Stock futures saw a slight rebound following a challenging day on Wall Street, where rising oil prices and bond yields exerted downward pressure on the markets. On Tuesday morning, these factors eased somewhat, improving investor sentiment. The 10-year Treasury yield notably climbed above 4%, reaching its highest level since early August, while West Texas Intermediate oil futures rose above $77 per barrel, impacting the broader market negatively. However, the energy sector benefited from the rise in oil prices, making it the only one of the 11 sectors in the S&P 500 to close Monday in positive territory. Investors are now turning their attention to upcoming economic data on small businesses and the trade deficit.

European markets continued to decline as regional sentiment worsened amid ongoing concerns about the Middle East conflict. Mining stocks led the losses, dropping 4.54%, while household goods fell by 2.37%. European luxury stocks, including major brands like LVMH and Kering, also opened lower as hopes for a demand boost from Chinese stimulus measures faded. This downturn follows a shaky start to the week, reflecting broader investor apprehension.

Chinese markets experienced a volatile session following a briefing from the National Development and Reform Commission that lacked specifics on additional stimulus measures. The CSI 300 index in mainland China surged over 10% at the opening but eventually trimmed its gains to close 5.93% higher at 4,256.1. Meanwhile, Hong Kong’s Hang Seng index saw a dramatic drop of over 10% before recovering slightly to end with a 9% loss. Other Asia-Pacific markets also faced declines, influenced by Japan’s economic data showing a 1.9% year-on-year decrease in household spending for August, marking the steepest decline since January.

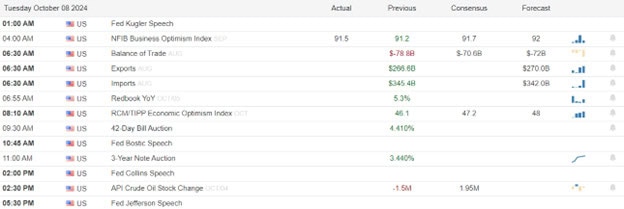

Economic Calendar

Earnings Calendar

Notable reports for Monday before the bell notable reports include PEP, & ACCD. After the bell there are no notable reports.

News & Technicals’

Uber is enhancing its platform with new sustainability-focused features. One notable addition is the “EV preference” option, allowing customers to choose fully electric vehicles by default when hailing a ride. On the delivery side, Uber Eats is expanding its offerings to include farmers’ market produce in New York City and Los Angeles. For drivers, Uber is introducing an “EV Mentor” program and an AI chatbot powered by OpenAI’s ChatGPT, designed to assist drivers with questions about purchasing and using battery electric vehicles instead of traditional gas-powered ones. These updates reflect Uber’s commitment to promoting environmentally friendly practices across its services.

A Delaware bankruptcy judge has approved FTX’s reorganization plan nearly two years after the cryptocurrency exchange filed for bankruptcy. The company has amassed between $14.7 billion and $16.5 billion in assets, which it intends to distribute to its creditors. Under the court-approved plan, 98% of FTX’s creditors are expected to receive 119% of their allowed claims, marking a significant recovery for those affected by the exchange’s collapse.

On Tuesday, South Korean tech giant Samsung Electronics announced that it anticipates lower-than-expected profits for the third quarter. The company, a leading memory chip manufacturer, projected an operating profit of approximately 9.10 trillion won, a significant increase from last year’s 2.43 trillion won. However, this figure falls short of the 11.456 trillion won ($7.7 billion) forecasted by analysts polled by LSEG for the quarter ending September 30.

Super Micro shares surged by 15% after the computer server company announced it is shipping over 100,000 graphics processing units (GPUs) per quarter, driven by the growing demand for artificial intelligence. As a major player in the AI boom, Super Micro provides computers that serve as servers for data storage, websites, AI training models, and more. Despite this positive momentum, the company is currently about nine weeks behind in releasing its annual report, which was initially expected in August.

Although the easing bond yields are providing a slight rebound this morning, we should remember the indexes remain within their choppy range and market breadth remains very low. Of course, big moves are possible if something changes in the Middle East. Other than that, the market will likely continue to chop until waiting on FOMC minutes, CP, PPI and beginning of earnings season on Friday. Trade wisely and try not anticipate ahead of these big data points.

Friday saw three moves by the market. A gap higher, fading of the gap, and a long, protracted rally. SPY gapped up 0.81%, DIA gapped up 0.58%, and QQQ gapped up 1.21%. At that point, all three major index ETFs sold off for more than an hour with SPY and QQQ not quite recrossing the gap, but DIA crossing all the way back below its prior close. However, shortly after 10:30 a.m., all three began a slow, steady rally that lasted right into the last five minutes of the day. This action gave us indecisive but bullish candles in all three. SPY and QQQ both printed long-legged Doji type candles that gapped up through and retested from above (passing that test) their T-line (8ema). At the same time, DIA gapped up through its T-line, retested its T-line from above, and printed a white-bodied Hanging Man type candle that also printed a new all-time high close. This all happened on below-average volume in the SPY, DIA, and QQQ.

On the day, all 10 sectors were in the green with Financial Services (+1.72%) out in front, leading the rest of the market higher. On the other side, Utilities (+0.23%) was the laggard. Meanwhile, SPY gained 0.91%, DIA gained 0.82%, and QQQ gained 1.19%. VXX fell 3.79% to close at 53.00 and T2122 popped up to just outside of its overbought territory to the top of its mid-range at 78.90. At the same time, 10-Year bond yields spiked to close at 3.969% while Oil (WTI) rose another 1.19% on Middle East fears to close at $74.60 per barrel. So, the end of the US port strike and great September jobs data showing the economy isn’t falling off a cliff led to a gap higher. At that point the profit-takers ran for an hour. However, the bulls stepped in to buy the dip and keep slowly buying all day long.

The major economic news scheduled for Friday included Sept. Avg. Hourly Earnings (Month-on-Month), which came in down but better than expected at +0.4% (compared to a forecast of +0.3% but down from August’s +0.5% reading). On an annualized basis, Sept. Avg. Hourly Earnings were up to +4.0% (versus the +3.8% forecast and August’s annual +3.9% number). At the same time, September Nonfarm Payrolls were much stronger than anticipated at +254k (compared to +147k forecast and +159k Aug. value). (It is worth noting that there were also upward revisions to summer payrolls numbers.) On the private side, September Private Nonfarm Payrolls were also much stronger than predicted at +223k (versus a +125k forecast and August’s +114k number). Meanwhile, the September Participation Rate remained steady at 62.7% (compared to a forecast and August reading of 62.7%). Taken together, this gave us a September Unemployment Rate that fell to 4.1% (versus a forecast and August value of 62.7%). So, the data showed us that the economy remains strong on the jobs side with growing earnings even as other data has shown inflation falling. That’s as close to a soft landing (the so-called golden path) as you can get. However, the Bears and folks who think they know better than the Fed, saw the data as an omen of either no rate cut in November or at the very least “disappointing the market” with a lesser cut than was expected. (That latter point overlooks that Fed members, including Fed Chair Powell, all but said were only getting a quarter-point cut in November.)

In Fed news, on Friday morning, Chicago Fed President Goolsbee told Bloomberg the US jobs report was “superb.” Goolsbee said, “You really couldn’t ask realistically for a better report for the economy, coupled with finding out that the (East Coast and Gulf Coast) port strike is not going to be an extended matter … those are two pieces of very good news for the economy.” He continued, “If we get more reports like this, I’m going to feel a lot more confident that we are in fact settling in at full employment.” Goolsbee went on to say there are even some signs that inflation will go lower than the FOMC’s 2% target. He went on to say that despite the strong jobs report, the Fed Funds rate is still far above what most FOMC members see as the eventual “settling point” and that it is appropriate for the Fed to bring the rate down “a lot” over the next 12-18 months.

In stock news, on Friday, rumors spread that APO is in advanced talks to acquire B for $45 per share. (B gapped higher and closed up 12.98% at $45.26 on the news.) Later, TELL announced that shareholders have approved the $1.2 billion acquisition of WOPEY (Australian energy producer Woodside Energy Group). At the same time, the BA and LMT joint venture (United Launch Alliance) announced it had successfully launched a second mission. (This is another step toward Dept. of Defense certification, which is required prior to carrying commercial contracts for national security payloads.) Later, META announce two new services aimed at bringing in more young adult users. The new “Local” and “Explore” tabs are currently being tested in various cities around the US. At the same time, GM announced it had halted production at two plants (an SUV assembly plant and a truck assembly plant) due to the impact of Hurricane Helen on parts suppliers.

Elsewhere, Reuters reported that GOOGL is experimenting with “verified” check marks in search results. (There is no word on whether or no GOOGL intends to monetize such a feature the way Elon Musk did with the former Twitter.) At the same time, UAW union workers at STLA’s Los Angeles parts distribution center voted in favor of strike unless the carmaker settled grievances related to company failures to make product and investments as promised in the most recent national contract with STLA. Later, JNJ announced it will discontinue a mid-stage trial of its experimental pill for the prevention of dengue fever. The company said this came after reprioritization of its R&D portfolio. At the same time, Reuters exclusively reported that RIO is in talks to acquire lithium miner ALTM. If the deal were closed, it would make RIO the third-largest producer of lithium in the world. (Sources tell Reuters the deal would value ALTM at between $4 billion and $6 billion.)

In stock legal and governmental news, on Friday, Reuters reported TMO repeatedly broke FDA contamination rules at its plant that manufactures infant formula and RSV drugs. The report cited documents from US FDA inspections. (TMO makes RSV drugs for SNY and infant formula on behalf of AZN.) At the same time, the NHTSA announced it has opened a probe into 260k F crossover SUVs over losses of braking due to a brake hose defect. Later, COIN announced it will delist certain stablecoins in the European Economic Area by year end. This move was in response to the EU’s landmark crypto regulatory framework which will be fully implemented by December.

Elsewhere, the EU voted to move ahead with tariffs (of up to 45%) on Chinese EVs. The contentious vote passed 10 to 5 with 12 abstentions. Later, the US Supreme Court agreed to hear an appeal from SWBI (Smith & Wesson) to a $10 billion lawsuit brought by the Mexican government. The suit alleges the company and Interstate Arms Company aided and abetted gun trafficking. At the same time, STLA sued the UAW union over strike threats stemming from the company’s plans to delay investments promise in the 2023 labor contract. After the close, the FDA placed a lupus treatment from KZR on hold following the death of four patients, which showed common symptoms and three deaths came soon after administration of the experimental drug.

In miscellaneous news, on Thursday night, the US port strike ended in a tentative deal over wages and benefits. (The automation negotiations will continue with no further strike until January.) Then Friday, Longshoreman resumed work at US East Coast and Gulf Coast ports. This means the port shutdown lasted three days and typically it will take nine days (three days per day of shutdown) to fully recover cargo backlogs. In France, the European Commission approved funds for the removal of 4% of the grape vines in that country. Back in the US, estimates now indicate that economic damage from Hurricane Helene will reach $250 billion. However, the insurance industry says that only about $5 billion of that will be covered by policies. As an immediate response is continuing, the disgraced ex-President and his conspiracy theorist minions (like Elon Musk) continue to sew doubt and deter people from using resources available to them by continually spreading lies, amplifying completely unfounded rumors, and distortions for their political gain.

In Fed prediction news, following Friday’s strong September jobs report, there was a huge shift in the implied probabilities of a November Fed rate cut. Fed Funds Futures trades now bake in a 97.4% probability of a quarter-point cut at the November meeting with 2.6% betting on no change in rates then. One week prior, 46.7% were expecting a half percent rate cut and 53.3% of trades expected a quarter point cut. There were no trades expecting no rate change one week ago.

In Middle East news, Israel continued heavy airstrikes on Gaza and Lebanon over the weekend. (The AP reported more than 30 strikes in Beirut alone on Sunday evening.) The Israeli ground invasion of Southern Lebanon also continued. Reports indicate over 100 Lebanese killed and an unknown number wounded over the weekend alone. One-third of the Lebanese population are now refugees. Israel confirmed 11 of the IDF ground forces have also been killed. This all comes as it appears Israel is preparing a retaliatory strike on Iran over the 180 missiles that country fired at/toward Israel last week. From an oil market perspective, the majority of oil flows that has been disrupted or are threatened would go to China. However, if China can’t buy from Iran or the rest of the Gulf can’t ship to China due to war, it will end up buying from other sources. This will allow US and other producers to sell at a premium. WTI is up 10% in the last 10 days as of Sunday.

Overnight, Asian markets were mostly green with Japan (+1.80%), Taiwan (+1.79%), and South Korea (+1.58%) pacing the gains. In Europe, the bourses are mixed at midday. The CAC (+0.18%), DAX (-0.24%), and FTSE (+0.46%) lead the region in early afternoon trade. Meanwhile, in the US, as of 7:30 a.m., Futures are pointing toward a down start to the day. The DIA implies a -0.40% open, the SPY is implying a -0.46% open, and the QQQ implies a -0.62% open at this hour. At the same time, 10-Year bond yields have spiked again to 4.002% and Oil (WTI) jumped another 2.5% on Israeli fears (continued bombing and invasion with threat of attack on Iran) in early trading.

The major economic news scheduled for Monday is limited to August Consumer Credit (3 p.m.). We also hear from Fed members Kashkari (1:50 p.m.) and Bostic (6 p.m.). There are no major earnings reports scheduled for either before the open or after the close Monday.

In economic news later this week, on Tuesday, we get August Exports, August Imports, August Trade Balance, EIA Short-Term Energy Outlook, and API Weekly Crude Stocks report. We also hear from Fed member Bostic (12:45 p.m.). Then Wednesday, EIA Crude Oil Inventories and the September FOMC Meeting Minutes are reported. However, we also hear from Fed member Bostic and Fed member Daly. On Thursday, we get Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, September Core CPI, September CPI, September Federal Budget Balance, and Fed Balance Sheet. We also hear from Fed member Williams. Finally, on Friday, September Core PPI, September PPI, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-Year Inflation Expectations, Michigan 5-Year Inflation Expectations, and the WASDE Ag report are delivered.

In terms of earnings reports later this week, on Tuesday, PEP reports. On Wednesday, we hear from HELE. Then Thursday, DAL and DPZ report. Finally, on Friday, earnings season kicks off again in earnest as BK, BLK, FAST, JPM, and WFC report.

With that background, markets look bearish so far in the premarket. All three major index ETFs gapped down to start the early session and have traded lower to retest their T-line (8ema) from above. However, all three are now trading above their T-line (8ema) at the moment. So, the short-term trend remains bullish. The mid-term trend remains bullish. In the longer-term we still have a strong Bull trend in all three major index ETFs and they remain not far from their all-time highs. With regard to extension, none of the major index ETFs are extended above its T-line (8ema). In addition, the T2122 indicator is still in its mid-range (although just outside of overbought territory. So, markets have room to run either direction, if either the Bulls or Bears can find momentum. However, the Bears have a little more slack and the Middle East situation in their corner. With regard to those 10 big dog tickers, nine of the 10 are modestly in the red. AMZN (-1.71%) leads the losses while AMD (+0.49%) is holding up far better than the others. It is worth noting that the biggest dog, NVDA (-0.48%) has traded only 1.5 times the dollar-volume as TSLA (-0.46%). This is typically a factor of three.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Stock futures declined on Monday as Wall Street faced struggle to maintain momentum. Contributing to the pressure was a rise in U.S. Treasury yields, with the benchmark 10-year Treasury yield increasing nearly 3 basis points to 4.008%, marking its first time above 4% since August. Keith Lerner, co-chief investment officer at Truist Wealth, warned that the upcoming U.S. presidential election and the potential for an “October surprise” could sustain market volatility in the coming weeks. Investors are also closely monitoring international developments, particularly the ongoing tensions in the Middle East.

European stocks began the new trading week on a positive note, initially buoyed by gains in Asia overnight, but quickly pared back those gains. Currently, banks and household goods are the only sectors in positive territory, with increases of 0.2% and 0.4%, respectively. Shares of Rio Tinto fell by 0.26% after the mining company confirmed it was in discussions to acquire lithium producer Arcadium Lithium. On the data front, the U.K.’s Halifax House Price Index revealed that British house prices rose in September at the fastest annual pace since November 2022. Additionally, euro zone retail sales in August edged up by 0.2% from the previous month, aligning with expectations from a Reuters poll.

This week, the financial spotlight is on the Asia-Pacific region as three central banks—the Bank of Korea (BOK), Reserve Bank of New Zealand (RBNZ), and Reserve Bank of India (RBI)—prepare to announce their interest rate decisions. According to a Reuters poll, economists anticipate rate cuts from both the BOK and RBNZ, while the RBI is expected to maintain its current rate. The Nikkei index saw a significant rise, climbing 1.8% to close at 39,332.74, driven by gains in financial and consumer cyclical stocks, with Mizuho Financial Group and Nikon among the top performers.

Economic Calendar

Earnings Calendar

Notable reports for Monday before the bell we have no notable reports. After the bell reports include NAPA.

News & Technicals’

Early Monday, Hurricane Milton intensified to a Category 2 storm, prompting Florida to prepare for its largest evacuation in seven years. The hurricane is projected to impact major population centers such as Tampa and Orlando. Although forecast models show varying paths, the most likely scenario indicates that Milton could make landfall in the Tampa Bay area on Wednesday and maintain its hurricane status as it traverses central Florida before moving into the Atlantic Ocean.

Beginning October 7, banks in the U.K. will be mandated to compensate victims of online fraud up to £85,000. This new regulation comes amid ongoing tensions between financial institutions and tech companies over the responsibility for combating online scams. On Thursday, London-based digital bank Revolut criticized Meta, claiming it has fallen “woefully short” in its global efforts to address fraud. For years, banks have felt they are shouldering the majority of the financial burden from virtual scam attacks, exacerbating the friction between these sectors.

Starboard Value has acquired approximately $1 billion stake in Pfizer, as reported by sources familiar with the situation. The activist fund, led by Jeff Smith, is considering involving former Pfizer CEO Ian Read and ex-finance chief Frank D’Amelio, though their potential roles remain unspecified. This investment comes at a challenging time for Pfizer, which is aggressively cutting costs due to declining demand for its Covid-19 treatments.

The 10-year Treasury yield, a key benchmark for mortgages and car loans, surged back above 4% amid stronger labor market data. This marks its highest level since early August and a significant rebound from its 2024 low of approximately 3.58% just over a month ago. Investors are closely watching speeches from Federal Reserve officials Neel Kashkari, Raphael Bostic, Michelle Bowman, and Alberto Musalem, scheduled for Monday. Additionally, the 10-year Treasury auction is set for Wednesday, which could further influence market dynamics.

I would not be surprised if the struggle to maintain momentum continued this week despite the bullish rally in the market on Friday squeaking out new record high close in the DIA. Market is highly anticipating the kick-off on earnings on Friday hoping the results will finally push us out of this choppy consolidation. However, between now and then we have an FOMC minutes release, a CPI report and a PPI report along with rising bond yields and oil prices providing uncertainty. Of course, all the geopolitical tensions and pending election just piles on the uncertainty facing the market.

October trading has begun on a challenging note, with escalating tensions in the Middle East dampening market enthusiasm. These growing concerns have also pushed oil prices higher, with U.S. crude futures rising by over 1.5%, contributing to a week-to-date gain of 4.6%. On Wall Street, investors are anticipating new labor market data, including the release of weekly initial jobless claims on Thursday and September’s payrolls report, which is due on Friday morning.

European stocks declined on Thursday, influenced by the ongoing conflict in the Middle East, which dampened regional investor sentiment. Auto stocks were particularly affected, falling by 1.87% amid reports that the European Union might impose tariffs of up to 45% on Chinese electric vehicle (EV) manufacturers as early as Friday. Investors also evaluated new unemployment data from the euro zone, which revealed that the unemployment rate remained steady at a record low 6.4% in August.

On Thursday, Hong Kong stocks experienced a significant drop, ending a six-day winning streak as the momentum from China’s stimulus measures began to wane. Concurrently, the Japanese yen weakened against the U.S. dollar, marking its largest single-day decline since June 2022. Meanwhile, markets in mainland China will remain closed until October 8th due to a week-long holiday, and South Korea’s markets are also closed for National Foundation Day. Additionally, Taiwan’s markets were shut for a second consecutive day as Typhoon Krathon brought heavy rainfall to the island.

Economic Calendar

Earnings Calendar

Notable reports for Thursday before the bell include ANGO & STZ. After the bell reports include TLRY.

News & Technicals’

Levi Strauss reported mixed quarterly results, announcing plans to sell its Dockers business. While the company experienced robust growth in its namesake brand and Beyond Yoga, sales at Dockers fell by 15% during the quarter. Despite this, Levi’s focus on direct selling and lower cotton costs contributed to a 4.4 percentage point increase in its gross margin.

Europe’s leading car manufacturers are growing increasingly anxious about the potential for substantial fines, especially as demand for electric vehicles (EVs) weakens ahead of stricter carbon regulations. Starting next year, European carmakers will face more stringent emission targets, with the EU cap on average emissions from new vehicle sales dropping to 93.6 grams of CO2 per kilometer. Renault CEO Luca de Meo recently indicated that if EV sales do not improve, the European auto industry could face financial penalties amounting to 15 billion euros ($16.5 billion).

Atlanta is expected to experience haze and a chlorine odor on Thursday as authorities work to manage the aftermath of a chemical lab fire that started on Sunday. Air quality monitoring around the BioLab facility in Conyers detected elevated chlorine levels overnight, according to a news release from the Georgia Emergency Management and Homeland Security Agency on Wednesday. The presence of chemical gas has led to a shelter-in-place recommendation for the entire county, which has a population of 93,570, and mandatory evacuation orders for residents in the vicinity of the plant.

The British pound dropped by over 1% against the U.S. dollar on Thursday following comments from Bank of England Governor Andrew Bailey. In an interview with the Guardian, Bailey suggested that further positive news on inflation could enable the central bank to adopt a more proactive stance on rate cuts. The Bank of England maintained interest rates at 5% in September after a 25-basis point cut in August, citing concerns about high services inflation. Bailey also expressed optimism that cost of living pressures had not been as persistent as previously anticipated.

Israel’s response early Thursday put geopolitics front and center in the minds of investors as the escalating tensions weigh on sentiment. The DIA, SPY and QQQ remain in choppy yet bullish patterns while market breadth continues to wane. I would expect more of the same today unless we can find some substantial inspiration in the weekly claims data. However, the pending employment situation report Friday could also inspire a break of this 2 week long consolidation.

Tuesday saw a modestly lower open and Bearish morning. SPY opened 0.09% lower, DIA opened down 0.17%, and QQQ opened 0.09% lower. At that point, the Bears were in-charge across all three major index ETFs, driving a sharp selloff that reached the lows of the day at 10:15 a.m. in DIA and 11:20 a.m. in the SPY and QQQ. From there, all three rode a slightly bullish roller coaster sideways the rest of the day. This action gave us large, black-bodied candles with significant lower wicks in the SPY and QQQ. Both of them crossed back below their T-line (8ema) and even retested (and passed the test) their 17ema. Meanwhile, DIA printed a black-bodied Spinning Top with most of its wick on the bottom side of the candle. It too retested its 8ema, but unlike the others, it stayed above its T-line. This happened on average volume in the SPY and QQQ but above average volume in the DIA.

On the day, seven of the 10 sectors were red with Technology (-1.71%) WAY out in front (by nine-tenths of a percent), leading the rest of the market lower. On the other side, Energy (+2.02%) was the biggest mover and outperformed the other sectors by more than 1.5%. Meanwhile, SPY lost 0.88%, DIA lost 0.38%, and QQQ lost 1.39%. VXX spiked 7.72% to close at 53.43 and T2122 dropped back to the middle of its mid-range at 54.67. At the same time, 10-Year bond yields fell to close at 3.735% while Oil (WTI) spiked on Middle East fears to close at $70.62 per barrel. So, for the most part, the Bears ruled the morning (mostly on fears over the Israeli invasion of Lebanon and Iran’s retaliatory attack over recent Israeli assassinations conducted in Iran).

The major economic news scheduled for Tuesday included September S&P Global Mfg. PMI, which was down but better than expected at 47.3 (compared to a forecast of 47.0 and an August reading of 47.9). Later August Construction Spending was up but worse than expected at -0.1% month-on-month (versus a +0.2% forecast and the July -0.5% value). At the same time, September ISM Mfg. PMI was flat, which was not as strong as predicted at 47.2 (compared to a 47.6 forecast and in-line with the August 47.2 reading). On the jobs side, Sept. ISM Mfg. Employment Index was down to 43.9 (versus a 47.0 forecast and a 46.0 August value). Related to costs, September’s ISM Mfg. PMI Price Index was significantly lower at 48.3 (compared to a 53.5 forecast and a 54.0 August reading). Meanwhile, August JOLTs Job Openings were up at 8.040 million (versus a 7.640 million forecast and a 7.711 million July number). Later, after the close, API Weekly Crude Oil Stocks were down a little less than anticipated at -1.458 million barrels (compared to the forecast calling for a 2.100-million-barrel drawdown and the previous week’s -4.339 million barrels).

After the close, CALM and LW reported beats on both the earnings and revenue lines. At the same time, NKE missed on revenue while beating on earnings.

In stock news, on Tuesday, SLTA announced an extension of their halt in production of the Fiat 500e until at least November 1. (The halt had initially been planned to end Oct. 11, but was extended three weeks amid slow electric vehicle sales.) At the same time, Reuters reported that sources tell it that AAPL may need to turn back to China to supply iPhone components after a fire destroyed at Tata Group’s Hosur Indian iPhone component plant. The weekend fire has caused what is being called “an indefinite production halt.” Later, EQIX announced it has entered into a $15 billion joint-venture with the Singapore sovereign wealth fund and the Canada Pension Plan Investment Board to build a US data center. (The data center is expected to eventually scale to use 1.5 gigawatts of power.) At the same time, Bloomberg reported that BA is looking to raise $10 billion by selling new shares. Later, MSFT announced it has begun rolling out updates to its consumer Copilot software, giving it an AI assistant and a “more amiable” voice. At the same time, GM reported that its Q3 new vehicle sales fell 2.2% due to fewer sales days in the quarter and lower consumer spending. TM reported an 8% decrease for the quarter. (F and STLA have yet to announce sales.)

Meanwhile, CVS said it would be laying off 2,900 employees (1% of workforce) as part of a cost-cutting plan. The cuts will primarily be at corporate headquarters in RI. Later, as with most competent companies, TM announced it had built extra inventory of vehicles and parts ahead of the US port strikes. At the same time, SCHW announced that its long-time CEO Bettinger will retire on January 1, after 16 years at the helm. He will be replaced current company President Wurster. Later, CI, CVS, HUM, CNC, and UNH unveiled their 2025 Medicare Advantage plans. The companies told Reuters that 83% of enrollees will have access to a $0 monthly premium plan. At the same time, BRKB announced it had purchase full control of its Energy unit, buying the remaining 8% of stock for $2.37 billion. Later, JNJ announced it will invest more than $2 billion in a new manufacturing facility in NC for the production of biologic drugs and therapies. At the same time, CNBC reported that 500 SBUX locations have voted to unionize as talks between the union and company continue. (The Starbucks Workers United union now represents more than 11k SBUX employees.) After the close, Bloomberg reported AAPL will launch upgrades to iPhone SE and iPad Air product lines in early 2025. At the same time, NKE withdrew its annual forecast and postponed its planned investor day when it reported earnings.

In stock legal and governmental news, on Tuesday, the CFTC announced BCS agreed to pay $4 million to settle civil charges that it violated US law and CFTC rules requiring accurate and timely reporting on swap transactions. (BCS failed to report 5 million such swap transactions from 2018 to 2023.) Later, a US district judge dismissed a shareholder suit against PTON. The suit had alleged PTON defrauded shareholders by concealing how demand for its exercise machines had fallen as COVID vaccines became available and people were allowed to return to public life. Later, the NHTSA announced that owners of 154k Jeep hybrid plug-ins should park the vehicle outside and away from buildings or other vehicles until recall repairs are completed.

At the same time, the Fed announced it had terminated a 2013 enforcement action filed against C related to money laundering. (The enforcement action did not carry a fine but required process and documentations changes.) In 2023, C announced it planned to split the offending unit from the rest of the bank in the second half of 2024. At the same time, the NRLB issued a complaint against AAPL for allegedly violating employees right to organize or advocate for better working conditions by maintaining unlawful workplace rules. (Among the alleged infractions were confidentiality, non-disclose, non-compete, employee misconduct, and off-time social media policies. Among the prohibited topics were pay, discrimination, and promotion standards.)

In miscellaneous news, on Tuesday evening, the state of MI announced the schedule resulting from a summer major MI State Supreme Court decision that raises the state’s minimum wage by 20% to $12.48/hour at the end of February. (The first increase will the to $10.56 on January 1 and then to $12.48 on February 21. It will increase again to $14.97 in February 2028 and then be followed by annual inflation adjustments.) The court decision ruled that after 280k MI voters signed petitions calling for a ballot issue on the state minimum wage, the GOP legislature passed changes in 2018 and then proceeded to illegally water down the increases to insignificant levels.

In Middle East news, Israel’s ground invasion of Lebanon continued, even as the Lebanese army had fled southern Lebanon. Reportedly, 60 Lebanese were killed and an unknown number wounded on Tuesday. Meanwhile, Iran chose to take a retaliatory action for last month’s Israeli assassination of Hamas’ top negotiator in Tehran. Iran fired about 180 missiles toward Israel Tuesday. Many of the missiles were intercepted by Israel’s Iron Dome air defense and US Navy anti-missile systems. However, a few Iranian missiles and a lot of missile fragments did hit southern Israel. No casualties were reported since Israel had plenty of time to move the public to bomb shelters. (The closest Iranian hit seems to have been a missile that landed within six-tenths of a mile from Mossad headquarters.) Israeli PM Netanyahu immediately vowed that “Iran will pay” for its attack.

Overnight, Asian markets were mostly red. Japan (-2.13%) was well out front followed by South Korea (-1.22%) and Malaysia (-1.03%) leading the losses. In Europe, we see a similar picture taking shape as 11 of the 14 bourses are modestly in the red at midday. The CAC (-0.12%), DAX (-0.59%), and FTSE (+0.18%) lead the region lower in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a down start to the day. The DIA implies a -0.38% open, the SPY is implying a -0.26% open, and the QQQ implies a -0.23% open at this hour. At the same time, 10-Year bond yields are up to 3.756% and Oil (WTI) has spiked another 3.62% on Middle East fears to $72.35 per barrel in early trading.

The major economic news scheduled for Wednesday includes September ADP Nonfarm Employment Change (8:15 a.m.), and EIA Weekly Crude Oil Inventories (10:30 a.m.). We also hear from Fed Governor Bowman at 11 a.m. The major earnings reports scheduled for before the open are limited to CAG and RPM. Then, after the close, LEVI reports.

In economic news later this week, on Thursday, we get Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, September S&P Global Services PMI, September S&P Global Composite PMI, August Factory Orders, September ISM Non-Mfg. Employment, September ISM Non-Mfg. PMI, September ISM Non-Mfg. PMI Price Index, and Fed Balance Sheet. We also hear from Fed member Bostic at 10:40 a.m. Finally, on Friday, September Avg. Hourly Earnings, September Nonfarm Payrolls, September Participation Rate, September Private Nonfarm Payrolls, and September Unemployment Rate. We also hear from Fed member Williams.

In terms of earnings reports later this week, on Thursday, we hear from STZ. However, on Friday, there are no earnings reports scheduled.

In economic news later this week, on Wednesday, September ADP Nonfarm Employment Change, and EIA Weekly Crude Oil Inventories are reported. We also hear from Fed Governor Bowman at 11 a.m. On Thursday, we get Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, September S&P Global Services PMI, September S&P Global Composite PMI, August Factory Orders, September ISM Non-Mfg. Employment, September ISM Non-Mfg. PMI, September ISM Non-Mfg. PMI Price Index, and Fed Balance Sheet. We also hear from Fed member Bostic at 10:40 a.m. Finally, on Friday, September Avg. Hourly Earnings, September Nonfarm Payrolls, September Participation Rate, September Private Nonfarm Payrolls, and September Unemployment Rate. We also hear from Fed member Williams.

In overnight news, a chlorine chemical cloud in Atlanta has triggered a new series of shelter-in-place orders for that major city. This is the fallout of Sunday’s fire at the BioLab chemical plant in Conyers, GA (25 miles Southeast of Atlanta). Multiple counties have had such shelter-in-place orders since the fire, but now the impact is being felt in a major urban population center. Elsewhere, early this morning, LLY announced it will build a $4.5 billion research, development, and manufacturing facility located near Lebanon, IN.

So far this morning, RPM reported a miss on revenue while also beating on earnings. However, CAG reported misses on both the top and bottom lines.

With that background, markets look indecisively bearish so far in the premarket. All three major index ETFs opened the early session lower and have printed mostly wick since that point. All three are now trading below their T-line (8ema). So, the short-term trend is now bearish. The mid-term trend remains bullish. In the longer-term we still have a strong Bull trend in all three major index ETFs and they remain not far from their all-time highs. With regard to extension, none of the major index ETFs are extended above its T-line (8ema). In addition, the T2122 indicator is back in the center of its mid-range. So, markets have room to run either direction, if either the Bulls or Bears can find momentum. However, the Bears have what momentum exists on the back of the Middle East situation and the US East and Gulf port strike. With regard to those 10 big dog tickers, eight of the 10 are modestly in the red. AAPL (-0.58%) leads the losses while META (+0.18%) and NFLX (+0.12%) are holding up better than the others. It is worth noting that the biggest dog, NVDA (-0.35%) has traded only a little more than 2 times the dollar-volume as TSLA (-0.31%). This is typically a factor of at least two to three.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The major averages emerging from a losing session, with rising Middle East tensions dampening risk appetite and investor enthusiasm for the new trading period. Stock futures declined on Wednesday morning as traders prepared for potential further losses at the start of October. Technology stocks were the worst performers on Tuesday. Investors are looking forward to gaining insights into private payrolls through ADP’s Employment Survey. Additionally, Friday’s nonfarm payrolls report is anticipated to significantly influence market direction and the Federal Reserve’s upcoming rate decisions as it begins its rate-cutting cycle.

European stocks edged slightly higher as investors tried to overlook the escalating tensions in the Middle East. The oil and gas sector saw a notable increase of 2.42%, while travel and leisure stocks dipped by 0.25% due to airlines diverting flights away from the conflict zone. Defense companies experienced gains amid rising conflict risks. Despite reporting revenues and profits that exceeded expectations for the first half, shares of British sports retailer JD Sports fell by 3.5%.

Hong Kong’s Hang Seng index surged over 6%, reaching a 22-month high and marking its sixth consecutive day of gains, driven by recent stimulus policies. Meanwhile, markets in mainland China were closed for the Golden Week holiday and will remain so for the rest of the week. In contrast, Australia’s S&P/ASX 200 dipped slightly by 0.13% to close at 8,198.2. South Korea’s Kospi experienced a more significant decline of 1.22%, ending at 2,561.69, while the small-cap Kosdaq slipped 0.23% to 762.13. Japan’s Nikkei 225 also saw a notable drop of 2.18%.

Economic Calendar

Earnings Calendar

Notable reports for Thursday before the bell include CAG & RPM. After the bell reports include LEVI.

News & Technicals’

Stephen Roach, a senior fellow at Yale Law School’s Paul Tsai China Center, warns that markets are at risk of being “whipsawed” due to the combination of regional conflict in the Middle East and rising unemployment in the United States. The situation in the Middle East intensified on Tuesday when Iran launched a ballistic missile attack on Israel following the killing of Hezbollah leader Hassan Nasrallah and an Iranian commander in Lebanon. Roach noted that the markets are likely to be uncertain about their direction, as the conflicts in the Middle East contribute to inflationary pressures just as global central banks are beginning to ease monetary policy.

The strike affecting ports along the East and Gulf coast could drive up prices for food, automobiles, and various other consumer goods, though the overall economic impact is expected to be modest. Key industries are likely to face significant challenges including coal, energy, and agricultural products. However, there are potential mitigations to the strike’s impact. West Coast ports are expected to absorb some of the freight that would typically be handled by the eastern ports. Additionally, some companies had foreseen the disruption and stockpiled goods in advance.

Nike has withdrawn its full-year guidance and announced the postponement of its investor day, originally scheduled for November. Despite beating earnings expectations by 18 cents, the company fell short on revenue as it focuses on refining its product assortment and revamping its innovation strategy. Additionally, Nike is preparing for a leadership transition with a new CEO set to take the helm.

In a Tuesday interview with CNBC’s Jim Cramer, Chipotle CSO Jack Hartung discussed the company’s business in California following a price increase in April. Hartung noted that there is “macro resistance” from consumers to inflation across the industry. He emphasized that the situation in California is more about broader economic impacts rather than specific resistance to Chipotle’s price hike. Hartung pointed out that restaurant transactions are down across the board, indicating a wider trend affecting the entire restaurant industry.

Clearly the rising Middle East tensions have added a dose of uncertainty and volatility to the price action but so far, the bullish patterns in the DIA, SPY and QQQ remain intact. In truth, yesterday pullback relieved a lot of overbought pressure and may well prove to have been a healthy relief. Remember, it’s the follow-though that matters and with the sharply declining market breadth that could be tough to achieve. Stick with the trend but be ready with a plan to protect your capital if or when Israel retaliates.

On the first trading day of October aa the fourth quarter begins, stock futures showed mixed results following a surprisingly strong performance in September. The S&P 500 and the Dow both reached closing records in the previous session, buoyed by Federal Reserve Chair Jerome Powell’s statement that the central bank is “not on any preset course” regarding future rate policy decisions. Investors are also keeping an eye on upcoming economic data, with the U.S. Bureau of Labor Statistics’ Job Openings and Labor Turnover Survey for August set to be released on Tuesday morning, along with the S&P Global U.S. Manufacturing Purchasing Managers’ Index and the ISM Manufacturing PMI readings.

European stocks began October on a positive note, buoyed by the news that euro zone inflation has fallen below 2% for the first time since mid-2021, according to preliminary data released on Tuesday. Despite this overall positive trend, Renault shares dropped by 3.6%, placing them at the bottom of France’s CAC 40 index. This decline extends the losses seen in the auto sector from the previous session, reflecting ongoing industry pressures. Additionally, German inflation data released on Monday indicated a decrease in the consumer price index to 1.8% in September.

The financial markets in South Korea, Hong Kong, and mainland China are closed due to a public holiday. Mainland China will remain closed for the rest of the week in observance of the Golden Week holiday. Meanwhile, in Japan, business optimism among large manufacturers has remained steady, showing no change. However, sentiment among large non-manufacturers has seen a slight improvement, rising to +34 from +33 in the third quarter.

Economic Calendar

Earnings Calendar

Notable reports for Thursday before the bell include AYI, MKC, PAYX, & UNFI. After the bell reports include CLAM, LW, NKE, & RGP.

News & Technicals’

Federal Reserve Chair Jerome Powell stated on Monday that the recent half percentage point interest rate cut should not be seen as an indication that future rate adjustments will be equally aggressive. Speaking to the National Association for Business Economics, Powell emphasized that the Fed is “not on any preset course” regarding monetary policy. He expressed confidence in the strength of the economy and anticipated that inflation would continue to decrease.

Between 2014 and 2015, the Chinese stock market experienced a dramatic surge, doubling in value over six months as leverage increased significantly, noted Aaron Costello, regional head for Asia at Cambridge Associates. However, he pointed out on Monday that the current market conditions are different, with less dramatic gains and lower leverage levels. Costello reassured that “we’re not in the danger zone yet,” but he also highlighted the uncertainty surrounding whether economic growth will be robust enough to sustain a long-term market rally.

CVS Health’s board has enlisted advisors to conduct a strategic review of its business amidst potential activist pressure and a significantly depressed stock price, according to sources familiar with the situation. This review has been in progress for some time, though it remains uncertain what actions, if any, will be taken. Following the news, CVS shares saw a rise of approximately 2.5% in after-hours trading on Monday.

Starting at 12:01 a.m. ET on October 1, approximately 50,000 longshoremen from the International Longshoremen’s Association (ILA) began a strike at East Coast and Gulf Coast ports, stretching from New England to Texas. This marks the union’s first strike since 1977, following unsuccessful contract negotiations with port ownership. The strike affects a significant portion of U.S. trade, as 43%-49% of all U.S. imports and billions of dollars in monthly trade pass through these ports. The ILA, the largest maritime union in North America, rejected a proposal from the port management group USMX on Monday, which included a nearly 50% wage increase over six years.

As the fourth quarter begins traders will be hoping for a follow-through to the sharp afternoon rally that occurred yesterday that squeaked out new records in Dow and SP-500. Market breadth, however, continued to decline with the indexes remaining in a choppy consolidating condition. Keep in mind that the big bank reports don’t begin until Oct. 11th so as we wait, don’t be surprised to see choppy light volume conditions persist. Middle eastern tensions continue to grow the longshoreman strike adds another layer of uncertainty for the traders to digest.

Markets were flat most of the day with mid-afternoon volatility and a strong rally into the close. SPY opened 0.16% lower, DIA opened down 0.10%, and QQQ gapped down 0.21%. From there, all three major index ETFs meandered sideways in a tight range until 2 p.m. At that point, all three sold off for 20 minutes, rallied back for 25 minutes, and then paused for 35 minutes. Finally, the last 25 minutes of the day was a sharp rally into the close. This action gave us white-bodied candles with significant lower wicks. SPY printed a Bullish Engulfing signal and closed at another all-time high close after retesting (and passing the test of) its T-line (8ema) earlier in the day. DIA gave us a white-bodied Hammer that also retested its T-line and closed at another all-time high close. Meanwhile, QQQ also retested (and passed the test of) its T-line while printing a white-bodied big-bodied Hammer type. The happened on well-below-average volume in the QQQ, slightly below-average volume in SPY, and just above-average volume in the DIA.

On the day, seven of the 10 sectors were green again with Healthcare (+0.42%) out in front, leading the rest of the market higher. On the other side, Basic Materials (-0.57%) and Consumer Cyclical (-0.53%) were the laggard sectors. Meanwhile, SPY gained 0.42%, DIA gained a slim 0.04%, and QQQ gained 0.27%. VXX dropped 2.35% to end at 49.54 and T2122 fell back to the bottom half of its overbought territory at 83.21. At the same time, 10-Year bond yields rose to close at 3.785% while Oil (WTI) remained unchanged to close at $68.19 per barrel. So, for the most part, the first 4.5 hours of the day were a boring market. Then Fed Chair Powell spoke. Initially, the market sold on Powell telling us that more, smaller cuts lay ahead. (Coming into Powell’s speech, 53% of Fed Fund Futures bets expected a half-percent cut in November. Afterward, only 36% expect the half-point cut.) However, the Bulls stepped in to buy that dip. This may have been a reaction to Powell saying the economy was fine, or it may have been a month-end or quarter-end push. Regardless of the cause, stocks rallied sharply the last 20 minutes with two of three major index ETFs closing at new all-time high closes.

The major economic news scheduled for Monday is limited to September Chicago PMI. This came in better than expected at 46.6 (compared to a forecast and August value of 46.1).

In Fed news, Atlanta Fed President Bostic told Reuters he was open to another half-percent cut in November if upcoming data shows job growth slowing. Bostic said, “A surprise to the weak side …. would pull me much further into really needing another dramatic move.” He continued, “If the story is that inflation is continuing its drop and the labor market is staying strong, I think we have the luxury of being a bit more patient with rate cuts.” … “If, on the other hand, the labor market comes in much weaker, I think that would add urgency to this (rate cutting cycle).” Later, Chicago Fed President Goolsbee (in an interview with Fox Business) was even more definite in saying he feels quarter-point cuts are the way to go. Goolsbee said, (With regard to monetary policy) “This is a process, over a year or more, that we’re trying to get the rates down to normal.” He continued regarding the pace of cuts, saying, “(The Fed Funds rate) has got to come down a lot more than 25 basis points over the next 12 months. It’s going to be a lot of cuts.”

However, the headline speaker Monday was Fed Chair Powell, who spoke to the National Assn. for Business Economics. Powell said, “Looking forward, if the economy evolves broadly as expected, policy will move over time toward a more neutral stance.” He continued, “The path of future interest rates isn’t on any preset course. … It will continue to make our decisions meeting by meeting.” Related to current inflation, he said, “Disinflation has been broad based, and recent data indicate further progress toward a sustained return to 2 percent.” Regarding the strength of the economy in terms of Gross Domestic Income versus GDP, Powell said, “That’s been a downside risk that we’ve been monitoring … but there’s now no gap between the two. … That, I would say, removes a downside risk to the economy.” Powell’s most widely reported remarks were “This is not a committee that feels like it is in a hurry to cut rates quickly. … We will do what it takes in terms of the speed with which we move.” In discussion, Powell indicated that the FOMC’s base case is for two additional quarter-point cuts for the remainder of 2024.

In stock news, on Monday, STLA cut its 2024 profit forecast and warned it would burn through more cash that previously expected. The company cited poor US sales and offering bigger discounts to revive US marketshare. STLA said it now expects a negative cash flow of between $5.58 billion and $11.17 billion instead of positive cash flow. At the same time, TPG announced it had acquired a minority stake in investment advisory Creative Planning for $2 billion. Later, MMC announced it agreed to acquire private insurance brokerage McGriff Insurance Services for $7.75 billion. At the same time, Reuters reported that PFE will sell 640 million shares in UK consumer healthcare company Haleon for about $3.25 billion.

Elsewhere, Reuters reported that VZ had sold the right to lease, operate, and manage 6.339 mobile phone towers covering 50 states and Washington DC to Vertical Bridge. The deal includes $2.8 billion in cash up front. The company is expected to lease the towers back to VZ for 10 years with an option to extend up to 50 years. At the same time, the Wall Street Journal reported that PEP is in advanced talks to buy private Siete Foods for more than $1 billion. Later, the Teamster Union announced it had signed a tentative agreement with HTZ covering nearly 3k members. (Union members had voted to strike if a deal was not reached Monday.) At the same time, Reuters exclusively reported that CVS is considering strategic options including the break-up of the company.

In stock legal and governmental news, on Monday, Russia fined GOOGL $38k (which I have a feeling will cost GOOGL more than that just to pay that paltry amount) for not removing content Russia deems illegal. Later, a trial against ABT, RBGPF (Reckitt Benckiser), and St. Louis Children’s Hospital began Monday with jury selection. The companies are being sued over severe intestinal illness that the suit alleges a baby got from premature infant formula he was given after birth. (There are nearly 1,000 similar cases pending nationwide.) At the same time, Epic Games filed suit against AAPL and Korea’s Samsung, alleging the pair conspired to protect the Google Play Store from competition. Later, the US Dept. of Commerce unveiled a new rule that could make it easier to ship AI chips to data centers in the Middle East. NVDA is the primary winner from the new rule, but AMD and to a lesser extent INTC could receive some benefit as well. At the same time, the NHTSA announced GM will pay a $1.5 million fine for failing to disclose details of an October 2023 crash involving one of its Cruise self-driving taxis.

Elsewhere, BMY won the dismissal of a $6.4 billion lawsuit brought by CELG shareholders who had claimed that by delaying federal approval of the cancer drug Breyanzi, BMY had been able to acquire CELG at an artificially low price. At the same time, the FCC reached a $31.5 million settlement with TMUS over issued related to significant data breaches of TMUS systems over 3 years. Later, SEC filings showed that XOM, CVX, and COP paid $42 billion to foreign governments last year for oil and gas extraction rights. This was about eight times what they paid the US government in 2023. At the same time, the NHTSA announced that STLA is recalling 194k Jeep plug-in hybrids over fire risk following 13 fire reports. Later, CA Governor Newsom vetoed an AI safety bill after strong opposition from GOOGL, META, MSFT and others. (TSLA had been a proponent for the bill.) At the same time, EBAY won the dismissal of a suit brought by the US Dept. of Justice. The suit alleged EBAY violated environmental laws by allowing hundreds of thousands of polluting and toxic products to be shipped to the US. The judge ruled Section 230 of the Communications Decency Act protects EBAY from any liability over user content and the company had not materially contributed to the products.

Meanwhile, the FCC announced it is investigating VZ for a service outage that affected thousands of user and left some in “SOS mode.” (There were over 105k new outage reports at the peak and 30k new outage reports at of 5 p.m. Eastern.) At the same time, the US Dept. of Justice and SEC announced TD will pay more than $20 million to settle charges of US Treasury market manipulations using “Spoof” orders. Later a federal judge ruled AMGN must face a class-action suit trial for waiting too long to tell shareholders it may owe $10.7 billion in unpaid taxes due to underreporting income for six years. At the same time, a federal just dismissed a suit against TSLA and its CEO Musk, that alleged the company defrauded then by overstating the effectiveness and safety of the company’s self-driving technology. (Even though he and the company had clearly lied about that for years, the judge ruled the plaintiffs had not proven they had directly said this would boost the stock price.) Later, WMT announced that Mexico’s antitrust regulator will rule on the company’s liability for antitrust pricing and terms imposed on distributors and suppliers in the next few days.

In miscellaneous news, on Monday, the Dept. of Energy bought 6 million barrels of oil for the Strategic Petroleum Reserve for $68.50/barrel. The oil will be delivered at a rate of 1.5 million barrels per month from February – May 2025. Elsewhere, analysts now estimate the financial cost of Hurricane Helene may be $160 billion (well above the $95 billion to $110 billion estimated prior to the storm). Meanwhile, Libyan oil production is set to resume in days after a political deal approved the appointment of an interim Libyan Central Bank Governor. (This comes after a month-long shutdown of Libyan oil production.) Finally, the East Coast and Gulf Coast port strike began at midnight. (For reference, it typically takes three days to recover for each day of shutdown.)

In Middle East news, Israel began what it says is a “limited ground operation” invasion of Lebanon Monday evening. The IDF said it has no plans for long-term occupation of Lebanon, but (as makes operational sense) gave no indication of goals or timeline. At the same time, Israel also began bombing the southern side of Beirut. This all comes after more than a million Lebanese have become refugees, 1,700 have been killed, and multiple thousands of casualties have been reported in the last two weeks.

Overnight, Asian markets were mixed but leaned toward the green even as Chinese markets are closed the rest of the week for their national holiday. Japan (+1.93%) and Thailand (+1.09%) led the gainers while Australia (-0.74%) paced the losses. In Europe, we see mostly green with only three of 14 bourses in the red at midday. The CAC (+0.02%), DAX (+0.45%), and FTSE (+0.46%) lead the region higher in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a mixed open. DIA implies a -0.20% open, the SPY is implying a +0.01% open, and QQQ implies a +0.17% open at this hour. At the same time, 10-Year bond yields are down to 3.743% and Oil (WTI) is oddly (given the Israeli invasion of Lebanon) down 0.75% to $67.69 per barrel in early trading.

The major economic news scheduled for Tuesday includes September S&P Global Mfg. PMI (9:45 a.m.), August Construction Spending, September ISM Mfg. PMI, Sept. ISM Mfg. Employment, September ISM Mfg. PMI Price Index, and August JOLTs Job Openings (all at 10 a.m.), and API Weekly Crude Oil Stocks (4:30 p.m.). We also hear from Fed Member Bostic twice (11 a.m. and 6:15 p.m.). The major earnings reports scheduled for before the open are limited to AYI, MKC, PAYX, and UNFI. However, after the close, CALM, LW, and NKE report.

In economic news later this week, on Wednesday, September ADP Nonfarm Employment Change, and EIA Weekly Crude Oil Inventories are reported. We also hear from Fed Governor Bowman at 11 a.m. On Thursday, we get Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, September S&P Global Services PMI, September S&P Global Composite PMI, August Factory Orders, September ISM Non-Mfg. Employment, September ISM Non-Mfg. PMI, September ISM Non-Mfg. PMI Price Index, and Fed Balance Sheet. We also hear from Fed member Bostic at 10:40 a.m. Finally, on Friday, September Avg. Hourly Earnings, September Nonfarm Payrolls, September Participation Rate, September Private Nonfarm Payrolls, and September Unemployment Rate. We also hear from Fed member Williams.

In terms of earnings reports later this week, on Wednesday, CAG, RPM, and LEVI report. On Thursday, we hear from STZ. However, on Friday, there are no earnings reports scheduled.

So far this morning, AYI, MKC, and UNFI all reported beats on both the revenue and earnings lines.

With that background, markets look indecisive so fat in the premarket. All three major index ETFs opened the early session flat and have printed mostly wick since that point. All three remain above their T-line (8ema). So, the short-term trend is still bullish. The mid-term trend is now also bullish with QQQ the laggard but now well over its downtrend line going back to the July all-time high. In the longer-term we still have a strong Bull trend all three major index ETFs and remain near all-time highs. With regard to extension, none of the major index ETFs are extended above its T-line (8ema). However, the T2122 indicator is still in the bottom of its overbought range. So, markets have room to run either direction, but the Bears have just a bit more slack to work with today if they can find momentum. With regard to those 10 big dog tickers, six of the 10 are in the green. GOOGL (+1.32%) leads the gainers while AAPL (-1.26%) paces the losses. It is worth noting that the biggest dog, NVDA (+0.24%) has traded only a little more than 1.5 times the dollar-volume as TSLA (+0.37%). This is typically a factor of at least two to three.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service