Jobless claims disappointed markets yesterday but having Congress adjourn for the weekend without reaching a stimulus deal appears to be the more significant disappointment this morning. The Whitehouse’s legal battle could also create considerable volatility in the days ahead, depending on how or if the Supreme Court gets involved. The market hates uncertainty, and as we slide into this weekend, considering this historic rally, traders have some tough decisions to make. Capture gains or wait, holding on to hopes for the week ahead. What’s your choice?

Asian markets finished the week with mixed results, but European markets see red across the board as Brexit, and the U.S. stimulus battle continues. The U.S. futures market point to a bearish open that could test index trend supports as traders grapple with the weekend’s uncertainty. It’s been a while since the bears showed much of a willingness to fight but never forget they can attack anytime, so have a plan to protect your capital should they decide to show some teeth.

Economic Calendar

Earnings Calendar

Although we have some very small-cap companies, Friday is a light day of quarterly reports. Looking through the list, I could only come up with one somewhat notable, JOUT.

News & Technicals’

An increase in unemployment has the bears stirring about yesterday, but overall the market was still hoping that Congress would reach a stimulus deal. Instead, Congress passed a single week stopgap spending bill avoiding a government shutdown and then adjourned for the weekend. As a result, the market is showing its disappointment, suggesting a bearish open. Prizer’s Covid vaccine took a big step forward with the FDA’s advisory committee recommendation for emergency use. Now it moves up the ladder looking for a full FDA agency approval. In a move that bucks the overall market love affair with Tesla, Jefferies downgraded the company, suggesting they don’t believe the carmaker can dominate the auto industry. Battleground states urge the Supreme Court to reject Texas efforts to overturn the election results. Seventeen states have joined with Texas setting up an interesting legal battle that could create substantial market shockwaves depending on how the battle progresses.

Although the pullback may be disappointing to many, the T2122 indicator has signaled this possibility for some time. Should the early morning bearishness hold through the open, the short-term trends will receive a test of support. If the bulls have the energy to defend, then there is no harm in taking a little break in the current rally. However, if the bears become emboldened, price support suggests that the pullback could be quite painful. Remember, the market has the propensity to throw a bit of a temper tantrum when they don’t get their stimulus fix. Stay focused and have a plan should the bears decide to show their teeth.

Markets gapped down about half a percent Thursday on a much higher than expected increase in Initial Jobless Claims (853,000 vs 730,000 expected) to a 3-month high. However, a recovery came quickly and the rest of the day was a range-bound gyration back and forth. At the end of the day, all 3 major indices printed indecisive candles (Doji, Spinning Top, and Large-wick candles). The SPY was flat at -0.03%, the DIA flat at -0.11% and the QQQ gained 0.40%. The VXX gained a percent to 17.39 and T2122 (4-week New High/Low Ratio) fell, but remains in overbought territory at 84.43. 10-year bond yields fall on stalled stimulus talks to 0.908% and Oil (WTI) gained 3% to $46.89/barrel.

Once again, the government failed to reach a deal on more stimulus as the market has been expecting. Senate Majority Leader McConnell outright rejected the bipartisan proposal which had been the basis of negotiations the last couple of weeks, instead saying that plan should be thrown out and new discussions begun around the last-minute plan from the Administration. (Business liability waivers is McConnell’s pet project and that seems to be the snag.) The Democrats felt he was just grandstanding and the change of starting point would be a waste of time. So, the House adjourned for the week (having already passed its one-week stopgap spending bill). This means there is little likelihood of any progress in talks prior to the December 18 end of funding to keep the government open.

Related to the virus itself, US infections continue to rage as the US. The totals have risen to 16,042,537 confirmed cases and 299,703 deaths. Thursday saw another day of 217,779 new cases and another grim record 2,974 new deaths (about one-third of world totals and we have only about 4% of the population). This brings the 7-day average of new cases to 212,969 while deaths are averaging deaths rose to 2,407/day. The FDA’s Vaccine Advisory Committee held a day-long public Zoom call to discuss, explain and then vote on recommending the vaccine. As expected, the vote was to recommend the PFE-BTNX be given approval for emergency use. This is not a final approval vote, but the full FDA is expected take the committee’s recommendation and quickly approve the PFE-BTNX vaccine.

Globally, the numbers rose to 70,852,192 confirmed cases and the confirmed deaths are now at 1,591,300 deaths. As a reference, the world is averaging about 625,000 new cases and almost 11,000 new deaths per day. In Europe, France has extended its lockdown until January 8th, though they are making an exception of Christmas day. Germany also reported another record number of cases and deaths Friday as their Economic Minister told reporters the country must act now to shutdown the spread before it wrecks the economy. Russia also reported a record increase in deaths, even though they are a week into mass vaccinations. AZN announced it will collaborate with the makers of the Russian vaccine for trials and GSK announced their own vaccine will be delayed until late 2021.

Overnight, Asian markets were mixed again. Malaysia (+1.82%) was a big outlier to the green side, with South Korea (+0.86%) as most green moves were very modest. On the Downside Shenzhen (-1.31%) and Shanghai (-0.77%) were the big losers. However, in Europe, markets are red across the board after the EU reached agreement on a $2.1 trillion Covid relief package. Among the 3 major bourses, FTSE is down 0.99%, DAX down 1.72%, and CAC down 1.04% so far today. As of 7:30 am, US futures are gap down to start the day. The SPY is implying a -0.72% open, the DIA implying a -0.63% open, and the QQQ implying a -0.75% open at this point in the premarket.

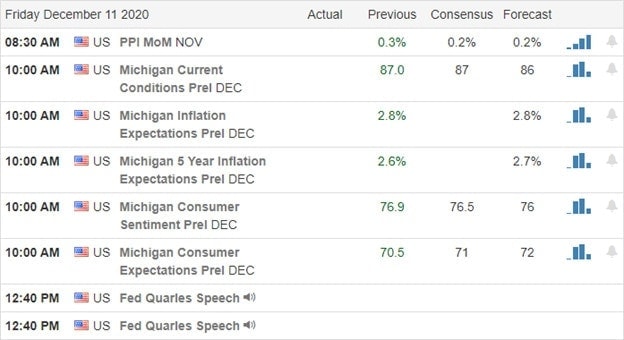

The major economic news for Friday is limited to Nov. PPI (8:30 am), Michigan Consumer Sentiment (10 am) and a Fed Speaker (Quarles at 12:40 pm). There are on major earnings reports on the day.

Once again, the virus, vaccine news, and more delays in stimulus are top of mind in the market. More bad news related to the Brexit deal has UK PM Johnson telling his country’s businesses and people to prepare for an “Australian-style” crash out of EU Trade. This while we sit near the all-time highs. So, continue to be careful and remember the market is overbought.

As always, respect support and resistance, the trend, and price action. Stay true to your trading rules and trust your process. Keep taking the singles and doubles the market offers you. Don’t try to sell every last share at the very top penny before the turn. Leave “top picking” to the traders who need their ego stroked more than they need to make money.

Ed

Swing Trade Ideas for your consideration and watchlist: STNG, MGM, HAL, JETS, UBER, NAT, ETSY. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Markets essentially opened flat Wednesday and then sold off until 2 pm, possibly on discouraging news on the stimulus front. From that point, all 3 major indices ground sideways the rest of the day. This left large black candles that created a Bearish Engulfing signal in the SPY and a Dark Cloud Cover in the DIA. On the day, the SPY fell 0.92%, the DIA fell 0.46%, and the QQQ fell 2.26%. The VXX rose 3.68% to 17.20 and T2122 fell 5% but remains in overbought territory at 89.50. 10-year bond yields rose strongly again to 0.939% and Oil (WTI) was flat at $45.62/barrel.

As mentioned, Wednesday saw more bad news related to stimulus, as the major players found another reason to stall the deal. This comes even though both sides agree on the top line numbers and most of the provisions. Rather than continue to work on wording around the bipartisan proposal (the basis of the last couple of weeks), Senate Majority Leader McConnell criticized House Speaker Pelosi for not embracing the new Administration offer. At the same time, Pelosi and Senate Minority Leader Schumer criticized the 11th-hour proposal from Treasury Sec. Mnuchin (who had been absent since before the election) and said negotiations should continue based on the bipartisan proposal. So, as always, the important thing in Washington is who gets the credit, who loses face, and who can be blamed in the next election much more than it is about the need or available resources

In other federal news, the House has approved a 1-week stop-gap spending bill to avoid a government shutdown. The extra week is intended to give more time to reach a longer-term spending agreement and the stimulus deal. The idea is that a desire to leave for the holidays and a government shutdown right before Christmas will be enough pressure on lawmakers to get a deal done. And finally, the Federal Government and dozens of State Attorneys General sued FB for anticompetitive behavior. The suit seeks to force FB to divest Instagram and WhatsApp.

Related to the virus itself, US infections continue to rage in the US. The totals have risen to 15,882,734 confirmed cases and 296,745 deaths. Wednesday saw another day of 226,762 new cases and another grim record of 3,260 new deaths (about one-third of world totals and we have only about 4% of the population). This brings the 7-day average of new cases is at 213,361 while average deaths rose to 2,400/day. The White House Task Force leader Dr. Birx told CNBC overnight that people need to adjust their expectations and that vaccines will not significantly reduce either hospitalizations or deaths until at least late spring. Until then, only behavior changes can reduce those two numbers. This came as Dr. Fauci (NIH) again pleaded for the public to avoid gatherings with people outside their immediate family this holiday season.

Globally, the numbers rose to 69,369,386 confirmed cases and the confirmed deaths are now at 1,578,356 deaths. As a reference, the world is averaging about 625,000 new cases and almost 11,000 new deaths per day. In potentially concerning news, 2 UK Health Workers have suffered severer allergic reactions after their vaccination jab. This has caused an immediate change in recommendations for who should and who should not be vaccinated. For the market, the main gist is that this may cause even more public concern and resistance to vaccination, therefore prolonging the period it will take to reach herd immunity. Beyond that, hospital beds are in short supply all around the world. For example, South Korea has begun using cots in shipping containers to supplement its shortage as they are now down to 3% of bed capacity still available for new patients.

Overnight, Asian markets were mixed but leaned to the downside. Taiwan (-0.98%) saw the worst action, but there was little green elsewhere in the region. Malaysia (+0.48%) was the best bull outlier example with most Asian exchanges moderately red. In Europe, markets are also mixed but leaning more heavily to the green side. The 3 major bourses are typical with the FTSE up 0.78%, the DAX flat at +0.09%, and the CAC up 0.38%. As of 7:30 am, US futures are pointing to a flat and mixed open. The SPY is implying -0.01%, the DIA implying -0.13%, and the QQQ a slight drop at -0.33% at this point in the premarket.

The virus, vaccine hope (the PFE-BTNX approval decision is expected any day), and fear over more stimulus delays are fighting for the emotions of the market. There was also another Brexit Trade Deal failure overnight with the year-end deadline fast approaching. Sitting near the all-time highs and having shown some semblance of resistance here, it feels like the market wants to be bullish, but is scared and waiting for another reason to make the next move. So, be careful and remember the market is overbought.

Respect support and resistance, the trend, and price action. Stay true to your trading rules and trust your process. Keep booking those singles and doubles. It’s the profits you take that pay the bills, not bragging rights. So, leave “picking the very top” to the traders more interested in stroking their ego than making money.

Ed

Swing Trade Ideas for your consideration and watchlist: OMI, F, CAT, ZM, NVDA, SLM, EVRI. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The markets once again took their cues from vaccine news and hopefulness for federal stimulus as the SP-500 topped 3700 for the first time in history and the Nasdaq set its 50th record high for the year. Valuations continue to soar as the overall market P/E Ratio stretches 72% above the 10-year average. The U.S. added 1 million new infections in just 4-days, but that is not slowing down the bull run with a parade of big investment banks predicting a bullish 2021 market. Trade with the trend but have a plan should the sentiment suddenly shift because current market prices are long from technical supports.

Asian markets traded mixed but mostly higher overnight, with the Shanghai down more than 1%. European markets are currently bullish across the board this morning, with Brexit talks in focus. U.S. Futures point to another morning of bullishness ahead of the JOLTS report and several earnings reports.

Economic Calendar

Earnings Calendar

On the Hump day earnings calendar, we have another light day but still have several quarterly reports of potential market moving. Notable reports include ADBE, CPB, DBI, HOV, VRA & VRNT.

News and Technicals’

It’s becoming all too common, with the market setting new record highs based on vaccine news and federal stimulus hopes. The SP-500 tops 3700 for the first time in history as the Nasdaq prints its 50th record high for the year. As the markets surge higher, so goes the pandemic infections adding 1 million new cases in just 4-days. Phizer is now warning that people with significant allergic reactions shouldn’t take the vaccine after two of Britain’s National Health Service experienced severe reactions. However, both are not recovering, according to the national medical director. Citi Private Bank added its voice to the chorus of big investment banks predicting market gains in 2021 and went on to say it loves these ‘unstoppable’ trend. Mortgage rates continue to fall, setting the 14th record low of the year today, driving more refinance demand.

Without question, the bulls have shown remarkable resiliency and a willingness to buy almost anything, no matter the price. Trends remain strong as we continue to extend steeply away from technicals supports. Stay with the trend, but once again, I caution you to be very careful not to overtrade or chase already extended stocks. Remember, what goes up in a euphoric market rally tends to have severe correction consequences at some point in time. Be prepared in case the sentiment suddenly shifts.

The NASDAQ sets if 49th record high of the year even as the bears make half-hearted attempts in the SPY and DIA. While there are clues that the economy is slowing due to pandemic shutdowns, the bulls remain resolute, showing a willingness to keep extending. Even with vaccines coming to market, we still have a long winter ahead of us, and in the short-term, markets look very extended. Euphoric markets tend to last longer than most would expect, so stay with the trend, avoid chasing extended stocks, and be careful not to overtrade. Runs like this tend to end in an ugly way.

Asian markets closed modestly lower across the board overnight, and European markets see red with a Brexit deal hanging in the balance. Ahead of earnings, another light economic calendar, and Congress still unable to get their act together, U.S. Futures point to lower open.

Economic Calendar

Earnings Calendar

Although the earnings have been winding down, we still have several stepping up with quarterly reports. Notable reports include CHWY, GME, AZO, CONN, GWRE, HRB, THO., BF.B.

News & Technicals’

Although we had a little selling yesterday, it was very controlled, and by the end of the day, the bulls maintained control of the trends. The NASDAQ fought the selling, rising to its 49th high record for the year. The Pfizer vaccine has begun rolling out, with a 90-year-old woman in the UK receiving the very first dose. The UK is dubbing the event at V-day after suffering considerable losses across the country due to the pandemic. With the federal government facing a funding shutdown on the 11th, the best it seems that Congress can do is attempt to pass a spending bill that will cover a single week of operation as they continue to haggle over the stimulus bill. With management like that, it’s no wonder that the federal debt is quickly approaching 30 trillion.

Bulls remain in control of the trends, and the T2122 indicator continues to flash a short-term overbought condition. There are so many stocks looking parabolic; it’s very reminiscent of the euphoria present in the 1999, 2000 tech bubble. Although the market conditions are very different, the fear of missing chase of very extended stock prices is much the same. A euphoric market can last much longer than one might think, but it is usually swift and very punishing for those coming to the party late when they end. Although I sound like a broken record, I want caution traders to stay with the trend but guard yourself against overtrading and avoid chasing already extended stocks.

On Monday the large-caps gave us a small gap down, followed by an indecisive, Doji type candle day. The DIA was a Doji Bearish Harami. The QQQ gave us a small gap up followed by more bullish follow-through. On the day, The QQQ gained 0.57% to close at yet another all-time high. The SPY lost 0.21% and DIA lost 0.49%. The VXX gained about half a percent to 17.21 and T2122 remains deep in overbought territory at 94.84. 10-year bond yields fell to 0.928% and Oil (WTI) fell a little over a percent to $45.63/barrel. In an interesting sidebar, Fresh Water (H2O) began trading as a commodity Monday.

Monday was a bad day and night for stimulus. Senate Majority Leader McConnell refused to endorse the bipartisan compromise bill and it appears Congress will need to pass a one-week spending extension on Wednesday to keep the federal government open until December 18. This is being done because the two sides of the stimulus negotiation have agreed on the high-level numbers, but they are not agreed on the wording of the specifics of spending. So, in order to roll this into an omnibus funding bill, they need to kick the can down the road another week.

In corporate news, TSLA will offer another secondary stock sale to raise $5 billion. This is the second time it has sold more stock in 3 months and may be an indication it is trying to squeeze every penny out of a very high market price for the stock. Meanwhile, GS has agreed to buy out its Chinese partner (and has applied to Chinese Regulators for the right to have 100% ownership of a securities entity in mainland China). This followed JPM taking 71% ownership in its own Chinese securities joint venture and CS announcing it would like to take 100% ownership of its mainland securities partnership.

Related to the virus itself, US infections continue to rage as the US. The totals have risen to 15,370,339 confirmed cases and 290,474 deaths. Monday saw another record 200,000+ new cases and 1,539 new deaths. This brings the 7-day average of new cases is at 206,259 while average deaths rose to 2,300/day. This comes as Dr. Fauci (NIH) told CBS reporters that the “full brunt of Thanksgiving gatherings on the Covid surge” has not hit yet…but it’s coming soon. This came as Fauci and several other health experts were urging the public to cancel or dramatically change holiday gathering plans.

Globally, the numbers rose to 68,055,468 confirmed cases and the confirmed deaths are now at 1,553,155 deaths. The big global news was that the UK has begun giving vaccinations using the PFE-BTNX vaccine. Due to the extreme cold needed and logistics, at least at first, they are focusing on hospital workers and priority patients (like the elderly) who are already located at a major hospital for appointments. However, across the channel, Germany reached a new record high infection rate. In Asia, Hong Kong increased restrictions on social distancing yet again while South Korea and Japan have called out their militaries to assist in medical staffing and contact tracing.

Overnight, Asian markets were mixed yet again. Thailand (+2.01%) was an outlier as the gains were generally modest. The same is true of South Korea (-1.62%) being abnormal while most losses were quite modest. In Europe, markets are leaning more heavily to the downside so far today. Only two minor markets are modestly green, but the 3 major bourses are typical with the FTSE down 0.48%, the DAX down 0.41%, and the CAC down 0.82%. As of 7:30 am, US futures are pointing to a modest gap down. The SPY (-0.56%), DIA (-0.47%), and QQQ (-0.39%) are all implying lower opens at this point in the premarket.

The major economic news is very limited for Tuesday. This includes Q3 Nonfarm Productivity and Q3 Unit Labor Costs (both at 8:30 am). The major earnings releases are also limited and include AZO, GIII, and THO before the open. Then after the close, CHWY and GME report.

Asia and Europe seem to be leading us lower on Tuesday, perhaps on at least a delay in any US stimulus or on the bad virus news from around the world. With limited economic news or earnings to change that lead, it looks like we may have a lower open. However, remember that hope springs eternal among bulls up near the all-time highs. The point being, it does not pay to fight the trend until it is broken. Just be careful.

Respect support and resistance, the trend, and price action. Remain true to your trading rules and trust your process. Keep booking those singles and doubles. It’s the profits you take that pay the bills. So leave “picking the very top” to the traders more interested in stroking their ego than making money.

Ed

Swing Trade Ideas for your consideration and watchlist: NAT, PINS, AAPL, XLC, COOP, AG, SOLO, BLNK, EGO. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

A slowing job growth proved to be no concern for the market on Friday, pushing all four indexes into new record territory. The rapidly rising pandemic infection rate, the death toll is, however, forcing states to increase restrictions as hospitalizations strain the capacity limits of the health care system. That said, no price seems too high as investors rush into stocks focused on stimulus hopes, vaccine news that points to 2021 recovery. However, at this elevation, if the market stumbles, the resulting pullback could be very painful if the market does suddenly decides we have pushed too high too quickly in anticipation.

Asian markets closed in red across the board overnight. European markets trade mixed as they push forward with last-ditch Brexit efforts. U.S. futures trade lower this morning but are will off the overnight lows as the morning lows as institutions try to keep investors buying, predicting a 2021 spring economic restart.

Economic Calendar

Earnings Calendar

We have several notable companies fessing up to quarterly results on the Monday earnings calendar. Notable reports include CASY, HQY, JKS, SFIX, SUMO & TOL.

News & Technicals’

Even with a sizable miss on the jobs front, the market continued to surge higher, setting new record highs on all four indexes. Futures markets are currently looking a bit lower this morning but have already bounced off the morning lows with the morning pump-up underway. As investors work the price, the market for a hopeful spring recovery of the pandemic rising oil prices becomes noticed at the gas pumps, with the national average price rising $0.04 a gallon. Simultaneously, the White House health advisor says this winter will be the worst event that this country has faced. California has issued a statewide stay at home order, and states around the country continue to ramp up restrictions measure to combat the spread.

Trends remain very bullish, and there seems to be a non-stop barrage from institution headlines predicting a massive restart to the economy in 2021. I certainly hope they are correct, but that has created a potentially dangerous short-term overbought condition. The T2122 indicator continues to warn that a pullback could begin at any time; however, stimulus hopes, vaccine news, record holiday salse, and 2021 predictions have investors willing to ignore the current pandemic economic impacts. How long this can continue is anyone’s guess but be careful not to overtrade because one day, the market may suddenly decide to care about the impacts, and the technical supports are a long way from current prices.

On Friday, all 3 major indices had a slight gap up and then the bulls followed through early. After about 10 am, the rest of the day was a sideways grind. On the day, the large-caps led as the SPY was up 0.86%, DIA up 0.84%, and the QQQ up 0.41%. All 3 of the indices then closed at all-time high closes. The VXX fell almost 2% to 17.11 and the T2122 remains deep in overbought territory at 96.91. The 10-year bond yields spiked (as money flowed out of bonds) to 0.973% and Oil (WTI) was up at $46.09/barrel.

Over the weekend, leaks from both sides indicated that a stimulus deal could be agreed in the next day or two at an agreed price tag of $908 billion. GOP Senators have said that Senate Majority Leader McConnell and President Trump will support the legislation. One of the agreed provisions seems to be a second $1,200 stimulus check, which retailers (particularly online retailers) will find very appealing, assuming it is not too late to get the checks out by year-end.

Chick-fil-A restaurant chain filed suit against all the major poultry suppliers (TSN, PPC, SAFM, JBSS), alleging price-fixing. In other corporate news, Airbnb raised the price range for their IPO due out on Thursday from $44-$50 to $56-$60 per share. KODK stock also shot as much as 70% higher in pre-market trading as a federal agency found that they had found no evidence of conflicts of interest from the unusual trading around the July announcement of the company’s pivot and announced government contract to supply ingredients for a potential Covid treatment.

Related to the virus itself, US infections continue to rage across the US. The totals have risen to 15,159,529 confirmed cases and 288,906 deaths. Friday saw another record 237, 372 new cases and 2,742 deaths. The 7-day average of new cases is at 200,012 while deaths are averaging 2,258/day. The country hit another record number of Covid hospitalizations Sunday as we have seen over 1 million new cases in the first 5 days of the month alone. In CA, more regions of the state were put under a “stay at home” order, including the San Francisco, Los Angeles, and San Diego regions. All in all, 33 million of the state’s residents are under the order as cases, ICU capacity, and deaths are at extreme levels. That said, we should also note that the FDA is expected to approve the emergency use of the PFE-BTNX vaccine on Thursday with first vaccinations likely to happen within a day after the approval. A vote on the approval of the MRNA vaccine is expected a week later. Distribution of both will still be challenging as many states only have a handful of hospitals in their entire state with the ultra-cold freezers needed to store and distribute these two vaccines.

Globally, the numbers rose to 67,493,569 confirmed cases and the confirmed deaths are now at 1,543,627 deaths. In Europe, Denmark has announced a partial lockdown after many cities report record new cases. The UK is set to begin administering the first batch of PFE-BTNX vaccine on Tuesday. In Asia, Japan saw another record number of new cases Sunday and South Korea is implementing new restrictions to stay ahead of the spread. In Indonesia, 1.2 million doses of a Chinese Covid-19 vaccine have arrived with another 1.8 million doses scheduled to arrive by early January.

Overnight, Asian markets were mixed. Hong Kong (-1.23%) and Shanghai (-0.81%) led the losses while Indonesia (+2.07%) and Taiwan (+0.88%) led the gainers. In Europe, we see a similar pattern so far in their day. Belgium (-0.87%) and the CAC (-0.74%) are leading the downside push while Denmark (+0.59%) and the FTSE (+0.38%) lead the gainers. As of 7:30 am, US futures are pointing to a lower open. The SPY (-0.37%), DIA (-0.41%), are implying a small gap down while the QQQ (-0.10%) indicates an open on the red side of flat.

There is no major economic news for Monday. Major earnings releases include JKS before the open and CASY and TOL after the close.

A lack of major econmic news is likely to be overwhelmed by optimism as the UK begins vaccinations with the US a few days behind. That plus the hope for economic stimulus may be enough to let the bulls run. Keep in mind that we are at all-time highs, in an overbought market, and the gains seem tentative. So, just be careful.

As always, don’t predict reversals (the trend is your friend until it is broken), but also don’t chase moves you missed. Respect support and resistance, the trend, and price action. Remain disciplined to your trading rules. Keep booking those singles and doubles. It’s the profits you take that pay the bills, not bragging rights of picking the very top.

Ed

Swing Trade Ideas for your consideration and watchlist: BERY, FUL, KNSL, KURA, RS, FOLD, STNG, ALB, ADP, CCK, ADT, CRBP, XLB, ARNC. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Ahead of the Employment Situation report, U.S. futures see nothing but bullishness, pushing for more record highs at the open. Let’s keep our fingers crossed that the pandemic, which is shutting down business all over the country, has not yet trickled into employment. The NASDAQ set its 47th new high record for the year in yesterday’s bull run even as hospitalizations reach critical capacity issues and the death toll surges. Have a plan just in case the market suddenly decides to care because it’s a long way to the daily 50-moving average.

Asian markets closed Friday trading mixed as SMIC shares plunge in Hong Kong after the Pentagon blacklisting. European market trade cautiously higher focused on U.S. stimulus efforts and Brexit issues. With a light day on the earnings calendar, the U.S. futures point to more recording highs ahead of the government’s reading on employment.

Economic Calendar

Economic Calendar

We have a light day on the Friday earnings calendar. Notable reports include BIG & GCO.

News and Technicals’

Bulls remain large and in charge, with the Nasdaq making it 47th new record high this year. News that suggested distribution issues with the new Phizer vaccine created a wild whipsaw near the end of the day. That said, the current market shakes off any concerning news, and the bulls rush back, bidding up already stretched and high priced stocks. Biden is endorsing the latest Covid stimulus deal saying it’s a good start, which would suggest even more deficit spending is on the way in his administration. A lot is riding on the 900 billion stimulus package success as Congress rushes to avoid a government shutdown on December 11th. In a surprising move, Warner Media announced that all scheduled 2021 new movies would simultaneously release to movie theaters and the HboMax.com streaming service. A massive blow to the theater business and a reminder of how the pandemic is reshaping the business landscape. Not that market cares, but there were more than 210,000 new infections reported yesterday and nearly 3000 deaths as hospitalizations soar, straining healthcare capacity. Also, in the news, the Pentagon blacklists China chipmaker SMIC and oil producer CNOOC in a reaction to a long history of Chinese espionage complaints.

Trends are most certainly bullish, and although all my trades are long positions, I’m becoming more and more concerned about the overextension I see so many stocks. Trade with the trend but guard yourself against overtrading and chasing already extend stocks. As yesterday’s vaccine news triggered the end of the day, whipsaw reminds us just how sensitive this market is and how quickly significant profits can disappear.

On Thursday, all 3 major indices put in indecisive Doji-like candles at the all-time highs, but failing to great out of resistance. Even the lower than expected Initial Jobless Claims number did not help. On the day the SPY was on the red side of flat (-0.03%), the QQQ on the green side of flat (+0.14%), and the DIA was mildly positive (+0.28%). The VXX rose just under one percent to 17.41 and T2122 rose again to 91.16, deep in overbought territory. 10-year bond yields fell to 0.911% and Oil (WTI) rose a bit to $45.65/barrel.

The DOJ sued FB Thursday, claiming the company has been discriminating against American workers by reserving 2,600 high-wage jobs for only foreign temporary visa holders. PFE stock was also fell when a report came out the company only expects to ship only half (50 mil. doses vs. 100 mil.) of the Covid-19 vaccine that was originally planned and promised by year end. The cause was said to be “supply chain problems” (raw materials that were not below standard). After hours, the Pentagon blacklisted 4 Chinese firms, including SMIC and CNOOC (adding them to the same list a Hauwei).

On the stimulus front, House Speaker Pelosi and Senate Majority Leader McConnell met to further discuss stimulus Thursday. McConnell said afterward that there were hopeful signs of reaching a deal before year-end. While McConnell still claims to back only half the amount the Democrats and a bipartisan Senate group propose, the main sticking point seems to be McConnell’s insistence the bill include blanket Covid-related liability waivers for businesses

Related to the virus itself, US infections continue to rage as the US. The totals have risen to 14,532,196 confirmed cases and 282,829 deaths. Thursday saw another record 218, 576 new cases and 2,918 deaths. That said, the 7-day average of new cases is at 176,145 while deaths are averaging deaths rise to 1,876/day. CA expanded on the Los Angeles lockdown, implementing regional “Stay at home” orders in areas of the state where the remaining ICU bed capacity has fallen below 15% of normal.

Globally, the numbers rose to 65,664,051 confirmed cases and the confirmed deaths are now at 1,514,619 deaths. In Asia, Hong Kong reports it is undergoing a “fourth wave” and Seoul South Korea is increasing restrictions in the city to fight what the Mayor reports is a “desperate crisis” as the country reported the highest increase in cases since March. Elsewhere, Tokyo reports that COVID-19 has raised the budget for the Olympics from $2.7 billion to $15.3 billion.

Overnight, Asian markets were mixed. South Korea (+1.31%) and Taiwan (+1.11%) led the gainers. Losses were more modest and Japan (-0.22%) and Malaysia (-0.39%) are typical of the losses. In Europe, markets are almost green across the board. Only the DAX (-0.16%) has failed to “get with the bull program” so far today. The FTSE (+0.82%) and CAC (+0.36%) are typical with no exchange moving one percent yet. As of 7:30 am, US futures are pointing to modestly higher open. The DIA is implying a gain of 0.48%, The SPY a 0.38% higher open, and the QQQ a 0.33% open up. However, remember we have a lot of data between now and the open.

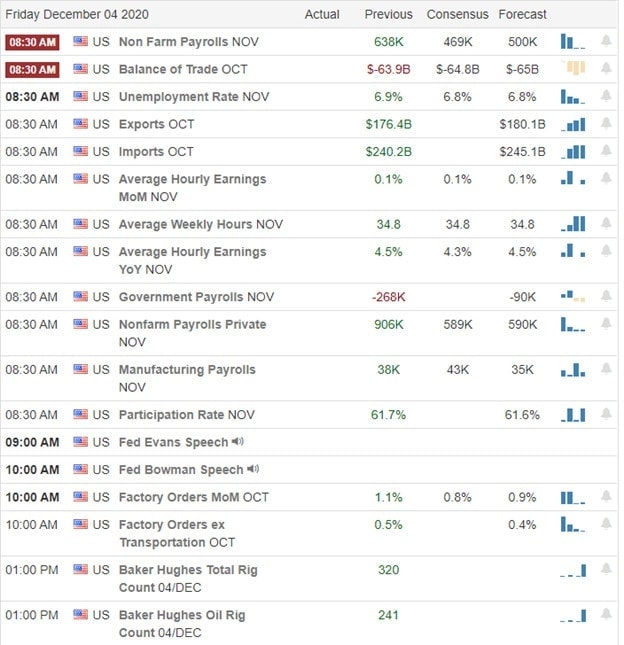

The major economic news for Friday includes Imports/Exports, Nov. Avg. Hourly Earnings, Nov. Nonfarm Payroll, Nov. Participation Rate, Oct. Trade Balance, Nov. Unemployment Rate, and Q-on-Q Unit Labor Costs (all at 8:30 am), and Oct. Factory Orders (10 am). There is also a Fed Speaker (Bowman at 10 am). Major earnings are limited to BIG before the open. There are no major reports after the close.

A big economic news day and hope related to stimulus talks are likely to call the tune at least early on in the day. At this point, we seem to be following Europe with an implied move to the upside. Regardless, keep in mind that we are at all-time highs, in an overbought market, and this is Friday. So, even if you don’t want to avoid weekend news cycle risk, there is a possibility that others will by day end. Just be careful.

As always, don’t predict reversals (the trend is your friend until it is broken), but also don’t chase moves you missed. Respect support and resistance, the trend, and price action. Remain disciplined to your trading rules. Keep booking those singles and doubles. It’s the profits you take that pay the bills, not bragging rights of picking the very top.

Ed

Swing Trade Ideas for your consideration and watchlist: SBUX, LPX, T, UAA, PINS, CMCSA, TUP, KO. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service