Member Login

Upcoming Events

Free Room Login

Contact Us

Search for:

Twitter

Youtube

Home

Member Workstations

Trading Results

HRC Win Wall

Current Trading Results

Previous Trading Results

Testimonials

About

FAQ

Educational Library

Double your money calculator

The Week Ahead – Sunday Videos

The Secret Sauce

TC2000 Resources

TOS Resources

Stock Trading

Candlesticks

Japanese Candlesticks

Doji and Doji Variations

Candlestick Trading Signals

Candlestick Tip Sheet

Candlestick Patterns

Preparing to Trade Candlesticks

Comprehensive Candlestick Library

Chart Patterns

Favorite Chart Patterns

T-Line Run

T-Line™ By Rick Saddler

Swing Trading the T-Line

Swing Trading Basics

Trade Plan Examples

Technical Analysis

Option Trading

Stock Option Basics

The Options Chain Demystified

Training

3×8 Trap Group Class

Private Coaching

Road To Wealth – Coaching

Webinar / Replay

1-Day Training Clinic

Membership Options

Hit & Run Candlesticks

Right Way Options

BYOB Day Trading

Products

E-Books and Books

Training Courses

Trial Offers

HRC Trial

RWO Trial

BYOB Trading Trial

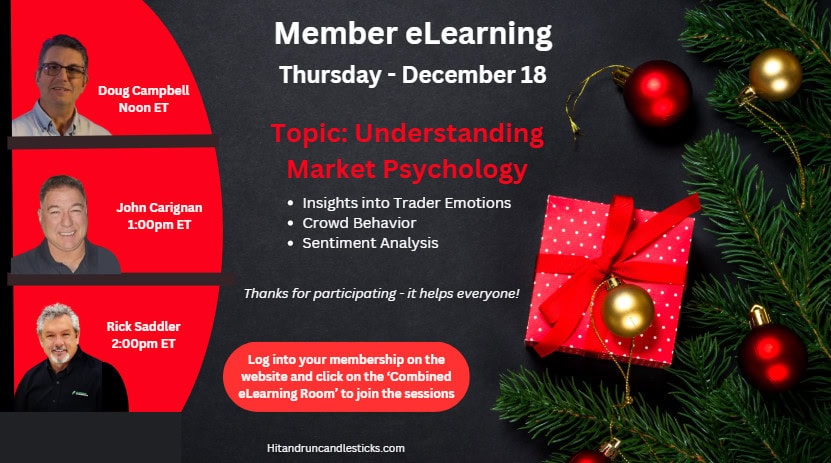

Member e-Learning 12-18-25 – John

December 18, 2025

by

Ed Carter

Member e-Learning 12-18-25 – John

Member e-Learning 12-18-25 – Doug

December 18, 2025

by

Ed Carter

Member e-Learning 12-18-25 – Doug

Member e-Learning 12-4-25 – John

December 4, 2025

by

Ed Carter

Member e-Learning 12-4-25 – John

Member e-Learning 12-4-25 – Rick

December 4, 2025

by

Ed Carter

Member e-Learning 12-4-25 – Rick

Member e-Learning 11-20-25 – John

November 21, 2025

by

Ed Carter

Member e-Learning 11-20-25 – John

Member e-Learning 11-20-25 – Rick

November 21, 2025

by

Ed Carter

Member e-Learning 11-20-25 – Rick

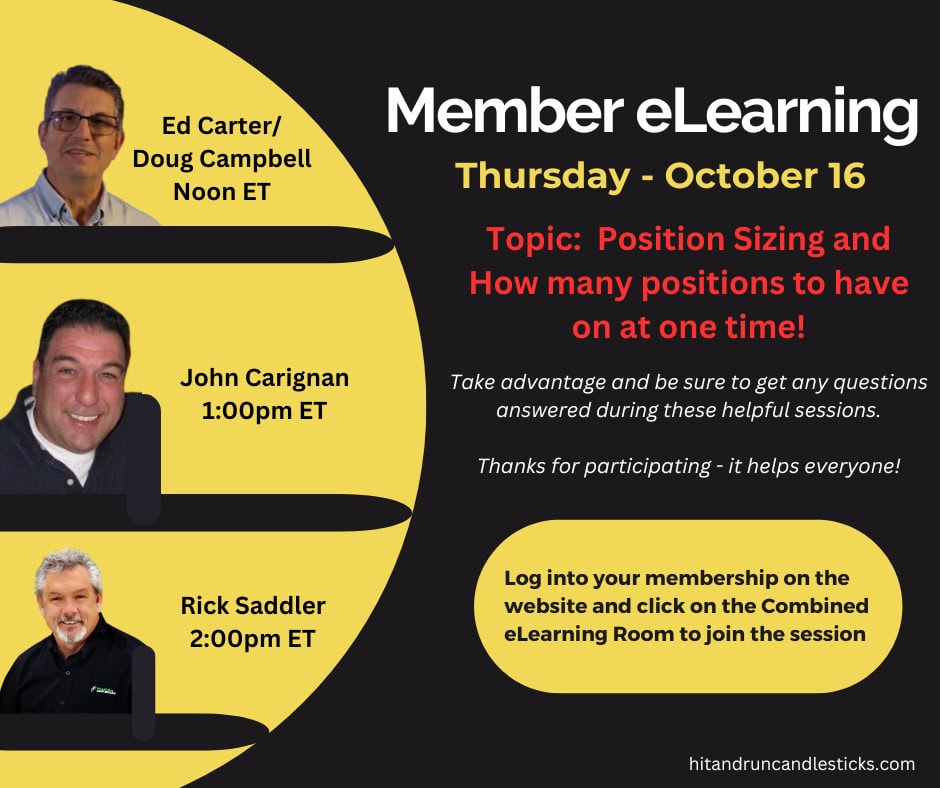

Member e-Learning 10-16-25 – Rick

October 16, 2025

by

Ed Carter

Member e-Learning 10-16-25 – Rick

Member e-Learning 10-16-25 – John

October 16, 2025

by

Ed Carter

Member e-Learning 10-16-25 – John

Member e-Learning 10-16-25 – Ed

October 16, 2025

by

Ed Carter

Member e-Learning 10-16-25 – Ed

Member e-Learning 10-2-25 – Rick

October 2, 2025

by

Ed Carter

Member e-Learning 10-2-25 – Rick

«

1

2

3

4

5

6

7

8

…

656

»

Search for: