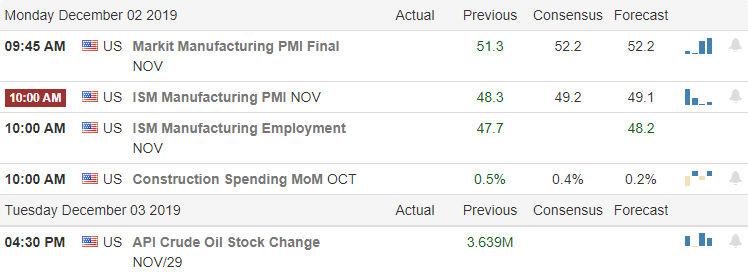

After a bearish short session on Friday, the bulls are trying to spark a rally this morning ahead of the PMI and ISM manufacturing reports. According to reports, the US consumer showed their confidence with an increase of 20% in Black Friday sales and an expectation that Cyber Monday could hit new record spending levels. That’s good for the economy but may prove to problematic for the market today with low volume as distracted traders search for online deals.

Asian markets were green across the board overnight fueled on better than expected Chinese manufacturing numbers. Unfortunately, the European markets are flat with mixed results as their manufacturing once again shrink. US Futures have pulled back from overnight highs as we wait on US Mfg reports at 9:45 and 10:00 AM Eastern. With Dec. 15th tariffs quickly approaching and China threatening retaliation for the bill supporting a Democratic Hong Kong, the path forward may have some new obstacles to overcome. As always, stay focused on price action for clues.

On the Calendar

On the Monday Earnings Calendar, we have a light day with

just 15 companies reporting as trading resumes after the Holiday. There are no particularly notable reports

today.

Action Plan

The market reacted negatively in the low volume, short

session, Friday after the President signed the bill supporting the Hong Kong

protesters. The December 15th

tariffs now come into focus as trade negotiations stall, and China threatens retaliation. On a positive note, holiday deal shoppers

were out in force with Black Friday sales up 20% according to reports. Retail is expecting today, Cyber Monday, to

set new sales records as consumers show signs of ramping up their holiday

online shopping.

Positive Chinese manufacturing data helped to boost overnight

markets, but Euro Zone manufacturing activity once again declined tempering

this morning’s bullishness. This morning

at 9:45 and 10:00, we will hear find out how US Manufacturing measures up with

the PMI & ISM reports. Consensus

estimates look favorable. Don’t be

surprised if volume quickly declines after the morning rush with traders extending

holiday vacations and distractions from Cyber Monday shopping.

The President’s positive comments on the Phase 1 trade

agreement has once again inspired the bulls to continue to reach out for new

highs. The earnings miss by DE has

dampened the overnight bullishness, but with a big morning of market-moving

economic reports that are expected to be positive according to consensus, all

signs point higher. Typically, after the

morning rush of activity, the volume will quickly diminish as traders set-out

to begin their holiday celebrations. Plan

accordingly.

Asian markets closed mixed but mostly higher with high hopes

news of a completed trade deal will be forthcoming. European are green across the board this morning

in response to the favorable trade comments by President Trump. US Futures point to modest gains at the open after

setting new records for the 10th time this month.

On the Calendar

On the pre-holiday Earnings Calendar, we have 21 companies

reporting quarterly results. Notable

reports include DE & DAKT, both reporting before the bell today.

Action Plan

President Trump has once again inspired the market this morning

suggesting they are very close to completing the Phase 1 trade deal. However, he also said they want to see a

democratic outcome in Hong Kong, which many see as a major obstacle to Chinese support. Yesterday, we saw record highs for the 10th

time in the last 30 days. Clearly, the

bulls are in control, and the trend remains very strong.

Although we have a rather light day on the earnings calendar

we have a very busy morning on the economic calendar with several potential

market-moving reports. The consensus

estimates of these reports are all positive, so only a major surprise seems capable

of derailing this relentless bull. Keep

in mind that volume is likely to decline very quickly after the morning rush as

traders head out for their holiday plans.

Although the market is open for short a session on Friday, the HRC and

RWO trading rooms will remain closed until Monday Dec. 2nd. I wish you all a very Happy Thanksgiving!

Markets drifted mildly higher all day on Tuesday on relatively low volume. This allowed the SPY, DIA, and QQQ all to close at another all-time high. So all-in-all it was a very blah day in the market. That said, we remain extended and the VXX continues to be in “dangerously complacent” territory.

In economic news, the President said Tuesday that trade talks “are in the final throes of a very important (Phase One) deal.” This came after the Chinese had announced the previous night that a phone call had been held between chief negotiators. Markets did not react to President Trump’s statement. (Perhaps this was because of the prior overnight announcement or maybe just fatigue of posturing around such a deal.)

$50.00 discount with code: Privilege

On other fronts, the FAA has said again that the BA 737 Max is not ready for recertification (and that it will take all the time needed to reevaluate the plane). This statement completely contradicts BA claims that it will resume deliveries of the 737 Max in December. In fact, the FAA said the Max won’t even make its recertification flight until mid-December and recertification may well take through the end of January. (I’m not sure how BA plans to deliver planes if they cannot fly them to the customers.) This news might have an impact on BA stock.

Major economic news for Wednesday includes Oct. Durable Goods, Q3 GDP, and Weekly Jobless Claims (all at 8:30am). This is followed by Oct. Pending Home sales and Crude Oil Inventories (both at 10 am). The only earnings of note are DE, who report before the Open.

Overnight, Asian markets were in the green. In Europe, the major markets are also in the green at this point. As of 7:30 am, U.S. futures are all pointing to a gap higher of between a quarter and a third of a percent.

Favorite Charting Software

While there is a fair amount of economic news today, it’s quite possible that many traders have already called it a week going into the holiday. Even if this is not the case in the morning, expect light volumes in the afternoon. The point is that it is quite possible we see another low-volume blah day in the markets.

Even so, the bulls have really been relishing their all-time highs. So, we may move higher, even on lower volume. As always, continue to lock-in profits, move stops, and trade your plan. Remember that your job is to make consistent gains and reduce risk, not to hit home runs every once in a while.

Ed

Sorry, no Swing Trade Ideas for your watchlist today as trading should be light before Thanksgiving. Trade smart, take profits along the way and trade your plan. Also, do not forget to check for upcoming earnings. Stocks we mention and talk about are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

With the bulls inspired by Hong Kong election results, renewed

trade hopes, and a huge day merger news made setting new record highs in the DIA,

SPY,and QQQ look easy as they quickly recovered last week’s pullback. Today, the attention will likely shift to earnings

and economic reports to find inspiration.

After such a big move yesterday and heading toward a major holiday. It

will be interesting to see if bulls can find the energy to continue their relentless

march higher.

Asian markets closed mixed but modestly higher with Alibaba

making a huge splash in Hong Kong markets.

European markets are treading cautiously with mixed results as they

continue to monitor US/China trade news.

US Futures are rather subdued this morning ahead of earnings reports and

several potential market-moving economic reports. With markets at new record highs consider

your risk carefully as the holiday shutdown approaches.

On the Calendar

On the Tuesday Earnings Calendar nearly 50 companies

reporting results. Notable reports

include BBY, ADSK, BNS, BOX, CHS, CBRL, DELL, DKS, DLTR, EV, GES, HRL, HPQ,

MOV, VEEV, and VMW.

Action Plan

Monday became on the biggest merger days in history, providing

additional energy to an already bullish sentiment setting new records in the

DIA, SPY, and QQQ in the process. T2122

suggests this bull run still has some upside potential but could soon reach a

short-term overbought condition if the bulls continue to find inspiration to

rally. Earnings reports could provide

that inspiration, or perhaps it will be the New Home Sales and Consumer

Confidence reports at 10:00 AM Eastern.

One thing for sure is that the bulls remain firmly in control of a trend

that shows no price action clues of ending at this point.

Futures markets seem much more subdued this morning, perhaps

needed a little rest after such a big effort yesterday. It is also possible with the Holiday looming

and the nasty weather conditions moving across the country that traders will

try and escape early. Don’t be too

surprised if volumes begin to decline quickly with price action becoming very

light and choppy after the morning rush Wednesday. As we push new market highs, plan your risk carefully

heading into the holiday.

The bulls ran hard the first hour of the day Monday (on optimism stemming from hope on the trade war front and merger news). After 10:30 am, markets drifted sideways the rest of the day. The indices closed near their highs for the day. The end result was another all-time high close in the SPY, DIA, and QQQ. Even the IWM had a very strong day, breaking out of its range going all the way back to March and (unlike the other indices) it did so on heavy volume.

If there was anything bad on the day, it was that the bullish surge took the T2122 indicator back up well into the overbought area at 88. (T2122 is a 4-week New High to New Low Ratio that has a 0-100 range with over 80 meaning over-bought.) Likewise, all the indices remain extended from their 50-day SMA.

$50.00 discount with code: Privilege

On the news front, overnight China’s top trade negotiator had a phone call with Sec. of Treasury Mnuchin to “address the core issues” last night. This is another signal of progress toward a trade deal and the market is quite likely to take this as bullish. However, in reality, this proves nothing as far as an actual deal goes.

In other news, Congressional Democrats say they expect to deliver their Impeachment report shortly after the Thanksgiving break. However, the door was left open for more hearings and last night a Federal Judge ruled that former White House Counsel McGahn must testify (a decision sure to be appealed). This all could lead to a House Impeachment vote (essentially indictment) before the Christmas break. The process (actual trial) would then be in the hands of the Senate and presided over by Chief Justice Roberts at that point.

Major economic news for Tuesday is limited to Conf. Board Consumer Confidence and Oct. New Home Sales (both at 10 am). In terms of earnings, ADI, BBY, DLTR, and HRL all report before the bell. (BBY reported a beat and raised forecasts.) After the close, ADSK, HPQ, and KEYS all report.

Favorite Charting Software

Overnight, Asian markets were mixed but mostly green. In contrast, European markets are mixed but mostly red at this point. As of 7:30 am, U.S. futures are all just on the green side of flat.

With the holiday coming and the most important economic news coming later in the week, it is quite possible Tuesday is a low-volume blah day in markets. Still, bulls have been hearing only what they want to hear lately. So, that phone call report may set off another rally. Regardless, be careful, as low volume is likely to magnify market over-reactions. Just remember that in the longer-term the market trend is bullish. Continue to take profits, move stops, and trade your plan. Keep in mind that a Trader’s job is to consistently make gains, not to hit home runs every once in a while.

Ed

Swing Trade Ideas for your watchlist and consideration. Long – DXC, AMG, NTAP, CXO, HAL, CBS, ARNC, DVA, CDW, ANTM, CTL. Trade smart, take profits along the way and trade your plan. Also, do not forget to check for upcoming earnings. Stocks we mention and talk about are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Friday was a low-volume, indecisive, green day across the markets. Expectations for a low-volume holiday week ahead and the desire to avoid weekend headline risk may well have led to this blah day. In any case, the SPY, DIA, and QQQ all appeared to be curling up after a three-day pullback. Likewise, T2122 rose back to mid-range. So, on a small green day, we started to see broader participation in the rally of the last nearly two months.

On the Trade War front, over the weekend the two Presidents continued to “talk past each other” as reported by Bloomberg. However, China did announce guidelines that it will increase penalties for violations of Intellectual Property rights, as part of an effort to “reduce frequent IP violations by 2022.” However, no details were released nor any mention made of state-sponsored or owned organizations (which are by far the biggest concerns in the IP theft arena). This was seen as an olive branch toward the Trump Administration who will be able to claim it as a trade war win.

$50.00 discount with code: Privilege

In Hong Kong, the pro-Democracy Party has won a huge victory in the “District Council” elections on the heaviest voter turnout ever. Results showed the Pro-Democracy party winning nearly 10 times the number of seats that the Pro-Beijing Party won. However, this will have no impact on actual governance in Hong Kong, as both the “Legislative Council” and Government Offices (who actually make and enforce laws) are essentially Beijing-controlled. Nonetheless, this result may send a message to the Mainland and might cause a rethinking of their approach.

There is no major economic news for Monday. The only earnings report of note before the bell is from JEC. However, in merger news, Swiss pharmaceutical giant Novartis agreed to buy MDCO. Meanwhile, overnight, Asian markets were mixed but mostly green. In Europe, all markets are almost all in the green as well at this point. As of 7:30 am, U.S. futures are pointing to a small gap higher.

Favorite Charting Software

We have the holiday coming this week and very little scheduled market-moving news. It is quite possible that we just drift, at least until next week when the initial Black Friday and Cyber Monday sales reports will be available. If we do get unexpected news this week, be careful, as low volume is likely to magnify the typical market over-reaction.

So, remember that in the longer-term the market is bullish. Continue to take profits, move stops, and trade your plan. Keep in mind that a Trader’s job is to consistently make gains, not to hit home runs every once in a while.

Ed

Swing Trade Ideas for your watchlist and consideration. Long – X, ADT, STT, BAC, DIS, NTAP, CTL, DXC, BIDU, PWR, FEYE. Trade smart, take profits along the way and trade your plan. Also, do not forget to check for upcoming earnings. Stocks we mention and talk about are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The pendulum of the Phase 1 deal that has swing somewhat

bearish heading into the weekend has this morning swing back to the bullish

side, helping to inspire a Monday morning gap.

The bulls got an early start after news that pro-democracy candidates

won big in Hong Kong. The pullback last

week that held trading sets up a great opportunity if the bulls can remain inspired

to attack all-time market highs as we head into the Thanksgiving Holiday.

Asian markets rallied substantially overnight in reaction to

Hong Kong election results. European

markets are also green across the board this morning on renewed US-China trade

hopes. US Futures opened bullishly and

remained strong throughout the night, currently pointing to gap up opens across

all indexes. Perhaps Santa can begin his

run early this year fueled by strong consumer sentiment.

On the Calendar

On the Monday earnings calendar we have 31 companies

stepping up to report. Notable reports

include PANW, A, AMBA, HPE, NTNX, & PVH.

Action Plan

Trade uncertainty dimmed Friday bullishness, but they have

spun the story once again, and this morning, the bulls are pushing for a higher

open. Pro-democracy candidates won big

in the elections on Sunday in Hong Kong with a record voter turnout. A major step for the people of Hong Kong but

they still have an uphill fight with the Beijing control of top

leadership.

With the short holiday week, we still have several notable

earnings reports Monday & Tuesday and a busy economic calendar through Wednesday. However, expect volumes to decline quickly by

mid-week and remain relatively low until Dec. 3rd as traders extend

their Thanksgiving vacations. That being

said the market indexes appear setup to attack new record highs as long as sentiment

on the Phase 1 agreement remains positive.

Last week’s strong consumer reading suggests Santa could have a nice run

this year.

Although we have had 3-days of pullback in the indexes, the VIX shows little to no fear, and so far the indexes has suffered no discernible technical damage. According to reports, the likelihood of a completed Phase 1 trade deal before the scheduled December 15th tariff increase has diminished. As we head into the uncertainty of the weekend and the coming holiday, it may be difficult for the bulls to find much inspiration. However, a consolidation at this level would be productive and bullish as we wait for some political clarity.

Asian markets closed mixed overnight as trade uncertainty

weighed on investor’s minds. Across the

pond, European markets are bullish following positive Euro data. US Futures point toward a modestly bullish

open ahead of Consumer Sentiment that consensus expects to increase slightly at

10 AM Eastern. Plan your risk carefully

as we head into the weekend.

On the Calendar

On the last day of trading this week, we have just 15 companies

reporting earnings. Notable reports

include BKE, FL, HIBB, and SJM.

Action Plan

During the impeachment hearings, the congress could not be

bothered to pass a federal budget but did set aside enough time to kick the can

down the road with another stopgap spending bill to avoid a government shutdown. It now looks as if there will not be a Phase

1 trade agreement before the scheduled December 15th tariffs

increases. China said in a report that they

want a trade deal but are not afraid to fight.

Impeachment hearings have not progressed into Russian election meddling as

the political drama extends.

With a light day of earnings and economic reports the US Futures

are trying to put on a brave face and break the 3-day pullback as we head into

the weekend. With not many places to

find inspiration and trade up in the air it may be difficult for the bulls to

gain much traction. However, if they can

prevent additional selling and slip the indexes into a consolidation I believe

that would be a win keeping the market trends bullish. Although we pulled back there has been on

technical damage, and this rest appears to very constructive thus far. According to the VIX, fear of a selloff remains

very low as we head into the weekend.

On Thursday, the bad news was that stocks posted their first 3-day losing streak since July. In the process, they broke their uptrend, which began back in early October. The good news is that this “selloff” has only totaled about one percent…and it was a well-needed rest after a strong six-week rally.

This pullback/pause has seemed to happen over indecision about the outcome of the Trade War with China, etc. Unfortunately, this is likely to continue simply because international trade is such a massive part of GDP around the world, including the US. Therefore, trade is a large driver of earnings and, therefore, stock markets. Moreover, it is likely that finding themselves in this conflict, the Chinese have no reason to rush to an agreement or make concessions, because President Trump faces an election next fall, while President Xi never will. The point is that we traders need to adapt to this new normal.

$50.00 discount with code: Privilege

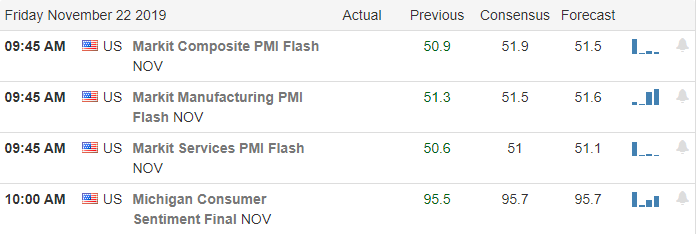

Perhaps the best news of the day is that Impeachment Hearings are now concluded. Obviously, there will be debate and votes on this case, as well as possibly a Senate trial. However, at least until that trial, these will be limited to being reported in sound bites now that the public hearings are concluded. Beyond that story, Friday’s major economic news includes the Nov. PMI (9:45 am) and Michigan Consumer Sentiment Survey (10 am). The only earnings of note before the bell are FL and SJM.

Overnight, Asian markets were mixed but mostly green. In Europe, all markets are in the green as well at this point. As of 7:30 am, U.S. futures are pointing to a quarter percent gap higher.

Favorite Charting Software

Remember that even with the uptrend line broken, we are not far off the highs and we did need a rest. So, be careful about getting too bearish or over-reacting. Yes, Trade War whiplash is likely to continue. However, in a longer-term view, the market is still bullish.

Today is Friday. So don’t forget to take profits in front of the weekend. Continue to lock-in gains, move stops, and trade your plan. Keep in mind that a Trader’s job is to consistently make gains, not to hit home runs every once in a while.

Ed

Sorry, but no Swing Trade Ideas for your watchlist on Friday. However, if you’re in the trading room at 9:10 am Eastern, we will cover some charts. Trade smart, take profits along the way and trade your plan. Also, do not forget to check for upcoming earnings. Stocks we mention and talk about are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service