Unable to agree on a stimulus deal, the futures were already pointing to a bearish open. The news that the President and the First Lady tested positive for COVID-19 added another layer of uncertainty for the path forward. Will the bull show the strength to defend the 50-day moving averages on the DIA, SPY, and QQQ or will the bear regain control of market direction? As we slide into the weekend, there seem to be more questions than answers for traders to grapple with, suggesting a volatile day of price action awaits.

Asian markets in a choppy session closed mixed but mostly lower overnight. European markets are lower across the board, with the DAX down 1% in reaction to the uncertainty ahead. Ahead of the Employment Situation number, US Futures point to a nasty gap down of more than 300 Dow points. With the path forward clouded in uncertainty, weigh your risk carefully as head into the weekend.

Economic Calendar

Earnings Calendar

On the Friday earnings calendar, we have eight companies on the list, but apparently, all of them are unconfirmed. Consequently, we have no notable reports today.

News & Technicals’

A choppy Thursday market session as we waited to hear deal or no deal on a fifth stimulus package. Failing to come to an agreement, the House moved forward, passing their 2.2 Trillion plan that has little to chance of getting past the Senate. According to reports, the two sides will continue to talk, but with congress about to recess, hopes that a deal has diminished. US Futures slipped into the red during the evening as a result. Then we heard the news the President and the First Lady tested positive for Covid-19, and futures quickly plunged 500 points. They have recovered from early morning lows, but the uncertainty about what comes next has the market facing a nasty gap down this morning.

Having recovered their 50-day averages, it will now be a critical test for the bulls to defend the level as support. A fall back below this crucial psychological level will damage the index chart technicals and could threaten the overall market confidence. Today we get a reading on the Employment Situation numbers before the bell, so get ready for a volatile morning of price action and carefully consider your risk as we head into an uncertain weekend.

Markets saw a significant gap higher at the open Thursday on renewed hopes for a new stimulus deal. However, we then faded that gap and started a roller-coaster day bouncing between the prior close and that cap-up open. In the end, this gave us indecisive Doji or Spinning Top candles in all 3 major indices. On the day, QQQ (led by those huge FAANGM stocks) closed up 1.59%, SPY up 0.64%, and DIA up 0.23%. VXX was basically flat at 25.01 and the T2122 (4-week New High/Low Ratio) remains in the mid-range at 53.55. 10-year bond yields were also flat at 0.679% and Oil (WTI) fell 4% to $38.58/barrel.

Despite the pre-market optimism Thursday, House Speaker Pelosi and Treasury Sec. Mnuchin were unable to reach a deal on more stimulus. This as the airline industry laid off 45,000 workers (more than the 32,000 threatened), but said they would rehire them if aa new $25 billion relief program is passed. In addition, reports surfaced saying the expiration of the $600 Enhanced Unemployment Payments has already begun causing a drag on the economy in terms of reduced personal expenditures. And more Fed speakers also echoed prior FOMC comments that more stimulus is needed. While no deal was reached Thursday, the House did pass another $2.2 Trillion stimulus bill, but again Senate Republicans are likely to not even consider the bill (2nd since May). Nonetheless, Speaker Pelosi told reporters that talks would continue today.

The (strangely) bi-partisan House Antitrust Committee completed its seventh and final hearing on antitrust actions by AAPL, AMZN, GOOG, and FB. A report will now be written and reviewed by committee members for at least several days. The themes seem to be increased staffing and funding for enforcement agencies, reversing court decisions that have over-ridden Congressional anti-trust intentions, shifting the burden to companies to prove that mergers were not anti-competitive, and prohibiting “anti-discriminatory” behaviors by companies. No specifics have yet been leaked on potential legislative remedies.

On the virus front, in the US, the numbers show we now have 7,497,256 confirmed cases and 212,694 deaths. The 7-day average daily new case count is back up to 42,952, while the 7-day average of deaths remains 731. This includes 30 states with increasing new case counts. Of course, the big US virus news today is that the President, First Lady, and close Trump Aide Hicks all tested positive and are now in quarantine. Their health is not an issue since they have the best healthcare possible for treating them. However, the image is important. In other virus news, AMZN reports that just under 20,000 of their employees have contracted Covid-19 so far (but for reference they have 1.37 million employees. So, compared to the general public, that 20,000 number is a bit over 40% less than expected.) CNBC also reported that vaccine trial participants (for PFE and MRNA candidates) have reported intense side-effects (fever, head/body aches, and exhaustion), but that those symptoms have only lasted a day on average. However, this was based on a minuscule sample of only 5 test subjects.

Globally, the numbers rose to 34,529,418 confirmed cases and the confirmed deaths are now at 1,028,517 deaths. (An increase of about 328,000 cases and 8,934 deaths.) Italy reported the highest increase in new cases since April on Thursday. However, following the President’s test results, no more international virus headlines were reported.

Overnight, Asian markets were mixed. Australia (-1.39%), Japan (-0.67%), Thailand (-0.81%) and Indonesia (-0.87%) paced the losers. Meanwhile, South Korea (+0.86%), Hong Kong (+0.79%), and India (+1.51%) paced gainers. In Europe, markets are red across the board, perhaps in reaction to the positive tests at the White House. Among the big 3 bourses, the DAX is down 0.96%, CAC down 0.87%, and FTSE off 0.67%. These are typical for other European markets although some of the smaller markets like Russia, Sweden and Portugal are down significantly more due to their own outbreaks. As of 7:30am, US futures are following Europe. We are looking at implied gap downs of about 1.4% in the large-cap indices and 2% in the tech-heavy Nasdaq.

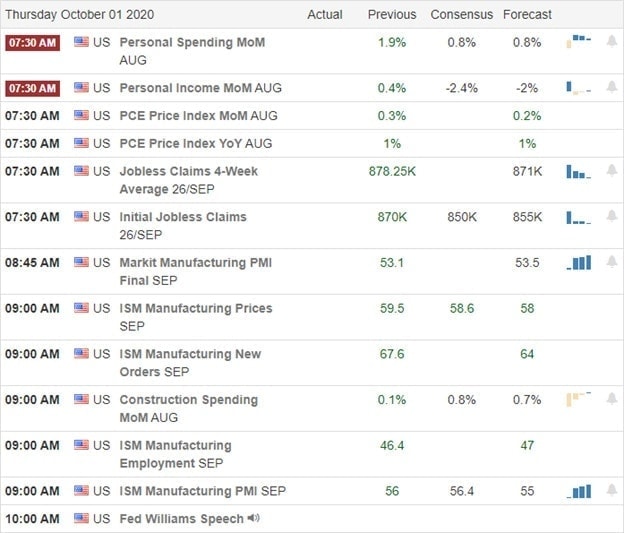

The major economic news for Friday includes Sept. Nonfarm Payrolls, Sept. Avg. Hourly Earnings, and Sept. Unemployment Rate (all at 8:30 am), Michigan Consumer Sentiment (10 am), and a Fed speaker (Harker at 9 am). There are no earnings reports scheduled for Friday.

Prior to the President’s diagnosis, the last Jobs Report before the November election was anticipated to drive markets this morning. Pre-report consensus expects the report to show a slowing, but continuing recovery of the jobs lost since March. However, now that there has been a Covid-19 positive, the news cycles and market mindshare are likely to be dominated by that and whether the White House adheres to CDC guidelines on the quarantine and post-positive precautions. That said, the market is prone to over-reaction followed by snap-backs, has a short attention span, and historically-speaking no person (including the President) has tended to have long-term impacts on the market.

After Thursday’s “gap and indecision,” we would normally like to see which way the market breaks. Today’s situation makes that less of a chart-based follow-up. So, be cautious, small, and quick in your trading until we get a read on the trend. Stick to your discipline. Don’t try to predict, chase moves that got away, or abandon your trade plans. Follow the trend and keep locking in profits and reducing risk. Also, regardless of theWhite House situation, today is Friday. So consider whether you want to lighten up over the long news cycle. Among the things we don’t know are what will happen on last-ditch stimulus talks (even though the Senate already left town for a long weekend) and how the situation may impact the President’s tweeting. He may have more time for it now, which is just to say it is an unknown and potential for more market-moving “news.”

Ed

There are no trade ideas today. Members can come to the trading room to see what we look at once things settle, but its too volatile to plan trades in front of the initial over reaction and snap back. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Stimulus hopes created a big short squeeze rally, but the uncertainty yesterday afternoon made tremendous price volatility as market sentiment swung violently. Renewed hopes once again have US Futures pointing to a big emotional morning gap, but traders will have to be on guard for more wild price swings driven by political news sensitivity. Adding to the potential volatility is a big day of economic reports that can potentially move the market substantially.

Asian markets had a rough overnight session with the NIKKEI closed due to an electronic system failure. European markets are cautiously bullish this morning as they track developments on the US stimulus package. Ahead of a busy economic calendar, US Futures point to Dow gap up as traders speculate on a stimulus agreement. It could be a wild ride today so stay focused and flexible.

Economic Calendar

Earnings Calendar

On the Thursday earnings calendar, we have another light day with just 9-confirmed reports. Notable reports include CAG, PEP, STZ & BBBY.

News and Technicals’

Hopes of a new stimulus bill and some end of quarter window dressing fueled a substantial short squeeze yesterday. Unfortunately, the day ended with tremendous price volatility when the House delayed the vote on the 2.4 trillion dollar plan. The President has extended an offer for 1.2 trillion, so the standoff continues today. Airlines are moving forward to Furlow around 38,000 employees today, saying they will reverse the decision if another 20 billion in bailout funds, that’s part of the stimulus plan, is approved. The Senate passed, and the President signed a spending bill after funding briefly lapsed, avoiding a government shutdown. Asian markets had a tough night with trading suspended for a full session due to a failure in the Tokyo fully electronic system. Apparently, the backup system all failed as well.

With some hope renewed on a stimulus bill, US Futures point to another big gap-up open this morning. Traders will have to stay on their toes as any news coming out the Washington spin cycle could crate quick price reversals should congress fail. The big move yesterday improved the technicals of the index charts pushing the DIA and SPY above their 50-day averages and increased the risk due to the substantial political uncertainty. Facing another big day of economic reports, prepare for anything as this wild rollercoaster ride continues.

After the severe disappointment of the Presidential debate and in the face of a bad GDP number, the bulls stood strong, gapping prices slightly higher on hope for a new stimulus deal. However, later reports of more failure on that front led to a selloff, only to again bounce as the bulls refused to give up. At the end of the day the 3 major indices were left with large upper wicks with the SPY having failed another test of the 50sma. On the day the DIA gained 1.20%, SPY gained 0.83%, and QQQ gained 0.68%. Given the debate fiasco, that was not too bad at all. The VXX was flat at 24.86 and T2122 remained in mid-range at 54.74. 10-year bond yields rose to 0.686% and Oil (WTI) rose to $39.90/barrel. This all closed out a down month for September and brought the quarter to an end.

Prior to the open, both Speaker of the House Pelosi and Treasury Sec. Mnuchin had said they were hopeful for a deal on another round of stimulus. However, then mid-day Senate Majority Leader McConnell came out to say the two sides were far apart. At day end Mnuchin said “they had made a lot of progress, but have no agreement” and that they would try again on Thursday. For their part, House Democrats gave more time for progress, delaying a vote on their latest $2.2 Trillion stimulus bill. It is notable that once again another trio of FOMC speakers called for more fiscal stimulus to get the economy out of a ditch. In addition, Dallas Fed President Kaplan said interest rates near zero will be needed for as much as 3 more years until we have weathered this crisis.

After the close, ALL announced they are cutting 3,800 jobs. JPM also said they will now resume job cuts, after pausing during earlier stimulus rounds, but only announced 400 cuts for now. In addition, the Fed announced they are extending the limits on big bank dividends and stock buybacks through at least Q4 as new stress tests are kicking off. UAL and AAL moved ahead with plans cut more than 32,000 jobs as the federal bailout funding ended Wednesday night and no new money has been approved. Still, in other air industry news the FAA Chief was upbeat after flying in the BA 737 Max during the day, although he said more fixes are needed and gave no timeline for any recertification.

On the virus front, in the US, the numbers show we now have 7,450,637 confirmed cases and 211,778 deaths. The 7-day average daily new case count is back up to 42,686, while the 7-day average of deaths is now 731. MRNA said Wednesday that they do not expect to apply for an emergency use authorization for their vaccine candidate prior to the election. They said the soonest they would have enough safety data would be November 25. Meanwhile the AZN trial in the US is still on hold with FDA Chief Hahn refusing to say why, noting the reason is confidential. However, in better news New York City, indoor dining is being allowed to resume at 25% capacity today.

Globally, the numbers rose to 34,201,965 confirmed cases and the confirmed deaths are now at 1,019,580 deaths. (An increase of about 315,000 cases and 6,200 deaths.) Israel reported a record number of new cases, despite its recently-invoked second lockdown. Spain announced new restrictions, reducing retail business capacities and outlawing gatherings of more than 6 people. A large study in India (3 million subjects) has found that super-spreaders are a serious problem with 8% of the infected responsible for 60% of new cases. The study also found that while children are spreaders, it is primarily among their age group and the much bigger threat of spread comes from people in their late teens and 20s.

Overnight, Asian markets were mostly green on mixed moves. Australia (+0.98%) and South Korea (+0.86%) led the major markets, while only Shanghai (-0.20%) and Malaysia (-0.53%) showed in the red. In Europe, we see a very similar story so far today with a lot of green, but uneven moves. The FTSE (+0.82%) and CAC (+0.84%) are up nicely, but the DAX (+0.29%) has more modest gains. As of 7:30am, US futures are following Europe and are pointing to significant gaps higher. The QQQ is leading the way (implied +1.29% open), with both large-cap indices pointing toward a 0.80% gap up.

The major economic news for Thursday includes August PCE Index, August Personal Spending, and Weekly Jobless Claims (all at 8:30 am), Sept. Mfg. PMI (9:45 am), Sept. ISM Mfg. PMI and Sept. ISM Mfg. Employment (both at 10 am) and another trio of Fed speakers (Harker at 9:30 am, Williams at 11 am), and Bowman at 3 pm). Major earnings reports on the day include BBBY, CAG, STZ, and PEP before the open. There are no major reports after the close.

Hope for a stimulus deal and good earnings reports from BBBY and PEP have the bulls charged up again this morning. However, considerable resistance levels remain overhead…and there is no deal in hand yet. So, be careful expecting politicians to do as you want or as they should. Again, we still do not have a bullish trend, but the bearish trend has been broken. All we know for sure is that volatility and a lack of deliberate tradings remains the norm.

As we start a new month and quarter, markets may be trying to turn the page after a down September by getting off to a fast start. Just don’t let market enthusiasm overtake your discipline or rational thought. Don’t try to predict, chase moves that got away, or break your trading rules. Follow the trend and keep locking in profits and reducing risk. Say it with me…singles and doubles are the keys to success not swinging for the fence. Welcome to October.

Ed

Swing Trade Ideas for your Consideration and Watchlist: DHI, SPCE, ETSY, QCOM, AAPL, INTC, LEN. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Heading into a big data deluge for the next 3-days the last thing we need was to hear was 28,000 job losses at Disney, 9000 from Shell that will add to the 10’s of thousands of airline workers that could lose their jobs tomorrow if billions in bail money is not approved in the next 24 hours. Expect the considerable price volatility and investor uncertainty to remain with us for the rest of the week if not through the election. As far as the debate goes, all we confirmed is the embarrassing behavior of our leaders.

Asian markets closed mixed but mostly lower overnight, and European markets trade cautiously bearish this morning with modest losses across the board. US Futures have bounced off overnight lows ahead of economic data and a very light day of earnings reports. Stay focused as we test resistance in the indexes as downtrends remain intact.

Economic Calendar

Earnings Calendar

On the hump day earnings calendar, we have a light day with just six companies expected to report. The only notable report is the gold miner NG.

News & Technicals’

As we head into October, the market focus will turn toward job numbers over the next 3-days. After the bell yesterday, Disney announced a layoff of 28,000 employees. Unless airlines receive billions in bailout money in the next 24 hours, 10’s of thousands of airline employees join the unemployment line. Adding insult to injury, Shell also announced 9000 job cuts as the oil sector continues to suffer impacts from coronavirus. US Futures remained bullish during most fo the Presidential debate, but after it ended, they began to sell-off. I’m not sure we learned anything in the argument that the market didn’t already know but rather sold off merely from the embarrassment of it all. Today before the bell, we will get a jobs reading from the ADP, a GDP report that’s likely to remain to be quite ugly, PMI, Pending Home Sales, and the Petroleum Status numbers. That said, expect more volatility and uncertainty heading into the close with another busy economic calander of market-moving reports on Thursday.

Yesterday’s price action seemed to reflect the uncertainty of the debate and the data deluge ahead, chopping in a rage with equally matched bulls and bears. The DIA, SPY, and IWM remain in downtrends while the QQQ tries to lead the market higher, holding on to its 50-day average by the close. However, with so much data coming our way, anything is possible, so stay focused and flexible.

Markets did very little Tuesday, perhaps waiting on either the Presidential Debate or on a stimulus package deal. After a flat open, stocks traded flat to slightly lower on the day, printing black-body indecisive candles. The SPY and DIA both failed to break through their 50sma and the QQQ failed to break through its 20sma. On the day SPY was down 0.53%, DIA down 0.53%, and QQQ down 0.45%. The VXX was down a bit to 24.91 and T2122 fell back to mid-range at 45.12. 10-year bond yields fell to 0.65% and Oil (WTI) dropped almost 4% to $38.99.

House Democrats unveiled their $2.2 Trillion ($200 billion less than expected) stimulus plan early in the day as talks resumed between Treasury Sec. Mnuchin and Speaker Pelosi. The Tuesday session was simply to outline the new Democrat proposal specifics with actual negotiation talks scheduled to resume Wednesday. In related news, AAL unions and company officials said up to 19,000 employees will lose their jobs this week unless a deal is reached to support the airline industry.

After the close, DIS announced it will lay off 28,000 employees across its Theme Parks and Consumer Products divisions. UNH also announced the purchase of an AMZN prescription mail-order service called DivvyDose. GOOG has made a fresh round of concessions on data gathering as well as allowing third-party wearable device makers to work with Fitbit. The concessions are likely to earn it the EU approval for its $2.1 billion purchase of Fitbit.

On the virus front, in the US, the numbers show we now have 7,406,729 confirmed cases and 210,797 deaths. The 7-day average daily new case count is back up to 42,804, while the 7-day average of deaths is now 755. New York City spiked to over a 3% positive test rate on Tuesday for the first time in months. The city may reintroduce restrictions as soon as today with the possibility of closing schools again next week if the rate does not fall. This comes as Bloomberg reports a 40% increase in bankruptcy filings in the city compared to 2019. In good news, REGN announced after the close that its 2-drug cocktail therapy for Covid-19 has shown to reduce the length symptoms in 275 non-hospitalized virus patients, with serious side-effects in just 2 patients in early testing. At nearly the same time, MRNA also released its Phase 1 vaccine trial (done in April) findings of an “acceptable safety” level, with only moderate side effects found among the 40 study participants.

Globally, the numbers rose to 33,879,038 confirmed cases and the confirmed deaths passed a grim milestone, now at 1,013,241 deaths. Amidst surging R-naught numbers, the Dutch government tightened restrictions Tuesday, reducing restaurant/bar hours, reducing permissible visitors to homes, reducing maximum gathering sizes to 4, and reducing room occupancy to 30. In Germany, Chancellor Merkel vowed to avoid another full lockdown by using immediate local and regional quarantines as soon as a flare-up is detected. This all said, France and Spain still report double the new cases daily of the UK, which itself reports triple the number of the next closest country. So, the immediate new surge seems far worse in the South of Europe.

Overnight, Asian markets were mixed again, but lean to the red. Australia (-2.29%), Thailand (-1.61%), and Japan (-1.5%) pace the losers. Meanwhile, South Korea (+0.86%) and Hong Kong (+0.79%) are the only significant gainers. In Europe the losses are much more widespread so far today. The only green is in Portugal and Greece, but it should also be said that losses are moderate so far. The CAC is down 0.44%, the DAX down 0.42%, and the FTSE down only 0.10%. At 7:30am, US futures are all just on the red side, pointing to a gap down of about half a percent. However, GDP numbers at 8:30 am may greatly influence the open.

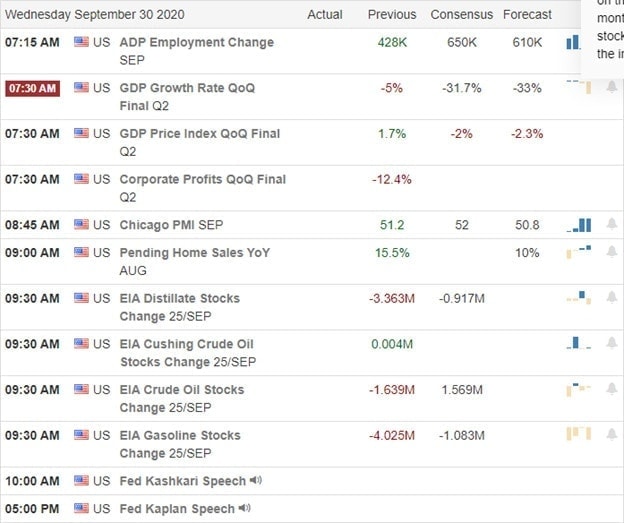

The major economic news for Wednesday includes ADP Nonfarm Employment (8:15 am), Q2 GDP (8:30 am), Sept. Chicago PMI (9:45 am), Au. Pending Home Sales (10 am), Crude Oil Inventories (10:30 am), and 3 more Fed speakers (Kashkari at 11 am, Bowman at 1:40 pm, and Kaplan at 6 pm). There are no major earnings reports on the day Wednesday.

Resistance held Tuesday as markets seemed to have been waiting on the debate. The futures this morning appear to signal that they didn’t hear anything they loved. So, we are left waiting on more news (GDP or a stimulus deal) to push the markets one way or the other. The only thing we know for sure is that we do not yet have a bullish trend, but the September downtrend has been broken as volatility continues.

With this being month-end, it is possible we see some window dressing today, although they certainly didn’t start that process yesterday. Don’t try to predict or guess the direction. Mr. Market has a way of making forecasters sorry they played that game. Either sit on the sidelines or be small and quick in your trading, looking for a trend in a smaller timeframe chart. If you do trade, stick to your rules, follow the trend, and don’t chase moves you have missed. Keep locking-in those profits, because singles and doubles are the keys to success.

Ed

Swing Trade Ideas for your Consideration and Watchlist: TGT, NUAN, BYND, CARR, TWTR, SNAP, PENN. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Yesterday’s rally was a tremendous relief from the selling pressure, but with the indexes thrusting up into price resistance levels all in one move, it also creates a tough decision for traders. Do you buy with the fear fo missing out at the price resistance where a reversal back down could occur, or do you wait for a lower risk entry? Tough decisions with a big week of economic data, coronavirus concerns, and massive political dramas on several fronts adding a hefty dose of uncertainty to the mix. Choose carefully because the next big swing could occur at any time.

Asian markets closed the day mixed but modestly higher in a choppy session, reflecting the uncertainty ahead. European markets after a big relief rally yesterday are in pulling back with Brexit issues and US politics, creating a bit of caution. US futures pulled back from evening highs, shifting slightly negative, but as we approach the open, they have become quite choppy ahead a light day of earnings reports and economic data.

Economic Calendar

Earnings Calendar

On the Tuesday earnings calendar, we have a light day with just 11 companies reporting quarterly reports. Notable reports include INFO, MKC & MU.

News and Technicals’

I’m running behind this morning, so this will be a short and sweet report. Yesterday was a nice rally, but unfortunitually, it didn’t change the technicals of the index charts. Pushing back into downtrends and price resistance can easily make us feel as if we’re missing out, and we make the mistake of buying at price resistance and breaking our trading plan rules. Though this could be the beginning of a rally that will extend higher, it could also be nearing the high point or failure point to continue the existing downtrend. Big tech seems to have the best chance of leading us higher, but the high price volatility, morning gaps, and overnight reversals require us to have a higher tolerance for risk.

The T2122 indicator went from oversold to nearly overbought in one fell swoop, and one has to consider the possibility that a similar reversal back down is equally possible. That creates a significant conflict in a trader between the fear of missing out and large potential losses that can quickly occur with such high volatility. The only way I know to resolve that conflict is to stick to your plan and follow your rules. Remember, your plan helps you make money; your plan helps you protect your capital. We have a lot of data coming our way in the next few trading days, so plan your risk carefully and expect the wild price volatility to continue for the foreseeable future.

Monday saw a gap up open following upbeat remarks from Speaker of the House Pelosi as she was scheduled to speak to Treasury Sec. Mnuchin again during the day to renew negotiations on stimulus. However, after the gap-up, both large-cap indices held in a tight range right at their 50-sma resistance level printing indecisive Spinning Top type candles. Meanwhile, the tech-heavy QQQ gapped up even further and printed a much wider range, ending up at the highs of the day in a potential Hanging Man type candle. On the day, the QQQ was up 2.08%, SPY up 1.68%, and DIA up 1.56%. The VXX was flat at 25.41 and T2122 jumped clear up into the overbought territory at 82.26. 10-year bond yields were flat at 0.661% and Oil (WTI) was up a bit to $40.59/barrel.

In an interesting twist to the tech industry, GOOG announced Monday that starting in a year, all app-makers who distribute through their Google Play Store will be forced to use the GOOG billing system and pay GOOG a 30% fee off the top. This falls in-line with the current AAPL policies regarding their app store, which they are being sued over by game-maker Epic Games, MTCH, and SPOT over supposed better deals that AAPL gives Netflix.

UAL pilots approved a pay cut to avoid furloughs of nearly 3,000 pilots through at least June 2021. The 3,000 were set to be laid off on October 1st prior to the announced deal. However, the airline is still planning to cut 13,000 jobs next month.

On the virus front, in the US, the numbers show we now have 7,361,889 confirmed cases and 209,815 deaths. The 7-day average daily new case count is now at 41,604, while the 7-day average of deaths is now 755. Dr. Fauci (NIH) said Monday that he is worried about where the US is in terms of daily case count as we enter the Fall/Winter flu season. This comes as 33 states report rising new case counts (especially Midwest and Western states). Both Fauci and CDC Dir. Redfield also added their concern that the President is being misinformed by new Task Force Member Atlas (a mask detractor and proponent of herd immunity) added to the Task force after being found to align with the President’s views. All this comes as VP Pence told a presser that Americans should expect a rise in cases soon based on the worrying testing trends. Nonetheless, in Chicago Mayor Lightfoot further eased restrictions in the city Monday.

Globally, the numbers rose to 33,585,721 confirmed cases and the confirmed deaths passed a grim milestone, now at 1,007,196 deaths. The WHO said Monday that the global Covid-19 death count is likely an underestimate. This comes on top of a Journal of Amer. Medial Assn. (JAMA) study that found the US death count is undercounted by as much as 28%. In Canada, the 2 largest provinces are applying broad restrictions as cases jumped 71% since August. In Europe, the EU added 4 more countries to the red list (increased cases) including Netherlands, Denmark, Iceland and Hungary. (Spain, France, Czech Republic, and Luxembourg were already listed). At the same time German Chancellor Merkel is meeting with the leaders of Germany’s 16 states to discuss introducing tougher restrictions.

Overnight, Asian markets were mixed again, but closer to flat. Shenzhen and South Korea paced the gainers while Hong Kong and most of the smaller economies all came in at half a percent to one percent loss. In Europe markets are leaning to the down side, but the worst of these moves is just over a half percent loss. Among the 3 major bourses, CAC is flat, DAX down 0.31%, and FTSE down 0.25%. At 7:30am, US futures are all just on the red side of flat

The major economic news for Tuesday includes August Trade Balance and August Retail Inventories (both at 8:30 am), Conf. Board Consumer Confidence (10 am), and 5 different Fed speakers (Williams at 9:15 am, Harker at 9:30 am, Clarida at 11:40 am, Quarles at 1 pm, and William again at 1 pm). Major earnings reports are limited to INFO and MKC before the open and MU and SNX after the close.

Markets may press pause today as they wait on the outcome of the first Presidential Debate tonight. The bulls have strung together a couple of consecutive nice days, but we still sit at resistance after a pullback of the last four weeks. This is still a volatile market with quarter-end in a couple of days. Don’t try to predict. Either sit on the sidelines or be small and quick in your trading. If you do trade, stick to your rules, follow the trend, and don’t chase moves you have missed. Keep locking-in those profits, because singles and doubles are the keys to success.

Ed

Swing Trade Ideas for your Consideration and Watchlist: LB, ETSY, QCOM, MRVL. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Last Monday, a punishing gap down for those holding long positions, so I guess its only fair to punish those who held short positions over the weekend with a massive gap up this morning. Anyone else tired of this all or nothing, whipsaw morning gap market? Sadly I suspect there is more to come this week as we face an economic calendar chalked full of market-moving events and enough political drama churning in the news to all investors on edge. If that’s not enough, let’s toss in rising pandemic numbers for an additional dose of uncertainty.

Asian markets closed mixed but mostly higher overnight following reports of US sanctions as tech tensions continue to rise between the US and China. European markets are decidedly bullish this morning, with HSBC bouncing more than 8% on the day. US Futures are wildly bullish this morning, suggesting a Dow gap of more than 300 points to test its 50-average as resistance. With so much data coming our way, expect another week of wild price volatility to challenge traders!

Economic Calendar

Earnings Calendar

On the Monday earnings calendar, we have 19 companies reporting quarterly results. Notable reports include CALM, SINA, THO, UNFI, & WB.

News and Technicals’

Last Monday, the market gapped down huge, so I guess it only makes sense that the futures are pointing to a considerable gap up this morning. The President’s taxes dominate the news cycle this morning with the NYT reporting that he paid no taxes for several years due to business losses. Is should make for some great political drama in the Presidential debate scheduled for tomorrow. A federal judge has temporarily blocked the administration’s ban on new TikTok downloads form US app stores. However, the much broader ban is set to come into effect on Nov.12th was not part of the judge’s order, so expect this more turbulence with the tech tensions between the US and China. Speaker Pelosi still believes there is a chance to pass a stimulus deal, but the other side of the aisle appears much less optimistic that a compromise can be struck. Treasury yields are on the rise as signs of a worsening pandemic worldwide and hear in the US keep investors on edge as to what comes next.

Looking that futures this morning, one would guess there must have been some big news to drive such a surge upward this morning. If there is, it has escaped me! In fact, we face a very uncertain week ahead with a full economic calendar, a GDP number expected to come in pretty ugly on Wednesday, and the Employment Situation on Friday, not mention all the political drama churning up emotion as the election approaches. The bullishness this morning is nice to see but keep in mind the significant price resistance above that includes 50-day moving averages. Traders will have to stay on their toes for a possible short squeeze triggered by the morning gap or the equally likely pop and drop that could occur at resistance. Please fasten your seat belt tightly; it could be a bumpy ride ahead.

Markets gapped down slightly Friday, but after bobbing around for an hour the bulls rallied the entire rest of the day. This gave us “Morning Star Like” candle signals in all 3 of the major indices. On the day SPY was up 1.62%, DIA was up 1.34%, and QQQ was up 2.32%. However, none of the three have broken their downtrend as we saw a fourth straight week of lower closes in the SPY and DIA. The VXX fell 2.48% to 25.54 and T2122 rose to 18.84, but remains just inside the oversold territory. 10-year bond yields fell slightly to 0.656% and Oil (WTI) fell back to $40.04/barrel.

Sunday Speaker of the House Pelosi said she is making another offer to Treasury Sec. Mnuchin in their negotiations while House Democrats move ahead with plans for a new $2.4 Trillion stimulus bill. She told reporters that the new offer will be revealed shortly and that there is still a chance for a deal. However, this seems like quite a mountain to climb with the Senate and White House focused on confirming ACB to the Supreme court and both parties heavily into campaign mode (doing their best to appease the extremes of their 2 bases).

In the ongoing TikTok saga, a Federal Judge blocked President Trump’s ban on TikTok and WeChat as unconstitutional Sunday evening. However, the judge did not block a broader set of restriction set to go into place November 12 that might effectively make TikTok unusable in the US anyway. Beyond the legal finding, the two sides to the deal (ORCL – WMT) and Byte Dance continue to argue over the terms of the deal, including ORCL claiming Byte Dance will retain no ownership of the new company, while all along it has been reported Byte Dance would retain 80% ownership.

On the virus front, in the US, the numbers show we now have 7,321,465 confirmed cases and 209,454 deaths. As usual, the weekend new case counts were down after seeing 55,000 on Friday. The 7-day average daily new case count is now at 41,461. Deaths came back atypically low at 276 while the 7-day average number is now 759. All this comes as FL Gov. Desantis did his Florida Man impression by completely opening the state and dropping restrictions.

Globally, the numbers rose to 33,342,965 confirmed cases and the confirmed deaths passed a grim milestone, now at 1,002,985 deaths. In the UK, one of the government science advisors has told the press he supports a repeated “mini-lockdown” (14-day) approach as a way to reduce case growth as the UK saw a 60% increase in cases in the last week. In France, intensive care admissions have more than tripled in the Southern region of the country. Down under in Australia, an inquiry has found that a “quarantine hotel” failed to do the isolation demanded in May (visitors, including sex workers, having been allowed into the hostel), which led to over 18,000 infections and over 750 deaths in the state of Victoria.

Overnight, Asian markets were mixed, but leaned to the green side. Japan (+1.32%), South Korea (+1.29%), and Taiwan (+1.88%) paced the gainers. China, Indonesia, and Australia led the losers. However, in Europe stocks are strongly in the green across the board so far today. The DAX is up 2.61%, CAC up 1.94%, and FTSE up 1.32%. At 7:30am, US futures are also pointing to a gap higher at the open. The QQQ is pointing to a 1.70% gap up, and both large cap indices are implying a 1.31% gap up as markets look to rebound after four straight down weeks and Quarter-end coming in a few days.

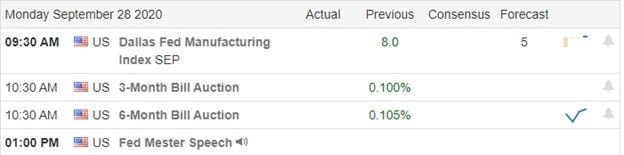

The only economic news of note for Monday is a Fed speaker (Mester at 2 pm). The only major earnings reports on the day are THO before the open and UNFI after the close.

The bulls are looking to rally at the open. This could be a response to the oversold conditions after 4 down weeks. Or it might be an attempt at quarter-end window-dressing. In either case, be wary of chasing gaps against the trend. All we can do is either sit on the sidelines or be very careful and quick in this market. If you do trade, stick to your rules, follow the trend, and don’t chase moves you have missed. Keep locking-in profits, because it’s the singles and doubles that add up to championships, not the occasional home runs.

Ed

Swing Trade Ideas for your Consideration and Watchlist: SRNE, PINS, FSLY, GAME. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service