, BYON CBT, COHR, COTY, FN, FIS, FMC, GBDC, GT, HIMS, IFF, JJSF, LCID, LITE, VAC, MTTR, MCHP, NIHI, ME, OGS, OTTR, PLTR, PLYA, PRI, PRA, PRI, PRA, O, RRX, RKX, RKLB, SAFE, SWAV, SPG, TALO, TDC, TBI, VRNS, VRTX, VMEO, VNO, & WMB.

News & Technicals’

In the city of Rafah, a humanitarian crisis looms large as over 1.2 million individuals have sought refuge, fleeing from various regions of the Gaza Strip. The majority find themselves in makeshift tented communities, grappling with a dire scarcity of essential resources such as clean water, adequate food supplies, and fundamental medical provisions. Amidst this escalating situation, the White House, alongside prominent international entities including the United Nations and the World Health Organization, has implored Israel to refrain from launching an offensive in the area. They caution that such actions could precipitate disastrous humanitarian repercussions, further exacerbating the plight of the already vulnerable population seeking shelter in Rafah.

The landscape of energy consumption is undergoing a transformative shift, with natural gas producers expressing optimism about the burgeoning demand. This confidence is largely attributed to the colossal energy requirements of burgeoning technologies such as artificial intelligence and the proliferation of data centers. A projection by Wells Fargo anticipates a 20% surge in electricity demand by the year 2030, underscoring the escalating need for power soon. Power companies are advocating for natural gas as an indispensable component of the energy mix, emphasizing its critical role in maintaining a steady supply of electricity, especially during periods when renewable sources fall short of generating sufficient power. This stance highlights the intricate balance between fostering sustainable energy practices and ensuring the reliability of power systems in an increasingly digital world.

Ant Group is poised to make a significant leap in the global payments landscape with its Alipay+ service, targeting expansion across Europe, the Middle East, and Latin America. Douglas Feagin, the senior vice president of Ant Group, shared insights with CNBC on consumer behavior, noting a preference for travelers to utilize their familiar domestic e-wallets while abroad, rather than transitioning to unfamiliar apps. Launched in 2020, Alipay+ has facilitated this preference by enabling international visitors to make payments in China—and potentially in other nations—using their native payment apps through the simple act of scanning Alipay’s QR codes. This strategic move by Ant Group caters to the convenience and comfort of users, fostering a seamless cross-border transaction experience that aligns with the modern, mobile-centric lifestyle.

U.S. Treasury yields experienced a downtrend on Monday, continuing the downward momentum from Friday’s session following the release of the April jobs report, which revealed payroll growth that didn’t meet expectations. The 10-year Treasury yield decreased by 2 basis points, landing at 4.475%. Concurrently, the 2-year Treasury yield also saw a marginal decline of 1 basis point, settling at 4.789%. It’s important to note that in the bond market, yields and bond prices have an inverse relationship. To put it into perspective, a single basis point is equivalent to 0.01%. This shift in yields reflects the market’s reaction to economic indicators and influences investment strategies across the board.

With a very light week of economic data, earnings and rate cut hopes will drive the market sentiment so continue to expect considerable volatility. Morning gaps will likely continue to produce whipsaws so plan your risk carefully.

Trade Wisely,

Doug

BRKB Reported Saturday Bulls Push Early

Friday saw another significant gap higher. The SPY gapped up 1.21%, DIA gapped up 1.28%, and QQQ gapped up 1.75%. From there, all three major index ETFs wobbled to the side, reentering the gap and crossing above the open, but never straying too far from the opening price. This lasted the entire session. This gave us gap-up, indecisive candles in all three. SPY printed a white-bodied Doji, QQQ gave us a white-bodied Spinning Top, and DIA printed a black-body Doji. All three are now firmly above their T-lines (8emas). This happened on average volume in the QQQ and DIA as well as just-less-than-average volume in the SPY.

On the day, all 10 sectors were in the green with Technology (+1.86%) far out front (by 0.75%) while Energy (+0.40%) lagged the other sectors. VXX dropped another 3.47% to close at 12.78 and T2122 climbed to the very top edge of its mid-range at 79.25. At the same time, 10-year bond yields fell sharply to 4.497% and Oil (WTI) fell 1.08%, to close at $78.10 per barrel. So, Friday saw all of its move in the opening gap. Most of the market analysts seemed to think that a decline in jobs increases and a climb in the Unemployment Rate will help clear the way for a Fed rate cut. After that start to the session, there were some waves but price oscillated in a fairly tight range around that opening price. It was as if traders had decided to head for the weekend early.

The major economic news scheduled for Friday included April Avg. Hourly Earnings (Year-on-Year) increased less than expected at +3.9% (compared to a forecast of +4.0% and the March increase of 4.1%). At the same time, April Nonfarm Payrolls increased far less than predicted at +175k (versus the +238k forecast and dramatically less than the March +315k). Meanwhile, April Private Nonfarm Payrolls also increased less than anticipated at +167k (compared to the +181k forecast and far less than the March +243k reading). The April Participation Rate remained steady at 62.7% (the same as March’s participation rate). Together, this gave us an April Unemployment Rate which increased to 3.9% (compared to a forecast and March value of 3.8%). Later, the April S&P Global Services PMI came in higher than expected at 51.3 (versus a 50.9 forecast but down from March’s 51.7). Combined with Thursday’s Mfg. data this gave us an April S&P Global Composite PMI of 51.3 (compared to a 50.9 forecast and March’s reading of 52.1). Later, the ISM Non-Mfg. Employment Index was lower than anticipated at 45.9 (versus a 49.0 forecast and the March 48.5 value). At the same time, the ISM Non-Mfg. PMI also came in low at 49.4 (compared the 52.0 forecast and the March reading of 51.4). On the cost side, the ISM Non-Mfg. PMI Price Index were significantly higher than expected at 59.2 (versus the 55.0 forecast and a March value of 53.4).

In Fed speak news, on Friday Fed Governor Bowman (a hawk) told an audience of bankers that she supports the current FOMC stance but still fears inflation risks. “My baseline outlook continues to be that inflation will decline further with the policy rate held steady, but I still see a number of upside inflation risks that affect my outlook, … While the current stance of monetary policy appears to be at a restrictive level, I remain willing to raise the federal funds rate at a future meeting should the incoming data indicate that progress on inflation has stalled or reversed.” Later, after the close, Chicago Fed President Goolsbee told a conference that the Fed’s “dot plots” (which are published once per quarter, showing the inflation predictions of each Fed member) need more context. Goolsbee said, “the dot plot is just a collection of opinions without economic content … Because it can’t be connected to the economic conditions the participant thinks will justify that interest rate, there is nothing to tell us why they think this a reasonable choice.” Instead, Goolsbee proposed “A matrix that anonymously matches the economic forecasts to the rate path for each participant would answer some important questions.”

In stock news, on Friday, ALK announced that it had received $61 million in credit toward future purchases of BA jets (in addition to the $162 million cash ALK got from BA) as compensation for the temporary grounding of all 737 MAX 9 jets earlier this year. At the same time, Reuters reported that LUV will be forced to reduce the hours (and thus pay) of its pilots later this year as it grapples with a lack of jets due to BA delivery delays. This is a problem, because LUV, like all major airlines has been trying to increase its pilot staff amidst an industry-wide pilot labor shortage. Lower pay will hardly help the plans to increase staff. Later, the New York Times reported that PARA will let its exclusive negotiation deal with Skydance lapse in the face of a competing bid from SONY and APO. At the same time, XOM told Reuters Friday that after reaching a deal with the FTC for approval of its acquisition of PXD, the oil giant expects it to take between 18 and 24 months to achieve full synergies of the purchase. (This will push XOM’s Permian Basin oil output by 1.3 million barrels per day with another 700k bpd added by 2027 due to integrating PXD technologies.

In stock legal and governmental news, on Friday, the Treasury Dept. gave automakers an extension until 2027 to remove Chinese-sourced trace minerals from electric vehicle batteries and still have their electric vehicles qualify for tax credits. (The announcement attributed the extension to the minerals being hard to source from other sources at this time.) At the same time, GOOGL and the Dept. of Justice finished closing arguments in the antitrust case the US brought against GOOGL related to web search and related advertising. Later, the FTC requested more information from NVO relate to its $16.5 billion bid to acquire CTLT. At the same time, GS announced it had finally reached an agreement in-principle to settle a 2014 class-action lawsuit over GS trading in platinum and palladium. (No terms were announced.) Later, AMRX announced it had reached a $270 settlement (payable over 10 years) agreement over its involvement in the US opioid epidemic.

Overnight, Asian markets were mixed but leaned toward the green side with eight of the 12 exchanges in the green. Shenzhen (+2.00%), Shanghai (+1.16%), and Taiwan (+0.95%) led the region higher. Meanwhile, in Europe, 13 of the 15 bourses are in the green at midday. The CAC (+0.76%), DAX (+0.89%), and FTSE (+0.51%) lead the region higher in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a green start to the day. The DIA implies a +0.32% open, the SPY is implying a +0.33% open, and the QQQ implies a +0.23% open at this hour. At the same time, 10-year bond yields are down to 4.481% and Oil (WTI) is up just less than a percent to $78.86 per barrel in early trading.

The major economic news scheduled for Monday is limited to Fed member Williams speaking at 1 p.m. The major earnings reports scheduled for before the open on Monday include, AMG, AMR, BRKB, BNTX, CAN, JLL, SAVE, THS, and TSN. Then, after the close, AAN, ACM, AL, BCC, BWXT, CBT, COHR, COTY, FN, FIS, FMC, GT, IFF, ITUB, JELD, VAC, DOOR, MCHP, NE, OGS, OTTR, PLTR, PARR, PRI, O, RRX, SPG, VRTX, and WMB report.

In economic news later this week, on Tuesday, we get March Consumer Credit, API Weekly Crude Stocks, and Fed member Kashkari speaks. Then Wednesday, EIA Weekly Crude Oil Inventories are reported. On Thursday, we get Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, and the Fed Balance Sheet. Finally, on Friday, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-Year Inflation Expectations, Michigan 5-Year Inflation Expectations, the WASDE report, and April Federal Budget Balance as well as Fed members Bowman and Vice Chair Barr speak.

In terms of earnings reports later this week, on Tuesday, we hear from GOLF, AHCO, ALGT, GBTG, ARMK, ATKR, AVNT, BLMN, BP, BLDR, CEIX, CROX, DDOG, DK, DUK, ERJ, ENR, EXPD, RACE, FTRE, GEO, GTN, HSIC, J, KVUE, NJR, NRG, OSCR, MD, PRGO, ROK, SCSC, SRE, SPR, SGRY, TPX, BLD, TDG, UBS, VVX, DIS, KLG, AMRK, AGL, ARKO, AIZ, BTG, BIO, BRFS, BHF, CRC, CHRD, CPNG, EC, EA, GMED, GO, GXO, HY, IAC, ICUI, JKHY, KGC, KD, LYFT, MTW, MASI, MTCH, MCK, OXY, OVV, PR, RYAM, RRR, RNG, RIVN, SU, VIV, TOST, TWLO, and WYNN. Then Wednesday, AFRM, BUD, BCO, BR, CLVT, SID, SATS, EPC, ELAN, EMR, FWONK, FOXA, GLP, DINO, IEP, INGR, KMT, LCII, LSXMA, LPX, MIDD, EYE, NEUE, NFE, NYT, NI, ODP, PFGC, RCM, REYN, SHOP, SWX, STWD, SUN, TGNA, TEVA, TM, UBER, VSH, VST, AE, ABNB, AMC, APP, ARM, ATO, CE, CENTA, CENT, CAKE, CCU, COMP, CPAY, CAPL, ET, EXAS, FG, FLNC, FNF, FWRD, HLI, HUBS, CART, JXN, MFC, MATV, MMS, MKSI, MRC, NWSA, NTR, PAAS, QDEL, RGLD, SBGI, SSRM, STN, STE, SNEX, RUN, TKO, MODG, TSE, TTEC, VSTO, WTS, and WES report. On Thursday, we hear from ADV, ALE, AZUL, BERY, CSIQ, CRL, COMM, CEG, EDR, EPAM, EVRG, HBI, HGV, H, ICL, IHRT, IBP, KELYA, NXST, NOMD, PZZA, PLTK, ACDC, RPRX, RBLX, SBH, SN, SOLV, SPB, TPR, TEF, TIXT, VTNR, VTRS, WBD, WMG, AKAM, COLD, AMN, BAP, DBX, SSP, EVH, FIHL, GEN, G, HRB, IAG, IOSP, MTD, PBA, RXT, RBA, and SLF. Finally, on Friday, AQN, AMCX, CLMT, CPG, CRH, ENB, HMC, and DNOW report.

So far this morning, BRKB, JLL, and L reported beats on both the revenue and earnings lines. Meanwhile, AMG and TSN missed on revenue while beating on earnings. On the other side, CNA and THS missed on revenue while beating on earnings. However, SAVE missed on both the top and bottom lines.

On Saturday, “Woodstock for Capitalists” took place in Omaha. Warren “The Oracle of Omaha” Buffett spoke and BRKB reported a massive 32% increase (year-over-year) in Q1 operating income. Yet, the company managed to report a huge 66% drop in net income for the quarter. As of the end of the quarter, BRKB was sitting on a record $189 billion pile of cash-on-hand. During the quarter, BRKB reduced its holding of AAPL by 13%, down to (a paltry) $135.4 billion. Still, AAAPL remains the biggest holding in the BRKB portfolio. During his Q/A session, Warren Buffett said he expects US taxes to rise to tackle the country’s wide federal deficit. Buffett said, “I think higher taxes are likely.” “They (Congress and the President) may not want to decrease spending and they may decide they’ll take a larger percentage of what we own…and we’ll pay it.” He continued, “Almost everybody I know pays a lot more attention to not paying taxes than I think they should, we don’t mind paying taxes at Berkshire.” Later, in answering questions, Buffett made it clear that Greg Abel will succeed him as the head of BRKB, claiming that Abel is already handling almost all of the company business. Specifically, Buffett said, “The number of calls I get from managers is essentially awfully close to zero and Greg is handling those. I don’t know quite how he does it, but we’ve got the right person, I can tell you that.”

With that background, it looks as if the Bulls are working again this morning. The premarket started a bit higher and all three major index ETFs have printed white-body candles since then in the early session. Only SPY and QQQ show any wick and those are both small upper wicks at this point. All three remain above their T-line (8ema). So, the short-term trend is now bullish again. Meanwhile, the mid-term remains bearish. The longer-term market remains Bullish but under pressure. Overall, the character of the market is indecisive, choppy, and volatile. In terms of extension, none of the three major index ETFs is extended above their T-line. At the same time, the T2122 indicator is now just outside of its overbought area at the top of the mid-range. So, both sides still have room to run if they can gain the momentum to do so. In terms of those 10 big dog tickers, eight of the 10 are in the green with AMD well out in front leading the charge. However, AAPL (-0.26%) is by far the biggest drag (probably on news Buffett reduced the BRKB holdings of AAPL) as the joy of the huge buyback program announcement fades a bit early. Keep in mind that this is not a heavy news week but we do have a lot of earnings reports. Perhaps more importantly, there are several Fed speakers planned and undoubtedly others will also pop off. Any of those statements could rock markets as the Bulls are now dreaming of a rate cut again.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Member e-Learning 5-2-24 – Doug

Member e-Learning 5-2-24 – John

Unprecedented AAPL Buyback Program

Markets gapped up Thursday as traders rethought their late-day selloff from the day before. SPY gapped up 0.76%, DIA gapped up 0.61%, and QQQ gapped up 0.94%. At that point, all three major index ETFs faded and recrossed the gap by 10:10 a.m. However, this was a Bear Trap with all three major index ETFs starting a steady rally at 10:15 a.m., recrossing the gap and continuing North and reaching the highs of the day at 3:15 p.m. From there, SPY, DIA, and QQQ all sold off modestly the last 45 minutes of the day. This action gave us white-bodied Hammer-type candles in all three major index ETFs. All three crossed back above their T-line (8ema) during the session. This all happened on less than average volume in all three, with QQQ have by far the weakest volume relative to its average.

On the day, all 10 sectors were in the green with Consumer Cyclical (+2.01%) far out front of Technology (+1.50%) which was far out in front of the other sectors, leading markets higher. At the same time, SPY gained 0.93%, DIA gained 0.89%, and QQQ gained 1.28%. VXX dropped 3.29% to close at 13.24 and T2122 popped higher and is now in the top-end of its mid-range at 70.16. 10-year bond yields fell to 4.589% and Oil (WTI) was just on the red side of flat, closing at $78.96 per barrel. So, Thursday was a rebound day after Wednesday’s Fed indecision. However, truly, nothing major has changed in the last 10-12 days as bullish moves are met with bearish moves and visa-versa.

The major economic news scheduled for Thursday included March Exports, which came in lower at $257.60 billion (compared to February’s $263.00 billion reading). The March Imports also fell to $327.00 billion (down from $331.90 billion in February). This gave us a March Trade Balance of -$69.40 billion, which was down slightly from the February -$69.50 billion value. At the same time, Weekly Initial Jobless Claims were lower than expected at 208k (compared to a 212k forecast but flat from the prior week’s 208k). On the ongoing side, Weekly Continuing Jobless Claims were flat at 1,774k (versus a forecast of 1,800k and the prior week’s 1,774k). Meanwhile, the Q1 Nonfarm Productivity was down slightly to +0.3% (compared to a much higher forecast value of +0.8% but only down a touch from Q4’s +3.5%). However, the bigger miss was on Q1 Unit Labor Cost (preliminary) which was up 4.7% (versus a +3.6% forecast and greatly higher than Q4’s +0.4%). Later, March Factory Orders were up to +1.6% (which was in line with the +1.6% forecast but up nicely from February’s +1.2%). Then, after the close, the Fed Balance Sheet showed a $40 billion reduction from $7.402 trillion to $7.362 trillion.

After the close, AMGN, AAPL, ACA, SQ, BKNG, BFAM, COIN, CTRA, DVA, EOG, EXPE, FTNT, GDDY, HOLX, HUN, ILMN, MTZ, MELI, MSI, OPEN, OTEX, PTVE, REZI, RGA, RKT, RYAN, SEM, and TXRH all reported beats on both the revenue and earnings lines. At the same time, AES, DLR, ED, FND, IR, ZEUS, POST, SM, and X missed on revenue while beating on earnings. On the other side, ALHC, BECN, CIVI, DKNG, LYV, MODV, and WSC beat on the revenue line while missing on earnings. However, AEE, WTRG, MNST, OEC, and SWN missed on both the top and bottom lines.

In stock news, on Thursday, CB told the Wall Street Journal is it preparing to pay a $350 million claim to the state of MD related to the collapse of the Francis Scott Key Bridge in March. At the same time, NVO announced it will be reducing the price of its blockbuster weight loss drug Wegovy amidst an increase in competition from LLY. After the close, AAPL reported that iPhone sales fell less than expected (down 10% year on year in Q1) while overall sales fell 4%. However, AAPL also announced the biggest stock buyback program in the history of the market at $110 billion (a 22% increase over their record $90 billion repurchase program from last year). AAPL share soared in post-market trading on the news. Also after the close, AMGN announced it had scrapped plans for a pill version of a weight loss drug and will move ahead with an injection version similar to NVO and LLY drugs in the same class. For what it is worth, the CEO of AMGN touted excellent early-phase results of its injectable weight loss candidate. Finally, SONY and APOS both expressed interest in buying PARA for $26 billion in cash as the company considers a bid from Skydance. Under the alternate offer, SONY would be the majority shareholder with APOS holding a minority position.

In stock legal and governmental news, on Thursday, a Russian court ruled that JPM assets held in accounts which cannot be transferred outside of Russia will not be seized. The court said this covered $2.25 billion of JPM’s assets. Later, the FCC told Congress Thursday that 40% of US telecom providers report they will need additional government money to fund the removal of Chinese equipment from Huawei and ZTE from their networks. (Congress approved $1.9 billion and the telecom companies report $4.98 billion will be needed to cover the 39.5% of replacement cost that the law said would be covered.) At the same time, SPR filed suit in US district court to block TX from demanding documents and conducting a probe of the company (which does no manufacturing in TX). Later, RIVN reported that it received $827 million in incentive packages from the state of IL to help fund the expansion of the company’s operations in that state. At the same time, the Wall Street Journal reported that the US Dept. of Justice has launched a probe into how Chinese drug traffickers have laundered money from the sale of fentanyl through TD (TD Bank). After the close, the USDA announced that WMT had recalled 16,000 pounds of ground beef due to a suspicion it is infected with E. coli.

Overnight, Asian markets were evenly mixed. Hong Kong (+1.48%) led the gainers while Shenzhen (-0.90%) paced the losses. In Europe, the bourses are much more bullish with 12 of 15 exchanges in the green at midday. The CAC (+0.53%), DAX (+0.40%), and FTSE (+0.49%) lead the region higher in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward another green start to the day. The DIA implies a +0.79% open, the SPY is implying a +0.40% open, and the QQQ implies a +0.68% open at this hour. At the same time, 10-year bond yields are down to 4.559% and Oil (WTI) is up 0.34% to $79.22 per barrel in early trading.

The major economic news scheduled for Friday include April Avg. Hourly Earnings, April Nonfarm Payrolls, April Private Nonfarm Payrolls, April Participation Rate, and April Unemployment Rate (all at 8:30 a.m.), April S&P Global Services PMI and April S&P Global Composite PMI (both at 9:45 a.m.), ISM Non-Mfg. Employment, ISM Non-Mfg. PMI, and ISM Non-Mfg. PMI Price Index (all at 10 a.m.), and Fed Member Williams speaks at 7:45 p.m. The major earnings reports scheduled for before the open include on Friday, ADNT, AXL, AMRX, BEPC, BEP, CBOE, CBRE, GTLS, LNG, CRBG, FLR, FYBR, GPRE, HSY, KOP, MGA, NMRK, NVT, PAA, PAGP, TRP, TAC, TRMB, and XPO. Then, after the close there are no major earnings report scheduled.

So far this morning, AMRX, BBU, CBOE, CRBG, FYBR, HSY, NVT, TRP, TRMB, and XPO all reported beats on both the revenue and earnings lines. Meanwhile, ADNT, CBRE, OMI, and TAC all missed on revenue while beating on earnings. On the other side, BEP and LNG beat on revenue while missing on earnings. However, GTLS, FLR, GPRE, and MGA missed on both the top and bottom lines. It is worth noting that MGA lowered its forward guidance.

With that background, it looks as if the Bulls are gapping markets higher today as all three major index ETFs opened the premarket higher. However, with the exception of DIA’s significant white body, they have only printed indecisive candles since the open of the early session. All three are back above their T-line (8ema). So, the short-term trend is now bullish again. Meanwhile, the mid-term remains bearish. The longer-term market remains Bullish but under pressure. Overall, the character of the market is indecisive, choppy, and volatile. In terms of extension, none of the three major index ETFs is extended above their T-line. At the same time, the T2122 indicator is now in the upper-end of its mid-range. So, both sides have room to run if they can gain the momentum to do so. In terms of those 10 big dog tickers, they are evenly split with 5 in the green and 5 in the red this morning. However, AAPL (+6.02%) is by far the biggest mover and dragging the overall market higher on its massive buyback program announced last night. Keep in mind that we still have the April Jobs Report is likely to cause volatility or a change in market direction this morning. Also, don’t forget this is Friday, pay day. So prepare your account for the weekend news cycle.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service