China Has Crazy Rally As Port Strike Looms

Friday saw some modest divergence in the markets. SPY opened 0.20% higher, DIA gapped up 0.25%, and QQQ opened up 0.21%. However, from that open, QQQ sold off in a very slow manner the rest of the day. It could almost have been called sideway the last couple of hours. Meanwhile, DIA rallied significantly until 11:30 a.m. before reversing and selling off slowly the rest of the day. For its part, after the open, SPY ground sideway until 11 a.m. and then sold off very slowly the rest of the day. This action gave us a white-bodied Shooting Star type candle in the DIA, a black-bodied, fat-body, Spinning Top in the SPY, and a black-bodied candle in the QQQ. This happened on average volume in the DIA and well-below-average volume in the SPY and QQQ.

On the day, eight of the 10 sectors were green again with Energy (+1.60%) far out in front, leading the rest of the market higher. On the other side, Technology (-0.56%) and Basic Materials (-0.28%) were the laggard sectors. At the same time, SPY lost 0.16%, DIA gained 0.31%, and QQQ lost 0.55%. VXX popped higher to close at 50.73 and T2122 climbed to the middle of its overbought territory at 90.32. At the same time, 10-Year bond yields fell to close at 3.754% while Oil (WTI) climbed 1.34% to close at $68.58 per barrel. So, taken as a whole, the three major index ETFs held their serve, staying in the existing trend, which are all bullish. DIA did fail a consolidation breakout attempt while QQQ printed a second gap-up, black-body candle. Meanwhile, SPY continued its melt higher ending not far above where it opened Monday.

The major economic news scheduled for Friday included the August Core PCE Price Index (month-on-month), which came in lower than expected at 0.1% (compared to a forecast and July reading of 0.2%). On an annual basis, August Core PCE Price Index (year-on-year), was up a tick as expected at 2.7% (versus a 2.7% forecast and a tick above July’s 2.6% reading). At the same time, the August PCE Price Index (month-on-month) was down and lower than predicted at 0.1% (compared to a forecast and July value of 0.2%). On the annual basis, the August PCE Price Index (year-on-year) was down significantly to 2.2% (from 2.3% forecast and down sharply from July’s 2.5%). At the same time, August Personal Spending (month-on-month) was also down sharply to 0.2% (versus a forecast of 0.3% and down sharply from July’s 0.5%). Meanwhile, the Preliminary August Goods Trade Balance was better than anticipated at -$94.26 billion (compared to a forecast of $100.60 billion and the July reading of -$102.84 billion). At the same time, Preliminary August Retail Inventories were up less than expected at +0.4% (versus the July +0.5% value). Later, Michigan Consumer Sentiment was a bit higher at 70.1 (compared to a 69.0 forecast and August reading). At the same time, Michigan Consumer Expectations were also higher at 74.4 (versus the 73.0 forecast and August value). In terms of future view, the Michigan 1-Year Inflation Expectations were flat at 2.7% (measured against a 2.7% forecast and August reading). In addition, Michigan 5-Year Inflation Expectations were also flat at 3.1% (compared to the 3.1% forecast and August value).

In stock news, on Friday, VLKAF (Volkswagen) cut its 2024 outlook for the second time in less than three months. The company also lowered its profit margin forecast to around 5.6% (down from a 6.5%-7.0% range set three months prior). Later, C warned employees and contractors about tighter scrutiny as it suspect fraud and unethical behavior by both groups in terms of what the company is billed. At the same time, Reuters reported that MS’s private equity unit is considering the sale of its HVAC firm Sila for about $1.5 billion. Later, Reuters reported growing backlogs of rail shipments to Mexico, just as US East Coast and Gulf Coast ports may shutter. At this point, UNP and BRKB-owned BNSF railways have stopped issuing new permits (orders) for railcar grain shipments to Mexico due to congestion in the Mexican rail system.

Elsewhere, after the close, CNBC reported that SATS is very near a deal to sell its Dish Network to DirecTV (which is owned by T and TPG). This comes as SATS will face a $1.98 billion debt payment in November and had just $521 million in cash on-hand as of June 30. The deal value is rumored to be in the $9 billion neighborhood. Later, Bloomberg reported that 16 European banks and payment processors are launching an alternative to V and MA called Wero.

In stock legal and governmental news, on Friday, the SEC announced that SAVA had agreed to pay a $40 million settlement over negligence-based non-disclosures. Later, the UK anti-trust regulator approved AMZN’s AI partnership with Anthropic and said it will not refer the matter for more investigation. At the same time, a federal judge ruled AAPL must face a lawsuit over its devices violating user privacy. The judge did throw out claims made based on the “Allow Apps to Request to Track” setting, but let claims related to the “Share Analytics” setting to proceed to trial. Later, NHTSA announced that TM will recall over 42k vehicles over the loss of power brake assist the extended the braking distance of the vehicles. At the same time, the NHTSA also announced that MBGAF (Mercedes Benz) is recalling 27k vehicles due to the risk of the engine control software causing the engine to overheat.

Elsewhere, the NHTSA announced that MZDAF (Mazda) is recalling 77k SUVs over a software error that could cause front airbags to deploy with excessive force. At the same time, Chinese authorities discouraged companies from buying NVDA AI chips as Beijing tried to boost its own Chinese chipmakers. (However, this is mostly a PR move at this point since there are no known Chinese-made AI chips anywhere near as powerful as the limited ones NVDA is allowed to sell China.) Later, the Dept. of Trans. fined ACDVF (Air Canada) $250k for operating flights in 2022 and 2023 over prohibited Iraqi airspace. At the same time, the EU fined META $101.5 million for storing user passwords with no protection or encryption. Later, a US District judge announced he will hold a hearing on Oct. 11 to receive the objections of crash victim’s families to the BA plea deal. At the same time, the FDA approved a GEHC diagnostic drug used for the detection of heart disease. On Saturday, TKO agreed to pay $375 million to settle a class-action lawsuit alleging the company had colluded with other martial arts groups to tamp-down the compensation of fighters.

In miscellaneous news, on Friday, there were 4.6 million customers without power in the Southeast US following Hurricane Helene. (At least 64 people were also killed.) Meanwhile, the UD Dept. of Commerce said US car sales could fall about 26k per year under proposed rules barring Chinese vehicles over software internet connection (sending data to China). For reference, US auto sales were 15.5 million in 2023 and were up about 3.5% in the first half of 2024.

In Middle East news, Israel continued its attacks on Lebanon Friday with airstrikes that leveled six hi-rise apartment buildings. The IDF said the target of the attack was the leader of Hezbollah. However, they also destroyed a very densely-populated Beirut neighborhood. In addition, many hundreds of thousands of Lebanese have fled as refugees to other cities and countries as well as 250k that are now living on the streets to avoid being near buildings. Meanwhile, Israeli PM Netanyahu told the UN General Assembly that the Lebanese people were to blame for forcing Israel to attack and kill them. He went on to say that their attacks will continue. Meanwhile, the IDF also called up reserves to the Lebanese border and is currently practicing for another ground invasion of Lebanon.

On Saturday, Hezbollah confirmed their leader Nasrallah had, in fact, been killed. (It is worth noting Israel also assassinated his predecessor in 1992.) In addition, Lebanon reported nearly 1000 people have been killed and several thousand others wounded by Israeli strikes in the last week. Various EU countries condemned the Israeli attacks and called for an end to hostilities by both sides. Meanwhile, Israel rejected a cease-fire deal put forth by the US in the same way it rejected a Gaza cease-fire. On Sunday, Israel increased its bombing (terror?) campaign with more strikes in Lebanon, the West Bank (Palestinian), and also expanded with strikes on Houthi Rebels in Yemen. Israel also ramped up its rhetoric threatening Iran over the weekend. The overall point, is that Israel seems to be intent on all-out regional war (with US arms and support in its back pocket). So, the region as well as Middle Eastern oil, gas, and shipping routes are under greater threat as a broader regional conflict seems much more likely than it was a week ago.

Overnight, Asian markets were very mixed with five of the 12 exchanges in the region showing green. However, massive Chinese moves of Shenzhen (+10.67%), Shanghai (+8.06%), and Hong Kong (+2.43%) led the region higher as that country reacts to more stimulus. On the other side, Japan (-4.80%), Taiwan (-2.62%), and South Korea (-2.13%) paced the losses. In Europe, with the sole exception of Norway (+0.07%) we see red across the board at midday. The CAC (-1.62%), DAX(-0.63%), and FTSE (-0.76%) lead the region lower in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward modestly red start to the day. The DIA implies a -0.14% open, the SPY is implying a -0.21% open, and the QQQ implies a -0.29% open at this hour. At the same time, 10-Year bond yields are up to 3.768% and Oil (WTI) is down 0.78% to $67.66 per barrel in early trading.

The major economic news scheduled for Monday is limited to September Chicago PMI. However, we also hear from Fed Governor Bowman (8:50 a.m.) and Fed Chair Powell (1:55 p.m.). The major earnings reports scheduled for before the open Monday are limited to CCL. However, after the close, there are no major reports scheduled.

In geopolitical news, Reuters reported Thursday that a senior Pentagon official said that China’s newest nuclear-powered submarine sank earlier this year. Apparently, the first-in-class Chinese nuclear attack sub sank alongside its pier sometime between May and June.

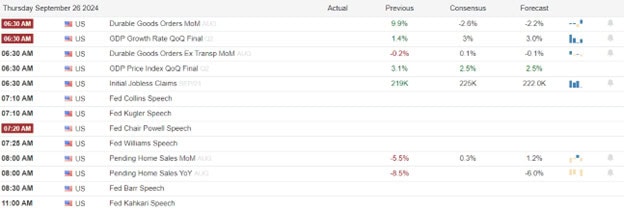

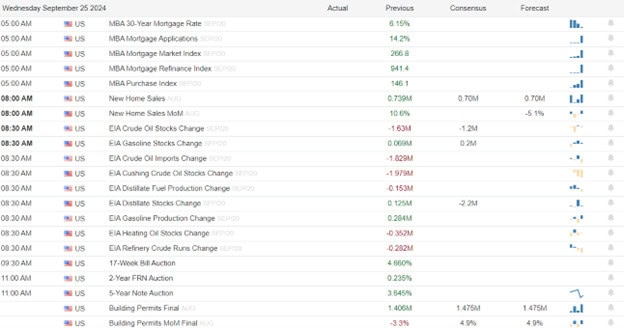

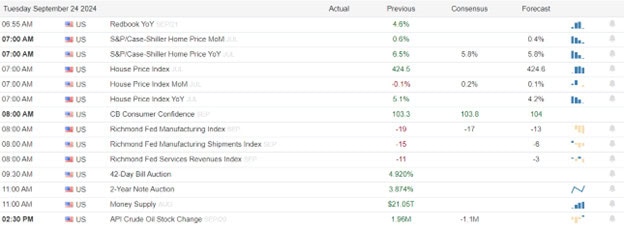

In economic news later this week, on Tuesday we get September S&P Global Mfg. PMI, August Construction Spending, September ISM Mfg. Employment, September ISM Mfg. PMI, September ISM Mfg. PMI Price Index, August JOLTs Job Openings, and API Weekly Crude Oil Stocks. We also hear from Fed Member Bostic twice (11 a.m. and 6:15 p.m.). Then Wednesday, September ADP Nonfarm Employment Change, and EIA Weekly Crude Oil Inventories are reported. We also hear from Fed Governor Bowman at 11 a.m. On Thursday, we get Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, September S&P Global Services PMI, September S&P Global Composite PMI, August Factory Orders, September ISM Non-Mfg. Employment, September ISM Non-Mfg. PMI, September ISM Non-Mfg. PMI Price Index, and Fed Balance Sheet. We also hear from Fed member Bostic at 10:40 a.m. Finally, on Friday, September Avg. Hourly Earnings, September Nonfarm Payrolls, September Participation Rate, September Private Nonfarm Payrolls, and September Unemployment Rate. We also hear from Fed member Williams.

In terms of earnings reports later this week, on Tuesday, we hear from AYI, MKC, PAYX, UNFI, CALM, LW, and NKE. Then Wednesday, CAG, RPM, and LEVI report. On Thursday, we hear from STZ. However, on Friday, there are no earnings reports scheduled.

In overnight news, DirecTV (owned by T and TPG) finally agreed to acquire Dish Network (owned by SATS). The move creates a network with 20 million subscribers. As part of the deal, DirecTV will assume $9.75 billion in debt. However, Dish shareholders will need to agree to a $1.57 billion haircut on that debt. As part of the deal, T will sell its 70% stake in DirecTV to TPG for $7.6 billion. (T originally bought its share of DirecTV for a little over $14 billion.) Elsewhere, more stimulus in China spiked global iron ore by 11% as Chinese cities agreed to ease home-buying restrictions.

With that background, it looks like the Bears are pushing this morning. All three major index ETFs opened the premarket flat, but have traded lower, printing black-body candles with little wick. DIA has the smallest candle in the early session. All three remain above their T-line (8ema). So, the short-term trend is still bullish. The mid-term trend is now also bullish with QQQ the laggard but now well over its downtrend line going back to the July all-time high. In the longer-term we still have a strong Bull trend all three major index ETFs and remain near all-time highs. With regard to extension, none of the major index ETFs are extended above its T-line (8ema). Still, the T2122 indicator is back up in the middle of its overbought range. So, markets have room to run either direction, but the Bears have more slack to work with today if they can find momentum. With regard to those 10 big dog tickers, nine of the 10 are in the red. It is worth noting that the biggest dog, NVDA (-2.87%) leads the losses and has more than twice the dollar-volume of the next closest, which is TSLA (-0.61%).

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service