Stock futures remained flat as investors wait for directional signals of follow-through up or down. This week’s earnings reports have been a mixed bag, with strong performances from major banks being counterbalanced by weaker outlooks from companies like UnitedHealth Group and Dutch chipmaker ASML. Investors are particularly focused on upcoming reports from Morgan Stanley and Abbott Laboratories, due before the market opens. Bryn Talkington, managing partner of Requisite Capital Management, mentioned on CNBC’s “Closing Bell” that the stock market is expected to be volatile in the coming weeks as investors navigate through earnings season and the presidential election.

European markets saw a decline as global market sentiment deteriorated. However, the FTSE 100 stood out among major regional indices, rising by 0.6% following the release of U.K. data indicating a significant drop in the inflation rate to 1.7% in September. Among individual stocks, LVMH experienced a notable drop of 6.3% at the opening, while British hotel group Whitbread emerged as the best performer, with its shares increasing by 3.7%.

Asia-Pacific markets experienced a downturn as investors remained cautious, anticipating potential stimulus measures aimed at bolstering China’s real estate sector. The upcoming press briefing by China’s housing minister on Thursday is expected to shed light on these measures. Meanwhile, New Zealand reported a 2.2% increase in its consumer prices index for the third quarter, indicating rising inflationary pressures. In South Korea, the seasonally adjusted unemployment rate slightly increased to 2.5% in September from 2.4% in August, reflecting minor fluctuations in the labor market.

Economic Calendar

Earnings Calendar

Notable reports for Wednesday before the bell include ABT, ASML, DFG, FHN, MS, OFG, PLD, SYF, USB, & WAFD. After the bell reports include AA, CNS, CCI, CSX, DFS, EFX, FR, HOMB, KMI, PPG, REXR, SLG, STLD, & SNV.

News & Technicals’

United Airlines reported third-quarter revenue and earnings that exceeded Wall Street expectations, signaling a strong performance. The airline also announced a $1.5 billion share buyback, marking its first repurchase since the onset of the Covid-19 pandemic. Additionally, United’s fourth-quarter earnings estimate surpassed analysts’ forecasts, further highlighting the company’s positive financial outlook.

On Wednesday, Asian and European chip stocks declined following disappointing sales forecasts from Dutch semiconductor equipment maker ASML, which negatively impacted global stocks in the sector. In Asia, Japan’s Tokyo Electron experienced the most significant losses, with its stock plummeting nearly 10%. Meanwhile, in Europe, ASML’s stock fell for the second consecutive day, losing 4% of its value. ASML’s CEO, Christophe Fouquet, highlighted customer caution in the company’s early released results, noting that the recovery is progressing more gradually than previously anticipated.

Boeing announced plans to raise up to $25 billion to strengthen its balance sheet, a move aimed at enhancing its financial stability. In a separate filing, the company disclosed that it has secured a $10 billion credit agreement with banks. Despite these efforts, Boeing is under scrutiny from credit ratings agencies, which have issued warnings that the company could lose its investment-grade rating. This highlights the ongoing financial challenges Boeing faces as it navigates a complex economic landscape.

Venture funding for cloud startups in the U.S., Europe, and Israel is expected to increase by 27% year-over-year, marking the first rise in three years, according to a report from VC firm Accel. Of the $79.2 billion raised by cloud firms, 40% was allocated to generative AI startups. Philippe Botteri, a partner at Accel, highlighted the dominance of AI in the sector, stating that “AI is sucking the air out of the room” in an interview with CNBC. This trend underscores the growing focus and investment in AI technologies within the cloud industry.

Mortgage Apps number came with a substantial disappointment this morning as investors wait for directional signals of what the follow-though will look like today. The ASML early report had bearish effects not only here in the U.S. but also translated into selling around the world last night. Of course, earnings results or the economic numbers are likely to provide the inspiration for the bulls or bears to make that decision. Remember that Thursday is a very big day of economic reports so plan your risk accordingly.

Stock futures remained relatively stable on Tuesday following record highs for both the Dow Jones Industrial Average (DIA) and the S&P 500 (SPY). Information technology stocks were the standout performers, driving the S&P 500 up by nearly 1.4%, with Nvidia’s 2.4% rally to a record close providing significant upward momentum. The focus now shifts to corporate earnings, with major financial institutions like Goldman Sachs, Citigroup, and Bank of America set to report. Additionally, earnings from United Airlines, Walgreens Boots Alliance, and Johnson & Johnson are anticipated. Investors are also keeping a close watch on manufacturing data and comments from several Federal Reserve speakers, which could influence market sentiment.

European stocks showed a mixed performance on Tuesday as third-quarter earnings reports began to emerge. The market saw a divergence across sectors, with travel stocks rising by 1.3%, while oil and gas stocks fell by 3.15%, mirroring declines in the oil market. Telecom stocks gained 1.39%, largely driven by a significant 8.5% jump in Sweden’s Ericsson, which exceeded earnings expectations despite a 4% drop in year-on-year sales. Meanwhile, the U.K.’s statistics agency reported that average wages excluding bonuses increased by 4.9% year-on-year, though earnings including bonuses fell to a two-year low of 3.8%.

China’s stock markets experienced a significant downturn on Tuesday following the release of disappointing September trade data. Both exports and imports fell short of expectations, with exports rising only 2.4% and imports increasing a mere 0.3% compared to the previous year. This led to a 2.66% drop in the CSI 300 index and a 3.67% decline in Hong Kong’s Hang Seng index. In contrast, South Korea’s Kospi index saw a modest gain of 0.39%, buoyed by revised trade data showing a substantial surplus of $6.7 billion for September. Japan’s Nikkei 225 and Australia’s S&P/ASX 200 also posted gains, rising 0.77% and 0.79%, respectively.

Economic Calendar

Earnings Calendar

Notable reports for Tuesday before the bell include ACI, BAC, C, SCHW, GS, JNJ, PNC, PGR, STT, UNH, & WBA. After the bell reports include FULT, HWC, IBKR, JBHT, OMC, PNFP, SGH, & UAL.

News & Technicals’

Nvidia shares have reached an all-time high, driven by soaring demand for it’s artificial intelligence chips. Major tech companies like Microsoft, Meta, Google, and Amazon are purchasing Nvidia’s graphics processing units (GPUs) in large quantities to build extensive AI computing clusters. This surge in demand has propelled Nvidia’s market valuation to over $3.4 trillion, underscoring its pivotal role in the AI revolution and solidifying its position as a leading player in the tech industry.

A federal appeals court has expedited the Commodity Futures Trading Commission’s (CFTC) case against the Kalshi exchange, which is offering contracts that function as bets on U.S. political elections. These contracts, facilitated by Kalshi and Interactive Brokers, allow bets on outcomes such as the presidential election, U.S. Senate races, and which party will control Congress. Notably, Kalshi has already booked over $7 million in contracts on the presidential race between former President Donald Trump and Vice President Kamala Harris. The court’s decision to fast-track this case underscores the regulatory scrutiny surrounding the legality of such political betting markets.

Ericsson reported adjusted third-quarter earnings of 7.327 billion Swedish crowns ($0.7 billion) on Tuesday, significantly exceeding the analysts’ forecast of 5.75 billion crowns. This impressive performance was largely driven by robust sales growth in North America, which saw a year-on-year increase of over 50%. The company’s strengthened position in the U.S. market, bolstered by securing a major contract with AT&T last year, where it outperformed Finnish competitor Nokia, has been a key factor in this success.

Federal Reserve Governor Christopher Waller indicated on Monday that upcoming interest rate cuts will be more measured compared to the significant reduction in September. He emphasized a gradual approach to lowering the policy rate over the next year, despite short-term uncertainties. Waller’s comments come amid mixed economic data, which the Fed is closely monitoring to guide its policy decisions. This cautious stance reflects the Fed’s aim to balance economic growth with inflation control.

With the DIA and SPY sporting fresh record highs we now face the ramp up of earnings reports likely to inspire significant price volatility. The rising dollar and bond yields continue to be a contradiction to the market’s bullish enthusiasm and the T2122 indicator continues to flag a short-term overbought condition. Stay with the trend but tighten stops as it would only take a minor stumble to trigger a profit taking wave.

Monday saw the bulls in control from the start. SPY gapped up 0.29%, DIA opened 0.10% lower, and QQQ gapped up 0.49%. From there, the Bulls took over in all three major index ETFs. The QQQ rallied sharply for 30 minutes, SPY rallied strongly tor 60 minutes, and DIA rallied more modestly, but steadily all day. After their initial rallies, SPY and QQQ traded mostly sideways with a slight bullish lean the rest of the day. It is worth noting that there was profit-taking across the board in the last 10 minutes. This action gave us large-body, white body candles in the SPY and DIA as well as a white-bodied candle in the QQQ. SPY gapped up and printed a new all-time high and new all-time high close. DIA opened a bit lower but gave us a large white-body candle that also printed a new all-time high and new all-time high close. QQQ gapped up well out of its range going back to late September. It closed as a white Spinning Top with the larger wick at the top and ended 1.25% below its all-time high. This all happened on well-below average volume in all three major index ETFs.

On the day, nine of the 10 sectors were in the green with Utilities (+1.27%) out in front leading the market higher. On the other side, Energy (-0.36%) was by far the laggard. Meanwhile, SPY gained 0.82%, DIA gained 0.50%, and QQQ gained 0.84%. VXX fell another 3.55% to close at 52.15 and T2122 fell but remained in the top half of its overbought territory, closing at 91.78. At the same time, 10-Year bond yields were flat at 4.096% while Oil (WTI) dropped 3.72% to close at $72.75 per barrel. So, the Bulls were again in control from the open. This led to a morning rally and then a drift higher the rest of the day in SPY, QQQ, and DIA. Once again, only a little profit-taking the last few minutes of the day stopped the SPY and DIA from closing on the highs.

There was no major economic news or earnings reports scheduled for Monday.

In Fed news, on Monday, Minneapolis Fed President Kashkari indicated that more rate cuts lie ahead, but guided expectations toward more modest rate cuts. Kashkari said, “As of right now, it appears likely that further modest reductions in our policy rate will be appropriate in the coming quarters to achieve both sides of our mandate.” As usual, he promoted the “data driven” mantra, saying “ultimately, the path ahead for policy will be driven by the actual economic, inflation and labor market data.” He went on to say that the economy is not on the verge of a rapid slowdown, but the Fed is “in the final stages of bringing inflation down to our 2% target.” Later, Fed Governor Waller called for “more caution” (smaller rate cuts) in the interest reductions ahead. Waller said, “Whatever happens in the near term, my baseline still calls for reducing the policy rate gradually over the next year.” While saying that there is “considerable room” to cut rates, he said “We are in the sweet spot right now, we got to keep it there, that’s our job.” He continued, “I view the totality of the data as saying monetary policy should proceed with more caution on the pace of rate cuts than was needed at the September meeting.” Waller concluded, “I will be watching to see whether data, due out before our next meeting, on inflation, the labor market and economic activity confirms or undercuts my inclination to be more cautious about loosening monetary policy.” (When asked what the word “gradually” means, Waller said, “It’s in the eye of the beholder, … That’s for you guys to figure out.”

In stock news, on Monday, ADBE said it has begun rolling out its Firefly AI model that can generate video from text prompts. Later, activist investor Elliott Investment Mgmt. has formally requested a shareholder meeting of LUV. (Elliott plans to put forward its own slate of eight directors against eight existing board members. For reference, LUV has a 12-member board with three open seats.) At the same time, GM and BCS both announced they have signed a long-term credit card partnership. Later, Danish drug maker Lundbeck A/S agreed to acquire LBPH for $2.6 billion ($60/share), which was a 54% premium on Friday’s close price. At the same time, GOOGL announced it had signed an agreement to buy 500 megawatts of electricity from multiple small modular nuclear reactors from Kairos Power. This will help support GOOGL’s AI processing. Later, VNDA rejected a second ($8/share) takeover bid from UK-based Cycle Pharmaceuticals. (VNDA closed a $4.44 prior to the $8/share offer and closed up to $4.81 on the news.)

Elsewhere, TSLA took another hit related to its Robotaxi “unveil” event last week. This came as Bloomberg reporting confirmed that the TSLA Optimus humanoid robots highlighted at the event were actually just radio-control units being controlled by human “driver.” At the same time, HYMTF (Hyundai) sold part of their Indian unit “Hyundai India” via a $989.4 million IPO. BLK, Fidelity, and the government of Singapore each bought $77 million stakes while Indian mutual funds bought $340 million. (At that valuation, the unit represents 40% of the HYMTF market cap.) Later, the Wall Street Journal reported that SBUX will offer fewer discounts and promotions as part of a plan to reposition SBUX as a premium brand and getting customers to pay full price. After the close, PSX announced it will sell 49% of its Coop Mineraloel AG to its Swiss joint venture partner for $1.24 billion. (The joint venture operates 324 petrol stations across Switzerland.)

In stock legal and governmental news, on Monday, acting US Labor Sec. Su flew to Seattle to meet with both sides in the BA strike that is entering its fifth week. (In related news, BA said it will issue “60-day” notices to another tranche of engineering union workers on November 15, with a second wave of 60-day notices going out in December if the strike had not been resolved.) After the close, Blue Cross Blue Shield agreed to pay $2.8 billion to settle class action lawsuits from hospitals, physicians, and other healthcare providers who alleged they had been underpaid for reimbursements. (The deal is still subject to approval by a US District Judge in Alabama.)

In analyst news, heading into earnings season, Bloomberg Intelligence reported that the data they have collected show analysts expect S&P 500 firms to report a 4.2% increase in third-quarter earnings versus a year earlier. However, company guidance, implies a jump of about 16%. This unusually large difference between the forecasts suggest to Bloomberg that companies should easily beat the estimates on average.

In miscellaneous news, on Monday, FEMA reported that over the weekend contractors in NC were forced to cease work and return to their hotels Sunday while security was arranged. This came after some of the lies of the disgraced ex-President and his conspiracy-loving minions came home to roost. On Sunday, active military units that had been deployed to help recovery came across a militia group out “hunting FEMA workers” (based on the militia’s belief of the lies spread by the MAGA fools). Separately, the Sheriff arrested one man armed with a handgun and semi-auto rifle, apparently from the same militia, who was out menacing recovery efforts, but he was later released on bond. Two full days of recovery in Western NC and Eastern TN lost thanks to the right-wing stirring hatred and distrust for the political gain of one man. Elsewhere, in Russia that man’s friend invited fellow BRICS members to join together to create an alternative to the IMF to counter Western political influence throughout the world.

In Middle East news, on Monday, Israel continued strikes in both Gaza and Lebanon. One of the strikes in Gaza hit a Palestinian hospital and refugee camp located beside the medical building. (There was video of patients burning alive in their hospital beds.) more than two dozen were killed including many children. Meanwhile, Israeli PM Netanyahu again demanded that the UN remove peacekeepers and observers from Lebanon, falsely claiming UN troops were shields for Hezbollah. On the other side, Hezbollah made a drone attack on an IDF base, killing four Israeli soldiers and injuring 60.

Overnight, Asian markets were mixed with China out front leading the losers down. Hong Kong (-3.67%), Shenzhen (-2.53%), and Shanghai (-2.53%) saw by far the biggest losses. Meanwhile, Taiwan (+1.38%), Australia (+0.79%), and Japan (+0.77%) paced the six gainers. In Europe, we see a similarly mixed picture that leans toward the red at midday. The CAC (-0.90%), DAX (+0.15%), and FTSE (-0.56%) lead the region with just five green bourses versus nine red ones in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing to a start just on the red side of flat. The DIA implies a -0.05% open, the SPY is implying a -0.01% open, and the QQQ implies a -0.06% open at this hour. At the same time, 10-Year bonds are down to 4.073% and Oil (WTI) has plummeted another 4.66% to $70.41 per barrel in early trading.

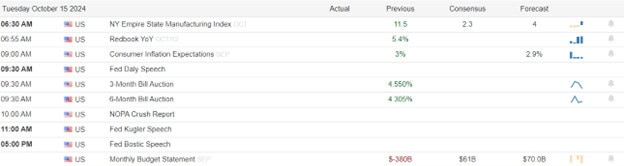

The major economic news scheduled for Tuesday is limited to NY Empire State Mfg. Index (8:30 a.m.), September NY Fed 1-Year Inflation Expectations, and September Federal Budget Balance (2 p.m.). We also hear from Fed members Daly (11:30 a.m.) and Bostic (7 p.m.). The major earnings reports scheduled for before the open include ACI, BAC, SCHW, C, ERIC, GS, JNJ, PNC, PGR, STT, UNH, and WBA. Then, after the close, IBKR, JBHT, OMC, and UAL report.

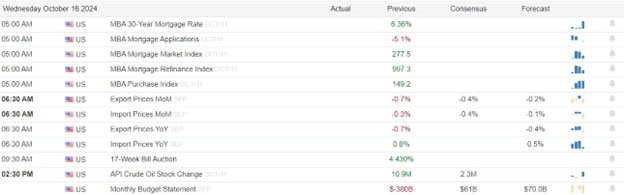

In economic news later this week, on Wednesday, September Export Price Index, September Import Index, and API Weekly Crude Stocks are reported. On Thursday, we get Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, September Core Retail Sales, Philly Fed Mfg. Index, Philly Fed Mfg. Employment, September Retail Control, September Retail Sales, September Industrial Production, August Business Inventories, August Retail Inventories, Weekly EIA Crude Oil Inventories, and the Fed Balance Sheet. Finally, on Friday, Preliminary September Building Permits and Preliminary September Housing Starts are reported. We also hear from Fed Governor Waller.

In terms of earnings reports later this week, on Wednesday, ABT, ASML, CFG, FHN, MS, PLD, SYF, USB, AA, CCI, CSX, DFS, EFX, KMI, LBRT, PPG, STLD, and SNV report. On Thursday, we hear from, BX, CMC, ELV, HBAN, INFY, KEY, MTB, MAN, MMC, SNA, TSM, TRV, TFC, WBS, WIT, CCK, ISRG, NFLX, WDFC, and WAL. Finally, on Friday, ALLY, AXP, ALV, CMA, FITB, PG, RF, and SLB report.

So far this morning, BAC, ERIC, GS, JNJ, PNC, STT, UNH, and WBA all reported beats on both the revenue and earnings lines. STT in particular had huge beats (+29.6% on revenue and +8.7% on earnings) while BAC managed +10.0% on revenue and +3.8% on earnings. GS was the king on profit, delivering a 22.6% beat on the earnings line.

With that background, it seems the premarket is undecided with all three major index ETFs basically flat and giving use Doji candles in the early session. The SPY, DIA, and QQQ all remain above their T-line (8ema). So, the short-term trend remains bullish. The mid-term and longer-term trends are also strongly Bull in all three. With regard to extension, none of the major index ETFs are too far extended from its T-line (8ema), although it is worth noting that DIA is getting close to extended. However, the T2122 indicator remains in the upper half of its overbought range. So, markets have room to run either direction, if traders can find momentum, but the Bears have more slack to work with today. With regard to those 10 big dog tickers, six are in the green this morning. AAPL (+0.88%) leads the way in gain while AMD (-1.59%) is the laggard in that regard. That biggest dog, NVDA (-0.62%) is back to leading all other tickers by a factor of three in terms of dollar-volume traded.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Markets diverged at the opening bell Friday. SPY opened just 0.01% lower, DIA opened 0.16% higher, and QQQ gapped down 0.39%. However, regardless of their open, the Bulls stepped in and rallied all three major index ETFs sharply for an hour. That was about it for the say as the SPY, DIA and QQQ meandered sideways with a slight bullish trend the rest of the day. This action gave us large white-bodied candles with small profit-taking wicks at the top in all three major index ETFs. SPY and DIA both printed new all-time highs and new all-time high closes on Doji Continuation Pattern (Doji Sandwich) signals. Meanwhile, the QQQ gave us the highest close since July 16. This happened on just above-average volume in DIA, just below-average volume in the SPY, and well-below average volume in the QQQ.

On the day, all 10 sectors were in the green with Utilities (+2.01%) well out in front leading the market higher. On the other side, Communication Services (+0.30%) was the laggard. Meanwhile, SPY gained 0.60%, DIA gained 0.96%, and QQQ gained just 0.16%. VXX fell 1.17% to close at 54.07 and T2122 spiked to the top of its overbought territory, closing at 93.98. At the same time, 10-Year bond yields climbed to close at 4.096% while Oil (WTI) fell 0.47% to close at $75.49 per barrel. So, the Bulls ruled the roost Friday as a strong morning rally led to a melt-up after the first hour. Only a little profit-taking the last few minutes of the day stopped the three major index ETFs from closing on the highs.

The major economic news scheduled for Friday included September Core PPI, which came in down, as expected, at +0.2% (compared to at +0.2% forecast and August’s +0.3% value). On the headline number, September PPI was down and better than was anticipated at 0.0% (versus a forecast of +0.1% and well down from August’s +0.2%). Later, Preliminary October Michigan Consumer Sentiment was down to 68.9 (versus a 70.9 forecast and a 70.1 September reading). In terms of the outlook, the Preliminary October Michigan Consumer Expectations were also down at 72.9 (compared to a 75.0 forecast and September’s 74.4 value). In terms of inflation, the Preliminary October Michigan 1-Year Inflation Expectations popped to 2.9% (versus a 2.7% forecast and previous month value). On the longer-term, Preliminary October Michigan 5-Year Inflation Expectations were down as expected to 3.0% (compared to a 3.0% forecast and a September 2.7% reading).

In stock news, on Friday, Nippon Steel announced it would sell its 50% stake in a joint-venture steel plant in AL to MT…if the X acquisition succeeds. Nippon would take a $1.55 billion loss on the joint-venture by selling their stake to MT for one dollar. Later, Bloomberg reported that HON is in advanced talks to sell its face mask (PPE gear) unit to private equity firm Odyssey for about $1.5 billion. At the same time, Reuters reported that CVS is exiting its “core infusion services” business and plans to close or sell 29 pharmacies as a result. (CVS had stopped taking new patients in that unit on Oct. 8.) The unit was purchase in 2013 for $2.1 billion. Meanwhile, after posting strong earnings, executives from both JPM and WFC commented that the consumers are still in good shape. JPM’s CFO said “Overall, we see the spending patterns as being sort of solid.” The CFO of WFC echoed the same sentiment, telling reporters that “spending on credit and debit cards, while down a little from earlier this year, was still quite solid.” Later, WSR said it will “carefully consider” at $15/share takeover offer from MCB Real Estate. (WSR stock closed at $14.15 Friday.)

In BA news, the company announced it was cutting 17,000 jobs (about 10% of workforce globally) and will delay the first delivery of its new 777X jet by a year (that plane had been halted prestrike due to cracking in the part connect engines to its wings). The company cited its dire financial situation as a month-long strike by 33k employees have idled manufacturing and delivery of its most profitable plane. (Years of quality debacles and mismanagement were also massive contributors.) Analysts say the move, as well as rescinding its most recent contract offer are moves designed to pressure the union into ending the strike. On the other side, credit analysts have BA on credit watch and have already said they will cut the company credit rating to junk unless the strike is resolved “soon.”

In stock legal and governmental news, on Friday, BA filed unfair labor practices against the union representing 33k striking workers with the NLRB. The company alleges the union is bargaining in bad faith. In unrelated news, the US Dept. of Transportation Inspector General said the FAA oversight of BA production was ineffective. The IG said the FAA did not have enough comprehensive presence to identify discrepancies and company non-compliance. (Of course, that is the entire intent of deregulation, cuts to the size of government, and moves toward company self-certification that has been lobbied for and granted for decades.) Later, a federal judge in TX criticized the terms of the plea deal BA had taken to avoid prosecution for violations of an earlier consent decree related to two fatal 737 MAX planes. The judge pressed the Dept. of Justice to justify the leniency of giving that deal to BA. (He later said he would rule on whether the deal was valid in the near future.)

Elsewhere, the NLRB filed a complaint against AAPL for restricting employee use of social media and messaging apps and doing illegal monitoring of them as a means of discouraging unionization. Later, a US Appeals Court placed approvals and permits for a KMI gas pipeline in TN on hold by over-riding the Army Corps of Engineers permit and TN Dept. of Environment and Conservations certification. The court said the stay would give the court time to consider the merits of a lawsuit brought by environmental groups. On Saturday, GOOGL filed a motion asking the judge to place his final ruling on the fate of “opening up the Google Play Store” following the jury ruling that GOOGL was an illegal monopoly. (GOOGL ask the judge to place an indefinitely hold on his judgement, which was due by November 1, while the company pursues appeals.)

In miscellaneous news, on Friday, the state of CA confirmed six more human cases of bird flu (four Thursday and two Friday). The US CDC said that all six cases appear to be due to human contact with animals (as opposed to human transmission) and that the public risk of the flu remains low as a result. Elsewhere, US and European officials confirmed to Bloomberg that India has become the second-biggest illegitimate supplier of restricted components (like microchips) to Russia, behind China. This comes as India doubled its export of those items to Russia in both April and May and increased it by more than 50% from those levels in July. Meanwhile, in Russian invasion news, on Friday multiple journalist outlets, all citing South Korean sources, reported the latter had made intercepts of communication between North Korean military units. Those intercepts indicate North Korea has sent troops to help in missile targeting and is now preparing to send ground troops to Ukraine to fight on behalf of Russia. (Obviously, this could give Russia thousands of trained troops, but may also result in changes to US policy on the use of US arms and potentially changes South Korea’s calculus on providing arms to Ukraine.) Russia denied the reports

In Middle East news, on Friday, the Israeli campaigns in Lebanon and Gaza continued as the Israelis fired on UN troop positions for the second day in a row, injuring another two of the peacekeepers. Israel also fired on Lebanese government (not Hezbollah) troops. However, the worse of the Israeli attacks Friday were in a residential section of central Beirut where bombing took out another pair of apartment blocks, a number of shops, as well as a refugee encampment. For their part, Hezbollah fired dozens of rockets into Northern Israel in response. On Saturday, Israel bombed towns in northern Lebanon, ordered the evacuation of 23 villages in “southern” Lebanon (North of Beirut), and also bombed the Bekaa Valley (45 miles Northeast of Beirut). Further south, Israel laid down heavy bombardment across northern Gaza, killing a few dozen more people. On Sunday, Israel ordered more evacuations in Lebanon, now including fully one-third of that country’s population has been ordered out. (This includes UN peacekeepers, where Israel has attacked and breached two UN bases Sunday, ordering UN troops to leave the country…for their own safety.)

In China news, on Saturday, Chinese Finance Minister Foan held a press conference in Beijing that was intended to calm markets. Foan pledged that the government will “significantly increase” debt to revive its sputtering economy. However, details on the actual amounts left investors guessing about the total size of the stimulus. (Last week the market had expected massive stimulus, but only got one-fifteenth the amount they had expected.) Foan said programs will offer subsidies for low-income people and also support property markets. Separately, Bloomberg reported Beijing is now considering injecting $142 billion into the country’s largest banks on top of $284 billion in stimulus (resulting from special sovereign bond sales) this year to be used to spur the economy. (Half of the $284 billion was to go to local governments and the other half to incentives for buying home appliances and other durable goods.)

Overnight, Asian markets were mostly green. Only Hong Kong (-0.75%), and New Zealand (-0.61%) were red while Shenzhen (+2.65%) and Shanghai (+2.07%) paced the 10 gaining exchanges. In Europe, markets are more mixed at midday with six bourses in the green and eight in the red. The CAC (-0.30%), DAX (+0.23%), and FTSE (-0.07%) are typical in early afternoon trade. Meanwhile, in the US, as of 7:30 a.m., Futures are pointing toward a mixed and modest start to the week. The DIA implies a -0.16% open, the SPY is implying a +0.15% open, and the QQQ implies a +0.27% open at this hour. At the same time, 10-Year bond yields are at 4.096% and Oil (WTI) is down 2.51% to $73.66 per barrel in early trading.

The major economic news scheduled for Monday are limited to NY Fed 1-Year Consumer Inflation Expectations (11 a.m.) and September Federal Budget Balance (2 p.m.). However, we also hear from Fed Governor Waller (3 p.m.). There are no major earnings reports scheduled for either before the open or after the close.

In economic news later this week, on Tuesday, we get NY Empire State Mfg. Index. We also hear from Fed member Daly. Then Wednesday, September Export Price Index, September Import Index, and API Weekly Crude Stocks are reported. On Thursday, we get Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, September Core Retail Sales, Philly Fed Mfg. Index, Philly Fed Mfg. Employment, September Retail Control, September Retail Sales, September Industrial Production, August Business Inventories, August Retail Inventories, Weekly EIA Crude Oil Inventories, and the Fed Balance Sheet. Finally, on Friday, Preliminary September Building Permits and Preliminary September Housing Starts are reported. We also hear from Fed Governor Waller.

In terms of earnings reports later this week, on Tuesday, we hear from ACI, BAC, SCHW, C, ERIC, GS, JNJ, PNC, PGR, STT, UNH, WBA, IBKR, JBHT, OMC, and UAL. Then Wednesday, ABT, ASML, CFG, FHN, MS, PLD, SYF, USB, AA, CCI, CSX, DFS, EFX, KMI, LBRT, PPG, STLD, and SNV report. On Thursday, we hear from, BX, CMC, ELV, HBAN, INFY, KEY, MTB, MAN, MMC, SNA, TSM, TRV, TFC, WBS, WIT, CCK, ISRG, NFLX, WDFC, and WAL. Finally, on Friday, ALLY, AXP, ALV, CMA, FITB, PG, RF, and SLB report.

With that background, the SPY and QQQ both opened the premarket flat but have printed white-body candles and are not far from their highs at this point of the early session up in clean air. Meanwhile, DIA opened higher but has put in a black candle so far to be back down slightly in the top of Friday’s candle. All three major index ETFs are above their T-line (8ema). So, the short-term trend remains modestly bullish. The mid-term trend remains bullish. In the longer-term we still have a strong Bull trend in all three major index ETFs. With regard to extension, none of the major index ETFs are too far extended from its T-line (8ema). However, the T2122 indicator is in the upper half of its overbought range. So, markets have room to run either direction, if traders can find momentum, but the Bears have more slack to work with today. With regard to those 10 big dog tickers, all 10 are in the green this morning. TSLA (+1.12%) leads the way in both price move and volume as it tries to come back from Friday’s robotaxi hammering. INTC (+0.25%) is the laggard among the 10. It is worth noting that TSLA has just slightly more dollar-volume traded than NVDA (+1.08%), which is abnormal (NVDA typically leads all other tickers by at least a factor of 2.5). So, just be aware.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Thursday was a volatile, up-and-down day in the market. SPY gapped down 0.22%, DIA opened flat, and QQQ gapped down 0.45%. From there, all three major index ETFs slowly rallied to the highs shortly after noon. Then they slowly sold off to the lows at 2:45 p.m. Finally, all three rallied back towards the highs again to end the day. This action gave us indecisive (more wick than body) candles in the top half of the prior day’s candle. The SPY printed a white-body Doji. Meanwhile, DIA gave us a black-bodied Hanging Man or Hammer type candle. Finally, the QQQ printed a white-bodied Spinning Top. All three remain above their T-line (8ema). This happened on below-average volume in the SPY, DIA, and QQQ.

On the day, eight of the 10 sectors were in the red with Communication Services (-0.72%) leading the way lower. On the other end of the spectrum, Energy (+0.88%) was far out ahead of the other sectors. Meanwhile, SPY lost 0.18%, DIA lost 0.09%, and QQQ lost 0.11%. VXX gained 1.26% to close at 54.71 and T2122 fell back to the lower half of its mid-range to 37.58. At the same time, 10-Year bond yields fell slightly to close at 4.067% while Oil (WTI) jumped another 3.21% to close at $75.59 per barrel. In summary, Thursday was just an indecisive “pause day” where most of the day was spent in the upper half of Wednesday’s strong bullish candle. There was no new all-time highs or new all-time high closes. However, SPY and DIA are withing spitting distance of both.

The major economic news scheduled for Thursday includes Weekly Initial Jobless Claims, which came in significantly higher than expected at 258k (compared to a 231k forecast and the previous week’s 225k). On the ongoing front, Weekly Continuing Jobless Claims were higher than expected at 1,861k (versus the 1,830k forecast and the prior week’s 1,819k). At the same time, September Core CPI (month-on-month) was flat at +0.3% (which was higher than the +0.2% forecast, but in-line with August’s +0.3%). On the annualized basis, September Core CPI (year-on-year) increased a tick to 3.3% (compared to an August reading and forecast of 3.2%). On the headline number, September CPI (month-on-month) was flat at +0.2% (versus a +0.1% forecast and in-line with August’s +0.2% value). Later, after the close, the September Fed Balance Sheet stayed dead flat for the week at $7.047 trillion.

In Fed news, on Thursday, Chicago Fed President Goolsbee reiterate that he foresees a series of rate cuts over the next year. Goolsbee said, “Over a 12-18 month period, I think we are going to gradually, whatever word you want to use, move to a steady state policy rate.” Later, NY Fed President Williams said he too expects more rate cuts lay ahead. Williams said, “Based on my current forecast for the economy, I expect that it will be appropriate to continue the process of moving the stance of monetary policy to a more neutral setting over time.” As usual, Williams indicated that all specific meeting decisions will be data driven. He said, “the timing and pace of future adjustments to interest rates will be based on the evolution of the data, the economic outlook, and the risks to achieving our goals.” Later, Atlanta Fed President Bostic seemed to indicate the Fed may skip a rate cut in November. Bostic said, “I am totally comfortable with skipping a meeting if the data suggests that’s appropriate.” He went on to say, “I think we have the ability to be patient and wait and let things play out a little longer…. There are elements of today’s report which I think validate that view.”

In stock news, on Thursday, NVDA held an “AI summit” to outline the advancements in its next generation AI chips. In an attempt to steal some of NVDA’s thunder, AMD also announced its own next generation AI chip (to be available in Q4 and ship in quantity in early 2025) at an event at the same time. (The problem for AMD is that NVDA offers a proprietary on-chip technology called CUDA cores and most AI software is written to take advantage of that technology. This means those users are locked into NVDA AI processors. AMD is still building out its competing tech called ROCm.) NVDA stock was up 1.,63% while AMD (-4.00%) got hammered. Later, GM announced they will be offering new home energy storage and solar collection products to EV customers (just as TSLA offers).

Elsewhere, UBS said integration of CS data into the UBS systems is on track after a test run. (UBS acquired CS in March 2023 to prevent the latter’s collapse.) Later, in a novel excuse, DAL warned of lower revenue and blamed the Q4 forecast reduction on the presidential election, saying that people are avoiding travel so they can stay home to vote. At the same time, Bloomberg reported that TGI is exploring strategic options including a sale of the company. At the same time, SNY announced it had closed the sale of its consumer health unit for $16.4 billion (to a private equity firm). After the close, SEC filings showed that BRKB has now reduced its BAC holdings below 10% by selling another 9.5 million shares this week. This sale netted BRKB $382.4 million.

In stock legal and governmental news, on Thursday, the Consumer Product Safety Commission announced MAT is recalling 21 different models of infant swings after five reported suffocation deaths. In addition, MAT is offering a $25 partial refund to those customers who just cut off the headrest and body support pad (offending parts) on their own. (About 2.2 million of the swings were sold in North American between 2012 and 2022.) At the same time, the US Justice Dept. announced that TD has plead guilty to conspiracy to commit money laundering and will pay a massive $3.1 billion fine. TD will also be subject to an asset cap and other restrictions as part of the guilty plea. Later, MSFT, GOOGL, META, and AMZN (among others) have proposed an “alternative framework” for how data centers pay for power in OH. This is a direct challenge to the AEP proposal that cryptocurrency miners and data centers prepay or offer other financial assurances for their massive energy needs.

Meanwhile, the US Dept. of Justice announced that TEVA has agreed to pay $450 million to resolve allegation it used charities to help cover Medicare patient out-of-pocket drug costs as a way to pay kickbacks to boost sales of its multiple sclerosis drug. (12 other drugmakers had previously settled over the same charges to the tune of $1 billion in fines. However, the case against REGN remains pending.) Later, a Philadelphi jury ordered BAYRY (Bayer) to pay $78 million to a PA man who had alleged he got cancer from using the company’s Roundup weedkiller. At the same time, a US Bankruptcy Judge overruled the motion from the US Justice Dept., ruling in favor of LNJ which is now allowed to pursue a third attempt to get a bankruptcy judge to end tens of thousands of lawsuits over talc cancer risks. (JNJ had “venue shopped” by filing the latest bankruptcy in TX after twice being denied by NJ bankruptcy courts.) Later, following a decade of unfulfilled promised and missed deadlines, TSLA held an event Thursday night to unveil their robotaxi, which they dubbed “Cybertaxi.”

In miscellaneous news, on Thursday, the largest US power grid operator issued a warning over potential disruptions which may be caused by a massive solar flare. (The warning expired very early Friday morning. Meanwhile, the Center for Disease Control said it had identified a cluster of 18 cases of MPOX (formerly Monkey Pox) that are drug-resistant across five states. Elsewhere, the FTC finalized changes to a rule covering what information companies must turn over when seeking approval for proposed mergers. Finally, Hurricane Milton appears to have killed 10 and left three million customers without power at one point Thursday. However, the damage was much less than had been expected, with the bulk coming from flooding due to intense rain as well as 27 tornadoes spawn by the storm. (After the close, DIS and CMCSA announced their theme parks in Orlando would resume operations Friday.)

In Middle East news, Israeli campaigns in Lebanon and Gaza continued Thursday. Israel killed 30 in the bombing of a school/shelter in Gaza and dozens more in attacks on buildings in central Beirut. In addition, Israel injured two UN peacekeepers in a tank fire accident. (The peacekeepers have been in place between Israel and Hezbollah in southern Lebanon since 1978, following a previous Israeli invasion.) In Europe, on the heels of France’s call for an arms embargo on Israel, Italy summoned the Israeli ambassador to make formal complaints over “unacceptable” actions in Southern Lebanon.

In other war news, it was confirmed Thursday that Russia has attacked three civilian ships under foreign flag (not Russian or Ukrainian) that were carrying commercial grain shipments. (None of the ships have been sunk. However, they were damaged and this is an escalation from early in Russia’s invasion when it boarded, inspected, and/or turned back ships.) In response, insurance rates on a $50 million ship increased by $125k per voyage in the Black Sea.

Overnight, Asian markets were mixed but leaned toward the red side. Shenzhen (-3.92%) and Shanghai (-2.55%) were far out front in terms of losses while Hong Kong (+2.98%) and Taiwan (+1.07%) were way out front leading the gainers. In Europe, we nearly see green across the board at midday the sole exception of London. The CAC (+0.10%), DAX (+0.19%), and laggard FTSE (-0.08%) lead the region higher in early afternoon trade. In the US, as of 8 a.m., Futures point toward a slightly lower start to the day. The DIA implies a -0.04% open, the SPY is implying a -0.10% open, and the QQQ implies a -0.30% open at this hour. At the same time, 10-Year bond yields are up to 4.098% and Oil (WTI) is down 0.71% to $75.29 per barrel in early trading.

The major economic news scheduled for Friday include September Core PPI and September PPI (both at 8:30 a.m.), Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-Year Inflation Expectations, and Michigan 5-Year Inflation Expectations (all at 10 a.m.), and the WASDE Ag report (noon). We also hear from Fed Governor Bowman at 1:10 p.m. The major earnings reports scheduled for before the open are limited to BK, BLK, FAST, JPM, and WFC as earnings season kicks into gear again. Then, after the close, there are no major reports scheduled.

So far this morning, BK, BLK, JPM, and WFC show a clean sweep of beats on both the revenue and earnings lines by the big banks. However, FAST missed on revenue even as it came in in-line on earnings.

With that background, markets are just on the red side of flat again at this point of the premarket. QQQ has the worst-looking candle and, even so, it is just a black spinning top inside the top half of yesterday’s inside candle. All three major index ETFs are above their T-line (8ema). So, the short-term trend remains modestly bullish. The mid-term trend remains bullish. In the longer-term we still have a strong Bull trend in all three major index ETFs. With regard to extension, none of the major index ETFs are extended from its T-line (8ema). In addition, the T2122 indicator remains in the lower half of its mid-range. So, markets have room to run either direction, if either the Bulls or Bears can find momentum. With regard to those 10 big dog tickers, six of the 10 are in the red this morning. TSLA (-6.01%) is getting hammered after a very unimpressive reveal of its robotaxi late last night. AMD (+0.96%) leads the gainers and for the first time in a long time, TSLA leads in terms of dollar-volume traded even on not heavy trading as NVDA (-0.01%) has EXTREMELY light, as in 10% of normal, volume in the premarket. This is very abnormal premarket trading. Don’t forget its Friday. So, prepare your account for the weekend.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Markets started the day flat, rallied into noon, and then traded sideways before rallying again the last 30 minutes. SPY opened up 0.02%, DIA opened dead flat, and QQQ opened down 0.06%. From there SPY and DIA began their rally into noon. QQQ pulled back for 20 minutes after the open, but then got in line and followed the other major index ETFs higher. At noon, all three took a 3.5-hour break before rallying into new highs near the close. They all would have closed on their highs except for profit taking the last 5 minutes. This action gave us large, white-bodied candles with tiny upper wicks in all three major index ETF. SPY printed a new all-time high and closed at a new all-time high close. DIA gave us a new all-time high close. QQQ didn’t make it as far, only printing its highest close since July 16. (QQQ is just less than 2% away from its all-time high close.) This all took place on below-average volume in SPY and QQQ and above-average volume in DIA.

On the day, nine of the 10 sectors were in the green with Technology (+0.79%) leading but not way out ahead of other sectors. Only Utilities (-0.62%) was in the red and lagged far behind all other sectors. Meanwhile, SPY gained 0.69%, DIA gained 1.01%, and QQQ gained 0.79%. VXX fell almost 2.5% to close at 54.03 and T2122 climbed a bit, but remains in its mid-range, at 68.36. At the same time, 10-Year bond yields rose to close at 4.073% while Oil (WTI) fell 0.38% to close at $73.28 per barrel. In summary, it was the Bull’s market from the open of the session. A flat start across the board led to a strong morning rally. This was followed by an afternoon pause, but the Bulls came back for the last 30 minutes to drive us back to new highs. It is worth noting that the September Fed Meeting Minutes were a nothing burger.

The major economic news scheduled for Wednesday was limited to Weekly EIA Crude Oil Inventories came in with a larger inventory build than expected at +5.810 million barrels (compared to a +2.000-million-barrel forecast and ever versus the prior week’s +3.889 million barrels).

As mentioned, we also got the September FOMC Meeting Minutes in the afternoon on Wednesday. They really revealed nothing that was not know from Fed Chair Powell’s post-decision press conference and other Fed member statements since. It said that Fed members “were divided” on whether the rat cut should have been a half percent. (That said, the most hawkish FOMC member, Fed Governor Bowman, was the only voter to vote against the half-percent cut. She said she preferred a quarter-point cut instead. In fact, the minutes said “a substantial majority” of Fed members backed the half-percent cut.) The minutes said, “Some participants observed that they would’ve preferred a 25-basis-point reduction of the target range at this meeting, and a few others indicated that they could have supported such a decision.” Later, the minutes said, “Participants emphasized that it was important to communicate that the recalibration of the stance of policy at this meeting should not be interpreted as evidence of a less favorable economic outlook or as a signal that the pace of policy easing would be more rapid than participants’ assessments of the appropriate path.” The bottom line is that FOMC members believed the economy remains in good shape and are confident inflation is falling toward the 2% target. The minutes showed the division was not over any data in-hand, but rather about their forecast of the future economy.

In other Fed news, on Wednesday, Dallas Fed President Logan said she supported last month’s half-point rate cut. However, she said she also wants smaller cuts in the meetings ahead given remaining upside risks on inflation and “meaningful uncertainty” over the economic outlook. She said, “Following last month’s half-percentage-point cut in the fed funds rate, a more gradual path back to a normal policy stance will likely be appropriate from here to best balance the risks to our dual-mandate goals.”

In stock news, on Wednesday, TSLA announced that its sales of China-made vehicles were up 19.2% in September (year-on-year) in China. (For reference, the Chinese EV maker BYD, which is TSLA’s main competitor reported a 45.56% increase year-on-year in September.) At the same time, Bloomberg reported that TSLA’s robotaxi will have two front seats and gull-wing doors. The report also said TSLA CEO Musk is expected to “discuss “Full Self-Driving” software assistance from TSLA semis soon. Later, META announced it is expanding the availability of its AI chatbot (META AI) to 21 new markets, including the UK and Brazil in efforts to compete with OpenAI’s ChatGPT. At the same time, EADSY (Airbus) reported that its plane deliveries fell 9% in September to 50 compared to the same month in 2023. (This comes a day after BA reported just 33 planes delivered last month.) Later, Bloomberg reported that the CEO of STLA is planning on making major management changes as he faces heavy pressure. The report said, CEO Tavares’ plan (offered to the board to save his job at a two-day meeting this week) could affect finance teams, regional heads and brand executives among others. After the close, CNBC reported that AMZN is now testing full-automated mini-warehouses for Whole Foods stores. The move is intended to let customers pick up orders at the checkout and reduce shopping time.

In stock legal and governmental news, on Wednesday, NVAX received European Commission approval for its latest version of COVID-19 vaccine which targets the currently predominant JN.1 strain of the virus. The authorization was for individuals 12 years and older throughout the EU. At the same time, BIIB’s flezartamab antibody treatment received the FDA’s “breakthrough therapy” designation. BIIB said the drug will now begin late-stage trials. Later, the NHTSA announced that HMC is recalling 2 million cars and SUVs over a steering issue that can increase the risk of crashes. (!.7 million of the vehicles are in the US with the remainder in Canada and Mexico.)

Elsewhere, the FTC announced that MAR and its subsidiary HOT have agreed to put in place an information security program to settle charges related to several data breaches (affecting 344 million customers) between 2014 and 2020. Separately, MAR agreed to pay a $52 million penalty to 49 states and the District of Columbia over the same issue. Later, GSK has settled 80,000 Zantac cancer-related lawsuits for $2.2 billion. The settlement, reached with 10 class-action law firms represent 93% of the company’s pending Zantac suits. GSK also announced it would pay $70 million to settle a related whistleblower lawsuit. At the same time, SMNEY (Siemens Energy) filed a lawsuit against Venezuela-owned Citgo Petroleum trying to recover about $200 million from a promissory note that is in default.

In miscellaneous news, on Wednesday evening Hurricane Milton came ashore as a Category 3 storm, making landfall just south of Tampa Bay in Bradenton to Sarasota, FL. As of this morning, millions of residents and an unknown number of businesses are without power. However, the worst is past as the storm crossed the peninsula and headed back out to sea after crossing Florida. Ahead of the storm, the disgraced ex-President and MAGA minions continue to spread lies, distortions, and misinformation related to FEMA, responses, conspiracy theory-based motives, available money, and everything else. It got so bad that even some GOP members have broken ranks to try to correct the lies and limit the damage. Elsewhere, in China, President Xi Jinping seems to have gotten the message after two days of fierce selling in Chinese markets. The stimulus package announced Monday fell flat as it came in 1/15th of what had been expected. So, the Chinese government announced it will hold a briefing Saturday on fiscal policy that is intended to buttress growth.

In Middle East news, Israeli campaigns in Lebanon and Gaza continued Wednesday. Israel sent thousands of additional ground troops into Lebanon during the day. In addition, Israeli air strikes in a Gaza refugee camp killed dozens. At the same time, the first Israeli civilian deaths (two of them) were reported in Northern Israel after 90+ (per BBC, I’ve seen other numbers) retaliatory Hezbollah rockets were fired into that area. At the political level, Israeli PM Netanyahu got the phone call he had demanded with President Biden (before allowing his rival to travel to the US), who told him to limit civilian casualties. This call will likely clear the way for Netanyahu’s (rival and) Defense Minister Gallant to travel to the US to discuss the Israeli retaliation for last week’s 180-missile Iran strike. Meanwhile, Israel again warned Lebanon they will “fall into the abyss of a long war that will bring destruction and suffering similar to what we see in Gaza,” implying they could avoid this fate by getting rid of Hezbollah. (Presumably, this PR stunt would mean he wants the Christian, Druze, and Sunni Lebanese to start a Lebanese civil war and take over from Israel…in the middle of the Israeli invasion and bombing campaign. That seems a lot like demanding a unicorn. It also sounds like “Don’t make me hurt you…see what you made me do.”)

Overnight, Asian markets were mostly green as the Chinese promise of a Saturday meeting to explain fiscal policy and how it will prop up their economy stopped the bleeding in Chinese markets. Shenzhen (-0.82%) was the only significant loser in the region while Hong Kong (+2.98%) and Shanghai (+1.32%) led the gains. In Europe, the bourses lean toward the red side at midday with 11 of 14 exchanges below break-even. The CAC (-0.22%), DAX (-0.06%), and FTSE (-0.25%) lead the region lower in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a slightly red star to the day. The DIA implies a -0.11% open, the SPY is implying a -0.18% open, and the QQQ implies a -0.22% open at this hour. At the same time, 10-Year bond yields are up to 4.092% and Oil (WTI) has popped 1.3% to $74.18 per barrel in early trading.

The major economic news scheduled for Thursday includes Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, September Core CPI, and September CPI, (all at 8:30 a.m.), September Federal Budget Balance (2 p.m.), and Fed Balance Sheet (4:30 p.m.). We also hear from Fed member Williams (11 a.m.). The no major earnings reports scheduled for before the open are limited to DAL and DPZ. Then, after the close, there are no major reports scheduled.

In economic news later this week, on Friday, September Core PPI, September PPI, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-Year Inflation Expectations, Michigan 5-Year Inflation Expectations, and the WASDE Ag report are delivered.

In terms of earnings reports later this week, on Friday, earnings season kicks off again in earnest as BK, BLK, FAST, JPM, and WFC report.

So far this morning, SVNDY reported beats on both the revenue and earnings lines. At the same time, DPZ missed on revenue while beating on earnings. However, DAL reported missed on both the top and bottom lines.

With that background, markets are just on the red side of flat at this point of the premarket. SPY opened the early session flat and has traded slightly lower. QQQ opened premarket lower and traded down before recovering. Meanwhile, DIA gapped a bit lower and has put in a white candle in the early session to also recover. All three major index ETFs are above their T-line (8ema). So, the short-term trend remains modestly bullish. The mid-term trend remains bullish. In the longer-term we still have a strong Bull trend in all three major index ETFs. (SPY and DIA both printed new all-time high closes again Wednesday.) With regard to extension, none of the major index ETFs are extended from its T-line (8ema). In addition, the T2122 indicator remains in the mid-range. So, markets have room to run either direction, if either the Bulls or Bears can find momentum. With regard to those 10 big dog tickers, seven of the 10 are in the red this morning. TSLA (+1.15%) leads the three gainers while AAPL (-0.33%) is at the head of those headed lower. The biggest dog, NVDA (-0.14%) is barely ahead of TSLA in terms of the dollar-volume traded. This is abnormal (at least for the last year or so) and not the common state of recent bullish moves by the market.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

U.S. stock futures dipped on Thursday as investors await the release of September’s CPI report, scheduled for 8:30 a.m. ET. The report is expected to provide further indications of whether inflation is continuing to cool. Economists surveyed by Dow Jones predict a modest 0.1% increase in the CPI monthly and a 2.3% rise over the past year. Additionally, Thursday morning will see the release of weekly initial jobless claims, adding to the day’s economic data that investors will be closely monitoring.

European markets opened slightly lower on Thursday morning as investors awaited the latest U.S. inflation data. The insurance sector saw a boost, with stocks rising by 0.72%, driven by stronger prospects following Hurricane Milton’s severe impact on Florida. Conversely, mining stocks experienced a decline, falling by 0.8%. This mixed performance reflects the varied investor sentiment across different sectors in anticipation of the upcoming economic indicators.

Asia-Pacific markets experienced a positive close on Thursday, with several key indices showing gains. In China, the central bank announced it is accepting applications from financial institutions to participate in a new liquidity tool, initially valued at 500 billion yuan ($70.7 billion), aimed at providing easier access to capital for the stock market.

Economic Calendar

Earnings Calendar

Notable reports for Wednesday before the bell include DAL, DPZ, NEOG, & TLRY. After the bell there are no notable reports.

News & Technicals’

Japanese convenience retailer Seven & i Holdings, the parent company of 7-Eleven, has revised its earnings forecast for the fiscal year ending February 2025, lowering its expectations. This decision comes as the company faces increasing pressure from investors to streamline its extensive business portfolio. In response, Seven & i Holdings announced plans to establish an intermediate holding company to manage its supermarket food business, specialty stores, and other ventures. This strategic move aims to enhance operational efficiency and address investor concerns about the company’s diverse range of businesses.

Amazon is experimenting with integrating automated mini warehouses into Whole Foods supermarkets, creating a new store format that enhances the shopping experience. This innovative approach allows customers to purchase items from Amazon’s online store and its mass-market supermarket chain while browsing Whole Foods, with the convenience of picking up their orders at checkout. By streamlining the shopping process, Amazon aims to attract more grocery shoppers and gain a competitive edge over its rivals, offering a one-stop solution for all their shopping needs.

Two former Pfizer executives, Ian Read and Frank D’Amelio, who were previously associated with activist investor Starboard Value’s campaign at the struggling pharmaceutical company, announced late Wednesday that they would step back from the effort. Both Read, the former CEO, and D’Amelio, the ex-CFO, expressed their full support for current CEO Albert Bourla and his management team. Meanwhile, Starboard Value has acquired a significant stake in Pfizer, amounting to approximately $1 billion, as it seeks to drive a turnaround at the company.

At their September meeting, Federal Reserve officials agreed to cut interest rates but faced uncertainty about the extent of the reduction. Minutes released on Wednesday revealed that a substantial majority of participants supported a half-percentage-point cut, though some expressed reservations about such a significant move. Since the meeting, economic indicators have suggested that the labor market is stronger than anticipated by those advocating for the 50-basis point cut, adding complexity to the decision-making process.

As we wait for September’s CPI report one must wonder if yesterday’s big push that set new record highs in the DIA and SPY if investors will be rewarded for their anticipation or disappointed should prices reverse. We will soon find out. The sharp rally in bond yields pushing rates higher seems to be a substantial contradiction to the bullishness. That said, it would be wise to be prepared for anything including the possibility we will still have to wait for earnings to really get prices moving.

U.S. stock futures dipped Wednesday as prices struggle to follow-through after a strong session Tuesday, driven by tech stocks and a decline in oil prices from their recent highs. Despite this positive momentum, the market could face further volatility, as October is historically the most turbulent month, especially with the U.S. presidential election just weeks away. Investors are also keenly awaiting the release of the latest Federal Reserve meeting minutes at 2 p.m. ET, which could provide further insights into the economic outlook and monetary policy direction.

On Wednesday, European markets experienced slight gains despite fluctuating positive sentiment, largely influenced by the volatility in Chinese markets. The mixed performance in Asia, especially the significant sell-off in Chinese stocks, led to a cautious mood among European investors. Nevertheless, certain sectors managed to post gains, with banks rising by 1.7% and oil and gas stocks adding 1.6%. Key events to watch in Europe today include the German government’s latest economic forecasts and the NATO defense ministers’ meeting in Belgium.

On Wednesday, Chinese stocks experienced a significant sell-off amid a volatile trading day across Asia-Pacific markets. The mainland CSI 300 index plummeted by 7.05%, ending a 10-day winning streak and closing at 3,955.98. Similarly, Hong Kong’s Hang Seng index dropped 1.7% in its final hour of trading. In contrast, Japan’s Nikkei 225 rose by 0.87% to 39,277.96, and the Topix index increased by 0.3%, closing at 2,707.24. Australia’s S&P/ASX 200 saw a modest gain of 0.13%, finishing at 8,187.4. Meanwhile, New Zealand’s central bank cut its policy rate by 50 basis points to 4.75%, whereas the Reserve Bank of India maintained its rate at 6.5%.

Economic Calendar

Earnings Calendar

Notable reports for Wednesday before the bell include HELE. After the bell reports include AZZ.

News & Technicals’

Boeing announced it has withdrawn its contract offer following a breakdown in negotiations with the machinist union. Over 32,000 Boeing machinists went on strike on September 13 after decisively rejecting a new contract proposal. The union stated that Boeing failed to offer wage increases and other improvements during the latest round of discussions, leading to the current impasse. This development marks a significant escalation in the labor dispute between Boeing and its machinists.

Starting Wednesday, Disneyland will increase the prices of its most popular tickets. While the base entry price will stay at $104, other ticket prices will rise by $7 to $12. Additionally, the cost of the Magic Key annual passes will see a hike of 6% to 20%, translating to an increase of $100 to $125 depending on the pass type. These adjustments reflect Disneyland’s ongoing efforts to manage demand and enhance the guest experience.

Late Tuesday, the Department of Justice announced it is contemplating a potential breakup of Google as an antitrust measure. The DOJ is evaluating both behavioral and structural remedies to prevent Google from leveraging products like Chrome, Play, and Android to favor its search engine. The judge has not yet ruled on these remedies, and Google is expected to appeal, which could prolong the legal process for years. This development marks a significant step in the ongoing scrutiny of Google’s market practices.

On Monday, a U.S. judge issued a permanent injunction requiring Google to provide alternatives to its Google Play store for downloading apps on Android phones. This ruling, delivered by Judge James Donato in a California court, represents the most significant outcome of Epic Games’ antitrust lawsuit against Google, which began in 2020. Additionally, Epic and Google will establish a three-person committee to review technical issues related to Google’s compliance with the injunction, according to the court filing.

Although very select stocks gave us an impression of a very bullish shift this morning, futures prove that the market remained locked in the consolidation range and struggle to follow through continues. The rising bond yields pushed mortgage rates higher triggering a sharp decline in applications this morning raising some uncertainty as we wait for the FOMC minutes. However, we are likely getting closer to big move in the market perhaps inspired by the Thursday CPI report or the big bank reports beginning Friday morning. Buckle up for a possible explosion of volatility in the days ahead.

Tuesday saw a drift higher across the market after the opening bell. SPY gapped up 0.47%, DIA gapped up 0.21%, and QQQ gapped up 0.52%. From there, both SPY and QQQ followed-through with a rally that lasted until 10:50 a.m. Then, those two major index ETFs ground sideways in a small range until 1 p.m. when a new steady rally kicked in. For its part, after the open, DIA immediately recrossed the gap and chopped sideways for the first hour. Then, it drifted slowly higher the rest of the day. This was broker by slight profit-taking the last minutes of the day in all three major index ETFs. This action gave us a large white-bodied candle in the SPY that recrossed above its T-line (8ema) and closed while testing its short-term downtrend line. (SPY also missed another all-time high close by just 65 cents.) At the same time, QQQ printed a large, white-bodied candle that crossed back above its T-line as well as its short-term downtrend line. For its part, DIA was the weakest of the three, giving us a white-body Spinning Top Bull Harami type candle that closed right at a retest of its T-line but did not get up to retest the short-term downtrend line. This happened on below-average volume in the SPY, DIA, and QQQ.

On the day, seven of the 10 sectors were in the green with Technology (+1.31%) far out in front (by 0.68%) of the rest of the group. On the other side, Energy (-2.30%) was by far the biggest mover and biggest loser. Meanwhile, SPY gained 0.95%, DIA gained 0.28%, and QQQ gained 1.49%. VXX fell 4.04% to close at 55.39 and T2122 climbed to the other side of its mid-range at 51.26. At the same time, 10-Year bond yields fell slightly to close at 4.018% while Oil (WTI) plummeted 4.24%, ostensibly on somewhat reduced Middle East war fears, to close at $73.89 per barrel. So, while there was no major driver for the rally Tuesday, Fed members generally leaning toward quarter-point cuts and a “no news is good news” feeling surrounding expansion of the conflicts (i.e. the next Israeli attack on Iran and perhaps Yemen also) led the Bulls to a modest gap up and then a drift higher.

The major economic news scheduled for Tuesday was limited to August Exports, which were up to $271.80 billion (compared to the July value of $266.60 billion). On the opposite side, August Imports were down a bit to $342.20 billion (versus July’s $345.40 billion reading). This resulted in an August Trade Balance of $70.40 billion (compared to a forecasted -$70.10 billion but down from July’s -$78.90 billion). Then, after the close, API Weekly Crude Stocks came in with a much bigger inventory build than anticipated at +10.900 million barrels (versus a forecasted +1.950 million barrels and the previous week’s 1.458-million-barrel drawdown).