The disappointing retail number energized the bears just enough to fill Monday’s vaccine news-driven gap. However, the bulls quickly went back to work as the push for the 30,000 Dow target resumes. We’re not going to allow the details of a suffering economy, unemployment, or a new record daily pandemic death rate deter the bulls from this mission. With the holiday shutdown just around the corner, they will have to work quickly; as volume begins to decline and trading floors start to clear.

Asian markets closed the day mixed but mostly higher as Japan’s autos slip and the dollar weakens. European markets trade with modest gains across the board this morning, extending the vaccine rally. The U.S. futures point to a bullish open ahead of earnings and a possible market-moving housing starts number.

Economic Calendar

Earnings Calendar

On the hump day earnings calendar, we have over 30 companies reporting quarterly results. Notable reports include BILI, CPRT, JACK, LB, LOW, NUAN, NVDA, SCVL, TGT, TJX, & ZTO.

News & Technical’s

It would appear that the surge in pandemic infections has already started to affect retail sales rising just .3% last month vs. the 1.6% gain last month. However, after a sharp but brief selloff to fill the Monday gap, bulls went back to work defending the lows trying to get back on track toward a 30,000 Dow. According to Johns Hopkins numbers, the U.S. set a new national record daily for pandemic deaths toping 1700. Emergency approval of the first home-based Covid test costing $50 will now be made available, a good sign considering the new public restrictions states have begun to enforce. You may soon see the Boeing 737 Max that has been grounded for nearly 2-years back in the sky with the expected approval by the FAA later today. ON the earings retail front, LOW earnings fall short of expectations, and the stock is indicated to decline more than 7% at the open. On the other have TGT topped expectations surging nearly 2.5% in premarket trading.

Filling the Monday gap and seeing the bulls work hard to defend its price support is a sign institutions will continue to push for the 30,000 Dow target. I suspect we will see this target reached before we take a break for Thanksgiving, even though indicators continue to suggest an extreme short-term overbought condition. Pandemic numbers don’t seem to matter, and disappointing retail results won’t stand in the way. Remember to consider your risk as we quickly approach the holiday when volume typically declines sharply.

Markets gapped down at the open Tuesday and then printed indecisive candles in all 3 major indices. The large-caps both printed white Doji type candles while the QQQ printed a black Spinning Top type candle. On the day, QQQ fell 0.32%, SPY fell 0.54% and DIA fell 0.56%. The VXX also fell a percent to 18.30 and T2122 dropped just a touch, but remains deep in overbought territory at 97.05. 10-year bond yields fell to 0.87% and Oil (WTI) was flat at $41.36/barrel.

A couple days after MRNA reported initial efficacy of 94.5% for their vaccine (95 test subjects), PFE and BNTX announced that additional analysis has shown their vaccine is 95% effective (170 test subjects) and they now have enough safety data to file for an emergency use waiver from the FDA within days. They report that there were 8 infections among those who got the vaccine (versus 162 among those who got a placebo) after 2 doses. So far, no “serious” safety concerns have been reported two months after the first administration. (There were 2% of recipients who had severe reactions to the first dose and just under 4% who reported fatigue after the first and/or second dose. However, those were not deemed major safety concerns. The typical 2-year study of long-term safety effects will be waived given the 1.3 million people who have already died from the virus worldwide.) This news is likely to buoy PFE, BTNX, MRNA (because they have the same class of vaccine), and the market as a whole (including Oil).

TGT crushed estimates in its early morning report. LOW came in short of estimates. BA is set to jump on both vaccine news and a Reuters report that the FAA has recertified the 737 Max to fly in the US again (after a 20-month grounding).

On the virus front, the US saw another 157,000+ cases and over 1,600 deaths on Tuesday. This surge has raised the US totals to 11,697,469 confirmed cases and 254,291 deaths. The 7-day average of new cases to 160,172 while the average deaths rose to 1,188/day. Again Tuesday, we saw new restrictions, partial lockdowns, and Governors/Municipalities begging people to take mitigation measures (wear masks, distance, and avoid gatherings, especially indoors) across the country. The FDA also approved the first self-test for home use from unlisted company Lucira.

Globally, the numbers rose to 56,069,908 confirmed cases and the confirmed deaths are now at 1,346,103 deaths. Asia is starting to see another surge as even Japan and South Korea are seeing record numbers of cases the last week. Southern Australia is locking down again (6 days this time) after a new cluster has been seen. In China, the government declared they have found their own vaccine is safe and effective. The difference of the Chinese vaccine versus the two in the US is that the Chinese version only requires standard refrigeration and is shelf-stable for up to 3 years. However, the numbers from their study were not provided and the study hasn’t yet been peer-reviewed. In Europe, there are first signs that the lockdowns started a couple of weeks ago are helping to plateau new case counts.

Overnight, Asian markets were mixed again, but leaned to the green side. Japan (-1.11%) led the few losers, while Taiwan (+1.33%) and Thailand (+1.09%) led gainers. So far today we see a modest green move across the board in Europe. The FTSE (+0.29%), DAX (+0.32%), and CAC (+0.50%) are typical of European bourses as of mid-day. As of 7:30 am, US futures are pointing to a modest green open. The DIA is implying a 0.47% gap up, the SPY implying a 0.35% gap, and the QQQ implying a 0.17% modest gain at the open.

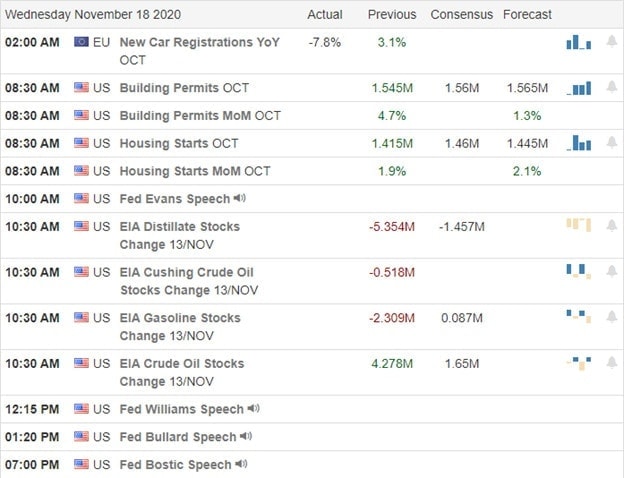

The major economic news for Wednesday includes Oct. Building Permits and Oct. Housing Starts (both at 8:30 am), Crude Oil Inventories (10:30 am), and 3 Fed Speakers (Williams at 12:15 pm, Bullard at 1:20 pm, and Bostic at 5 pm). Major earnings reports on the day include AVYA, LOW, TGT, and TJX before the open. After the close, KEYS, LB, NVDA, and UGI report.

The bulls are likely to run today on positive vaccine news. However, don’t get caught up in FOMO. Remember that price moves in a zig-zag pattern. So, don’t be the last one buying the zig unless you can handle the zag to come. Focus on discipline, taking profits (goals/targets) on the way, and work your trade plan. Consistency trumps the occasional homerun every time. Stick to the trading rules you have built, follow the trend, and respect support and resistance. Good trading!

Ed

Swing Trade Ideas for your consideration and watchlist: ICPT, WLL, DKNG, GTHX, MUR, DVAX, OXY, CPE, WFC, APA, OKE. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The vaccine news-driven rally pushed the DJ-30 to a new record high and finished the day within striking distance of 30,000. As the bulls try to price in a pandemic recovery, 22 states have added restrictions that could have significant business impacts ahead, as infection rates continue to surge throughout the country. While I believe the institutions will not miss out on achieving a Dow 30,000 headline, the path may be challenging in this very news-driven extended market environment. Plan carefully.

Asian markets closed overnight with modest gains after an initial jump higher in reaction to vaccine news. European markets are currently edging lower this morning, and the U.S futures point to a lower open ahead of several potentially market-moving economic reports. The wild price volatility is likely to continue as investors grapple with holiday restrictions and shutdowns.

Economic Calendar

Earnings Calendar

We have more than 30 companies stepping up to report quarterly results this Tuesday. Notable reports include NIO, HD, WMT, KSS, LZB & SE.

News & Technicals’

The Dow hit new record highs yesterday, rallying 470 points hopeful vaccine news closing the day just 50 points below 30,000. Unfortunately, at the same time, the pandemic surge has inspired 22 to add new restrictions likely to impact the overall economy. While the bulls try to price the market for the hopeful better days ahead, the short-term impacts could be challenging to grapple with, keeping the price action volatile. Tesla shares jump in aftermarket trading after its addition to the S&P 500 average. Shared of Home Depot are dipping this morning despite a strong earnings report. Amason Pharmacy has launched, allowing its customers to order prescriptions online. Shares of AMZN are modestly higher on the news. Futures currently indicate a lower open ahead of several potential market-moving economic reports. With the Dow so close to 30,000, it hard to imagine the institutions will miss the opportunity to claim that headline. I’m guessing the hats are already on the floor of the exchanges, just waiting for the photo opportunity. Of course, pandemic, political, and economic news could make it a challenging and choppy process.

Technically speaking, there really is not much to say except the bulls are in control, and the indexes appear extremely extended in the short-term. While I believe the institutions will not miss the opportunity to test 30,000 the path, there may not be a straight one. Odds of fast intraday whipsaw and full overnight reversals remain high in this very emotionally charged market. Plan your risk carefully and guard yourself against chasing into already extended stocks.

Large-caps gapped higher Monday on the news of the MRNA vaccine 94% (first look) effectiveness report. After early follow-through, that market vacillated the rest of the day except for a strong surge the last 5 minutes. As a result, both large caps printed white Hammer type candles and the QQQ printed a large-body white candle. On the day, DIA was up 1.67%, SPY up 1.25%, and QQQ up 0.78%. The VXX lost another 2% to 18.65 and T2122 rose to extremely overbought at 99.03. 10-year bond yields rose again to 0.909% and Oil (WTI) was up over 3% to $41.44/barrel.

After the close Monday it was announced that TSLA will be joining the S&P500 in December. The CEOs of both FB and TWTR will face Senate Republicans on Tuesday in a session that will likely focus on perceived “silencing conservatives.” However, they may not get any quarter from the Democrats, who are likely to hammer them over not being more restrictive on lies and misinformation

On the virus front, the spread continues unchecked. This surge has raised the US totals to 11,540,461 confirmed cases and 252,684 deaths. The 7-day average of new cases to 158,363 while the average number of deaths rose to 1,170/day. Meanwhile, hospitalizations continue to rise, climbing to over 73,000 on Monday. In response, new restrictions and partial lockdowns continue from coast to coast as states continue to have to act on their own to control outbreaks.

Globally, the numbers rose to 55,466,741 confirmed cases and the confirmed deaths are now at 1,334,671 deaths. New restrictions and lockdowns are taking place in Europe as well, even as countries that locked down a couple weeks ago (such as Germany) are starting to report progress in getting new case numbers to plateau.

Overnight, Asian markets were mixed, but leaned to the green side. Singapore (+1.11%), and India (+0.74%) led the gainers. Meanwhile, Shenzhen (-0.89%) paced the losers with other exchanges showing modest moves. In Europe, markets are mixed, but lean heavily red so far today. The FTSE (-1.12%), DAX (-0.27%), and CAC (-0.29%) are relatively typical across the continent. However, there are a couple of gainers such as Greece (+0.55%). As of 7:30am, US futures are pointing to a lower open on the large caps, with DIA implying a -0.59% and SPY implying a -0.46% open. The NASDAQ is implying a modest open to the up side at +0.25%.

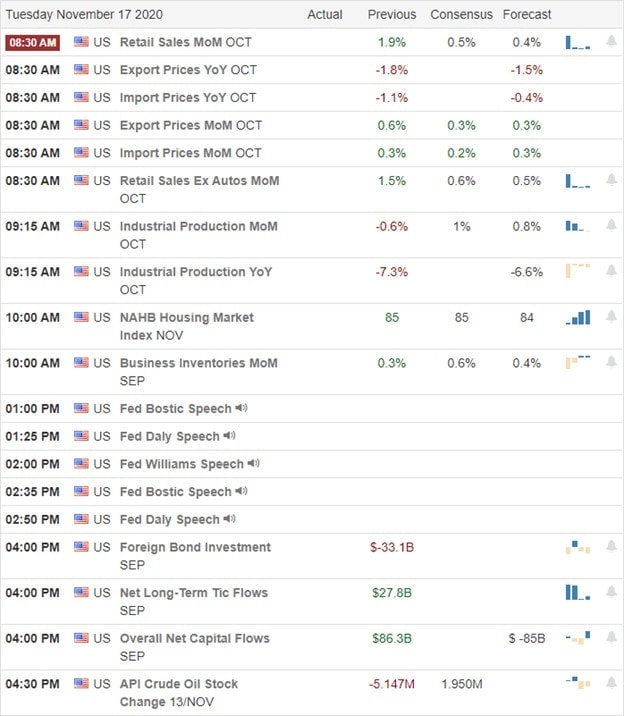

The major economic news for Tuesday includes Oct. Retail Sales, Oct. Export Price Index, and Oct. Import Price Index (all at 8:30 am), Oct. Industrial Production (9:15 am), Sept. Business Inventories (10 am), and 2 Fed Speakers (Bostic and Daily both at noon). Major earning releases include ARMK, HD, KSS, SE, and WMT before the open. There are no major earnings announcements after the close.

WMT and HD posting beats this morning is helping futures. However, the worsening virus conditions and local/state mitigation measures are sure to continue to give volatility. Big tech names may get beaten up as FB and TWTR take their turn in the shooting gallery today. So, even with positive trends and the recent good vaccine news to help bulls, be careful.

Remember that price moves in a zig-zag pattern. Don’t be the last one buying on the zig unless you can handle the zag to come. There will always be either another stock setup down the road. Keep locking in your profits, maintain your discipline, and work your trade plan. Stick to the trading rules you have built, follow the trend, and respect support and resistance. Good trading!

Ed

Swing Trade Ideas for your consideration and watchlist: ESNT, SHOO, AEO, MFC, KNSL, DAR, ERIE, WING. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The bulls are undoubtedly in charge, or could this be irrational exuberance as the DIA and IWM leap to new record highs and states impose economic restrictions on the holidays just around the corner. One thing for sure, there seems to be no shortage of traders willing to chase prices higher with little regard to risk. The T2122 indicator indicates an extreme short-term overbought condition, so stay focused on price action for any signs of a pullback. Also, keep in the possibility of overnight reversals as you plan your risk and avoid chasing stocks already extended with the fear of missing out.

Asian markets were sharply higher overnight in reaction to signing a massive trade deal with 14 Asian countries. European markets are decidedly bullish this morning as vaccine hopes continue to inspire hopes of recovery. U. S. futures continue to leap higher as the DIA and IWM look to open at new record highs while infection rates and hospitalizations notch new records as well.

Economic Calendar

Earnings Calendar

We have a rather large week of earnings kicking it off with more than 70 companies fessing up to results this Monday. Notable reports include JD, ACM, FUV, BIDU, CSPR, GAN, KRUS, PANW, SDC, SOHU, & TSN.

News & Technicals’

China and 14 other Asian-Pacific countries signed the world’s largest trade agreement over the weekend. According to analysts, economic benefits are modest and would take years to materialize. Texas and Washington set new Covid records this weekend as Midwest states as the Dakota’s and Nebraska set the largest daily increases per capita. As states across the country implement restrictions with severe potential economic impacts, the market continues to surge focused on the hopeful vaccines. Though some point to a possible bubble forming, it has done nothing to dissuade traders from buying up stocks even as P/E ratio’s swell and prices leap toward new record highs. How much longer that can continue is anyone’s guess but, it would be wise for traders to be mindful of the substantial risks with just a pullback to support.

Technically speaking, the indexes appear very extended, and the T2122 indicator is registering an extreme short-term overbought condition even as the futures point to another gap higher this morning. The DIA and IWM will break out to new record highs at the open today, with the SPY not far behind, assuming the futures hold on to the overnight bullishness. Plan your risk carefully as price volatility remains high in this wildly energetic and emotionally charged news-driven environment.

The market gapped about two-thirds of a percent higher Friday at the open. From there, we saw a sideways grind in all three major indices until an afternoon rally took off. Profit taking the last 15 minutes of the day closed markets off their highs, but it was still a white candle day in all 3 of the major indices. The QQQ printed an indecisive Spinning Top type candle while the DIA printed something that could be called a Morning Star signal if you squint. For the day QQQ closed up 0.88%, SPY up 1.38%, and DIA up 1.41%. The VXX lost 6% to close at 19.08 and T2122 (4-week New High/Low Ratio) shot up back deep into overbought territory at 94.70. 10-year bond yields rose to 0.898% and Oil (WTI) fell two and a half percent to $40.12/barrel.

Early Monday, MRNA announced that its vaccine candidate was 94% effective against Covid-19 according to the initial look at 54 cases. As has been mentioned previously, this does not speak to the safety of the vaccine and it is based on a small sample size. However, markets are likely to jump on this news at least as confirmation of the PFE vaccine news from a week or so ago. At most, this is the second source of a vaccine against the virus, but this one too requires strict extreme low-temperature storage requirements.

In other business news, on Sunday AAL announce dit is slashing the number of flights between the US and UK in December due to weak demand brought on by the virus surge in both countries. Early Monday, PNC announced it will buy the US operations of Spanish bank BBVA. This $11.6 billion deal would be the second-largest bank merger of all time.

On the virus front, the spread continues unchecked. Friday the US had the worst day of any country since the beginning of the pandemic and had a new case count (188,000) almost 2.5 times higher than our worst day during the summer surge. This raised the US totals to 11,367,214 confirmed cases and 251,901 deaths. The 7-day average of new cases to 152,136 while the average deaths rose to 1,156/day. 45 states saw an increase of more than 10% in new case counts week-to-week with 17 of those seeing an increase of more than 50% in the period. 4 states saw a small increase (up less than a 10% week-on-week) and on SC reported a reduction (but that is believed to be a reporting glitch with their state’s data). This comes as many states are enacting new lockdown and restrictions.

Globally, the numbers rose to 54,936,761 confirmed cases and the confirmed deaths are now at 1,326,265 deaths. With lockdowns in place in many parts of Europe for the last couple of weeks, there is starting to be a little better news. Germany reported last night that they are seeing the first signs of infection rates flattening. Meanwhile, the spread is picking up steam in Asia as Japan reported 3 consecutive record-high case count days,

Overnight, Asian markets were green across the board. Australian markets were paused at the open due to a data issue, but managed to recover. Taiwan (+2.10%), Japan (+2.05%), and South Korea (+1.97%) led the gainers. There were no losers although New Zealand markets were closed. In Europe, we see a very similar picture so far today. The only red is from Denmark (-0.90%), while the rest of the continent followed Asia higher. Among the 3 major bourses, FTSE is up 1.61%, DAX up 1.35%, and CAC up 2.24% as of mid-day. These are typical of the rest of the indices across Europe. As of 7:30 am, US futures are pointing to strong gaps higher in the large-caps. The DIA is implying a 1.75% gap up and the SPY is implying a 1.19% pop higher at the open. The NASDAQ is implying a flat open with the QQQ at -0.04% as of now.

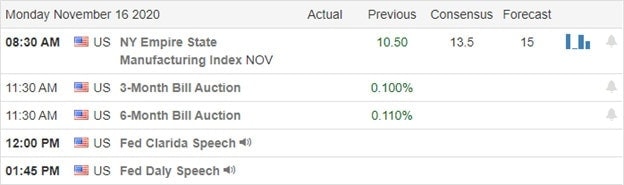

The major economic news for Monday is limited to Nov. NY Empire State Mfg. Index (8:30 am) and 2 Fed Speakers (Daily at 1:45pm and Clarida at 2 pm). Major earning releases include ACM, JD, PANW, and TSN before the open. After the close, BIDU, IQ, and BEKE report.

The MRNA vaccine news was expected, but very welcome nonetheless. Futures show we are going to get a pop out of the news and maybe a resumption of rotations out of the lockdown tech names. Remember not to chase the moves that you have missed. Fear of missing out can be deadly for a trading account. Keep in mind that the market moves in a zig-zap pattern. Don’t be the last one buying on the zig unless you can handle the zag to come. There will always be either another stock setup down the road. So, keep locking in profits, maintain discipline, and working your plan. Stick to your trading rules, follow the trend, and respect support and resistance.

Ed

Swing Trade Ideas for your consideration and watchlist: BP, JETS, UPWK, EVRI, KO, TGI, PSX. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The bears came out to play yesterday, but fear seemed to remain in check as the selling appeared to be measured and controlled. It is very surprising with pandemic numbers on the rise and hospitalizations beginning to strain the country’s healthcare system. Jerome Powell once again called for more stimulus to combat the economic impacts, but Mitch McConnell stated and unwillingness to negotiate and larger spending plan. That said, the tenacious bulls are fighting back this morning with the futures pointing to a gap up open.

Asian markets closed the day seeing read across the board in reaction to rising infection rates. European markets opened the day lower but have rallied, holding very modest gains at the time of this report. However, here in the U.S, futures point to a 200 point Dow gap up ahead of a lighter earrings day and the pending PPI Report. The question is, will we see follow-through buyers at the open, or might this setup a pop and drop pattern heading into the uncertainty of the weekend?

Economic Calendar

Earnings Calendar

On the Friday earnings calendar, we have a lighter day of reports dominated by small-cap companies. Notable reports include DKNG, MANU, SPB, & VIPS.

News & Technicals’

The pandemic numbers brought out the bears yesterday, but the selling appeared controlled, with the VIX rising only slightly. Chicago issued a stay at home order begins on Monday except for essential needs. Mitch McConnell added pressure to the market, saying he had no interest in negotiating a larger stimulus plan. That comment came on the heals of Jerome Powell’s speech, where he said more stimulus is needed to battle the impacts of the rising pandemic numbers. The U.S. set another new record as infection numbers jumped to over 150,000, with hospitalizations up by at least 5% in 47 states. Treasury yields slumped yesterday in reaction to the rising numbers, with gold and silver rebounding slightly as a result.

After reading the paragraph above, one would expect the market would be following through with the selling that began yesterday but no, the relentless bulls are fighting back this morning. Perhaps traders are responding to the positive earnings after the bell yesterday, where DIS, AMAT, and CSCO rallied after better than expected results. This morning’s question yet to be answered, will the gap find buyers after the open, or will we see a pop and drop heading into the uncertainty of the weekend? Remain focused and flexible, weighing the risk you carry into the weekend carefully.

The major indices gapped in a mixed manner Thursday, with large-caps both gapping down about half a percent while the QQQ gapped about a third of a percent higher. However, after the open, all three then trended lower all day on fears over the Covid-19 surge. At the end of the day, DIA closed down 1.04%, SPY down 0.97%, and QQQ down 0.47%. The VXX gained about 7% to 20.33 and T2122 fell back into the mid-range at 69.77. 10-year bond yields fell to 0.883% and Oil was off a percent to $40.69/barrel.

During the day, Fed Chair Powell and ECB President Lagarde agreed that the virus has changed the economy forever. While both expect the economy to recovery and eventually surpass the size of the pre-covid GDP. However, both say they expect it to be a different environment with automation replacing many human jobs and technology being leveraged to enabled far more virtual and distributed work. Generally speaking, they seemed to say that this pandemic has forced a dramatic increase in the pace of prior trends with technology. To them, this implies that the divergence between low-pay workers and high-pay workers will accelerate, meaning that portions of the economy dependent on low-pay workers as customers are at significant risk. At the same time, consumers will now be much more accustomed to online buying and remote service. So, retail and foot-traffic dependent businesses are all facing a different world than 12 months ago. Powell also took the chance to say the Fed will still need to do more than it already has and to lobby for more Congress and the Administration to do more fiscal stimulus.

The virus continues its wildfire surge. Thursday saw another huge spike in cases, up to a record 161,541 (a 20,000 case jump) in the US. This raised the totals to 10,873,936 confirmed cases and 248,585 deaths. The 7-day average of new cases to 135,399 while the average deaths rose to 1,086/day. During the day Thursday, Chicago issued a new stay at home order and the Mayor implored people to cancel Thanksgiving celebrations and stay locked down instead. CA also followed TX to become the second state to record over 1 million cases. Dr. Fauci (NIH) repeated his call to protect others by following guidelines, this time aiming at anti-maskers who he called “Americans with an independent spirit.”

Overnight, Asian markets were mixed, but mostly red again. Shanghai (-0.86%) led the losses, which were widespread but generally moderate. South Korea (+0.76%) and Thailand (+0.74%) led the gainers. In Europe, we see the same picture as mixed, but mostly moderately red so far today. Among the 3 major bourses, the FTSE is down 0.50%, the Dax up 0.18%, and the CAC up 0.35% at this point in their day. As of 7:45 am, US futures are also pointing to three-quarters of a percent gap higher at the open as of now.

The major economic news for Friday includes Oct. PPI (8:30 am), Michigan Consumer Sentiment (10 am), and a couple Fed Speakers (Williams at 7 am and Bullard at 8:30 am). Major earnings reports on the day are limited to SPB and VIPS before the open.

With a raging virus, very limited news, and a lack of major earnings today, expect the bears to have the edge and volatility to continue. Still, with the prospect of MRNA reporting initial effectiveness results (based on 54 patients) sometime in the next few days, the volatility could be on both sides. We need to remember that this is Friday and there is a long news cycle ahead. Don’t get caught unprepared come Monday morning.

Don’t chase the moves that you have missed. Fear of missing out (FOMO) is a deadly condition for traders. You don’t NEED to trade every day. There will always be either another stock setup down the road. So keep locking in profits, maintain your discipline, and working your plan. Stick to your trading rules, follow the trend, and respect support and resistance.

Ed

Swing Trade Ideas for your consideration and watchlist: MAC, DIS, EVRI, ROKU, XLE, KO, UPWK, GLUU. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Though considerably overextended in the short-term, the vaccine news and hopes of recovery continued to encourage the bulls as the tech sector bounced off support. Sadly, news of 144,000 new infections and possible business restrictions or lockdowns weigh heavy on this morning market. Facing a big day of data, the gap down in the Dow will challenge the support of Monday’s massive rally. Buckle up for another day of new-driven volatility.

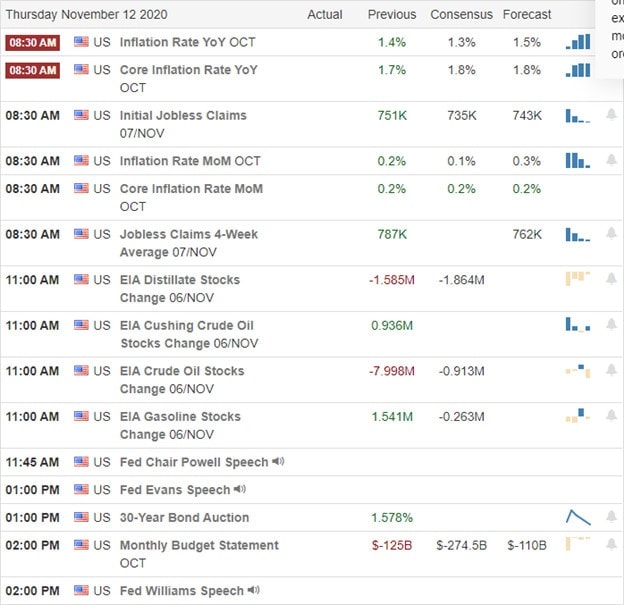

Asian markets closed mixed but mostly lower in a relatively muted day of trading. European markets have a bearish attitude this morning, with the DAX and CAC trading more than 1% lower at the time of this report. As we wait on Jobless Claims, GDP, a Powell speech, and a big round of earnings reports, futures currently point to bearish open. Of course, the news events could quickly improve or worsen the current sentiment. Stay focused.

Economic Calendar

Earnings Calendar

We have our most important day of earnings this week, with more than 150 companies fessing up to quarterly results. Notable reports include DIS, AQN, AMAT, BZH, CSCO, DGLY, DLB, ENR, FTCH, GLOB, DGRX, HIMX, JAMF, MFG, PLTR, PDD, SBH, TK, TDG, U, & WIX.

News & Technicals’

A tech bounce led the market yesterday, with the SPY and IWM struggling to find direction, while the DIA ran into a little profit-taking. As the Presidential election saga drags on, the U.S. experienced another new record in COVID infections topping 144,000. That is the 9th straight day of more than 100k new infections, Ugg. Yew York has imposed a curfew on restaurants, bars, gyms and limited home gatherings to ten. The Biden Covid advisor is suggesting a lockdown of 4 to 6 weeks to control the surging pandemic. It looks like we’re in for a long winter and a tough holiday season. President Trump continues to allege fraudulent election activity, filing multiple lawsuits and appeals even as Biden moves forward with the transition appointing his close friend as Chief of Staff. The Republican state AG says it’s highly unlikely that Trump will win in Arizona, citing no fraud evidence. Georgia will do a hand recount of election ballots, but the Biden lead continues to grow, according to reports.

Though the T2122 indicator continues to warn of an overbought condition, the tenacious bulls hold firm fending off any attempt by the bears. Unfortunately, worry over pandemic numbers, and the threat of more lockdowns have the futures pointing to a gap down open this morning will test the support of Monday’s massive rally. With a big day of earnings and economic reports, price volatility could be high, and news-driven whipsaws and reversals are possible. Stay focused, and flexible.

Markets gapped up Wednesday and generally ground sideways the rest of the day. The DIA ground slightly lower, the QQQ slightly higher, and the SPY almost dead sideways. On the day, DIA was flat (-0.10%), SPY up (+0.76%), and QQQ led the way (+2.24%) on a bounce-back after a couple of days of rotation out of the high-tech names. VXX fell 2% again to 19.03 and T2122 fell slightly to 88.00. 10-year bond yields rose to 0.96% and Oil (WTI) was flat at $41.52/barrel.

The only major economic or business news revolves around the virus, methods to control the pandemic or vaccine trials. If you don’t like that sort of news, this post will not please you.

The virus continues its massive surge. Wednesday saw another record 142,906 new cases and 1,479 deaths. This raised the totals to 10,708,728 confirmed cases and 247,398 deaths. The 7-day average of new cases to 129,475 while the average deaths rose to 1,080/day. In sum, hospitals nationwide are coming under strain as they now are nearing capacity. As an example, El Paso Texas has 20 mobile morgues (refrigerated semi trailers) in place as their system is overwhelmed. In addition, that city has begun looking for suitable brick-and-mortar overflow capacity such as an ice rink.

Wednesday, one of President-elect Biden’s virus advisory group said that a 4-6 week national lockdown could control the pandemic until vaccines are available and the worst of flu season is passed. Obviously, Biden would not have any authority until at least January 20 and even then there would be massive resistance from business interests and groups. For example, polls (depending on whether you believe polls) show that fewer than half of Americans would comply with another lockdown order. However, this advisor’s talking point may still throw a scare into markets now. In positive news, MRNA has reached its own first threshold of cases so that preliminary efficacy data can be released. So in the next day or so, expect another announcement like the PFE announcement last week (an initial view of the effectiveness of the MRNA vaccine.

Overnight, Asian markets were mixed, but mostly red. Japan (+0.68%) and Malasia (+1.32%) led gainers while the losses were widespread, but moderate. In Europe, we see the same picture as markets are mostly red, with a couple minor spots of green. Among the 3 major bourses, the FTSE is down 0.60%, the Dax down 0.96%, and the CAC down 1.12% at this point in their day. As of 7:45 am, US futures are also pointing to small gaps at the open. The DIA is implying a -0.60% loss, the SPY implying a 0.32% loss, and the QQQ implying a +0.18% gain at the open as of now.

The major economic news for Thursday is limited to Oct. Core CPI and Weekly Jobless Claims (both at 8:30 am), Crude Oil Inventories (11 am), Oct. Federal Budget Balance (2 pm), and a Fed Speaker (Williams at 2 pm). Major earnings reports include ENR, IGT, MTOR, PDD, SBH, TCEHY, and TDG before the open. Then after the close AMAT, CSCO, and DIS report.

Volatility is likely to continue. A lack of hard news is likely to be filled with speculation over the pandemic. mitigation measures, and vaccine hopes. Remember to not get caught up chasing moves that you have missed. Fear of missing out (FOMO) is a deadly condition for traders. You don’t NEED to trade every day. There will always be either another stock setup down the road. So keep locking in profits and maintain your discipline. Stick to your trading rules, follow the trend, and respect support and resistance.

Ed

Swing Trade Ideas for your consideration and watchlist: SIRI, PZZA, MRNA, INTC, GILD, CRUS, ACMR, ABT. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service